Utility Terrain Vehicles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 6.66 Billion |

| Market Size (2030) | USD 8.56 Billion |

| Growth Rate (2025 - 2030) | 5.16% CAGR |

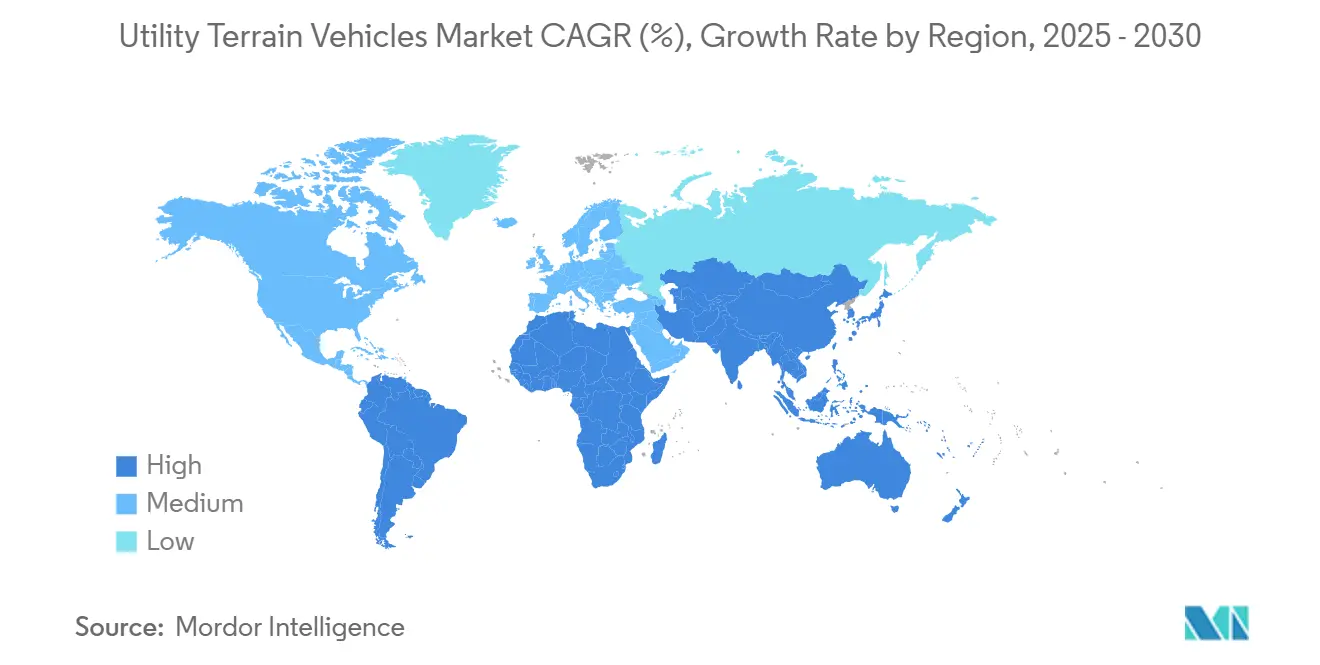

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

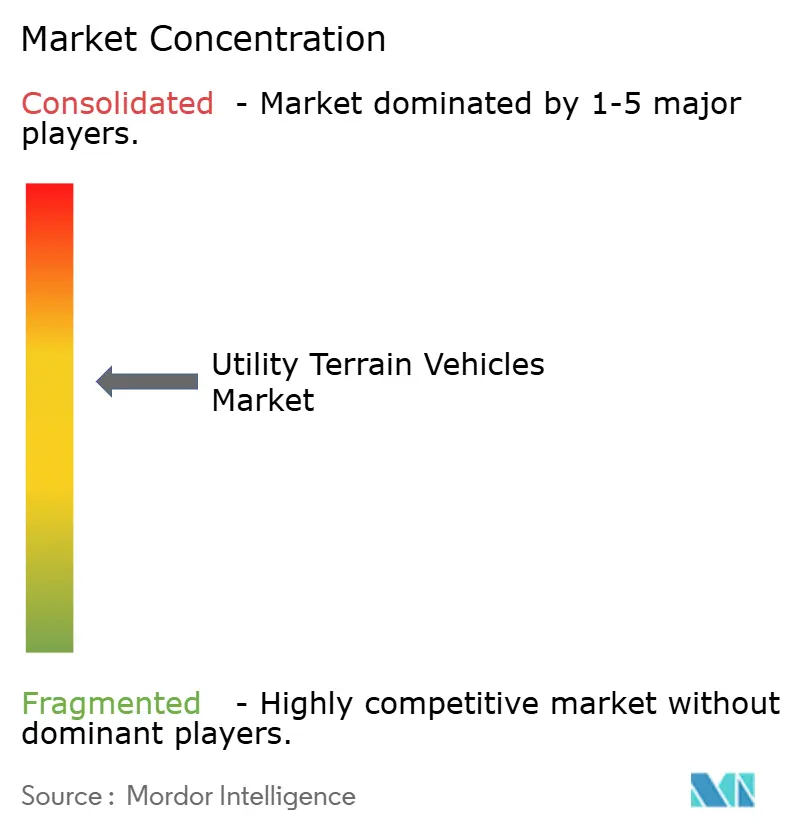

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Utility Terrain Vehicles Market Analysis by Mordor Intelligence

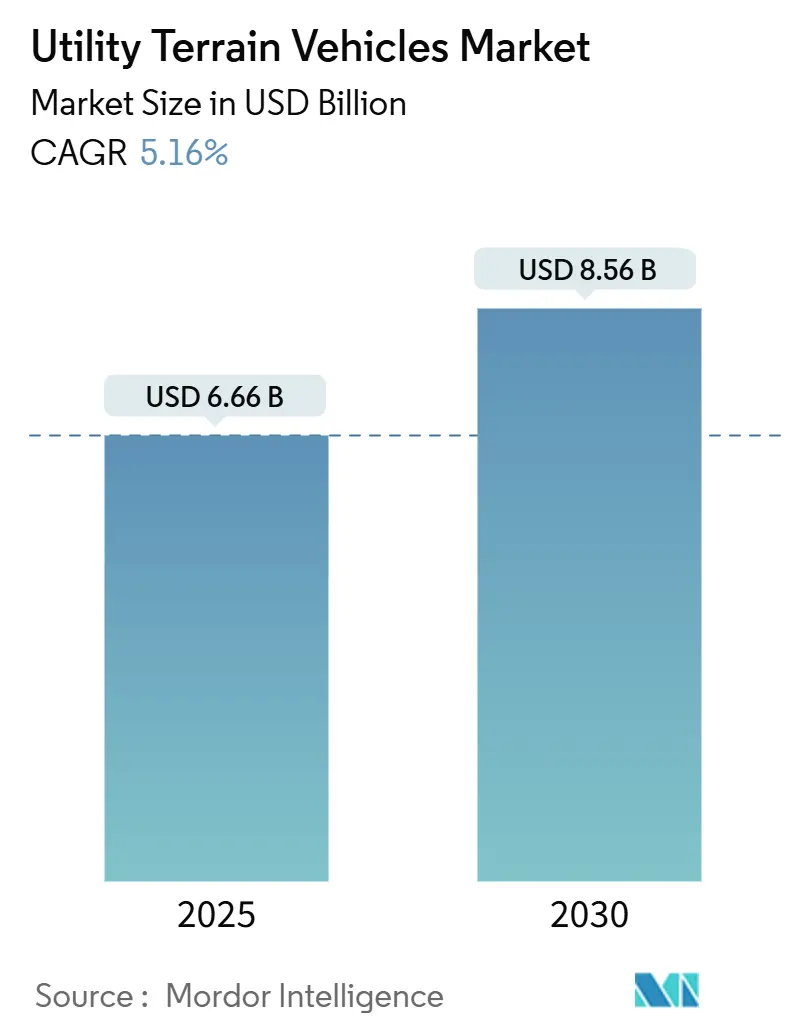

The Utility Terrain Vehicles Market size is estimated at USD 6.66 billion in 2025, and is expected to reach USD 8.56 billion by 2030, at a CAGR of 5.16% during the forecast period (2025-2030). Heightened demand from military modernization programs, agricultural mechanization, and mainstream off-road recreation positions the utility terrain vehicles market for durable mid-single-digit growth. Defense agencies favor compact, air-deployable UTV platforms that trim logistical burdens, while farmers adopt the vehicles as lower-cost, precision-ready substitutes for complete tractors. On the recreational side, multi-passenger models broaden the addressable base beyond traditional powersports enthusiasts, aided by OEM financing and turnkey race packages. Supply chain resilience and raw-material control, particularly for lithium, now influence competitive advantage as electrified variants accelerate. As a result, the utility terrain vehicles market is becoming a focal point for new-energy specialists, autonomous-mobility start-ups, and vertically integrated incumbents seeking margin defense through technology differentiation.

Key Report Takeaways

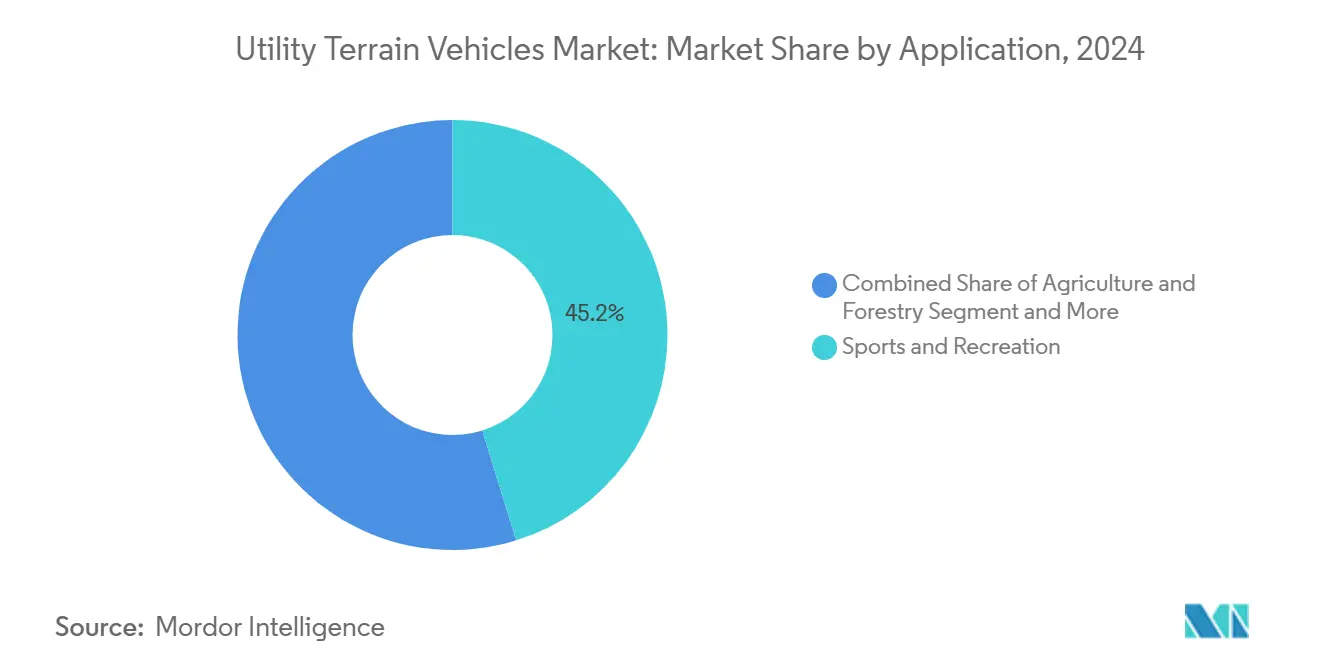

- By application, sports and recreation led the utility terrain vehicles market with 45.17% of the share in 2024; the military and law-enforcement segment is forecast to expand at a 5.17% CAGR through 2030.

- By propulsion type, internal-combustion engines captured an 85.16% share of the utility terrain vehicles market in 2024, while battery-electric variants are projected to post the fastest growth at a 5.22% CAGR to 2030.

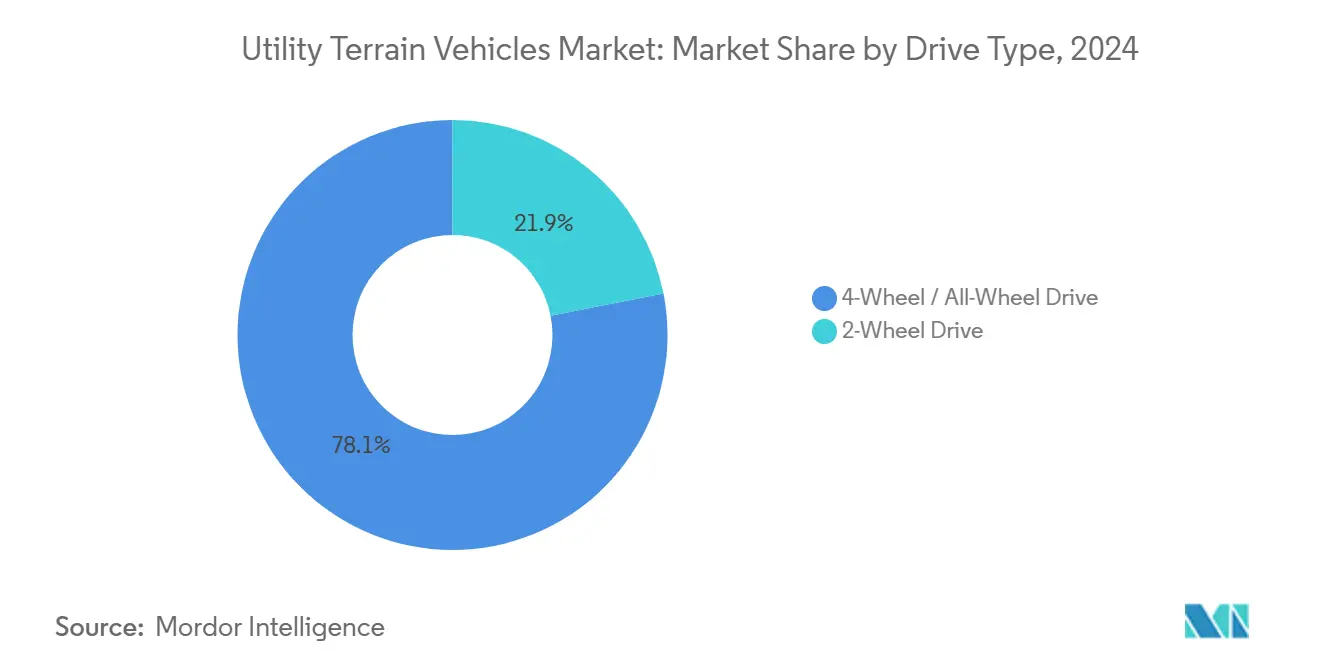

- By drive configuration, the 4-wheel/all-wheel drive segment held 78.14% of the utility terrain vehicles market size in 2024, supported by a sustained 5.19% CAGR outlook.

- By seating capacity, 3-4 seater models commanded 53.26% of the utility terrain vehicles market share in 2024, and more-than-4-seater vehicles are tracking a 5.27% CAGR between 2025 and 2030.

- By region, North America accounted for 38.73% of the utility terrain vehicles market share in 2024, whereas Asia-Pacific records the highest projected CAGR at 5.21% through 2030.

Global Utility Terrain Vehicles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand For Off-Road Recreation | +1.2% | North America and Europe, spill-over to Asia Pacific | Medium term (2-4 years) |

| Rapid Adoption In Agriculture And Forestry | +0.9% | Global, with early gains in North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Growing Use On Industrial And Construction Sites | +0.8% | Global, concentrated in Asia Pacific and North America | Medium term (2-4 years) |

| Military Modernization Programs | +0.7% | North America, Europe, Asia-Pacific core | Long term (≥ 4 years) |

| Incentives For Zero-Emission Vehicles | +0.4% | North America and EU primarily | Short term (≤ 2 years) |

| Telematics-Enabled Autonomous UTV Fleets | +0.3% | North America, Europe, selective Asia Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Off-Road Recreation

Recreational uptake of utility vehicles is expanding beyond traditional motorsports into mainstream family-oriented outdoor pursuits. Demographic shifts toward experiential spending have elevated multi-passenger UTVs as an alternative to separate cars for each rider. OEMs now bundle showroom-ready race kits that let buyers enter sanctioned events without aftermarket modification, shortening adoption cycles. National off-road associations confirm double-digit increases in UTV race entries since 2023, with vehicles often eclipsing motorcycle lap times on desert courses. Youth-specific models, safety harnesses, and graduated power maps foster early driver participation, extending lifetime customer value.

Rapid Adoption in Agriculture & Forestry

Farmers increasingly view UTVs as affordable, versatile companions to tractors. Kubota’s Thai engine plant expansion is projected to grow exponentially by 2026, underscoring mounting demand for compact powertrains that propel agricultural UTVs. Integrated GPS guidance, sprayer modules, and variable-rate input systems transform the vehicles into precision-ag platforms that reduce chemical drift and fuel consumption. Forestry crews rely on narrow-profile UTVs to haul gear deep into stands without disturbing sensitive soil. The vehicles’ lighter weight also minimizes carbon emissions relative to skid-steers, aligning with global food-security and sustainability programs backed by the FAO.

Incentives for Zero-Emission Vehicles in Protected Parks

National park authorities in the United States and France now restrict internal-combustion off-road vehicles during the high season, accelerating fleet conversion to battery-electric UTVs. The U.S. National Park Service offers up to USD 7,500 per electric UTV under its Alternative Fuel Vehicle grant, tapering by 2027[1]“Alternative Fuel Vehicle Grants,” U.S. National Park Service, nps.gov. Similar subsidy structures across Europe aim to cut particulate emissions on sensitive trails and reduce noise disturbance for wildlife.

Telematics-Enabled Autonomous “Follow-Me” Fleets

Industrial operators deploy convoy-style UTV fleets in which one human-driven lead vehicle guides autonomous “follow-me” units loaded with tools or materials. John Deere demonstrated such functionality at CES 2025, integrating lidar and real-time kinematic positioning for sub-inch tracking accuracy[2]“Autonomous Tractor and Off-Road Technology at CES 2025,” Deere & Company, deere.com . Mining firms in Western Australia and Quebec pilot the systems to reduce human exposure to hazardous zones and to extend 24/7 operations without driver fatigue.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront And Maintenance Cost | -0.8% | Global, particularly price-sensitive markets | Medium term (2-4 years) |

| Safety Incidents Tightening | -0.5% | North America and Europe primarily | Short term (≤ 2 years) |

| Lithium Supply Constraints | -0.4% | Global, concentrated impact on electric variants | Medium term (2-4 years) |

| Competition From Compact Track Loaders | -0.3% | Industrial applications globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront & Maintenance Cost vs ATVs

Entry-level UTVs such as Kawasaki’s Mule SX retail highly, materially higher than comparable ATVs priced reasonably. Multi-passenger frames, rollover protection, and more complex drivetrains raise initial outlays and maintenance labor. Insurance premiums track the higher vehicle value, dissuading budget-conscious buyers in emerging economies. Smallholder farmers thus often default to ATVs, slowing conversion in price-sensitive pockets of the utility terrain vehicles market.

Safety Incidents Tightening Trail-Access Rules

Rollover accidents prompted U.S. states such as Utah and Colorado to demand operator certificates and impose width restrictions on specific trails. European land managers follow suit, mandating speed governors and event data recorders. These rules add compliance costs for OEMs and owners, tempering growth in the most significant recreational segment of the utility terrain vehicles market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Military Segment Drives Premium Growth

The sports and recreation segment still anchors the utility terrain vehicles market, accounting for 45.17% revenue in 2024. OEMs pivot toward family-oriented four-seater trims and subscription-based servicing packages to defend share. Agriculture & forestry represent an emerging middle tier as mechanization grants farmers capital flexibility, generating cross-cycle revenue. Industrial & construction applications adopt sealed lithium packs to comply with zero-tailpipe mandates on enclosed jobsites. Niche uses in tourism and search-and-rescue add incremental demand but remain sub-scale. The military and law-enforcement segment is on track for a 5.17% CAGR, outpacing the overall trend yet starting from a smaller base. Active procurement agendas among NATO members and Indo-Pacific allies underpin steady volume, while defense-grade customization elevates ASPs.

Continued battlefield digitalization steers military agencies toward UTVs fitted with ISR pods, remote-weapon stations, and hybrid silent-watch modes. Dual-use spillovers elevate civilian safety tech such as 360° night-vision, amplifying value perception in the utility terrain vehicles market. Agricultural buyers increasingly specify precision ag bundles with ISOBUS compatibility, syncing UTV telemetry with farm-management systems. Construction firms, meanwhile, weigh telematics-based rental models to minimize idle-time cost.

By Propulsion Type: Electric Variants Challenge ICE Dominance

Internal-combustion engines led utility terrain vehicles market with 85.16% share in 2024, yet battery-electric models posted the fastest 5.22% CAGR thanks to park incentives and corporate ESG targets. Expect hybrid variants to bridge use-case gaps where range anxiety lingers, especially in patrol routes over 160 kilometers. If lithium supply stabilizes, the utility terrain vehicles market size for electrified models could grow exponentially by 2030. Hydrogen fuel-cell pilots by the HySE consortium indicate future long-range options for desert or alpine missions where charging stations are scarce. China’s role in lithium refining and cathode fabrication creates both opportunity and concentration risk; Western OEMs hedge with localized pack assembly and recycled-content anodes.

Battery costs remain the prime hurdle. Even with nickel-manganese-cobalt chemistry trending below USD 80/kWh by 2028, electric UTVs still list one-fourth higher than ICE peers on equivalent spec. Yet fleet TCO often swings in their favor within three years once gasoline at-pump prices exceed USD 1.10/liter. Expect software-locked power maps and over-the-air updates to add subscription revenue streams unique to battery platforms.

By Drive Type: All-Wheel Drive Maintains Technical Advantage

Four-wheel/all-wheel drive dominated the utility terrain vehicles market with 78.14% revenue in 2024, reflecting users' willingness to pay for traction assurance. The segment’s 5.19% CAGR aligns with escalating terrain diversity from Canadian winter forestry to Indo-Malaysian palm-oil estates. Electronic differential locks and torque vectoring now migrate from high-end pickups to mainstream UTV trims, narrowing performance gaps across price tiers.

Two-wheel drive persists in flat-terrain farms and gated community security fleets, but its share erodes as AWD cost economies improve. Advanced hub-drive systems under test promise modular redundancy, enabling limping-home capability even after axle failure, key for military and remote mining operations.

By Seating Capacity: Multi-Passenger Configurations Gain Traction

Three-to-four-seater models balanced agility with capacity to hold 53.26% of the utility terrain vehicle market share in 2024, and their popularity endures across rental fleets and family recreation. Over-four-seater variants will post the briskest 5.27% CAGR, buoyed by work-crew shuttles at industrial plants and tourism safari operators. Less-than-two-seater configurations remain vital for solo ranchers and fire-break scouts but face substitution from lightweight electric quad-cycles.

Modular row-delete kits and fold-flat benches let owners convert between passenger and cargo duty, safeguarding resale values. Safety regulators, especially in Europe, have begun mandating energy-absorbing ROPS for vehicles above 25 kilowatts gross power, nudging design toward robust tubular frames.

Geography Analysis

North America held 38.73% of the utility terrain vehicles market share in 2024 due to entrenched dealer ecosystems and broad-based applications in recreation, agriculture, and defense procurement. The utility terrain vehicles market in the region benefits from F&I financing penetration surpassing three-fifths, which softens elevated ASPs. U.S. military development programs—such as the Marine Corps ULTV—inject advanced materials, situational-awareness suites, and hybrid drivetrains into the commercial pipeline. Although some states tightened public-trail rules after accident spikes, private-land adventure parks are growing, preserving recreational momentum.

Asia-Pacific delivers the fastest 5.21% CAGR as rapid industrialization in China and India catalyzes demand for low-cost logistics and field mobility. Chinese manufacturers run more than 295 verified export-grade lines, pushing ex-factory UTV pricing as low as USD 1,500 for basic carbureted two-seat models. Concurrently, premium domestic brands invest in LFP battery packs for the electric utility terrain vehicles market, aiming at park fleets that must meet zero-tailpipe mandates. India targets a 36% CAGR in its EV battery manufacturing chain between 2021 and 2026, laying the groundwork for local electric UTV assembly[3]“India Battery Supply Chain Report,” NITI Aayog, niti.gov.in. Japan and South Korea contribute automated-driving stacks and hydrogen fuel-cell know-how, elevating the innovation profile of regional exports.

Europe foregrounds environmental stewardship, driving preference for battery-electric and low-noise drivetrains. Germany’s Federal Office for Economic Affairs subsidies cover up to two-fifths of incremental capex for electric off-road machinery. Nonetheless, the European Commission flags lithium-supply vulnerability as an impediment to scale[4]“Lithium Supply Chain Vulnerability Study,” European Commission, europa.eu. OEMs counter by signing offtake agreements with Portuguese and Canadian hard-rock miners. South America’s market remains tied to agri-mechanization cycles and mining exploration budgets, with Brazil registering the bulk of the continent’s demand. Meanwhile, Middle East and African uptake is tethered to infrastructure builds and safari tourism; volume remains lower, but ASPs skew premium due to import tariffs.

Competitive Landscape

Established OEMs Polaris and BRP, with Kawasaki, Yamaha, and Honda controlling nearly one-third of global revenue in 2024, gave the field a moderate concentration profile. Chinese assemblers such as CFMoto and Linhai compress price bands, compelling incumbents to lean on brand equity, parts networks, and finance alliances. The utility terrain vehicles market now witnesses tech-led disruptors like Volcon and Nikola Recreational courting ESG-oriented buyers with full-electric, over-the-air-upgradable models. A supply-chain strategy is emerging as a separation line: Polaris inked a multi-year lithium hydroxide pact with Livent to lock cost baselines. At the same time, BRP invests in in-house cell-to-pack assembly in Mexico.

Product innovation pivots on autonomy and active suspension. Fox Factory’s Upfit UTV division pairs Live Valve electronic damping with cloud-configurable ride maps, carving a premium after-sales niche. GM Defense prototypes integrate 4G-mesh radios and AI-based terrain classification to allow semiautonomous patrols. Hydrogen remains exploratory but garners OEM collaboration via the HySE consortium, which prototypes polymer-electrolyte stacks optimized for vibration loads standard to off-road duty. EPA and DOT certification rules pose entry barriers, yet start-ups circumvent them through contract manufacturing under existing Type-2 exemptions.

Dealer consolidation reshapes go-to-market footprints: U.S. retail chains Freedom Powersports and RideNow merged over 55 stores, extracting purchasing leverage and standardized service plans. Digital direct-to-consumer pilots surface, but models still depend on brick-and-mortar for PDI and warranty work. Accessory ecosystems flourish: SuperATV’s 2024 acquisition of HCR Racing adds billet suspension to its aftermarket stack, capturing higher wallet share per unit sold.

Utility Terrain Vehicles Industry Leaders

Polaris Inc.

BRP Inc. (Can-Am)

Honda Motor Co.

Yamaha Motor Co.

Kawasaki Heavy Industries

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hyundai Motor Company and TVS Motor Company partnered to develop electric three-wheelers and micro four-wheelers for India’s last-mile segment. Hyundai supplies design engineering while TVS handles manufacturing and distribution.

- October 2024: SuperATV acquired HCR Racing, expanding its vertically integrated catalog of performance suspension kits and reinforcing aftermarket leadership.

- September 2024: Volcon ePowersports launched the HF1 electric UTV for recreational and utility use, featuring 160 horsepower peak output and 100-mile city range.

Global Utility Terrain Vehicles Market Report Scope

| Sports & Recreation |

| Agriculture & Forestry |

| Industrial & Construction |

| Military & Law-Enforcement |

| Other Commercial (Tourism, Search-and-Rescue) |

| Internal-Combustion (Gasoline / Diesel) |

| Hybrid |

| Battery-Electric |

| Hydrogen Fuel-Cell |

| 2-Wheel Drive |

| 4-Wheel / All-Wheel Drive |

| Less than 2 Seater |

| 3-4 Seater |

| More than 4 Seater |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Sports & Recreation | |

| Agriculture & Forestry | ||

| Industrial & Construction | ||

| Military & Law-Enforcement | ||

| Other Commercial (Tourism, Search-and-Rescue) | ||

| By Propulsion Type | Internal-Combustion (Gasoline / Diesel) | |

| Hybrid | ||

| Battery-Electric | ||

| Hydrogen Fuel-Cell | ||

| By Drive Type | 2-Wheel Drive | |

| 4-Wheel / All-Wheel Drive | ||

| By Seating Capacity | Less than 2 Seater | |

| 3-4 Seater | ||

| More than 4 Seater | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected CAGR for the utility terrain vehicles market from 2025 to 2030?

The utility terrain vehicles market is expected to register a 5.16% CAGR during the forecast period.

Which region will grow the fastest in utility terrain vehicles between 2025 and 2030?

Asia-Pacific leads with a projected 5.21% CAGR, propelled by industrialization in China and India.

How much market share did sports and recreation UTVs capture in 2024?

The sports and recreation UTVs accounted for 45.17% of worldwide revenue.

Which propulsion technology is expanding the quickest in the UTV space?

Battery-electric variants are pacing the field with a 5.22% CAGR outlook to 2030.

Who are the leading companies in the UTV competitive landscape?

Polaris, BRP, Kawasaki, Yamaha, and Honda are the leading companies in the UTV market.

What factor most restrains electric UTV scale-up?

Concentrated lithium supply, with China processing roughly four-fifths of global output, poses the primary bottleneck.

Page last updated on: