Used Bikes Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

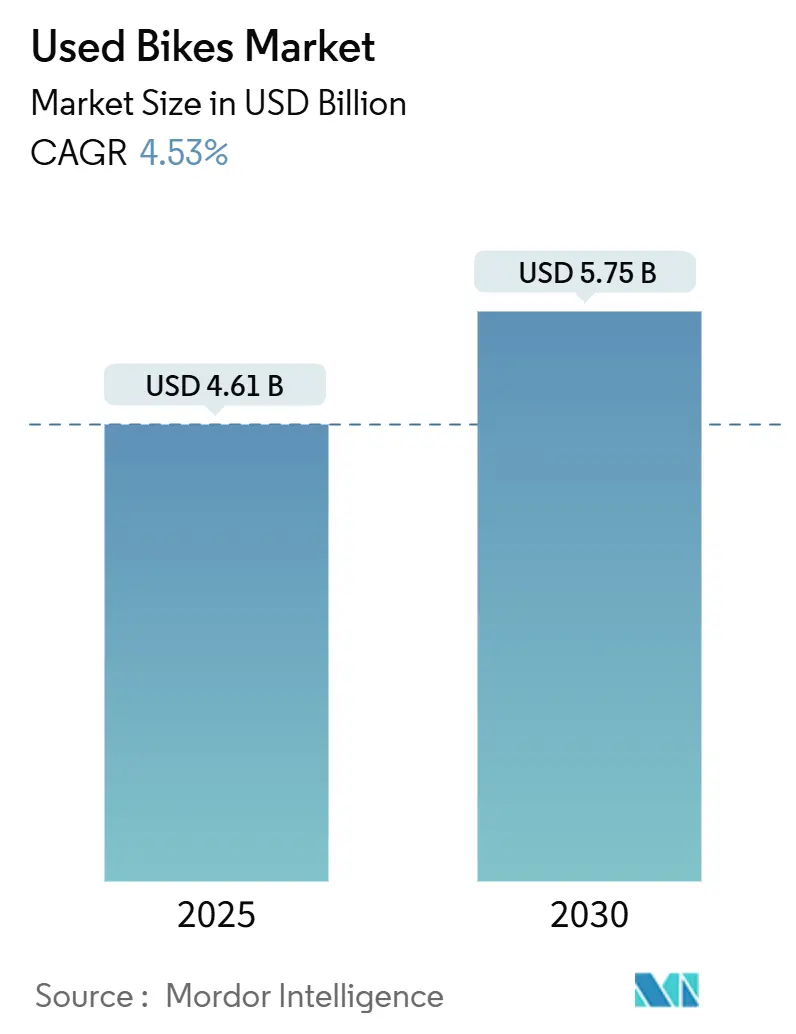

| Market Size (2025) | USD 4.61 Billion |

| Market Size (2030) | USD 5.75 Billion |

| Growth Rate (2025 - 2030) | 4.53% CAGR |

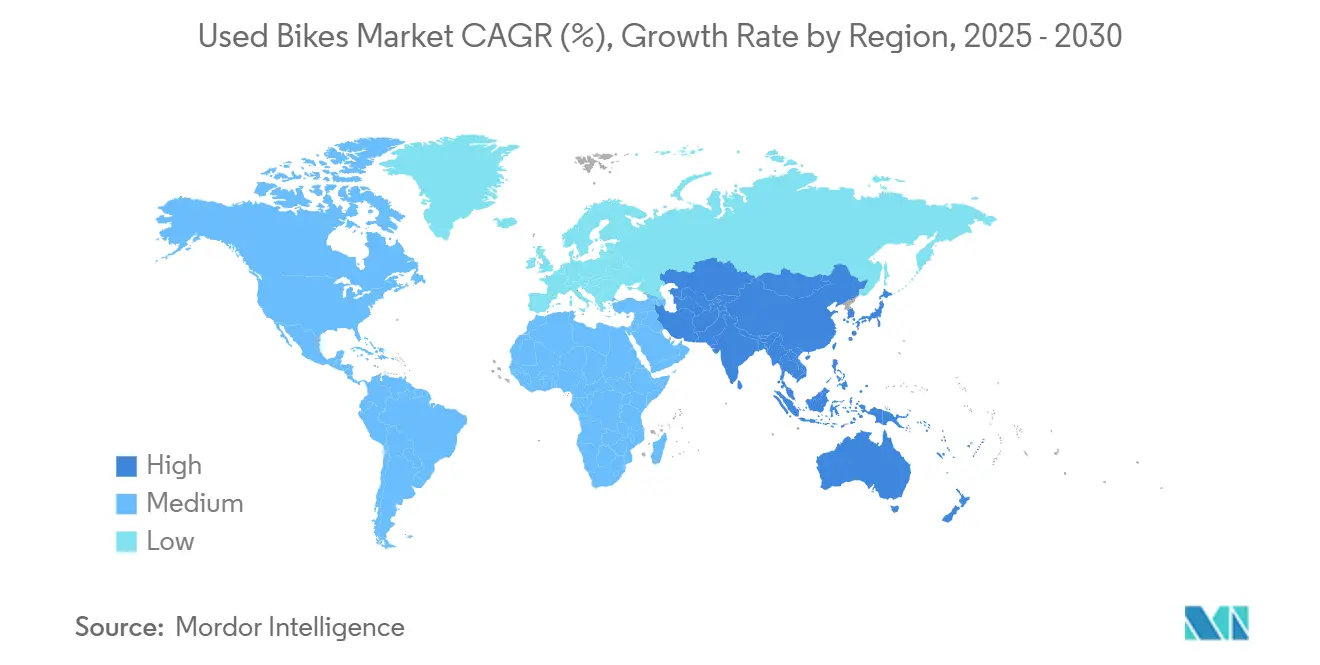

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

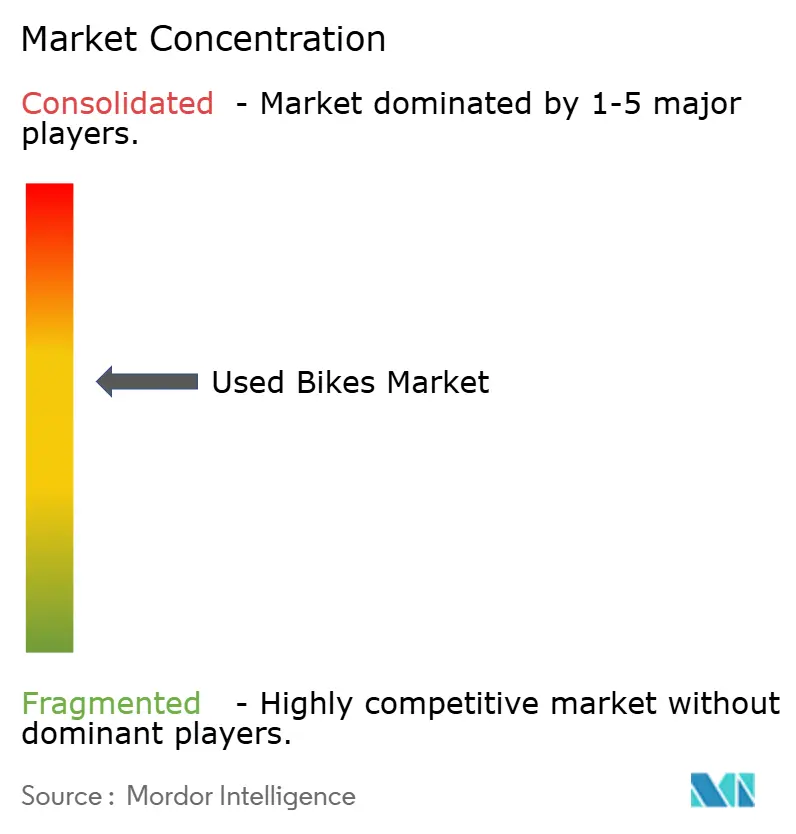

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Used Bikes Market Analysis by Mordor Intelligence

The Used Bikes Market size is estimated at USD 4.61 billion in 2025, and is expected to reach USD 5.75 billion by 2030, at a CAGR of 4.53% during the forecast period (2025-2030). This steady advance reflects mounting cost pressures on new-bike buyers, growing environmental awareness, and supportive workplace mobility subsidies that collectively redirect demand toward refurbished inventory. Municipal cycle-infrastructure expansion, tighter e-bike import tariffs, and OEM-certified refurbishment programs have further amplified secondary-market visibility among both first-time and repeat cyclists. Platform consolidation is beginning to resolve long-standing liquidity constraints, while AI-enabled pricing engines encourage individual sellers to engage more confidently. At the same time, battery-health uncertainty in e-bikes and persistent warranty gaps temper growth, compelling marketplaces to invest in diagnostic technology and insurance partnerships.

Key Report Takeaways

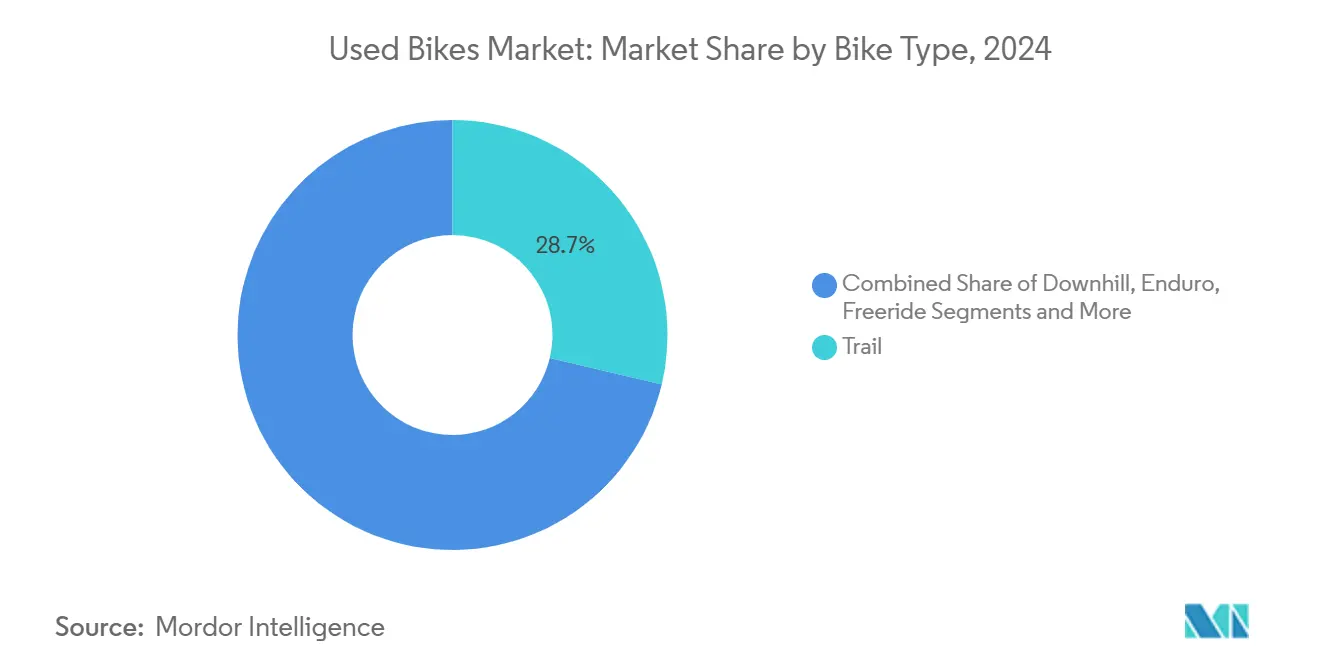

- By bike type, trail models accounted for a 28.73% share in the used bikes market in 2024, and are projected to register the highest 4.57% CAGR through 2030.

- By application, leisure riding held a 71.25% share in the used bikes market in 2024; racing bikes are expected to expand at a market-leading 4.61% CAGR over the same period.

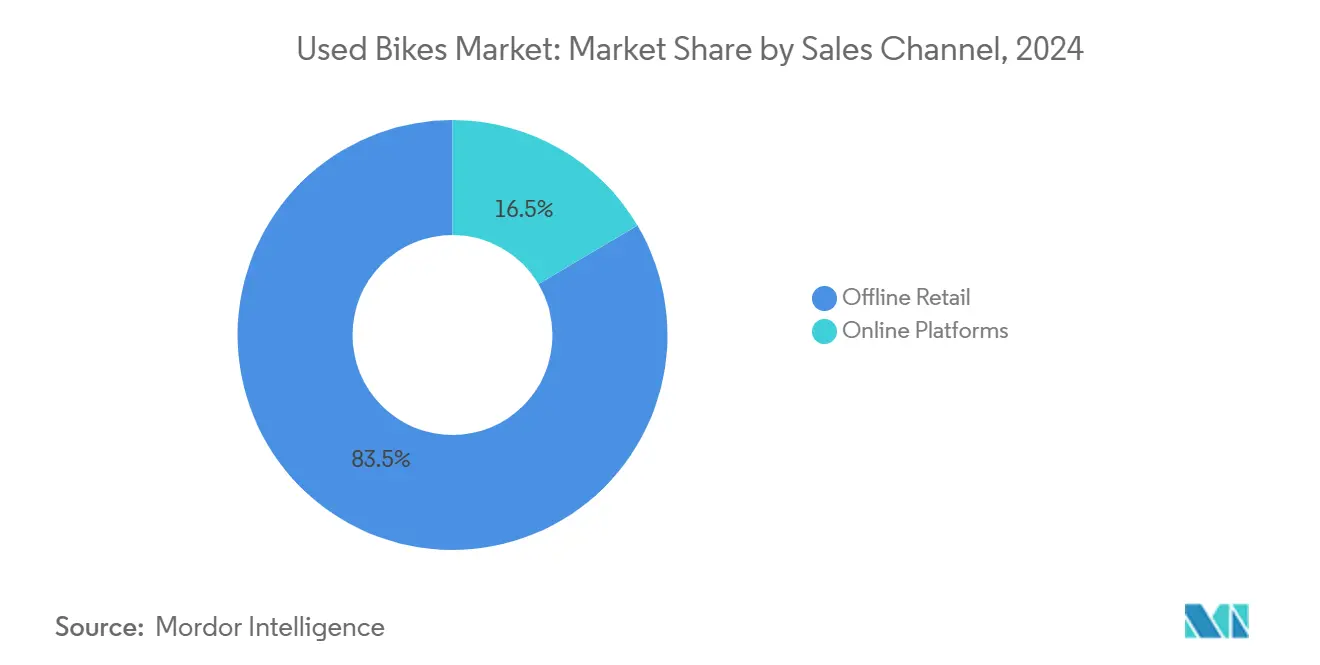

- By sales channel, offline retail commanded an 83.46% share in the used bikes market in 2024, whereas online platforms are poised to grow fastest at a 4.66% CAGR to 2030.

- By consumer segment, commuters captured a 43.25% share in the used bikes market in 2024; fitness-oriented buyers are set to post a 4.65% CAGR through 2030.

- By geography, Asia-Pacific contributed a 36.71% share in the used bikes market in 2024 and is projected to record a 4.55% CAGR to 2030.

Global Used Bikes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Focus On Affordable | +1.2% | Global, strongest in Europe and Asia Pacific | Medium term (2-4 years) |

| Surge In Online Resale Platforms | +0.9% | North America and Europe core, expanding to Asia Pacific | Short term (≤ 2 years) |

| Growing Popularity Of Mountain-Bike | +0.7% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| OEM-Certified Pre-Owned Programs | +0.6% | North America and Europe | Medium term (2-4 years) |

| Corporate Wellness Bike-Commuting Subsidies | +0.5% | Europe and North America | Medium term (2-4 years) |

| AI-Driven Dynamic Pricing Tools | +0.4% | Global, led by developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Focus on Affordable, Eco-Friendly Mobility

Public and corporate sustainability mandates are transforming refurbished bicycles into main stream transportation tools. Cycle-to-work schemes in Europe give employees two-fifth tax savings, effectively underwriting demand that bypasses retail shops entirely[1]“Employers’ Cycle to Work Guidance,” GOV.UK, gov.uk . Corporate procurement teams now specify certified used bikes because reconditioned models deliver comparable performance at three-fifth lower cost. These buyers also benefit from materially lower embedded carbon than purchasing new frames, helping firms meet Scope 3 emissions targets. Municipal bike-share operators in Belgium and the Netherlands have begun sourcing refurbished fleets to boost capacity within fixed budgets. The convergence of environmental reporting requirements and tight capital expenditure envelopes positions the used bikes market as a pragmatic solution for organizations under financial stress.

Surge in Online Resale Platforms

Digital marketplaces have dissolved geographic constraints that once limited liquidity in the used bike market.Germany-based Buycycle added component listings in 2024, bundling drivetrain sales with frame transactions to raise ticket sizes[2]“Spare Parts Launch Announcement,” Buycycle, buycycle.de. Real-time AI pricing tools ingest comparable-sales data, narrowing valuation spreads and shortening negotiation cycles. The closure and 2025 relaunch of The Pro’s Closet under Elshair Companies revealed the importance of scale economies in inventory management within the used bike market. Cross-border shipping agreements now allow European sellers to tap North American buyers, creating arbitrage plays professional resellers exploit. Hybrid models that merge peer-to-peer storefronts with on-staff mechanics for inspection services are emerging as the sector’s next trust-building mechanism.

Growing Popularity of Mountain-Bike Disciplines

Trail and enduro categories draw riders seeking versatility and aggressive geometry, reinforcing resale values that are less sensitive to commoditization. Broadcast coverage of the Enduro World Series provides halo effects lasting two-to-three years beyond model discontinuation in the used bike market. E-mountain bikes add a robust CAGR tailwind but raise battery-health valuation challenges, making diagnostic-ready platforms more attractive. Facility constraints, such as the conversion of some British Columbia trails into pickleball courts, cap participation in mature regions; however, indoor bike parks and pump tracks sustain year-round engagement. Advanced suspension and proprietary drivetrains make certified pre-owned programs appealing because they guarantee serviceability for technically complex models in the used bike market.

OEM-Certified Pre-Owned Programs

Manufacturers such as Trek and Giant are capturing secondary-market margins in the used bike market by refurbishing trade-ins and reselling them with limited warranties that command one-fourth premiums over peer listings. Trek’s Consumer Choice initiative allows direct-to-consumer fulfillment, bypassing dealer fees and feeding consistent inventory back into refurbishment loops. Programs generally restrict eligibility to bikes under six years old or originally priced above USD 1,500, which leaves entry-level buyers on unregulated platforms. Some OEMs now pilot component-only refurbishment, targeting high-value wheelsets and electronic drivetrains. While factory backing reduces perceived risk, it also concentrates supply of premium units, raising questions about future inventory sufficiency in the used bike market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quality And Warranty Concerns | -0.8% | Global, most acute in North America | Medium term (2-4 years) |

| Battery-Health Uncertainty | -0.7% | Global, led by developed markets | Medium term (2-4 years) |

| Lack Of Grading / Inspection Standards | -0.6% | Global, varies by regulatory framework | Long term (≥ 4 years) |

| Post-Pandemic Inventory Overhang Depressing Prices | -0.4% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Quality & Warranty Concerns for Used Bikes

Limited warranty transferability fuels buyer hesitancy, especially for carbon frames and e-bike drive units where repair costs are high. Many independent shops refuse service on bikes sourced from online classifieds, creating post-purchase support gaps that deter novice cyclists. Commercial insurers often exclude coverage for secondhand fleets used in delivery applications, narrowing the addressable B2B segment. Absence of an internationally recognized grading protocol lets sellers overstate component condition, amplifying information asymmetry. Marketplaces that offer in-house refurbishment and six-month warranties consistently secure higher conversion rates, illustrating the premium customers place on post-sale assurance.

Battery-Health Uncertainty in Used E-Bikes

Lithium-ion packs lose one-fifth of their capacity during the first ownership year, radically altering residual values in the used bike market. Replacement batteries can cost two-fifths of a bike’s original MSRP, making accurate capacity measurement central to fair pricing. Proprietary battery-management systems block third-party diagnostic apps, forcing buyers to trust screenshots or subjective claims. UL 2849 certification in the United States and the EU Battery Regulation impose safety disclosures that do not always apply to older models, complicating cross-border transactions[3]“Regulation on Batteries and Waste Batteries,” European Commission, eur-lex.europa.eu . Leasing schemes introduced for new e-bikes are not yet available in the used channel, leaving a financing void that stifles upgrade cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bike Type: Trail Dominance Drives Premium Valuations

Trail models delivered 28.73% of 2024 revenue, the single largest slice of the used bikes market size. Their capability across commuting and singletrack explains resilient liquidity during seasonal demand shifts. Trail variants are expected to rise at a 4.57% CAGR as improved motor compactness of Battery-assisted Trail variants reduces weight penalties. Freeride and downhill categories remain niche, yet their specialized geometry secures premium resale prices within enthusiast circles. Fat-bike demand clusters in snow-prone geographies, producing regional price spikes that professional traders monitor for arbitrage. Suspension and component complexity make buyers gravitate toward refurbishment programs, reinforcing OEMs’ growing influence in the used bikes industry.

Price erosion is slower for high-spec enduro bikes because limited production runs and racing endorsements create scarcity. Conversely, simple hardtail cross-country frames churn more frequently, leading to steeper early-life depreciation but faster liquidity on classifieds. The used bikes market share for trail models is expected to climb marginally as trail-capable gravel bikes siphon demand from traditional hardtails. Continuous improvements in dropper-post design and tubeless-tire compatibility enhance the value proposition of secondhand builds, boosting average selling prices on specialized platforms.

By Application: Leisure Segment Sustains Market Foundation

Leisure riding generated 71.25% of 2024 sales, underscoring the importance of comfort-oriented geometry and reliability. Family budgets favor secondhand hybrids and cruisers because spare-part availability lowers lifetime ownership costs. Meanwhile, racing bikes are on track for a 4.61% CAGR as event participation rebounds, widening the used bikes market size for performance equipment. Aggressive seat-tube angles and carbon lay-ups limit broad appeal, yet aspirational buyers still view ex-pro frames as gateways into competition.

Overlap between leisure and commuting blurs product boundaries, spurring interest in multipurpose racks, fenders, and relaxed cockpit setups. Suburban weekend riders increasingly pick up used racing frames to gain speed on charity rides, fueling cross-segment inventory flows. Corporate wellness reimbursements remove sticker shock for many commuters, incentivizing them to invest in higher-quality albeit previously owned models. This blending of use cases keeps stock-turn high for versatile platforms while leaving ultra-niche designs more exposed to price swings.

By Sales Channel: Digital Transformation Accelerates

Offline outlets retained 83.46% of 2024 turnover, benefiting from hands-on inspection that assuages safety worries. Brick-and-mortar consignment corners within bike shops allow local sellers to leverage professional mechanic endorsements. However, online marketplaces are scaling fastest at 4.66% CAGR, due to AI valuation dashboards and escrow payment solutions that minimize fraud. Augmented-reality sizing apps reduce misfit risk, nudging cautious shoppers toward remote purchases.

Shipping-damage anxiety persists, prompting hybrid models where buyers reserve bikes online and test-ride at partner shops before final payment. Marketplace partnerships with last-mile couriers that include pre-assembly services are tackling the complexity of shipping fully built e-bikes. As algorithms refine seasonal demand curves, sellers time listings to peak price windows, elevating margins and supply fluidity. Offline retailers respond by broadcasting real-time floor inventory across social channels to widen reach without sacrificing in-store experience.

By Consumer Segment: Commuters Lead Market Expansion

Commuters absorbed 43.25% of 2024 demand, validated by crowded urban bike lanes and expanded secure parking facilities. Employer subsidies and ride-to-work tax programs shift purchasing power toward higher-spec secondhand machines, increasing average transaction value. Fitness-centric buyers form the fastest-growing cohort at 4.65% CAGR, capitalizing on smart-trainer integrations that allow seamless indoor-outdoor use.

Delivery couriers prize robustness and minimal maintenance; they often select steel frames and hub-gear drivetrains, creating sub-markets with lower but more stable pricing. Students remain highly price-sensitive, gravitating toward basic models that trade at higher velocity but thinner margins. Engagement campaigns by city councils highlight cycling’s health benefits, nudging casual riders into regular commuting habits that sustain used bikes market momentum.

Geography Analysis

Asia-Pacific commanded a 36.71% revenue lead in 2024, the highest regional slice of the used bikes market share. Rapid urbanization in China and India funnels commuters toward two-wheels as congestion worsens and parking costs soar. Government-backed pollution targets encourage corporate fleet electrification, indirectly stimulating demand for secondhand conventional bicycles when companies offload legacy stock. Japan operates mature digital resale ecosystems with strict grading criteria that lift buyer confidence. In contrast, Indonesia and Vietnam rely primarily on social media listings, limiting formal warranty uptake. The region’s 4.55% CAGR outlook rests on continued bike-lane build-outs and the regional harmonization of safety standards.

North America remains the spiritual home of premium mountain bikes, making it a magnet for high-ticket transactions. Post-pandemic inventory gluts have depressed prices, attracting hobbyists who now afford carbon builds previously out of reach. Tariff regimes that elevate the landed cost of new imports incentivize domestic resale. Relabeled factory-demo units from OEM demo fleets further bolster supply. The U.S. market’s fragmented state is evident in regional price dispersion; savvy resellers leverage arbitrage by transporting inventory from saturated to undersupplied metro areas.

Europe benefits from a coherent policy framework that supports cycling as both transport and recreation. Cycle-to-work incentives in the U.K., Belgium, and the Netherlands yield predictable demand independent of consumer sentiment swings. German dealers integrate trade-in portals directly into point-of-sale systems, ensuring steady certified inventory. EU Battery Regulation adds compliance complexity to cross-border e-bike sales, temporarily constraining used battery-assisted models while pushing traction toward traditional frames. Scandinavia’s high willingness to pay for warranty coverage underpins premium pricing. Brexit-related customs frictions affect only a minor share of secondary transactions because most sales remain domestic.

Competitive Landscape

The used bikes market exhibits moderate fragmentation, with no single player exceeding one-tenth penetration. Generalist sites like eBay and Facebook Marketplace offer vast reach but minimal authentication, appealing to bargain hunters tolerant of risk. Vertical specialists such as Buycycle and Pinkbike BuySell attract enthusiasts willing to pay higher commissions for curated listings. The 2025 resurrection of The Pro’s Closet underscores the need for disciplined inventory turnover; the refocused model leans on consignment rather than outright purchases to limit capital lock-up.

OEMs are increasingly active. Trek, Giant, and Brompton deploy certified refurb schemes that capture margin, control brand presentation, and dampen gray-market cannibalization. Their limited warranty coverage and verified inspections justify one-fourth premiums and deepen brand loyalty. Technological differentiation is emerging through AI pricing models, automated condition assessments, and blockchain-based provenance tracking. Platforms that integrate these features improve liquidity and reduce transaction cycles, giving them a competitive edge over classifieds.

Regulatory barriers such as UL 2849 e-bike certification and regional import duties raise the administrative bar for new entrants, incentivizing partnerships between marketplaces and logistics firms specializing in hazmat-compliant battery shipping. White-space opportunities lie in battery leasing for secondhand e-bikes, corporate fleet remarketing portals, and subscription-based maintenance. Geographic expansion is tempered by language localization costs and differences in consumer protection statutes, leading most platforms to deepen share in home markets before crossing borders.

Used Bikes Industry Leaders

eBay

The Pro’s Closet

BikeExchange

Buycycle

Craigslist

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The Pro’s Closet reopened under Elshair Companies, restoring consignment services and prioritizing dealer partnerships to reduce capital exposure.

- October 2024: Buycycle added pre-owned components to its catalog, targeting drivetrain and wheel sales to increase customer-lifetime value.

- October 2024: Brompton introduced its Renewed factory-refurbished folding bikes in North America, marking a significant OEM entry into certified used sales.

- July 2024: Trek launched Consumer Choice direct-to-consumer sales with integrated trade-in options feeding its refurbishment pipeline.

Global Used Bikes Market Report Scope

| Cross-Country |

| Downhill |

| Enduro |

| Trail |

| Freeride |

| Dirt Jumping |

| Fat Bikes |

| Racing |

| Leisure |

| Offline Retail |

| Online Platforms |

| Students |

| Commuters |

| Recreational Riders |

| Fitness Enthusiasts |

| Delivery Workers |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Bike Type | Cross-Country | |

| Downhill | ||

| Enduro | ||

| Trail | ||

| Freeride | ||

| Dirt Jumping | ||

| Fat Bikes | ||

| By Application | Racing | |

| Leisure | ||

| By Sales Channel | Offline Retail | |

| Online Platforms | ||

| By Consumer Segment | Students | |

| Commuters | ||

| Recreational Riders | ||

| Fitness Enthusiasts | ||

| Delivery Workers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the 2025 valuation of the used bikes market?

The used bikes market size reached USD 4.61 billion in 2025.

How fast is secondary bicycle commerce expected to grow through 2030?

Revenue is projected to advance at a 4.53% CAGR between 2025 and 2030.

Which bike type currently dominates resale activity?

Trail models held 28.73% of 2024 sales, the largest share among bike types.

Which geographic region leads in used bicycle revenue?

Asia-Pacific contributed 36.71% of 2024 global revenue and is forecast to remain in front.

What is the biggest technical restraint facing e-bike resales?

Battery-health uncertainty, with first-year capacity loss reaching 20-30%, complicates valuation and safety checks.

Which sales channel is expanding fastest?

Online platforms are projected to grow at 4.66% CAGR to 2030, outpacing offline outlets.

Page last updated on: