Used Semi-Truck Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

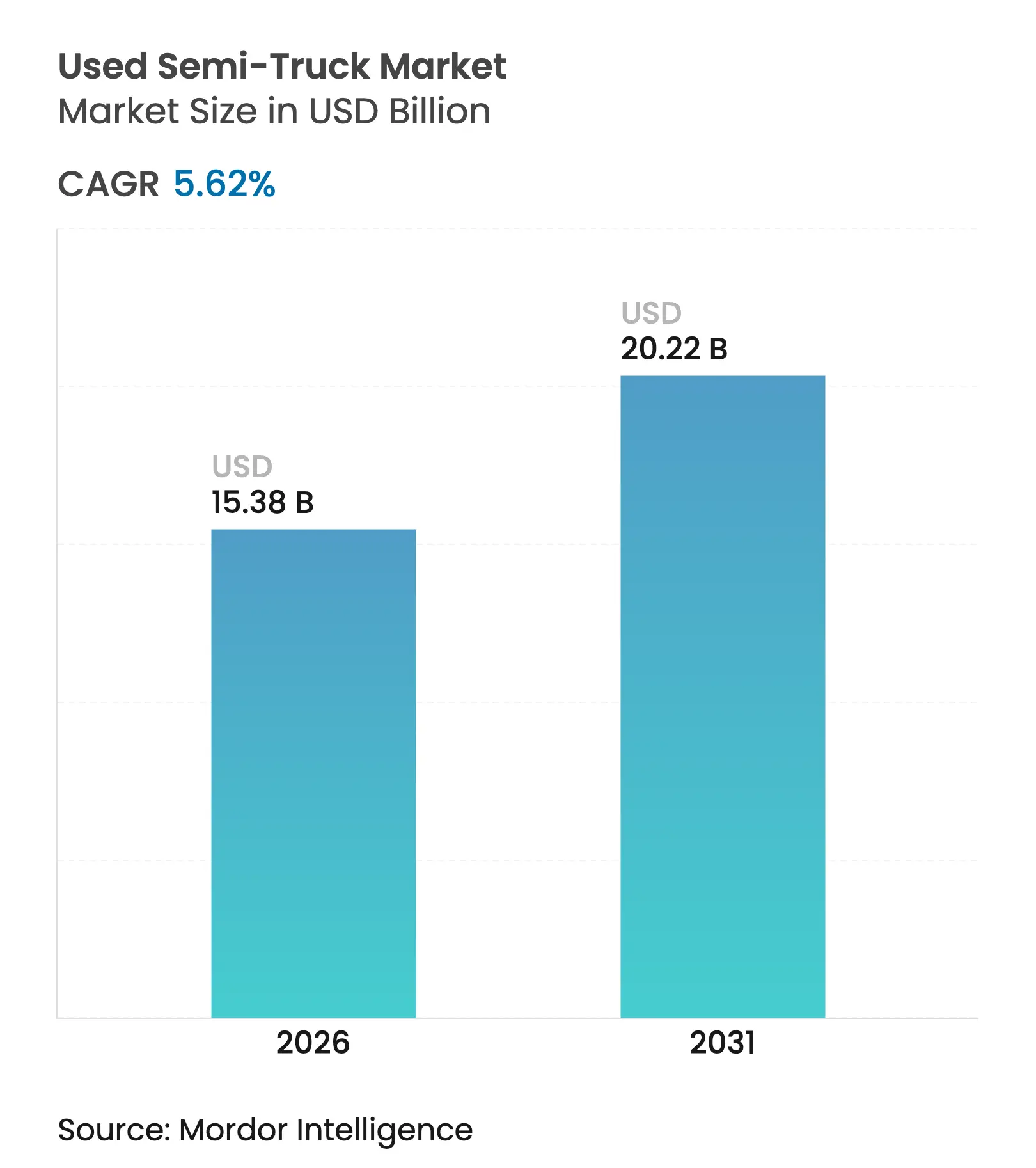

| Market Size (2026) | USD 15.38 Billion |

| Market Size (2031) | USD 20.22 Billion |

| Growth Rate (2026 - 2031) | 5.62 % CAGR |

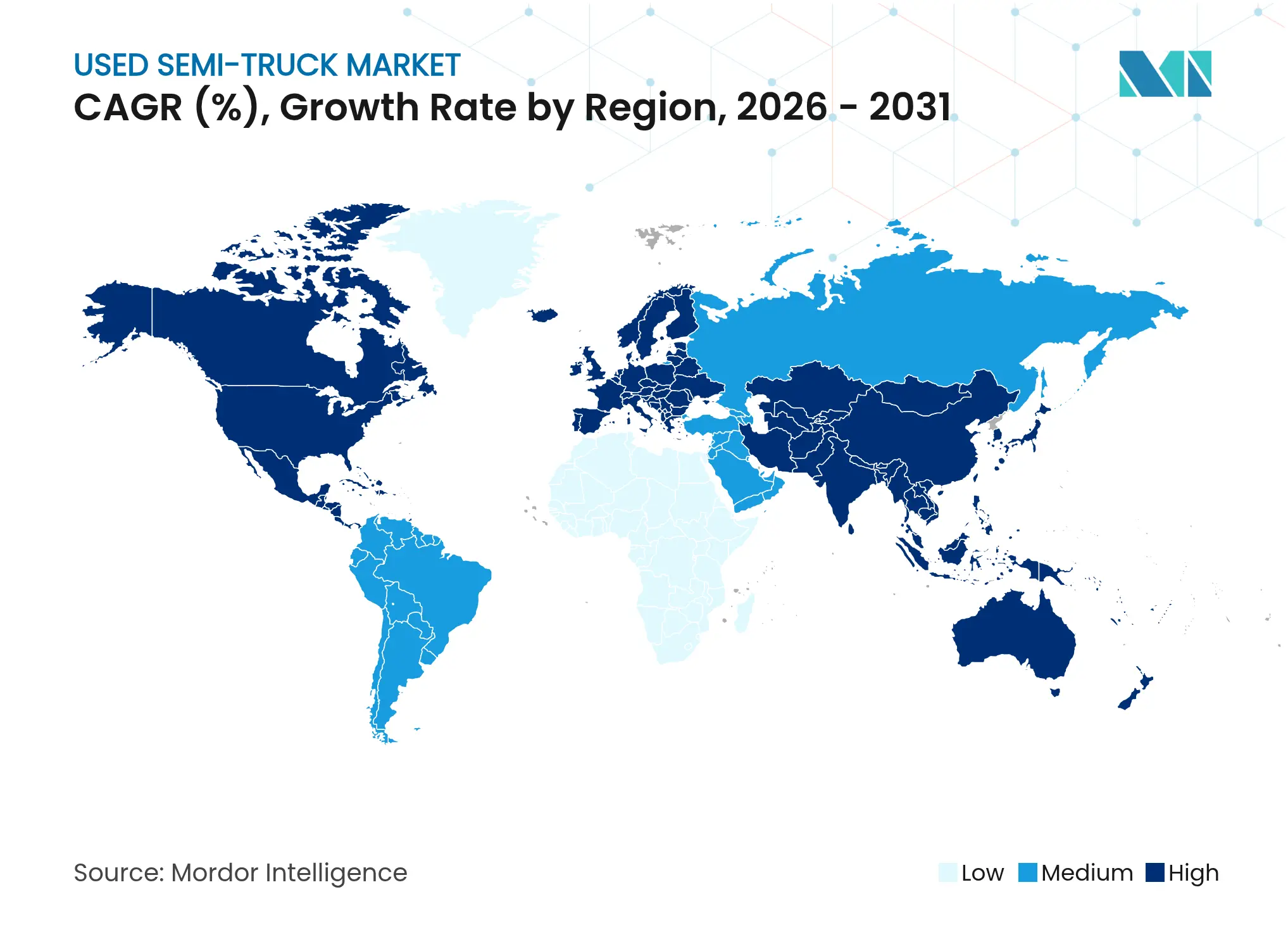

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Used Semi-Truck Market Analysis by Mordor Intelligence

Used semi-truck market size in 2026 is estimated at USD 15.38 billion, growing from 2025 value of USD 14.56 billion with 2031 projections showing USD 20.22 billion, growing at 5.62% CAGR over 2026-2031. Fleet operators are accelerating pre-2027 purchases to avoid Environmental Protection Agency Phase 3 compliance costs that could add USD 20,000–30,000 to a new tractor’s sticker price[1]"Final Rule: Greenhouse Gas Emissions Standards for Heavy-Duty Vehicles – Phase 3", United States Environmental Protection Agency, www.epa.gov.. Heavy-duty models retain commanding resale value thanks to 10–15-year service lives, while rapid e-commerce expansion is pulling light-duty volumes higher. Diesel technology still dominates, but battery-electric trucks are gaining ground as retrofit kits, second-life battery programs, and green-loan financing improve the economics of electrification. Digital auction houses and data-driven marketplaces are boosting price discovery, reshaping traditional dealer economics, and extending the geographic reach of every transaction.

Key Report Takeaways

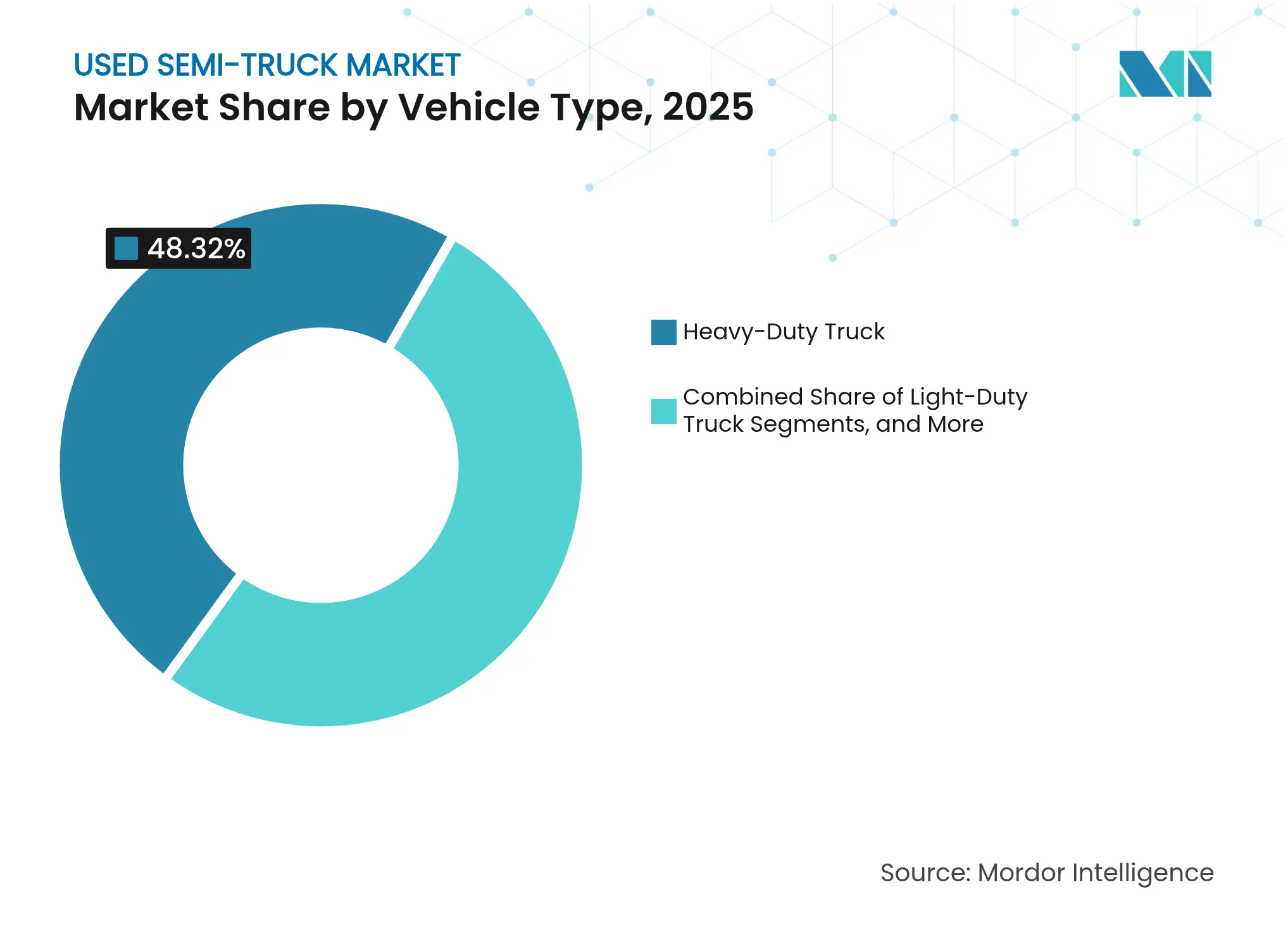

- By vehicle type, heavy-duty trucks led with 48.32% of the used semi-truck market share in 2025; light-duty units are projected to grow at a 16.74% CAGR through 2031.

- By propulsion, internal-combustion trucks held 86.85% of the used semi-truck market share in 2025, while battery-electric trucks are on track for a 34.96% CAGR to 2031.

- By sales channel, franchised dealers captured 45.78% of the used semi-truck market in 2025; online auction platforms exhibit the highest forecast CAGR at 18.76% to 2031.

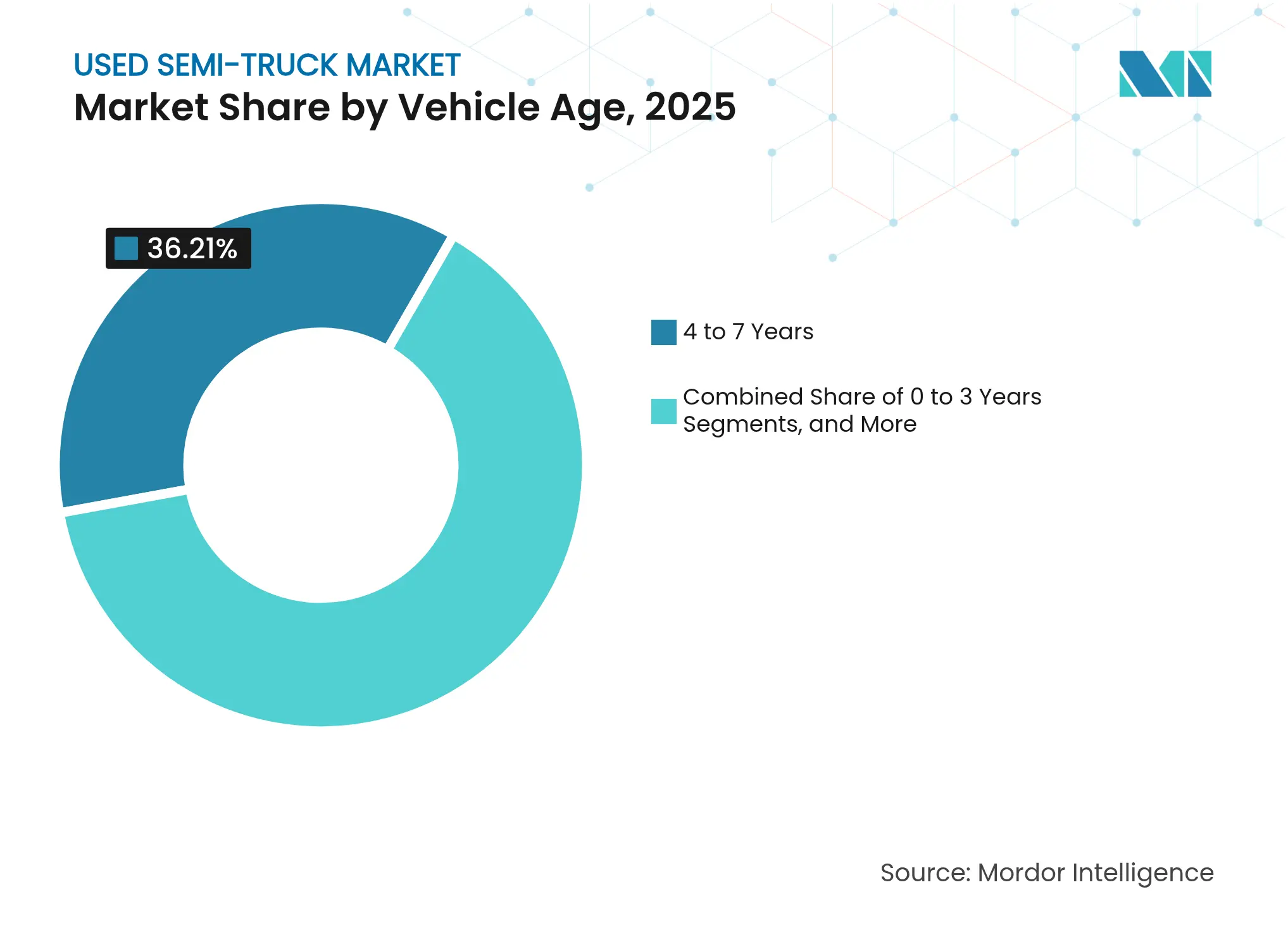

- By vehicle age, the 4-7-year cohort accounted for 36.21% of the used semi-truck market in 2025 transactions, whereas the 0 to 3-year cohort is advancing at 20.12% CAGR during the forecast period.

- By end-use, logistics and freight activities represented 46.35% of the used semi-truck market size in 2025 and are expanding at 13.84% through 2031.

- By geography, North America commanded 34.05% of the used semi-truck market revenue in 2025; Asia-Pacific is set to climb at an 11.21% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Used Semi-Truck Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

OEM Production Bottlenecks Shift Demand To Used Inventory OEM Production Bottlenecks Shift Demand To Used Inventory | +1.5% | North America & Europe primarily | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:+1.5% | Geographic Relevance:North America & Europe primarily | Impact Timeline:Short term (≤ 2 years) |

Cost-Effective Ownership & Affordability Cost-Effective Ownership & Affordability | +1.2% | Global, with strongest impact in North America & Europe | Short term (≤ 2 years) | |||

Rapid E-Commerce-Driven Freight Growth Rapid E-Commerce-Driven Freight Growth | +0.8% | Global, concentrated in Asia-Pacific and North America | Medium term (2-4 years) | |||

Data-driven online marketplaces improving price transparency Data-driven online marketplaces improving price transparency | +0.7% | Global, led by North America adoption | Medium term (2-4 years) | |||

ESG-linked financing incentives for life-cycle extension ESG-linked financing incentives for life-cycle extension | +0.6% | Europe and North America, expanding to Asia-Pacific | Long term (≥ 4 years) | |||

Battery-electric retrofitting kits extending fleet life Battery-electric retrofitting kits extending fleet life | +0.4% | Europe and select North American markets | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

OEM Production Bottlenecks Shift Demand To Used Inventory

Manufacturing constraints across major truck OEMs have created extended delivery timelines for new vehicles, with some customers facing wait times exceeding 12 months for specific configurations, thereby redirecting immediate capacity needs toward the used market. Production challenges stem from semiconductor shortages, supply chain disruptions, and strategic inventory management as manufacturers prepare for 2027 regulatory transitions, with some OEMs deliberately constraining current-generation production to avoid excess inventory. TRATON GROUP's 10% decline in Q1 2025 unit sales to 73,100 vehicles exemplifies industry-wide production normalization efforts that are tightening new vehicle availability. Fleet operators requiring immediate replacements are increasingly willing to pay premium prices for late-model used trucks rather than delay operations while waiting for new deliveries. This dynamic has created arbitrage opportunities for dealers and auction platforms, as the spread between new and used vehicle pricing has compressed significantly compared to historical norms.

Cost-Effective Ownership & Affordability

Fleet operators increasingly gravitate toward used semi-trucks as regulatory compliance costs for new vehicles escalate dramatically, with 2027 EPA-compliant tractors expected to cost 10-12% more than current models. This cost differential is particularly pronounced for small and medium enterprises that lack the capital reserves to absorb higher acquisition costs, creating sustained demand for pre-regulation inventory. The total cost of ownership advantage extends beyond purchase price, as older trucks avoid the complexity and maintenance costs associated with advanced emissions control systems required for 2027 compliance. Financing institutions are responding by extending loan terms for certified pre-owned vehicles, with some lenders offering rates comparable to new truck financing for vehicles meeting specific age and mileage criteria. The affordability imperative is further amplified by rising interest rates, which have increased monthly payments for new truck purchases by approximately 15-20% since 2023, making used alternatives increasingly attractive for cost-conscious operators.

Rapid e-commerce-driven freight growth

E-commerce expansion continues to generate substantial demand for last-mile and regional delivery vehicles, with medium-duty trucks experiencing particularly strong secondary market activity as logistics providers scale operations without committing to new vehicle capital expenditures. The shift toward omnichannel fulfillment models requires diverse fleet compositions, driving demand for specialized used vehicles, including refrigerated units, liftgate-equipped trucks, and urban delivery configurations that may have limited availability in new production schedules. Amazon's logistics network expansion and similar initiatives by major retailers are creating downstream effects throughout the used semi-truck market, as smaller logistics providers seek cost-effective vehicles to compete for subcontracting opportunities. The growth trajectory is particularly evident in Asia-Pacific markets, where e-commerce penetration rates continue climbing and infrastructure development supports expanded freight networks. Digital freight matching platforms are simultaneously improving asset utilization rates, extending the economic viability of older trucks that might otherwise be retired from service[2]"Trends in heavy-duty electric vehicles", International Energy Agency,iea.org..

Data-driven online marketplaces improving price transparency

Digital transformation across semi-truck remarketing is fundamentally altering price discovery mechanisms, with platforms like RB Global's Marketplace-E serving 1.3 million registered users and facilitating transparent bidding processes that reduce information asymmetries between buyers and sellers. Advanced analytics platforms are incorporating real-time market data, maintenance records, and operational history to generate more accurate residual value predictions, enabling both buyers and sellers to make informed decisions based on comprehensive vehicle lifecycle data. AI-driven pricing algorithms are beginning to factor in regulatory compliance status, fuel efficiency ratings, and regional demand patterns to optimize listing strategies and timing. The proliferation of digital channels has expanded market reach beyond traditional geographic boundaries, with online auctions now attracting international buyers and creating more competitive pricing environments. McKinsey research indicates that AI-enhanced remanufacturing processes can improve profit margins by 2-4% through optimized core forecasting and pricing strategies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rising Regulatory Barriers on High-Emission Legacy Engines Rising Regulatory Barriers on High-Emission Legacy Engines | -1.1% | North America & Europe primarily | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-1.1% | Geographic Relevance:North America & Europe primarily | Impact Timeline:Short term (≤ 2 years) |

Persistent Quality & Reliability Concerns Persistent Quality & Reliability Concerns | -0.9% | Global, most pronounced in developing markets | Medium term (2-4 years) | |||

Limited Certified Refurbishment Infrastructure Limited Certified Refurbishment Infrastructure | -0.6% | Global, acute in Asia-Pacific and MEA regions | Long term (≥ 4 years) | |||

Export Restrictions Limiting Cross-Border Secondary Sales Export Restrictions Limiting Cross-Border Secondary Sales | -0.7% | Global, concentrated impact on MEA and South America | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Persistent Quality and Reliability Concerns

Quality assurance challenges continue to constrain the expansion of the used semi-truck market, particularly as buyers struggle to assess the true condition and remaining useful life of complex modern vehicles equipped with sophisticated emissions control and electronic systems. The absence of standardized condition reporting across the industry creates information asymmetries that inflate risk premiums and reduce buyer confidence, especially for high-mileage or older vehicles approaching major maintenance intervals. Certified pre-owned programs like Peterbilt's Red Oval Certified initiative, which requires 150-point inspections and offers extended warranties, represent attempts to address quality concerns but remain limited in scope and geographic coverage. The complexity of modern truck systems makes independent quality assessment increasingly difficult for smaller buyers who lack specialized diagnostic capabilities. Warranty limitations and the high cost of major repairs for sophisticated emissions systems create ongoing concerns about the total cost of ownership for used vehicle purchasers.

Limited Certified Refurbishment Infrastructure

The scarcity of qualified refurbishment facilities capable of restoring used semi-trucks to like-new condition constrains market growth by limiting the supply of high-quality used vehicles that can command premium pricing. Refurbishment requires specialized equipment, trained technicians, and access to OEM parts and specifications, creating barriers to entry that have prevented the development of a robust refurbishment ecosystem comparable to other commercial equipment sectors. The remanufactured parts market, valued at USD 7 billion, offers 40-60% cost savings compared to new components but requires sophisticated reverse logistics and quality control processes that many potential refurbishers lack. Geographic concentration of refurbishment capabilities in developed markets creates supply chain inefficiencies and limits access to refurbished vehicles in emerging markets where demand is growing rapidly. The transition to electric and hybrid powertrains will require new refurbishment competencies that current facilities may lack, potentially exacerbating infrastructure constraints.

Segment Analysis

By Vehicle Type: Heavy-Duty Dominance Amid Light-Duty Acceleration

Heavy-duty trucks maintain commanding market leadership with 48.32% of the used semi-truck market share in 2025, reflecting their extended operational lifecycles, higher residual values, and the substantial capital investments required for new vehicle acquisition in this segment. The segment's dominance stems from fleet operators' preference for maximizing asset utilization through extended ownership periods, often keeping heavy-duty trucks in service for 10-15 years compared to 7-10 years for lighter vehicles. Light-duty trucks are experiencing rapid expansion at 16.74% CAGR through 2031, driven by e-commerce growth, last-mile delivery requirements, and the proliferation of urban logistics applications that favor smaller, more maneuverable vehicles. Medium-duty trucks occupy a stable middle position, serving specialized applications including regional delivery, municipal services, and construction support, where their payload capacity and maneuverability advantages create sustained demand.

The regulatory prebuy phenomenon is particularly pronounced in the heavy-duty segment, where EPA 2027 compliance costs could add USD 25,000 to new vehicle prices, creating strong incentives for fleet operators to acquire pre-regulation inventory through the used market. Class 8 truck production outpaced expectations in 2024 with 308,200 factory shipments. Still, retail sales lagged behind production, leading to record inventory levels that are now flowing into the used market as dealers manage working capital constraints. The emergence of truck-as-a-service models could reshape vehicle type preferences, as operators gain access to diverse fleet compositions without long-term ownership commitments, potentially accelerating turnover rates across all vehicle categories.

Note: Segment shares of all individual segments available upon report purchase

By Propulsion Type: ICE Resilience Meets Electric Disruption

Internal combustion engine vehicles command 86.85% of the used semi-truck market share in 2025, demonstrating the continued relevance of proven diesel technology despite mounting regulatory and environmental pressures. This dominance reflects the mature infrastructure supporting diesel vehicles, established maintenance networks, and the operational flexibility that ICE trucks provide across diverse duty cycles and geographic regions. Battery electric trucks are accelerating at 34.96% CAGR through 2031, driven by total cost of ownership improvements, regulatory mandates, and the development of charging infrastructure that supports commercial operations. Hybrid vehicles occupy a transitional position, offering fuel efficiency benefits while maintaining the operational flexibility that pure electric vehicles may lack in certain applications.

The International Energy Agency reported that global sales of electric medium- and heavy-duty trucks exceeded 90,000 units in 2024, marking an 80% increase primarily driven by China's vehicle scrappage schemes and purchase incentives. Battery electric trucks are expected to achieve total cost of ownership parity with diesel vehicles in China and Europe by 2030, creating compelling economic incentives for fleet electrification that will generate substantial used electric truck inventory. The development of battery second-life applications and retrofit programs could extend the economic viability of electric trucks beyond their initial operational lifecycle, creating new value streams that support higher residual values. Renewable natural gas and renewable diesel alternatives are gaining traction as bridge technologies that allow fleet operators to reduce emissions while maintaining existing vehicle infrastructure.

By Sales Channel: Digital Transformation Reshapes Distribution

Franchised dealers maintain a 45.78% of the used semi-truck market share in 2025, leveraging established customer relationships, financing capabilities, and service networks that provide comprehensive support throughout the vehicle lifecycle. The franchised channel's strength lies in its ability to offer integrated solutions, including maintenance, parts, and warranty support that independent channels may struggle to match. Online auction platforms are expanding rapidly at a 18.76% CAGR through 2031, driven by digital transformation initiatives that improve price transparency, expand geographic reach, and reduce transaction costs for buyers and sellers. Independent dealers continue serving specialized market segments and providing personalized service that larger channels may not offer, while customer-to-customer transactions remain important for individual operators and small fleets.

RB Global's acquisition of IAA and expansion of its digital marketplace capabilities demonstrate the strategic importance of online channels, with the company processing 1.3 million registered users across its platforms and generating USD 1.73 billion in revenue from 228,000 asset sales in 2023. Mitsui's acquisition of Taylor & Martin Enterprises reflects international interest in the U.S. truck auction business, recognizing the market's USD 13.5 million truck fleet as a substantial opportunity for value-added services. Integrating AI-driven residual value analytics and predictive pricing algorithms enables more sophisticated inventory management and pricing strategies across all sales channels. Through platforms like GovPlanet, government surplus channels contribute additional inventory, particularly for specialized vehicles and equipment that may not be available through traditional commercial channels.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

By Age of Vehicle: Near-New Inventory Gains Momentum

The 4-7 years age segment represents 36.21% of the used semi-truck market size in 2025, reflecting the sweet spot where vehicles retain significant operational capability while offering substantial cost savings compared to new alternatives. This age category benefits from completing initial depreciation curves while avoiding the higher maintenance costs and reliability concerns associated with older vehicles. The 0-3 years segment is expanding at 20.12% CAGR through 2031, driven by OEM production bottlenecks forcing immediate capacity needs toward nearly-new inventory, lease returns from shortened replacement cycles, and fleet optimization strategies favoring newer, more efficient vehicles. The 8-15 years category continues serving price-sensitive market segments, while vehicles over 15 years face increasing regulatory constraints and operational limitations.

Copart's Q4 2024 earnings revealed an 8.6% year-over-year decline in the Manheim Used Vehicle Value Index, indicating broader used vehicle market pressures affecting pricing across age categories. The company's 20.4% increase in volume from non-insurance sellers, particularly in fleet and rental segments, suggests that commercial operators are accelerating vehicle turnover to optimize fleet composition ahead of regulatory changes. Ryder System has lowered residual value estimates to mitigate risks associated with used vehicle pricing volatility, reflecting industry-wide concerns about asset values in an uncertain regulatory environment. The emergence of certified pre-owned programs creates premium pricing tiers within age categories, as buyers seek quality assurance and warranty protection for their used vehicle investments.

Note: Segment shares of all individual segments available upon report purchase

By End-use Industry: Logistics Leadership Drives Market Dynamics

Logistics and freight applications dominate with a 46.35% of the used semi-truck market share in 2025 while maintaining a 13.84% growth through 2031, underscoring the sector's fundamental role in supporting economic activity despite cyclical freight market volatility. The segment's resilience stems from structural demand drivers, including e-commerce growth, supply chain regionalization, and the ongoing need for goods movement across diverse economic conditions. Construction applications benefit from infrastructure spending initiatives and urban development projects that require specialized vehicles with extended operational lifecycles. Mining and quarrying operations typically retain vehicles longer due to harsh operating conditions and specialized configurations that limit resale markets, creating distinct pricing dynamics within this segment.

The trucking industry's capacity outlook for 2025 indicates stabilization after a period of excess capacity, with motor carrier registrations increasing 13% despite a 3.7% decrease in operating authorities, suggesting market consolidation that could affect used vehicle demand patterns. Agriculture and forestry applications face seasonal demand variations and specialized equipment requirements that create niche market opportunities for dealers and auction platforms with expertise in these sectors. Municipal and utility applications often involve extended replacement cycles and specific regulatory requirements influencing vehicle specifications and resale values. The emergence of truck-as-a-service models could reshape end-use industry preferences by providing access to diverse vehicle types without long-term ownership commitments, potentially accelerating turnover rates across all application categories.

Geography Analysis

North America secured 34.05% of the used semi-truck market revenue in 2025, aided by mature infrastructure, diverse financing, and high digital adoption. Prospective 25% import tariffs on Canadian and Mexican trucks could affect 45% of cross-border movements, supporting domestic resale prices.

Asia-Pacific leads growth at 11.21% CAGR. Mainland policy favors CNG and LNG rigs, while subsidy-driven electric adoption accelerates. India’s highway build-out and e-commerce boom underpin demand for diesel and electric trucks. Indonesia’s market, over 16 tons, grew 2.5% amid a 10% overall decline, highlighting infrastructure-related heavy-haul needs.

Europe is normalizing after elevated pandemic-era backlogs. TRATON unit deliveries slowed, while the European Investment Bank’s green loan to Ayvens finances 19,000 electric vans that will form tomorrow’s used semi-truck market inventory. Brazil props up South American demand; elsewhere, the continent remains mixed. Export restrictions and currency swings temper activity in the Middle East and Africa. However, cross-border land bridges like Trucknet’s Gulf-Israel logistics route cut transit times and lift tractor utility.

Competitive Landscape

Market Concentration

The used semi-truck market exhibits moderate fragmentation with established auction houses, franchised dealers, and emerging digital platforms competing across multiple distribution channels and geographic markets. Traditional franchised dealers leverage established customer relationships and integrated service capabilities, while independent dealers focus on specialized market segments and personalized service offerings that larger channels may not provide.

The competitive intensity is increasing as digital transformation enables new entrants to access previously protected geographic markets and customer segments. Strategic consolidation reshapes the competitive landscape, with major OEMs forming partnerships to address technological transitions and regulatory compliance challenges. Daimler Truck and Volvo Group's joint venture to develop a software-defined vehicle platform, launched as Coretura in 2025, demonstrates how traditional competitors collaborate on foundational technologies while maintaining competitive differentiation in other areas.

The emergence of AI-driven residual value analytics, truck-as-a-service models, and battery second-life ecosystems creates new competitive dynamics that favor companies with technological capabilities and data analytics expertise. International expansion continues as demonstrated by Mitsui's acquisition of Taylor & Martin Enterprises to enter the U.S. truck auction business, recognizing the strategic value of the world's largest truck fleet market.

Used Semi-Truck Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Daimler Truck and Toyota finalized their plan to merge truck manufacturing subsidiaries Hino Motors and Mitsubishi Fuso Truck & Bus under a new holding company by April 2026, with each parent company owning 25% of the combined entity to enhance profitability and innovation in the commercial vehicle sector.

- June 2025: Volvo Group and Daimler Truck launched Coretura, their joint venture focused on developing a standardized software platform for commercial vehicles, aiming to enable wireless updates for digital applications with products expected by 2030.

- May 2024: Iveco rebranded its used truck offering from OK Trucks to Iveco Certified Pre-Owned. The revamped program encompasses electric vehicles alongside traditional diesel and natural gas models. This marked the latest evolution of the Italian truck maker's second-hand initiative, which began in 1995 under the Used Plus brand. After introducing the OK Trucks brand in 2015, Iveco transitioned to the Certified Pre-Owned label, backed by a comprehensive 10-pillar promise.

Table of Contents for Used Semi-Truck Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Cost-effective ownership & affordability

- 4.2.2OEM production bottlenecks shift demand to used inventory

- 4.2.3Rapid e-commerce-driven freight growth

- 4.2.4Data-driven online marketplaces improving price transparency

- 4.2.5Battery-electric retrofitting kits extending fleet life

- 4.2.6ESG-linked financing incentives for life-cycle extension

- 4.3Market Restraints

- 4.3.1Rising regulatory barriers on high-emission legacy engines

- 4.3.2Persistent quality & reliability concerns

- 4.3.3Limited certified refurbishment infrastructure

- 4.3.4Export restrictions limiting cross-border secondary sales

- 4.4Porter’s Five Forces

- 4.4.1Threat of New Entrants

- 4.4.2Bargaining Power of Buyers

- 4.4.3Bargaining Power of Suppliers

- 4.4.4Threat of Substitutes

- 4.4.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1By Vehicle Type

- 5.1.1Light-Duty Truck

- 5.1.2Medium-Duty Truck

- 5.1.3Heavy-Duty Truck

- 5.2By Propulsion Type

- 5.2.1Internal Combustion Engine (ICE)

- 5.2.2Battery Electric

- 5.2.3Hybrid

- 5.3By Sales Channel

- 5.3.1Franchised Dealer

- 5.3.2Independent Dealer

- 5.3.3Customer-to-Customer (C2C)

- 5.3.4Online Auction Platform

- 5.4By Vehicle Age

- 5.4.10 to 3 Years

- 5.4.24 to 7 Years

- 5.4.38 to 15 Years

- 5.4.4More than 15 Years

- 5.5By End-use Industry

- 5.5.1Logistics & Freight

- 5.5.2Construction

- 5.5.3Mining & Quarrying

- 5.5.4Agriculture & Forestry

- 5.5.5Others (Municipal, Utilities)

- 5.6By Geography

- 5.6.1North America

- 5.6.1.1United States

- 5.6.1.2Canada

- 5.6.1.3Rest of North America

- 5.6.2South America

- 5.6.2.1Brazil

- 5.6.2.2Argentina

- 5.6.2.3Rest of South America

- 5.6.3Europe

- 5.6.3.1Germany

- 5.6.3.2United Kingdom

- 5.6.3.3France

- 5.6.3.4Italy

- 5.6.3.5Spain

- 5.6.3.6Russia

- 5.6.3.7Rest of Europe

- 5.6.4Asia-Pacific

- 5.6.4.1China

- 5.6.4.2India

- 5.6.4.3Japan

- 5.6.4.4South Korea

- 5.6.4.5Indonesia

- 5.6.4.6Vietnam

- 5.6.4.7Philippines

- 5.6.4.8Australia

- 5.6.4.9Rest of Asia-Pacific

- 5.6.5Middle East & Africa

- 5.6.5.1Saudi Arabia

- 5.6.5.2United Arab Emirates

- 5.6.5.3South Africa

- 5.6.5.4Egypt

- 5.6.5.5Turkey

- 5.6.5.6Rest of Middle East & Africa

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Strategic Moves

- 6.3Market Share Analysis

- 6.4Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1Daimler Truck AG

- 6.4.2AB Volvo

- 6.4.3Paccar Inc

- 6.4.4International Motors LLC (Navistar International)

- 6.4.5Scania AB

- 6.4.6Iveco Group

- 6.4.7Ritchie Bros. Auctioneers

- 6.4.8Ryder System Inc.

- 6.4.9Penske Corporation

- 6.4.10BigIron Auctions

7. Market Opportunities & Future Outlook

- 7.1Accelerated demand for certified low-emission retrofit programs

- 7.2AI-driven residual-value analytics platforms

- 7.3Subscription-based “truck-as-a-service” models for SMEs

- 7.4Cross-border digital escrow services to unlock MEA & S. America trade

- 7.5Emerging battery-second-life ecosystem for electric tractors

Global Used Semi-Truck Market Report Scope

A used semi-truck, often called a tractor or big rig, is a heavy-duty vehicle previously owned and primarily used for hauling freight. As the front part of tractor-trailers, these trucks are engineered to pull one or more trailers laden with goods. For owner-operators and small businesses aiming to expand their fleets, buying a used semi-truck presents a budget-friendly alternative to investing in a brand-new vehicle.

Used Semi-truck Market is segmented vehicle type, propulsion type, sales channel and geography. Based on the vehicle type, the market is segmented into light-duty truck, medium-duty truck, and heavy-duty truck. Based on the propulsion type, the market is segmented into ICE and Electric. Based on sales channel, the market is segmented into franchised dealer, independent dealer and Customer to Customer. Based on the geography, the market is segmented into the North America, Europe, Asia Pacific and Rest of the World. For each segment, market sizing and forecast have been done on the basis of value (USD).