Bicycle Suspension System Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

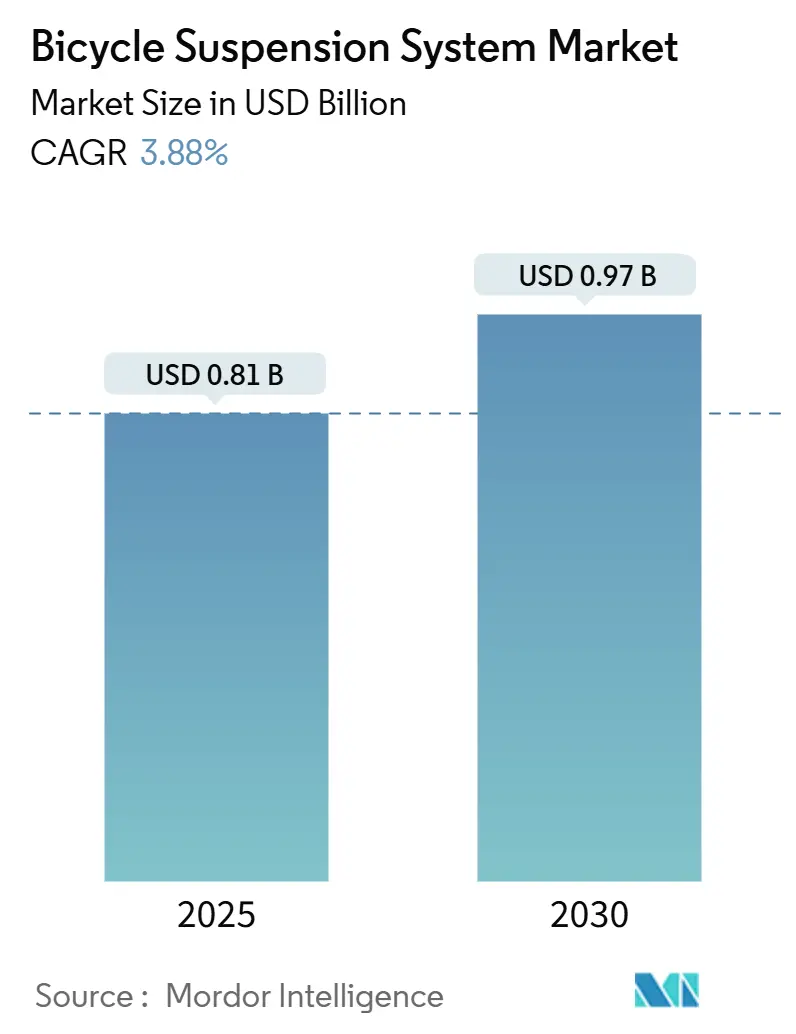

| Market Size (2025) | USD 0.81 Billion |

| Market Size (2030) | USD 0.97 Billion |

| Growth Rate (2025 - 2030) | 3.88% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bicycle Suspension System Market Analysis by Mordor Intelligence

The Bicycle Suspension System Market size is estimated at USD 0.81 billion in 2025, and is expected to reach USD 0.97 billion by 2030, at a CAGR of 3.88% during the forecast period (2025-2030). This trajectory indicates a maturing global landscape in which manufacturers focus less on sheer volume and more on technological differentiation that improves ride quality, boosts durability, and unlocks new use-case scenarios. Elevated aluminum prices, which have surged since the pandemic, have prompted producers to seek materials engineering breakthroughs that safeguard margins without increasing retail prices. At the same time, smart suspension integration reshapes user expectations through automated compression and rebound tuning. Geopolitical friction and shifting tariff structures add a second layer of complexity by redistributing sourcing footprints into Vietnam and Cambodia. Yet, sustained e-bike demand prevents inventory backlogs from stalling long-term expansion in the bicycle suspension system market.

Key Report Takeaways

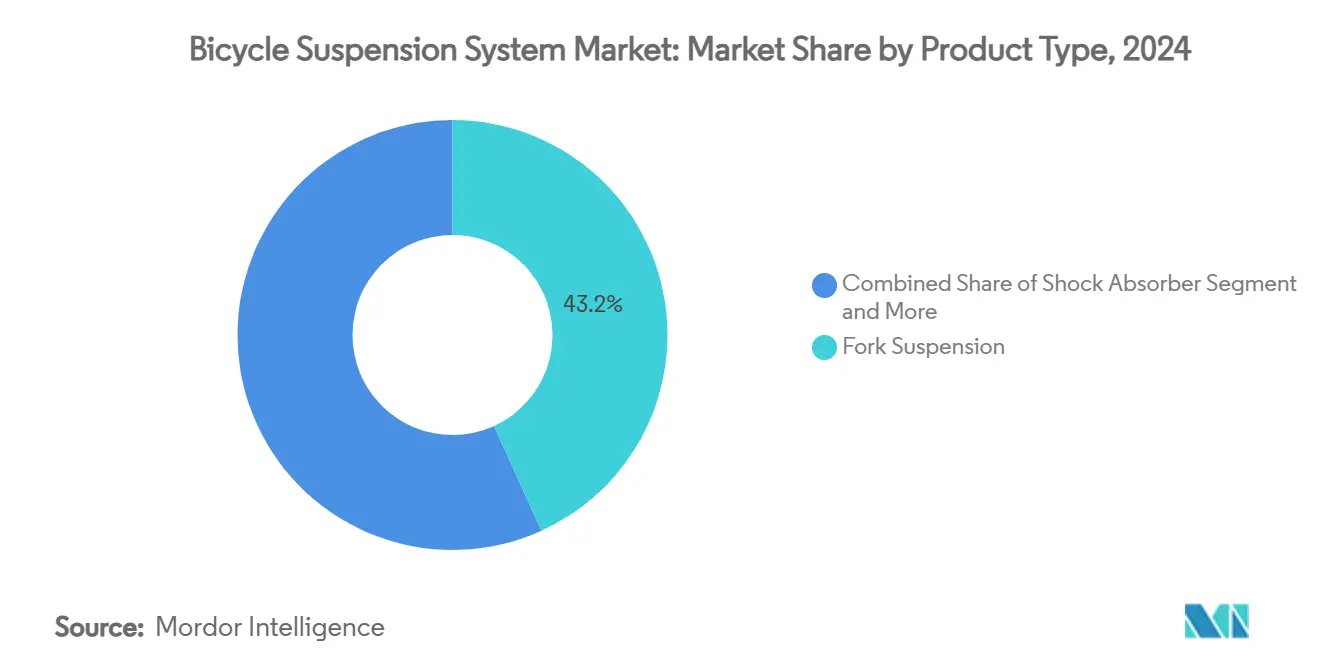

- By product type, fork suspension led with 43.18% revenue share in 2024; full suspension is forecast to expand at a 3.92% CAGR through 2030.

- By bicycle type, mountain bikes accounted for 38.15% of the bicycle suspension system market share in 2024, while electric bikes recorded the fastest projected 3.95% CAGR through 2030.

- By technology, air suspension commanded 54.11% share of the bicycle suspension system market size in 2024, and remote-controlled active systems are advancing at a 3.97% CAGR through 2030.

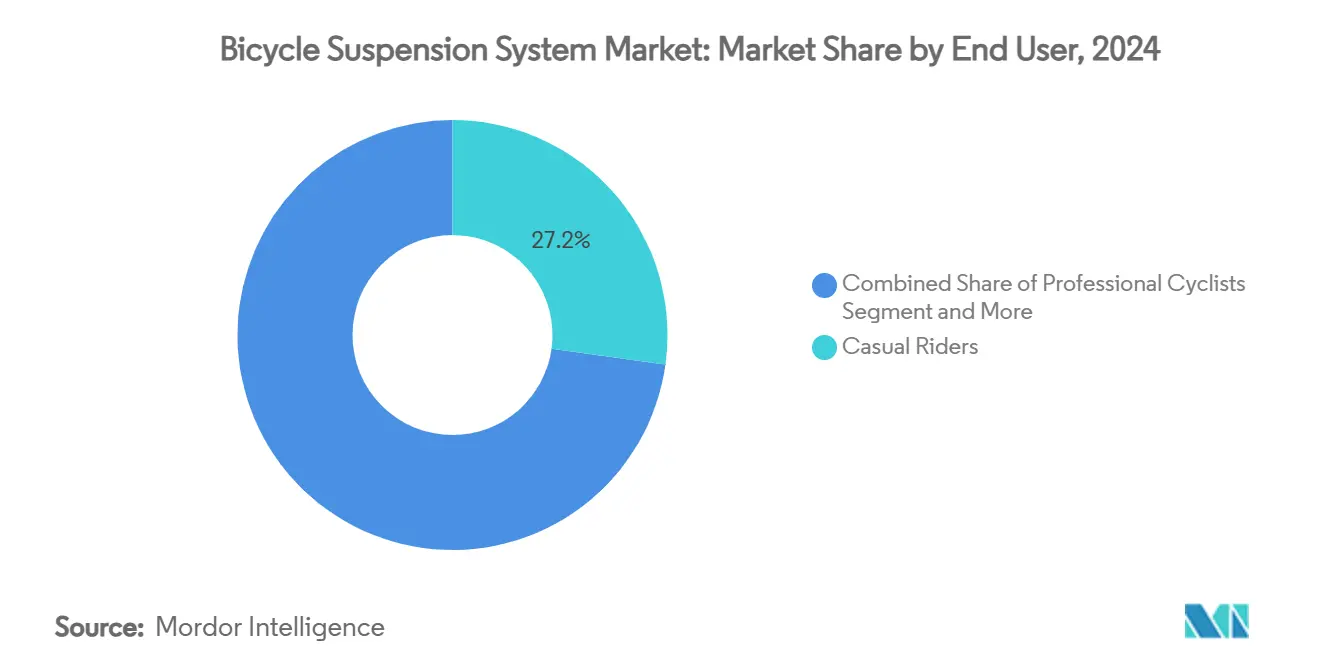

- By end-user, casual riders represented a 27.19% share in 2024, and rental services are projected to grow at a 4.01% CAGR between 2025 and 2030.

- By distribution channel, specialty bike shops held a 31.26% share in 2024; OEM direct sales show the highest 4.04% CAGR through 2030.

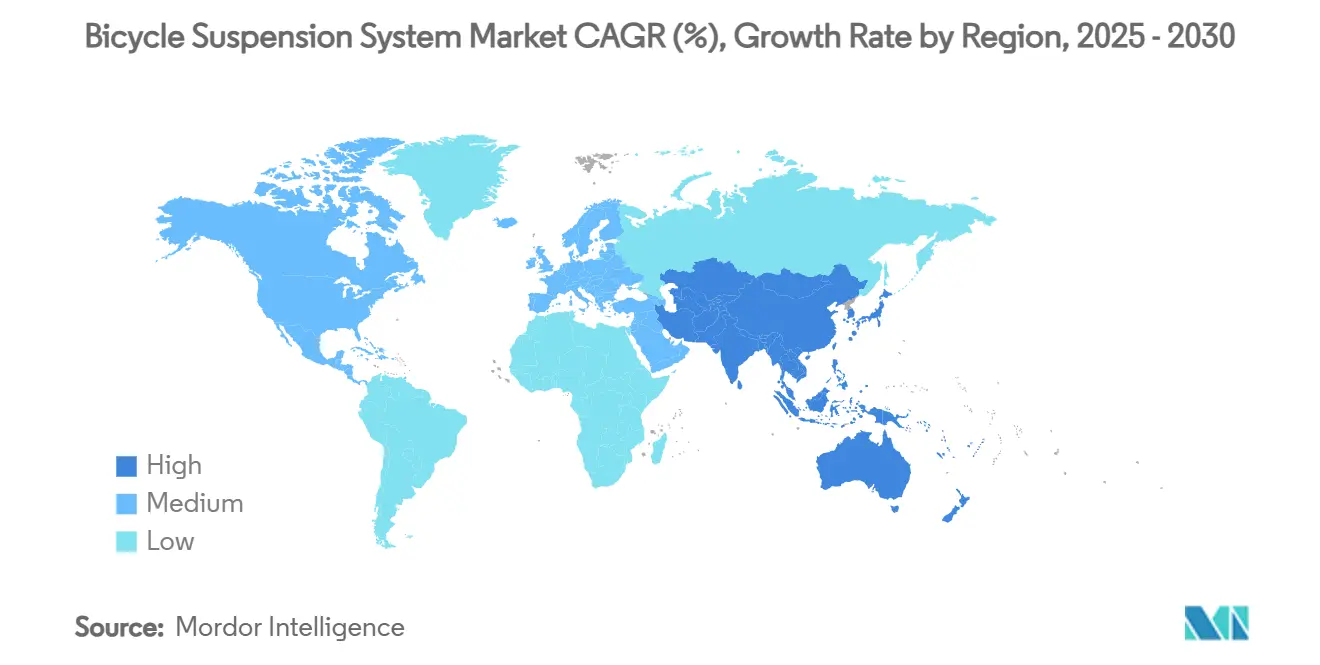

- By geography, Asia-Pacific held 36.15% of the bicycle suspension system market share in 2024, the region is also forecasted to expand at the fastest 4.07% CAGR through 2030.

Global Bicycle Suspension System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Bike Adoption Wave | +1.2% | Global, with North America and Europe leading | Medium term (2-4 years) |

| OEM Integration of Smart/Active Suspension | +0.9% | Global, with early adoption in premium segments | Medium term (2-4 years) |

| Rapid MTB & Gravel Bike Volume Upswing | +0.8% | North America and Europe core, spill-over to Asia Pacific | Short term (≤ 2 years) |

| Premiumisation in Urban Commuter Bikes | +0.6% | Global urban centers, concentrated in developed markets | Long term (≥ 4 years) |

| Growing Trail Diversity | +0.5% | North America and Europe, emerging in Asia Pacific | Long term (≥ 4 years) |

| Micro-mobility Fleet Upgrades | +0.4% | Urban centers in North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Bike Adoption Wave

Electrification alters every element of suspension design because heavier chassis, quicker acceleration, and higher sustained speeds increase peak loads on forks and shocks. Fox Factory’s Live Valve now plugs directly into an e-bike’s battery to power millisecond-level damping shifts that maximise pedalling efficiency on climbs and enhance control on steep descents.[1]Fox Factory Holding Corp., “Live Valve White Paper,” foxfactory.com City programmes mirror this trend: Fort Worth introduced 340 suspension-equipped e-bikes into its 400-unit Trinity Metro fleet, prioritising comfort for users traversing cracked pavement, curbs, and rail crossings.

OEM Integration of Smart/Active Suspension

Digitally controlled suspension redefines the bicycle suspension system market by allowing OEMs hard-wire performance advantages into complete bikes. SRAM collects real-time rider data across its AXS ecosystem and tailors damping curves to rider weight, cadence, and terrain morphology—outcomes that standalone aftermarket forks cannot readily replicate. Shimano’s recent patent for machine-learning-driven damping shows how industry giants are committing R&D dollars toward software-defined ride quality. With wireless Live Valve Neo, Fox removes cables, simplifies assembly, and cuts setup time, allowing factories in Vietnam and Cambodia to tackle high-mix, low-volume premium models more efficiently.

Rapid MTB & Gravel Bike Volume Upswing

Mountain bike (MTB) demand is rising as riders seek bikes that climb efficiently yet absorb impacts on increasingly technical trails. Gravel bikes also shift from rigid layouts to shorter-travel suspension solutions such as Cane Creek’s Invert fork series. This shows that comfort and control matter on mixed-surface routes previously served by rigid frames. RockShox migrated its Flight Attendant algorithm to cross-country racing, recording average speed gain by continuously adapting damping to course conditions. Parallel investment in bike parks across North America widens terrain options and pushes consumers toward tunable forks that maintain cadence on climbs yet remain stiff under braking on fast descents.

Premiumisation in Urban Commuter Bikes

Urban riders shift spending away from automobiles toward higher-quality bicycles that can handle potholes, speed bumps, and cobblestone streets. Specialized’s Diverge STR integrates seat-tube suspension that isolates the rider from surface chatter without penalising power transfer. Shimano’s 2025 Q’Auto automatic shifting couples with micro-suspension to provide commuters with a smoother ride and lower maintenance routines. As bike-sharing networks lengthen average trip distances, specification upgrades migrate from MTB lines to everyday commuters, cementing the premium fork as a must-have in many city models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Unit Cost vs. Rigid Forks | -0.70% | Global, more pronounced in price-sensitive markets | Medium term (2-4 years) |

| Magnesium & Carbon Shortages | -0.50% | Global, with acute impact on premium segments | Short term (≤ 2 years) |

| Lightweight Range-Anxiety | -0.30% | Europe and North America, premium e-road segment | Medium term (2-4 years) |

| After-sales Service Complexity | -0.20% | Global, concentrated in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Unit Cost vs. Rigid Forks

Compared with rigid forks, budget suspension forks can cost three to four times more, discouraging adoption in emerging markets where entry-level commuter bikes dominate. Premium products, such as Manitou’s Dorado Pro, limit uptake to enthusiast circles. Suspended forks also carry higher maintenance costs because seals, bushings, and oil need periodic replacement. When aluminium prices rose significantly between 2020 and 2024, OEMs faced thin margins and deferred spec upgrades on value-oriented models. Prospective a massive tariffs on Chinese bicycle components further inflate costs in the United States, threatening to keep advanced damping systems out of lower-priced builds.

Magnesium & Carbon Shortages

China supplies more than 85% of the world’s magnesium; production curtailments for environmental reasons have hamstrung aluminium alloy output critical to fork crown and lower-leg parts. Simultaneously, aerospace and wind turbine demand siphon carbon fibre away from cycling brands, stretching lead times and raising prices. Oak Ridge National Laboratory reports prototype carbon fibres with 50% higher tensile strength, yet commercial deployment lags by several years. These shortages push manufacturers toward alternative materials such as thermoplastic composites. Still, re-engineered supply chains curb near-term volume and lengthen product launch cycles, imposing a drag on the bicycle suspension system market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fork Suspension Leads Innovation

Fork suspension systems generated 43.18% of 2024 revenue, underscoring their status as the default upgrade path for riders across every discipline in the bicycle suspension system market. High-volume economies of scale keep retail prices accessible, and incremental design tweaks—such as lighter magnesium lowers and enlarged negative air chambers—add performance without significant cost hikes. Full-suspension frames are gaining a 3.92% CAGR as new mountain bike geometries prioritise rear-wheel traction and all-day comfort. Meanwhile, hard-tail aficionados still value pedal stiffness for cross-country events, making the category resilient despite slower growth.

New inverted layouts demonstrate how pro-level innovation flows into mainstream forks. Fox’s Podium Inverted Fork debut maximises stiffness-to-weight ratios, while Manitou’s R8 Pro leverages travel-adjust chips so one SKU can cover 80-120 mm use-cases, cutting dealer inventory risk. DVO targets custom-tuning enthusiasts by selling retrofit shim stacks and damper upgrades that end users can install at home. These tactical product choices encourage repeat purchases and extend the life-cycle of each chassis, enlarging aftermarket revenue within the bicycle suspension system market.

By Bicycle Type: E-Bikes Drive Growth

Mountain bikes held a 38.15% share in 2024, but e-bikes are advancing the fastest at a 3.95% CAGR, reshaping design criteria across the bicycle suspension system market size. Additional mass and higher top speeds oblige OEMs to spec thicker stanchions, beefier thru-axles, and larger volume air springs to handle braking loads. Cargo-oriented utility bikes adopt suspension forks once considered overkill for city commuting, proving that performance components can unlock new urban business models.

Fox’s Live Valve interfaces directly with Bosch or Shimano motor batteries, permitting microsecond lockout decisions that save energy on climbs yet cushion potholes on the flats. Small-batch maker Wren Sports supplies 110 mm-travel forks for e-cargo bikes that carry up to 80 kg payloads without bottoming out at low tyre pressures. Regulatory changes in Europe, where speed-pedelecs gain dedicated lanes, further accelerate demand for stable, adaptive suspensions that predict heavier frames under high-speed cornering. As a result, the bicycle suspension system market registers outsized unit value growth despite moderate unit volumes.

By Technology: Air Suspension Dominance

Air spring designs retained 54.11% market share in 2024 due to weight savings and home-mechanic-friendly tuning. Riders can adjust sag and progressiveness within minutes using a shock pump rather than swapping steel coils. Still, remote-controlled and active systems seize mind-share as they grow at a 3.97% CAGR, promising the convenience of always-correct damping without rider intervention. SRAM’s Flight Attendant illustrates this shift by producing more than 1,300 automated valving decisions in a typical 90-minute trail session, boosting cadence efficiency by minimising bobbing.

Coil shocks remain the choice for downhill racers who need consistent heat management over four-minute runs. Still, incremental innovations like multi-rate springs soften the weight penalty for all-mountain fans. CounterShox introduces tuned mass dampers that attach to outside fork legs and absorb chassis harmonics, providing an upgrade path that sidesteps complete fork replacement. By marrying air with electronic valves, Fox’s Live Valve Neo merges the lightness advantage of air springs with automated lockout control, pushing the bicycle suspension system market toward a software-defined future.

By End-User: Rental Services Accelerate

Casual cyclists represented 27.19% of global demand in 2024 and still dominate unit volumes because affordable hard-tail bikes suit recreational usage. Rental and sharing fleets, however, show the fastest 4.01% CAGR, as municipal programmes seek durable forks that reduce maintenance downtime and enhance safety for novice riders. Lyft Urban Solutions specifies sealed damper cartridges rated for 10,000 km before overhaul, a ten-fold increase over typical consumer forks, curbing operational expenditure.

Professional racers continue to validate next-gen technologies, shortening the innovation cycle for amateurs. World Cup downhill results prove whether new valving designs live up to marketing claims, and subsequent consumer trickle-down builds credibility around premium pricing. As fleet managers standardise on mid-range suspension to widen rider eligibility, the bicycle suspension system market attracts higher average selling prices. It incentivises manufacturers to create semi-custom “fleet spec” SKUs.

By Distribution Channel: OEM Direct Gains

Specialty bike shops retained a 31.26% share in 2024, but direct sales from OEM web portals climbed at a 4.04% CAGR. Direct-to-consumer models let brands secure full retail margins and gather buyer data for future digital services such as suspension-tuning apps. Inventory overhangs and diminished floor-space productivity have led nearly half of the United States shops to drop some of the legacy brands they once prominently featured.

Giant partners with Dick’s Sporting Goods’ specialty outlets to keep touch-and-feel opportunities alive while centralising inventory upstream in regional warehouses for click-and-collect. Kona’s rollout of consumer-direct shipment met retailer pushback, signalling an industry still in flux as it rebalances between experiential stores and e-commerce. As OEMs automate suspension calibration via smartphone apps at first ride, they reduce post-purchase service tasks historically performed by dealers, further shifting revenue toward factory channels and sustaining growth in the bicycle suspension system market.

Geography Analysis

Asia-Pacific generated 36.15% of global revenue in 2024 and is tracking a 4.07% CAGR to 2030, supported by China’s robust export surge from January to October 2024 and Vietnam’s zero-duty access to the EU for bikes with almost half of local content.[2]Ministry of Commerce of the People’s Republic of China, “Bicycle Export Statistics 2024,” mofcom.gov.cn Cambodian plants enjoy duty-free access for e-bikes, giving regional OEMs strategic flexibility to hedge against tariffs. Magnesium constraints in China add cost pressure to higher-end air-spring and carbon-crown forks. However, supply-chain clustering around Guangdong and Zhejiang still confers scale advantages that are unmatched elsewhere in the bicycle suspension system market.

Europe currently wrestles with what trade media call the “largest crisis ever in the bike industry". Yet more than a billion EUR of fresh production capacity is underway, aimed at premium suspension-equipped bikes that will ship as inventories normalise by 2025. Bianchi’s on-shore carbon-fibre line in Italy cuts shipping time by four weeks, while German contract manufacturer Bike-Valley builds automated wheel-assembly cells to absorb fluctuating order books.

North America shows dichotomous trends: trade war tariffs inflate input costs. Yet, Fox Factory’s Specialty Sports Group booked 6.5% net sales growth to USD 355 million in Q1 2025, driven by suspension demand for gravel and e-mountain bikes. The expansion of bike parks from Utah to Quebec introduces new riders to long-travel forks, reinforcing premium aftermarket sales. Middle East and Africa markets are smaller but adopt suspension quickly, where infrastructure investments create dedicated cycling corridors in Abu Dhabi and Cape Town, positioning the bicycle suspension system market to capture first-mover gains when disposable incomes rise.

Competitive Landscape

The bicycle suspension system market features medium fragmentation. Fox Factory and SRAM command a significant share, yet challengers such as DVO Suspension and Manitou deploy agile engineering teams and direct-to-consumer engagement to erode legacy dealership advantages. Brembo’s January 2025 acquisition of Öhlins Racing underlines a consolidation wave that blurs the line between braking and suspension technologies, allowing cross-selling in high-performance segments.

Innovation cycles now revolve around firmware as much as hardware. SRAM pushes over-the-air updates that refine Flight Attendant algorithms, while Fox’s Live Valve Neo works on a separate wireless protocol to avoid cross-talk with drivetrain signals. Shimano’s machine-learning patent grants the group the option to bundle drivetrain, brake, and suspension components under one software umbrella, heightening customer lock-in. DVO relies on open-dock valving kits that let riders self-tune, positioning itself as the enthusiast’s choice for personalisation.

Material supply insecurity acts as a competitive differentiator. Vertically integrated brands that handle in-house forging, anodising, and final assembly mitigate magnesium and carbon fibre shortages better than pure assemblers. Makers with global factory footprints spread risk: Fox produces key castings in Taiwan, shock internals in the United States, and final assembly in Thailand, allowing demand spikes in one region to be buffered by capacity elsewhere. As a result, software prowess, materials access, and channel control now overshadow pure unit volume in deciding leadership within the bicycle suspension system market.

Bicycle Suspension System Industry Leaders

SR Suntour

DT Swiss

Fox Factory Holding Corp.

SRAM LLC.

Shimano, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Fox Factory launched the Podium Inverted Fork at Eurobike 2025, touting higher torsional rigidity and lighter unsprung mass.

- January 2025: Brembo completed its acquisition of Öhlins Racing, pairing braking expertise with suspension know-how in performance bicycle applications.

- July 2024: Manitou unveiled lightweight cross-country fork and shock systems aimed at competitive XC race teams.

- June 2024: DVO Suspension introduced the Prime Shock Damper featuring tool-free compression adjustments and enhanced air-bladder reliability.

Global Bicycle Suspension System Market Report Scope

| Fork Suspension |

| Shock Absorber |

| Full Suspension Systems |

| Hard-tail Suspension Systems |

| Mountain Bikes |

| Road Bikes |

| BMX Bikes |

| Hybrid Bikes |

| Cruiser Bikes |

| Electric Bikes (E-Bikes) |

| Air Suspension |

| Coil Suspension |

| Progressive Suspension |

| Blind-Mount Systems |

| Remote-Controlled / Active Systems |

| Professional Cyclists |

| Competitive Teams |

| Amateur Cyclists |

| Casual Riders |

| Rental & Sharing Services |

| OEM Direct |

| Online Retail |

| Specialty Bike Shops |

| Department / Sporting Goods Stores |

| Wholesale Distributors |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| UAE | |

| Turkey | |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Fork Suspension | |

| Shock Absorber | ||

| Full Suspension Systems | ||

| Hard-tail Suspension Systems | ||

| By Bicycle Type | Mountain Bikes | |

| Road Bikes | ||

| BMX Bikes | ||

| Hybrid Bikes | ||

| Cruiser Bikes | ||

| Electric Bikes (E-Bikes) | ||

| By Technology | Air Suspension | |

| Coil Suspension | ||

| Progressive Suspension | ||

| Blind-Mount Systems | ||

| Remote-Controlled / Active Systems | ||

| By End-User | Professional Cyclists | |

| Competitive Teams | ||

| Amateur Cyclists | ||

| Casual Riders | ||

| Rental & Sharing Services | ||

| By Distribution Channel | OEM Direct | |

| Online Retail | ||

| Specialty Bike Shops | ||

| Department / Sporting Goods Stores | ||

| Wholesale Distributors | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| UAE | ||

| Turkey | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the bicycle suspension system market?

The bicycle suspension system market size is USD 0.81 billion in 2025 and is forecast to reach USD 0.98 billion by 2030.

Which product category dominates revenue?

Fork suspension systems lead with 43.18% market share in 2024 due to their universal application across bike types.

Which segment is growing fastest among bicycle type?

Electric bikes grow fastest at a 3.95% CAGR through 2030 because heavier frames and higher speeds demand advanced damping.

Why are OEM direct sales increasing?

OEM direct sales are projected to expand at a 4.04% CAGR as brands capture retail margins and offer smartphone-based suspension setup tools that lessen dealer involvement.

How do raw-material shortages affect pricing?

Magnesium and carbon fibre shortages raise component costs and can delay product launches, putting near-term downward pressure on volume growth.

Page last updated on: