Vietnam Bike-Sharing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

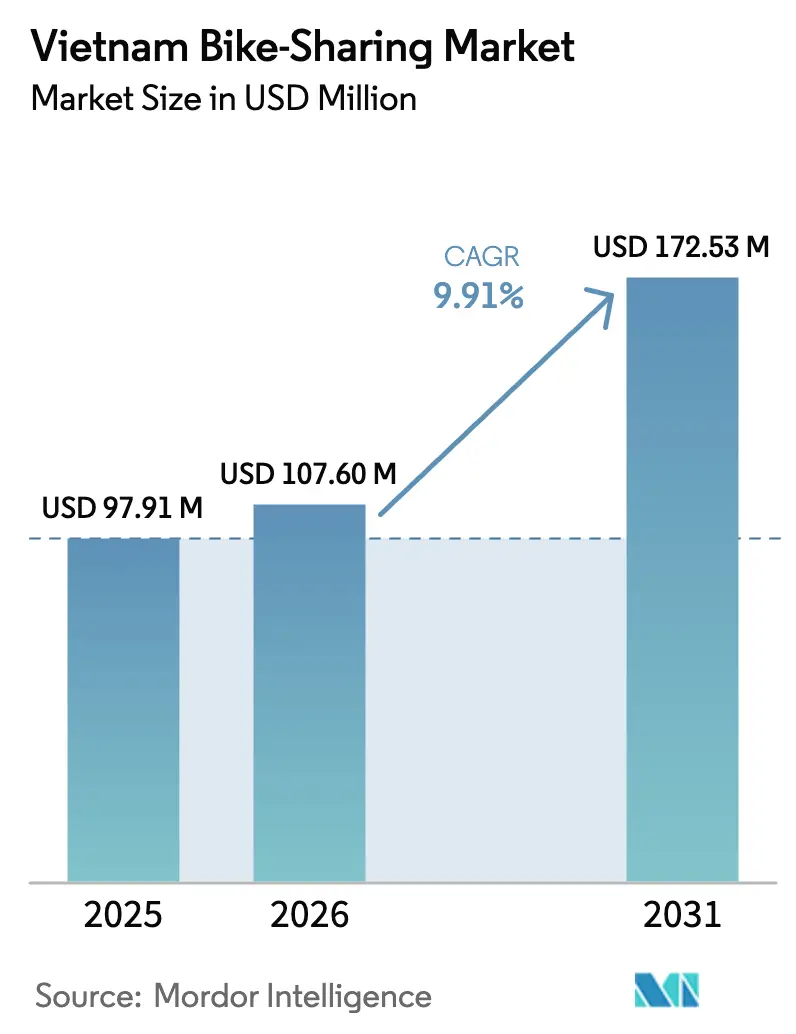

| Base Year Market Size (2025) | USD 97.91 Million |

| Market Size (2026) | USD 107.6 Million |

| Market Size (2031) | USD 172.53 Million |

| Growth Rate (2026 - 2031) | 9.91% CAGR |

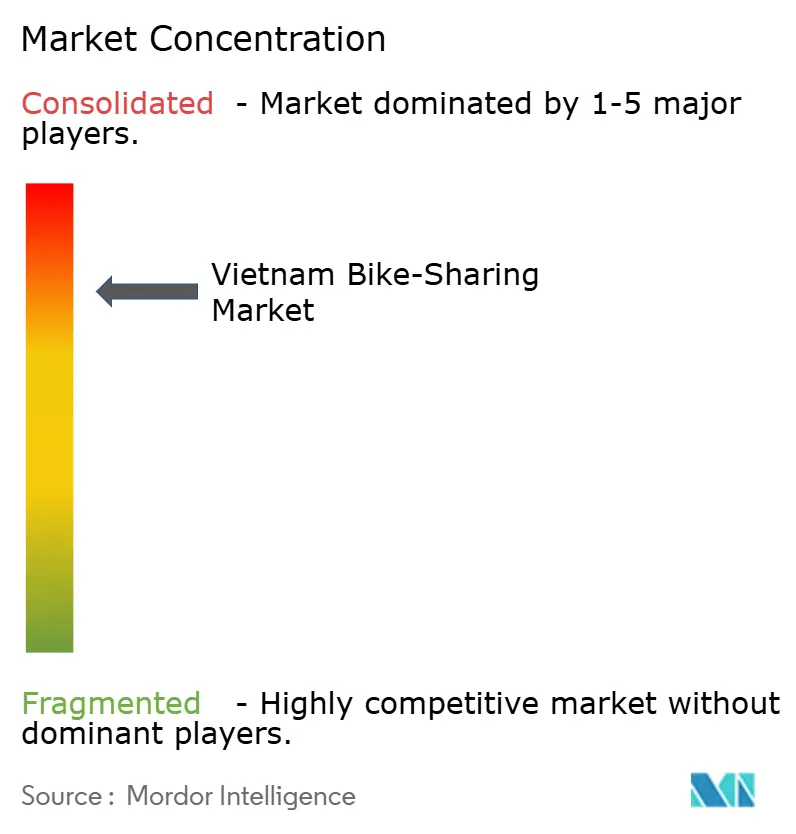

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vietnam Bike-Sharing Market Analysis by Mordor Intelligence

The Vietnam bike sharing market size was valued at USD 97.91 million in 2025 and estimated to grow from USD 107.6 million in 2026 to reach USD 172.53 million by 2031, at a CAGR of 9.91% during the forecast period (2026-2031). Rapid urban migration, a 98% tourism recovery rate in 2024, and firm government commitments to Net-Zero 2050 collectively anchor demand for easy-to-access micro-mobility[1]VnExpress, “Vietnam Achieves 98% Tourism Recovery in 2024,” vnexpress.net . The mainstream move toward electric two-wheelers, expanding public docking infrastructure in Hanoi and Ho Chi Minh City, and rising corporate ESG ride-credit programs further propel adoption. Operators concentrate on app-based services that sync with cashless ticketing for buses and upcoming metro lines, while tourism hubs such as Huế and Hội An showcase strong seasonal peaks. Competitive intensity remains moderate, with top players vying to pair e-bike fleets with charging and battery-swap ecosystems that improve uptime and user convenience[2]“User Satisfaction Dashboard 2025,” TriNam Group, tngo.vn.

Key Report Takeaways

- By bike type, traditional bicycles held 57.38% of the Vietnam bike sharing market share in 2025, whereas e-bikes are projected to grow at a 14.12% CAGR through 2031.

- By sharing system, dockless models led with 59.42% revenue share in 2025 and are expanding at a 12.63% CAGR to 2031.

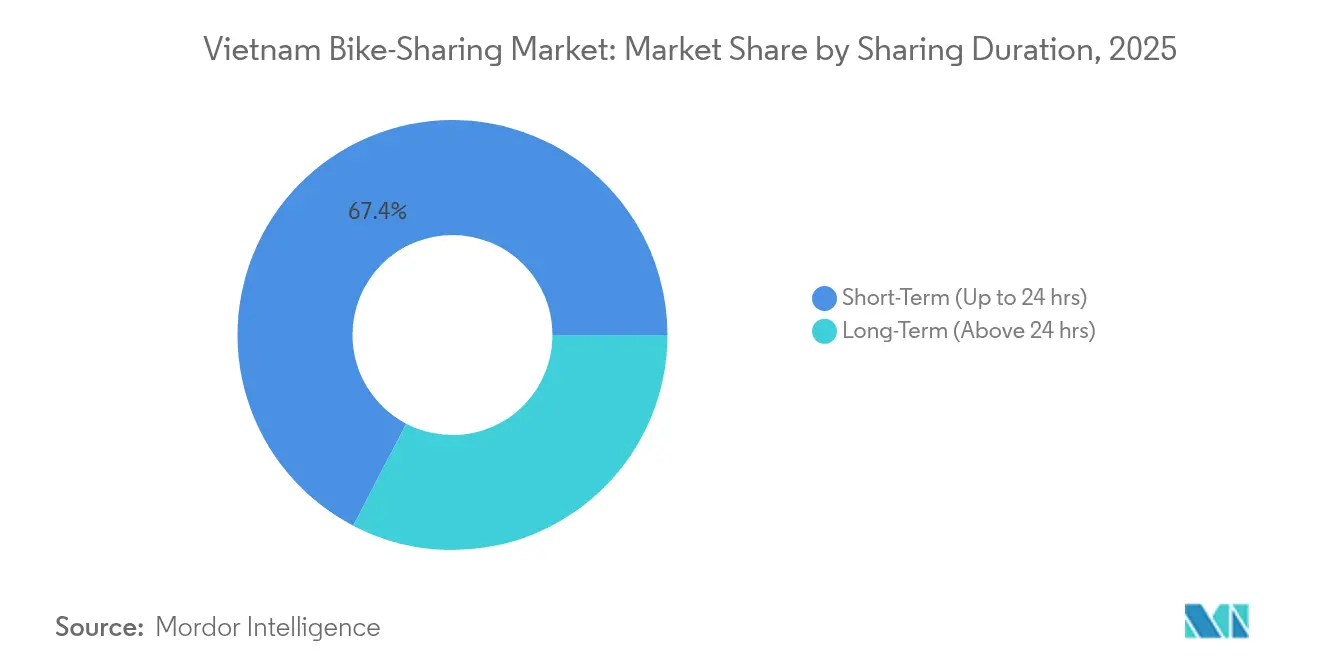

- By sharing duration, short-term rentals accounted for 67.35% share of the Vietnam bike sharing market size in 2025 and will widen at an 11.05% CAGR.

- By application, regular commuting captured 62.61% share in 2025, but tourism-focused services are rising fastest at a 14.31% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Vietnam Bike-Sharing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mainstream Shift to Eco-Friendly Mobility | +2.8% | Global, strongest in Hanoi & HCMC | Medium term (2-4 years) |

| Government Low-Carbon Transport Targets (Net-Zero 2050) | +2.1% | National, with early gains in major cities | Long term (≥ 4 years) |

| Rapid Rollout of Public Docking Infrastructure in Hanoi and HCMC | +1.9% | Hanoi & HCMC core, spillover to secondary cities | Short term (≤ 2 years) |

| Tourism-Led Demand Spikes in Heritage Cities (Huế, Hội an) | +1.4% | Central Vietnam heritage corridor | Medium term (2-4 years) |

| Integration of Bike-Sharing with Metro Smart-Ticketing | +1.2% | Hanoi & HCMC metro catchment areas | Short term (≤ 2 years) |

| Corporate ESG Ride-Credit Programs for Employees | +0.8% | Major urban centers with multinational presence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mainstream Shift to Eco-Friendly Mobility

Electric two-wheelers move from niche to mainstream as Ho Chi Minh City rolls out a plan to convert 400,000 gasoline motorbikes used by delivery riders to electric alternatives. Support programs backed by Vingroup and university-led R&D reduce upfront costs and speed up battery-swap station deployment. Government targets call for 25% of two-wheelers to be electric by 2030, fostering ample spillover infrastructure for shared fleets. Private innovators install interoperable battery stations that shrink downtime and enlarge service radius, enabling dockless operators to reach peri-urban districts. Early adopters that combine dynamic pricing with carbon-credit rewards appreciate a rise in repeat rides, signaling that environmental preference is translating into recurring demand. The shift also improves air-quality indices in congested corridors, consolidating public sentiment around greener mobility choices.

Government Low-Carbon Transport Targets (Net-Zero 2050)

The Action Programme on Green Energy Transformation sets binding milestones: 100% electric public buses by 2025, 50% green-energy vehicles by 2030, and a full fossil-fuel phase-out by 2040. Hanoi’s Plan 149/KH-UBND dovetails with national goals, earmarking downtown lanes for zero-emission vehicles and subsidizing smart docks at metro exits. United Nations Development Programme workshops detail standardization of docking hardware and data-sharing protocols to ease multimodal transfers. Operators that align with these guidelines access low-interest loans and waived import duties on high-efficiency batteries. Such incentives reduce total cost of ownership and accelerate fleet renewal cycles. Over the long term, capped inner-city car quotas are expected to divert incremental commuters to bike sharing, sustaining a double-digit growth trajectory for the Vietnam bike sharing market.

Rapid Rollout of Public Docking Infrastructure in Hanoi and HCMC

TriNam Group’s station-based pilot around Hoan Kiem Lake added 1,000 bikes—half electric—and achieved ride-per-bike ratios high enough to justify phase-two expansion. Ho Chi Minh City’s initial 43-station grid, launched in 2021, proved scalable, prompting municipal offices to release additional curb-side allocations in Districts 1 and 3. Proximity to bus routes and metro Line 1 improves first-mile/last-mile connectivity, raising ticket validations per passenger. Funding partnerships with multilateral lenders offset capital costs for internet-of-things locks and real-time occupancy dashboards. Public visibility of these hubs normalizes shared cycling as a daily habit, shrinking perceived effort barriers among non-cyclists. The build-out also strengthens brand presence of leading operators, reinforcing user trust in asset availability and system uptime.

Tourism-Led Demand Spikes in Heritage Cities (Huế, Hội An)

Heritage sites see a steep jump in rental volume following a 29.6% year-over-year surge in international arrivals during Q1 2025. Huế’s certification under the national LOTUS green-building scheme underscores policy backing for low-impact mobility in protected zones. Local tourism boards subsidize app-guided cycling tours that bundle tickets to monuments and museums, boosting average revenue per ride. German-funded pilot projects in Hội An provide free safety gear to visitors, lowering liability concerns and setting operating benchmarks. Seasonal climbs around cultural festivals accentuate the need for flexible fleet rebalancing, encouraging operators to integrate predictive demand algorithms. Cross-selling with hotel loyalty platforms further entrenches bike sharing within tourist itineraries, adding a durable, high-yield layer to operator revenue mixes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Incidence of Bike Vandalism and Theft | -1.8% | Urban centers, particularly HCMC & Hanoi | Short term (≤ 2 years) |

| Limited Li-Ion Battery Recycling Logistics | -1.2% | National, concentrated in major cities | Medium term (2-4 years) |

| Seasonal Monsoon Affecting Utilisation Rates | -0.9% | National, strongest impact in central regions | Short term (≤ 2 years) |

| Zoning Rules Limiting Curb-Side Parking Space | -0.7% | HCMC & Hanoi central districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Incidence of Bike Vandalism and Theft

Unregulated curb-side parking leads to asset losses and higher maintenance outlays, especially in districts with dense night-time economies. Enforcement gaps allow informal parking attendants to overcharge, creating friction that deters casual users. Earlier university pilots recorded rapid fleet deterioration when smart locks malfunctioned under heavy rain, illustrating the need for robust hardware. Leading operators now embed tamper-proof GPS and geofenced parking zones in their apps, which has elevated recovery rates. Collaboration with municipal CCTV networks improves offender traceability, yet the capital burden for advanced anti-theft systems remains high. The near-term challenge compels operators to balance open-access convenience with tighter station control until regulatory clarity improves.

Limited Li-ion Battery Recycling Logistics

Vietnamese e-mobility confronts a nascent recycling chain, with only one domestic facility able to process spent electric-vehicle batteries at scale. Rising e-bike numbers elevate future waste volumes, placing pressure on operators to arrange reverse logistics ahead of statutory deadlines. Cross-border shipping of used cells raises compliance costs and emissions, undermining green-transport branding. Joint ventures with global recyclers are progressing, but nationwide coverage will take several years. Meanwhile, operators must factor battery-end fees into ride pricing, which can erode price sensitivity in lower-income user groups. The shortfall highlights the strategic value of long-life battery chemistries and modular pack designs that simplify refurbishment cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bike Type: E-Bikes Accelerate Premium Uptake

Traditional bicycles, reliable and inexpensive, commanded 57.38% of 2025 revenue, an anchor for cost-conscious riders in crowded urban lanes. Their low operating cost suits short-haul errands, but limited hill-climbing ability and sweat concerns cap appeal among office commuters. E-bikes are rewriting this equation. The segment grows at a brisk 14.12% CAGR, powered by manufacturer subsidies on battery packs and frequent firmware updates that extend range. VinFast delivered 44,904 e-two-wheelers in Q1 2025 alone, creating familiarity that spills over into shared-fleet demand. The Vietnam bike sharing market size for e-bikes is projected to increase its revenue contribution steadily as battery swap hubs multiply across 63 provinces. Subsidy programs offering registration-fee waivers quicken fleet turnover, making e-bikes the chief growth vector despite their higher ticket prices.

Operators differentiate through motor wattage and torque, tailoring bikes for hilly heritage routes or flat inner-city grids. App interfaces now display real-time battery percentage, easing range anxiety and nudging riders to end trips near swap cabinets. Sponsorship deals with electronics brands cover part of battery lease costs, lowering payback periods. Insurance products bundled into ride fees shield operators from high-voltage component failures, raising trust in the emerging premium tier. By 2030, service analytics anticipate parity in trip counts between electric and manual fleets, a pivotal milestone that could reorient procurement toward electric-heavy portfolios. Within the broader Vietnam bike sharing market, e-bike success underscores how hardware evolution feeds directly into recurring revenue uplift.

By Sharing System: Dockless Services Dominate Urban Choice

Dockless architecture, capturing 59.42% share in 2025, epitomizes the country’s mobile-first culture. Quick QR code unlocks and flexible drop-offs shorten travel chains, winning over time-pressed commuters. With a 12.63% CAGR, the segment benefits from improved GPS accuracy and stricter geofence penalties that curb clutter. Hanoi’s pilot showed daily turnover of 7–8 rides per bike, enough to recover capex within 18 months. In districts where footpath width limits dock installations, dockless fleets broaden coverage without civil-works delays. The Vietnam bike sharing market size linked to these free-floating bikes expands in tandem with real-time curb-side parking maps rolled out via city transport portals.

Station-centric models persist near metro hubs, offering predictability that tourists value. Hybrid formulas blend both: users dock for free in busy nodes or pay minor surcharges for curb-side returns elsewhere. Municipal data trusts grant top operators privileged access to traffic flows, allowing proactive repositioning ahead of peak surges. The format also encourages cross-border replication; Vietnamese firms exporting know-how to Laos deploy dockless as default to bypass nascent infrastructure constraints. Freed from fixed bay limits, operators can unlock latent suburban demand, carving fresh revenue lanes inside the Vietnam bike sharing market.

By Sharing Duration: Short-Term Rentals Lead Usage Patterns

Short-duration hires up to 24 hours represented 67.35% of revenue in 2025 and grew at an 11.05% CAGR through 2031. Pricing menus that include the first 15 minutes free coax modal shifts from motorcycles on congested stretches. Micro-rentals match last-mile gaps between metro exits and office blocks, augmenting public-transit appeal. Riders appreciate app prompts that recommend optimal routes avoiding heavy traffic. Dynamic surge factors are lower than in ride-hailing, improving price certainty for office workers on strict budgets. The Vietnam bike sharing market size attributed to short-term use remains the backbone of operator liquidity, as high turnover limits idle depreciation.

Longer rentals find traction among tourists in heritage corridors who prefer day passes packaged with attraction bundles. Weekend family outings in waterfront cities such as Da Nang also lift multi-hour bookings that yield higher basket values. Operators employ machine-learning forecasts to allocate sturdier bikes with baskets to leisure zones, while performance-oriented models populate business districts. Seasonal monsoon dips prompt temporary discounts to sustain baseline usage. The fine-grained mix of durations empowers operators to diversify revenue per asset without diluting brand consistency across the Vietnam bike sharing market.

By Application: Tourism Emerges as Fastest-Growing Vertical

Regular commuting and recreation captured 62.61% of 2025 revenue, reflecting established integration with daily activity chains. Employee ride-credits bundled into payroll platforms promote weekday peaks, while weekend recreation fills off-peak hours. Tourism, although smaller in nominal terms, exhibits a 14.31% CAGR—the swiftest among all categories—as inbound arrivals rebound to pre-pandemic levels. Heritage cities partner with operators to create themed routes, distributing footfall away from fragile monuments. The Vietnam bike sharing market share linked to tourism is expected to widen as AI-powered itinerary planners inside mobility apps upsell culinary or cultural experiences timed with ride paths.

Corporate hospitality programs extend free ride minutes to convention delegates, boosting mid-week volumes. Operators deploy multilingual app interfaces that handle foreign cards, capturing an audience still underserved by cash-centric public buses. Ride data guides city planners when expanding pedestrian zones, reinforcing a positive feedback loop between tourism demand and cycling infrastructure investment. In the Vietnam bike sharing market, tourism’s momentum offers margin upside, given riders’ higher willingness to pay for convenience and curated experiences.

Geography Analysis

Hanoi contributed a significant chink in Vietnam bike-sharing market revenue, underpinned by dense population, the launch of metro Line 2A, and city grants that subsidize smart-lock stations. Fleet utilisation tops 8 rides per unit daily around the Hoan Kiem–Ba Dinh corridor. Ho Chi Minh City follows, powered by proactive private investment and a vibrant tourism-retail mix. The Vietnam bike sharing market size in Da Nang, Hai Phong, Vũng Tàu, and Quy Nhơn benefits from provincial incentives that waive curbside fees for the first two operating years.

Central Vietnam’s Hue–Hoi An heritage belt posts standout growth through bundled eco-tourism projects. Local authorities cap internal-combustion vehicle entry during festival periods, handing micro-mobility an exclusivity edge that uplifts yield per ride. Coastal rainfall seasonality previously suppressed winter demand, but waterproof drive-trains and ride-pause billing features now extend ridership. Planned expressway links and smart-city grants are expected to unlock latent demand from 2027 onward, presenting fresh canvases for operators looking beyond saturated tier-one markets.

Urbanisation is climbing toward 45% by 2025, concentrating most new demand along the Red River Delta and Southeast corridors. Government transport blueprints adding new expressways and orbital rail ties will shrink inter-provincial travel time, increasing the viability of one-way cross-city bike sharing for late-night arrivals when buses cease. Vietnamese firms exporting operating playbooks to Laos and Indonesia validate the scalability of home-grown solutions across Southeast Asia, reinforcing the long-term expansion narrative for the Vietnam bike sharing market.

Competitive Landscape

The competitive landscape indicates a concentrated scenario, reflecting an emerging but diversified market structure. TriNam leverages early public-private partnerships and exclusive municipal permits in core city centres such as Hanoi and Ho Chi Minh City. Meituan (Mobike) brings algorithmic excellence honed in China, deploying dynamic fleet balancing to optimise bike availability. Lemonc Vietnam capitalises on strong financial backing and technology sharing from Mobike, growing rapidly in mixed-use districts. TUMI focuses on flexible service models tied to hospitality and urban mobility platforms, while Hue Smart Bike thrives regionally through close integration with tourist boards and cultural landmarks in central Vietnam.

Strategic positioning hinges on local ecosystem alignment. TriNam embeds its services within city-level mobility portals and public transport apps, ensuring seamless journey planning. Lemonc builds API partnerships with digital wallets and lifestyle apps to drive usage beyond tourism peaks. TUMI develops seasonal service packages with hotel operators, creating new demand from transient user groups. Foreign-backed players like Meituan must navigate localised data compliance and licensing frameworks, often through joint ventures or branded partnerships with Vietnamese entities. Market consolidation looms as smaller regional operators seek capital to match expanding technology and maintenance requirements, opening opportunities for mergers or franchised operations.

Technology differentiation remains a core battleground. Leaders deploy AI-driven rebalancing algorithms, blockchain-supported ESG tracking for CO₂ savings, and real-time component diagnostics via IoT-enhanced bike hardware. Innovations such as instant unlock via NFC and edge-processed QR recognition reduce wait times and improve customer experience. Advanced fleet health monitoring cuts repair cycles, enhancing operational uptime. As Vietnam’s bike-sharing ecosystem matures, the ability to translate such technical advantages into lower operational costs and higher customer loyalty will increasingly define competitive success.

Vietnam Bike-Sharing Industry Leaders

TriNam Group (TNGo)

Meituan (Mobike)

Lemonc Vietnam (MBI Sharing)

TUMI

Hue Smart Bike

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: JiBike launched its electric bike rental service in central Vietnam to enhance tourist experiences and attract more visitors.

- October 2024: GSM entered the bike sharing market with the launch of its Xanh SM Bike platform designed for VinFast electric motorcycles, paired with a competitive revenue-sharing policy.

Vietnam Bike-Sharing Market Report Scope

Bike-sharing refers to a shared transportation service wherein individuals gain access to conventional or electric bikes for commuting purposes at a specified rent.

The Vietnamese bike-sharing market is segmented by bike type, sharing system, sharing duration, and application. By bike type, the market is segmented into traditional/conventional bikes and e-bikes. By sharing system, the market is segmented into docked/station-based, dockless, and hybrid. By sharing duration, the market is segmented into short-term and long-term. By application, the market is segmented into regular commutes and recreation, and tourism. The report offers market size and forecasts in value (USD) for all the above segments.

| Traditional / Conventional Bikes |

| E-Bikes |

| Docked / Station-based |

| Dockless |

| Hybrid |

| Short-Term (Up to 24 hrs) |

| Long-Term (Above 24 hrs) |

| Regular Commute and Recreation |

| Tourism |

| By Bike Type | Traditional / Conventional Bikes |

| E-Bikes | |

| By Sharing System | Docked / Station-based |

| Dockless | |

| Hybrid | |

| By Sharing Duration | Short-Term (Up to 24 hrs) |

| Long-Term (Above 24 hrs) | |

| By Application | Regular Commute and Recreation |

| Tourism |

Key Questions Answered in the Report

What is the current value of the Vietnam bike sharing market?

The Vietnam Bike-Sharing Market size is expected to reach USD 107.6 million in 2026 and grow at a CAGR of 9.91% to reach USD 172.53 million by 2031.

Which bike type is growing fastest?

E-bikes lead growth with a 14.12% CAGR, driven by national electrification targets and expanded battery-swap infrastructure.

How large is the dockless segment?

Dockless services represent 59.42% of 2025 revenue and grow at a 12.63% CAGR, reflecting consumer preference for flexible pick-ups and drop-offs.

Why is tourism important for operators?

Tourism applications grow at a 14.31% CAGR, the quickest across segments, thanks to a 98% tourism recovery rate and heritage-site demand for low-impact transport.

Who is the market leader?

TriNam Group leads the market, benefiting from early public-private partnerships and high user-satisfaction ratings.

Page last updated on: