Kale Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

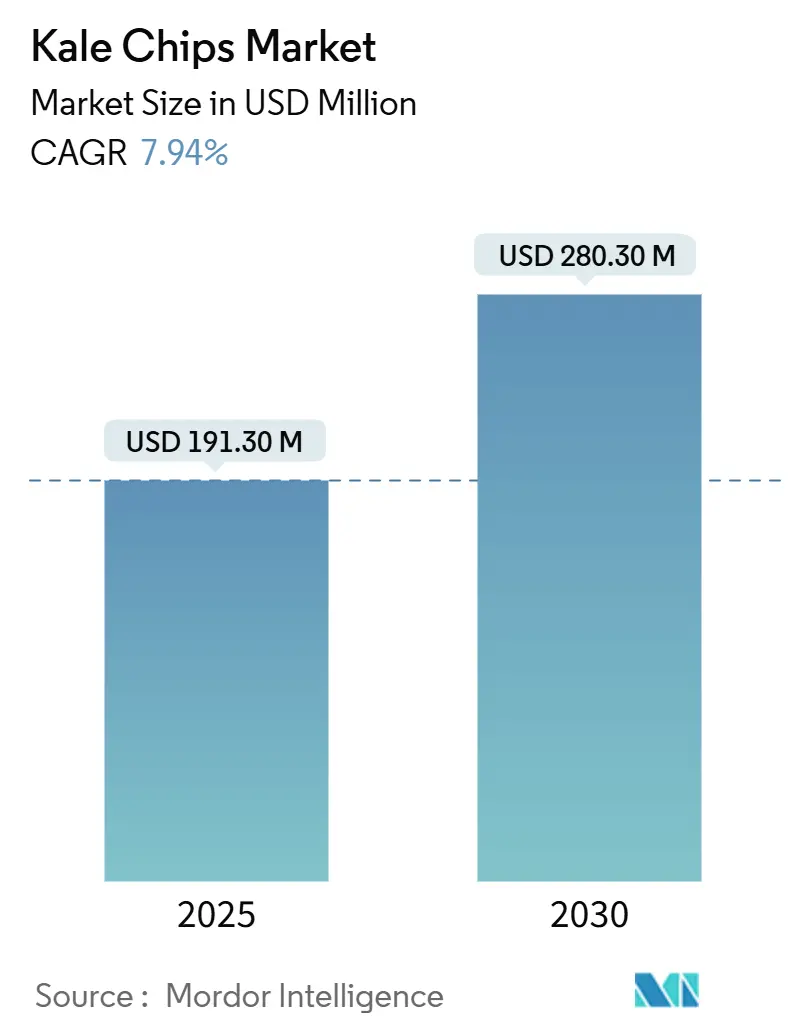

| Market Size (2025) | USD 191.30 Million |

| Market Size (2030) | USD 280.30 Million |

| Growth Rate (2025 - 2030) | 7.94% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Kale Chips Market Analysis by Mordor Intelligence

The kale chips market is valued at USD 191.3 million in 2025 and is projected to reach USD 280.3 million by 2030, expanding at a compound annual growth rate (CAGR) of 7.94%. This growth trajectory reflects a fundamental shift in consumer snacking behavior, where nutritional density increasingly trumps traditional taste preferences. The market's expansion coincides with the broader healthy snacking sector, which benefits from organic retail sales reaching USD 69.7 billion in 2023, according to USDA data[1] U.S. Department of Agriculture Economic Research Service, “Organic Situation Report 2025,” usda.gov. The FDA's updated guidance on low-moisture ready-to-eat food safety standards directly impacts kale chip manufacturers, establishing clearer pathways for compliance and market entry. Rising demand for vegetable chips in healthy snacking options is anticipated to drive market growth. Demand for gluten-free food products and acceptance of different types of vegetable chips as healthy snacks have been positive factors for the kale chips market. Moreover, a rising preference for plant-based food products is expected to drive the product demand.

Key Report Takeaways

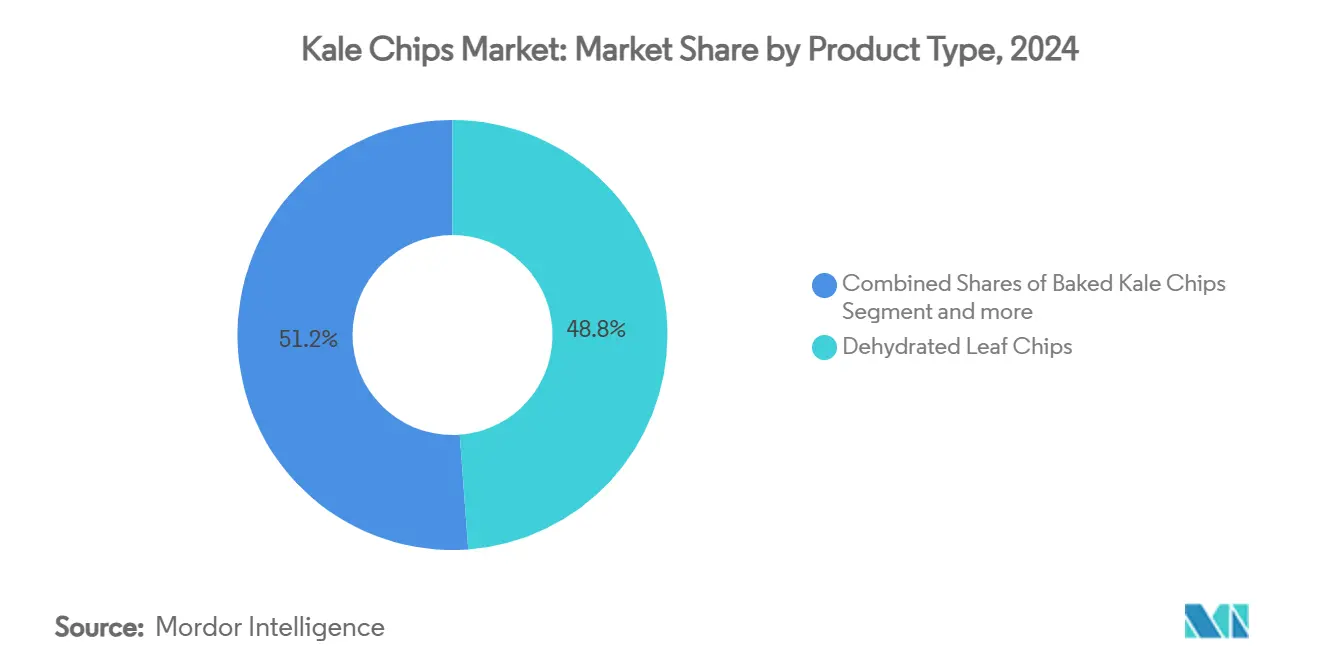

- By product type, dehydrated leaf chips held 48.84% of the kale chips market share in 2024, while vacuum-fried formats are projected to grow at an 8.53% CAGR through 2030.

- By flavor, seasoned variants captured 69.22% revenue share in 2024; unflavored chips are forecast to advance at an 8.12% CAGR to 2030.

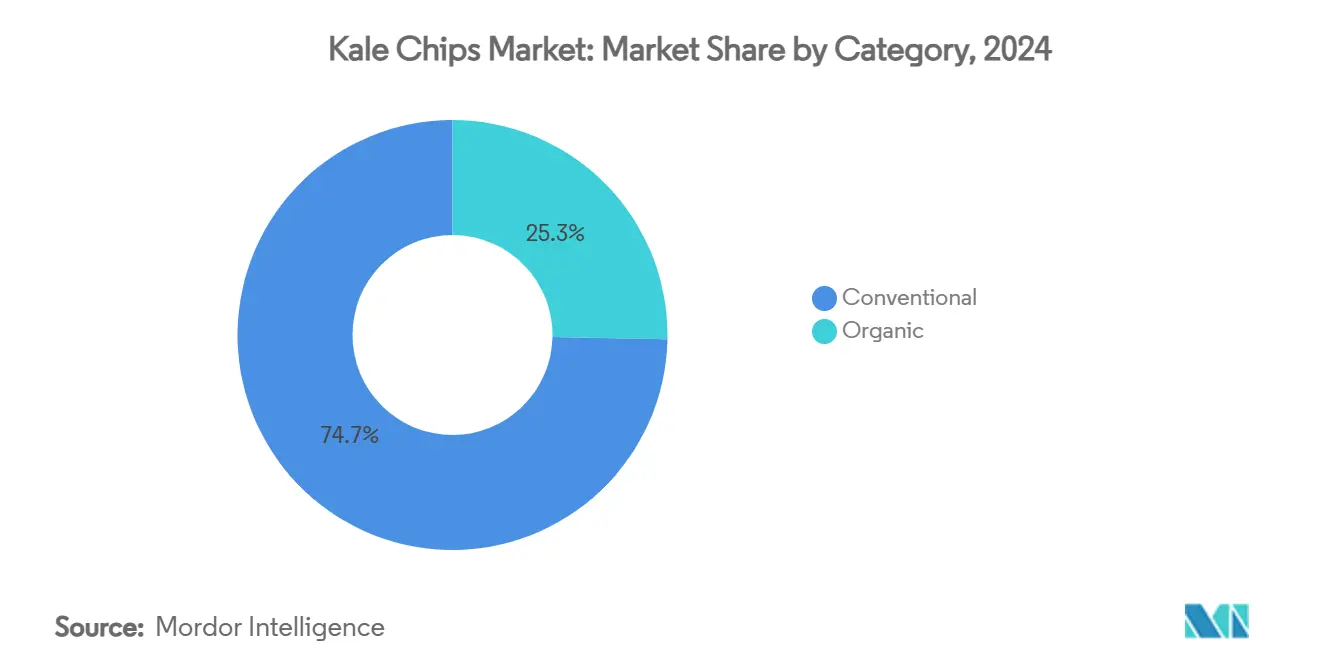

- By category, conventional items formed 75.43% of 2024 sales, yet organic lines are set to rise at a 9.32% CAGR between 2025-2030.

- By distribution channel, hypermarkets and supermarkets accounted for 55.55% of 2024 turnover, while online platforms will post the quickest 8.88% CAGR over the outlook.

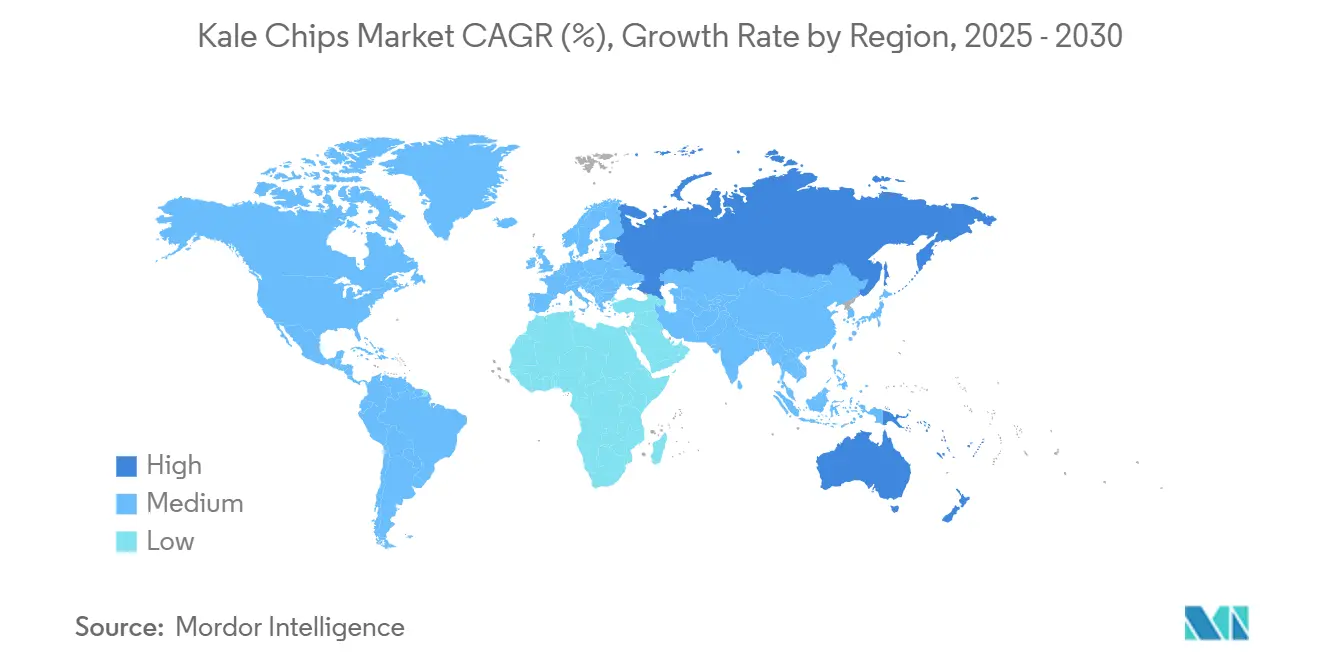

- By geography, North America led with a 36.13% share in 2024, whereas Asia-Pacific is expected to climb at an 8.67% CAGR during 2025-2030.

Global Kale Chips Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | impact Timeline |

|---|---|---|---|

| Rising consumer demand for healthy snacks | +2.1% | Global, with North America and Europe leading adoption | Medium term (2-4 years) |

| Increasing availability in mainstream retail channels | +1.8% | North America & EU, expanding to APAC urban centers | Short term (≤ 2 years) |

| Growth of e-commerce grocery platforms | +1.4% | Global, with highest penetration in developed markets | Short term (≤ 2 years) |

| Product innovation in flavours & formats | +1.2% | Global, with premium positioning in developed markets | Medium term (2-4 years) |

| Growth in Plant-Based and Vegan Diet Adoption | +0.9% | APAC core, spill-over to MEA, strong in North America | Long term (≥ 4 years) |

| Adoption of gentle vacuum-dehydration technology | +0.7% | Global, with manufacturing concentration in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Demand for Healthy Snacks

Kale chips meet consumer demand by providing nutritious alternatives in familiar snack formats. These products offer a healthier option while maintaining the satisfying crunch and convenience of traditional chips. The growing health consciousness among consumers has led to increased adoption of these alternative snacks in both retail and foodservice sectors. The USDA's Food Access and Retail Expansion Fund in 2024, with USD 60 million in funding, aims to improve healthy food access in underserved communities, supporting kale chip distribution networks. The fund enables retailers to expand their healthy food offerings and strengthen supply chain infrastructure. This initiative has particularly benefited small and medium-sized manufacturers entering the market. FDA guidance on low-moisture ready-to-eat foods provides safety standards that benefit premium snack manufacturers, ensuring product quality and consumer safety throughout the production process. These regulations have helped establish industry-wide benchmarks for food safety and quality control, contributing to market growth and consumer trust.

Increasing Availability in Mainstream Retail Channels

The retail adoption of kale chips has transformed them from specialty items into widely available snack alternatives, marking a significant shift in consumer accessibility. According to U.S. Census [2]U.S. Census Bureau, “Monthly Retail Trade Report 2025,” census.govdata, grocery store sales were USD 73.77 billion in 2024, indicating strong consumer demand for healthier snack options. Retailers' strategic focus on high-margin health products has supported this expansion by helping differentiate their product offerings and meeting evolving consumer preferences. The store's success exemplifies the growing consumer interest in nutritious, convenient snack alternatives. The diversification of retail channels has reduced distribution risks while increasing consumer access points, supporting sustained market growth beyond specialized health food retailers. This broader distribution network has enabled kale chip manufacturers to reach diverse consumer segments and establish a stronger presence in the mainstream snack market.

Growth of E-commerce Grocery Platforms

The rise in digital grocery shopping has increased access to kale chips. According to the U.S. Department of Agriculture, Economic Research Service, 19.4% of U.S. grocery shoppers aged 15 and older purchased groceries online at least once in the past 30 days in 2022 and 2023. E-commerce platforms allow manufacturers to sell directly to consumers, avoiding traditional retail markups while providing comprehensive product information for health-conscious consumers. Online sales channels are particularly effective for premium products like kale chips, as consumers can research nutritional information and ingredient sources before making purchases. The growth in e-commerce enables geographic expansion without investments in physical retail infrastructure, allowing smaller kale chip manufacturers to compete with larger companies through digital marketing and subscription services.

Product Innovation in Flavours & Formats

Flavor innovations are transforming kale chips from health-focused products into mainstream snacking alternatives. Advanced processing methods, particularly vacuum-frying technology, help retain flavors while preserving nutritional value, allowing kale chips to compete with conventional chips in taste. The introduction of new flavors, including spicy, savory, and sweet varieties, appeals to diverse consumer preferences. Manufacturers are also experimenting with different textures and shapes to enhance the snacking experience. The diversification of product formats reduces consumer fatigue and expands market reach, enabling premium pricing through product differentiation. This evolution in kale chip production has attracted both health-conscious consumers and traditional snack enthusiasts, contributing to the segment's growth in the broader snack food market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Premium price versus conventional chips | -1.6% | Global, with higher sensitivity in emerging markets | Short term (≤ 2 years) |

| Shelf-life & texture degradation from moisture re-absorption | -0.8% | Global, particularly humid climates and extended distribution | Medium term (2-4 years) |

| Lack of Consumer Awareness in Emerging Markets | -0.7% | APAC emerging markets, Latin America, MEA | Long term (≥ 4 years) |

| Taste Acceptance Barrier | -0.5% | Global, with higher resistance in traditional snacking markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Premium Price Versus Conventional Chips

Price sensitivity constrains market expansion as kale chips command 2-3x premiums over conventional potato chips, creating affordability barriers despite growing health consciousness. The USDA's Livestock, Dairy, and Poultry Outlook reports overall food price inflation at 2.3% in 2024, down from 5.8% in 2023, yet premium snack categories face ongoing cost pressures from specialized processing requirements. Vacuum-frying technology, while preserving nutritional quality, requires specialized equipment and longer processing times that increase manufacturing costs compared to conventional chip production. The organic segment faces particular pressure as USDA data indicates declining price premiums for organic products, potentially compressing margins for organic kale chip producers. Economic headwinds disproportionately impact discretionary spending on premium snacks, with households prioritizing essential food purchases over health-positioned alternatives during inflationary periods.

Lack of Consumer Awareness in Emerging Markets

Consumer education gaps in emerging markets limit adoption despite growing middle-class populations and increasing health awareness. Asia-Pacific's alternative protein sector, while receiving significant investment, faces regulatory complexity across markets like Indonesia, Malaysia, and Thailand, where novel food definitions vary significantly. Traditional snacking preferences in emerging markets favor familiar flavors and textures, requiring extensive marketing investment to establish kale chips as acceptable alternatives. The European Food Safety Authority's[3]European Food Safety Authority, "what EFSA’s updated guidance means for safety assessments", www.efsa.europea.euupdated novel foods guidance, effective February 2025, creates regulatory pathways but also highlights complexity in introducing unfamiliar food products across diverse markets. Distribution infrastructure limitations in emerging markets restrict product availability and increase costs, while limited cold-chain capabilities threaten product quality during extended transportation. Cultural resistance to unfamiliar vegetables compounds awareness challenges, requiring localized flavor development and extensive consumer education campaigns that increase market entry costs and extend payback periods for international expansion investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vacuum-Frying Gains Despite Dehydrated Dominance

Processing technology differentiation drives competitive positioning within the kale chips market, where dehydrated leaf chips maintain a 48.84% market share in 2024 through cost advantages and established production infrastructure. Vacuum-fried kale chips, despite smaller current volumes, command the fastest growth at 8.53% CAGR through 2030, supported by superior nutrient retention and enhanced flavor profiles that justify premium pricing. Baked kale chips occupy the middle ground, offering healthier positioning than conventional chips while maintaining accessible price points for mainstream consumers. Extruded chips represent the smallest segment but provide manufacturing scalability advantages for large food companies seeking to enter the category through existing production capabilities.

The vacuum-frying segment benefits from technological advancement that addresses traditional limitations of oil absorption and nutrient degradation, creating products that compete directly with conventional snacks on taste while maintaining health positioning. Cryo-curing patent applications demonstrate emerging preservation technologies that could revolutionize plant-based snack processing by reducing preparation time from weeks to hours while preserving essential compounds. This technological evolution suggests product type segmentation will increasingly favor advanced processing methods that deliver superior nutritional profiles and sensory experiences, supporting the vacuum-fried segment's accelerated growth trajectory.

By Flavor: Unflavored Growth Challenges Seasoned Dominance

Flavor segmentation analysis shows that flavored products hold a 69.22% market share in 2024, while unflavored variants are growing at a higher CAGR of 8.12% through 2030. Flavored products maintain their market dominance by effectively masking kale's natural bitterness and offering familiar taste profiles that help consumers transition from traditional chips. Global snacking trends and international flavor preferences continue to drive innovation in seasoned varieties.

The unflavored segment's growth reflects increasing consumer preference for natural vegetable flavors without additives, particularly among health-conscious consumers. This aligns with the clean-label movement, as consumers increasingly examine ingredient lists and seek products with minimal processing. The growth in unflavored products presents opportunities for manufacturers to develop premium products using high-quality raw materials and advanced processing techniques that enhance kale's natural flavor profile.

By Category: Organic Surge Pressures Conventional Leadership

Category segmentation demonstrates the organic transition accelerating across food markets, where conventional kale chips maintain 75.43% market share in 2024 but organic alternatives expand at 9.32% CAGR through 2030, outpacing overall market growth by 138 basis points. Conventional products benefit from established supply chains and lower production costs that enable broader market accessibility, particularly important for mainstream retail channel expansion. The USDA's Organic Transition Initiative, backed by USD 300 million in funding, specifically supports producers transitioning to organic practices, potentially increasing organic kale supply and reducing cost premiums over time.

Organic segment growth reflects consumer willingness to pay premiums for perceived health and environmental benefits, despite declining organic price premiums noted in the USDA analysis, creating margin pressure for producers. The Plant Based Foods Association's certification program, which has certified over 1,100 products, provides market validation that supports organic positioning through third-party verification, according to the Plant Based Foods Association. Controlled environment agriculture investments, highlighted in USDA research, enable consistent organic kale production that supports year-round supply chain reliability. The organic segment's accelerated growth trajectory indicates structural demand shift toward sustainable agriculture practices, creating opportunities for producers who can achieve organic certification while maintaining competitive pricing through operational efficiency and scale advantages.

By Distribution Channel: E-commerce Disrupts Traditional Retail Patterns

Distribution channel evolution reflects broader retail transformation where hypermarkets and supermarkets control 55.55% market share in 2024, yet online retail channels accelerate at 8.88% CAGR through 2030, leveraging digital adoption trends that reshape consumer purchasing behavior. Traditional retail dominance stems from established infrastructure and consumer shopping habits, particularly for food products, where tactile evaluation influences purchase decisions.

Convenience stores and specialty stores serve complementary roles, providing impulse purchase opportunities and curated health food selections that support premium positioning. Digital channel growth creates scalable distribution that supports geographic expansion without physical retail infrastructure investments, enabling smaller brands to compete through targeted marketing and subscription models that build customer loyalty and predictable revenue streams.

Geography Analysis

North America holds 36.13% market share in 2024, driven by its mature health food retail infrastructure and consumer acceptance of premium snack alternatives. The USDA's Food Access and Retail Expansion Fund, with USD 60 million in funding, supports healthy food access in underserved communities, strengthening the distribution infrastructure. Online grocery adoption shows 19.3% of consumers purchasing monthly, with higher participation among women (22%) and households with children (23%), matching health-conscious kale chip consumer demographics.

Asia-Pacific demonstrates the highest growth rate at 8.67% CAGR through 2030, supported by alternative protein investments exceeding USD 300 million and supportive government policies. Singapore's '30 by 30' food security initiative and Australia's Modern Manufacturing Initiative provide institutional support for alternative protein development, benefiting plant-based snack categories. Market entry strategies must navigate diverse regulatory frameworks, including FSANZ in Australia and New Zealand, BPOM in Indonesia, and SFA in Singapore. The region's expansion potential derives from its growing middle class, rising health awareness, and urbanization, though market success depends on consumer education and distribution network development.

Europe shows consistent growth through established organic food markets and structured regulatory systems. The European Food Safety Authority's updated guidance, effective February 2025, provides clear market entry pathways while maintaining safety standards. South America and Middle East Africa present growth opportunities through expanding middle-class populations and increasing health consciousness, requiring market-specific product adaptation. The EU's regulatory framework for processed vegetables includes mandatory HACCP compliance and specific labeling requirements, favoring established producers. International market expansion requires balancing production efficiency with regional taste preferences and varying regulatory requirements.

Competitive Landscape

The kale chips market exhibits fragmented competition with a concentration score of 3 out of 10, indicating numerous players competing across different strategic dimensions without dominant market control. This fragmentation creates opportunities for both established food companies and specialized health snack producers to capture market share through differentiated positioning strategies. Technology adoption emerges as a key competitive differentiator, with vacuum-frying capabilities enabling premium product positioning that commands higher margins while addressing consumer demands for superior taste and nutritional retention.

Strategic patterns reveal three distinct competitive approaches: premium positioning through organic certification and advanced processing, mainstream market penetration through retail channel expansion, and direct-to-consumer strategies leveraging e-commerce platforms for brand building and customer relationship development.

White-space opportunities exist in flavor innovation, international market expansion, and processing technology advancement, while emerging disruptors focus on sustainable packaging, direct-to-consumer distribution, and plant-based protein enhancement that appeals to evolving consumer preferences for functional nutrition and environmental responsibility.

Kale Chips Industry Leaders

-

General Mills Inc.

-

Brad'S Plant Based, LLC

-

Vermont Kale Chips

-

Simply 7 Snacks, LLC

-

The Angel Kale Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2020: Ecoideas announced the launch of Solar Raw's Kaley's Kale Chips in four new flavors to meet the growing demand for nutritionally dense and naturally delicious plant based snacks that appeal to mainstream snacker.

- November 2019: San Miguel Produce, Inc., the leader in value-added dark leafy greens, announced the launch of its new line of fresh Kale Chip Kits under their Cut 'N Clean Greens label.

Global Kale Chips Market Report Scope

The kale chips are generally made with fresh kale which is tossed in oil and sea salt. The Global kale chips market is segmented by product type, distribution channel, and geography. The market is segmented by product type into dehydrated leaf crisps/chips and extruded chips. Based on the Distribution Channel, the market is diversified into supermarkets/hypermarkets, convenience stores, specialty stores, and online stores. Moreover, the market is segmented by Geography into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of the value (in USD million).

| Dehydrated Leaf Chips |

| Baked Kale Chips |

| Vacuum-Fried Kale Chips |

| Extruded Chips |

| Flavored |

| Unflavored |

| Conventional |

| Organic |

| Hypermarkets/Supermarkets |

| Convenience Stores |

| Speciality Stores |

| Online Retail/E-commerce |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Dehydrated Leaf Chips | |

| Baked Kale Chips | ||

| Vacuum-Fried Kale Chips | ||

| Extruded Chips | ||

| By Flavor | Flavored | |

| Unflavored | ||

| By Category | Conventional | |

| Organic | ||

| By Distribution Channel | Hypermarkets/Supermarkets | |

| Convenience Stores | ||

| Speciality Stores | ||

| Online Retail/E-commerce | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the global kale chips market in 2025?

The kale chips market is valued at USD 191.3 million in 2025.

What is the projected growth rate for kale chips between 2025 and 2030?

Industry revenue is forecast to expand at a 7.94% CAGR and reach USD 280.3 million by 2030.

Which product type is expected to grow the fastest?

Vacuum-fried kale chips post the quickest trajectory, advancing at an 8.53% CAGR through 2030.

Which regions lead the market today and which are rising the fastest?

North America holds 36.13% of 2024 sales, while Asia-Pacific is projected to record the highest 8.67% CAGR over the forecast period.

Page last updated on: