Banana Chips Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

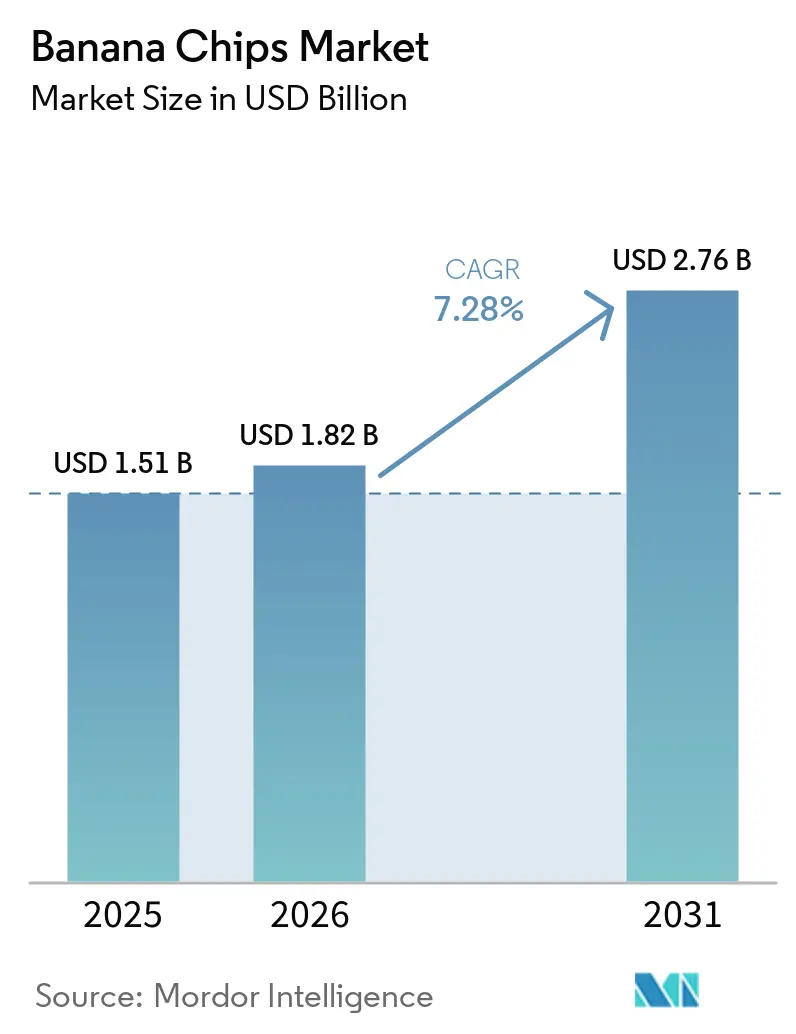

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 2.76 Billion |

| Growth Rate (2026 - 2031) | 7.28% CAGR |

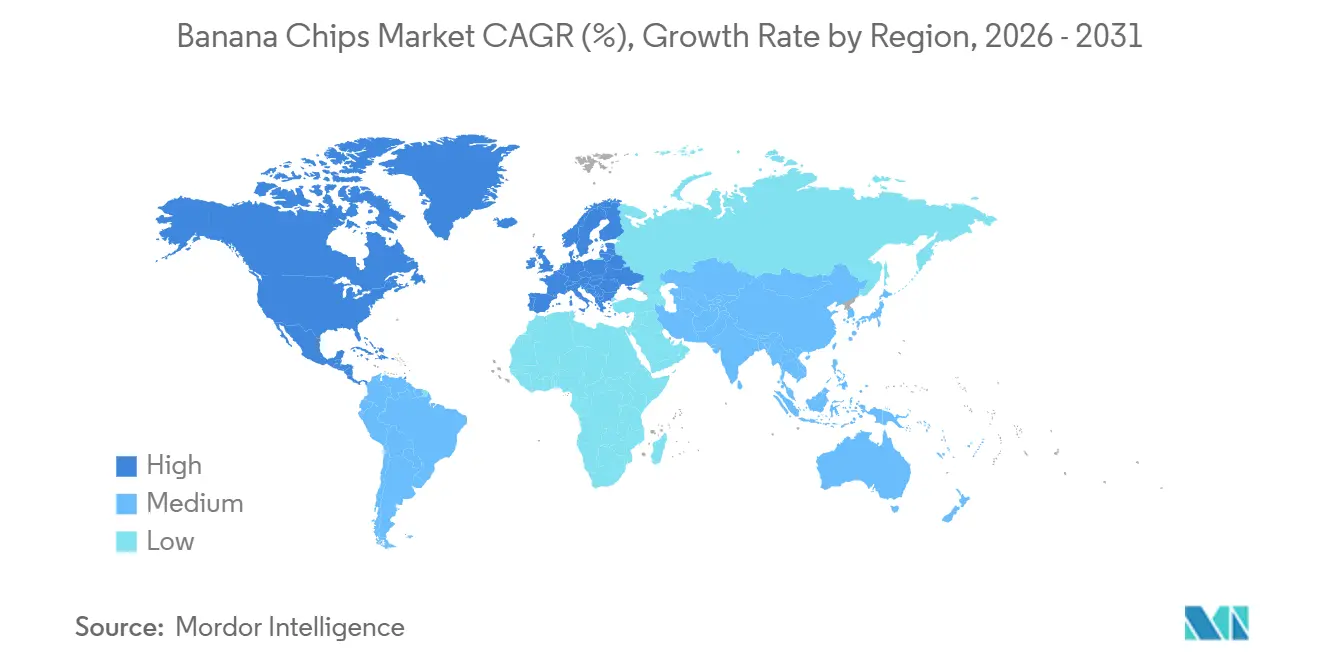

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Banana Chips Market Analysis by Mordor Intelligence

The banana chips market size is expected to increase from USD 1.51 billion in 2025 to USD 1.82 billion in 2026 and reach USD 2.76 billion by 2031, growing at a CAGR of 7.28% over 2026-2031. Rising demand for plant-based, minimally processed snacks is shifting volume away from traditional salty products toward fruit-based alternatives. Abundant raw materials in Indonesia, India, Vietnam, and the Philippines, coupled with strong consumption growth in China, where banana imports climbed 17% in value and 15% in volume during 2025, underpin supply security. Health-centric preferences are catalyzing baked variants, organic certification, and clean-label ingredient lists, while quick-commerce and subscription models accelerate impulse purchasing in urban Asia-Pacific and North America. Intensifying competition from vegetable crisps, chickpea puffs, and protein snacks is steering producers toward flavor innovation, sustainable sourcing, and omnichannel distribution.

Key Report Takeaways

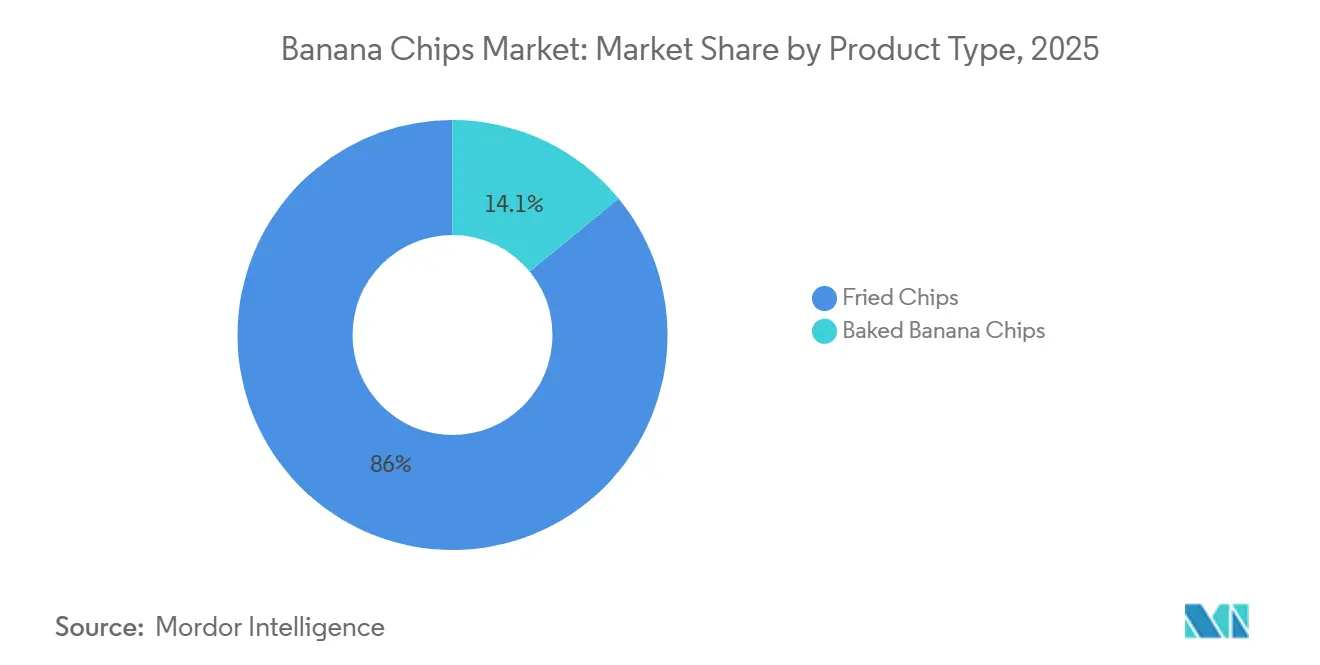

- By product type, fried chips led with 85.95% of the banana chips market share in 2025, while baked chips are projected to advance at an 8.21% CAGR through 2031.

- By flavor, salted variants captured 46.86% revenue in 2025; spiced and herb formats are set to expand at a 7.99% CAGR to 2031.

- By nature, conventional products held 75.68% of 2025 sales, whereas organic chips are forecast to post an 8.51% CAGR through 2031.

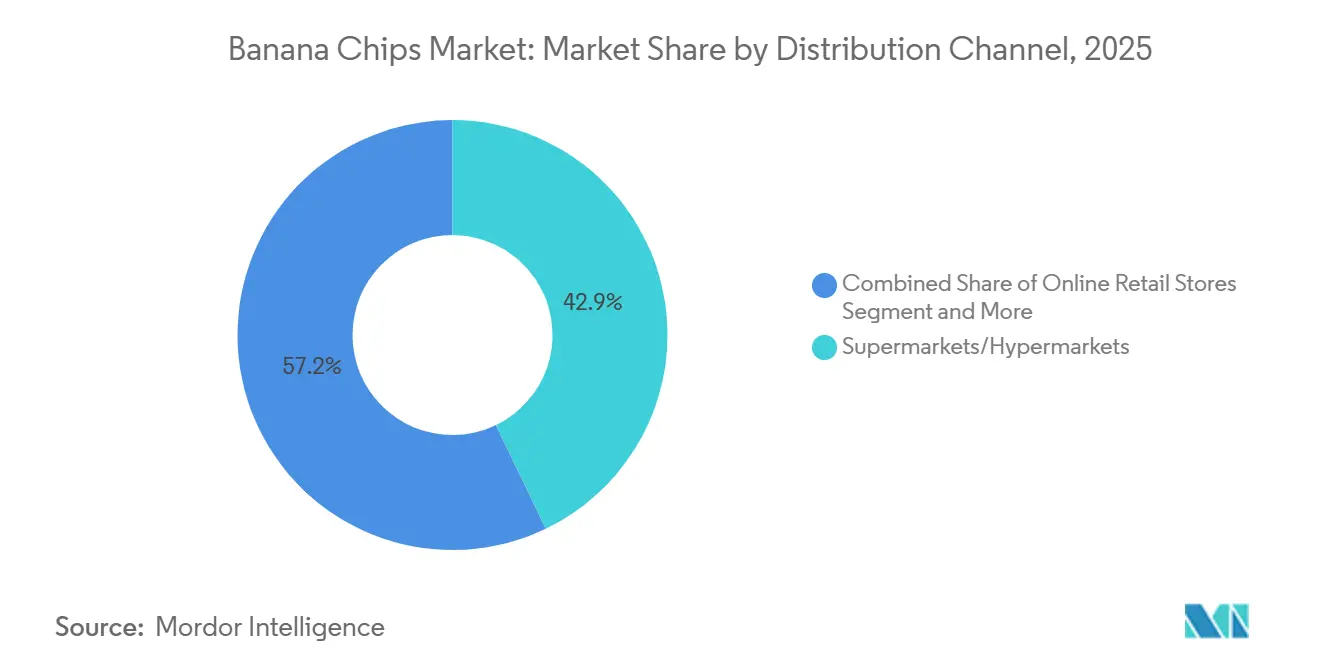

- By distribution, supermarkets and hypermarkets controlled 42.85% of the 2025 volume; online retail is the fastest-growing channel at 8.58% CAGR to 2031

- By geography, Asia-Pacific commanded 43.22% of global revenue in 2025 and is progressing at a 8.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Banana Chips Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Demand for Healthier Snack Alternatives | +1.8% | Global, with concentration in North America, Europe, and urban Asia-Pacific | Medium term (2-4 years) |

| Rising Popularity of Plant-Based and Vegan Diets | +1.2% | North America, Europe, urban India, China | Medium term (2-4 years) |

| Product and Flavor Innovation | +1.5% | Global, led by India, North America, Southeast Asia | Short term (≤ 2 years) |

| Increasing Consumer Preference for Convenient, On-the-Go Snacks | +1.3% | Global, strongest in Asia-Pacific metro areas, North America | Short term (≤ 2 years) |

| Rising Awareness of Natural and Minimally Processed Foods | +0.9% | North America, Europe, Australia | Long term (≥ 4 years) |

| Increasing Demand for Organic and Specialty Snack Products | +0.6% | North America, Europe, select Asia-Pacific urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Healthier Snack Alternatives

Consumers are reallocating snack budgets toward perceived better-for-you options, creating headroom for banana chips positioned as fruit-based and lower in artificial additives. PepsiCo's October 2025 reformulation of Lay's to remove artificial flavors and colors, coupled with the introduction of olive and avocado oils in Baked and Kettle Cooked variants, underscores how legacy potato-chip brands are responding to clean-label pressure. This competitive repositioning elevates consumer expectations for ingredient transparency across all chip categories, including banana chips. Brands emphasizing no artificial colors or synthetic flavors, such as Beyond Snack, which secured USD 8.3 million in Series A funding in January 2025, are capturing shelf space in modern retail and quick-commerce platforms. The shift is particularly pronounced in North America and Europe, where consumers scrutinize ingredient lists and favor recognizable components. Baked banana chips, which offer approximately 50% less fat than fried variants, are expanding at 8.21% CAGR, outpacing the overall market and signaling a structural preference for reduced-fat formats. This trend compels manufacturers to invest in vacuum heat pump drying and other technologies that preserve nutritional content while minimizing oil absorption.

Rising Popularity of Plant-Based and Vegan Diets

Plant-based eating patterns are normalizing beyond niche demographics, and banana chips benefit from inherent vegan credentials without requiring reformulation. Unlike dairy-based snacks or meat-alternative products that face ingredient-cost inflation, banana chips derive from a single, widely cultivated crop, simplifying supply chains and enabling competitive pricing. India's banana production remained stable at approximately 9.26 million tons in 2024, with East Java, Lampung, and West Java provinces in Indonesia contributing an additional 5.59 million tons, ensuring abundant raw material availability for processors. China's banana imports reached 1.94 million tonnes in 2025, up 15% year-on-year, driven by rising middle-class demand for convenient, plant-forward snacks. Retailers in North America and Europe are expanding plant-based snack assortments, and banana chips occupy a favorable position due to their shelf stability and minimal processing compared to extruded or puffed alternatives. The absence of common allergens (gluten, dairy, and nuts in most formulations) further broadens addressable consumer segments, including schools and institutional foodservice. As plant-based diets transition from trend to mainstream, banana chips stand to capture incremental volume from consumers seeking minimally processed, recognizable ingredients.

Product and Flavor Innovation

Flavor diversification is unlocking new consumption occasions and demographic segments, moving banana chips beyond traditional salted formats. Beyond Snack's portfolio includes Peri Peri, Salt & Black Pepper, Sour Cream & Onion, and Parsley variants, alongside a Kerala-style chip cooked in coconut oil, demonstrating how regional authenticity and global flavor profiles can coexist. Spiced and herb flavors are growing at 7.99% CAGR, outpacing salted chips and reflecting consumer appetite for bold, globally inspired tastes. Manufacturers are leveraging vacuum frying and freeze-drying technologies to preserve natural banana sweetness while accommodating savory seasonings; a 2024 peer-reviewed study demonstrated that vacuum heat pump drying at 50°C and 80 kPa retained 55.9% of vitamin C in green banana slices, offering a technical pathway to market products with enhanced nutritional claims. Haldiram, with Rs 12,977 crore in FY2025 revenue and operating margins of 18-19%, possesses the scale and R&D capacity to introduce localized banana chip variants across its 26 manufacturing units, potentially disrupting regional players. Flavor innovation also enables premiumization, with organic and specialty SKUs commanding 20-30% price premiums in modern retail channels.

Increasing Consumer Preference for Convenient, On-the-Go Snacks

Urbanization and longer commute times are driving demand for portable, shelf-stable snacks that require no refrigeration or preparation. Banana chips fit this profile, with typical moisture content below 10%, enabling ambient storage and extended shelf life. Beyond Snack claims top-selling status on leading e-commerce and quick-commerce platforms in India, leveraging digital channels to bypass traditional retail gatekeepers and reach younger, digitally native consumers. The rise of co-working spaces, flexible work arrangements, and travel resumption post-pandemic has expanded snacking occasions beyond traditional meal times. Manufacturers are responding with 25-50 gram single-serve packs and 100-150 gram resealable pouches, optimizing pack sizes for portability and portion control. This shift also benefits brands with strong e-commerce capabilities, as online channels enable direct-to-consumer subscription models and personalized assortments that traditional retail cannot easily replicate.

Restraint Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fat and Calorie Content in Fried Banana Chips | -0.7% | Global, most acute in health-conscious North America and Europe | Short term (≤ 2 years) |

| Competition from Alternative Snack Products | -0.9% | Global, intensifying in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Shelf Life and Product Preservation Challenges | -0.4% | Tropical and high-humidity regions (Southeast Asia, South America, MEA) | Long term (≥ 4 years) |

| Processing and Manufacturing Limitations | -0.5% | Emerging markets with limited access to advanced drying equipment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Fat and Calorie Content in Fried Banana Chips

Regulatory scrutiny is intensifying; India's Food Safety and Standards Authority (FSSAI) mandates nutritional labeling per the Food Safety and Standards (Packaging and Labelling) Regulations, and contaminant limits for ready-to-eat products include total aflatoxins ≤15 µg/kg and aflatoxin B1 ≤10 µg/kg, requiring processors to implement rigorous quality controls[1]Source: Food Safety and Standards Authority of India. "Nutritional Labeling per the Food Safety and Standards", fssai.gov.in. Consumers increasingly compare fat content across snack categories, and fried banana chips' calorie density (approximately 500-550 kcal per 100 grams) can deter purchase in markets where portion-controlled, lower-calorie snacks are gaining traction. Vacuum frying, demonstrated to reduce oil absorption while preserving color and vitamin C, requires capital investment in specialized equipment, limiting adoption among small and medium processors. The restraint is most acute in North America and Europe, where clean-label and reduced-fat claims are table stakes for modern retail listings, and less pronounced in price-sensitive emerging markets where taste and affordability outweigh nutritional considerations.

Competition from Alternative Snack Products

Banana chips compete for wallet share with an expanding array of vegetable crisps, kale chips, chickpea puffs, and protein-enriched snacks, many of which leverage superior health halos or functional benefits. Vegetable crisps often market higher fiber and micronutrient content, while protein snacks appeal to fitness-focused demographics seeking satiety and muscle recovery. Banana chips' inherent sweetness, even in salted formats, can limit appeal among consumers seeking savory, umami-forward profiles. Shelf-space competition is intensifying in supermarkets and hypermarkets, which accounted for 42.85% of 2025 distribution; category managers allocate linear footage based on velocity and margin, and emerging snack formats with higher price points and faster turnover can displace slower-moving SKUs. Online retail, growing at 8.58% CAGR, partially mitigates this risk by enabling long-tail assortments, yet digital channels also amplify consumer access to niche and imported alternatives. Brands must differentiate through flavor innovation, origin storytelling, or certifications (organic, Fair Trade, non-GMO) to defend share.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Baked Variants Narrow the Gap

Fried chips commanded 85.95% of the 2025 market share, reflecting entrenched consumer preference for the crisp texture and flavor intensity achieved through traditional frying processes. Baked chips, though starting from a smaller base, are expanding at 8.21% CAGR through 2031, driven by health-conscious consumers seeking lower-fat alternatives and manufacturers' investments in vacuum heat pump drying and air-frying technologies. A 2024 peer-reviewed study confirmed that vacuum drying at 50°C and 80 kPa preserved 55.9% of vitamin C in green banana slices while reducing oxidative browning, offering a technical pathway for baked products to match fried chips' color and nutritional appeal. Fried chips retain dominance in price-sensitive markets across Asia-Pacific and Latin America, where taste and affordability outweigh nutritional considerations, and in foodservice channels that prioritize bulk purchasing and familiar formats.

Baked variants face technical and economic hurdles that constrain near-term share gains. Vacuum frying and heat pump drying equipment require capital outlays of USD 50,000-200,000 per line, limiting adoption among small and medium processors in India, Indonesia, and Vietnam, which collectively supply the majority of Asia-Pacific production. Baked chips also command 15-25% price premiums in retail, narrowing addressable consumer segments in emerging markets. However, regulatory tailwinds are building; India's FSSAI classifies banana chips under Food Product Category 18.2.2 (Fruit and vegetable based snacks) and mandates compliance with contaminant limits and microbiological standards, creating a level playing field for baked and fried formats. As consumer awareness of trans fats and oxidized oils grows, baked chips are positioned to capture incremental volume from health-forward demographics in North America, Europe, and urban Asia-Pacific.

By Flavor: Spiced Varieties Gain Traction

Salted banana chips held 46.86% of the 2025 market share, benefiting from universal appeal and established taste profiles that span demographic and geographic segments. Spiced and herb flavors, however, are accelerating at 7.99% CAGR, reflecting consumer appetite for bold, globally inspired tastes and manufacturers' efforts to differentiate in crowded retail environments. Beyond Snack's portfolio, including Peri Peri, Salt & Black Pepper, Sour Cream & Onion, and Parsley, demonstrates how flavor innovation can unlock new consumption occasions and attract younger, experimentation-oriented consumers. Sweet banana chips, often lightly caramelized or honey-coated, occupy a niche in confectionery-adjacent channels and appeal to consumers seeking dessert alternatives, though their higher sugar content limits growth in health-conscious segments. Other flavors, including regional variants such as Kerala-style chips cooked in coconut oil, cater to diaspora populations and consumers seeking authentic, origin-specific products.

Flavor innovation enables premiumization and margin expansion, with spiced and organic SKUs commanding 20-30% price premiums over salted commodity formats. Haldiram, with Rs 12,977 crore in FY2025 revenue and 26 manufacturing units across India, possesses the scale and distribution reach to introduce localized banana chip variants tailored to regional taste preferences, potentially disrupting smaller players. Sweet formats face headwinds from rising consumer scrutiny of added sugars and regulatory pressure; FSSAI's contaminant regulations apply uniformly to all banana chip formats, and processors must ensure compliance with pesticide maximum residue limits (MRLs) for banana, including carbendazim (1 mg/kg) and diuron (0.1 mg/kg). Spiced and herb varieties are best positioned to capture incremental volume, as they align with global snacking trends toward savory, umami-forward profiles without compromising health perceptions.

By Nature: Organic Certification Unlocks Premium Channels

Conventional banana chips accounted for 75.68% of the 2025 market share, reflecting cost advantages and established supply chains that prioritize volume and affordability. Organic banana chips, though starting from a smaller base, are expanding at 8.51% CAGR through 2031, driven by consumer willingness to pay premiums for certified products and regulatory frameworks that facilitate traceability and market access. India's National Programme for Organic Production (NPOP), updated in its 8th edition in 2024, requires ≥95% certified organic ingredients for products to carry the "Certified Organic" label and India Organic Logo, with mandatory Tracenet usage for chain-of-custody and transaction certificates for every sale[2]Source: APEDA, "NATIONAL PROGRAMME FOR ORGANIC PRODUCTION (NPOP)", npop.apeda.gov.in. Organic certification enables access to premium retail channels in North America and Europe, where consumers scrutinize labels and favor products with third-party verification. NPOP also mandates residue testing for at least 5% of certified operators annually, using ISO/ILAC accredited laboratories, ensuring that organic banana chips meet importing-country phytosanitary standards.

Conventional chips retain dominance in price-sensitive markets across Asia-Pacific, Latin America, and the Middle East, where affordability and taste outweigh certification status. Indonesia's 9.26 million tons of banana production in 2024 and exports of 26,240 tons to Malaysia, Japan, and Singapore underscore the region's role as a low-cost raw-material supplier, supporting conventional chip manufacturing BPS Indonesia. Organic production faces technical and economic barriers, including 2-3 year conversion periods for banana farms, higher input costs for approved fertilizers and pest-control agents, and compliance costs for certification and testing.

By Distribution Channel: E-Commerce Reshapes Access

Supermarkets and hypermarkets held 42.85% of 2025 distribution share, leveraging extensive footprints, promotional activity, and consumer familiarity to drive volume. Online retail, however, is accelerating at 8.58% CAGR through 2031, the fastest among all channels, as e-commerce and quick-commerce platforms enable impulse purchases, subscription models, and direct-to-consumer engagement. Beyond Snack claims top-selling status on leading e-commerce and quick-commerce platforms in India, leveraging digital channels to bypass traditional retail gatekeepers and reach younger, digitally native consumers. The brand's January 2025 Series A funding of USD 8.3 million, led by 12 Flags Group (founded by ex-Reckitt CEO Rakesh Kapoor), will support geographic expansion and supply-chain infrastructure, including backend integration and efficiency improvements within the agricultural value chain.

Supermarkets and hypermarkets face margin pressure from private-label competition and must allocate shelf space based on velocity and profitability, creating barriers for emerging brands. Haldiram, with ~20,000 retail outlets across India and exports to the USA, Europe, the Middle East, Australia, and Canada, exemplifies how scale and distribution reach enable broad market coverage. Online retail mitigates this risk by enabling long-tail assortments and personalized recommendations, though digital channels also amplify consumer access to imported and niche alternatives. Convenience stores benefit from high-traffic locations and extended operating hours, capturing on-the-go consumption occasions, while specialty stores command premiums for organic, Fair Trade, and artisanal products.

Geography Analysis

Asia-Pacific, which accounted for 43.22% of 2025 revenues, is projected to retain its dominant position in the banana chips market, with an anticipated CAGR of 8.42% through 2031. In 2024, Indonesia produced 9.26 million tons of bananas, exporting 26,240 tons to key markets such as Malaysia, Japan, and Singapore. At the same time, Indian processors are capitalizing on the domestic banana surplus to target GCC markets, as highlighted by BPS.GO.ID. The rising demand from China's growing middle class is evident, with the country importing 1.94 million tonnes of bananas in 2025. Additionally, local brands are increasingly utilizing e-commerce platforms to penetrate tier-2 cities and cater to the Southeast Asian diaspora, thereby expanding their market reach.

Conversely, North America and Europe are experiencing mid-single-digit growth, constrained by higher import costs and saturated snack aisles. The European Union is expected to see a 16.3% decline in banana production in 2025, with output projected to fall to 566,592 tonnes[3]Source: European Commission, “EU Banana Market,” europa.eu. Spain, the largest banana producer in the EU, is forecast to witness a substantial 24% reduction in production volumes. This decline is accompanied by a significant rise in farm-gate prices, which are expected to increase from EUR 0.84-0.89/kg in 2024 to EUR 1.14-1.25/kg in 2025, further impacting the market dynamics.

South America, the Middle East, and Africa collectively represent less than 20% of the current demand for banana chips but are experiencing faster volume growth, driven by urbanization and the expansion of modern retail infrastructure. Haldiram's planned factory in the UAE is a strategic move aimed at reducing freight costs and catering to the Gulf's expatriate populations. Despite challenges such as infrastructure deficiencies and fragmented regulatory frameworks, processors in India and Ecuador are well-positioned to scale up exports. This growth is supported by competitive FOB pricing and the ongoing development of cold-chain networks, which are expected to enhance supply chain efficiency and market accessibility.

Competitive Landscape

The banana chips market exhibits moderate consolidation. Dominating the market are key players such as PepsiCo, Haldiram, and Dole. At the same time, emerging disruptors like Beyond Snack are gaining traction by adopting digital-first approaches and emphasizing clean-label products. In April 2025, Haldiram executed a significant merger, combining its Delhi and Nagpur operations to create a USD 1.55 billion entity. This merger not only solidified Haldiram's position in the market but also secured a 40% share of India's organized snacks segment, enhancing its procurement and distribution capabilities.

Additionally, PepsiCo's reformulation of Lay’s using olive oil reflects a broader industry trend, signaling a potential shift in consumer expectations for banana chips and other snack categories. Adopting advanced technology is emerging as a critical differentiator in the market. For instance, vacuum heat-pump drying technology is gaining prominence for its ability to retain nutrients and maintain the natural color of banana chips, offering a premium appeal to baked product lines. Furthermore, companies are strengthening their intellectual property by developing patent portfolios focused on antioxidative dipping techniques and puree stabilization, which are instrumental in controlling oxidation.

Established players are increasingly integrating backward into raw material sourcing and forward into omnichannel sales strategies to enhance operational efficiency. On the other hand, newer entrants, often supported by venture capital, are prioritizing brand storytelling, showcasing strong environmental, social, and governance (ESG) credentials, and rapidly innovating with new flavors to capture consumer interest.

Banana Chips Industry Leaders

-

Beyond Snack

-

Seeberger GmbH

-

Traina Foods

-

Celebes Coconut Corporation

-

Four Seasons Dry Fruit Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Super Munchies brand launched a new range of banana chip flavors in India. The flavors include Classic Salted, Flamin' Hot, Sweet and Sour, and Thai Chili. The products are made without any artificial flavors or preservatives.

- April 2025: In collaboration with the movie Pushpa 2, Beyond Snack launched the ‘Flower Nahi Fire’ banana chips, featuring a bold and spicy flavor profile that pays homage to the popular film. This is India’s first movie-themed banana chip flavor, capturing attention through vibrant branding and intense spices.

- March 2024: Pukpip launched ‘Real Banana Bites’—frozen banana slices dipped in milk chocolate, dark chocolate, or peanut butter. With an emphasis on real fruit and upcycled bananas, this product caters to both indulgence and sustainability trends, offering vegan-friendly options and tapping into the frozen snack segment.

Global Banana Chips Market Report Scope

| Fried Chips |

| Baked Chips |

| Salted |

| Sweet |

| Spiced |

| Others |

| Organic |

| Conventional |

| Supermarkets/Hypermarkets |

| Convenience Stores |

| Specialty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Vietnam | |

| Indonesia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Peru | |

| Colombia | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| Product Type | Fried Chips | |

| Baked Chips | ||

| Flavor | Salted | |

| Sweet | ||

| Spiced | ||

| Others | ||

| Nature | Organic | |

| Conventional | ||

| Distribution Channels | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Specialty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Peru | ||

| Colombia | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the banana chips market be by 2031?

The banana chips market size is forecast to reach USD 2.76 billion by 2031, rising at a 7.28% CAGR from 2026-2031

Which region will post the fastest growth?

Asia-Pacific is projected to expand at an 8.42% CAGR through 2031, supported by plentiful raw materials and robust domestic demand

What product type is gaining momentum among health-minded consumers?

Baked banana chips are advancing at an 8.21% CAGR as lower-fat processing technologies gain traction

How significant is online retail for banana chips?

Online channels are the fastest-growing distribution avenue at 8.58% CAGR, driven by quick-commerce and subscription models.

Page last updated on: