U.S. Medical Tubing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

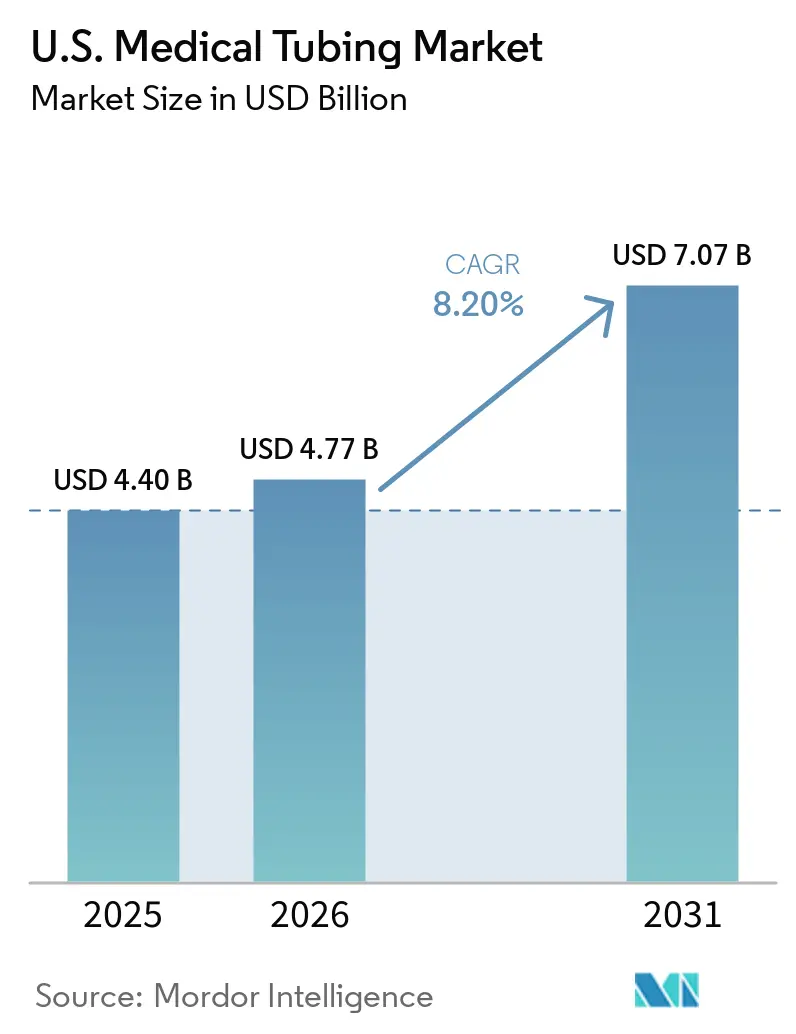

| Base Year Market Size (2025) | USD 4.40 Billion |

| Market Size (2026) | USD 4.77 Billion |

| Market Size (2031) | USD 7.07 Billion |

| Growth Rate (2026 - 2031) | 8.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Medical Tubing Market Analysis by Mordor Intelligence

The U.S. Medical Tubing Market size is expected to grow from USD 4.40 billion in 2025 to USD 4.77 billion in 2026 and is forecast to reach USD 7.07 billion by 2031 at 8.20% CAGR over 2026-2031.

The United States medical tubing market is growing due to three overlapping demand cycles driving both replacement and new unit demand across the care pathway. Growth is supported by increased catheter-based procedures in structural heart and electrophysiology, a shift of infusion therapy to home and ambulatory settings, and a reformulation cycle linked to PFAS review and substitution. These trends are driving demand for tighter tolerances, complex tubing designs, and broader qualification support, pushing value growth beyond procedure counts. The competitive landscape is becoming more dynamic as established specialists invest in proprietary material systems, while mid-sized manufacturers enhance extrusion, cleanroom, and regulatory capabilities to secure development programs.

Key Report Takeaways

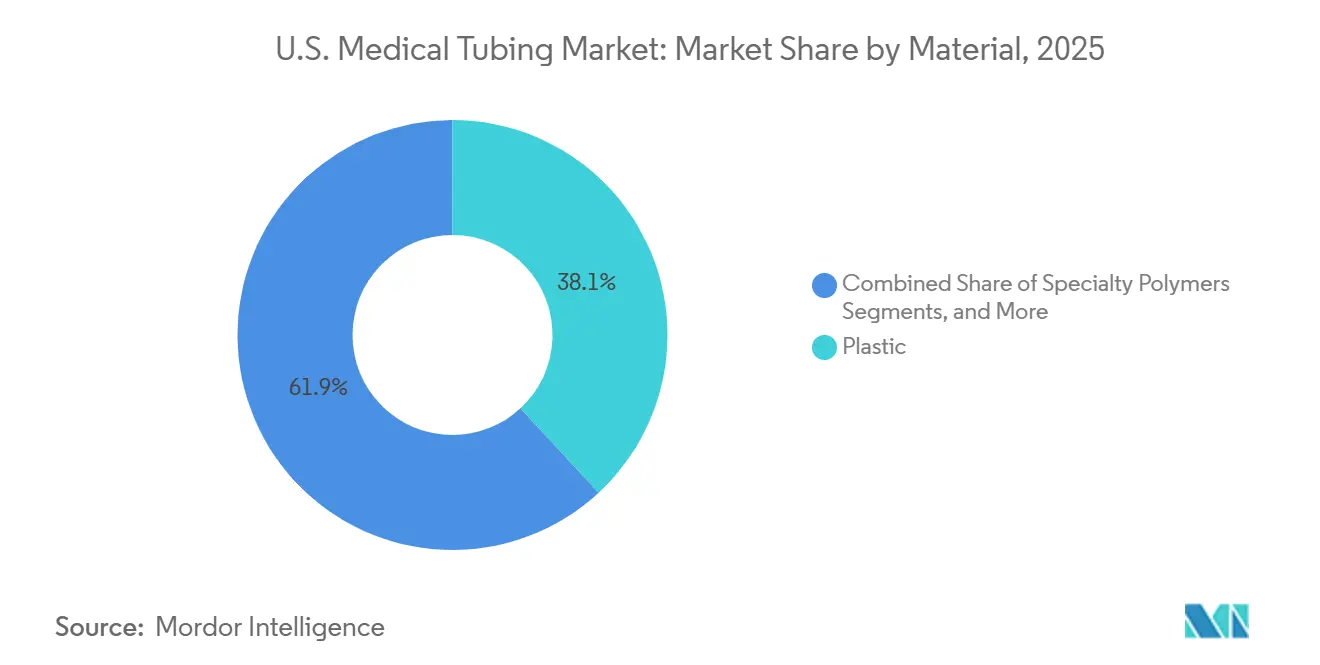

- By material, plastic tubing held 38.12% of the U.S. medical tubing market share in 2025, while specialty polymers are projected to grow at a 10.18% CAGR through 2031.

- By structure, single-lumen tubing accounted for 40.25% of the U.S. medical tubing market size in 2025, while micro-extruded and microbore tubing are projected to expand at a 10.75% CAGR through 2031.

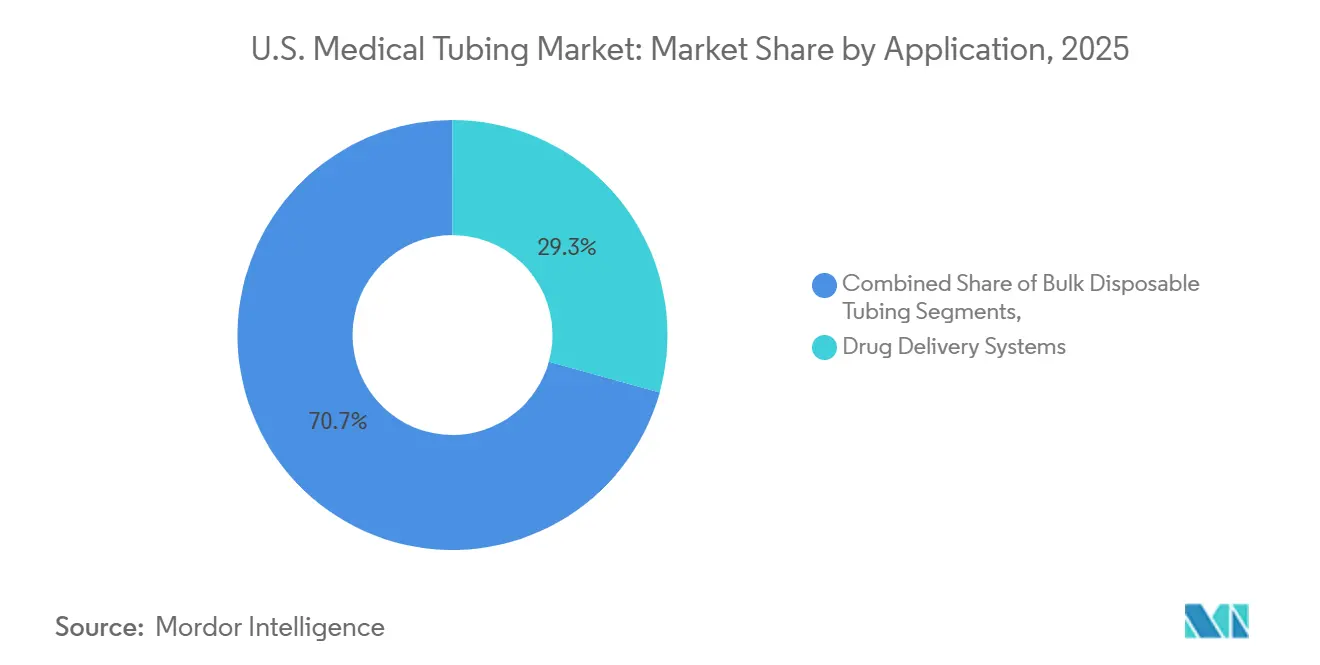

- By application, drug delivery systems represented 29.31% of the U.S. medical tubing market size in 2025, while suction, smoke evacuation, and drainage tubing are expected to advance at a 9.45% CAGR through 2031.

- By end user, hospitals and integrated delivery networks held 52.68% of the U.S. medical tubing market share in 2025, while home care is projected to grow at a 9.34% CAGR through 2031.

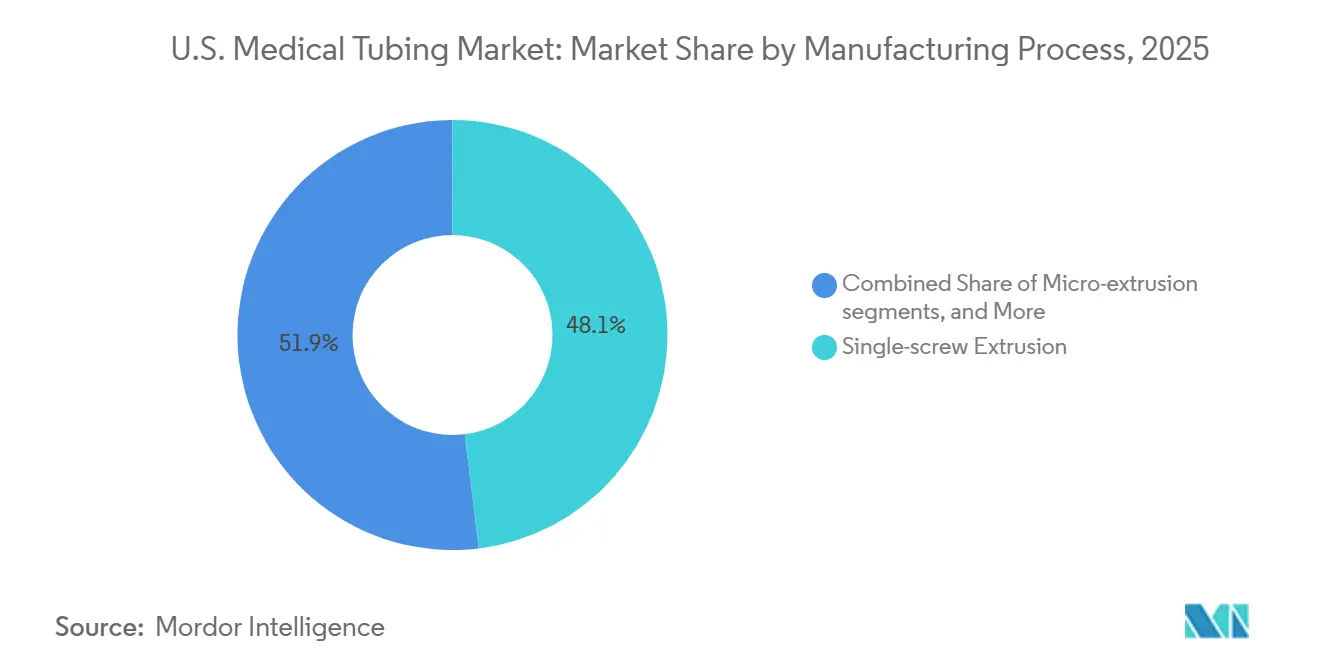

- By manufacturing process, single-screw extrusion captured 48.05% of production volume in 2025, while micro-extrusion is projected to record a 10.51% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Medical Tubing Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising minimally invasive and catheter-based procedure volumes | +2.3% | National, concentrated in major cardiac and electrophysiology centers across the Northeast, Midwest, and South | Medium term (2-4 years) |

| Higher single-use tubing demand from infection control and care settings | +1.4% | National | Short term (≤ 2 years) |

| Aging chronic-care population lifting dialysis, cardiovascular, and home care tubing demand | +1.1% | National, with early intensity in Sun Belt states | Long term (≥ 4 years) |

| Home infusion and ambulatory care migration expanding pump and fluid-transfer tubing demand | +0.9% | National, with gains in Northeast and Southeast ambulatory corridors | Medium term (2-4 years) |

| PFAS-free liner substitution cycle creating redesign-driven replacement volume | +0.7% | National, with spillover regulatory influence from EU REACH proposals affecting export-oriented manufacturers | Medium term (2-4 years) |

| Electrophysiology and structural-heart device scaling increasing demand for high-performance catheter tubing | +0.6% | National, centered on major cardiac surgery and electrophysiology lab networks | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Minimally Invasive and Catheter-Based Procedure Volumes

The United States medical tubing market is experiencing significant growth, driven by the transition from open surgeries to catheter-based interventions. Transcatheter aortic valve replacements have exceeded 100,000 annual procedures, while mitral transcatheter edge-to-edge repairs have surpassed 15,000 cases annually.[1]Contemporary Operator Procedural Volumes and Outcomes for TAVR and MTEER in the US,” PubMed Central, pmc.ncbi.nlm.nih.gov This increase in structural heart procedures is reshaping demand, as modern catheter systems require advanced designs with tighter tolerances, thinner walls, and layered shaft constructions. These advancements are driving demand for premium catheter liners, reinforced shafts, and multi-material tubing. Additionally, the expansion of ambulatory surgical centers is diversifying procurement channels, creating opportunities for more suppliers to enter the market.

Higher Single-Use Tubing Demand from Infection Control and Care Settings

Rising infection control requirements across inpatient, outpatient, and procedural settings are boosting demand for single-use tubing. Pre-sterilized and disposable tubing assemblies align with risk reduction protocols and reduce the burden of reprocessing. This shift increases replacement frequency, accelerating the refresh cycle for administration sets, pump tubing, and sterile fluid-transfer assemblies. The FDA's updated quality framework further supports this trend by emphasizing risk management and process control for device manufacturers.

Aging Chronic-Care Population Lifting Dialysis, Cardiovascular, and Home Care Tubing Demand

The growing chronic disease burden in the United States is driving demand for medical tubing in dialysis, cardiovascular care, and home-based therapies. Each setting has unique material and dimensional requirements, ensuring broad product demand. Dialysis tubing requires specific performance profiles, cardiovascular applications have distinct needs, and home infusion therapy relies on pump tubing, IV sets, and enteral feeding assemblies. This ongoing utilization tied to continuous care ensures steady demand. The National Home Infusion Association's March 2026 report highlights home infusion's growing impact across outpatient, home, and ambulatory care channels, supporting tubing volume growth through the forecast period.[2]NHIA Releases Infusion Industry Trends Report,” National Home Infusion Association, nhia.org

Home Infusion and Ambulatory Care Migration Expanding Pump and Fluid-Transfer Tubing Demand

The shift of infusion therapy to ambulatory centers and home settings is reshaping purchasing dynamics in the United States medical tubing market. As care moves away from hospital outpatient departments, purchasing decisions now emphasize flexibility, service levels, and qualification support. This shift creates opportunities for specialized tubing manufacturers capable of catering to smaller lot sizes and faster response times. Additionally, payer-driven transitions of oncology, immunology, and anti-infective infusions to cost-effective care sites are expanding demand for pump tubing and single-use fluid-transfer products. The National Home Infusion Association's 2026 industry update underscores home infusion's growing role in the infusion care model.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| FDA biocompatibility and extractables characterization burden on tubing development timelines | -0.8% | National, with compliance factors applying across all U.S. manufacturing and distribution sites | Medium term (2-4 years) |

| Volatility in medical-grade silicone, PVC, fluoropolymer, and specialty material pricing | -0.6% | National, with upstream feedstock concentration creating localized supply risk | Short term (≤ 2 years) |

| Pfas phase-down forces revalidation of catheter liner formulations and manufacturing processes | -0.5% | National, with heightened risk for manufacturers supplying EU markets in parallel | Medium term (2-4 years) |

| QMSR, connector compatibility, and DEHP-related redesign costs slow product development cycles | -0.4% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FDA Biocompatibility and Extractables Characterization Burden

In the U.S. medical tubing market, biocompatibility and extractables assessments pose significant challenges for product developers. The FDA's alignment with ISO 10993 standards has intensified the toxicological reviews and material assessments for tubing, especially those used in drug delivery, dialysis, and infusion.[3]“PFAS in Medical Devices,” U.S. Food and Drug Administration, fda.gov New polymer designs, lacking the extensive usage history of established PVC or silicone systems, face heightened scrutiny. This not only extends development timelines but also hampers the transition from prototype to commercial production. Furthermore, the Federal Register's rulemaking on QMSR introduces additional design-control and documentation mandates, further delaying the entry of new tubing designs into regulated production.

Volatility in Medical-Grade Silicone, PVC, Fluoropolymer, and Specialty Material Pricing

The U.S. medical tubing industry is feeling the pinch of material cost fluctuations, impacting both profit margins and strategic planning. This pricing uncertainty is particularly challenging as tubing manufacturers often finalize commitments to customer programs before fully grasping the trajectory of feedstock costs. The challenge spans multiple material families: silicone, PVC, fluoropolymers, and various specialty polymers can all experience supply disruptions or price shifts at different times. Notably, fluoropolymer sourcing has become increasingly delicate, with supplier concentration tightening due to the exit of prominent producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Specialty Polymers Lead the Innovation Cycle

Specialty polymers are the fastest-growing material segment in the United States medical tubing market, with a projected CAGR of 10.18% from 2026 to 2031. Advanced catheter and drug delivery designs increasingly require properties that commodity materials cannot consistently provide. Materials like PEBA, PEEK, and thermoplastic polyurethane are preferred for tighter dimensional control, enhanced kink resistance, and superior chemical stability. This shift is most significant in vascular, neurovascular, and minimally invasive applications, where tubing performance directly impacts device handling.

In 2025, plastic tubing held a 38.12% share of the United States medical tubing market, reflecting its strong presence in high-volume disposable and IV administration applications. PVC remains popular due to its cost efficiency, processability, and extensive biocompatibility documentation. Rubber tubing, led by silicone and latex-based formats, is essential in peristaltic pump systems, respiratory circuits, and long-duration drainage applications.

By Structure: Single-lumen Dominance Supports Mass-Volume Production

Single-lumen tubing accounted for 40.25% of the United States medical tubing market in 2025, making it the largest structural format. Its simplicity suits bulk applications like IV sets and catheter shafts, ensuring production efficiency and compatibility with conventional extrusion platforms. This structure remains integral to fluid management products widely used in hospitals and ambulatory settings. Single-lumen tubing continues to dominate due to its broad demand and recurring replacement volumes.

Micro-extruded and microbore tubing is the fastest-growing structural segment, with a 10.75% CAGR from 2026 to 2031. This growth is driven by catheter miniaturization in neurovascular access and robotic-assisted systems, where smaller profiles enhance navigation and outcomes. Multi-lumen and co-extruded tubing are also gaining traction as advanced catheter shafts integrate multiple functionalities. Zeus highlighted this trend in January 2026 with the launch of the PFX platform and PFX Flex Sub-Lite-Wall, designed for modern catheter construction.

By Application: Drug Delivery Leads, Drainage Tubing Accelerates

Drug delivery systems represented 29.31% of the United States medical tubing market in 2025, driven by IV therapy, infusion pump cassettes, and specialty delivery catheters. These applications demand biocompatibility, stable extractables profiles, and precise dimensional control. The growing home infusion channel is expanding the demand base as more patients receive biologics and specialty infusions outside hospitals. This trend broadens the market footprint without shifting demand away from traditional care settings.

Suction, smoke evacuation, and drainage tubing is the fastest-growing application segment, with a 9.45% CAGR from 2026 to 2031. The rise in minimally invasive surgeries and robotic-assisted procedures is increasing the need for controlled smoke evacuation and fluid management. Biopharmaceutical laboratory tubing, though smaller in volume, remains a high-value niche due to single-use bioprocessing infrastructure and stricter manufacturing standards. Other segments like catheters, dialysis tubing, and respiratory systems continue to diversify the market with distinct material and dimensional needs.

By End User: Hospital Networks Consolidate Procurement, Home Care Accelerates

Hospitals and integrated delivery networks held 52.68% of the United States medical tubing market share in 2025, reflecting their dominance in high-complexity procedures and disposable consumption. Centralized purchasing through group structures ensures volume visibility, even amid competitive pricing. Hospital demand anchors tubing programs tied to IV administration, catheterization, and procedural care, maintaining its leading position in the market.

Home care is the fastest-growing end-user segment, with a 9.34% CAGR from 2026 to 2031. The shift of infusion therapy, dialysis, and enteral feeding into home settings is driving recurring tubing use in cost-effective care environments. Ambulatory surgical centers are also expanding as more procedures move out of hospital outpatient departments. Physician offices and specialty clinics see steady growth, while laboratories and biopharmaceutical facilities remain smaller but high-value segments due to specialized tubing needs.

By Manufacturing Process: Micro-extrusion Captures High-Precision Segment Growth

Micro-extrusion is the fastest-growing manufacturing process in the United States medical tubing market, with a 10.51% CAGR from 2026 to 2031. Rising demand for precise internal diameters and wall thicknesses in catheter programs drives this growth. Manufacturers with validated micro-extrusion operations and expertise in materials like PEBA and PEEK gain a competitive edge, ensuring pricing resilience and market leadership.

Single-screw extrusion accounted for 48.05% of production volume in 2025, highlighting its role in large-scale output for PVC and polyolefin programs. Twin-screw extrusion is gaining importance in specialty compounding, ensuring better mixing of additives for high-performance formulations. The industry is evolving with a layered manufacturing mix, where legacy platforms and high-precision technologies coexist to meet diverse market demands.

Geography Analysis

The United States medical tubing market operates nationally, but demand, innovation, and production are concentrated in specific regional hubs. The Northeast, particularly the Boston, New York, and Philadelphia corridor, combines academic medical centers, integrated delivery networks, and a strong biopharma presence. This drives demand for drug delivery tubing, catheter components, and laboratory processing tubing in clinical and manufacturing settings.

The South and Southeast are emerging as significant manufacturing hubs and fast-growing procedural markets. Zeus, a leading catheter tubing and liner specialist, is headquartered in Orangeburg, South Carolina, with multiple facilities supporting catheter OEMs nationwide. RAUMEDIC’s operations in Mills River, North Carolina, enhance the region's profile as a cleanroom-based production hub for customized tubing and molded components.

The Midwest remains vital due to its concentration of medical device OEMs and established catheter assembly and extrusion capabilities. Minneapolis exemplifies this, hosting major device manufacturers whose R&D programs sustain demand for precision tubing and assembly services. Spectrum Plastics Group, now part of DuPont, has expanded its Minneapolis operations with catheter assembly capabilities, reinforcing the region's role in high-value tubing programs.

Competitive Landscape

The United States medical tubing market is moderately fragmented, with a layered structure rather than a dominant player scenario. Zeus Company LLC and Spectrum Plastics Group, now part of DuPont, lead as vertically integrated specialists with expertise in material science and extensive platform reach. Surrounding them are precision extruders and contract manufacturers competing on responsiveness, regulatory capabilities, and process specialization.

Strategy in the market is increasingly driven by material positioning and processing expertise. Zeus’s January 2026 launch of the PFX platform and PFX Flex Sub-Lite-Wall highlights its shift from film-cast PTFE in catheter programs to a non-fluorinated liner with thermoplastic bonding capabilities. In March 2026, Zeus expanded its PTFE liner and heat-shrink product offerings, enabling faster sourcing for catheter engineers. DuPont’s healthcare manufacturing expansion in Costa Rica in June 2025 strengthened its medical tubing and sterile packaging capacity for the Americas.

Opportunities are strongest in surface-engineered tubing, sensor-ready constructions, and low-impact material systems compatible with existing qualification pathways. OEMs seek tubing that reduces secondary coating steps, supports embedded sensing, and simplifies compliance without compromising performance. This demand creates space for suppliers combining material innovation with manufacturability and regulatory expertise.

U.S. Medical Tubing Industry Leaders

Compagnie de Saint-Gobain S.A.

Freudenberg Medical, LLC

Nordson Corporation

Zeus Company LLC

Spectrum Plastics Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Zeus Company LLC partnered with Chamfr to expand catheter component distribution, offering over 100 PTFE liner and heat-shrink products for OEM customers.

- April 2026: Freudenberg Medical opened a new ISO Class 5 cleanroom in Kaiserslautern, Germany, to support pre-sterilized single-use assemblies for biopharmaceutical clients.

- February 2026: The FDA implemented QMSR, replacing the 1996 Quality System Regulation with a framework aligned to ISO 13485:2016 for U.S. medical tubing manufacturers.

- January 2026: Zeus Company LLC launched the PFX platform, introducing PFX Flex Sub-Lite-Wall, a non-fluorinated catheter liner compatible with thermoplastic bonding and advanced sterilization methods.

- August 2025: The FDA confirmed the safety of fluoropolymers like PTFE and FEP in medical devices, citing no need for usage restrictions based on an independent review.

U.S. Medical Tubing Market Report Scope

As per the scope of the report, Medical tubing is highly specialized, sterile, and biocompatible piping designed to safely transport fluids, gases, or medical instruments within the human body or in clinical environments. It is a critical component in healthcare, rigorously manufactured to meet exact standards for safety and flexibility.

The U.S. medical tubing market is segmented by material, structure, application, end-user, and manufacturing process. By material, the market includes plastic, rubber, and specialty polymers. By structure, the market is segmented into single-lumen tubing, multi-lumen tubing, co-extruded/multi-layer tubing, tapered/bump tubing, braided/reinforced tubing, balloon tubing, heat-shrink tubing, and micro-extruded/microbore tubing. By application, the market is categorized into bulk disposable tubing, catheters & cannulae, drug delivery systems, dialysis & renal care tubing, IV infusion & fluid administration tubing, respiratory, anesthesia & gas supply tubing, enteral feeding & gastrointestinal tubing, suction, smoke evacuation & drainage tubing, biopharmaceutical laboratory & processing tubing, and peristaltic pump tubing. By end-user, the market is segmented into hospitals & integrated delivery networks, ambulatory surgical centers, physician offices & specialty clinics, home care settings, and medical laboratories & biopharmaceutical facilities. By manufacturing process, the market includes single-screw extrusion, twin-screw extrusion, micro-extrusion, co-extrusion/multi-layer extrusion, braiding, coiling & secondary shaft reinforcement, and heat-shrink & reflow processing. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Plastic |

| Rubber |

| Specialty Polymers |

| Single-lumen Tubing |

| Multi-lumen Tubing |

| Co-extruded / Multi-layer Tubing |

| Tapered / Bump Tubing |

| Braided / Reinforced Tubing |

| Balloon Tubing |

| Heat-shrink Tubing |

| Micro-extruded / Microbore Tubing |

| Bulk Disposable Tubing |

| Catheters & Cannulae |

| Drug Delivery Systems |

| Dialysis & Renal Care Tubing |

| IV Infusion & Fluid Administration Tubing |

| Respiratory, Anesthesia & Gas Supply Tubing |

| Enteral Feeding & Gastrointestinal Tubing |

| Suction, Smoke Evacuation & Drainage Tubing |

| Biopharmaceutical Laboratory & Processing Tubing |

| Peristaltic Pump Tubing |

| Hospitals & Integrated Delivery Networks |

| Ambulatory Surgical Centers |

| Physician Offices & Specialty Clinics |

| Home Care Setting |

| Medical Laboratories & Biopharmaceutical Facilities |

| Single-screw Extrusion |

| Twin-screw Extrusion |

| Micro-extrusion |

| Co-extrusion / Multi-layer Extrusion |

| Braiding, Coiling & Secondary Shaft Reinforcement |

| Heat-shrink & Reflow Processing |

| By Material | Plastic |

| Rubber | |

| Specialty Polymers | |

| By Structure | Single-lumen Tubing |

| Multi-lumen Tubing | |

| Co-extruded / Multi-layer Tubing | |

| Tapered / Bump Tubing | |

| Braided / Reinforced Tubing | |

| Balloon Tubing | |

| Heat-shrink Tubing | |

| Micro-extruded / Microbore Tubing | |

| By Application | Bulk Disposable Tubing |

| Catheters & Cannulae | |

| Drug Delivery Systems | |

| Dialysis & Renal Care Tubing | |

| IV Infusion & Fluid Administration Tubing | |

| Respiratory, Anesthesia & Gas Supply Tubing | |

| Enteral Feeding & Gastrointestinal Tubing | |

| Suction, Smoke Evacuation & Drainage Tubing | |

| Biopharmaceutical Laboratory & Processing Tubing | |

| Peristaltic Pump Tubing | |

| By End User | Hospitals & Integrated Delivery Networks |

| Ambulatory Surgical Centers | |

| Physician Offices & Specialty Clinics | |

| Home Care Setting | |

| Medical Laboratories & Biopharmaceutical Facilities | |

| By Manufacturing Process | Single-screw Extrusion |

| Twin-screw Extrusion | |

| Micro-extrusion | |

| Co-extrusion / Multi-layer Extrusion | |

| Braiding, Coiling & Secondary Shaft Reinforcement | |

| Heat-shrink & Reflow Processing |

Key Questions Answered in the Report

How large is the U.S. medical tubing market in 2026 and where is it heading by 2031?

The U.S. medical tubing market stands at USD 4.77 billion in 2026 and is projected to reach USD 7.07 billion by 2031, growing at an 8.20% CAGR.

What is driving demand for medical tubing in the United States?

Demand is being lifted by higher catheter-based procedure volumes, growth in home infusion, expansion of ambulatory care, and redesign activity tied to PFAS review and material substitution.

Which material category is growing the fastest?

Specialty polymers are the fastest-growing material segment, with a 10.18% CAGR from 2026 to 2031, supported by the need for tighter tolerances and higher performance in advanced catheter systems.

Which application area holds the largest revenue share?

Drug delivery systems led with a 29.31% share in 2025, reflecting the scale of IV therapy, infusion pump systems, and specialty drug administration across U.S. care settings.

Which end-user group accounts for the largest share of demand?

Hospitals and integrated delivery networks held 52.68% share in 2025 because they concentrate high-complexity procedures, catheter-intensive specialties, and large disposable consumption volumes.

Why is micro-extrusion becoming more important in catheter tubing?

Micro-extrusion is projected to grow at a 10.51% CAGR through 2031 because many catheter programs now require very small diameters and thin walls that standard extrusion platforms cannot consistently deliver.

Page last updated on: