Healthcare Fluid Connectors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

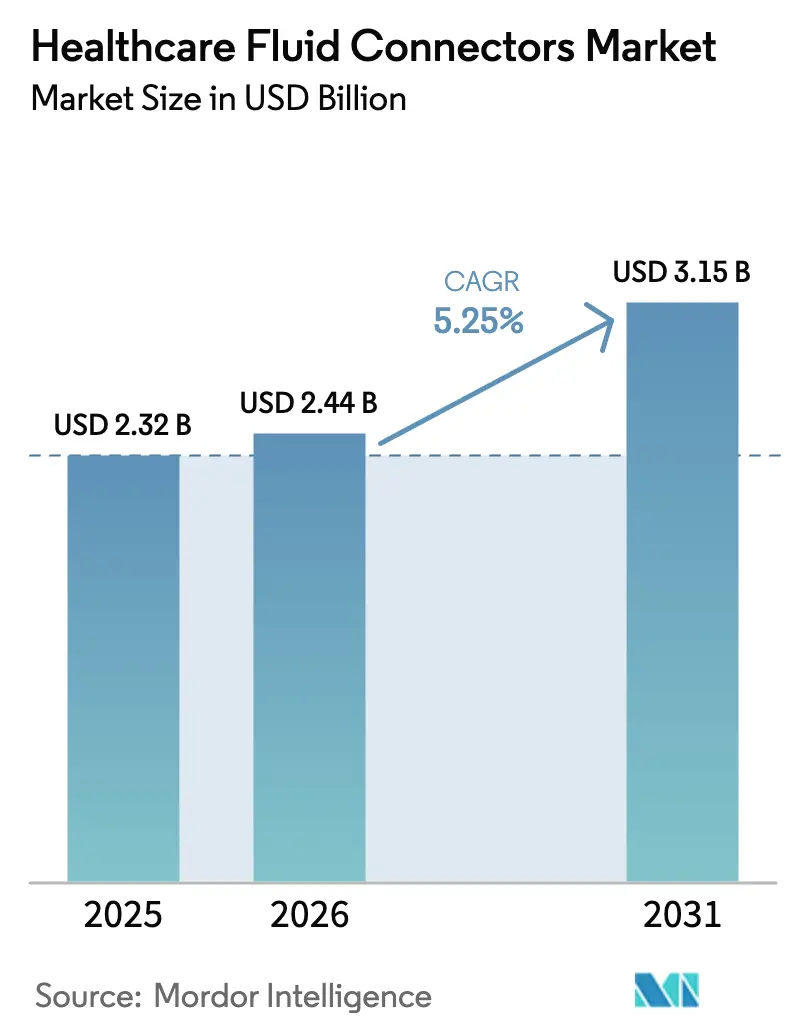

| Market Size (2026) | USD 2.44 Billion |

| Market Size (2031) | USD 3.15 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

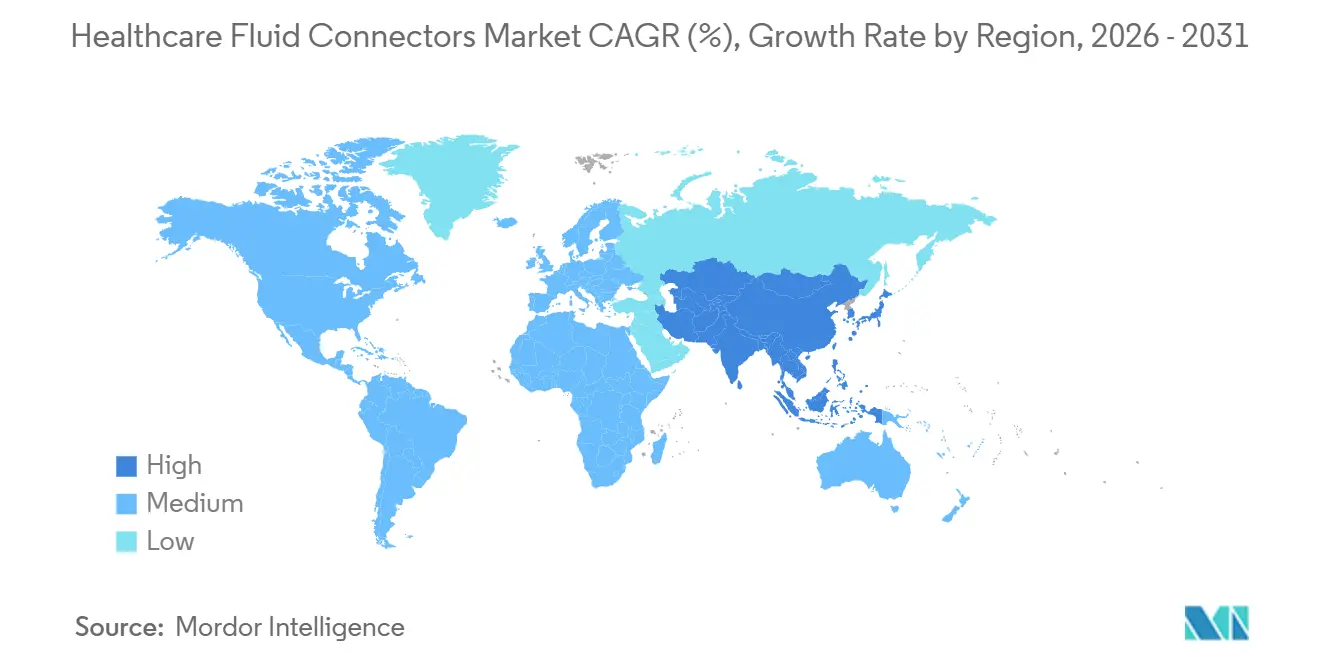

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

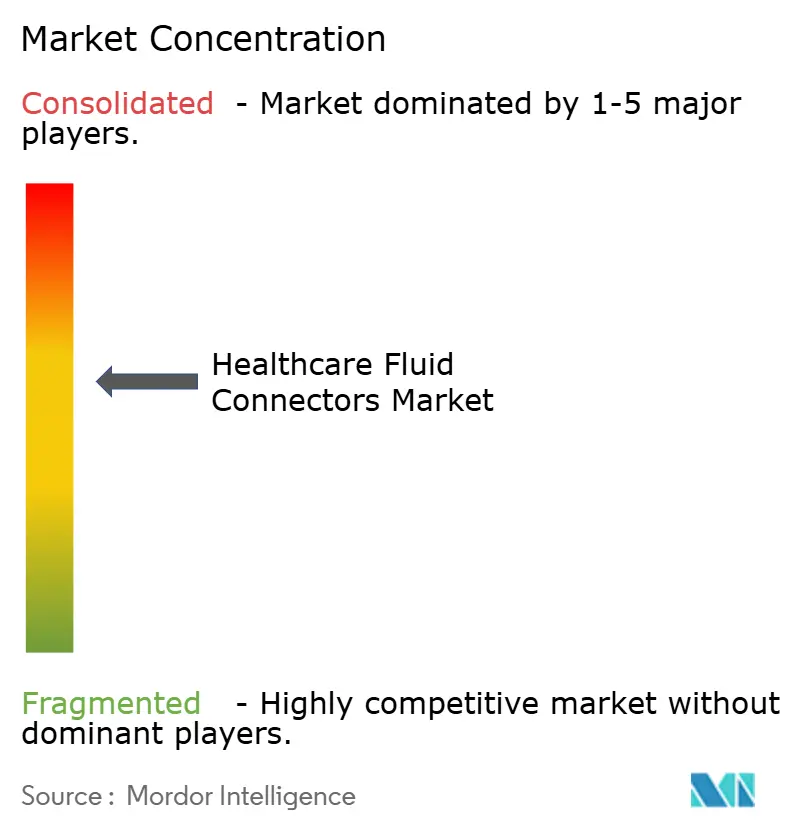

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Fluid Connectors Market Analysis by Mordor Intelligence

The Healthcare Fluid Connectors Market size is expected to increase from USD 2.32 billion in 2025 to USD 2.44 billion in 2026 and reach USD 3.15 billion by 2031, growing at a CAGR of 5.25% over 2026-2031.

Rising biologics output, accelerating adoption of closed-system transfer devices, and payer-led migration of infusion services to lower-acuity sites are driving steady unit growth even as group-purchasing organizations (GPOs) cap annual price increases at 2-3%. Suppliers that completed ISO 80369 redesign work by 2025 now benefit from first-mover access to hospital tenders that specify compliant connectors, a competitive edge magnified by the fact that each ISO update triggers 18-24-month revalidation cycles for lagging portfolios[1]U.S. Food and Drug Administration, “MedWatch Safety Information,” fda.gov. Material substitution is another pivot: thermoplastic elastomers (TPE) and bio-based PVC blends are displacing legacy PVC in premium SKUs because they meet phthalate-free mandates and survive 25-50 kGy gamma sterilization without embrittlement. Finally, quick-disconnect sterile fittings are scaling beyond biopharma plants into high-throughput cell-therapy suites, sharpening demand for connectors that guarantee aseptic transfer with minimal operator intervention.

Key Report Takeaways

- Needleless IV connectors commanded 37.55% of the 2025 healthcare fluid connectors market share, while quick-disconnect fittings are forecast to expand at a 6.25% CAGR through 2031.

- Hospitals generated 65.23% of 2025 revenue, yet clinics and specialty centers are set to grow 7.15% annually as payers steer infusion and chemotherapy away from high-cost inpatient settings.

- PVC retained a 41.15% material share in 2025, but thermoplastic elastomers will advance at an 8.51% CAGR on the back of ISO 10993-compliant, phthalate-free formulations that withstand high-dose gamma sterilization.

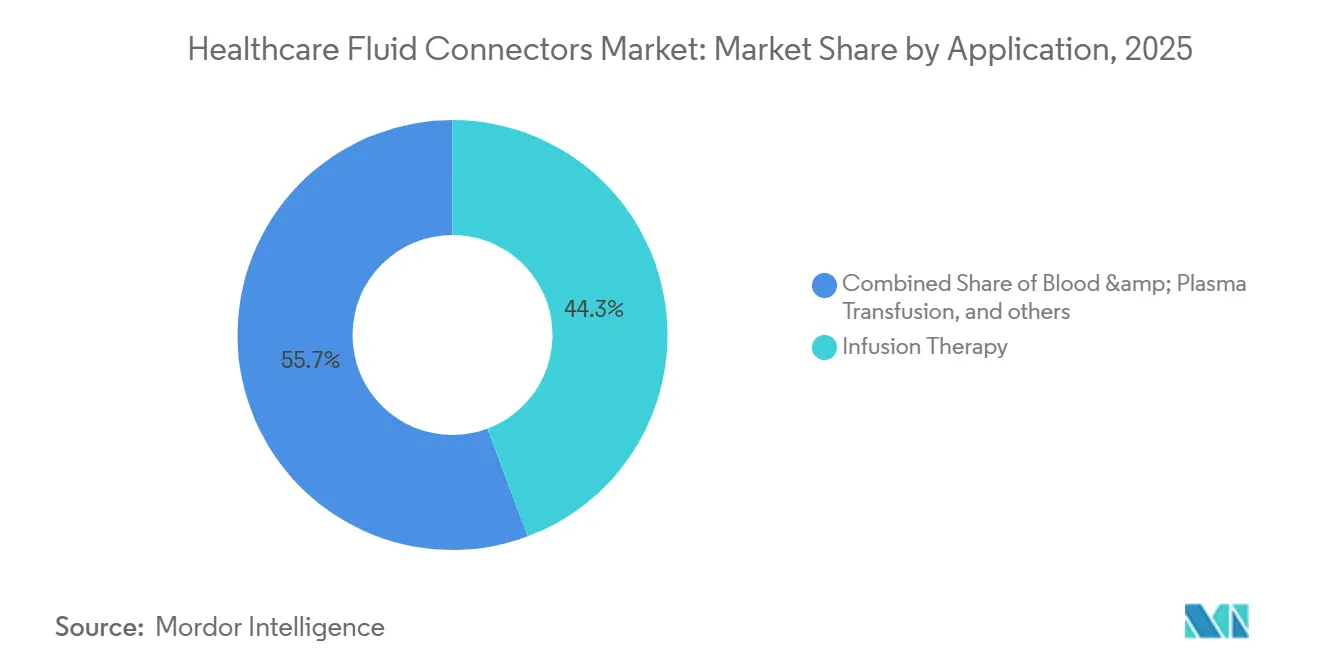

- Infusion therapy delivered 44.35% of 2025 application revenue, whereas drug-delivery and chemotherapy connectors are projected to grow 9.11% per year in response to USP <800> enforcement of closed-system transfer devices.

- North America accounted for 36.25% of revenue in 2025, though Asia-Pacific is projected to grow at an 8.02% CAGR as Healthy China 2030 funds 15,000 new community health centers equipped with ISO-compliant connector inventories.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Fluid Connectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Disease Prevalence Boosting IV Therapy Volumes | +1.2% | Global, with concentration in North America, Europe, and aging Asia-Pacific markets | Long term (≥ 4 years) |

| Regulatory Mandates for Needle-Free Safety Connectors | +0.9% | North America & EU, with spillover to APAC through ISO harmonization | Medium term (2-4 years) |

| Expansion of Minimally-Invasive & Home-Infusion Care | +1.1% | North America & EU core, emerging in urban APAC and Middle East | Medium term (2-4 years) |

| Digital-Ready Smart Connectors Enabling Closed-Loop IV Workflows | +0.6% | North America hospitals, pilot programs in EU and select APAC facilities | Long term (≥ 4 years) |

| Sustainability Goals Spurring PVC-Free Biocompatible Materials | +0.7% | EU regulatory push, North America voluntary adoption, limited APAC uptake | Long term (≥ 4 years) |

| Near-Shoring of Micro-Extrusion Capacity to Cut Supply-Chain Risk | +0.5% | North America & Mexico, EU reshoring from Asia, limited Middle East activity | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Disease Prevalence Boosting IV Therapy Volumes

Diabetes, cancer, and chronic kidney disease now affect more than 500 million people worldwide and require repeated infusions or dialysis sessions, each consuming multiple connectors per treatment episode[2]International Diabetes Federation, “IDF Diabetes Atlas,” idf.org. Between 2019 and 2024, home dialysis use in the United States rose from 12% to 18% of incident patients, translating into a monthly demand of 12-16 sterile connector sets per patient[3]U.S. Renal Data System, “Annual Data Report,” usrds.org. An aging demographic intensifies this pull: the global 65-plus cohort will double to 1.6 billion by 2050, and older adults consume three to four times more IV therapy than younger groups. For manufacturers, high procedure counts translate into structural volume growth, although pricing stays under pressure in cost-sensitive health systems. The workload also elevates infection-control stakes, reinforcing the need for connectors with proven microbiological barriers.

Regulatory Mandates for Needle-Free Safety Connectors

OSHA’s enforcement of the Needlestick Safety and Prevention Act obliges U.S. facilities to adopt engineering controls such as needleless valves, while the EU MDR accelerates a similar transition by forcing re-certification of legacy Luer-slip devices. ISO 80369-7, finalized in 2024, standardizes intravascular connector dimensions and compels suppliers to redesign valve springs and seals, a project that costs USD 0.5-1.5 million per product family and absorbs 18-24 months. Harmonization via the International Medical Device Regulators Forum is cascading into Japan, South Korea, and Australia, yet asynchronous rollouts require dual inventories, straining working-capital budgets. Early movers that completed retooling by 2025 now command premium bids in tenders that stipulate ISO-compliant connectors, while laggards scramble to avoid stockouts as the 2027 EU MDR cutoff approaches[4]European Commission, “Medical Device Regulation,” europa.eu.

Expansion of Minimally Invasive & Home-Infusion Care

Medicare’s 2024 Home Infusion Therapy benefit broadened reimbursement to antibiotic, immunoglobulin, and chemotherapy infusions, unlocking a USD 4.5 billion addressable pool and spurring a double-digit rise in outpatient admissions. Ambulatory surgery centers, which completed 28.6 million U.S. procedures in 2023, depend on single-use connector kits to streamline anesthesia and medication lines. In Australia, home dialysis penetration among kidney disease patients reached 31% in 2024, the highest rate among OECD members, demonstrating how government incentives can tilt modality choice. Connector OEMs, therefore, design color-coded, pictogram-guided kits that mitigate user error among non-clinical caregivers. Yet the migration also heightens exposure to infection risk: a 2024 study reported home-infusion bloodstream infection rates of 1.2 per 1,000 catheter-days, twice the hospital benchmark, underscoring the need for foolproof valved designs.

Sustainability Goals Spurring PVC-Free Biocompatible Materials

The EU Single-Use Plastics Directive imposes extended producer-responsibility fees of EUR 0.05-0.15 per connector, eroding margins on commodity SKUs and catalyzing interest in phthalate-free alternatives. Healthcare systems generate 5.9 million tons of plastic waste annually, with PVC accounting for 25% of that total; incineration releases regulated dioxins in 12 member states. TPE and TPU compounds meet ISO 10993 and withstand 50 kGy gamma doses, eliminating plasticizer migration risks that plague legacy PVC. Teknor Apex’s sugarcane-based PVC blend, rolled out in March 2024, reduces life-cycle carbon emissions by 22% while retaining USP Class VI certification. Adoption remains price-sensitive. 2025 surveys show only 9% of European hospitals have moved beyond neonatal units, yet the regulatory direction is unambiguous, and early adopters are negotiating green-procurement premiums with national health systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Multi-Jurisdictional Regulatory Burden & Approval Lags | -0.8% | Global, with highest friction in EU (MDR) and emerging APAC markets | Medium term (2-4 years) |

| GPO Price Pressure And Low-Cost Asian Competitors | -0.6% | North America GPO-dominated procurement, EU tender systems, price-sensitive APAC | Short term (≤ 2 years) |

| Rapid ISO 80369 Updates Causing Redesign & Obsolescence Cycles | -0.5% | Global, affecting all manufacturers with legacy Luer-lock portfolios | Short term (≤ 2 years) |

| Plastics-Waste Legislation Inflating Disposable-Device Costs | -0.4% | EU extended producer responsibility, select U.S. states, limited APAC enforcement | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Multi-Jurisdictional Regulatory Burden & Approval Lags

EU MDR clinical-evidence demands have stretched notified-body review times to 18-36 months, leaving 40% of legacy connector SKUs awaiting re-certification at the end of 2024. U.S. suppliers face a 12-18-month 510(k) cycle that costs USD 150,000-300,000 even for color changes, while India’s CDSCO and China’s NMPA require in-country testing, doubling validation spend for multi-region launches. Mexico eased pressure in 2026 by extending renewals to 10 years, but that relief is local. Small and mid-cap firms lacking global regulatory teams risk forced exits or distressed sales, effectively raising barriers to entry and nudging overall prices upward despite GPO bargaining power.

GPO Price Pressure and Low-Cost Asian Competitors

U.S. GPOs wield USD 84 billion in purchasing power and cap annual list-price hikes at 2-3%, compressing branded suppliers' gross margins by 400-600 basis points vs. direct channels. Multi-source awards funnel 60-70% of volume to the lowest-bid vendor, enabling Chinese manufacturers to undercut catalog prices by 20-30% and reach 18% share of U.S. connector imports in 2024. Western incumbents counter with antimicrobial coatings and RFID-enabled smart sets, but those features command only niche premiums. Cardinal Health has already divested one low-margin consumables line, signaling ongoing portfolio rationalization among branded players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Quick-Disconnect Fittings Extend Biologics Momentum

Quick-disconnect sterile fittings are forecast to post a 6.25% CAGR through 2031, outpacing the needleless mainstay that held a 37.55% 2025 healthcare fluid connectors market share. The surge stems from biologics and cell-therapy producers that favor single-use systems, eliminating cleaning validation. The AseptiQuik portfolio appears in 70% of monoclonal-antibody green-field builds commissioned during 2024-2025, illustrating the move toward standard hygienic designs that operators can connect and disconnect without the need for laminar-flow hoods. Needleless IV connectors remain the volume leader in the healthcare fluid connectors market because they are embedded in almost every hospital infusion protocol, yet pricing has commoditized under GPO frameworks and penetration exceeds 85% in U.S. acute-care facilities.

Growth prospects also brighten for micro-bore connectors used in minimally invasive cardiovascular and neurovascular cases, driven by ISO 80369-7 dimensional harmonization that finally allows cross-vendor mating. Y-connectors and manifolds will trail the overall healthcare fluid connectors market because infection-control teams now cap the number of access points per IV line, and recent infection-control studies link each additional junction to an 8% rise in bloodstream-infection risk.

By End-User: Clinics & Specialty Centers Capture Payer Migration

Hospitals accounted for 65.23% of 2025 revenue, but clinic and specialty-center lines will grow 7.15% annually as insurers redirect infusion, dialysis, and chemotherapy protocols to lower-acuity venues where costs run 40-60% below inpatient rates. The shift widens the installed base for lower-pressure connector models that standardize across multiple modalities and simplify cross-site training.

Home-health uptake adds a further catalyst. Medicare’s expanded benefit coverage now reimburses antibiotic, immunoglobulin, and oncology infusions in residential settings, pushing steady double-digit growth in home-infusion admissions and spawning demand for color-coded kits with pictorial instructions. Diagnostic labs and research institutes contribute to steady replacement cycles but remain a niche share of the overall healthcare fluid connectors market, largely mirroring pharmaceutical R&D budgets.

By Material: TPE and TPU Scale on Sustainability & Gamma Stability

PVC retained a 41.15% share in 2025 thanks to cost advantages and decades of tooling compatibility, yet its reliance on DEHP and other phthalates conflicts with rising scrutiny of toxic chemicals. TPE and TPU compounds are forecast to grow 8.51% annually because they pass ISO 10993 extracts testing, survive up to 50 kGy gamma sterilization without plasticizer bleed, and meet hospital “green procurement” checklists. As a result, premium neonatal and oncology connectors are already migrating to TPE, even though TPE costs USD 3.50-5.00 per kg, versus USD 1.20-1.50 for PVC.

Silicone remains the material of choice for neonatal feeding tubes where softness and transparency trump economics, while polyurethane enjoys niche traction in abrasion-prone ECMO circuits. Bio-based PVC and biodegradable PLA remain below 1% of the healthcare fluid connectors market size due to cost premiums and limited clinical validation, yet pilot programs in Germany show hospitals will pay for low-carbon SKUs if long-term contracts offset initial price gaps.

By Application: Chemotherapy Connectors Accelerate on USP <800>

Infusion therapy accounted for 44.35% of 2025 revenue, but drug-delivery and chemotherapy connectors will compound at 9.11% annually as USP <800> enforcement mandates closed-system transfer devices to prevent aerosol leaks during hazardous-drug admixture. Oncology-pharmacy upgrades favor connectors with integrated venting membranes and tamper-evident shut-off valves to buttress worker safety.

Blood and plasma connectors track a mature transfusion segment that grows only in line with population health needs, whereas dialysis connectors benefit from rising home-modality penetration in the United States, Japan, and Australia. Surgical-anesthesia connectors face volume headwinds as hospitals transition appropriate cases to ambulatory centers, yet microbore designs gain relevance in catheter-based valve repairs and neurointerventions. Respiratory connectors, elevated during the COVID-19 surge, will fall back to the general trajectory of mechanical-ventilation volumes over the forecast horizon.

U.S. GPOs wield USD 84 billion in purchasing power and cap annual list-price hikes at 2-3%, compressing branded suppliers' gross margins by 400-600 basis points vs. direct channels. Multi-source awards funnel 60-70% of volume to the lowest-bid vendor, enabling Chinese manufacturers to undercut catalog prices by 20-30% and reach 18% share of U.S. connector imports in 2024. Western incumbents counter with antimicrobial coatings and RFID-enabled smart sets, but those features command only niche premiums. Cardinal Health has already divested one low-margin consumables line, signaling ongoing portfolio rationalization among branded players.

Geography Analysis

North America will defend its 36.25% 2025 revenue lead on the back of high per-capita health spending, universal adoption of needleless connectors, and rising deployment of RFID-enabled smart sets that integrate with electronic health records. Growth, however, will lag the global average because penetration is mature and GPO contract ceilings restrain price uplift.

Asia-Pacific is forecast to expand at an 8.02% CAGR, the quickest pace among macro regions, fueled by China’s Healthy China 2030 plan to build 15,000 community health centers and India’s Ayushman Bharat insurance rollout that extends coverage to 500 million beneficiaries. Government procurement frameworks in both countries increasingly specify ISO-compliant small-bore connectors, a shift that favors multinationals already through redesign, even as domestic firms leverage cost advantages in commodity SKUs. Japan’s super-aging profile boosts home-dialysis adoption, while Australia leads OECD peers in home-infusion penetration, raising baseline connector demand.

Europe exhibits mixed momentum. Germany and France invest in digital-health infrastructure linking smart connectors to e-prescribing, yet southern states apply procurement austerity. EU MDR costs and extended producer-responsibility fees on PVC-based disposables are nudging hospitals toward green-labeled, yet pricier, TPE sets. The Middle East and Africa add opportunistic volume, primarily from GCC medical-tourism hubs upgrading to ISO-80369 conforming products, whereas Latin America experiences episodic restocking cycles tied to macro-currency swings, such as Argentina’s 2024 devaluation that cut import costs for USD-denominated devices by 40%.

Competitive Landscape

The top five suppliers, BD, ICU Medical, Baxter, B. Braun, and Terumo, collectively controlled a sizable share of 2025 revenue, yet specialty niches and regional tenders sustain a second tier of agile manufacturers. ICU Medical’s USD 2.4 billion acquisition of Smiths Medical in 2024 added 12,000 infusion-pump accounts to its cross-sell pool, strengthening negotiating clout with GPOs and biopharma clients. BD’s USD 30 million expansion of Utah extrusion capacity, completed in 2025, slashed U.S. customer lead times to four weeks, a decisive edge in sole-source negotiations with hospitals pursuing just-in-time inventory.

Technology differentiation is shifting toward informatics: BD’s Alaris pumps now pair with RFID-tagged connectors that verify drug-line compatibility in real time, cutting wrong-drug errors by 34% at pilot sites, yet only 15% of hospitals can integrate the feature because legacy pumps lack compatible firmware. Meanwhile, Qosina and Saint-Gobain Performance Plastics exploit 6-8-week custom-tooling cycles to win quick-disconnect contracts in biopharmaceutical plants, nibbling at incumbent share. ISO-80369 compliance serves as a moat; manufacturers that completed redesign ahead of the 2027 EU MDR deadline already win sole-source deals in Europe, while laggards face obsolescence or acquisition offers from compliance-ready rivals.

Healthcare Fluid Connectors Industry Leaders

B. Braun Melsungen AG

Baxter International Inc.

Becton, Dickinson and Company (BD)

Terumo Corporation

ICU Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: HAI Solutions received FDA De Novo classification for its QIKCAP System, a UVC-based adjunct that disinfects needle-free Luer connectors in situ.

- September 2025: ICU Medical obtained FDA 510(k) clearance for its next-generation Clave needle-free connector portfolio, which adds integrated flow-control features.

Global Healthcare Fluid Connectors Market Report Scope

As per the report's scope, healthcare fluid connectors are specialized components used to safely link tubing, catheters, and fluid‑handling devices within medical systems. They ensure secure, leak‑free transfer of liquids such as medications, nutrients, and diagnostic fluids. Designed for biocompatibility, sterility, and ease of use, these connectors support reliable performance across infusion, dialysis, surgical, and diagnostic applications.

The healthcare fluid connectors market segmentation includes product type, end-user, material, application, and geography. By product type, the market is segmented into needleless IV connectors, mechanical-valve connectors, Y-connectors & manifolds, tubing sets & extension lines, small-bore & micro connectors, and quick-disconnect fittings. By end-user, the market is segmented into hospitals, ambulatory surgical centers, home healthcare, clinics & specialty centers, and diagnostic & research labs. By material, the market is segmented into PVC, silicone, polyurethane, thermoplastic elastomers (TPE/TPU), metals & alloys, and other material. By application, the market is segmented into infusion therapy, blood & plasma transfusion, dialysis & renal care, drug-delivery & chemotherapy, surgical & anesthesia fluid management, and respiratory & critical-care fluids. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Needleless IV Connectors |

| Mechanical-Valve Connectors |

| Y-Connectors & Manifolds |

| Tubing Sets & Extension Lines |

| Small-Bore & Micro Connectors |

| Quick-Disconnect Fittings |

| Hospitals |

| Ambulatory Surgical Centers |

| Home Healthcare |

| Clinics & Specialty Centers |

| Diagnostic & Research Labs |

| PVC |

| Silicone |

| Polyurethane |

| Thermoplastic Elastomers (TPE/TPU) |

| Metals & Alloys |

| Other Material |

| Infusion Therapy |

| Blood & Plasma Transfusion |

| Dialysis & Renal Care |

| Drug-Delivery & Chemotherapy |

| Surgical & Anesthesia Fluid Management |

| Respiratory & Critical-Care Fluids |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Needleless IV Connectors | |

| Mechanical-Valve Connectors | ||

| Y-Connectors & Manifolds | ||

| Tubing Sets & Extension Lines | ||

| Small-Bore & Micro Connectors | ||

| Quick-Disconnect Fittings | ||

| By End-user | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home Healthcare | ||

| Clinics & Specialty Centers | ||

| Diagnostic & Research Labs | ||

| By Material | PVC | |

| Silicone | ||

| Polyurethane | ||

| Thermoplastic Elastomers (TPE/TPU) | ||

| Metals & Alloys | ||

| Other Material | ||

| By Application | Infusion Therapy | |

| Blood & Plasma Transfusion | ||

| Dialysis & Renal Care | ||

| Drug-Delivery & Chemotherapy | ||

| Surgical & Anesthesia Fluid Management | ||

| Respiratory & Critical-Care Fluids | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the healthcare fluid connectors market by 2031?

It is expected to reach USD 3.15 billion, reflecting a 5.25% CAGR from 2026 to 2031.

Which product category is growing fastest within healthcare fluid connectors?

Quick-disconnect sterile fittings, projected at a 6.25% CAGR through 2031 as biologics and cell-therapy plants favor single-use aseptic transfer.

Why are thermoplastic elastomers gaining traction in connector manufacturing?

TPE/TPU compounds eliminate phthalates, tolerate 50 kGy gamma sterilization, and align with EU sustainability fees, driving an 8.51% CAGR in the material segment.

How do regulatory changes affect connector suppliers?

ISO 80369 revisions and EU MDR evidence demands lengthen re-certification cycles to as much as 36 months, raising compliance costs and favoring early movers.

Which region will post the highest growth rate for healthcare fluid connectors?

Asia-Pacific, forecast at an 8.02% CAGR, buoyed by China’s community-health build-out and India’s expanded insurance coverage.

How are smart connectors reducing medication errors?

RFID-enabled sets pair with infusion pumps to verify drug compatibility and log connection times, cutting wrong-drug incidents by more than one-third in pilot hospitals.

Page last updated on: