Sterile Tubing Welder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.94 Billion |

| Market Size (2031) | USD 3.82 Billion |

| Growth Rate (2026 - 2031) | 5.39% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

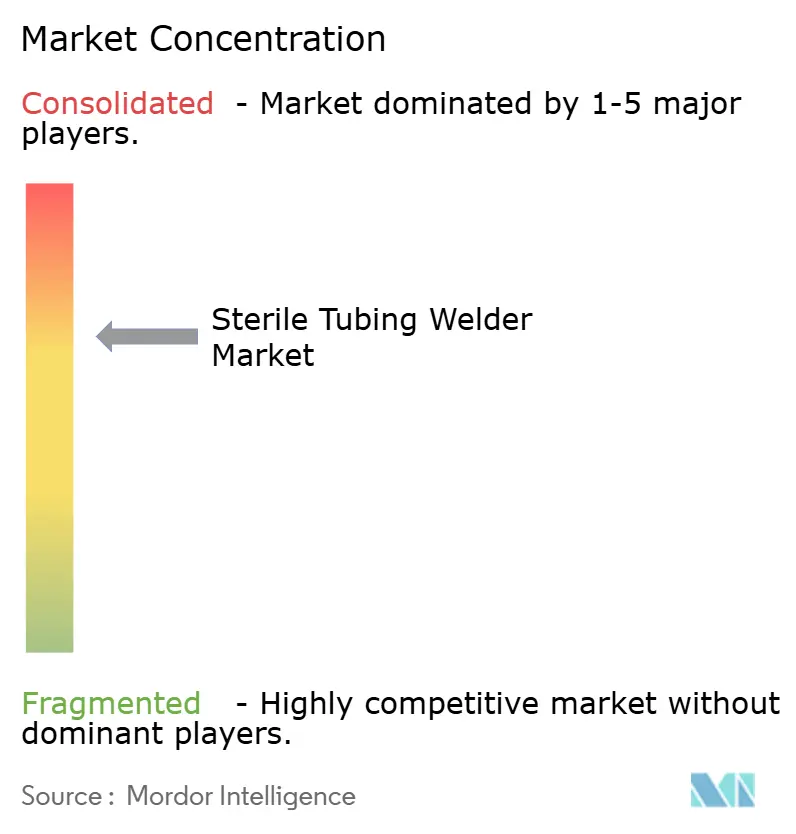

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterile Tubing Welder Market Analysis by Mordor Intelligence

The sterile tubing welder market size is expected to grow from USD 2.79 billion in 2025 to USD 2.94 billion in 2026 and is forecast to reach USD 3.82 billion by 2031 at 5.39% CAGR over 2026-2031. This performance positions the sterile tubing welder market as a critical pillar of modern bioprocessing, buoyed by the pharmaceutical transition to single-use systems, the rapid scale-up of biologics, and increasingly stringent contamination-control rules issued by the FDA and the European Commission. The sterile tubing welder market is also benefiting from the dominance of thermoplastic elastomer (TPE) tubing, the continued preference for automatic welding platforms, and rising demand from blood-component processing centers that require high-throughput, closed-system operations. Regulatory momentum under revised EU GMP Annex 1 has converted automated welding from optional to mandatory in many settings, while advanced therapy manufacturing—cell and gene therapies in particular—creates new volumes of aseptic connections per batch, enlarging the sterile tubing welder market opportunity.

Key Report Takeaways

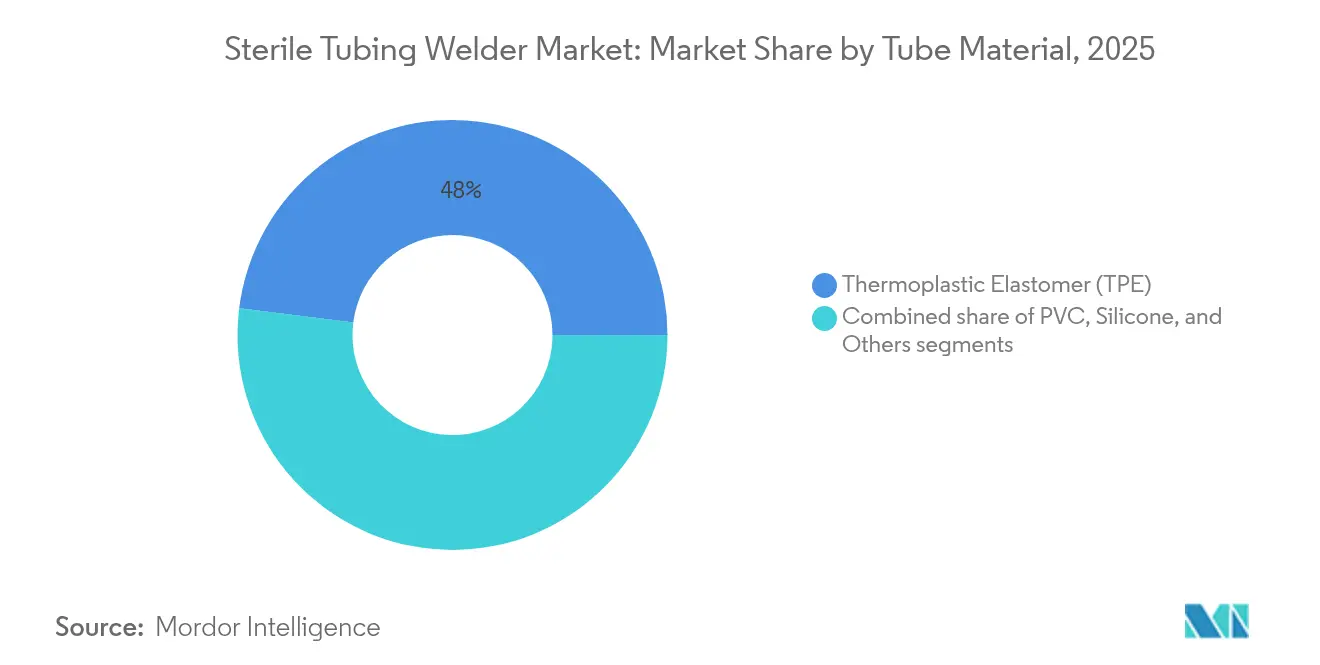

- By tube material, TPE commanded 48.02% of the sterile tubing welder market share in 2025, and PVC alternatives will trail as TPE expands at a 5.55% CAGR through 2031.

- By mode, automatic systems led with 62.10% revenue share in 2025; the same segment is forecast to register a 5.51% CAGR to 2031.

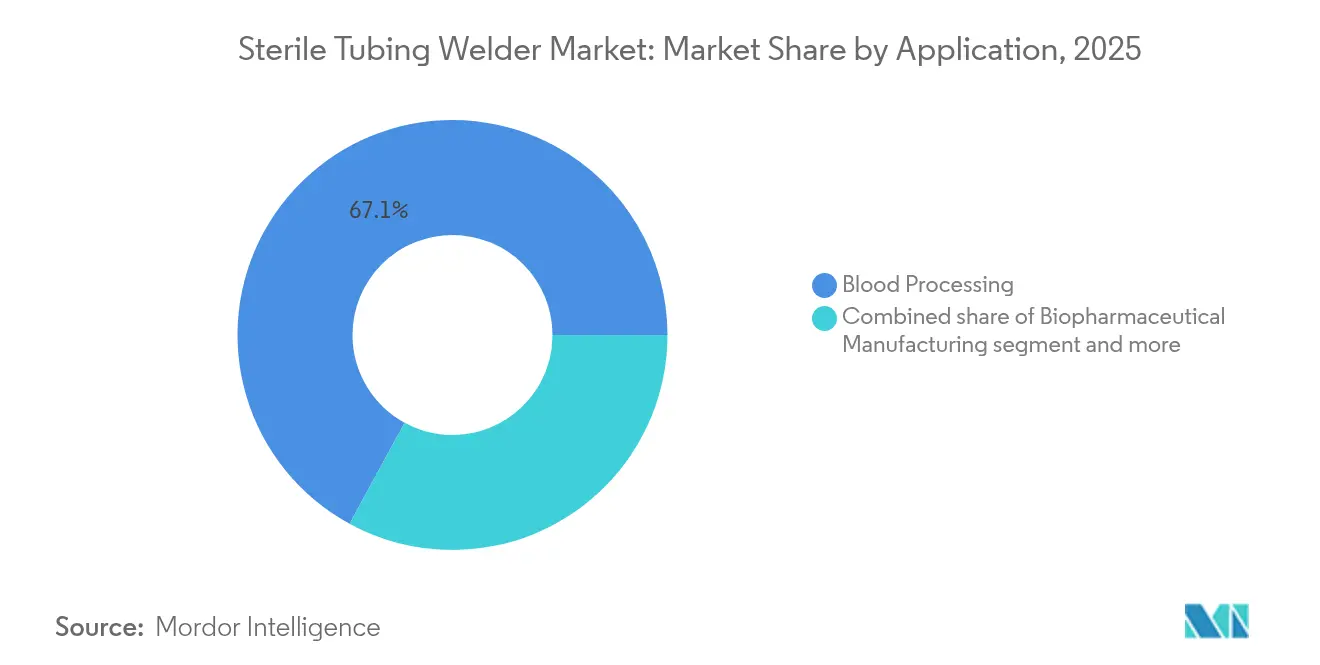

- By application, blood processing held 67.05% of the sterile tubing welder market size in 2025, while biopharmaceutical manufacturing is projected to accelerate at a 5.95% CAGR between 2026 and 2031.

- By end-user, hospitals represented 52.25% share of the sterile tubing welder market in 2025; contract development and manufacturing organizations (CDMOs) are set to log the fastest 5.82% CAGR through 2031.

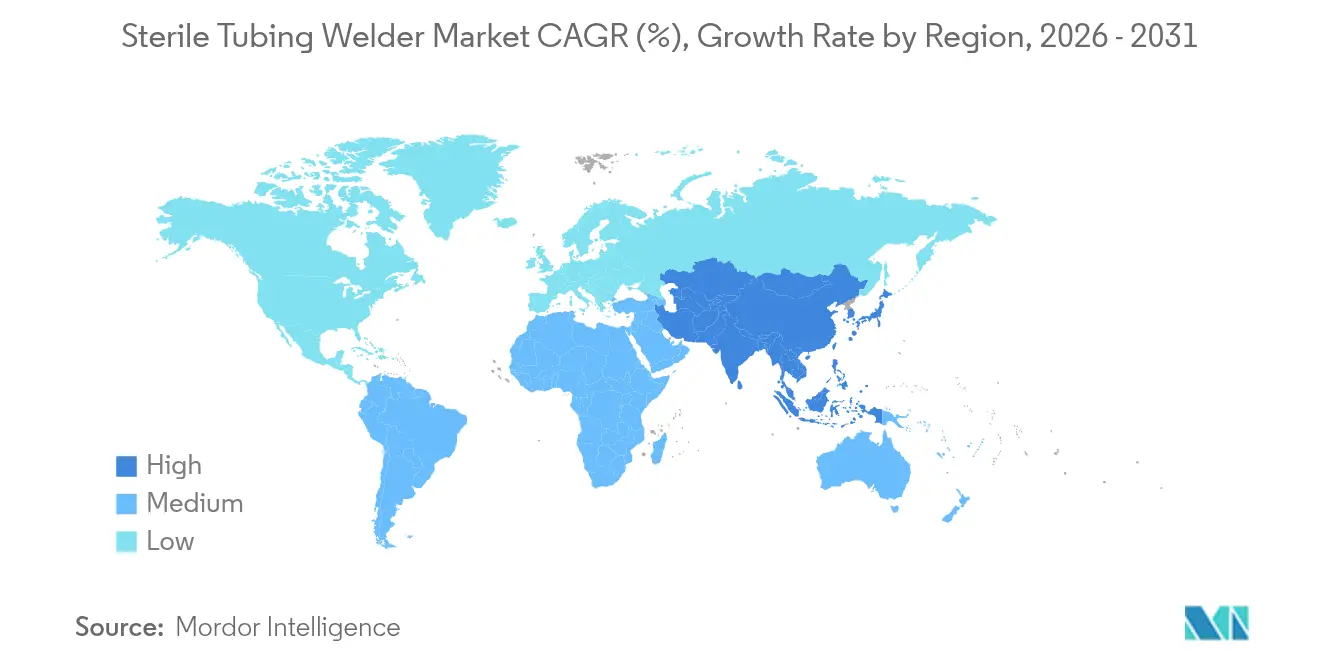

- By geography, North America occupied 38.12% of global revenue in 2025, whereas Asia-Pacific is poised to grow the quickest at 6.07% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Sterile Tubing Welder Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of single-use bioprocessing | +1.8% | North America & Europe lead | Medium term (2-4 years) |

| Expanding biologics & cell-gene therapy pipelines | +1.5% | North America & EU, increasing APAC | Long term (≥ 4 years) |

| Growth in global blood & plasma collections | +1.2% | Worldwide with APAC acceleration | Long term (≥ 4 years) |

| Stricter cGMP sterility regulations | +0.9% | Global | Short term (≤ 2 years) |

| Decentralized point-of-care manufacturing push | +0.7% | Pilot programs in North America; EU exploration | Medium term (2-4 years) |

| Multi-use aseptic connectors lowering validation cost | +0.5% | Cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Single-Use Bioprocessing

Single-use assemblies already support more than 1.2 million sterile connections per year, according to Sartorius. Eliminating cross-contamination between batches can trim facility capital outlays by up to 40%, encouraging large commercial plants to integrate disposables alongside legacy stainless downstream trains. More robust connectors that comply with the ASME BPE code now anchor these systems, satisfying auditor concerns over integrity. As regulatory bodies have endorsed disposables within EU GMP Annex 1, plant managers are expanding inventories of flexible tubing and calling for welders capable of handling TPE, silicone, and multilayer films in fast changeovers. This dynamic secures a durable growth path for the sterile tubing welder market while reinforcing automation investment to close remaining contamination gaps.

Expanding Biologics & Cell-Gene Therapy Pipelines

Cell and gene therapy batches require up to 10 times more sterile connections than legacy small-molecule processing, a reality now shaping equipment budgets across the sterile tubing welder market. Singapore’s investment in mRNA cancer vaccines and South Korea’s USD 1.92 billion allocation for home-grown mRNA platforms underscore regional appetite for advanced modality capacity. Portable, modular factories such as MIT’s InSCyT system highlight how distributed production demands compact welders that can validate hundreds of connections per shift. As regulators draft guidance on decentralized manufacturing, suppliers able to ensure sterility in small-footprint devices will capture share. Continuous activity in novel vectors and personalized immunotherapies sustains elevated connection volumes, pushing the sterile tubing welder market toward higher-throughput, auto-calibrating equipment.

Growth in Global Blood & Plasma Collections

The worldwide plasma fractionation boom keeps blood centers at the top of the sterile tubing welder market hierarchy. Recent FDA approvals[1]U.S. Food and Drug Administration, “2025 Biological Device Application Approvals,” fda.gov for blood processing devices confirm device-maker commitment to closed-loop designs. Emerging economies—from India to Indonesia—are expanding donation infrastructure, and each new collection line typically requires multiple welders to maintain Grade A integrity during bag transfers. In addition, advanced clarification modules such as GEA’s hycon are joining in-line welding to form fully automated plasma processing suites. As throughput per center scales, welded joins remain the gold standard for contamination control, defending market share against connector alternatives in this high-risk segment.

Stricter cGMP Sterility Regulations

EU GMP Annex 1 revisions[2]Directorate-General for Health and Food Safety, “EudraLex—Volume 4, EU GMP Annex 1 (2022),” health.ec.europa.eu oblige manufacturers to document every aseptic connection under a contamination-control strategy, evidencing how and where welds are made. In parallel, the FDA stresses proactive risk mitigation, compelling plants to upgrade from manual clamps to programmable welders with electronic batch records. These mandates re-orient cap-ex plans toward automation, igniting brisk replacement of aging manual units. Suppliers are responding with welders that embed electronic signature capture, temperature pairing, and pressure decay tests, features that simplify audits and fast-track batch-release. The sterile tubing welder market therefore moves-in-step with rule-making cycles, as compliance timelines translate directly into procurement deadlines.

Restraints Impact Analysis of Sterile Tubing Welder Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & validation cost of automated welders | -1.1% | Emerging markets, small manufacturers | Long term (≥ 4 years) |

| Availability of sterile connector alternatives | -0.8% | Global | Medium term (2-4 years) |

| Shortage of skilled operators / training gaps | -0.6% | Global, acute in APAC | Short term (≤ 2 years) |

| TPE-grade supply chain volatility | -0.4% | Global supply chains | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Validation Cost of Automated Welders

A fully qualified welding skid can exceed USD 100,000 and accrues another 30-50% in validation labor. Smaller CDMOs in Latin America and Southeast Asia often postpone purchases, favoring outsourced batch preparation where the welder is already installed. The sterile tubing welder market thus experiences elongated sales cycles in emerging regions. Vendors are piloting equipment-as-a-service contracts that spread payments over multi-year terms, and some offer pre-validated “smart welders” bundled with digital IQ/OQ templates to curb consultant fees.

Availability of Sterile Connector Alternatives

Genderless and multi-use fittings cut qualification steps, winning converts in cost-sensitive labs. CPC’s AseptiQuik G DC, for instance, combines connection and disconnection in a single sterile maneuver, eliminating the melting process inherent to welding. Research outfits with modest batch sizes adopt these connectors to sidestep capital expense, nibbling at sterile tubing welder market share. Front-line vaccine and plasma units, however, still favor weld technology because the molten interface delivers superior barrier integrity, so displacement is incremental rather than wholesale. The rivalry nevertheless forces welder manufacturers to shorten cycle times and introduce entry-level models.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Sterile Tubing Welder Market Segment Analysis

By Tube Material:

TPE Dominance Drives InnovationTPE tubing captured 48.02% of the sterile tubing welder market share in 2025 and is expanding at a 5.55% CAGR, reflecting pharmaceutical preference for low-extractable, gamma-compatible materials. This leadership locks in large volumes for welders configured specifically for TPE melt temperatures, broadening the sterile tubing welder market size derived from TPE lines alone. PVC persists in budget-focused blood centers, while silicone finds narrow roles where elevated temperatures or solvents demand it.

Manufacturers such as Teknor Apex are launching clear, ultra-low-spallation grades that allow optical inspection during welding. KRAIBURG’s PFAS-free advances future-proof supply amid tightening chemical restrictions, reinforcing TPE’s pull on capital budgets. Meanwhile, force-majeure events have pushed end-users to qualify multiple TPE brands to secure continuity, prompting welder firmware updates that store unique heat profiles for each compound.

By Mode:

Automation Accelerates AdoptionAutomatic units owned 62.10% of the sterile tubing welder market size in 2025 and show the highest 5.51% CAGR, a twin-lead gained by eliminating human contact and standardizing weld quality. Their batch-record integration supports real-time release criteria, a factor especially valued in EU inspections. Because of that compliance edge, automatic platforms are the reference specification for every new commercial bioreactor suite, cementing the sterile tubing welder market size advantage over manual units.

First-generation bench welders required expert setup, yet modern models calibrate themselves through barcode-driven tubing IDs, cutting training hours. Inline sensors measure weld pressure and temperature, feeding data to manufacturing execution systems that trigger preventive maintenance. Manual devices remain in R&D cabinets where flexibility matters, but they now compete on price alone as automatic prices fall.

By Application:

Blood Processing Leads, Biopharma AcceleratesBlood processing generated 67.05% of sterile tubing welder market share in 2025 due to high-volume donation centers that rely on melt-seam integrity for plasma safety. However, biopharmaceutical runs are slated for the quickest 5.95% CAGR as monoclonal antibodies, viral vectors, and mRNA expand. For every 2,000 L single-use reactor, biomanufacturers perform hundreds of sterile cuts and joins, inflating welder cycles per batch.

The Aurora Xi plasmapheresis clearance re-emphasized automated sterile processing as a regulatory requirement in blood centers. In contrast, biopharma expansions such as Samsung Biologics’ 784,000 L project create bulk orders for welders with Industry 4.0 connectivity, effectively doubling software revenue streams tied to analytics modules.

By End-User:

Hospitals Dominate, CDMOs Drive GrowthHospitals retained 52.25% share of the sterile tubing welder market size in 2025 because most national blood programs operate inside clinical networks. Yet CDMOs will post a 5.82% CAGR as pharma sponsors outsource advanced therapy manufacturing to specialist plants. Outsource models enable smaller biotech firms to enter trials without building on-site cleanrooms, thereby consolidating welder demand within contract hubs.

Wuxi Biologics’ decision to expand its Worcester, Massachusetts site from 24,000 L to 36,000 L by 2025 illustrates the magnet effect CDMOs have on equipment vendors. Their bulk purchase power influences welder design roadmaps, encouraging modular assemblies that support multi-client turnover. Hospitals, in contrast, focus on durability and simple user interfaces that accommodate rotating staff.

Geography Analysis

North America Sterile Tubing Welder Market

North America accounted for 38.12% of the sterile tubing welder market revenue in 2025, propelled by its dense biopharma corridor, historic uptake of single-use technology, and a regulatory culture that rewards advanced contamination controls. Thermo Fisher Scientific’s USD 2 billion multi-year capacity investment amplifies the regional order book, while Danaher’s Cytiva-Pall consolidation broadens a service backbone that accelerates validation. Vendor training academies in Boston and San Diego also mitigate operator shortages, sustaining utilization rates across installed fleets.

APAC Sterile Tubing Welder Market

Asia-Pacific is the fastest-growing territory at 6.07% CAGR through 2031. China’s USD 4.17 billion biomanufacturing incentive, Samsung Biologics’ 784,000 L build-out, and Singapore’s mRNA programs are channeling record equipment imports. Regional governments have also streamlined GMP licensing, removing one historical hurdle to automated welding adoption. While skill gaps remain acute, suppliers have localized after-sales hubs in Shanghai, Seoul, and Hyderabad to provide on-site validation.

EMEA and LATAM Sterile Tubing Welder Market

Europe maintains steady expansion under hard-line sterility rules. Annex 1 revisions oblige legacy plants to retrofit welders into Grade A cleanrooms, inflating replacement demand. The continent additionally benefits from aggressive cell-therapy pipelines in France and the United Kingdom, spawning many small clinical-scale units that collectively lift volume. In emerging regions—Latin America, the Middle East, and Africa—market momentum stems from public blood-bank upgrades and new vaccine fill-finish lines, though funding cycles stretch project timelines.

Competitive Landscape

The sterile tubing welder market is moderately consolidated, with the top five players capturing an estimated 55–60% combined share. Danaher’s USD 7.5 billion Pall-Cytiva integration exemplifies strategic bundling of upstream disposables with downstream filtration, offering clients single-source procurement. Thermo Fisher’s proposed USD 4.1 billion purchase of Solventum’s purification and filtration assets further intensifies scale advantages.

Technology differentiation revolves around automation layers—AI-driven weld parameter optimization, onboard analytics, and MQTT connectivity. Smaller innovators compete in portable welders under 15 kg that target point-of-care cell-therapy suites. Component suppliers such as CPC continue to attack with connector systems that threaten low-throughput welder placements, but major weld vendors bundle extended warranty and validation kits to lock in loyalty. Service contracts covering remote calibration and GMP audit preparation now constitute up to 20% of vendor revenue, reflecting how compliance complexity drives ancillary sales.

Looking ahead, integrated software ecosystems will be decisive. Vendors embedding weld data into electronic batch-records help manufacturers fulfill real-time release ambitions. Consolidation among elastomer suppliers may follow the equipment trend, ensuring secure tubing supplies that are pre-qualified to machine parameters, a synergy play that could further entrench incumbents.

Sterile Tubing Welder Industry Leaders

Danaher Corporation

Genesis BPS

MGA Technologies

Sartorius AG

Terumo Corporation

- *Disclaimer: Major Players sorted in no particular order

Sterile Tubing Welder Market Companies Covered in this Report

- Aseptic Group

- Avantor

- ChargePoint Technology

- Colder Products Company (CPC)

- Danaher

- Entegris

- Genesis BPS

- GMPTEC GmbH

- Hangzhou Cobetter Filtration Equipment Co., Ltd

- Meissner Filtration Products

- MGA Technologies

- Parker Hannifin

- PendoTECH

- Repligen

- Saint-Gobain Life Sciences

- Sartorius

- Terumo

- Thermo Fisher Scientific

- Vante Biopharm/Sebra

- Watson-Marlow Fluid Technology

Recent Industry Developments in Sterile Tubing Welder Market

- February 2025: Thermo Fisher Scientific announced acquisition of Solventum’s Purification & Filtration business for USD 4.1 billion, targeting USD 125 million in synergies by year five.

- January 2025: Terumo launched Injection Filter Needle under the INFINO Development Program, broadening sterile injection toolkits for hypodermic and intravitreal use.

- November 2024: Teknor Apex released new medical-grade TPE compounds designed for biopharma tubing, featuring reduced spallation and enhanced clarity.

- February 2024: Terumo broke ground on a new Puerto Rico manufacturing site to boost global supply chain resilience for sterile medical devices.

Sterile Tubing Welder Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the sterile tubing welder market as all new, purpose-built devices that aseptically fuse two compatible lengths of thermoplastic tubing used in blood processing, biopharmaceutical production, and diagnostic workflows.

Scope Exclusion: Refurbished or non-sterile industrial tube welders employed outside regulated life-science environments are not counted.

Segments Covered in This Report

- By Tube Material

- Thermoplastic Elastomer (TPE)

- PVC

- Silicone

- Others

- By Mode

- Automatic

- Manual

- By Application

- Blood Processing

- Biopharmaceutical Manufacturing

- Diagnostic Laboratories

- Others

- By End-User

- Hospitals

- Research & Academic Institutes

- Contract Manufacturing

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed device engineers, procurement leads at blood centers across North America, Europe, and Asia, plus contract biologics manufacturers, to refine unit-throughput ratios and validate preliminary model outputs. Follow-up surveys with regional distributors clarified channel mark-ups and warranty replacement rates, strengthening confidence in cost-of-ownership curves.

Desk Research

We started by mapping publicly available demand drivers, annual blood donation volumes from the WHO, FDA 510(k) clearances for single-use welding systems, Eurostat biopharma output indices, and ISO 3826 standards for blood bag connectors. Company 10-Ks, investor decks, and association portals such as the International Society of Blood Transfusion added recent shipment and pricing clues. Where revenue splits were missing, D&B Hoovers and Dow Jones Factiva supplied ballpark sales ranges that anchor our base year.

A secondary scan of peer-reviewed journals and patent families in Questel illustrated technology migration from manual to automatic units, helping us flag replacement cycles and ASP shifts. The sources cited above illustrate the mix; many others were tapped to cross-check figures and narrative consistency.

Market-Sizing & Forecasting

We employ a top-down construct. Global blood bags processed, bioreactor batch counts, and diagnostic test volumes create three demand pools that are then multiplied by observed welds-per-procedure and average selling prices. Select bottom-up checks, sampled supplier invoices and distributor shipment audits, guide calibration. Key variables include (i) share of automatic welders, (ii) mean welds per 100 liters of cell-culture media, (iii) average device lifespan, (iv) regional cap-ex intensity, and (v) regulatory adoption lags. A multivariate regression links these indicators to historical sales and produces the 2025-2030 outlook, with scenario analysis layering supply-chain or policy shocks where experts see material risk. Data gaps in bottom-up rolls are smoothed using median ASPs from confirmed transactions.

Data Validation & Update Cycle

Outputs pass a three-tier review, analyst peer check, senior domain lead sign-off, and automated variance alerts against external trade data. Reports refresh annually; interim flashes occur when recalls, major capacity additions, or currency swings exceed preset thresholds. Before delivery, an analyst re-runs the latest quarter's inputs so clients receive the freshest view.

How Mordor Intelligence's Sterile Tubing Welder Market Size Compares to Other Published Estimates

Published figures often diverge because firms adopt unequal scopes, varying ASP assumptions, and different refresh cadences. Recognizing this variance up front is healthy for decision makers.

Key gap drivers include whether manual welders are counted, if replacement units are separated from first-install volumes, and the year chosen as the baseline. Some publishers also roll forward 2023 exchange rates or apply blanket discount factors, whereas Mordor updates FX quarterly and keeps regional ASP differentials intact before conversion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.79 B (2025) | Mordor Intelligence | - |

| USD 2.71 B (2025) | Global Consultancy A | Excludes manual welders and small clinics, leading to narrower unit count |

| USD 2.62 B (2024) | Trade Journal B | Uses older base year and static 2024 FX rates without regional ASP splits |

| USD 2.43 B (2023) | Industry Association C | Limits scope to hospital settings; biopharma and research labs omitted |

These differences show why Mordor's balanced, variable-driven approach, validated by end-user conversations and refreshed every year, offers the most dependable starting point for strategic planning.

Key Questions Answered in the Report

What regulatory change is currently driving fastest adoption of sterile tubing welders?

Revised EU GMP Annex 1 and parallel FDA contamination-control guidance are pushing manufacturers to automate every aseptic connection, making welders the default compliance solution.

How are single-use bioprocessing lines reshaping welder design requirements?

Flexible, disposable assemblies require welders that can identify multiple tubing chemistries, perform rapid cycle changes, and log parameters directly into electronic batch records.

Which application sees the highest connection frequency, and why?

Cell and gene therapy production demands many more sterile joins per batch than traditional biologics because of small lot sizes and closed, patient-specific workflows.

Why do users increasingly prefer automatic over manual welding units?

Automated systems cut operator intervention, standardize weld quality, and generate audit-ready data, reducing both contamination risk and documentation workload.

How is TPE supply volatility influencing buyer behavior?

To hedge raw-material disruptions, end-users are pre-qualifying multiple TPE grades and favoring welders with programmable heat profiles for rapid material switching.

What strategic role do CDMOs play in the sterile tubing welder ecosystem?

Pharmaceutical outsourcing concentrates high-end manufacturing in specialized hubs, driving bulk purchases of advanced welders and setting industry benchmarks for validation practices.

Page last updated on: