U.S. Medical Tapes And Bandages Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

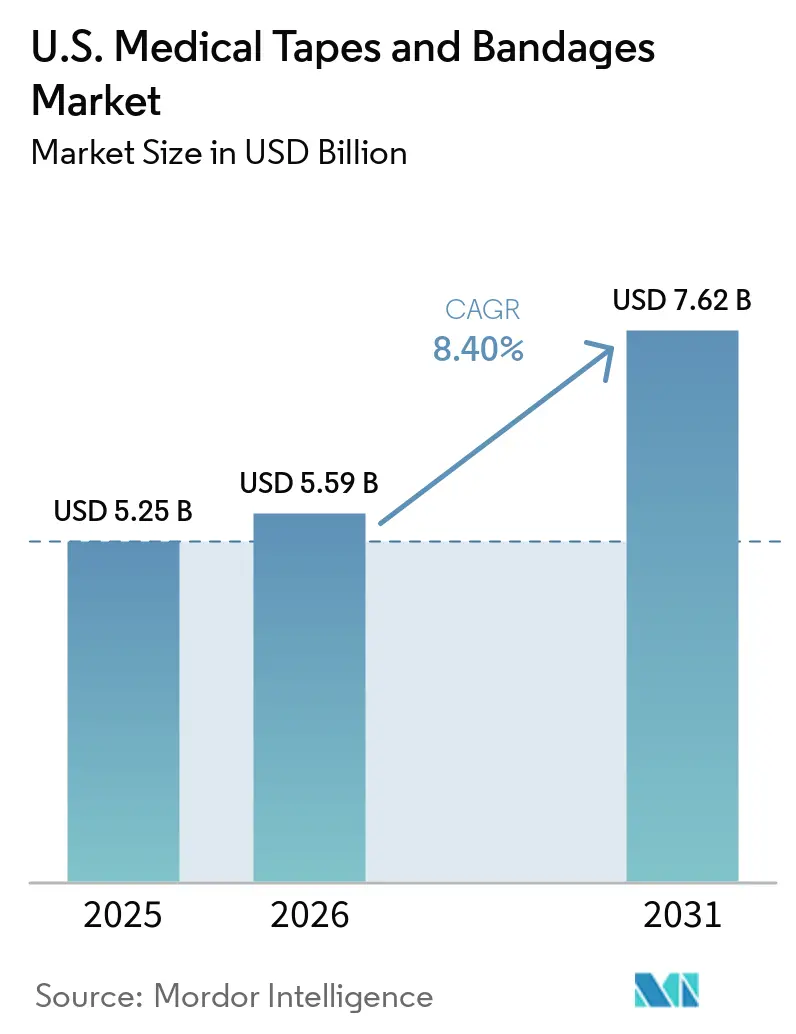

| Base Year Market Size (2025) | USD 5.25 Billion |

| Market Size (2026) | USD 5.59 Billion |

| Market Size (2031) | USD 7.62 Billion |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Medical Tapes And Bandages Market Analysis by Mordor Intelligence

The U.S. Medical Tapes And Bandages Market size is expected to grow from USD 5.25 billion in 2025 to USD 5.59 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at 8.40% CAGR over 2026-2031.

The United States medical tapes and bandages market is driven by the increasing prevalence of chronic wounds, a growing diabetic population, and the shift of procedures to ambulatory settings. These products maintain consistent demand due to their repeated use across hospitals, surgery centers, physician offices, retail channels, and home care environments. Market growth is further supported by the rising adoption of continuous glucose monitors, insulin pumps, and other wearable devices requiring secure, skin-compatible adhesives for extended use. Additionally, the shift toward home-based wound care has increased demand for easy-to-apply dressings, bordered foam products, and tape systems tailored for non-institutional settings.

Key Report Takeaways

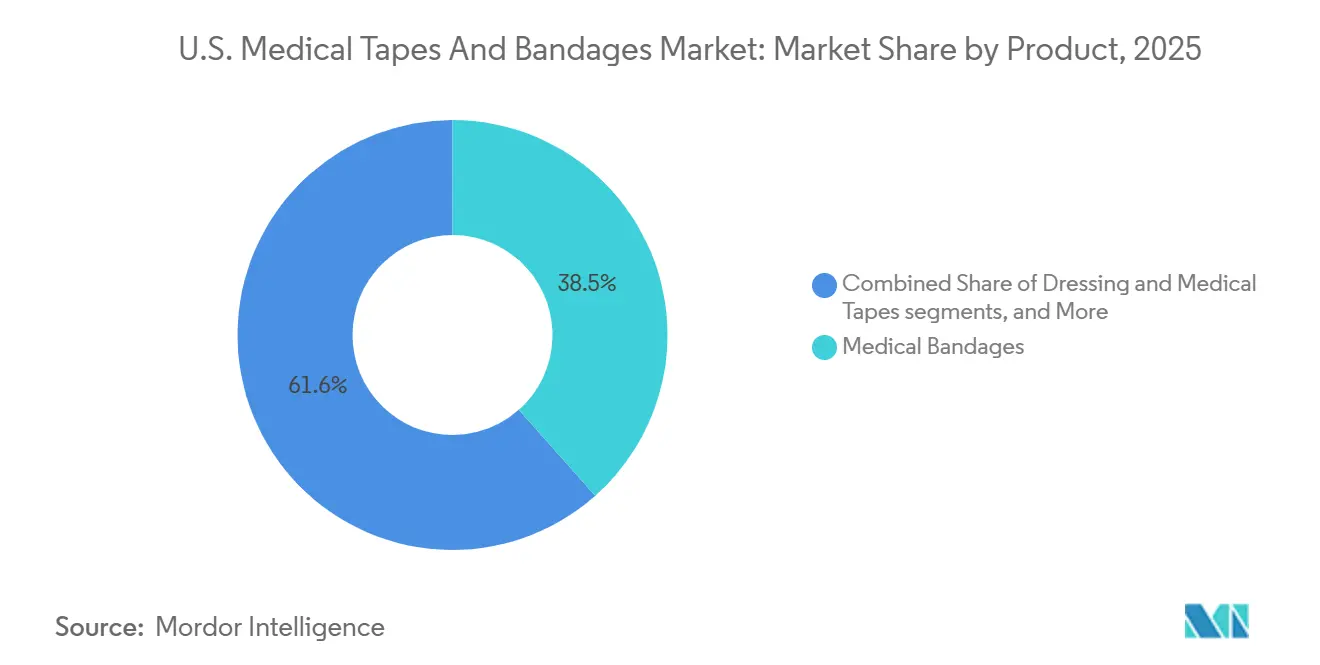

- By product, medical bandages held 38.45% of the U.S. medical tapes and bandages market share in 2025, while medical tapes is projected to expand at an 8.25% CAGR through 2031.

- By application, surgical wounds accounted for 35.66% of the U.S. medical tapes and bandages market size in 2025, while ulcers treatment is projected to grow at a 7.95% CAGR through 2031.

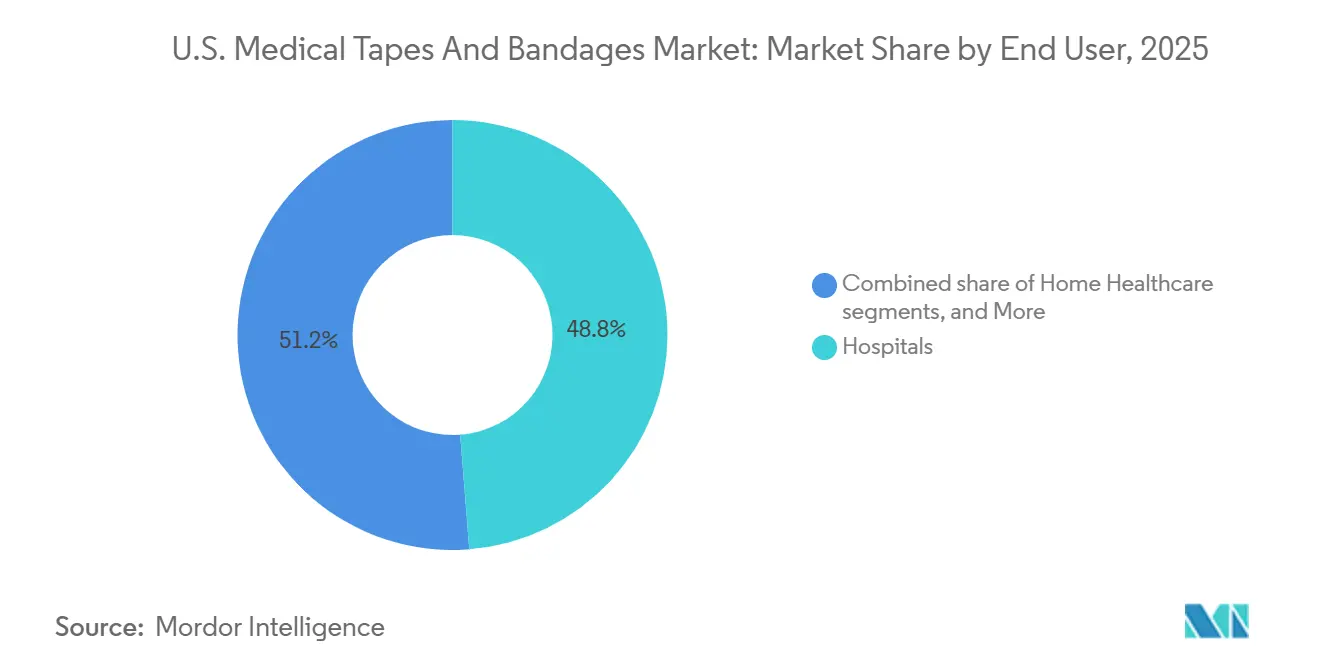

- By end user, hospitals held 48.75% of revenue in 2025, while home healthcare is projected to advance at an 8.86% CAGR through 2031.

- By distribution channel, retail pharmacies captured 42.59% of revenue in 2025, while E-commerce and online medical supply are expected to grow at a 7.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Medical Tapes And Bandages Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Chronic wound and diabetes burden | +2.1% | National, highest disease concentration in Southeast and Midwest | Long term (≥ 4 years) |

| High surgical and ASC procedure volumes | +1.4% | National, Sun Belt states such as Texas, Florida, and Arizona show strong ASC expansion | Medium term (2-4 years) |

| Aging patient mix and pressure injury risk | +1.2% | National, with larger 65+ cohorts across Pacific Coast and Southeast states | Long term (≥ 4 years) |

| Shift toward home and alternate-site wound care | +0.9% | National, with faster relevance in rural and underserved areas | Medium term (2-4 years) |

| Adhesive securement demand from CGMs, insulin pumps, and wearable devices | +0.8% | National, with high adoption in urban diabetes care and cardiology settings | Short term (≤ 2 years) |

| CMS site-of-care and supply reimbursement mechanics favor office and outpatient use | +0.6% | National, especially in states with high Medicare managed care penetration | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Wound and Diabetes Burden Creating Persistent Volume Demand

The United States medical tapes and bandages market experiences steady demand due to the high prevalence of chronic wounds and diabetes. In 2025, chronic wounds impacted 10.5 million Medicare beneficiaries, generating USD 22.5 billion in annual care costs, with wound dressings comprising a significant share.[1]Medicare Payment Advisory Commission, “Ambulatory Surgical Center Services, Status Report,” Report to the Congress: Medicare Payment Policy, medpac.gov Additionally, 53.1 million Americans with diabetes faced a 15%-34% lifetime risk of diabetic foot ulcers, driving recurring demand for securement tapes, bordered dressings, and bandage systems.[2]Chandan K. Sen, “Human Wound and Its Burden: Updated 2025 Compendium of Estimates,” Advances in Wound Care, pubmed.ncbi.nlm.nih.gov These products are consumed over extended treatment cycles, ensuring consistent demand despite reimbursement challenges.

High Surgical and ASC Procedure Volumes Sustaining Core Tape and Bandage Demand

The United States medical tapes and bandages market benefits from the growing shift of procedures to ambulatory surgery centers (ASCs). In 2024, 6,436 Medicare-certified ASCs performed 6.4 million fee-for-service Medicare procedures, with a 3.5% year-over-year increase in procedure volume per 1,000 beneficiaries.[3]enters for Medicare & Medicaid Services, “Calendar Year (CY) 2026 Home Health Prospective Payment System Final Rule (CMS-1828-F),” CMS Fact Sheet, cms.gov Rising total knee and hip arthroplasty volumes, along with the 2026 ASC Covered Procedure List expansion adding 560 procedures, further boost demand for wound covering and securement products in outpatient settings.

Wearable Medical Devices Redefining Adhesive Tape Specifications

Wearable medical devices are driving innovation in adhesive tape performance in the United States medical tapes and bandages market. Devices like continuous glucose monitors and insulin pumps require securement solutions that withstand movement, moisture, and extended wear. With Dexcom reporting USD 1.209 billion in Q3 2025 revenue, reflecting a 22% year-over-year growth, the market is shifting from commodity products to performance-driven solutions emphasizing comfort, adhesion, and ease of removal.

Payer-Driven Home Care Migration Expanding Alternate-Site Product Needs

The United States medical tapes and bandages market is evolving with the increasing shift of wound care to home settings. CMS raised payment for disposable negative pressure wound therapy devices to USD 282.10 in 2026, supporting advanced home wound therapy and recurring use of consumables like adhesive securement products.[4]Payment Policies Under the Physician Fee Schedule (CMS-1832-F),” Federal Register/CMS Final Rule Material, cms.gov However, bundled billing rules for routine supplies necessitate practical, easy-to-use products, highlighting the growing relevance of self-applied and caregiver-friendly solutions over clinician-managed formats.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| MARSI and skin irritation risk | -0.5% | National, with highest incidence in critical care units and elderly long-term care populations | Long term (≥ 4 years) |

| Pricing pressure from GPOs and distributor consolidation | -0.7% | National, concentrated in integrated delivery networks and large hospital systems | Medium term (2-4 years) |

| 2026 skin-substitute payment reset disrupting office wound-care economics | -0.8% | National, with strongest impact in physician office settings and selected pilot states | Short term (≤ 2 years) |

| Routine-vs-nonroutine supply reimbursement complexity in home health | -0.4% | National, with disproportionate effect in rural areas with high home health dependency | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

2026 CMS Payment Reset Reshaping Office Wound Care Economics

The United States medical tapes and bandages market is experiencing a major payment shift in office-based wound care. Under the CY 2026 Physician Fee Schedule final rule, CMS reclassified several skin substitutes as "incident-to" supplies and introduced a flat national payment rate of USD 127.28 per square centimeter, replacing the previous ASP+6% structure that allowed reimbursements exceeding USD 2,000 per square centimeter. This change is expected to reduce gross Medicare fee-for-service spending on skin substitute services by USD 19.6 billion in 2026, significantly altering advanced wound treatment economics. While physician offices may shift toward conventional wound products, the disruption could delay product decisions as workflows adjust, creating short-term uncertainty in purchasing behavior.

GPO Consolidation Compressing Institutional Tape and Bandage Margins

Pricing pressures continue to challenge the United States medical tapes and bandages market, particularly in hospital channels. A 2025 study highlighted that group purchasing organizations facilitated procurement for 96% of acute-care hospitals, with 70% of hospital medical supply purchases made through GPO-negotiated contracts, contributing to a total institutional supply spend of USD 146.9 billion in 2023. This structure favors scale and price consistency, limiting margin flexibility for high-volume suppliers. Smaller or specialized players may find opportunities with silicone tapes or specialty dressings but face challenges as hospital systems prioritize consolidated buying and standardized formularies, tightening institutional pricing conditions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Medical Bandages Lead Share as Medical Tapes Accelerate Innovation

In 2025, Medical Bandages accounted for 38.45% of revenue, leading the United States medical tapes and bandages market. Their dominance stems from extensive use in post-operative care, compression support, first-aid treatment, and routine wound covering across hospitals, ASCs, physician offices, retail stores, and homes. Serving both institutional and consumer needs, bandages maintain stable demand across clinical and over-the-counter channels.

Medical Tapes, the fastest-growing segment, is projected to achieve an 8.25% CAGR from 2026 to 2031. Growth is driven by increased adoption of CGMs, insulin pumps, and advanced tape formats like transparent film securement and silicone tapes. Enhanced focus on adhesion, skin tolerance, and removal comfort is driving innovation in this segment.

By Application: Surgical Wound Management Anchors the Core as Ulcer Treatment Accelerates

Surgical wounds contributed 35.66% of revenue in 2025, making them the largest application in the United States medical tapes and bandages market. This is linked to the high volume of outpatient and ambulatory procedures requiring post-treatment care, creating consistent demand for tapes, dressings, and bandages.

Ulcer Treatment, the fastest-growing application, is expected to post a 7.95% CAGR from 2026 to 2031. Growth is fueled by the diabetic population and demand for conventional wound care in managing diabetic, pressure, and venous ulcers. CMS payment changes in 2026 are further driving demand for foam dressings and securement tapes.

By End User: Hospitals Dominate as Home Healthcare Claims Structural Growth

Hospitals held 48.75% of revenue in 2025, dominating the United States medical tapes and bandages market. Their leadership is due to high procurement volumes for surgical dressings, retention tapes, and other products used in inpatient and outpatient care.

Home Healthcare, the fastest-growing segment, is projected to grow at an 8.86% CAGR from 2026 to 2031. CMS support for home-based wound care and billing rules that include routine wound supplies in home health payments are driving demand for user-friendly tape and dressing formats.

By Distribution Channel: Retail Pharmacies Hold the Largest Share as E-Commerce Disrupts

Retail Pharmacies captured 42.59% of revenue in 2025, leading the United States medical tapes and bandages market. Their strength lies in serving both over-the-counter consumers and institutional replenishment needs, supported by strong product visibility and trusted brand placement.

E-commerce and Online Medical Supply, the fastest-growing channel, is projected to record a 7.67% CAGR from 2026 to 2031. CMS formalized HCPCS codes for tape products in 2025, improving billing pathways and enhancing product visibility in reimbursable home delivery systems.

Geography Analysis

Hospitals, particularly in states such as California, Texas, and Florida with high surgical activity, represent the largest end-user segment. These states frequently perform orthopedic and reconstructive procedures. In the U.S., approximately 544,000 hip replacements and 790,000 knee replacements are conducted annually, driving significant demand for surgical tapes and dressings.

States like Florida, Arizona, and Pennsylvania, which have substantial elderly populations, are critical markets. Seniors account for 85% of chronic wound cases, with an estimated 8.2 million Americans aged 65 and older projected to experience chronic wounds. This trend is fueling the demand for advanced bandages and adhesive solutions in long-term care facilities.

Competitive Landscape

The United States medical tapes and bandages market is moderately fragmented, with no single supplier dominating. Global companies like Solventum, Smith & Nephew, Mölnlycke, Convatec, and B. Braun maintain strong positions in institutional settings, while Medline, Cardinal Health, Dynarex, Dukal, and Kenvue enhance competition through private labels, channel coverage, and consumer-focused products. This competitive landscape spans hospitals, ASCs, physician offices, retail outlets, and home care, driven by factors such as evidence, pricing, channel access, and brand recognition.

Strategic moves in 2025 and 2026 highlight efforts by leading companies to strengthen their market positions. In December 2025, Solventum acquired Acera Surgical for USD 725 million upfront, with up to USD 125 million in milestone payments, expanding its reach in complex wound management through the Restrata platform.

Channel-specific purchasing priorities shape competition further. Hospitals and health systems focus on formulary access, contracting terms, and compliance readiness, while retail and consumer channels prioritize visibility, packaging, and brand loyalty. Office and home care settings favor products that combine clinical reliability with ease of use.

U.S. Medical Tapes And Bandages Industry Leaders

Medtronic plc

Medline Industries Inc.

Smith & Nephew plc

Cardinal Health Inc.

Solventum Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Smith+Nephew introduced the RENASYS EDGE Negative Pressure Wound Therapy system, a portable device designed to enhance patient self-care with an 88% compliance rate and no annual servicing requirements.

- March 2026: Smith+Nephew launched the ALLEVYN COMPLETE CARE Foam Dressing in the U.S., featuring advanced technologies to reduce pressure injury risk by over 65% and retain over 99% of bacteria from wounds.

- December 2025: Solventum acquired Acera Surgical for USD 725 million upfront, with additional milestone payments of up to USD 125 million, as Acera projected USD 90 million in 2025 sales.

U.S. Medical Tapes And Bandages Market Report Scope

As per the scope of the report, medical tapes and bandages are essential healthcare materials designed to secure wound dressings, immobilize injured areas, and support healing. Tapes are pressure-sensitive adhesives that hold dressings in place, while bandages are fabric or elastic materials used to wrap, compress, or protect body parts.

The U.S. medical tapes and bandages market is segmented by product, application, end-user, and distribution channel. By product, the market includes medical tapes (paper tapes, fabric tapes, plastic tapes, silicone/acrylic/rubber tapes, transparent film/dressing retention tapes, elastic/waterproof/specialty tapes), dressings (foam dressings, hydrocolloid dressings, film dressings, alginate dressings, hydrogel dressings, collagen dressings, superabsorbent dressings, antimicrobial dressings, other advanced dressings), and medical bandages (adhesive bandages/first aid bandages, gauze bandage rolls, elastic bandage rolls, cohesive/self-adherent bandages, conforming bandages, triangular bandages, orthopedic/cast bandages, others). By application, the market is segmented into surgical wounds, traumatic wounds, ulcer treatment, sports injuries, burn injuries, and others. By end-user, the market is categorized into hospitals, ambulatory surgery centers, clinics and physician offices, home healthcare, long-term care and skilled nursing facilities, retail/consumer self-care, and military and emergency care. By distribution channel, the market includes distributors, direct sales/enterprise contracts, retail pharmacies, e-commerce/online medical supply, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Medical Tapes | Paper Tapes |

| Fabric Tapes | |

| Plastic Tapes | |

| Silicone / Acrylic / Rubber Tapes | |

| Transparent Film / Dressing Retention Tapes | |

| Elastic / Waterproof / Specialty Tapes | |

| Dressings | Foam Dressings |

| Hydrocolloid Dressings | |

| Film Dressings | |

| Alginate Dressings | |

| Hydrogel Dressings | |

| Collagen Dressings | |

| Superabsorbent Dressings | |

| Antimicrobial Dressings | |

| Other Advanced Dressings | |

| Medical Bandages | Adhesive Bandages / First Aid Bandages |

| Gauze Bandage Rolls | |

| Elastic Bandage Rolls | |

| Cohesive / Self-Adherent Bandages | |

| Conforming Bandages | |

| Triangular Bandages | |

| Orthopedic / Cast Bandages | |

| Others |

| Surgical Wounds |

| Traumatic Wounds |

| Ulcers Treatment |

| Sports Injuries |

| Burn Injuries |

| Sport Injuries |

| Others |

| Hospitals |

| Ambulatory Surgery Centers |

| Clinics and Physician Offices |

| Home Healthcare |

| Long-Term Care and Skilled Nursing Facilities |

| Retail / Consumer Self-Care |

| Military and Emergency Care |

| Distributors |

| Direct Sales / Enterprise Contracts |

| Retail Pharmacies |

| E-commerce / Online Medical Supply |

| Others |

| By Product | Medical Tapes | Paper Tapes |

| Fabric Tapes | ||

| Plastic Tapes | ||

| Silicone / Acrylic / Rubber Tapes | ||

| Transparent Film / Dressing Retention Tapes | ||

| Elastic / Waterproof / Specialty Tapes | ||

| Dressings | Foam Dressings | |

| Hydrocolloid Dressings | ||

| Film Dressings | ||

| Alginate Dressings | ||

| Hydrogel Dressings | ||

| Collagen Dressings | ||

| Superabsorbent Dressings | ||

| Antimicrobial Dressings | ||

| Other Advanced Dressings | ||

| Medical Bandages | Adhesive Bandages / First Aid Bandages | |

| Gauze Bandage Rolls | ||

| Elastic Bandage Rolls | ||

| Cohesive / Self-Adherent Bandages | ||

| Conforming Bandages | ||

| Triangular Bandages | ||

| Orthopedic / Cast Bandages | ||

| Others | ||

| By Application | Surgical Wounds | |

| Traumatic Wounds | ||

| Ulcers Treatment | ||

| Sports Injuries | ||

| Burn Injuries | ||

| Sport Injuries | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centers | ||

| Clinics and Physician Offices | ||

| Home Healthcare | ||

| Long-Term Care and Skilled Nursing Facilities | ||

| Retail / Consumer Self-Care | ||

| Military and Emergency Care | ||

| By Distribution Channel | Distributors | |

| Direct Sales / Enterprise Contracts | ||

| Retail Pharmacies | ||

| E-commerce / Online Medical Supply | ||

| Others | ||

Key Questions Answered in the Report

How large is the U.S. medical tapes and bandages space in 2026?

It stands at USD 5.59 billion in 2026 and is forecast to reach USD 7.62 billion by 2031 at a CAGR of 7.40%.

What is driving demand for medical tapes and bandages in the United States?

Demand is being supported by chronic wounds, diabetes, higher outpatient procedure volumes, home-based wound care, and growing use of wearable medical devices that need adhesive securement.

Which product category is growing the fastest?

Medical Tapes is the fastest-growing product segment, with a projected CAGR of 8.25% from 2026 to 2031.

Which application holds the largest revenue share?

Surgical Wounds led applications with 35.66% of revenue in 2025 because procedures create immediate and repeat demand for dressings, tapes, and bandages.

Why is home healthcare becoming more important for suppliers?

Home Healthcare is projected to grow at an 8.86% CAGR, supported by reimbursement backing for home-based wound treatment and rising use of caregiver-friendly supply formats.

What is the main pricing risk for manufacturers?

The largest near-term pressure comes from CMS payment changes in office wound care and continued GPO-driven pricing pressure in hospitals and health systems.

Page last updated on: