U.S. Laparoscopic Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

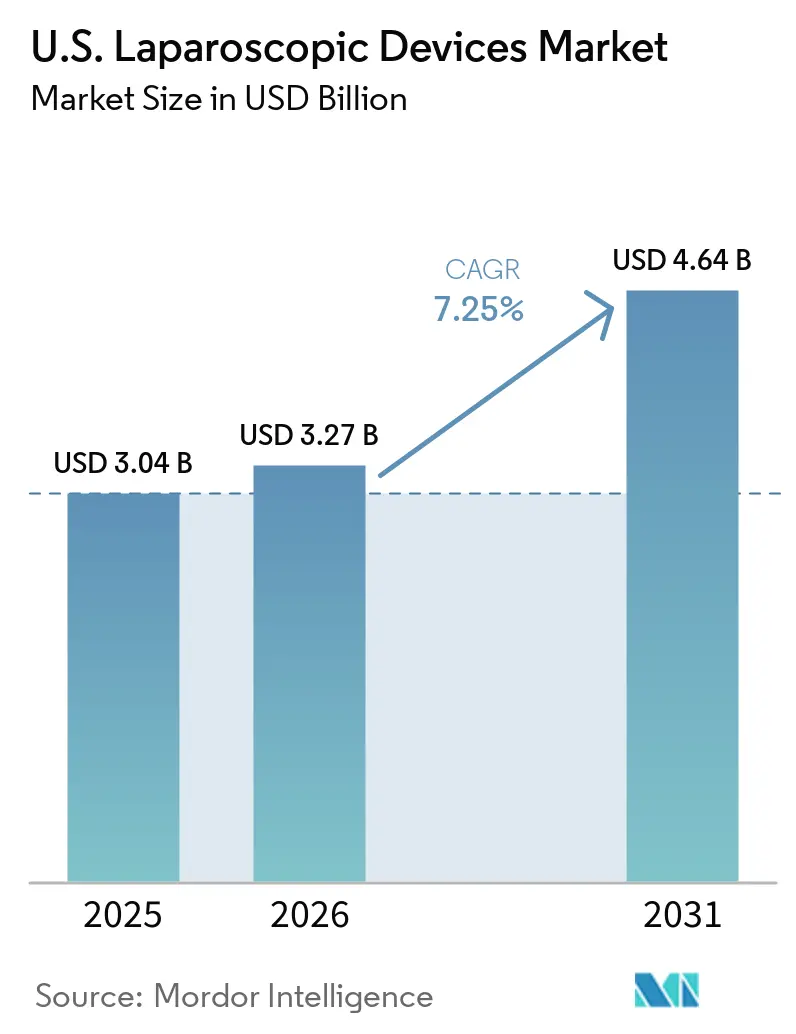

| Base Year Market Size (2025) | USD 3.04 Billion |

| Market Size (2026) | USD 3.27 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 7.25% CAGR |

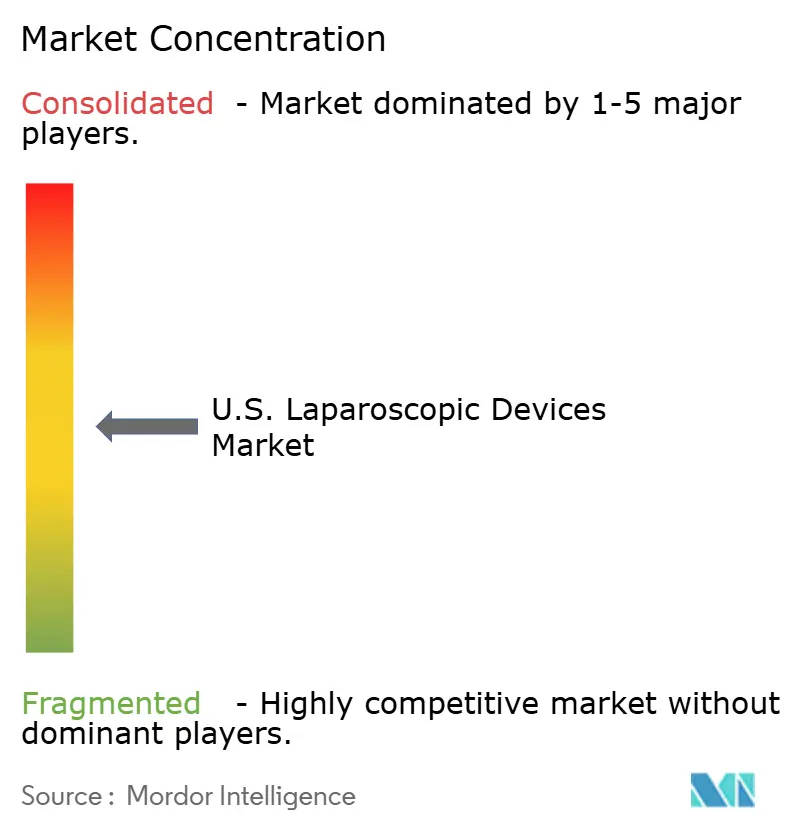

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Laparoscopic Devices Market Analysis by Mordor Intelligence

The U.S. Laparoscopic Devices Market size is projected to expand from USD 3.04 billion in 2025 and USD 3.27 billion in 2026 to USD 4.64 billion by 2031, registering a CAGR of 7.25% between 2026 to 2031.

Surgeons are increasingly shifting procedures from traditional inpatient hospitals to outpatient departments and ambulatory surgical centers. These centers have seamlessly integrated minimally invasive tools into their standard practices. In a move signaling strong support for this trend, the 2026 CMS OPPS and ASC final rule added 547 surgical procedure codes to the ASC Covered Procedures List. Additionally, it granted a 2.6% payment update for qualifying ASCs, bolstering outpatient laparoscopic care reimbursements in the United States. This policy cycle also initiated the phaseout of the Inpatient-Only list, removing 285 services in 2026. This shift not only encourages more cases to migrate to outpatient settings but also broadens the demand for compact visualization, access, energy, and robotic systems.

Key Report Takeaways

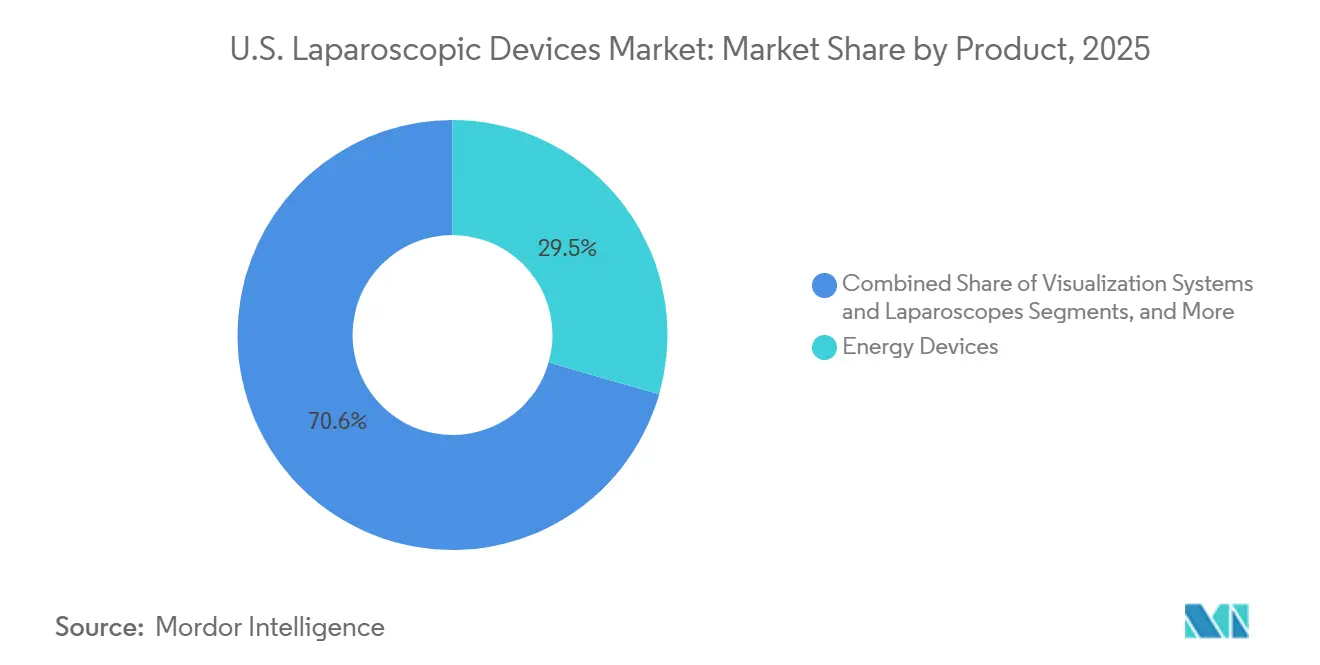

- By product, energy devices held 29.45% share in 2025, while robotic-assisted laparoscopy platforms and instruments recorded the fastest projected CAGR at 8.12% through 2031.

- By application, general surgery accounted for 84.12% of demand in 2025, while gynecological surgery is forecasted to expand at a 7.95% CAGR through 2031.

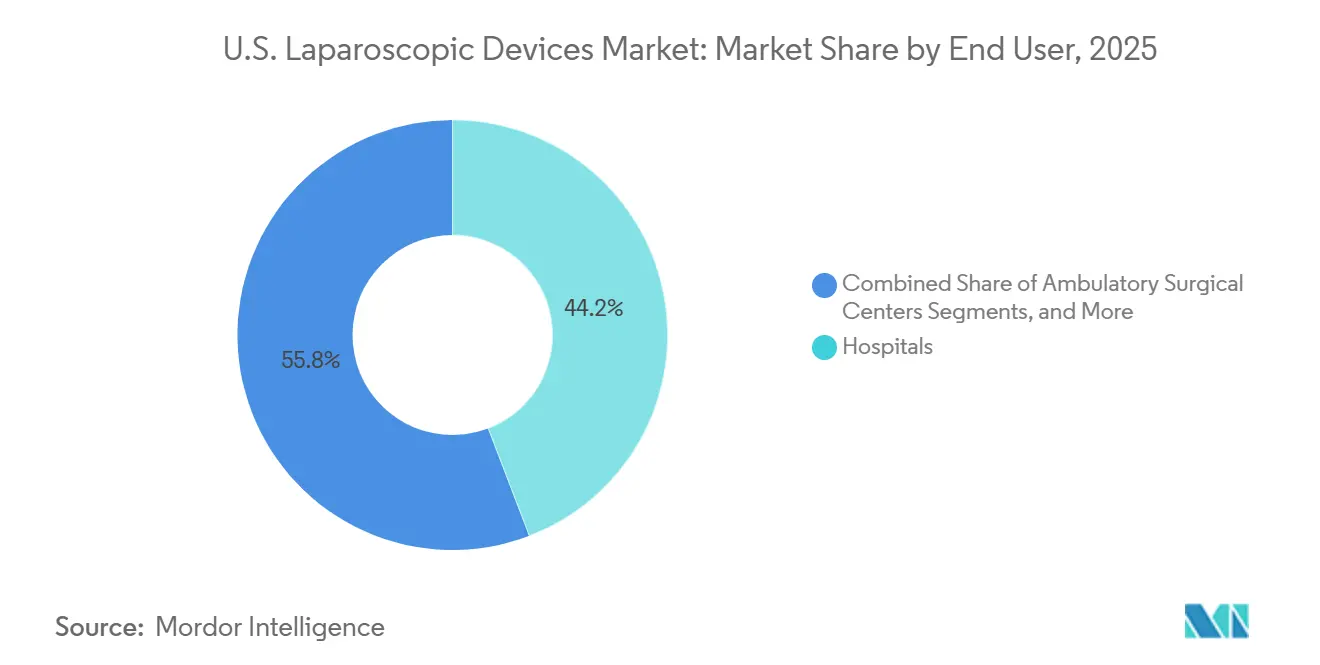

- By end user, hospitals held 44.18% share in 2025, while ambulatory surgical centers are projected to record the highest CAGR at 8.25% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Laparoscopic Devices Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hospital outpatient and ASC migration for robotic and laparoscopic procedures | +1.8% | National, with highest impact across Sun Belt and Midwest ASC corridors | Short term (≤ 2 years) |

| High obesity burden sustaining bariatric and adjacent laparoscopic demand | +0.6% | National, concentrated in Southern and Midwestern high-obesity states | Medium term (2-4 years) |

| Premiumization of energy and powered stapling devices | +1.3% | National urban and academic medical center markets | Medium term (2-4 years) |

| Robotic-enabled minimally invasive surgery adoption | +1.4% | National, with early acceleration in Tier 1 and Tier 2 metropolitan markets | Long term (≥ 4 years) |

| OR staffing variability favoring integrated, workflow-efficient platforms | +0.7% | National, acute in rural and community hospital settings | Short term (≤ 2 years) |

| Smoke evacuation mandates and stable low-pressure pneumoperitoneum standards | +0.5% | 17-state mandate footprint, expanding to additional states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Hospital and ASC Migration Rewriting Capital Equipment Cycles

In 2026, the CMS OPPS and ASC final rule added 547 codes to the ASC Covered Procedures List, expanding the range of reimbursable procedures in ambulatory settings. Additionally, CMS began a three-year phaseout of the Inpatient-Only list, removing 285 services in 2026, further shifting surgical volumes to cost-effective outpatient sites.[1]Centers for Medicare & Medicaid Services, “Calendar Year 2026 Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment Systems Final Rule Summary,” Healthcare Financial Management Association, hfma.org This transition is reshaping the United States laparoscopic devices market, as ASCs prioritize compact systems, simpler setups, and faster room turnovers over traditional inpatient OR configurations. Medtronic’s Hugo robotic-assisted surgery system reflects this shift with its modular architecture, adaptable to outpatient environments.

Robotic-Enabled Surgery Reshaping the High-Value Instrument Tier

The rise of robotic surgery is driving the United States laparoscopic devices market toward premium instruments and accessories, focusing on recurring use rather than one-time capital investments. Intuitive reported a 17% increase in da Vinci procedures in Q4 2025 and USD 1.69 billion in instruments and accessories revenue in Q1 2026, reflecting a 23% year-over-year growth. Each robotic procedure requires compatible devices, often replacing traditional laparoscopic tools.[2]Intuitive Surgical, “2025 Annual Report Form 10-K,” U.S. Securities and Exchange Commission, sec.gov Medtronic’s Hugo and Johnson & Johnson’s OTTAVA platforms signal growing competition, with market dynamics now centered on capital access, OR footprint, and robust instrument ecosystems rather than platform availability alone.

OR Staffing Constraints Driving Demand for Integrated Workflow Platforms

Staffing challenges are increasing the demand for integrated systems in the United States laparoscopic devices market. These systems streamline workflows by combining visualization, energy control, insufflation, and procedural data into a single platform, reducing setup complexity and room turnaround time. Intuitive’s My Intuitive+ ecosystem exemplifies this trend by integrating simulation, telepresence, and performance tools into a unified framework, enhancing team coordination and surgeon training. Hospitals and surgery centers are prioritizing solutions that support lean perioperative teams, driving demand for platforms that simplify workflows and offer operational support alongside clinical capabilities.

Energy and Stapling Premiumization Expanding Per-Procedure Revenue

Energy and stapling tools are driving revenue growth in the United States laparoscopic devices market by reducing instrument changes and integrating seamlessly into standardized workflows. Advanced vessel-sealing and tissue-dissection platforms are gaining traction in general surgery and gynecological procedures, with robotic systems further embedding premium energy and stapling categories into procedure economics. Facilities are increasingly adopting products that minimize handoffs and tray changes, enhancing throughput in hospitals and ASCs. Multi-year purchasing agreements for advanced stapler reloads, vessel-sealing instruments, and accessory bundles are strengthening incumbent positions, as bundled offerings raise switching costs for providers over a platform’s lifecycle.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High capital and disposable cost burden for robotic and advanced laparoscopic systems | -1.5% | National, most acute in community and rural hospitals lacking capital budgets | Medium term (2-4 years) |

| Robotic substitution eroding volume in conventional laparoscopic device categories | -0.6% | National urban centers with high robotic penetration | Long term (≥ 4 years) |

| Reimbursement compression in high-volume laparoscopic procedure codes | -0.9% | National, highest impact in Medicare-heavy outpatient volumes | Short term (≤ 2 years) |

| FDA quality and supply chain scrutiny under QMSR and device-class enforcement | -0.5% | National manufacturing and distribution | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital Cost Concentration Limiting Platform Penetration in Community Settings

High capital costs significantly limit the adoption of laparoscopic platforms in the United States market. Intuitive reported that the standard sale or lease of a da Vinci system costs between USD 0.6 million and USD 3.1 million, with annual service fees ranging from USD 95,000 to USD 225,000 and per-procedure costs between USD 900 and USD 3,700. While large academic institutions and major health networks can absorb these costs, community hospitals and smaller surgical centers with limited budgets face challenges.[3]Intuitive Surgical, “Intuitive Announces First Quarter Earnings,” U.S. Securities and Exchange Commission, sec.gov This cost disparity slows the adoption of robotic technology in smaller facilities, creating a divided demand where some providers invest in advanced robotics while others opt for cost-effective disposables and incremental upgrades. Modular systems from newer entrants may address this gap over time, but current pricing remains a barrier to faster growth.

CMS Reimbursement Compression Narrowing Margin Headroom for Common Procedures

Reimbursement pressures in the United States laparoscopic devices market often prevent proportional margin growth despite rising procedure volumes. CMS policies encouraging cost-effective settings and tighter operating margins reduce the willingness to invest in premium disposables for routine procedures. This is particularly evident in high-volume categories like cholecystectomy, hernia repair, and appendectomy, where price sensitivity is higher than in complex specialty procedures. As ASC purchasing teams gain leverage, suppliers face increased pressure to justify premium features through operational benefits like faster turnover or reduced complications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Energy Devices Lead While Robotic Instrumentation Redefines the Growth Ceiling

In 2025, Energy Devices held a 29.45% share of the United States laparoscopic devices market, leading the product category. This reflects a shift from traditional electrosurgical methods to advanced vessel-sealing and tissue-management technologies, streamlining minimally invasive procedures. These devices are widely used in general surgery, gynecology, colorectal treatments, and bariatric surgery, ensuring consistent demand.

Hand Instruments, Closure and Stapling Devices, Access Devices, and Visualization Systems remain essential but are evolving with a focus on disposables, integrated workflows, and enhanced imaging. Single-use access products simplify logistics in outpatient settings, while advanced visualization stacks gain traction for their 3D, 4K, or fluorescence capabilities. Robotic-Assisted Laparoscopy Platforms and Instruments are projected to grow at an 8.12% CAGR through 2031, driven by Medtronic’s Hugo, Johnson & Johnson’s OTTAVA, and Intuitive’s expanding installed base.

By Application: General Surgery Anchors Volume While Gynecology Captures Growth Premium

In 2025, General Surgery accounted for 84.12% of the United States laparoscopic devices market, driven by high procedural volumes in cholecystectomy, appendectomy, and hernia repairs. This demand allows suppliers to bundle products into comprehensive contracts and provides market stability against specialty-specific fluctuations. The increasing adoption of robotic systems in general surgery is steering spending toward premium instruments and accessories.

Gynecological Surgery is expected to grow at a 7.95% CAGR through 2031, making it the fastest-growing segment. Intuitive reported an 11% increase in gynecological procedures using the da Vinci platform in 2025, highlighting strong demand for minimally invasive technologies. Gynecological surgeries often serve as a gateway for robotic adoption, with hospitals investing in platforms for multi-specialty use. While other specialties contribute to the market, they do not match the scale and growth of general surgery and gynecology.

By End User: Hospitals Retain Dominance as ASCs Set the Pace of Structural Shift

In 2025, hospitals held 44.18% of the United States laparoscopic devices market, driven by their role in handling complex cases and high-acuity procedures. Intuitive reported 6,477 da Vinci systems installed in hospitals and surgery centers as of Q1 2026, reflecting their dominance in advanced technologies. Hospitals remain key buyers of premium imaging and digital surgery ecosystems due to larger budgets and clinical goals, maintaining influence over technology standards.

Ambulatory Surgical Centers (ASCs) are projected to grow at an 8.25% CAGR through 2031, making them the fastest-growing segment. Policy changes, such as CMS expanding the ASC payable list and removing procedures from the Inpatient-Only list, are driving outpatient laparoscopic and robotic case migration. ASCs prioritize compact systems, mobile robotics, and consumable bundles tailored for high-throughput practices, positioning suppliers with such offerings for growth.

Geography Analysis

The Northeast remains a key region for adopting advanced medical technologies due to its dense network of academic medical centers and teaching hospitals, which lead in implementing premium robotic and visualization upgrades. These institutions influence surgeon preferences, procurement norms, and training pathways, driving both initial capital investments and recurring demand for instruments, accessories, imaging, and services as procedural intensity grows.

The Sun Belt is the fastest-growing region in the United States laparoscopic devices market, driven by a large ASC footprint, a significant Medicare-eligible population, and high demand for obesity-related and abdominal surgeries. States like Texas and Florida play a critical role in shaping national purchasing trends in bariatric, general, and colorectal surgeries. Additionally, expanding smoke evacuation mandates across states have increased the importance of integrated insufflation and operating room safety solutions, while outpatient growth and physician-owned surgical centers boost demand for compact systems and disposable products.

Competitive Landscape

The United States laparoscopic devices market is moderately concentrated, with Intuitive Surgical, Ethicon, Medtronic, Olympus, CONMED, and KARL STORZ leading in robotics, energy, visualization, and access categories. These companies leverage a recurring revenue model, where initial capital placements generate long-term income through instruments, accessories, services, and software. Once a platform is installed, associated consumables and accessories often remain in use for years, providing a competitive edge.

Medtronic expanded its portfolio by introducing the Hugo platform, which received FDA clearance in December 2025 and was first used commercially in February 2026. Johnson & Johnson demonstrated its intent to compete by submitting OTTAVA for FDA De Novo classification in January 2026, targeting upper-abdomen surgeries. Olympus raised the bar in imaging by launching VISERA ELITE III in March 2026, combining advanced features like True 4K, 3D, and ICG fluorescence into a software-upgradable platform.

Growth opportunities are strongest in compact robotics for ASCs and community hospitals, high-value imaging upgrades, and compliance-driven categories like smoke evacuation. The United States laparoscopic devices market is shifting toward a more competitive structure, where platform diversity and adaptability are critical. Companies that integrate flexible capital models, efficient consumable strategies, and outpatient-focused solutions are likely to drive the next phase of market share changes.

U.S. Laparoscopic Devices Industry Leaders

Medtronic plc

Stryker Corporation

Boston Scientific Corporation

Olympus Corporation

KARL STORZ Endoscopy-America, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Johnson & Johnson announced that the OTTAVA robotic surgical system met safety and performance goals in a 30-patient gastric bypass cohort, with all procedures completed robotically. This supported its FDA De Novo application for potential U.S. marketing authorization.

- March 2025: Olympus introduced the VISERA ELITE III surgical imaging platform in the U.S., featuring advanced imaging capabilities. A 2025 survey indicated strong surgeon support for its Yellow Enhancement feature in identifying critical structures during surgeries.

- February 2026: Medtronic conducted the first U.S. commercial surgery using the Hugo robotic-assisted system, a prostatectomy at Cleveland Clinic. The system targeted competition with Intuitive Surgical’s da Vinci system, with initial installations at leading hospitals.

- January 2026: Intuitive Surgical secured FDA 510(k) clearance for the da Vinci 5 system, expanding its indications to cardiothoracic surgery and adding a sixth specialty to its platform.

- January 2026: Johnson & Johnson submitted the OTTAVA Robotic Surgical System to the FDA for De Novo classification, seeking approval for upper-abdomen surgeries. The submission was supported by early 2025 IDE study data.

U.S. Laparoscopic Devices Market Report Scope

As per the scope of the report, laparoscopic Devices are specialized surgical instruments used in minimally invasive abdominal and pelvic surgeries. They allow surgeons to operate through tiny (0.5–1.5 cm) incisions using a tiny camera (laparoscope) and long, thin tools rather than making large cuts.

The U.S. laparoscopic devices market is segmented by product, application, and end-user. By product, the market includes visualization systems and laparoscopes (rigid laparoscopes, flexible/deflectable laparoscopes, camera heads and video processors, light sources, and 3D/4K/fluorescence imaging platforms), access devices (trocars and cannulas, Veress needles, and others), insufflation and smoke management (insufflators, tubing sets, and smoke evacuation systems), hand instruments (graspers, dissectors, scissors, needle holders, retractors, and others), energy devices (advanced bipolar vessel sealing, ultrasonic energy devices, and others), closure and stapling devices (endoscopic linear staplers, circular staplers used in laparoscopic procedures, reloads and buttressing materials, and sutures and ligation clips), suction, irrigation, and retrieval devices (suction-irrigation systems and specimen retrieval bags), cholangiography and ancillary devices, and robotic-assisted laparoscopy platforms and accessories (multiport robotic platforms, miniaturized/table-mounted robotic platforms, robotic-compatible access and insufflation accessories, and robotic stapling and energy instruments). By application, the market is categorized into general surgery, bariatric surgery, gynecological surgery, urological surgery, colorectal surgery, and thoracic and other laparoscopic-adjacent MIS procedures. By end-user, the market is segmented into hospitals, ambulatory surgical centers, specialty clinics and office-based surgical centers, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Visualization Systems and Laparoscopes | Rigid Laparoscopes |

| Flexible / Deflectable Laparoscopes | |

| Camera Heads and Video Processors | |

| Light Sources | |

| 3D / 4K / Fluorescence Imaging Platforms | |

| Access Devices | Trocars and Cannulas |

| Veress Needles | |

| Others | |

| Insufflation and Smoke Management | Insufflators |

| Tubing Sets | |

| Smoke Evacuation Systems | |

| Hand Instruments | Graspers |

| Dissectors | |

| Scissors | |

| Needle Holders | |

| Retractors | |

| Others | |

| Energy Devices | Advanced Bipolar Vessel Sealing |

| Ultrasonic Energy Devices | |

| Others | |

| Closure and Stapling Devices | Endoscopic Linear Staplers |

| Circular Staplers Used in Laparoscopic Procedures | |

| Reloads and Buttressing Materials | |

| Sutures and Ligation Clips | |

| Suction, Irrigation, and Retrieval Devices | Suction-Irrigation Systems |

| Specimen Retrieval Bags | |

| Cholangiography and Ancillary Devices | |

| Robotic-Assisted Laparoscopy Platforms and Accessories | Multiport Robotic Platforms |

| Miniaturized / Table-Mounted Robotic Platforms | |

| Robotic-Compatible Access and Insufflation Accessories | |

| Robotic Stapling and Energy Instruments |

| General Surgery |

| Bariatric Surgery |

| Gynecological Surgery |

| Urological Surgery |

| Colorectal Surgery |

| Thoracic and Other Laparoscopic-Adjacent MIS Procedures |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics and Office-Based Surgical Centers |

| Others |

| By Product | Visualization Systems and Laparoscopes | Rigid Laparoscopes |

| Flexible / Deflectable Laparoscopes | ||

| Camera Heads and Video Processors | ||

| Light Sources | ||

| 3D / 4K / Fluorescence Imaging Platforms | ||

| Access Devices | Trocars and Cannulas | |

| Veress Needles | ||

| Others | ||

| Insufflation and Smoke Management | Insufflators | |

| Tubing Sets | ||

| Smoke Evacuation Systems | ||

| Hand Instruments | Graspers | |

| Dissectors | ||

| Scissors | ||

| Needle Holders | ||

| Retractors | ||

| Others | ||

| Energy Devices | Advanced Bipolar Vessel Sealing | |

| Ultrasonic Energy Devices | ||

| Others | ||

| Closure and Stapling Devices | Endoscopic Linear Staplers | |

| Circular Staplers Used in Laparoscopic Procedures | ||

| Reloads and Buttressing Materials | ||

| Sutures and Ligation Clips | ||

| Suction, Irrigation, and Retrieval Devices | Suction-Irrigation Systems | |

| Specimen Retrieval Bags | ||

| Cholangiography and Ancillary Devices | ||

| Robotic-Assisted Laparoscopy Platforms and Accessories | Multiport Robotic Platforms | |

| Miniaturized / Table-Mounted Robotic Platforms | ||

| Robotic-Compatible Access and Insufflation Accessories | ||

| Robotic Stapling and Energy Instruments | ||

| By Application | General Surgery | |

| Bariatric Surgery | ||

| Gynecological Surgery | ||

| Urological Surgery | ||

| Colorectal Surgery | ||

| Thoracic and Other Laparoscopic-Adjacent MIS Procedures | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics and Office-Based Surgical Centers | ||

| Others | ||

Key Questions Answered in the Report

What is driving growth in U.S. laparoscopic devices through 2031?

Growth is being supported by outpatient migration, ASC reimbursement support, robotic adoption, and continued demand for advanced energy and visualization tools. The market is valued at USD 3.27 billion in 2026 and is forecast to reach USD 6.64 billion by 2031 at a 7.25% CAGR.

Which product category leads device demand in the United States?

Energy Devices are the leading product segment, holding 29.45% share in 2025 because they are widely used across high-volume minimally invasive procedures.

Which application area is growing the fastest?

Gynecological Surgery is the fastest-growing application, with a projected 7.95% CAGR through 2031, supported by rising robotic use in benign hysterectomy and related procedures.

Why are ASCs becoming more important for laparoscopic equipment suppliers?

ASCs are the fastest-growing end-user group at an 8.25% CAGR through 2031. CMS added 547 procedures to the ASC payable list for 2026, which expands outpatient opportunities for laparoscopic and robotic systems.

How is robotic competition changing the surgical devices space in the United States?

Intuitive remains the leading robotic player, but Medtronic entered the U.S. market with Hugo and Johnson & Johnson has advanced OTTAVA with an FDA De Novo submission. This is expanding platform choice and raising pressure on instrument and accessory pricing.

What is the biggest restraint on wider robotic penetration?

Capital intensity remains the biggest barrier. Intuitive reported da Vinci system pricing at USD 0.6 million to USD 3.1 million, plus annual service and per-procedure accessory costs, which limits adoption in smaller community settings.

Page last updated on: