Asia-Pacific Bariatric Surgery Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

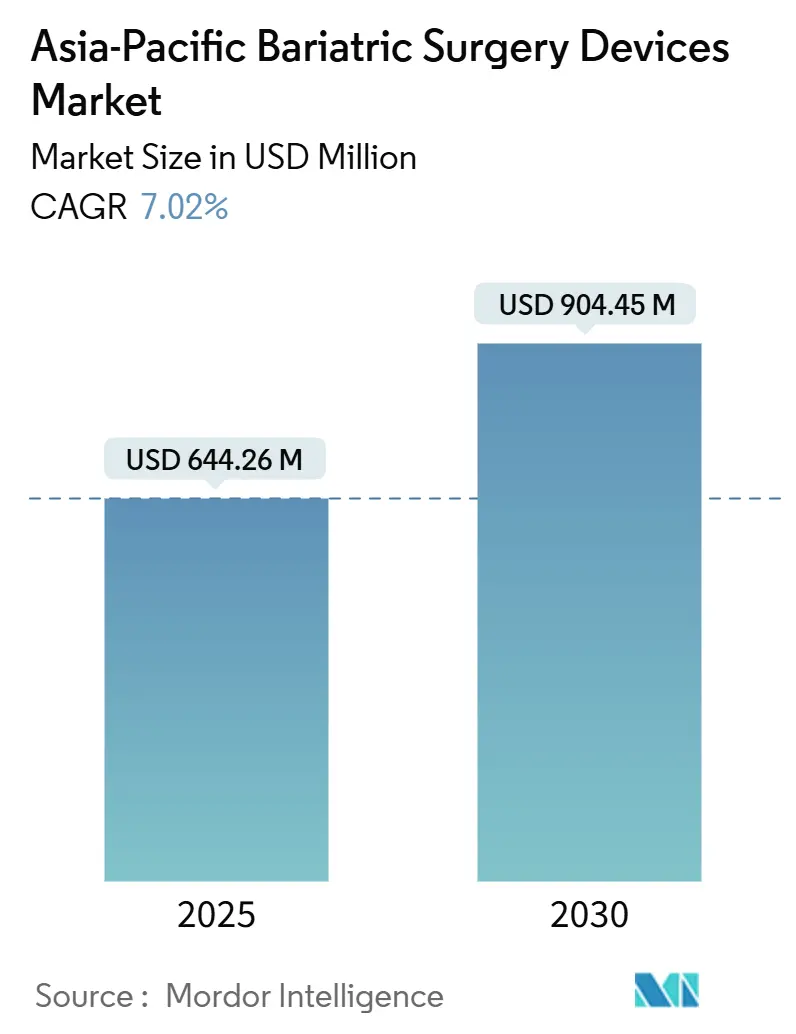

| Market Size (2025) | USD 644.26 Million |

| Market Size (2030) | USD 904.45 Million |

| Growth Rate (2025 - 2030) | 7.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Bariatric Surgery Devices Market Analysis by Mordor Intelligence

The Asia-Pacific bariatric surgery devices market size stood at USD 644.26 million in 2025 and is projected to reach USD 904.45 million by 2030, advancing at a 7.02% CAGR over the forecast period. Steady expansion comes from rising obesity prevalence, widening reimbursement, and procedure innovation, even as GLP-1 medications begin to divert a subset of borderline-BMI candidates. Sleeve gastrectomy keeps the highest procedure volumes because of its short operative time and low leak risk, yet endoscopic sleeve gastroplasty (ESG) and implantable balloons are delivering faster growth thanks to day-care pathways and minimal invasiveness. Device demand remains concentrated in staplers, suturing systems, and other consumables that anchor every laparoscopic or robotic case. China contributes nearly one-half of regional revenue, but India shows the quickest pace as private hospitals court medical tourists and employers add metabolic surgery to wellness benefits. Competitive intensity is climbing, led by Chinese robotic systems that under-price Western incumbents and by endoscopy vendors promoting suture-based “procedure-less” alternatives.

Key Report Takeaways

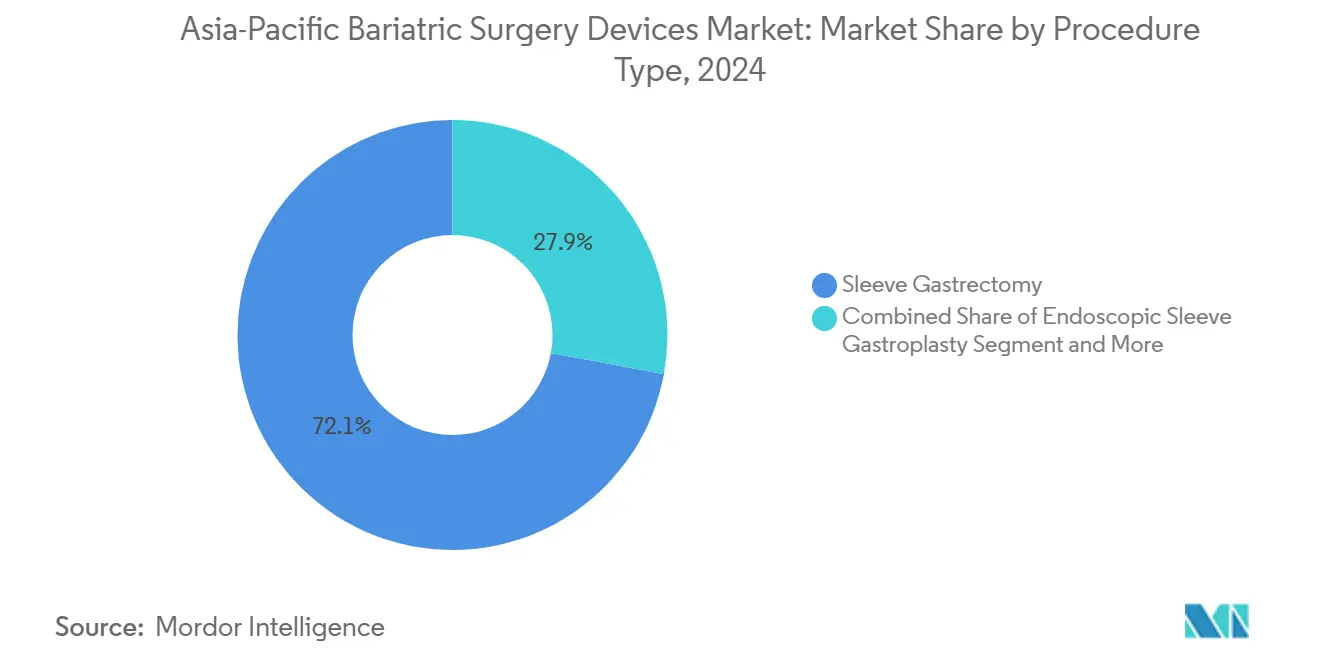

- By procedure type, sleeve gastrectomy led with 72.12% share in 2024; endoscopic sleeve gastroplasty is forecast to expand at an 8.6% CAGR to 2030.

- By device type, assisting devices captured 58.1% of revenue in 2024; implantable devices are projected to grow at a 9.8% CAGR through 2030.

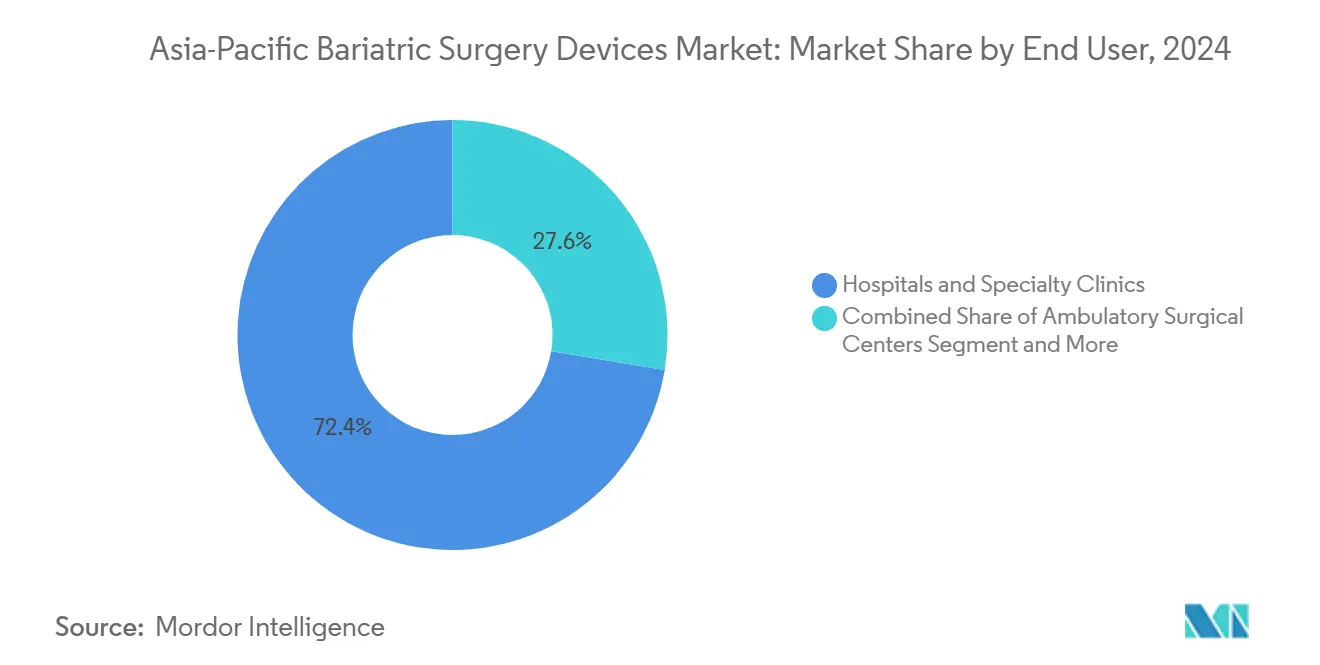

- By end user, hospitals and specialty clinics accounted for 72.4% of 2024 revenue; ambulatory surgical centers are advancing at a 9.7% CAGR to 2030.

- By patient age group, adults 18-64 years represented 45.5% of 2024 volume; adolescent procedures are increasing at an 8.7% CAGR during 2025-2030.

- By geography, China contributed 46.5% of 2024 revenue; India is expected to post the fastest 8.2% CAGR up to 2030.

Asia-Pacific Bariatric Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Obesity Prevalence and Cardiometabolic Disease Burden | +1.8% | Global, with highest absolute burden in China (402M adults overweight/obese) and India (180M adults) | Long term (≥ 4 years) |

| Preference for Minimally Invasive and Day-Care Pathways | +1.2% | APAC core (Japan, South Korea, Australia), spill-over to urban China and India | Medium term (2-4 years) |

| Growing Reimbursement and Guideline Expansion for Metabolic Surgery in APAC | +1.5% | South Korea, Japan (NHI coverage), Australia (MBS items), China (NHSA provincial pilots) | Medium term (2-4 years) |

| Rapid Uptake of Endoscopic Bariatric Options (ESG/TORe) and Targeted Robotics Adoption | +1.0% | Urban centers in China, India, Japan, Australia; early adoption in Singapore, Malaysia | Short term (≤ 2 years) |

| Bariatric Surgery Shown More Cost-Effective Than Other Long-Term Therapies | +0.8% | Australia (MBS modeling), South Korea (NHI cost-benefit studies), Japan (NHI pricing reviews) | Long term (≥ 4 years) |

| Employer-Sponsored Coverage, COE Pathways, and Wellness Incentives in Private Markets | +0.5% | India (corporate wellness programs), China (private insurance riders), Singapore (MediSave eligibility) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Obesity Prevalence and Cardiometabolic Disease Burden

China and India together host 582 million adults living with overweight or obesity, a figure that underpins sustained procedure demand. Asians develop visceral adiposity and type 2 diabetes at lower BMI levels, prompting guideline bodies to recommend surgery from BMI ≥27.5 when diabetes is present. Revised national rules in South Korea and Singapore therefore expand eligibility to younger and lower-BMI cohorts, explaining why adolescent procedures are growing faster than any adult segment.

Preference for Minimally Invasive and Day-Care Pathways

Payers are steering cases toward laparoscopy, robotics, and ESG so that patients can leave the hospital the same day, freeing beds and lowering bundled costs. Japan’s National Health Insurance and Australia’s Medicare Benefits Schedule both reimburse same-day metabolic surgery, while the Intuitive SureForm 30 curved stapler and Boston Scientific’s OverStitch NXT make shorter operative times feasible[1]U.S. Food and Drug Administration, “510(k) Premarket Notification: SureForm 30,” fda.gov.

Growing Reimbursement and Guideline Expansion for Metabolic Surgery in APAC

Coverage wins keep unlocking latent demand: South Korea’s 2019 benefit addition lifted national volumes fourfold within three years, and Japan’s 2024 inclusion of semaglutide proves policymakers will subsidize weight-management tools across both surgery and pharmacotherapy. China’s NHSA remains cautious, yet several provinces now pilot partial coverage.

Rapid Uptake of Endoscopic Bariatric Options and Targeted Robotics Adoption

A decade of clinical follow-up confirms ESG durability, and OverStitch’s global rollout supplies the only FDA-cleared suturing system dedicated to ESG, helping urban Asian centers launch day-care bariatric programs. In robotics, Shanghai MicroPort MedBot’s Toumai platform has cleared 12,000 cases and secured remote-surgery approval, while Medicaroid’s hinotori offers Japan a domestic alternative.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Procedure and Device Costs; Capital and Disposables | -0.9% | India (private-pay dominance), China (limited public reimbursement), rural APAC | Short term (≤ 2 years) |

| Post-Operative Complications and Long-Term Follow-Up Burden | -0.4% | Global, with higher readmission rates in centers lacking multidisciplinary teams | Long term (≥ 4 years) |

| Rising Adoption and Awareness of GLP-1 Weight-Loss Medications | -0.7% | China (Wegovy NHI coverage Nov 2024), Japan (semaglutide approved 2023), urban centers globally | Short term (≤ 2 years) |

| Surgeon Capacity Constraints and COE Volume Requirements Limiting Throughput | -0.3% | Rural China, India (tier-2/3 cities), Southeast Asia (limited training infrastructure) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Procedure and Device Costs; Capital and Disposables

Total episode costs span USD 5,000–15,000 in Asia, with robotics lifting per-case consumables to USD 2,000-3,000. India’s Ayushman Bharat cap rarely covers a full sleeve gastrectomy, and China’s NHSA catalog omits the procedure altogether, pushing most patients to self-pay or seek employer help.

Post-Operative Complications and Long-Term Follow-Up Burden

Staple-line leaks, micronutrient deficiencies, and internal hernias demand lifelong multidisciplinary care, yet rural Asia often lacks endocrinologists and dietitians. A PLOS One review shows financial and travel hurdles cause many low-income patients to disengage from follow-up once early weight loss goals are met.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Procedure Type: Sleeve Gastrectomy Dominance Masks Endoscopic Disruption

The Asia-Pacific bariatric surgery devices market share for sleeve gastrectomy reached 72.12% in 2024, while ESG volume is set to rise at an 8.6% CAGR. Sleeve gastrectomy keeps leadership due to simpler technique and fewer leaks than Roux-en-Y gastric bypass, yet its growth trails ESG, which achieves 13.6% total body-weight loss with only 1.25% serious adverse events.

Despite maturity, sleeve gastrectomy remains first line for BMI ≥35, whereas Roux-en-Y retains a niche for severe reflux or super-obesity. Adjustable gastric banding has largely exited guidelines, and OAGB gains followers in India and Southeast Asia for shorter operative times. Allurion’s swallowable balloon broadens the pool of BMI 27-35 candidates who prefer a non-surgical approach.

By Device Type: Staplers and Suturing Systems Anchor Revenue, Implantables Accelerate

Assisting devices generated 58.1% of 2024 revenue, reflecting 3-5 cartridges and pairs of trocars consumed per case. The Asia-Pacific bariatric surgery devices market size for implantables will expand fastest at a 9.8% CAGR on swallowable balloons such as Elipse, which now tops 100,000 global placements.

Advances include Ethicon’s adjustable-height cartridges that cut leak risk, Intuitive’s force-sensing curved stapler, and Boston Scientific’s OverStitch NXT, the only dedicated ESG suturing system. Chinese low-cost trocars undercut multinationals by 30-40%, widening price pressure in commoditized accessories.

By End User: Hospitals Retain Volume, ASCs Capture Growth

Hospitals and specialty clinics held 72.4% revenue in 2024, but ASCs are projected to log a 9.7% CAGR. The Asia-Pacific bariatric surgery devices market size in ASC settings is rising as insurers reimburse same-day discharge, and Getinge-Zimmer Biomet’s 2025 alliance targets equipping these centers with turnkey operating-room platforms.

ESG’s incision-less profile suits outpatient care, slashing total costs by up to 50% compared with laparoscopy. Robotics vendors now offer smaller footprints and remote guidance to meet ASC space limits, bolstering adoption outside big tertiary hospitals.

By Patient Age Group: Adults Dominate, Adolescents Accelerate

Adults aged 18-64 years supplied 45.5% of 2024 volume, yet adolescent surgeries are climbing at an 8.7% CAGR thanks to lowered BMI thresholds. South Korea authorizes surgery for adolescents when BMI ≥35 or 120% of the 95th percentile with comorbidities, and Allurion’s trial shows its balloon safe for 15-17-year-olds who dislike permanent gastric alteration.

Geriatric demand also grows as ESG and balloons avoid lengthy anesthesia. Japan’s aged population values mobility gains and reduced polypharmacy, pushing low-risk options. Ethnicity-adjusted criteria in Singapore and Australia likewise swell eligible pools across all ages.

Geography Analysis

China contributed 46.5% of Asia-Pacific bariatric surgery devices market revenue in 2024, aided by a 402 million-person obesity burden and rapid uptake of domestic robots. Remote-surgery clearance in 2025 lets Toumai specialists cover rural counties, though NHSA still excludes surgery from the national catalog, dampening penetration[2]MicroPort MedBot, “Interim Report 2025,” ir.medbotsurgical.com.

India is forecast to deliver the fastest 8.2% CAGR through 2030. Private hospitals bundle bariatric surgery with medical tourism packages priced 50-70% below Western peers, and KKR’s purchase of Healthium Medtech underscores investor confidence in a consumables-driven market. Patchy public funding persists, yet employer plans and PMJAY pilots are widening access.

Japan, Australia, and South Korea show mature but steady trajectories. National insurers in all three markets reimburse sleeve gastrectomy and, increasingly, ESG. South Korea quadrupled annual surgical volumes within three years of adding coverage, yet further upside remains owing to guidelines that now permit operations from BMI 27.5 with diabetes.

Competitive Landscape

The Asia-Pacific bariatric surgery devices market is moderately concentrated. Intuitive Surgical keeps headline share through its da Vinci installed base and SureForm consumables, while acknowledging GLP-1-linked softness in U.S. bariatric volumes[3]U.S. Securities and Exchange Commission, “Intuitive Surgical Form 10-K 2024,” sec.gov. Shanghai MicroPort MedBot offers comparable robotics at 60-70% of da Vinci cost and has logged over 12,000 cases, including 500 remote procedures, challenging incumbents at the top end.

Boston Scientific controls ESG hardware after acquiring Apollo Endosurgery, and OverStitch now anchors most endoscopic sleeves. Ethicon, Medtronic, and local Chinese manufacturers dominate staplers, energy devices, and trocars, with Healthium Medtech’s discounted accessories widening price competition. In procedureless devices, Allurion leads but still reaches <5% of its potential Chinese and Indian base, signaling room for growth or future partnership deals.

Asia-Pacific Bariatric Surgery Devices Industry Leaders

Intuitive Surgical Inc.

Olympus Corp.

Medtronic plc

Johnson and Johnson

Boston Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: President of IRCAD India performed a long-distance robotic bariatric telesurgery, highlighting near-term viability of 5G-enabled remote care.

- April 2025: MicroPort MedBot’s Toumai Remote system obtained NMPA approval, the world’s first registered remote surgical robot, and has since completed 500 bariatric and other procedures.

Asia-Pacific Bariatric Surgery Devices Market Report Scope

Bariatric surgery devices are specialized medical tools and implants used to assist weight loss procedures in patients with obesity. These devices help reduce stomach capacity, alter digestion, or promote feelings of fullness to facilitate significant and sustained weight reduction. Examples include gastric bands, gastric balloons, and other implantable or removable devices designed for bariatric interventions.

The Asia-Pacific bariatric surgery devices market is segmented by procedure type, which includes sleeve gastrectomy, Roux-en-Y gastric bypass, adjustable gastric banding, biliopancreatic diversion with duodenal switch, one anastomosis gastric bypass, endoscopic sleeve gastroplasty, and other procedures. By device type, the market is categorized into assisting devices, such as suturing devices, closure devices, stapling devices, trocars, and other assisting devices, as well as implantable devices, including gastric bands, electrical stimulation devices, gastric balloons, gastric emptying devices, and other devices. By end user, the market is segmented into hospitals & specialty clinics, bariatric surgery centers, ambulatory surgical centers, and others. By patient age group, the market is divided into adolescents (12–17), adults (18–64), and geriatric (≥65). For each segment, the market size is provided in terms of value (USD).

| Sleeve Gastrectomy |

| Roux-en-Y Gastric Bypass |

| Adjustable Gastric Banding |

| Biliopancreatic Diversion with Duodenal Switch |

| One Anastomosis Gastric Bypass |

| Endoscopic Sleeve Gastroplasty |

| Other Procedures |

| Assisting Devices | Suturing Device |

| Closure Device | |

| Stapling Device | |

| Trocars | |

| Other Assisting Devices | |

| Implantable Devices | Gastric Bands |

| Electrical Stimulation Devices | |

| Gastric Balloons | |

| Gastric Emptying | |

| Other Devices |

| Hospitals & Specialty Clinics |

| Dedicated Bariatric Surgery Centers |

| Ambulatory Surgical Centers |

| Others |

| Adolescents (12-17) |

| Adults (18-64) |

| Geriatric (Greater than 64) |

| China |

| India |

| Japan |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Procedure Type | Sleeve Gastrectomy | |

| Roux-en-Y Gastric Bypass | ||

| Adjustable Gastric Banding | ||

| Biliopancreatic Diversion with Duodenal Switch | ||

| One Anastomosis Gastric Bypass | ||

| Endoscopic Sleeve Gastroplasty | ||

| Other Procedures | ||

| By Device Type | Assisting Devices | Suturing Device |

| Closure Device | ||

| Stapling Device | ||

| Trocars | ||

| Other Assisting Devices | ||

| Implantable Devices | Gastric Bands | |

| Electrical Stimulation Devices | ||

| Gastric Balloons | ||

| Gastric Emptying | ||

| Other Devices | ||

| By End User | Hospitals & Specialty Clinics | |

| Dedicated Bariatric Surgery Centers | ||

| Ambulatory Surgical Centers | ||

| Others | ||

| By Patient Age Group | Adolescents (12-17) | |

| Adults (18-64) | ||

| Geriatric (Greater than 64) | ||

| By Country | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific bariatric surgery devices market in 2025?

It is valued at USD 644.26 million and is projected to grow to USD 904.45 million by 2030.

Which procedure generates the most device demand today?

Sleeve gastrectomy accounts for 72.12% of procedures, driving the bulk of stapler and trocar consumption.

What is the fastest-growing device segment?

Implantable devices, mainly swallowable balloons, are forecast to expand at a 9.8% CAGR between 2025 and 2030.

Why are ambulatory surgical centers gaining share?

Payers reimburse same-day discharge, and ESG's incision-less profile lets patients leave within hours, pushing ASC revenue up at a 9.7% CAGR.

How do GLP-1 medications affect surgery demand?

They divert some BMI 30-35 candidates, yet 50-70% discontinuation within the first year limits long-term substitution.

Which country will post the quickest growth?

India is expected to record an 8.2% CAGR through 2030, helped by private-hospital investment and medical-tourism inflows.

Page last updated on: