Laparotomy Sponges Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 1.83 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

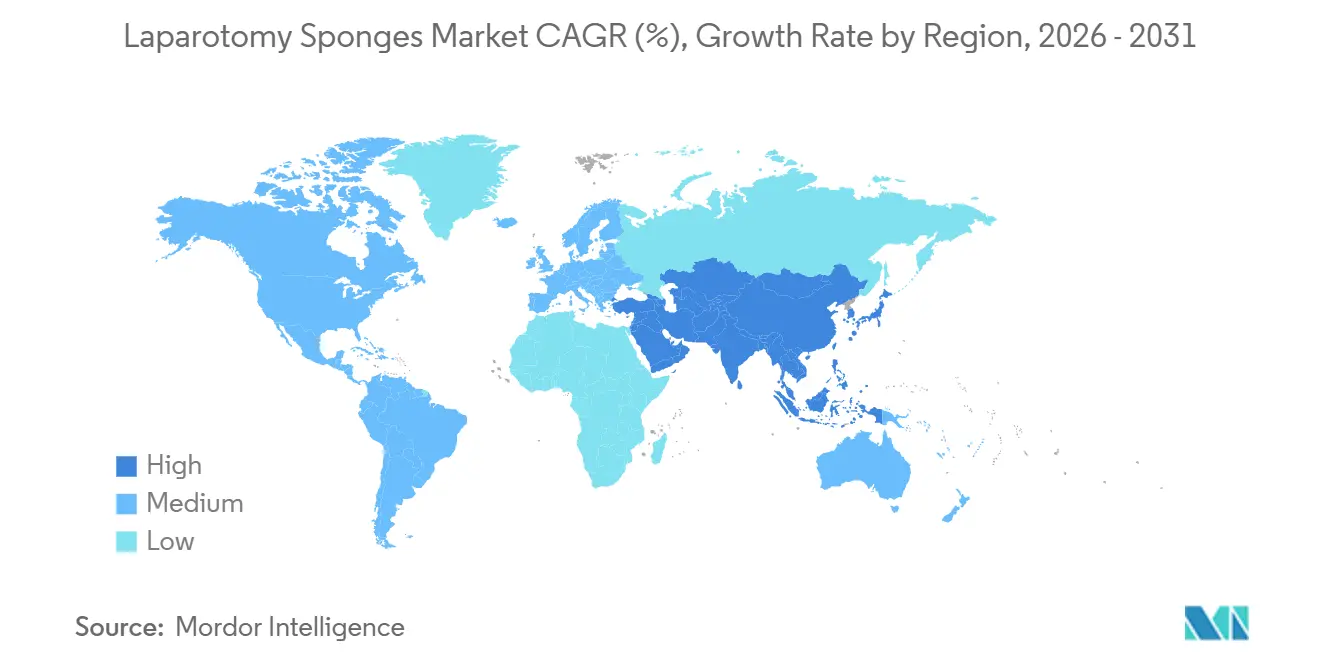

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laparotomy Sponges Market Analysis by Mordor Intelligence

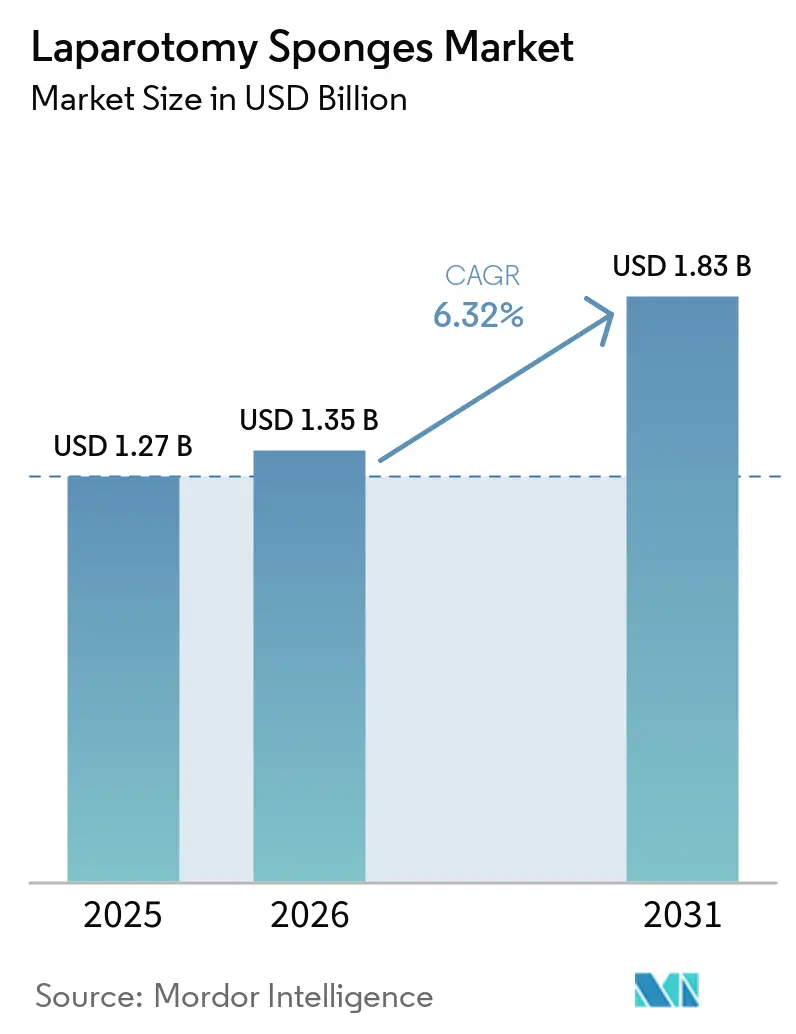

The Laparotomy Sponges Market was valued at USD 1.27 billion in 2025 and is projected to grow to USD 1.35 billion in 2026, reaching USD 1.83 billion by 2031. The market is expected to register a CAGR of 6.32% during the forecast period of 2026-2031.

Demand is accelerating because hospitals now see every sponge as a liability-control device rather than a low-value consumable. Hospitals in North America have begun embedding RFID tags or barcodes that integrate with AI-count platforms to meet Joint Commission Universal Protocol rules, while California’s SB 707 is nudging early adopters toward biodegradable composites. At the same time, the Centers for Medicare & Medicaid Services (CMS) expanded the ASC Covered-Procedures List in 2026, pushing higher-acuity procedures into ambulatory surgical centers and rewarding suppliers that can ship pre-sterilized single-use packs optimized for rapid turnover. Asia-Pacific is emerging as the fastest-growing region as India’s Union Budget 2026-27 injects USD 12.7 billion into trauma centers, district hospitals, and clinical-trial sites, widening the installed base of operating rooms that rely on radiopaque or RFID-enabled sponges.

Key Report Takeaways

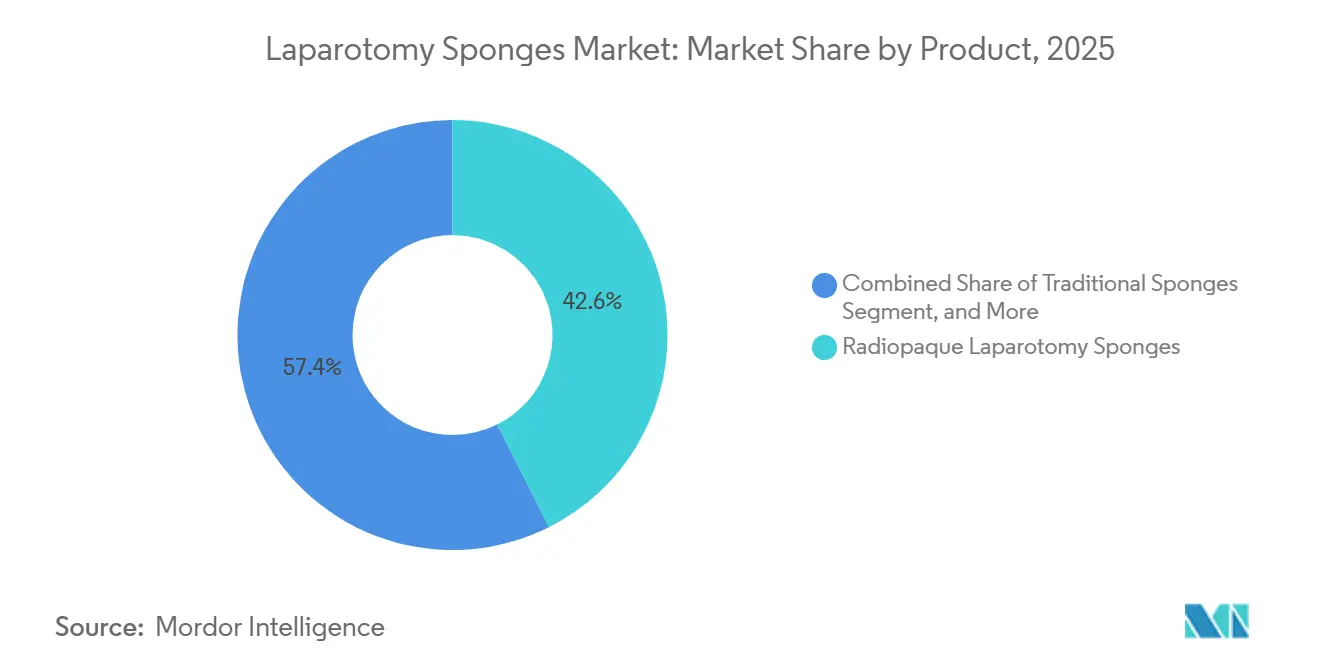

- By product, radiopaque variants are expected to lead the laparotomy sponges market with a 42.57% share in 2025, while RFID-enabled sponges are forecast to expand at a 7.56% CAGR through 2031.

- By material, cotton is projected to account for 34.78% of the laparotomy sponges market share in 2025. Rayon and viscose are expected to witness significant growth, with a CAGR of 7.54% projected through 2031.

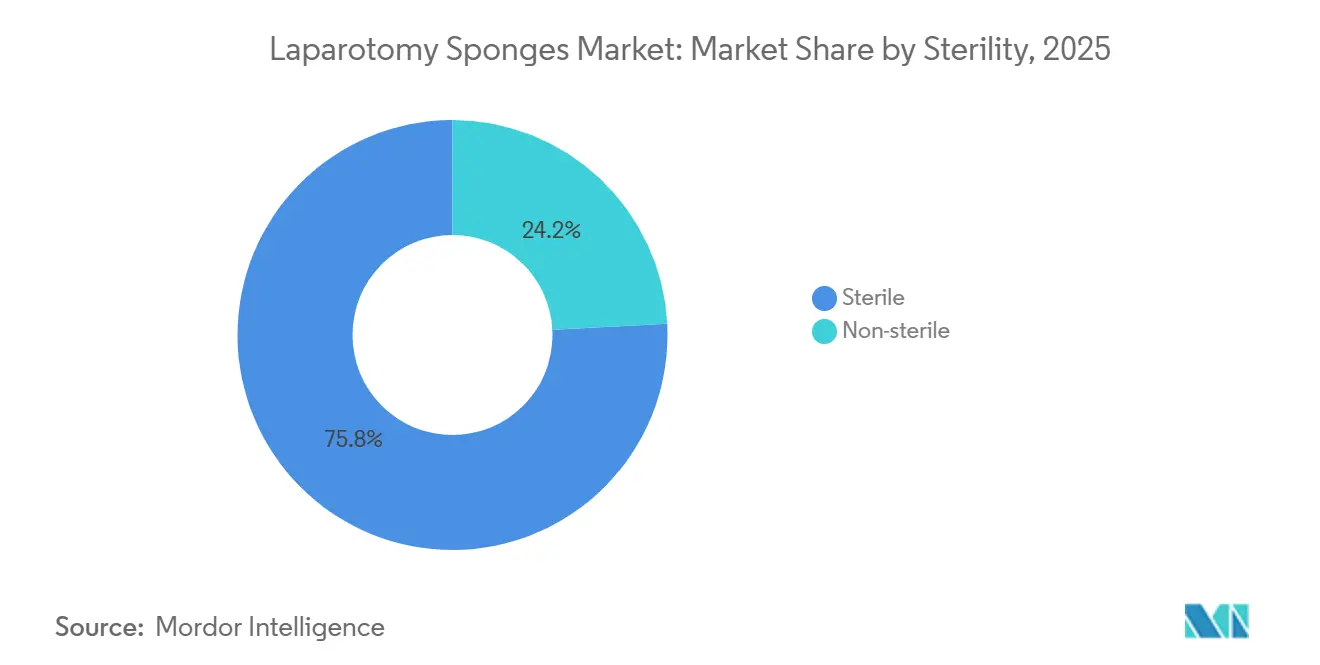

- By sterility, sterile sponges are forecast to account for 75.84% of the laparotomy sponges market size in 2025, while non-sterile products are expected to grow at an 8.59% CAGR through 2031.

- By end-user, hospitals and clinics are anticipated to hold 63.28% of sales in 2025, whereas ambulatory surgical centers are forecast to advance at a 9.41% CAGR through 2031.

- By geography, North America is forecast to capture a 38.49% revenue share in 2025, and Asia-Pacific is expected to grow at a 12.68% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Laparotomy Sponges Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Volume of Surgical Procedures | +1.8% | Global, strongest in APAC and Middle East | Medium term (2-4 years) |

| Growing Focus on Surgical Safety & RSI Prevention | +1.5% | North America & EU with spill-over to APAC and MEA | Short term (≤ 2 years) |

| Technological Advancements (radiopaque, RFID, AI) | +1.2% | North America, Western Europe, pilot sites in APAC | Medium term (2-4 years) |

| Expansion of Healthcare Infrastructure in Emerging Markets | +1.0% | APAC, GCC, Sub-Saharan Africa | Long term (≥ 4 years) |

| AI-Enabled Real-Time Sponge-Count Systems | +0.6% | North America (academic medical centers, large systems) | Short term (≤ 2 years) |

| Sustainability Mandates Boosting Biodegradable Sponges | +0.3% | California, EU, pilots in Canada and Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Volume of Surgical Procedures

Global case counts continue to climb, yet day-surgery protocols now dominate at major centers such as West China Hospital, where same-day procedures rose from 6.16% to 25.11% of total surgical volume and cut costs by 15%.[1]World Bank, “Hospitals in Health Systems,” India’s 2026-27 budget channels USD 4.7 billion into the National Health Mission and USD 573 million into PM-ABHIM, creating new OR capacity but driving volume toward price-sensitive tenders. Consequently, suppliers must package sponges with logistics, consignment, or count-verification services to protect margins.

Growing Focus on Surgical Safety & RSI Prevention

AORN and the American College of Surgeons updated guidelines in 2024 to recommend radiopaque or RFID adjuncts when manual counts are unreliable. The Joint Commission recorded 119 RSI sentinel events in 2024; each costs hospitals roughly USD 525,000, so risk officers now prioritize traceability tools over unit price. Augustine Biomedical’s 2024 RFID patent shows the technical path forward, allowing tags to survive 134 °C autoclaves.[2]Augustine Biomedical, “U.S. Patent 12,255,380 B2,” Liability fears are therefore shifting purchasing power from supply managers to clinical-quality teams.

Technological Advancements (Radiopaque, RFID, AI-Analytics)

Radiopaque threads remain standard, but the competitive edge now comes from digital integration. FDA 510(k) clearances in 2024-2025 including GELITA-SPON, PROTEC, and Triton validate passive-tracking systems. Early adopters have cut count-verification time by up to 30%, translating into higher case throughput and lower RSI risk. European growth trails the United States because GDPR questions still cloud RFID data handling, with clarity expected once EUDAMED becomes mandatory in May 2026.

Expansion of Healthcare Infrastructure in Emerging Markets

Asia-Pacific leads volume growth as India allocates USD 12.7 billion to new trauma centers and China scales provincial purchasing alliances. B. Braun has invested more than EUR 800 million (USD 936 million) in automated sterile-goods factories to supply high-volume tenders at competitive cost. Public procurement favors domestic or localized production, so multinationals must partner or build local plants to win commodity contracts while marketing RFID upgrades to private tertiary hospitals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Minimally Invasive / Hemostatic Substitutes | -1.4% | North America, Western Europe, urban APAC | Medium term (2-4 years) |

| Regulatory & Compliance Burden | -0.5% | North America, EU | Short term (≤ 2 years) |

| Cotton-Price Volatility & Supply-Chain Disruptions | -0.4% | Global | Short term (≤ 2 years) |

| Data-Privacy Concerns Slowing RFID Uptake | -0.3% | EU, North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Minimally Invasive / Hemostatic Substitutes

Robotic surgery’s share of U.K. general surgery rose from 0.4% in 2015 to 7.0% in 2024 and is on track to eclipse open techniques within five years.[3]Donald N. et al., “Adoption and Expansion of Robotic Surgery Across General Surgery in the United Kingdom,” U.S. hospitals using robotic platforms push MIS rates above 65%, cutting sponge consumption per case by up to 60%. New hemostatic agents such as chitosan-copper composites further displace traditional sponges in high-bleed fields. Suppliers must therefore redesign products for laparoscopic ports and fluoroscopic visibility or risk volume loss.

Regulatory & Compliance Burden

The MDR’s EUDAMED registration deadline of May 28, 2026, and FDA’s biocompatibility dossiers impose costs that small manufacturers struggle to fund. Cardinal Health’s FY2026 filing notes tariffs and compliance expenses squeezing segment profit, illustrating how even scale players face pressure.[4]USDA, “Cotton Market and Trade Data,” Consolidation will accelerate as regional firms exit or sell, concentrating innovation among companies that can amortize regulatory overhead across global volumes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: RFID Variants Gain as Liability Costs Outweigh Unit Premiums

Radiopaque sponges commanded 42.57% of the laparotomy sponges market share in 2025, reaffirming their role as the baseline safety standard. RFID-enabled products, however, are projected at a 7.56% CAGR through 2031 as hospitals weigh USD 525,000 average RSI liability against a 30-50% price premium. Augustine Biomedical’s 2024 patent, which allows RFID tags to survive 134 °C autoclaving, removes a technical barrier to adoption.

Hospitals in litigation-prone markets are layering RFID on top of radiopaque threads, while cash-strapped public hospitals in India and Africa still opt for manual counts. The bifurcation forces suppliers to market dual portfolios: premium RFID packs for trauma and transplant centers and low-cost radiopaque lines for routine appendectomies, an approach that maximizes reach across the laparotomy sponges market.

By Material: Antimicrobial Coatings Emerge as Cotton Faces Price Swings

The laparotomy sponges market saw cotton account for 34.78% of its share in 2025. Rayon and viscose are anticipated to witness significant growth, with a projected CAGR of 7.54% through 2031. Cotton dominated shipments in 2025 thanks to supply chains in India, Brazil, and the United States, though spot prices fluctuated between 60 and 78 per pound and exposed buyers to cost risk. Rayon and viscose blends are gaining share among health-system group purchasing organizations that lock in multi-year contracts for price stability.

Regulators in California and the EU are pushing biodegradable PLA and PHA options, yet unit prices remain 2-3 × higher than cotton. Antimicrobial silver-copper coatings are penetrating colorectal and trauma surgeries where infection risk is greatest, letting suppliers defend margins through outcome-based value propositions within the laparotomy sponges market size.

By Sterility: Non-Sterile Growth Reflects ASC Point-of-Use Sterilization

Sterile packs retained 75.84% share in 2025 because hospitals value contamination control. Ambulatory surgical centers, however, sterilize in-house to save carrying costs, driving non-sterile variants at an 8.59% CAGR and underscoring how care-site migration reshapes the laparotomy sponges market. EU MDR compliance costs could slow non-sterile adoption in Europe, whereas North American ASCs will keep favoring in-house sterilization to shorten lead times.

By End-User: ASCs Capture High-Acuity Procedures, Hospitals Defend Complex Cases

Hospitals accounted for 63.28% of demand in 2025 on the back of complex oncology and transplant workloads that consume high volumes of RFID or antimicrobial products. The 9.41% CAGR at ASCs reflects CMS policy shifts that allow total hip arthroplasty and colorectal resections in outpatient settings. Suppliers therefore build tiered catalogs: broad commodity-to-premium ranges for hospital systems and high-throughput single-use kits for ASC chains, keeping products aligned with every buying center across the laparotomy sponges industry.

Geography Analysis

North America led with 38.49% revenue share in 2025 as RSI litigation costs pushed hospitals toward RFID and AI-count systems. Each sentinel event averages USD 525,000, so purchasing committees now treat sponges as risk-mitigation tools. CMS’s 2026 ASC rule is fragmenting demand and favoring suppliers that preload sponges into sterile high-throughput kits, sustaining growth despite tariff-driven margin pressure flagged by Cardinal Health’s FY2026 update.

Asia-Pacific will post the fastest 12.68% CAGR through 2031 thanks to India’s USD 12.7 billion healthcare allocation and China’s province-wide procurement alliances that standardize specifications and scale volumes. Multinationals localize production to win the lowest-bid tenders, while private hospitals in Japan and Australia adopt RFID to market premium safety credentials to medical tourists.

Europe sits in the mid-teens share bracket but faces volume drag from robotic surgery. Robotic anterior resections already represent 30% of U.K. rectal cases, a trajectory that may suppress sponge demand by 40-60% per case within five years. EUDAMED registration in 2026 will likely trim the supplier pool, advantaging firms with deep MDR experience and broad CE-marked portfolios. GCC countries and Brazil round out high-growth pockets as they fund medical-city mega projects and public-system upgrades that require CE- or FDA-listed consumables.

Competitive Landscape

Global revenue is concentrated among Cardinal Health, Medline Industries, Integra LifeSciences, B. Braun, and 3M, leaving the laparotomy sponges market fragmented. Cardinal Health delivered USD 3.25 billion in Q2 FY2026 medical distribution revenue, but tariffs and compliance costs clipped margins, prompting investments in vendor-managed inventory programs that help hospitals cut working capital. B. Braun generated EUR 9.4 billion (USD 10.9 billion) in fiscal 2025 sales and invested over EUR 800 million (USD 936 million) in automated sterile lines, bundling sponges with digital workflow tools to justify premium pricing.

Product differentiation now hinges on technology integration, regulatory credentials, and service depth. Augustine Biomedical’s autoclave-survivable RFID patent shores up performance gaps, while startups like Tally use AI-vision to bypass RFID infrastructure costs and appeal to budget-constrained ASCs. White-space lies in RFID-as-a-service models that convert capital outlay into per-case fees, and in biodegradable composites that answer emerging producer-responsibility statutes, though cost and waste-segregation hurdles keep volumes small for now.

Laparotomy Sponges Industry Leaders

B. Braun Melsungen AG

Cardinal Health

Integra LifeSciences

Medline Industries

Solventum Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: B. Braun posted EUR 9.4 billion (USD 10.9 billion) FY 2025 revenue, up 5.1%, and invested EUR 800 million (USD 936 million) in CO₂-neutral and automated surgical-consumable plants.

- February 2026: Cardinal Health’s Q2 FY2026 medical segment revenue hit USD 3.259 billion, with profit doubling on volume gains and cost controls despite tariff drag.

Global Laparotomy Sponges Market Report Scope

As per the scope of the report, a laparotomy sponge is a large, highly absorbent surgical gauze pad used during abdominal and other major surgeries to soak up blood and bodily fluids. It helps maintain a clear surgical field for better visibility and precision. These sponges are typically made from cotton or cotton-blend materials and are often equipped with radiopaque markers to ensure they can be detected on imaging if unintentionally left inside the body. They are used in sterile conditions and counted carefully before and after procedures to prevent retention errors.

The laparotomy sponge market is segmented by product, material, sterility, end-user, and geography. By product, the market is segmented into radiopaque laparotomy sponges, traditional (conventional) sponges, and RFID-enabled laparotomy sponges. By material, the market is segmented into cotton, rayon/viscose, non-woven & synthetic blends, and antimicrobial/biodegradable composites. By sterility, the market is segmented into sterile and non-sterile. By end-user, the market is segmented into hospitals & clinics, ambulatory surgical centers (ASCs), and specialty clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Radiopaque Laparotomy Sponges |

| Traditional (Conventional) Sponges |

| RFID-enabled Laparotomy Sponges |

| Cotton |

| Rayon / Viscose |

| Non-Woven & Synthetic Blends |

| Antimicrobial / Biodegradable Composites |

| Sterile |

| Non-sterile |

| Hospitals & Clinics |

| Ambulatory Surgical Centers (ASCs) |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of MEA | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Radiopaque Laparotomy Sponges | |

| Traditional (Conventional) Sponges | ||

| RFID-enabled Laparotomy Sponges | ||

| By Material | Cotton | |

| Rayon / Viscose | ||

| Non-Woven & Synthetic Blends | ||

| Antimicrobial / Biodegradable Composites | ||

| By Sterility | Sterile | |

| Non-sterile | ||

| By End-User | Hospitals & Clinics | |

| Ambulatory Surgical Centers (ASCs) | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of MEA | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the global laparotomy sponges market?

It is expected to increase from USD 1.35 billion in 2026 to USD 1.83 billion by 2031.

How fast is global demand expected to grow through 2031?

The market is projected to expand at a 6.32% CAGR between 2026 and 2031.

Which region is poised for the quickest revenue expansion?

Asia-Pacific is forecast to post the fastest growth, advancing at a 12.68% CAGR through 2031.

Why are ambulatory surgical centers influencing product design?

CMS now reimburses higher-acuity procedures in ASCs, so suppliers are engineering pre-sterilized, single-use packs that fit ASC turnover and cost requirements.

Who are the dominant platform manufactures?

B. Braun Melsungen AG, Cardinal Health, Integra LifeSciences, Medline Industries, and Solventum Corporation that accelerate laparotomy sponges market.

Page last updated on: