Laparoscopy Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

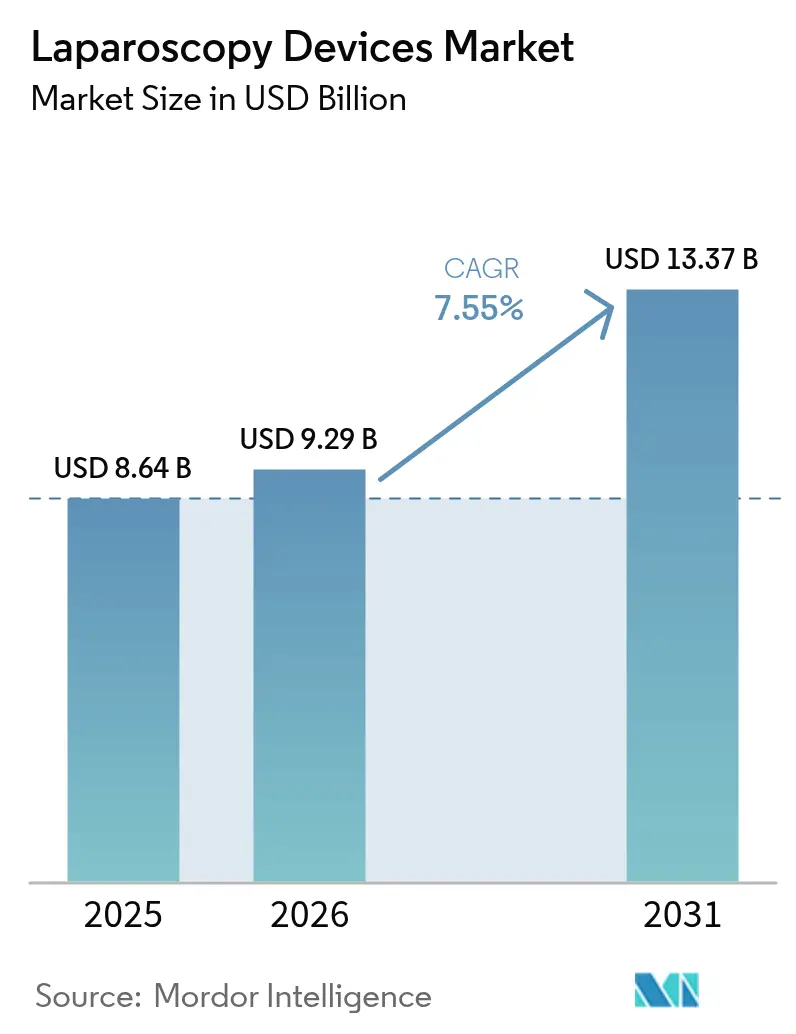

| Market Size (2026) | USD 9.29 Billion |

| Market Size (2031) | USD 13.37 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

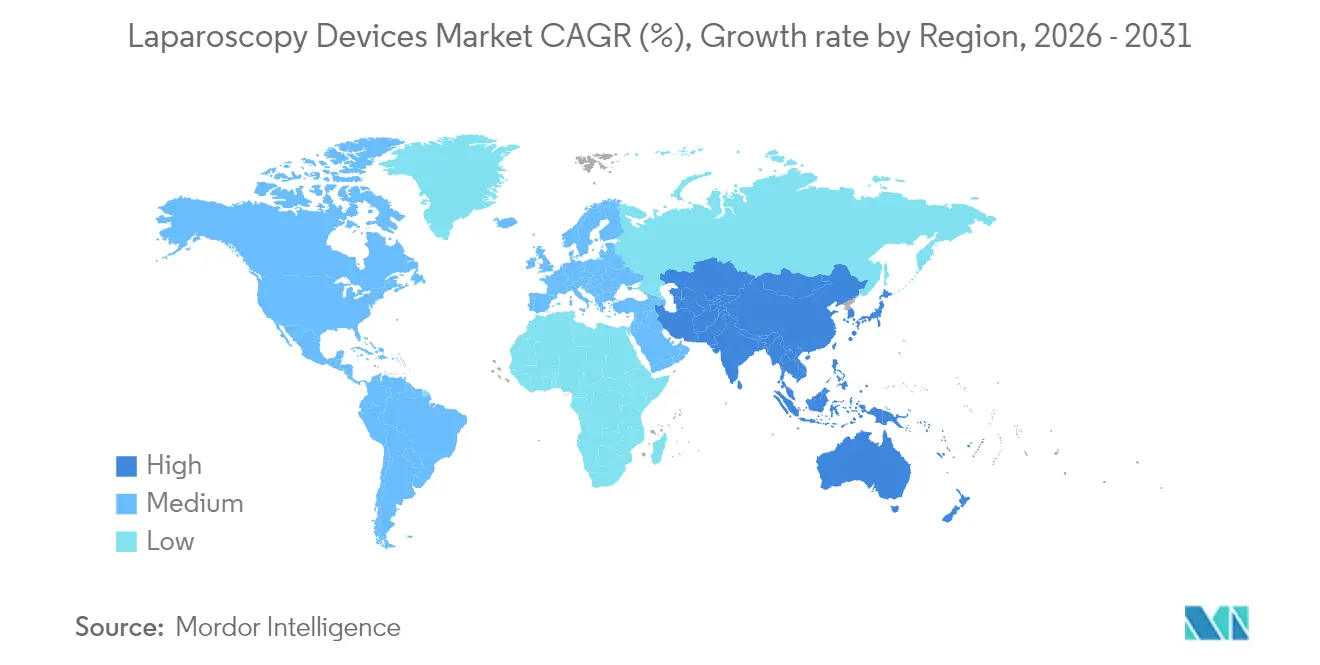

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Laparoscopy Devices Market Analysis by Mordor Intelligence

Laparoscopic devices market size in 2026 is estimated at USD 9.29 billion, growing from 2025 value of USD 8.64 billion with 2031 projections showing USD 13.37 billion, growing at 7.55% CAGR over 2026-2031. Momentum is underpinned by the rising preference for minimally invasive procedures, steady regulatory support for AI-enabled surgical systems, and wider availability of ambulatory surgical centers. Sustained demand also comes from the convergence of 4K and 3D imaging, robotic platforms that improve dexterity, and growth in obesity-related metabolic surgeries. Manufacturers are responding with reusable tool innovations that address sustainability concerns while maintaining sterility standards. Simultaneously, regional supply-chain diversification mitigates logistics risks and tightens delivery timelines for key components.

Key Report Takeaways

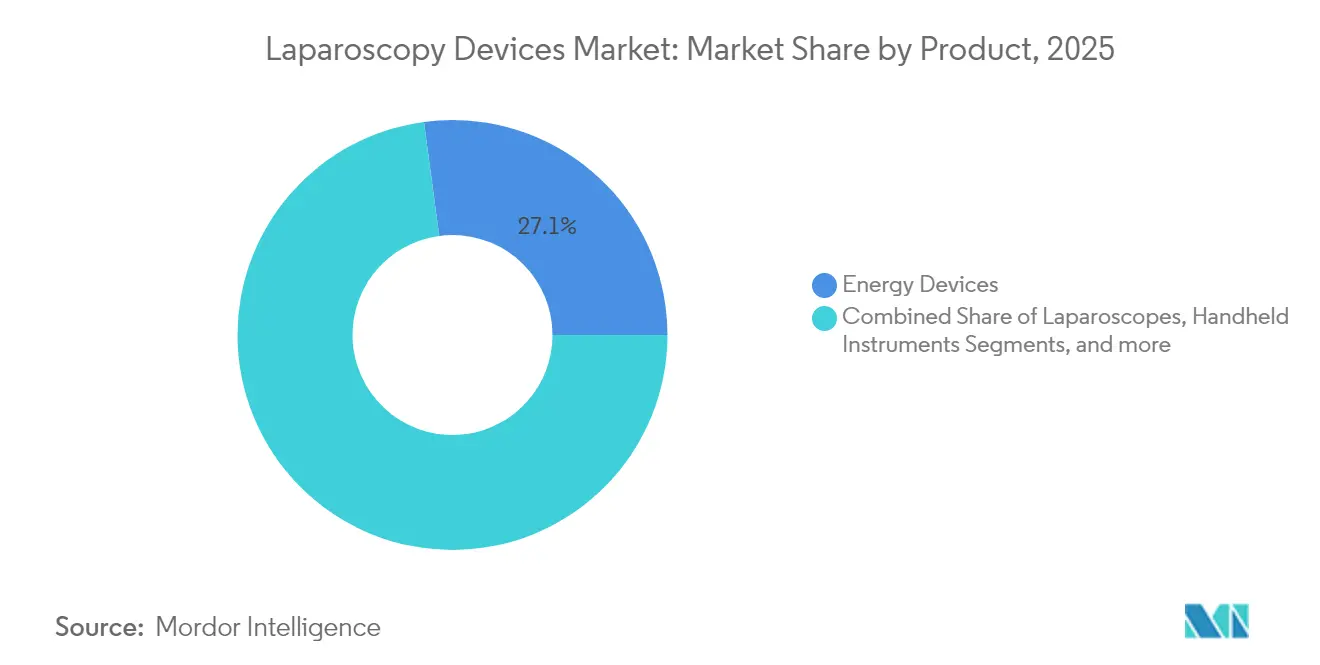

- By product, energy devices led with 27.12% revenue share in 2025, while robotic-assisted platforms are projected to post the fastest 8.27% CAGR through 2031.

- By application, general surgery accounted for 29.52% of the laparoscopic devices market share in 2025; gynecological surgery is positioned to grow at an 8.05% CAGR to 2031.

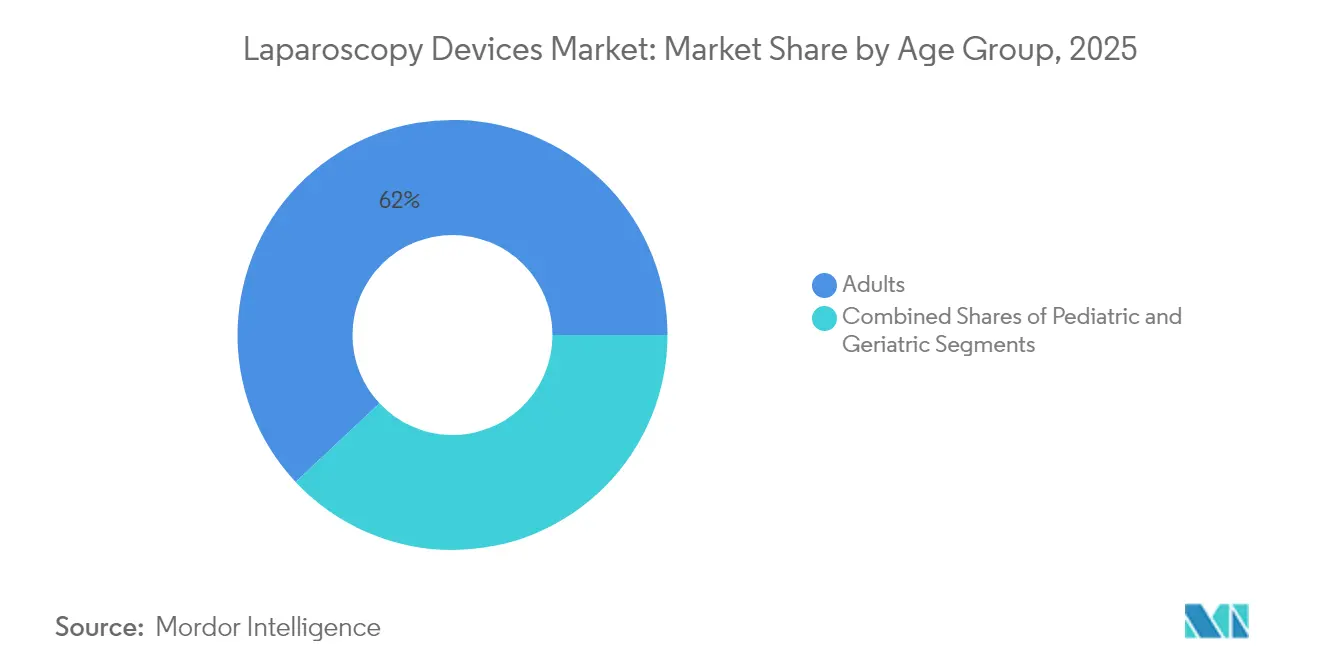

- By age group, adults dominated at 61.98% in 2025, whereas the geriatric cohort is set to expand at an 7.95% CAGR.

- By end user, hospitals held 65.62% of the laparoscopic devices market size in 2025, but ambulatory surgical centers are expected to climb at an 8.11% CAGR.

- By geography, North America captured 40.05% revenue share in 2025; Asia-Pacific is forecast to register the highest 8.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Laparoscopy Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for minimally-invasive procedures | +1.8% | Global; strongest in North America and Europe | Medium term (2-4 years) |

| 4K/3D/AR and AI visualization breakthroughs | +1.5% | North America and European Union lead; APAC catching up | Long term (≥ 4 years) |

| Growing obesity and metabolic disease burden | +1.2% | Global; concentrated in high-income economies | Long term (≥ 4 years) |

| Accelerated ambulatory surgical center build-out | +1.0% | North America and Europe core; APAC expansion | Medium term (2-4 years) |

| Shift toward single-use instruments | +0.8% | Global | Short term (≤ 2 years) |

| AI-enabled intra-operative analytics | +0.7% | North America and Europe early adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Minimally-Invasive Procedures

Elective and acute surgeries increasingly favor laparoscopic techniques because average hospital stays fall by 2–3 days, and postsurgical recovery accelerates. Hospitals benefit from lower readmission rates, while patients report less postoperative pain and faster return to work. Fellowship enrollments in minimally invasive surgery have risen, ensuring a steady pipeline of skilled practitioners. The virtuous cycle of patient preference, payer support, and surgeon competency continues to lift the laparoscopic devices market.

Technological Leaps Including 4K/3D/AR and AI Vision

New imaging stacks quadruple resolution and add depth perception that reduces error rates in intricate dissections. AI-enabled systems such as the da Vinci 5 supply predictive analytics that anticipate instrument trajectory, helping surgeons identify critical structures sooner. Augmented reality overlays align preoperative scans with live anatomy and shorten operative times, improving operating-room turnover.

Growing Prevalence of Obesity & Metabolic Disease

Bariatric volumes keep rising as obesity reaches pandemic levels. Laparoscopic metabolic procedures remain the gold standard for sustained weight loss and diabetes remission, even as GLP-1 agonists gain traction, with combination therapy producing longer-term success. Robotic platforms lower complication rates further, reinforcing uptake at high-volume centers.

Rapid Ambulatory Surgical Centers Build-Out in High-Income Economies

Ambulatory surgical centers (ASCs) deliver procedures at markedly lower cost than hospital outpatient departments and now attract complex laparoscopic workloads. Portable towers and compact insufflators designed for rapid case turnover optimize ASC efficiency. Payment parity policies encourage migration of appropriate procedures to these sites, propelling demand for cost-effective but advanced systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance outlay | -1.2% | Global; acute in emerging markets | Medium term (2-4 years) |

| Shortage of advanced-skill laparoscopic surgeons | -0.8% | Global; severe in developing regions | Long term (≥ 4 years) |

| Sustainability backlash on disposable plastics | -0.6% | Europe and North America | Medium term (2-4 years) |

| Endoluminal therapies cannibalizing procedure share | -0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital & Maintenance Outlay

Fully-featured robotic suites can cost USD 2–3 million with ongoing service fees topping USD 200,000 annually, delaying purchases by mid-tier hospitals. Supply chain turbulence has lifted logistics costs, causing providers to scrutinize total cost of ownership. Pay-per-use financing and shared-ownership models have emerged to counterbalance these barriers.

Shortage of Advanced-Skill Laparoscopic Surgeons

Training requirements remain steep and senior mentorship capacity limited, producing regional care gaps. VR simulators now reduce learning curves and AI-guided modules gauge proficiency in real time [1]Miranda X. Morris, “Current and Future Applications of Artificial Intelligence in Surgery,” Frontiers in Surgery, frontiersin.org. Even so, workforce shortfalls may restrain procedure volumes in lower-income regions until upskilling accelerates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Robotic Systems Drive Innovation

Energy instruments held the largest slice of the laparoscopic devices market at 27.12% in 2025 because almost every procedure requires electrosurgery or tissue sealing. Robotic-assisted systems, while smaller in absolute volume, are forecast to post an 8.27% CAGR through 2031. That expansion will lift the laparoscopic devices market size for robotic suites to USD-denominated double-digit billions by decade-end. Next-generation laparoscopes integrate 4K/3D optics, automated white-balance, and leak-proof trocar seals that maintain stable pneumoperitoneum. Hand instruments adopt haptic feedback motors that lessen surgeon fatigue during lengthy bariatric cases. Disposable trocars continue shifting toward plant-based or recyclable materials to address environmental targets. Manufacturers also bundle service analytics that predict instrument wear, limiting unplanned downtime.

The pivot to single-use instruments spreads quickly across suction-irrigation and stapler lines because hospitals calculate that reprocessing costs can surpass USD 200 per item. Smart energy devices now feature tissue-contact sensors that moderate thermal spread, improving safety in confined spaces. Premium accessory lines thus supply recurring revenue that softens pricing pressure on capital equipment.

By Application: Gynecological Surgery Accelerates

General surgery contributed the largest 29.52% slice of the laparoscopic devices market in 2025, owing to high volumes of cholecystectomy and anti-reflux procedures. Gynecology, however, shows the highest 8.05% CAGR as robotic hysterectomy adoption widens. That trajectory will lift gynecology’s laparoscopic devices market share notably by 2031.

In colorectal and urological surgery, AI-enabled cameras help clinicians consistently achieve critical-view benchmarks, slashing intraoperative injuries. Bariatric volumes rise steadily with obesity growth, while robotic platforms further shorten hospital stays. Thoracic and pediatric segments remain smaller yet gain momentum from tool miniaturization.

By Age Group: Geriatric Segment Surges

Adults commanded 61.98% of the laparoscopic devices market share in 2025, yet the geriatric cohort is advancing at an 7.95% CAGR that will noticeably lift the laparoscopic devices market size by 2031. Hospitals increasingly clear older patients for minimally invasive procedures as enhanced recovery programs and refined anesthesia protocols lower postoperative risk. Shorter inpatient stays and faster return to baseline function have made laparoscopy the preferred approach for oncologic, hernia, and gallbladder interventions in seniors.

Surgeons report fewer wound complications and lower pulmonary morbidity among geriatric patients when operations are performed laparoscopically rather than through open incisions, reinforcing physician confidence . Device makers are responding with age-specific instrumentation that features slimmer shafts, gentler tip profiles, and ergonomic handles to reduce operating-room fatigue during lengthier oncologic cases. At the same time, AI-driven visualization platforms help surgeons navigate fragile anatomy, improving precision and decreasing conversion rates to open surgery. The combination of demographic momentum and demonstrable clinical benefits positions the geriatric segment as a key long-term growth engine within the broader laparoscopic devices market.

By End User: ASCs Challenge Hospital Dominance

Hospitals retained 65.62% of global revenue in 2025 by handling high-acuity and multi-procedure cases, but ambulatory surgical centers (ASCs) are forecast to expand at an 8.11% CAGR and steadily erode that lead. Payer initiatives that equalize reimbursement across care settings, together with patient demand for same-day discharge, are steering gallbladder, hernia, and bariatric procedures toward outpatient venues. This migration will enlarge the laparoscopic devices market size captured by ASCs through 2031.

ASC operators are investing in compact towers, mobile insufflators, and single-port wristed instruments optimized for rapid case turnover and limited footprint environments. Disposable trocar and clip-applier kits bundled with service contracts simplify inventory management while safeguarding sterility, a critical requirement for high-volume outpatient workflows. Manufacturers that pair equipment leasing with on-site staff training capture loyalty and minimize capital barriers for new centers. As more spine and urology cases transition to outpatient settings, the ASC channel will grow in strategic importance, prompting device suppliers to tailor product roadmaps specifically for this fast-scaling customer segment.

Geography Analysis

North America controlled 40.05% of global revenue in 2025, anchored by dense installed bases and favorable reimbursement. United States facilities logged double-digit growth in robotic general surgery cases after the da Vinci 5 launch. Canadian hospitals replicate performance through provincial funding schemes, while Mexico increases private-sector adoption to serve cross-border medical tourists.

Asia-Pacific is forecast to post the fastest 8.22% CAGR. Chinese hospitals continue large-scale build-outs and accelerate local production of cost-optimized robotic platforms following recent domestic approvals. Japan and South Korea leverage their imaging expertise to export high-resolution camera stacks. India’s tier-one cities witness robust demand, though rural uptake remains slower due to capital limitations. Medical-tourism corridors in Thailand and Malaysia further boost case volumes. European growth is stable, supported by national health insurance and surgeon training networks. Budget caps, however, can delay broad robotic acquisition outside Northern Europe. Intra-region initiatives promote reusable instrument procurement to align with decarbonization goals. The Middle East and Africa observe rising adoption in Gulf Cooperation Council states investing in flagship medical cities, whereas sub-Saharan Africa relies heavily on donor-funded MIS programs . South America sees moderate gains centered on Brazil’s private insurers and Argentina’s public-sector modernization.

Regulatory Landscape

In the United States, laparoscopic and adjacent endoscopic instruments typically move through FDA pathways such as 510(k) for Class II devices, with quality compliance anchored in 21 CFR requirements. A notable 2025 action was the FDA classification of laparoscopic gastrointestinal sizing tools into Class II with special controls (August 2025), clarifying controls for certain procedure-specific accessories and shaping documentation for clinical performance and labeling.

Global manufacturers also work within quality-system harmonization and region-specific technical expectations. The FDA Quality Management System Regulation (QMSR) became effective in February 2026, incorporating ISO 13485:2016 by reference, which supports QMS alignment for multinational laparoscopic portfolios sold in the US. In Europe, access remains governed by the EU Medical Device Regulation (MDR), with the European Commission monitoring via Notified Body surveys (May 2026 data-collection cycle). In China, NMPA activity increased for endoscopic and laparoscopic categories, including publication of final device guidelines in December 2025, a 2026 guideline-revision plan affecting both Class II and Class III device categories (April 2026), draft registration guidance for endoscopic imaging with tighter performance benchmarks (June 2026), and medical device GMP updates taking effect in November 2026, adding compliance workload for imaging stacks, access devices, and related manufacturing documentation.

Value Chain Analysis

The laparoscopy devices value chain starts with upstream inputs such as 316L/304 stainless steels, titanium alloys, optics, and medical-grade polymers used across trocars, handheld instruments, camera components, and insufflation consumables. These materials then flow into OEM design and manufacturing (precision machining, molding, coating, assembly, sterilization validation, and packaging), followed by quality and regulatory documentation aligned with frameworks such as ISO 13485 and biocompatibility expectations (commonly ISO 10993 and related test matrices), which shape supplier qualification, process controls, and change management.

Downstream, distribution typically runs through direct sales forces and channel partners to hospitals and ambulatory surgical centers, where operating-room stakeholders, value-analysis committees, and procurement groups influence product adoption and standardization. Purchasing decisions are heavily influenced by surgeon preference and procedure workflows, while contracting through hospital networks and Group Purchasing Organizations can shorten adoption cycles. Operational bottlenecks remain concentrated in electronics and specialized components for imaging and connected-OR stacks, alongside tariff-related cost volatility that has pushed suppliers toward diversification and more localized sourcing for critical subassemblies.

Competitive Landscape

Industry concentration remains fragmented. Intuitive Surgical, Medtronic, Johnson & Johnson MedTech, and Stryker collectively hold a sizeable installed base, but nimble entrants launching single-port robots and wristed handhelds erode incumbent share.

AI software updates delivered under new FDA-predetermined change control pathways allow premium vendors to extend asset life cycles without hardware swaps. Vertical integration trends pair imaging platforms with analytics dashboards, increasing switching costs for hospitals.

Supply-chain resilience strategies push manufacturers to dual-source semiconductors and establish regional assembly hubs. Sustainability adds another dimension of competition; firms that commercialize low-plastic or reusable portfolios may qualify for environment-linked tenders. Global OEMs also sponsor surgeon-training academies that certify proficiency on specific platforms, further embedding their ecosystems.

Laparoscopy Devices Industry Leaders

Karl Storz GmbH & Co.KG

Olympus Corporation

Boston Scientific Corporation

Johnson & Johnson (Ethicon)

Medtronic plc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Robotic-assisted laparoscopy and connected-OR ecosystems create whitespace where hospitals and ASCs look for workflow gains without wholesale infrastructure replacement. Platform vendors are expanding capability through software and ecosystem integration rather than only hardware refreshes, supported by regulatory pathways that accommodate controlled software updates and by quality-system convergence such as the FDA QMSR effective in February 2026 (ISO 13485:2016 alignment). Within robotic systems, multi-specialty utilization is an actionable opportunity: CMR Surgical reported more than 45,000 patients treated globally with Versius and initiated US expansion in March 2026 following FDA clearance in December 2025, indicating commercial traction for systems that can support general surgery and gynecology case mixes.

Europe also offers a tangible entry point for new robotic and laparoscopic platforms that meet MDR requirements. Cornerstone Robotics announced EU CE mark certification under MDR for the Sentire Surgical System (May 2026), expanding the pool of MDR-cleared robotic options for hospitals balancing clinical demand with procurement scrutiny. At the same time, opportunities extend to imaging and visualization stacks that meet tighter performance expectations, and to reusable or lower-plastic instrument portfolios that align with hospital sustainability procurement while maintaining sterility and reprocessing requirements. These shifts favor suppliers that can pair advanced visualization, standardized consumable kits, and training support to accelerate adoption in fast-throughput settings such as ASCs.

Recent Industry Developments

- May 2026: Cornerstone Robotics announced EU CE mark certification under MDR for the Sentire Surgical System, expanding the portfolio of MDR-cleared robotic laparoscopic platforms. The approval broadens adoption potential in European hospitals by easing procurement and clinical alignment with MDR requirements.

- May 2025: MicroPort received NMPA approval for the Toumai SP laparoscopic robot across urology, general surgery, and gynecology. This approval broadens the addressable installed base for single-port robotic laparoscopy in China and increases pressure on incumbents to localize portfolios and service models.

- October 2024: LivsMed launched ArtiSential 5, a 5 mm wristed articulating laparoscopic instrument series. The product supports more complex minimally invasive maneuvers through smaller access ports, strengthening the premium segment for advanced handheld instruments in hospitals and high-throughput centers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenues earned from devices used to perform laparoscopic (minimally invasive) abdominal and pelvic procedures, including systems and tools for access, visualization, insufflation, dissection, closure, and the related consumables sold to care providers.

Scope exclusions: Refurbished equipment resale, standalone service contracts, and standalone robotic platforms are excluded from the market value.

Segmentation Overview

- By Product

- Energy Devices

- Electrosurgical / Bipolar Generators

- Ultrasonic & RF Energy Systems

- Laparoscopes

- Video Laparoscopes (HD/4K/3D)

- Fibre-optic Laparoscopes

- Insufflation & Access Devices

- CO2 Insufflators

- Trocars & Cannulas

- Handheld Instruments

- Graspers & Dissectors

- Scissors & Shears

- Suction / Irrigation Devices

- Robotic-Assisted Laparoscopy Systems

- Accessories & Consumables

- Energy Devices

- By Application

- General Surgery

- Bariatric Surgery

- Gynecological Surgery

- Urological Surgery

- Colorectal Surgery

- Other Applications

- By Age Group

- Adults

- Pediatric

- Geriatric

- By End User

- Hospitals

- Ambulatory Surgical Centers (ASCs)

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to map the device workflow in laparoscopy and then build a clean list of what should be counted as revenue and what should not. We start with public healthcare statistics and procedure context from sources such as the World Health Organization, the US FDA device databases and safety communications, the US Centers for Medicare and Medicaid Services reimbursement references, and OECD health statistics.

After that, the model inputs are supported using broader public sources such as UN Comtrade for trade direction checks, peer reviewed clinical journals that describe minimally invasive surgery adoption, and company annual reports and investor decks to understand how firms report exposure to laparoscopy related categories. Where needed, we also used paid subscriptions for company financials and intelligence, patent databases, and shipment level import or export data to sanity check category presence and timing. The desk sources listed here are illustrative only, and we used other public references as well for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is actually purchased and replaced in the OR, and how pricing changes with mix shifts between reusable and disposable items. We spoke with manufacturers, distributors, hospital procurement staff, and practicing clinicians across major regions, so assumptions around utilization, replacement cycles, and price bands could be corrected before finalizing the totals.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 16% | APAC: 47% |

| Mid tier: 49% | Functional/Unit leaders: 33% | EMEA: 30% |

| Smaller Players: 17% | Managers: 51% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts from a top-down view where procedure volumes and care setting mix are used to reconstruct the demand pool for laparoscopy toolkits, and then it is translated into revenue using typical per procedure consumption and average selling price ranges. To keep the totals practical, the results are corroborated with selective bottom-up approximations, including sampled price band checks for trocars, hand instruments, and energy devices. Supplier and channel feedback is then used to adjust for undercounting.

Key inputs that move the model include adoption of minimally invasive surgery by specialty, the disposable versus reusable mix for access and closure items, replacement cycles for visualization and insufflation systems, typical instrument sets per OR, and observed pricing progression by geography and tendering patterns. Forecasting is run using scenario analysis supported by a light multivariate regression, where drivers such as procedure growth, outpatient migration, and hospital capital spending trends are tested together. The scenarios are then aligned to what primary respondents expect over the next few years. When country level data is thin, we handle gaps with proxy indicators such as comparable health spend per capita and surgical volume intensity, and then recheck these assumptions in interviews.

Data Validation & Update Cycle

Validation is done through stepwise triangulation, where the final number must make sense against multiple independent signals such as procedure growth, hospital purchasing cycles, and trade direction checks for device categories. Outliers are flagged early, and the assumptions behind them are reviewed again, followed by a second analyst check before sign-off.

The study is refreshed annually, and interim revisions are triggered when material events can change pricing or adoption patterns. Before delivery, we run a fresh pass on key inputs such as currency conversion timing, price band movement, and procedure growth assumptions so the latest view is reflected in the model outputs.

Mordor Intelligence's Laparoscopy Devices Market Size Compared With Other Published Estimates

Published market sizes for laparoscopy devices do not always align, even when the titles look similar, because the counted products and the timing of pricing and currency conversion can shift the totals. Differences also come from whether a study relies more on device shipment proxies or on procedure driven consumption logic.

The gap is often explained by how pricing is refreshed across reusable capital equipment versus disposable items, and whether validation checks are run back to procedure growth and replacement cycles before final totals are locked. When average selling price progression is updated at a different point in the year and currency timing is handled differently, the size can move even without a real demand change. In this context, the refresh cadence and consistency checks used in Mordor Intelligence help keep the scope traceable for this market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 9.29 B (2026) | |

| Industry Publisher A | USD 9.00 B (2025) | Uses an earlier base year and may include a wider device basket that blends adjacent robot assisted systems, with limited clarity on excluding refurbished resale and service revenues, which can lift the total. |

| Global Publisher B | USD 9.25 B (2025) | Reported in a different base year and may apply a flatter price inflation path across device types, which can overstate growth for capital equipment compared with replacement cycle checks by category. |

Across the three figures, the spread is mainly explained by base year choice and what is counted around capital systems versus accessories, followed by timing of currency and price updates. By keeping scope boundaries explicit and then pressure testing revenue against procedure linked demand signals, the final value stays traceable to inputs that can be revisited and repeated.

Key Questions Answered in the Report

What is the current value of the laparoscopic devices market?

The market is worth USD 9.29 billion in 2026 and is projected to reach USD 13.37 billion by 2031.

Which product segment holds the largest share?

Energy devices lead with 27.12% revenue share in 2025.

Which application area is expanding the fastest?

Gynecological surgery is forecast to grow at an 8.05% CAGR through 2031.

Why are ambulatory surgical centers important to future growth?

ASCs deliver procedures at lower cost, attract patient preference, and will expand at an 8.11% CAGR, challenging hospital dominance.

Which region offers the highest growth opportunity?

Asia-Pacific is expected to record an 8.22% CAGR owing to infrastructure investment and rising disposable incomes.

How is sustainability influencing device design?

Hospitals increasingly favor reusable or recyclable instruments, prompting manufacturers to launch low-plastic alternatives that meet infection-control requirements.

Page last updated on: