Healthcare Membranes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

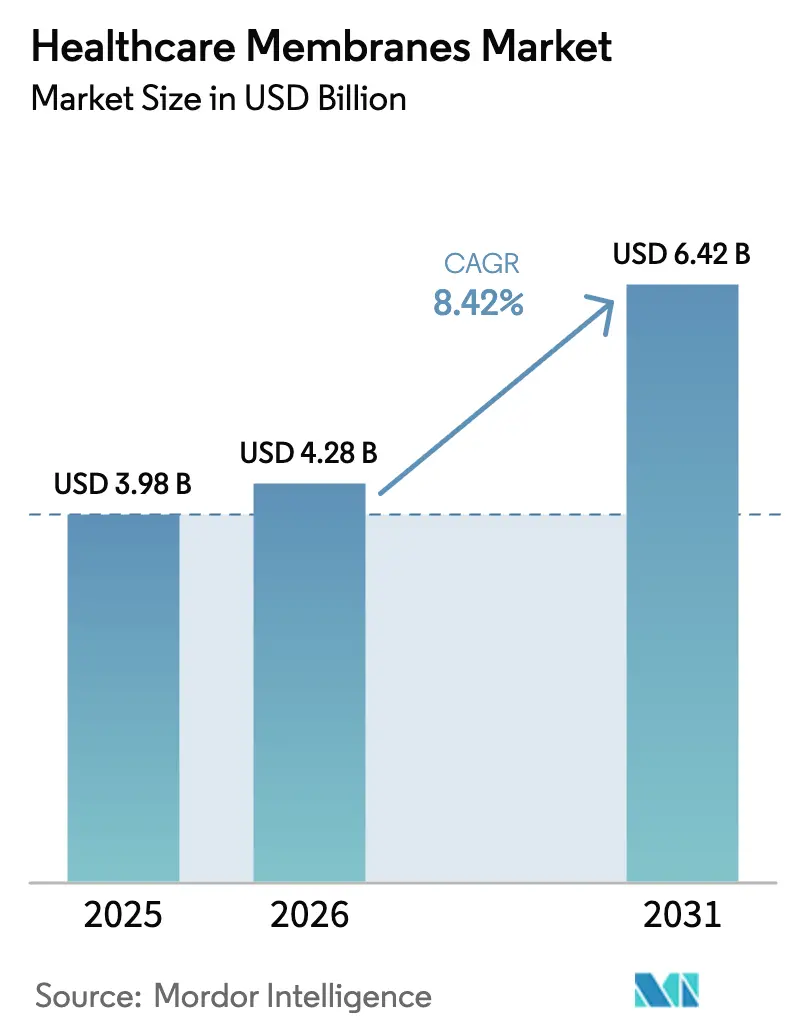

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 6.42 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

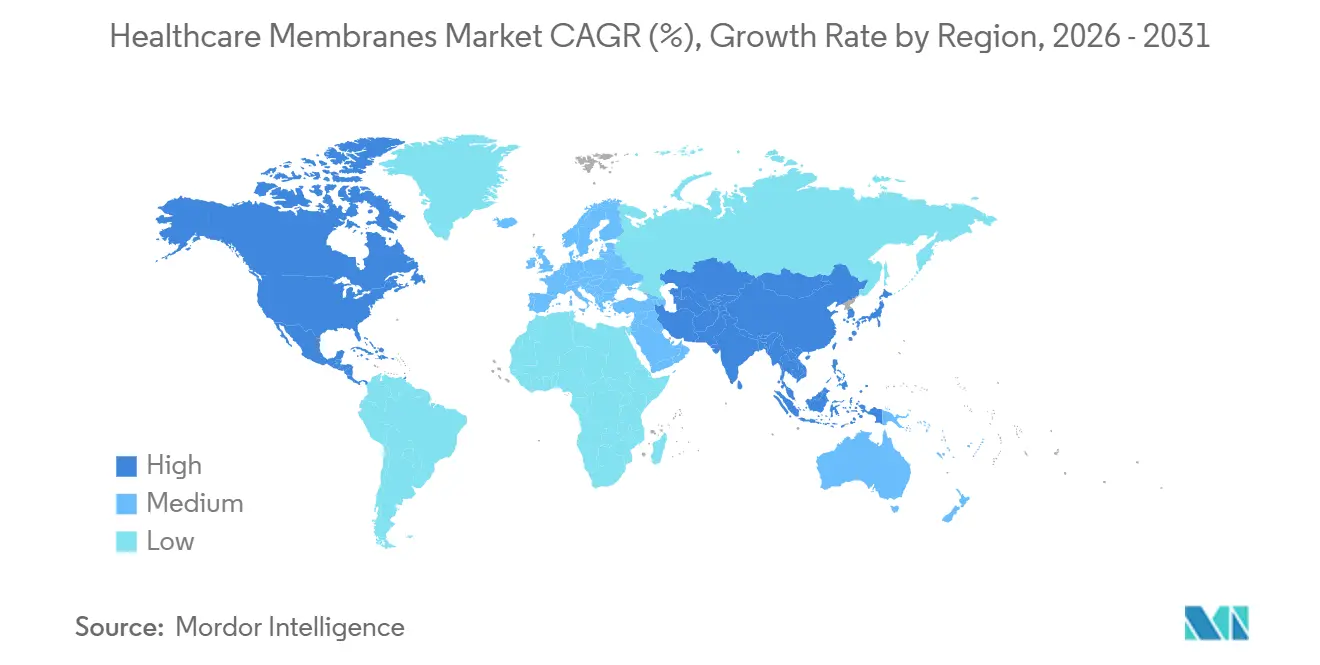

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Healthcare Membranes Market Analysis by Mordor Intelligence

The healthcare membranes market size is expected to increase from USD 3.98 billion in 2025 to USD 4.28 billion in 2026 and reach USD 6.42 billion by 2031, growing at a CAGR of 8.42% over 2026-2031. Demand pivots from cost-per-square-meter competition toward value-per-batch economics as biopharmaceutical producers pay premiums for membranes that shorten viral clearance studies, sustain flux above 150 L m² h⁻¹, and meet sterility assurance levels exceeding 7-log parvovirus reduction. Regulatory tightening by the FDA, EMA, and PMDA rewards suppliers that pre-validate endotoxin retention, extractables, and integrity testing, effectively creating a 24-month entry barrier for new entrants. Material innovation shapes differentiation; polyethersulfone (PESU) gains traction because it tolerates ≥25 kGy gamma-irradiation and ≥50 sodium-hydroxide cleaning cycles without flux decay, a profile prized in single-use systems. Technology shifts track the biosimilar and cell-therapy pipelines, with nanofiltration replacing dual-stage chromatography to shave 14-21 days from manufacturing calendars. Geographic growth centers migrate to Asia-Pacific contract development and manufacturing organizations (CDMOs) that leverage regulatory arbitrage between EMA and PMDA pathways while installing integrated membrane assemblies for real-time bioburden control.

Key Report Takeaways

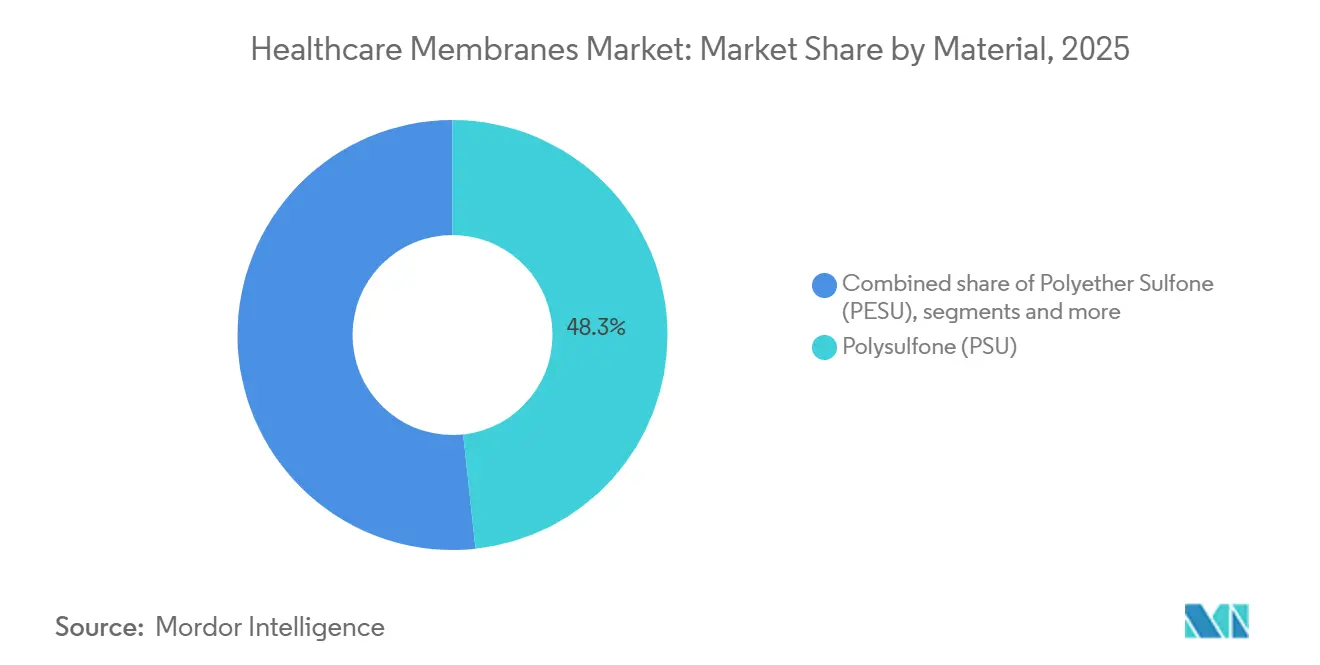

- By material, polysulfone led with 48.26% of the healthcare membranes market share in 2025; polyethersulfone is forecast to expand at a 9.81% CAGR through 2031.

- By technology, ultrafiltration commanded 39.69% share of the healthcare membranes market size in 2025, while nanofiltration is advancing at a 10.17% CAGR over 2026-2031.

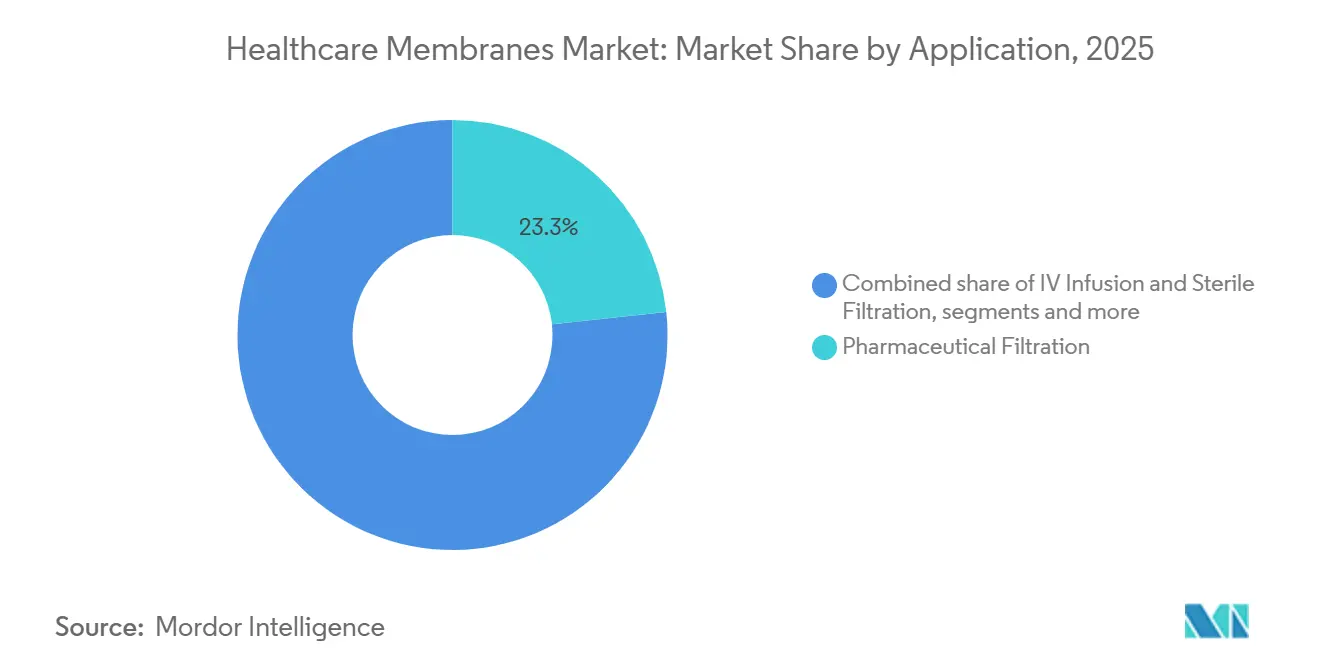

- By application, pharmaceutical filtration accounted for a 23.31% share of the healthcare membranes market size in 2025, and Sterilization is growing at a 10.20% CAGR to 2031.

- By geography, North America held 41.68% of the healthcare membranes market share in 2025; Asia-Pacific is projected to record the highest CAGR at 9.83% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Healthcare Membranes Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Sterile Filtration & Drug Purification | +2.1% | Global, concentrated in North America & Europe | Medium term (2–4 years) |

| Technological Advancements in Membrane Materials | +1.8% | Global, led by Asia-Pacific hubs | Long term (≥ 4 years) |

| Growth in Biopharmaceutical & Injectable Therapies | +2.4% | North America, Europe, Asia-Pacific | Medium term (2–4 years) |

| Increasing Prevalence of Chronic Diseases | +1.3% | Global, acute in Japan, Germany, United States | Long term (≥ 4 years) |

| Stringent Regulatory Standards for Purity & Safety | +1.6% | North America & EU, spillover to APAC | Short term (≤ 2 years) |

| Integration of AI in Membrane Design & Monitoring | +0.9% | North America, Europe, select APAC sites | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Sterile Filtration & Drug Purification

Biopharmaceutical manufacturers steadily replace batch sterilization with continuous inline membrane steps to achieve real-time microbial control and eliminate terminal heat treatment. FDA guidance issued in 2024 formally recognizes inline sterile filtration as a critical control point, enabling sponsors to trim 90-120 days from time-to-market once membrane validation dossiers are accepted. Biosimilar development accelerates this pull; 47 new biosimilar files entered FDA review during 2025, each consuming 15-20 m² of nanofiltration area for virus removal. Technological advancements in membrane systems are playing a pivotal role in addressing the evolving needs of the pharmaceutical industry. In December 2023, Asahi Kasei introduced an innovative membrane system designed to dehydrate organic solvents for pharmaceutical applications, eliminating the need for heat or pressure [1]Asahi Kasei Corporation, “Asahi Kasei Develops Innovative Healthcare Membranes 2023,” asahi-kasei.com. Emerging applications in plasmid DNA purification for mRNA vaccines further amplify demand. Emerging modalities such as plasmid DNA for mRNA vaccines add incremental demand because they depend on high-capacity ultrafiltration cassettes that tolerate organic solvents without extractables. The cumulative effect lifts volume growth even in mature geographies where traditional small-molecule sterile production is flat.

Technological Advancements in Membrane Materials

Polyethersulfone membranes demonstrated resistance to 1 M sodium hydroxide, sustaining flux across 50-75 reuse cycles in monoclonal-antibody purification at Lonza’s Singapore site, compared with 20-30 cycles for legacy polysulfone . Asymmetric polytetrafluoroethylene membranes introduced in 2025 achieved single-stage clarification of harvests containing 18 million cells mL⁻¹, eliminating depth filters that formerly consumed 22% of downstream time. Artificial-intelligence models trained on 340,000 performance datapoints now predict fouling onset with 87% accuracy, allowing predictive maintenance schedules that cut unscheduled downtime by 41% across global networks. By imparting antimicrobial and anti-fouling properties, these advancements improved the safety and efficacy of medical devices. A May 2025 article in Frontiers in Drug Delivery illustrated this with examples of functionalized membranes that reduced infection risks in implantable devices and enhanced patient safety in long-term dialysis [2]Frontiers in Drug Delivery, “Advancements in AI‑Driven Drug Delivery Systems 2025,” frontiersin.org. These innovations fostered trust in advanced medical technologies, thereby accelerating the market adoption of these technologies. These material and digital innovations keep the healthcare membranes market on an innovation curve that offsets commoditization pressure in lower-value segments.

Growth in Biopharmaceutical & Injectable Therapies

High-concentration biologics exceeding 150 mg mL⁻¹ require ultrafiltration membranes with 30-100 kDa cut-offs to reach target potency while stripping aggregates and endotoxin. Commercial cell-and-gene-therapy capacity came online in 2025, installing large-surface-area PESU tangential-flow modules for viral-vector clarification and concentration. Membrane economics favor ultra-rare therapies with <15,000 patients annually, because chromatography capital costs outstrip membrane costs by 2.3× at small scale. Consequently, 73% of active rare-disease programs in clinical development now specify membrane-based purification sequences. Parallel growth in autoinjectors and prefilled syringes multiplies demand for inline sterilizing filters that protect sensitive high-value protein formulations during filling . All told, biologic and injectable therapies act as high-margin anchors that lift the healthcare membranes market beyond commodity pricing.

Increasing Prevalence of Chronic Diseases

Global diabetes prevalence reached 589 million adults in 2024; 2.3 million insulin-pump users replace sterile membrane infusion sets every three days. Parallel spikes in oncology drive demand for implantable chemotherapy ports fitted with 0.2-micron filters that prevent bloodstream infections during at-home infusion. India recorded 1.53 million cancer cases in 2024, spurring local device makers to retool with ISO 10993-compliant membrane components that satisfy upcoming CDSCO regulations [3]CDSCO, “India Recorded Over 15 Lakh Cancer Cases in 2024: Minister 2025,” cdsco.gov.in. As populations age, single-patient-use devices become the norm to mitigate cross-contamination, embedding membranes in dialysis sets, wound-care dressings, and portable oxygen concentrators. These chronic-care applications continually renew baseline volume, stabilizing revenue for suppliers even during bioprocessing investment cycles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Membrane Technologies | −1.4% | South Asia, Latin America, Sub-Saharan Africa | Medium term (2–4 years) |

| Complex Manufacturing & Regulatory Compliance | −0.9% | Global | Short term (≤ 2 years) |

| Limited Accessibility in Emerging Markets | −0.7% | South Asia, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Surface Fouling & Maintenance Challenges | −1.1% | Global, high-throughput sites | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Membrane Technologies

Turnkey nanofiltration skids cost USD 1.2-2.8 million, pricing out contract manufacturers that service biosimilar sponsors with sub-USD 50 million development budgets. Single-use membrane cartridges list at USD 2,400-4,100 for 2.5 m², a hurdle for therapies produced below 200 kg y⁻¹. Validation packages for novel materials reach USD 340,000, covering extractables, bacterial retention, and three-batch PPQ runs. Total cost of ownership ranges USD 47-83 g⁻¹ of purified protein, versus USD 28-51 g⁻¹ for chromatography in high-volume plants, restricting membranes to niches where selectivity or speed outweighs capital economics. Consequently, emerging-market firms prolong legacy stainless installations, tempering penetration even as global demand accelerates.

Complex Manufacturing & Regulatory Compliance

Membrane casting requires ISO-7 cleanrooms; establishing a greenfield line costs ≥USD 28 million excluding validation. FDA, EMA, and PMDA dossier compilation stretches 18-24 months and can exceed 3,800 pages, consuming USD 1.2-1.9 million in analytical fees. Post-approval change control demands prospective validation across three consecutive lots, discouraging iterative optimization. Annual raw-material supplier audits drain resources and limit sourcing agility during shortages. These hurdles consolidate supply among a half-dozen global vendors, slowing local production rollouts and moderating competitive entry in the healthcare membranes market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Reusability Economics Drive PESU Adoption

Polysulfone maintained 48.26% of healthcare membranes market share in 2025 because its four-decade validation history reassures quality teams and regulators. Polyethersulfone posted the fastest 9.81% CAGR as single-use systems proliferated; PESU withstands ≥25 kGy gamma-irradiation without embrittlement, a critical attribute for disposable modules. The healthcare membranes market size for PESU-based products is projected to reach USD 2.68 billion by 2031, reflecting widespread migration within perfusion harvest and virus-removal sequences. Polytetrafluoroethylene addresses aggressive-solvent and vent-filtration niches, capturing value disproportionate to volume. Polypropylene lingers in plasma separation, but limited chemical compatibility curbs expansion. Acrylic-based and polyvinylidene-fluoride innovations pursue cell-therapy opportunities, yet protracted validation keeps penetration below 3% through mid-decade.

Installed-base inertia still favors polysulfone in dialysis, sterile water generation, and legacy stainless systems, yet total cost-of-ownership analyses increasingly tip toward PESU when ≥50 cleaning cycles or gamma sterilization are required. Regulatory shifts toward single-patient-use devices accelerate that transition. Suppliers respond by bundling PESU membranes with integrity-test hardware and digital validation templates, locking in customers for seven-year qualification cycles. As a result, material choice increasingly aligns with lifecycle economics rather than upfront membrane-area pricing, reshaping vendor competitive positions within the healthcare membranes market.

By Technology: Nanofiltration Captures Virus-Removal Premium

Ultrafiltration dominated the healthcare membranes market size at USD 1.58 billion in 2025, reflecting its ubiquity in concentration, diafiltration, and buffer exchange. However, nanofiltration revenue is projected to grow 10.17% CAGR. Single-pass removal of 18-100 nm viruses eliminates low-pH inactivation and dual-column chromatography, slicing 14-21 days from batch release and saving 2,400-3,800 L of buffer. Microfiltration, anchored in 0.2-µm sterilizing-grade filters, remains essential but grows at a slower clip as reuse cycles plateau. Reverse-osmosis retains a niche in water-for-injection generation; energy-efficient membrane distillation threatens partial substitution but wider rollout awaits broader pharmacopeial acceptance.

Gas-separation applications in oxygen concentrators expand modestly because Medicare reimbursement caps stifle innovation. Nonetheless, emerging needs in extracellular-vesicle and exosome therapy push ultrafiltration cut-off precision to new limits, commanding premium pricing. Suppliers that integrate real-time fouling sensors and AI-controlled pressure modulation into skids capture outsized share of greenfield CDMO projects. Overall, technology migration to nanofiltration underpins margin expansion in the healthcare membranes market even as square-meter pricing commoditizes for ultrafiltration.

By Application: IV Infusion Growth Tracks Home-Care Boom

Pharmaceutical filtration accounted for USD 0.93 billion in 2025, equaling 23.31% of the healthcare membranes market size. Yet, sterilization is advancing fastest at 10.20% CAGR by 2031. Post-pandemic shifts toward home infusion therapy in the United States, Germany, and Japan mean every multi-day antibiotic or immunoglobulin cycle now uses inline 0.2-µm filters rated for 72-hour sterility. Prefilled syringe and autoinjector formats multiply microfiltration unit volumes because each device embeds a hydrophilic PTFE vent to equalize pressure while retaining bacteria.

Protein purification remains a backbone application, especially as sub-10,000-L biologics plants adopt single-use tangential-flow skids for monoclonal-antibody and enzyme production. Cell separation rides the gene-therapy wave; leukocyte depletion filters processed 89% of transfused blood components in developed economies during 2025. Controlled-release drug-delivery systems, including implantables and transdermals, add specialty demand for acrylic and silicone-based membranes with picoliter-per-hour permeability control. As healthcare decentralizes, application diversity insulates the healthcare membranes market from cyclical capital-spending dips.

Geography Analysis

North America held 41.68% of healthcare membranes market share in 2025, supported by a dense cluster of biologic license holders and FDA’s push toward continuous manufacturing. The region’s membrane demand skews to premium PESU and modified acrylic chemistries bundled with digital integrity-test platforms. Europe follows, with Germany, Ireland, and Switzerland attracting investment owing to tax incentives and a skilled workforce. EMA’s alignment with ICH Q13 on continuous manufacturing sustains ultrafiltration and nanofiltration upgrades across brownfield plants.

Asia-Pacific is the fastest-growing geography at a 9.83% CAGR through 2031. South Korea’s Songdo bio-cluster, Singapore’s Tuas Biomedical Park, and multiple Chinese CDMO campuses collectively added 890,000 L of bioreactor capacity in 2025, each liter requiring 0.8-1.2 m² of membrane area. Regional governments subsidize single-use technology adoption to lure multinational sponsors seeking regulatory arbitrage between EMA and PMDA. Japan’s emphasis on sustainability underlines demand for Asahi Kasei’s EcoVadis-gold Microza hollow fibers, prized for low energy consumption.

Latin America and the Middle East & Africa remain smaller but strategically important. Brazil and Argentina anchor South American demand, but currency instability slows capital upgrades, favoring modular single-use skids that defer large outlays. In Sub-Saharan Africa, dialysis commands up to 84% of membrane usage, with sterile filtration adoption constrained by limited ISO-class cleanrooms. Donor-funded vaccine fill-finish projects in Kenya and Senegal may catalyze future demand. Overall, divergent regional dynamics ensure that the healthcare membranes market retains multiple growth vectors rather than relying solely on North American biologics.

Competitive Landscape

The healthcare membranes market is significantly concentrated, with the top five suppliers accounting for a majority of the revenue in 2025. However, the diversity of applications and regional preferences continues to support a competitive mid-tier segment. Incumbents leverage installed bases: validated housings, bubble-point testers, and IQ/OQ/PQ protocols erect switching costs that can exceed USD 0.9 million per production train. Vertical integration surged in 2025 as Thermo Fisher and Danaher bundled proprietary hollow-fiber cartridges with perfusion bioreactors, capturing greenfield single-use installations and pressuring standalone membrane vendors to innovate at the surface-chemistry level.

White-space lies in cell and gene-therapy purification, where only 11% of processes currently deploy membranes for viral-vector concentration. Specialized entrants focus on extracellular vesicle, plasmid DNA, and mRNA purification, offering rapid customization and tight tolerances unattainable in broad portfolios. Asian manufacturers chase cost-optimized polysulfone products to supply biosimilar CDMOs, while Western innovators command premium pricing for low-fouling PESU and hydrophilic PTFE.

Strategic moves in 2025 included Merck KGaA’s EUR 150 million filtration plant in Cork, which shortens EU supply chains, and Sartorius’s AI software rollout across 47 customer sites, which locked in membrane-skid-plus-digital subscriptions. Suppliers hedge with service and analytics bundles that convert one-time cartridge sales into multi-year platform annuities. The balance of these forces yields a stable but innovation-hungry competitive field in the healthcare membranes market.

Healthcare Membranes Industry Leaders

Thermo Fisher Scientific Inc.

Sartorius AG

Danaher Corporation

NIPRO

Asahi Kasei Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Kovalus invested over USD 20 million in a new spiral-wound assembly facility in Mexico to serve food, dairy, and pharmaceutical clients.

- September 2025: Merck KGaA broke ground on a EUR 150 million filter manufacturing plant in Cork, Ireland, adding 3,000 m² of ISO-class cleanroom to meet global vaccine and monoclonal antibody demand.

- September 2025: Thermo Fisher Scientific acquired Solventum’s Purification & Filtration business, adding membranes for bioprocessing, healthcare, and industrial markets.

Global Healthcare Membranes Market Report Scope

According to the scope of this report, healthcare membranes are specialized filtration materials used in medical devices to separate, purify, or concentrate biological fluids, thereby ensuring safety and efficacy in treatments such as dialysis, drug delivery, and blood oxygenation. These membranes are engineered for biocompatibility, precise pore structure, and high selectivity, supporting critical healthcare applications.

The healthcare membranes market is segmented into material, technology, application, and geography. By material, the market is segmented into polysulfone (PSU), polyether sulfone (PESU), polypropylene (PP), polytetrafluoroethylene (PTFE), polyvinylidene fluoride (PVDF), polyethylene (PE), and modified acrylics. By technology, the market is segmented into microfiltration, ultrafiltration, nanofiltration, reverse osmosis, dialysis, and gas separation. By application, the market is segmented into pharmaceutical filtration, iv infusion & sterile filtration, drug delivery, hemodialysis, bio-artificial pancreas, protein purification, cell separation, water management, and sterilization. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for all the above segments.

| Polysulfone (PSU) |

| Polyether Sulfone (PESU) |

| Polypropylene (PP) |

| Polytetrafluoroethylene (PTFE) |

| Polyvinylidene Fluoride (PVDF) |

| Polyethylene (PE) |

| Modified Acrylics |

| Microfiltration |

| Ultrafiltration |

| Nanofiltration |

| Reverse Osmosis |

| Dialysis |

| Gas Separation |

| Pharmaceutical Filtration |

| IV Infusion & Sterile Filtration |

| Drug Delivery |

| Hemodialysis |

| Bio-Artificial Pancreas |

| Protein Purification |

| Cell Separation |

| Water Management |

| Sterilization |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Material | Polysulfone (PSU) | |

| Polyether Sulfone (PESU) | ||

| Polypropylene (PP) | ||

| Polytetrafluoroethylene (PTFE) | ||

| Polyvinylidene Fluoride (PVDF) | ||

| Polyethylene (PE) | ||

| Modified Acrylics | ||

| By Technology | Microfiltration | |

| Ultrafiltration | ||

| Nanofiltration | ||

| Reverse Osmosis | ||

| Dialysis | ||

| Gas Separation | ||

| By Application | Pharmaceutical Filtration | |

| IV Infusion & Sterile Filtration | ||

| Drug Delivery | ||

| Hemodialysis | ||

| Bio-Artificial Pancreas | ||

| Protein Purification | ||

| Cell Separation | ||

| Water Management | ||

| Sterilization | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the healthcare membranes market by 2031?

It is forecast to reach USD 6.42 billion, growing at an 8.42% CAGR between 2026 and 2031.

Which material is expanding fastest within healthcare membrane applications?

Polyethersulfone is advancing at a 9.81% CAGR because it withstands gamma irradiation and caustic cleaning in single-use systems.

Why is nanofiltration gaining share over ultrafiltration?

Nanofiltration removes 18-100 nm viruses in a single pass, eliminating dual-stage viral inactivation and cutting 14-21 days from production cycles.

Which region is expected to grow most rapidly?

Asia-Pacific, supported by CDMO capacity expansions in South Korea, Singapore, and China, is projected to grow at 9.83% CAGR through 2031.

Page last updated on: