Sterile Filtration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

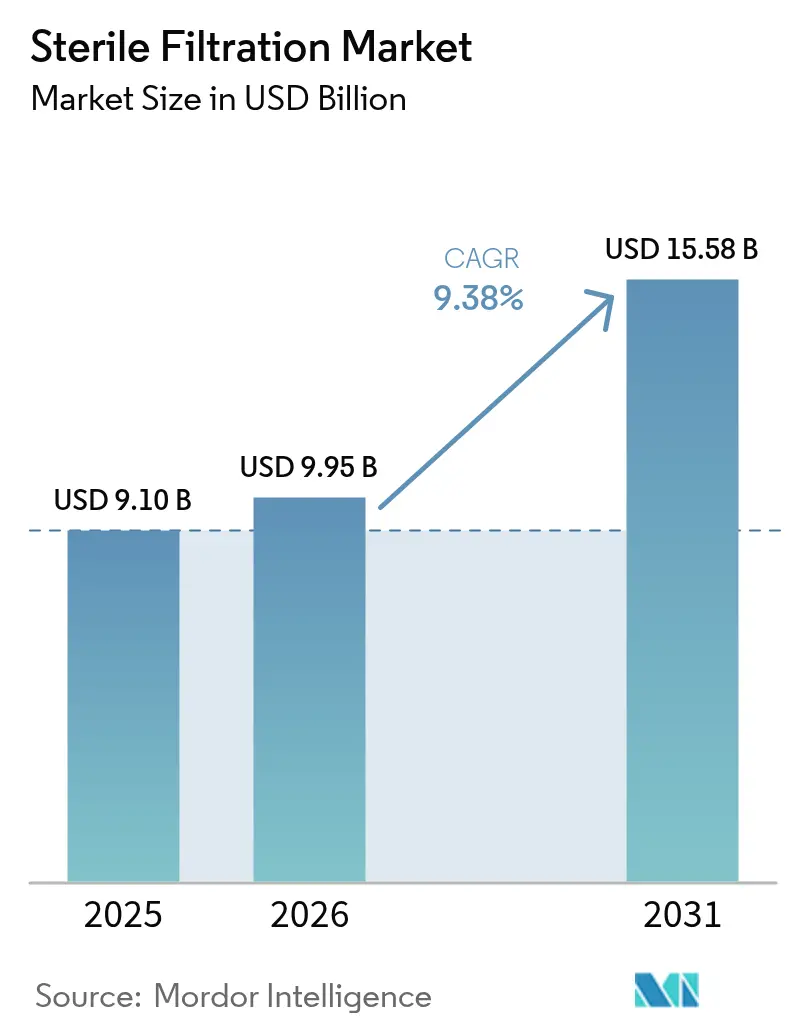

| Market Size (2026) | USD 9.95 Billion |

| Market Size (2031) | USD 15.58 Billion |

| Growth Rate (2026 - 2031) | 9.38% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterile Filtration Market Analysis by Mordor Intelligence

Sterile filtration market size in 2026 is estimated at USD 9.95 billion, growing from 2025 value of USD 9.1 billion with 2031 projections showing USD 15.58 billion, growing at 9.38% CAGR over 2026-2031. Rising contamination-control standards for advanced therapy medicinal products, together with the European Medicines Agency’s revised Annex 1 guidelines that require rigorous pre-use post-sterilization integrity testing, keep capital and validation spending on an upward trajectory. Demand scales further as chronic diseases spur sterile injectable volumes and single-use manufacturing gains wider acceptance. Contract development and manufacturing organizations (CDMOs) boost regional capacity, helping biopharma companies de-risk supply chains while maintaining speed to clinic. Cartridge filters remain the volume workhorse, yet capsule filters grow fastest on the back of small-batch gene and cell therapy requirements. Polyethersulfone (PES) membranes lead current installations, although looming PFAS restrictions are pushing producers to diversify away from polyvinylidene fluoride (PVDF).

Key Report Takeaways

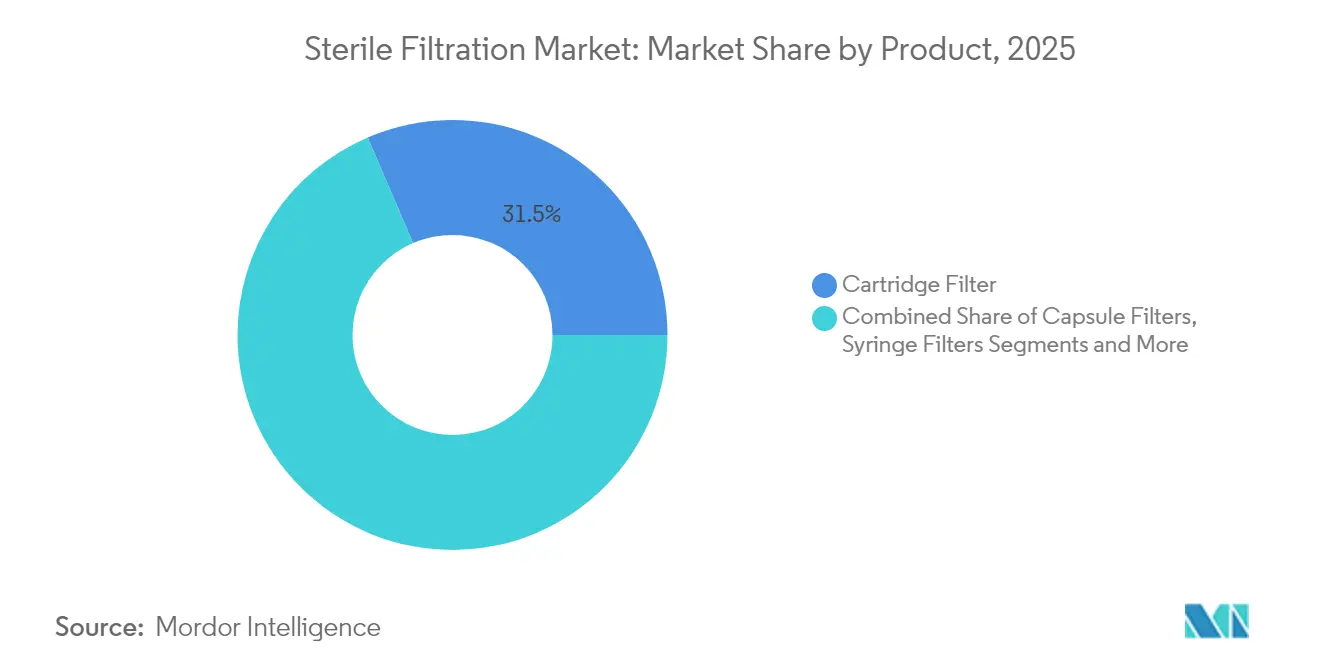

- By product type, cartridge filters held 31.45% of the sterile filtration market share in 2025, while capsule filters are projected to register a 10.22% CAGR through 2031.

- By membrane material, PES led with 24.95% share of the sterile filtration market size in 2025; PVDF membranes are set to expand at 10.03% CAGR between 2026-2031.

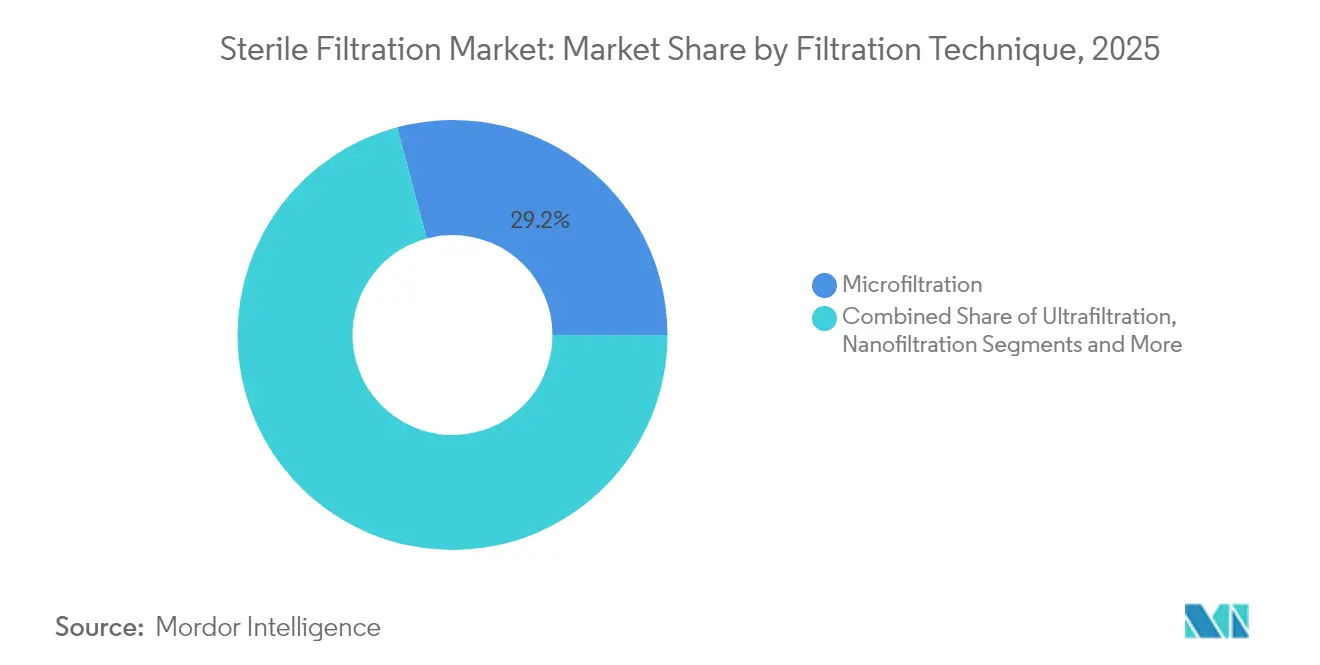

- By filtration technique, microfiltration accounted for 29.15% revenue in 2025, whereas ultrafiltration is expected to grow at 12.34% CAGR to 2031.

- By application, final fill/finish secured 19.75% share of the sterile filtration market size in 2025, and ATMP small-batch filtration is forecast to advance at a 13.05% CAGR through 2031.

- By end user, pharmaceutical and biopharmaceutical firms captured 39.75% revenue in 2025, while CDMOs are poised to expand at 12.64% CAGR to 2031.

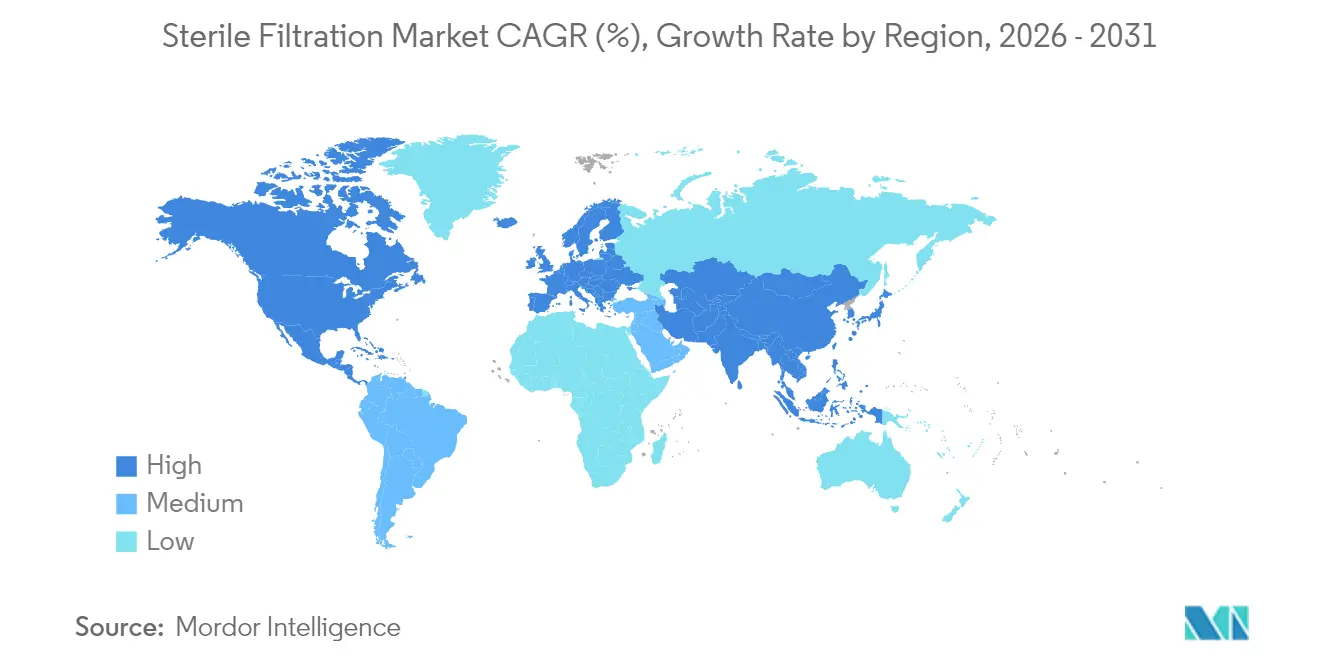

- By geography, North America led with 38.10% revenue share in 2025, while Asia Pacific is forecast to expand at a 8.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sterile Filtration Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Burden Of Chronic & Rare Diseases | +2.10% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Expansion Of Global Biopharmaceutical Manufacturing Capacity | +1.80% | APAC core, spill-over to North America & Europe | Medium term (2-4 years) |

| Shift Toward Single-Use And Modular Production Facilities | +1.50% | Global, led by North America & Europe | Medium term (2-4 years) |

| Stricter Global GMP & Annex 1 Revisions Tightening Filter Validation | +1.30% | Europe primary, North America secondary | Short term (≤ 2 years) |

| Surge In Advanced-Therapy Medicinal Products (ATMPs) Needing Low-Volume Sterile Runs | +1.20% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| AI-Driven Predictive Maintenance Reducing Filtration Failure Risk | +0.60% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Chronic & Rare Diseases

Orphan drugs represented nearly 50% of FDA-recognized therapeutics in 2024, anchoring sustained demand for final fill/finish filtration and driving long-run volume growth in the sterile filtration market. Capsule formats benefit most because they match low-volume, high-value production, while expedited approval pathways compress timelines and increase readiness pressure. Aging populations in developed economies, alongside improved access in emerging regions, hard-wire this demand driver into long-term health-care infrastructure.

Expansion of Global Biopharmaceutical Manufacturing Capacity

Total installed biopharma capacity rose from 16.5 million L in 2018 to 17.4 million L in 2025, with Samsung Biologics and MilliporeSigma committing multi-billion-dollar programs in South Korea. CDMOs are forecast to control 54% of global biologics capacity by 2028, underscoring the importance of standardized, validated filtration lines that can switch rapidly between client projects while meeting harmonized regulatory demands.

Shift Toward Single-Use and Modular Production Facilities

Single-use technology continues to grow at double-digit rates because it limits cross-contamination risk and curtails cleaning validation, thereby reinforcing sterile filtration market adoption. Integrated capsule filters reduce aseptic connections, streamline facility start-up, and enable distributed regional manufacturing footprints that align with personalized-medicine supply chains.

Stricter Global GMP & Annex 1 Revisions Tightening Filter Validation

Europe’s revised Annex 1, effective August 2023, mandates contamination-control strategies that elevate integrity-testing frequency and automation. Filter vendors differentiate through validation services and real-time monitoring, but smaller producers face higher compliance overhead, accelerating consolidation among manufacturers with robust regulatory infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Total Cost Of Ownership Of Validated Sterile Filters | -1.40% | Global, with highest impact in cost-sensitive emerging markets | Medium term (2-4 years) |

| Membrane Fouling & Integrity Test Failures Causing Downtime | -0.90% | Global, particularly affecting high-volume production facilities | Short term (≤ 2 years) |

| Long Lead-Times For Regulatory Re-Validation After Filter Or Process Change | -0.70% | Global, with highest impact in highly regulated markets | Medium term (2-4 years) |

| Emerging PFAS Regulations Threatening PTFE/PVDF Membrane Supply | -0.80% | Europe primary, with global supply chain implications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost of Ownership of Validated Sterile Filters

EU Annex 1 compliance has increased filtration-related costs by as much as 30%, a burden that smaller biopharma firms struggle to absorb. Fixed validation expenses encourage outsourcing to CDMOs with established platforms, creating scale advantages for larger players and raising entry barriers for novel filter formats that require extensive re-qualification.

Membrane Fouling & Integrity Test Failures Causing Downtime

Complex biologics can foul membranes or trigger integrity-test failures, causing line stoppages that jeopardize batch release.[1]Johannes E. Vogel, “Development and Upscaling of a Sterile Filtration Step for Concentrated Lentiviral Vectors,” Biotechnology Journal, onlinelibrary.wiley.com Advanced therapy manufacturers are especially exposed owing to high-value, low-volume lots. Predictive maintenance tools help mitigate the risk but demand capital and data expertise that not all sites can marshal.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Capsule Filters Drive Innovation

Cartridge filters dominated 2025 with 31.45% revenue, confirming their incumbency in high-volume plant operations. Capsule filters, however, are forecast to log a 10.22% CAGR owing to flexible batch scalability for personalized therapies. This momentum anchors the sterile filtration market size expansion for ATMP producers that need rapid changeovers without re-cleaning. Cytiva’s Emflon II gamma-compatible modules exemplify single-use advances that eliminate CIP validation burdens.

Syringe filters keep laboratory and clinical trial workflows moving even though their growth remains modest. Accessories such as holders, vent filters, and assemblies provide incremental gains as manufacturers emphasize closed-system integration to limit contamination events. This is a critical concern for regulators enforcing Annex 1 clarity on aseptic connections.

By Membrane Material: PES Dominance Faces PVDF Pressure

Polyethersulfone membranes held a 24.95% share in 2025 due to low protein binding and robust throughput, cementing their status for final fill/finish lines. PVDF variants are projected to grow 10.03% annually until 2031, driven by chemical resistance, yet pending PFAS restrictions in Europe threaten long-term accessibility. PES suppliers invest in next-generation grades to capture capacity migrating from PVDF.

PTFE, nylon, and mixed cellulose ester membranes fill application niches spanning gas filtration to low-cost buffer prep. The sterile filtration market is expected to witness accelerated R&D in fluoropolymer-free chemistries as customers look to de-risk material compliance and avoid costly system re-validation.

By Filtration Technique: Ultrafiltration Gains Momentum

Microfiltration sustained 29.15% revenue in 2025 as the default microbial barrier in bulk drug manufacturing. Ultrafiltration, growing at 12.34% CAGR, is increasingly chosen for virus clearance and protein concentration, serving the surge in monoclonal antibody and gene therapy pipelines. Toray’s hollow-fiber development, which marries selectivity with high flux, illustrates technical progress that shortens processing cycles.

Nanofiltration and reverse osmosis continue to underpin water-for-injection and buffer concentration schemes, though their higher energy and capital intensity keep them in specialized roles rather than broad adoption across the sterile filtration market.

By Application: ATMP Small-Batch Drives Growth

Final fill/finish retained 19.75% share of the sterile filtration market in 2025 because regulations require terminal filtration immediately before container closure. The ATMP small-batch niche is on track for 13.05% CAGR as gene and cell therapy pipelines commercialize and require validated, low-hold-up volume capsules.

Buffer/media prep and water-for-injection filtration move in lock-step with overall capacity additions, whereas air and gas sterilization rise as single-use systems demand validated venting for blow-fill-seal lines and closed processing steps.

By End User: CDMOs Accelerate Adoption

Pharmaceutical and biopharmaceutical companies produced 39.75% of 2025 sales, yet CDMOs will advance faster at 12.64% CAGR as sponsors outsource production and expect plug-and-play validation files. The sterile filtration market share gains for service providers mirror their rising stake in global biologic capacity, forecast to reach 54% by 2028.

Academic and government labs sustain steady bench-scale demand, while food and beverage processors adopt pharmaceutical-style sterility assurance mainly in high-risk liquids such as dairy concentrates and probiotic beverages.

Geography Analysis

North America and Europe command the lion’s share of 2025 revenue owing to entrenched biopharmaceutical clusters, advanced regulatory oversight, and a strong pipeline of injectable therapeutics. U.S. capacity expansions from Novo Nordisk’s USD 4.1 billion site in North Carolina to Eli Lilly’s USD 2 billion Concord investment embed long-run demand for filtration hardware and validation services. Europe’s Annex 1 revisions, now the global contamination-control benchmark, compel every drug maker exporting into the region to align filtration strategies.

Asia Pacific, led by South Korea, delivers the fastest-growing sterile filtration market through 2031 because of major greenfield projects such as Cytiva’s USD 326 million Incheon plant and Samsung Biologics’ multi-billion-dollar campus. China and India scale facilities that meet FDA and EMA standards, while Japan’s materials expertise buttresses membrane R&D, reinforcing regional self-sufficiency goals. MilliporeSigma’s EUR 300 million Daejeon center underlines incumbent suppliers’ commitment to localizing production.

Middle East & Africa and South America remain emerging but strategic territories. Brazil and Argentina advance fill/finish lines to curb import reliance, and GCC nations embed pharmaceutical manufacture within diversification plans. Technology transfer initiatives and government incentives ease skills gaps and build the regulatory foundations needed for future sterile filtration market penetration.

Competitive Landscape

The sterile filtration market demonstrates moderate concentration. Danaher, Sartorius, and Merck KGaA leverage broad portfolios, validation toolkits, and global supply chains to safeguard their share as Annex 1 rules tighten. Danaher reported USD 5.74 billion revenue for Q1 2025 with sustained bioprocessing order growth over seven quarters, reflecting resilient demand for filtration and single-use assemblies.

Thermo Fisher’s USD 4.1 billion purchase of Solventum’s purification and filtration line intensifies competition, extending its reach into high-growth biologics workflows. AI-driven predictive maintenance, disposable system integration, and PFAS-free membrane alternatives are becoming decisive differentiators. Smaller innovators thrive in niches—virus filters with superior flux or regional servicing—but higher compliance hurdles encourage strategic partnerships or bolt-on deals with larger multinationals.

Regulators also spur innovation; FDA patent activity around real-time integrity analytics indicates a future where automated systems can flag contamination risks as batches run, rewarding suppliers equipped with sensor-rich cartridges and data platforms.[3]U.S. Food and Drug Administration, “Q5A(R2) Viral Safety Evaluation of Biotechnology Products,” fda.gov As customers prioritize risk mitigation over unit cost, technology leadership and global support networks outweigh simple price competition.

Sterile Filtration Industry Leaders

Merck KGaA

Danaher Corporation

ThermoFisher Scientific Inc.

Sartorius AG

GE Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Thermo Fisher Scientific closed the USD 4.1 billion acquisition of Solventum’s Purification & Filtration business, adding roughly USD 1 billion in 2024 revenue to its bioprocessing division.

- February 2025: Resilience received USD 17.5 million from the U.S. Department of Health and Human Services to expand domestic sterile filtration capability.

- January 2025: DuPont introduced FilmTec LiNE-XD nanofiltration elements for lithium brine purification, underscoring membrane innovation that can translate back into pharmaceutical filtration workflows.

- November 2024: Cytiva inaugurated a 6,100 m² Incheon plant focused on sterile filtration production, projected to add 150 jobs

Global Sterile Filtration Market Report Scope

As per the scope of the report, sterile filtration is a technique used in manufacturing drugs to avoid contamination by filtering the micro-organisms without degrading product quality. The sterile filtration market is segmented by product (cartridge filter, capsule filter, syringe filter, other membrane filters, accessories), end user (pharmaceutical and biopharmaceutical companies, contract research organizations, research laboratories), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions. The report offers the value of market sizes and forecasts in USD million for the above segments.

| Cartridge Filters |

| Capsule Filters |

| Syringe Filters |

| Other Membrane Filters |

| Accessories |

| PES |

| PVDF |

| PTFE |

| Nylon & MCE |

| Others (PP, RC, etc.) |

| Microfiltration |

| Ultrafiltration |

| Nanofiltration & Reverse Osmosis |

| Final Fill / Finish |

| Buffer & Media Preparation |

| Water-for-Injection & Utilities |

| Air & Gas Sterilization |

| Others |

| Pharmaceutical & Biopharmaceutical Companies |

| Contract Development & Manufacturing Organizations (CDMOs) |

| Academic & Government Research Labs |

| Food & Beverage Manufacturers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina |

| By Product | Cartridge Filters | |

| Capsule Filters | ||

| Syringe Filters | ||

| Other Membrane Filters | ||

| Accessories | ||

| By Membrane Material | PES | |

| PVDF | ||

| PTFE | ||

| Nylon & MCE | ||

| Others (PP, RC, etc.) | ||

| By Filtration Technique | Microfiltration | |

| Ultrafiltration | ||

| Nanofiltration & Reverse Osmosis | ||

| By Application | Final Fill / Finish | |

| Buffer & Media Preparation | ||

| Water-for-Injection & Utilities | ||

| Air & Gas Sterilization | ||

| Others | ||

| By End User | Pharmaceutical & Biopharmaceutical Companies | |

| Contract Development & Manufacturing Organizations (CDMOs) | ||

| Academic & Government Research Labs | ||

| Food & Beverage Manufacturers | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

Key Questions Answered in the Report

What is the current size of the sterile filtration market?

The sterile filtration market is valued at USD 9.95 billion in 2026 and is projected to grow to USD 15.58 billion by 2031.

Which product type leads the sterile filtration market?

Cartridge filters lead with 31.45% share in 2025, while capsule filters are growing fastest at a 10.22% CAGR.

Why is Asia Pacific the fastest-growing region?

Large-scale investments by Samsung Biologics, Cytiva, and others are boosting biopharmaceutical capacity and driving filtration demand.

How are Annex 1 revisions affecting filtration suppliers?

The new guidelines increase integrity-testing frequency and validation documentation, favoring suppliers with advanced monitoring and compliance services.

Which end-user group is expanding the quickest?

CDMOs are forecast to rise at 12.64% CAGR as pharmaceutical companies outsource more manufacturing activities.

Page last updated on: