Pharmaceutical Membrane Filtration Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

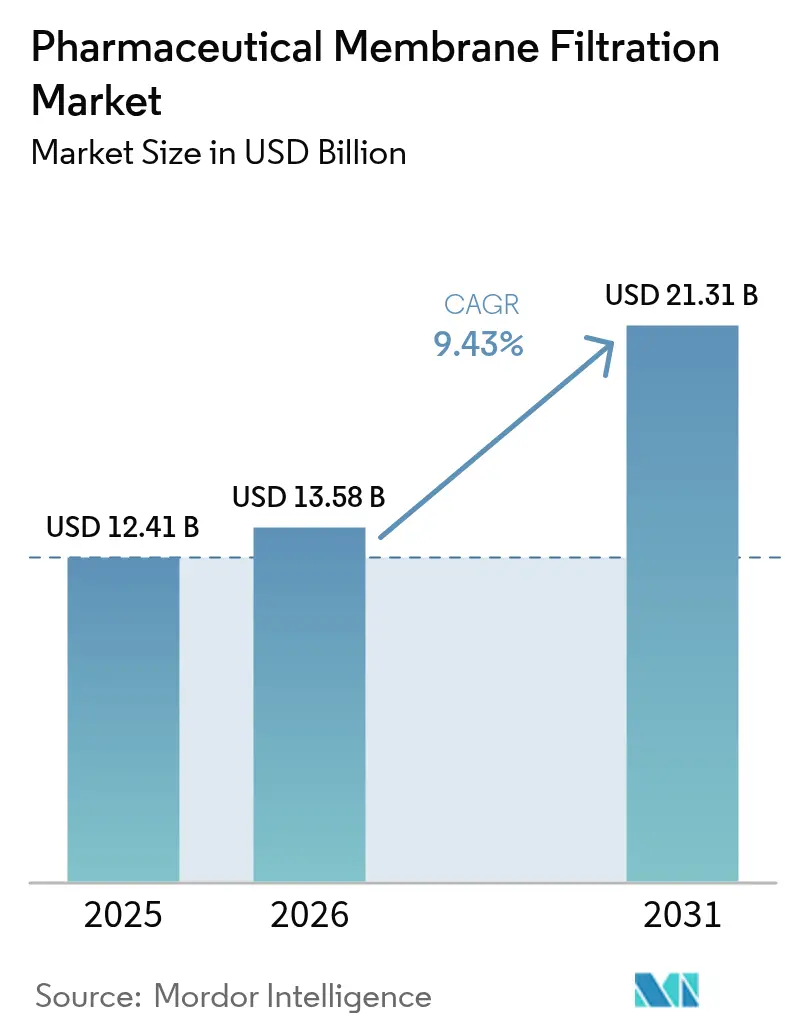

| Market Size (2026) | USD 13.58 Billion |

| Market Size (2031) | USD 21.31 Billion |

| Growth Rate (2026 - 2031) | 9.43% CAGR |

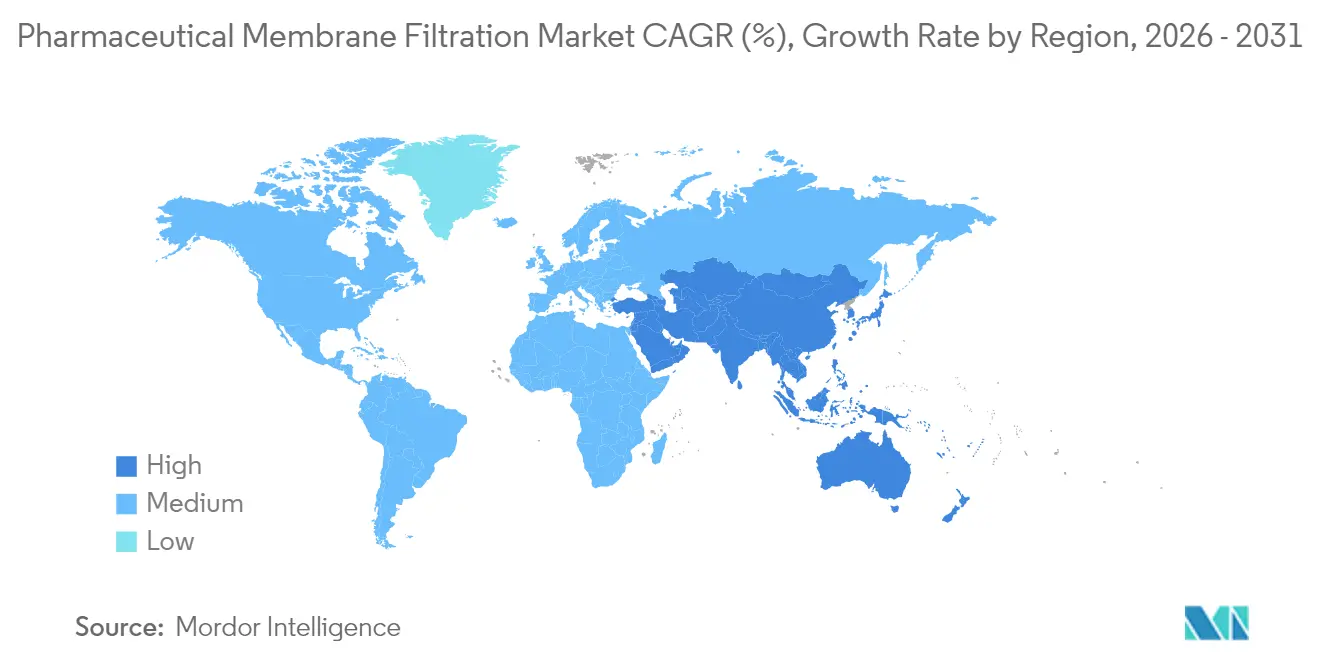

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Membrane Filtration Market Analysis by Mordor Intelligence

The Pharmaceutical Membrane Filtration market size is expected to grow from USD 12.41 billion in 2025 to USD 13.58 billion in 2026 and is forecast to reach USD 21.31 billion by 2031 at 9.43% CAGR over 2026-2031.

Demand stems from the surge in biologics, gene therapies, and vaccine programs that require sterile, high-performance filters. The sector also benefits from regulatory pressure to prove viral clearance and from single-use systems that heighten production agility while curbing cross-contamination. Investments in nanofiltration, continuous processing, and real-time analytics further lift adoption, especially for virus removal, protein concentration, and water-for-injection operations. North America retains a leading position thanks to an entrenched bioprocessing base and clear guidance from the FDA, while Asia-Pacific gains momentum on the back of large-scale capacity additions and biotech incentives.

Key Report Takeaways

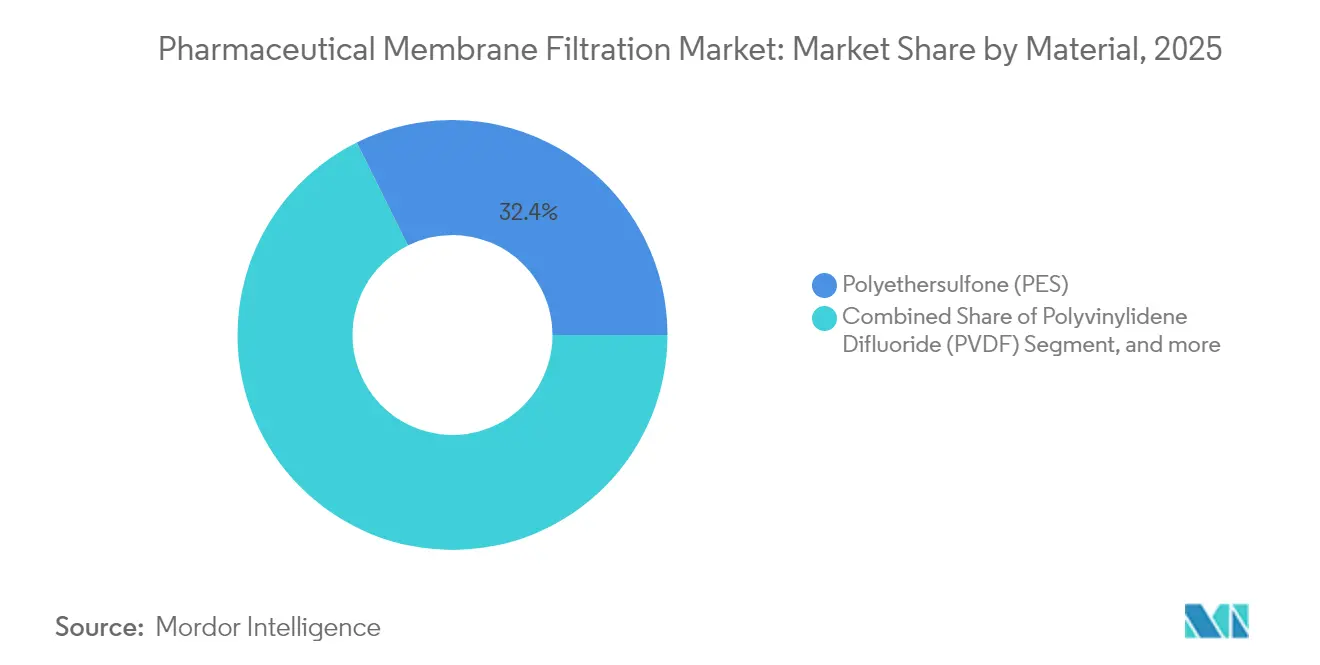

- By material, polyethersulfone led with 32.35% revenue share in 2025; polyvinylidene difluoride is projected to advance at a 9.73% CAGR to 2031.

- By technique, microfiltration accounted for 43.75% of the pharmaceutical membrane filtration market size in 2025 while nanofiltration is forecast to grow at 12.45% CAGR through 2031.

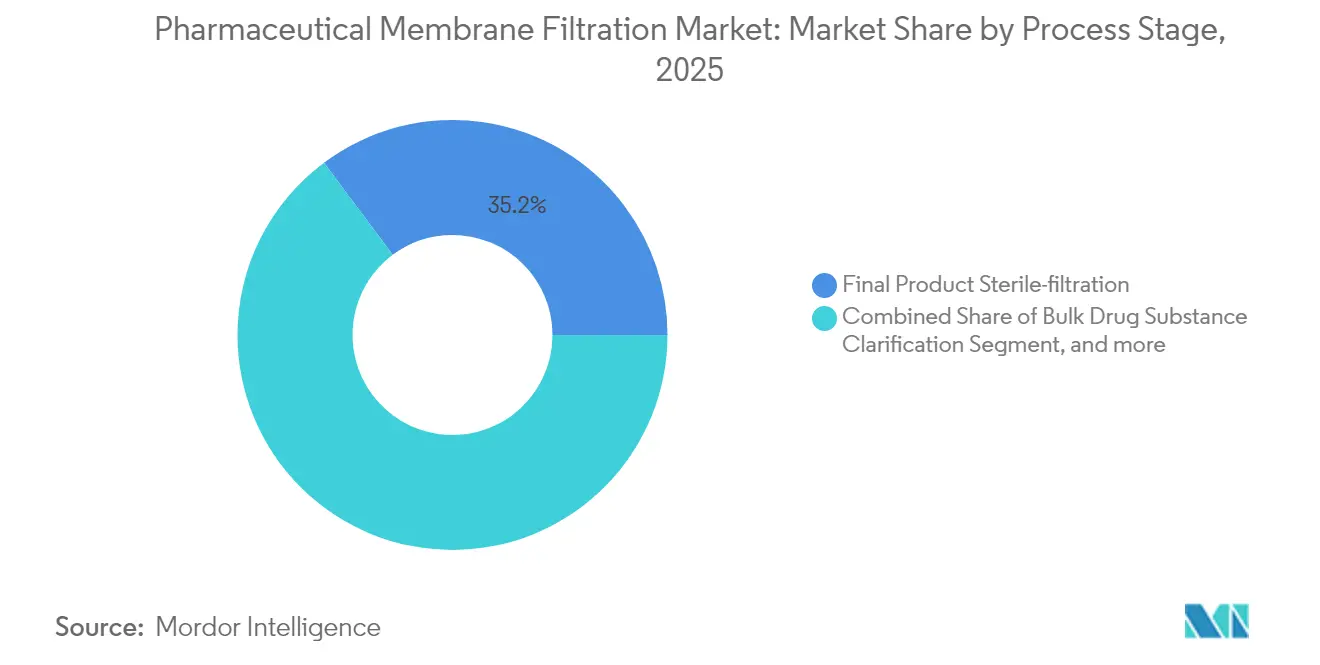

- By process stage, sterile filtration held 35.20% of pharmaceutical membrane filtration market share in 2025; bulk drug substance clarification is set to expand at 14.07% CAGR up to 2031.

- By scale, commercial production commanded 52.90% of the pharmaceutical membrane filtration market in 2025; laboratory scale exhibits a 10.04% CAGR through 2031.

- By geography, North America captured 36.10% of the pharmaceutical membrane filtration market share in 2025 while Asia-Pacific posts the fastest 11.23% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Pharmaceutical Membrane Filtration Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing adoption of single-use technologies | +1.8% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Expansion of biologics and gene therapy pipelines | +2.1% | North America and Europe core, expanding to APAC | Long term (≥ 4 years) |

| Stringent regulatory requirements | +1.2% | Global, with EU leading PUPSIT mandates | Short term (≤ 2 years) |

| Advancements in nanofiltration technology | +1.5% | Global, R&D concentrated in developed markets | Medium term (2-4 years) |

| Rising R&D investments | +1.0% | North America, Europe, and emerging APAC markets | Long term (≥ 4 years) |

| Expanding pharmaceutical manufacturing in emerging markets | +1.4% | APAC core, Latin America and MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Adoption of Single-Use Technologies

Single-use filtration assemblies shorten change-over times by up to 50% and remove cleaning validation, making them a central pillar of modern biologics facilities. Compatibility with hollow-fiber tangential-flow designs lets producers retrofit legacy lines quickly. Flexible bag-based systems permit parallel campaigns for personalized therapies, while built-in sensors transmit critical quality data that satisfy FDA expectations for continuous monitoring. Cost advantages rise as utilities and labor shrink, and waste volumes decline thanks to lighter construction materials. As gene therapy volumes scale, single-use cartridges rated to >99.999% endotoxin removal enable rapid batch turnaround without risking cross-product carryover.[1]Masahito Tahashi, “Planova FG1: Next-Generation Virus Filter,” asahi-kasei.com The model aligns with pandemic-preparedness strategies that require fast site deployment and surge capacity.

Expansion of Biologics & Gene Therapy Pipelines

The global biologics pipeline surpasses 10,000 active programs, each requiring robust virus filtration that meets >6 log10 reduction mandates. Plasmid DNA and viral vectors impose high-viscosity loads that spur demand for membranes with optimized pore geometry to avoid shear-induced degradation.[2]Food and Drug Administration, “Q5A(R2) Viral Safety Evaluation,” fda.govAsahi Kasei’s Planova FG1 delivers seven-fold higher flux, cutting process time without compromising retention. Updated Q5A(R2) guidance promotes risk-based validation, encouraging application-specific filter development that supports rapid commercialization. The trend extends to mRNA vaccines, where clarification and sterilization must proceed under low binding conditions to protect fragile lipid nanoparticles.

Stringent Regulatory Requirements

Revised EU Annex 1 enforces Pre-Use Post-Sterilization Integrity Testing that forces manufacturers to integrate real-time leak detection and automated reporting.[3]Pharmaceutical and Healthcare Association, “Annex 1 Sterile Manufacturing Revision,” pda.org Divergent US and EU positions create dual compliance paths, prompting global firms to adopt the stricter standard to avoid repeat qualification. Authorities now expect Failure Modes and Effects Analysis on every filter train, driving uptake of fully automated testers that log events and prevent operator errors. Continuous process verification places extra weight on in-line analytics, increasing capital outlays but accelerating deviation response. PDUFA VII signals ongoing FDA support for advanced manufacturing, reinforcing the business case for cutting-edge filtration.

Advancements in Nanofiltration Technology

Breakthroughs in graphene and MXene layers produce membranes with near-atomic thickness that deliver higher flux at the same selectivity, easing the historical permeability-selectivity trade-off. High-pressure systems now maintain precise 200–1,000 Da cut-offs, letting manufacturers fine-tune protein purification. Solvent-resistant variants enable direct processing of organic reaction streams, removing dry-down steps and saving energy. Optimization studies show nanofiltration throughput can climb from 100 L/m² to 900 L/m² when pH, conductivity, and pressure are balanced, trimming filtration cost per gram of biologic. Predictive modeling software embedded in skid controls accelerates tech transfer by simulating performance on varied feedstocks.

Restraints Impact Analysis of Pharmaceutical Membrane Filtration Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital investment | -1.3% | Global, higher in emerging markets | Short term (≤ 2 years) |

| Membrane fouling and reduced lifecycle | -1.1% | Global, affecting continuous operations | Medium term (2-4 years) |

| Complexity in integration | -0.8% | Developed markets with advanced manufacturing | Medium term (2-4 years) |

| Limited awareness in developing regions | -0.6% | APAC emerging markets, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Investment

Commercial-scale filtration suites cost upward of USD 10 million once skids, analytics, and validation are included, a hurdle for small firms and CDMOs. Integration of PAT sensors raises spending further because data historians and cybersecurity layers must be certified. Emerging-market manufacturers often rely on subsidies or partnerships to secure funding, and currency fluctuations can erode budgets. Thermo Fisher’s USD 4.1 billion Solventum purchase shows the size of bets required to stay competitive in purification technology. Multinational companies must duplicate test protocols across regions, swelling capital tied up in duplicate equipment.

Membrane Fouling Issues & Reduced Lifecycle

Protein aggregates, DNA, and lipids form cakes and adsorb on pore walls, cutting permeate flux by 35% if unmanaged. Virus filtration is prone to nanoparticle capture inside depth layers that shift under load, risking breakthrough. Cleaning cycles add downtime and chemical costs, while harsh agents shorten membrane life. Anti-fouling surface treatments and asymmetric pore designs mitigate the effect, but users must validate new materials, extending project timelines. Continuous manufacturing heightens risk because filters stay online longer, making predictive fouling analytics a growing requirement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Pharmaceutical Membrane Filtration Market Segment Analysis

By Material:

PES Dominance Faces PVDF InnovationPES accounted for 32.35% of the pharmaceutical membrane filtration market in 2025, favored for high chemical resistance and low protein binding. Its hydrophilic nature supports 211 mL/min flow rates with protein adsorption below 1%, enabling consistent yields in mAb purification. Surface sulfonation and PEG grafting deepen hydrophilicity, stretch lifespan, and limit fouling.

PVDF is projected to grow at 9.73% CAGR despite PFAS scrutiny, owing to its low extractables and suitability for final fill lines. Regulatory uncertainty encourages suppliers to devise PFAS-free variants, but users value PVDF’s thermal stability for steam-in-place cycles. Mixed cellulose ester, nylon, and polypropylene membranes satisfy niche lab or cost-sensitive tasks where extreme robustness is not essential. Comparative studies find PES retains permeability under high solids loads while PVDF excels in low-binding sterile filtration. Manufacturers target ultraclean grades that meet ever tighter leachables limits, preserving product purity throughout storage.

By Technique:

Microfiltration Leads While Nanofiltration AcceleratesMicrofiltration held 43.75% revenue share in 2025 due to entrenched use for cell harvesting and bioburden reduction. Resistance-in-series models allow accurate scale-up, ensuring pilot data translate to manufacturing. Continuous microfiltration combined with alternating tangential flow lifts harvest titers for intensified fed-batch cultures. Nanofiltration is set to rise at 12.45% CAGR on the back of vaccine and gene therapy pipelines demanding virus removal under high flux.

Two-dimensional material coatings raise water permeability without sacrificing 20 nm pore exclusion, facilitating >6 log10 virus clearance. Scale-down rigs help define optimal pH and conductivity windows, driving 900% throughput gains when parameters are tuned. Ultrafiltration remains vital for buffer exchange and protein concentration, whereas reverse osmosis handles water treatment for injection systems.

By Process Stage:

Sterile Filtration Dominance Challenged by Clarification GrowthFinal sterile filtration captured 35.20% of the pharmaceutical membrane filtration market size in 2025, reflecting its role as the last barrier before fill-finish. Authorities demand Brevundimonas diminuta challenge tests that prove absolute retention, prompting widespread use of 0.22 µm PES and PVDF cartridges. Single-use capsule formats enjoy popularity for small campaign drugs because integrity tests can be run in line without product loss.

Bulk drug substance clarification is forecast to climb at 14.07% CAGR as high-cell density cultures raise impurity loads needing depth filtration before chromatographic polishing. Next-generation depth media with dual-layer designs remove DNA and HCP while controlling turbidity. Water and utility filtration, air and gas filters, and cell-harvest steps continue to underpin upstream hygiene, but the shift toward continuous processing increases demand for robust clarification trains that sustain days of operation.

By Scale:

Commercial Production Leads Laboratory InnovationCommercial plants made up 52.90% of the pharmaceutical membrane filtration market in 2025, underscoring mature blockbuster portfolios. Integrated suites merge clarification, concentration, and virus filtration on a single skid to minimize footprint. Pilot lines bridge R&D and plant, offering right-first-time tech transfer through matched shear and flux conditions.

Laboratory systems are projected to expand at 10.04% CAGR as gene editing and mRNA research accelerates, fueling demand for flexible bench rigs that evolve into GMP platforms. Scale-down cross-flow cells preserve feed ratios so developers can model fouling and optimize CIP prior to capex approval. Modular designs let users add steps progressively, aligning spend with program milestones and reducing financial exposure.

Geography Analysis

North America and Europe Pharmaceutical Membrane Filtration Market

North America retained 36.10% share of the pharmaceutical membrane filtration market in 2025, powered by a dense network of biologics plants and an FDA that endorses advanced manufacturing with clear guidance. Federal incentives for pandemic preparedness sustain spending on high-capacity single-use systems and continuous lines. Europe follows closely, driven by Annex 1 revisions that compel producers to adopt PUPSIT and automated integrity checks. Firms invest in virus filters and data-rich skids to navigate stringent audit expectations.

APAC, LATAM and Middle East Pharmaceutical Membrane Filtration Market

Asia-Pacific is set to grow at 11.23% CAGR through 2031 as governments pour funds into biotech hubs. Cytiva’s USD 150 million Korean site and MilliporeSigma’s EUR 300 million plant in Daejeon signal the region’s ascent, offering local supply of sterile filters and single-use kits that shorten logistics chains. China and India increase GMP adherence, with close to 90% of Chinese and 100% of Indian biomanagers targeting global market entry. Latin America and the Middle East make incremental progress, led by Brazil and Saudi Arabia, which court CDMOs to diversify their economies. Harmonization of ICH guidelines eases technology transfer, enabling global firms to deploy identical filtration trains across multiple continents.

Regulatory Landscape

Sterile manufacturing and viral safety expectations continue to shape membrane selection, validation depth, and integrity testing practices in pharmaceutical filtration. In the European Union, EU GMP Annex 1 is fully enforceable (with the final provision taking effect in August 2024), requiring a site-wide Contamination Control Strategy (CCS) and tightening control of sterile filtration steps, including Pre-Use Post-Sterilization Integrity Testing (PUPSIT) for sterilizing-grade filters. In parallel with Annex 1 implementation, EDQM issued revised guidance in November 2024 (PA PH CEP (23) 54) clarifying dossier requirements for sterile substances, including explicit documentation and validation evidence for sterilizing filtration, such as filter identification and microbial challenge testing.

In the United States, cGMP expectations under 21 CFR Parts 210 and 211 continue to underpin filter validation and in-process control, with FDA guidance widely used to demonstrate bacterial retention capability of membrane filters. A major 2026 standards milestone also affects filtration assemblies and single-use components: USP General Chapters 665 and 1665 became fully enforceable on May 1, 2026, establishing a risk-based framework for evaluating process equipment-related leachables (PERLs) from polymeric components. This increases documentation and qualification burden for plastic housings, connectors, and single-use filtration flow paths used in drug substance and drug product manufacturing.

Competitive Landscape

The pharmaceutical membrane filtration market shows moderate consolidation. Danaher merged Cytiva and Pall, forming a USD 7.5 billion bioprocessing unit that delivers end-to-end filtration and purification. Thermo Fisher broadened its footprint by buying Solventum’s purification business for USD 4.1 billion, linking chromatography resins with single-use systems. Asahi Kasei advances virus filters with Planova FG1, achieving higher flux that shortens cycle times.

Suppliers discriminate through regulatory expertise, especially around PUPSIT and Annex 1, and through digital twins that predict fouling. Parker-Hannifin leverages industrial filtration know-how to address pharmaceutical gas and utility lines, expanding its sector reach. Competition intensifies in Asia-Pacific where local manufacturers seek regional suppliers to avoid import bottlenecks. Emerging players focus on graphene and MXene membranes with anti-fouling coatings, aiming to displace incumbents in high value virus removal niches.

Pharmaceutical Membrane Filtration Industry Leaders

3M

Danaher Corporation

GE Healthcare

Thermo Fisher Scientific

Merck KGaA

- *Disclaimer: Major Players sorted in no particular order

Pharmaceutical Membrane Filtration Market Companies Covered in this Report

- 3M

- Danaher

- Merck

- Sartorius

- Thermo Fisher Scientific

- Parker Hannifin

- Repligen

- GEA Group

- Graver Technologies

- GE Healthcare

- Meissner Filtration

- Alfa Laval

- Cobetter Filtration

- Amazon Filters

- Porvair Filtration Group

- Novasep

- Donaldson Company

- Asahi Kasei

- Tami Industries

- Cole-Parmer

Read Analysis of Pharmaceutical Membrane Filtration Companies

Market Opportunities and Future Outlook

Annex 1 execution, along with broader contamination control expectations, is creating near-term demand for validated, automated integrity testing and closed-system sterile filtration configurations that reduce operator variability while supporting audit-ready electronic records. Standardization efforts are also expanding addressable needs: ASTM released Standard Practice E3469-26 in April 2026 for validating end-user sterilizing filtration of pharmaceutical and biological products. This supports more consistent qualification approaches across sites and CDMOs, while also enabling pull-through demand for fit-for-purpose test methods, training, and validation services tied to sterilizing-grade membrane filters.

Process intensification in biologics and viral vector manufacturing is creating specific opportunities in higher-throughput TFF/UF-DF systems, improved cleaning strategies, and newer membrane materials aimed at the fouling and productivity constraints seen in continuous or long-duration operations. Peer-reviewed work published in 2026 also points to practical development paths for viral vector-compatible membranes, scale-up toolkits, and application-specific consumables, including scalable continuous concentration and diafiltration using dual-membrane technology (Biotechnology Progress, June 2026) and TFF cassette geometries evaluated for reproducible AAV8 downstream processing (MDPI Membranes, February 2026). At the same time, new validation and materials research, including COF-based membranes for precise pharmaceutical molecule separations (Journal of Membrane Science, May 2026), reflects a technology pipeline that supports tighter selectivity targets while preserving manufacturability for virus removal, protein concentration, and polishing steps where yield and cycle-time constraints are most acute.

Recent Industry Developments in Pharmaceutical Membrane Filtration Market

- April 2026: Merck KGaA announced the expansion of its manufacturing facility in Peenya, Bengaluru, India, adding new production lines for filtration hardware systems and Pellicon 2 ultrafiltration cassettes. The expansion strengthens in-region supply for single-use and membrane-based operations, supporting faster fulfillment and redundancy for bioprocess filtration demand across Asia-Pacific.

- September 2025: Thermo Fisher Scientific completed its acquisition of Solventum’s Purification and Filtration business for about USD 4.0 billion in cash. The combination expands Thermo Fisher’s filtration and purification portfolio across bioprocessing and adjacent industrial applications, increasing its ability to deliver integrated workflows spanning upstream through downstream operations.

- June 2024: Thermo Fisher Scientific introduced the KingFisher PlasmidPro Maxi Processor, an automated system for plasmid DNA purification. By accelerating plasmid preparation used in cell and gene therapy development, the launch supports higher-throughput programs that drive downstream filtration, UF/DF, and sterile processing needs as candidates transition toward GMP manufacturing.

Pharmaceutical Membrane Filtration Market Report Scope and Research Methodology

Market Definition and Coverage

This market covers membrane-based filtration technologies used in pharmaceutical and biopharmaceutical manufacturing to remove particles, microbes, and, in some cases, viruses, from drug substances, drug products, and supporting process fluids across lab, pilot, and commercial operations.

Scope exclusions: We exclude separation that does not use an integral membrane, such as depth-only filtration, centrifugation, and chromatography-only steps.

Segments Covered in This Report

- By Material

- Polyethersulfone (PES)

- Polyvinylidene Difluoride (PVDF)

- Mixed Cellulose Ester & Cellulose Acetate (MCE & CA)

- Nylon

- Polypropylene & Others

- By Technique

- Microfiltration

- Ultrafiltration

- Nanofiltration

- Reverse-Osmosis & Others

- By Process Stage

- Final Product Sterile-filtration

- Bulk Drug Substance Clarification

- Cell Separation & Harvesting

- Water & Utility Filtration

- Air/Gas Filtration

- By Scale

- Laboratory

- Pilot

- Commercial Production

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research sets the boundaries and gives the hard-to-argue context that a model needs, such as manufacturing activity, regulatory expectations around sterile processing, and where capacity is being added. We typically reference public sources such as the US FDA database and guidance libraries, EMA publications, the US International Trade Commission trade statistics, UN Comtrade, and peer-reviewed journal articles on membrane performance and sterilizing-grade filtration.

To convert the context into sizing inputs, we also use items like company annual reports and investor presentations, industry association notes, and reputable press coverage on capacity additions and biologics pipelines. In some cases, paid subscriptions for company financials, patent intelligence, and shipment-level trade views are used to cross-check revenues, technology adoption, and import-export signals. These desk sources are illustrative only, and many other references are used during data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test what the public data cannot fully show, such as how filtration is counted at each process stage, how single-use assemblies are priced, and how quality and validation requirements shift demand. We speak with a mix of manufacturers, distributors, and end users across APAC, EMEA, and the Americas so assumptions on volumes, replacement cycles, and ASP movement can be adjusted to what is seen in real buying and qualification decisions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 12% | APAC: 41% |

| Mid tier: 49% | Functional/Unit leaders: 29% | EMEA: 36% |

| Smaller Players: 17% | Managers: 59% | Americas: 23% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where production and trade signals, along with sterile-processing intensity, are used to reconstruct the demand pool for membrane filtration used in pharma manufacturing. The model is then corroborated with selective bottom-up approximations, such as sampled ASP times unit volumes for commonly purchased formats and supplier-channel checks, and gaps are handled using conservative ranges that are narrowed through interviews.

Key inputs (illustrative) include biologics and vaccine manufacturing scale-up activity, sterile fill-finish throughput, adoption of single-use filtration assemblies, validation and integrity testing requirements, and membrane type mix by technique and process stage. For the forecast, scenario analysis is used so demand can be flexed based on capacity additions, mix shift toward biologics, and expected pricing movement that respondents see in contracts and qualification cycles. When assumptions conflict, the final number is anchored to the set that best matches observed production activity and replacement behavior.

Data Validation & Update Cycle

Outputs are checked against independent signals such as manufacturing expansion announcements, trade movement for relevant filtration items, and reported exposure of key suppliers to bioprocessing and pharma consumables. Variance checks are run across regions and process stages, and outliers are reviewed in a second analyst pass before sign-off.

The dataset is refreshed on an annual cycle, and interim updates are made when a material event changes demand or pricing assumptions. Before delivery, a final review pass is completed so clients receive an updated view that matches the latest public releases and what experts confirm in follow-up calls.

Mordor Intelligence's Pharmaceutical Membrane Filtration Technologies Market Market Estimate Compared With Other Published Estimates

Published market sizes for pharmaceutical membrane filtration technologies can differ a lot, even when the topic sounds the same at first glance. In our experience, the split usually comes from how each study draws the boundary of what counts as a membrane filtration sale, and then how pricing and replacement cycles are handled over the forecast window.

Trade-linked signals and process-stage checks are often the deciding evidence, because they show whether a number is accidentally mixing in adjacent separation tools, or missing single-use assemblies that are routinely qualified and replaced. Those same checks keep Mordor Intelligence aligned to membrane-integral units and assemblies used across lab, pilot, and commercial drug manufacturing, instead of blending in non-membrane steps or broader water-treatment scopes.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.58 B (2026) | |

| Industry Publisher A | USD 5.11 B (2025) | Uses a narrower counted scope that can lean toward membrane filter consumables and selected pharma use cases, which tends to reduce the total versus counting membrane-integral assemblies across multiple manufacturing stages. |

| Industry Publisher B | USD 2.87 B (2025) | Appears to apply tighter inclusion rules and technique coverage, and may treat parts of single-use filtration assemblies and process-fluid filtration as outside scope, which lowers the stated value. |

Looking across the three figures, the spread is mainly explained by what is counted as in-scope membrane filtration, and whether multi-stage pharma manufacturing use is fully captured. By tying the model to observable production intensity, technique and stage mix, and interview-led replacement and pricing realities, the estimate stays traceable and repeatable even when public data is incomplete.

Key Questions Answered in the Report

What is driving growth in the pharmaceutical membrane filtration market?

Demand for biologics, stringent viral clearance regulations, and the shift to single-use systems are the dominant growth catalysts that sustain a 9.43% CAGR through 2031.

Which material currently leads the pharmaceutical membrane filtration market?

Polyethersulfone holds 32.35% share because of its chemical stability, thermal resistance, and low protein binding.

Why is nanofiltration growing faster than other techniques?

Nanofiltration offers precise virus removal and selective small-molecule separation, driving a 12.45% CAGR as gene and cell therapies expand.

How do regulatory changes affect sterile filtration operations?

EU Annex 1 now mandates Pre-Use Post-Sterilization Integrity Testing, compelling manufacturers to deploy automated testers and enhanced leak detection.

Which region is expected to post the fastest growth?

Asia-Pacific stands out with an 11.23% CAGR due to large-scale facility build-outs and strong government support for biotechnology.

Page last updated on: