U.S. Dental Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year Market Size (2025) | USD 215 Billion |

| Market Size (2026) | USD 224.56 Billion |

| Market Size (2031) | USD 279.18 Billion |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Dental Care Market Analysis by Mordor Intelligence

The U.S. Dental Care Market size is projected to expand from USD 215 billion in 2025 and USD 224.56 billion in 2026 to USD 279.18 billion by 2031, registering a CAGR of 4.45% between 2026 to 2031.

In 2024, national dental care expenditures reached USD 189 billion, reflecting a 3.6% increase in inflation-adjusted terms from 2023. This growth indicates that spending was already on the rise before the current forecast period began.[1]American Dental Association, “The Dental Care Market,” ADA Health Policy Institute, ada.org By early 2026, consumer dental spending showed resilience, with January figures 4% higher than the previous year, highlighting steady demand for routine and elective care. The U.S. dental care market is expanding due to improved insurance access. In 2025, 97% of Medicare Advantage plans included dental benefits, and more states extended adult Medicaid dental coverage.[2]Centers for Medicare & Medicaid Services, “Medicare Advantage and Medicare Prescription Drug Programs to Remain Stable as CMS Implements Improvements to the Programs in 2025,” CMS Fact Sheet, cms.gov These changes are driving more seniors and lower-income adults into formal care. Digital tools like scanners and AI-supported diagnostics are enabling providers to perform higher-value procedures more consistently.

Key Report Takeaways

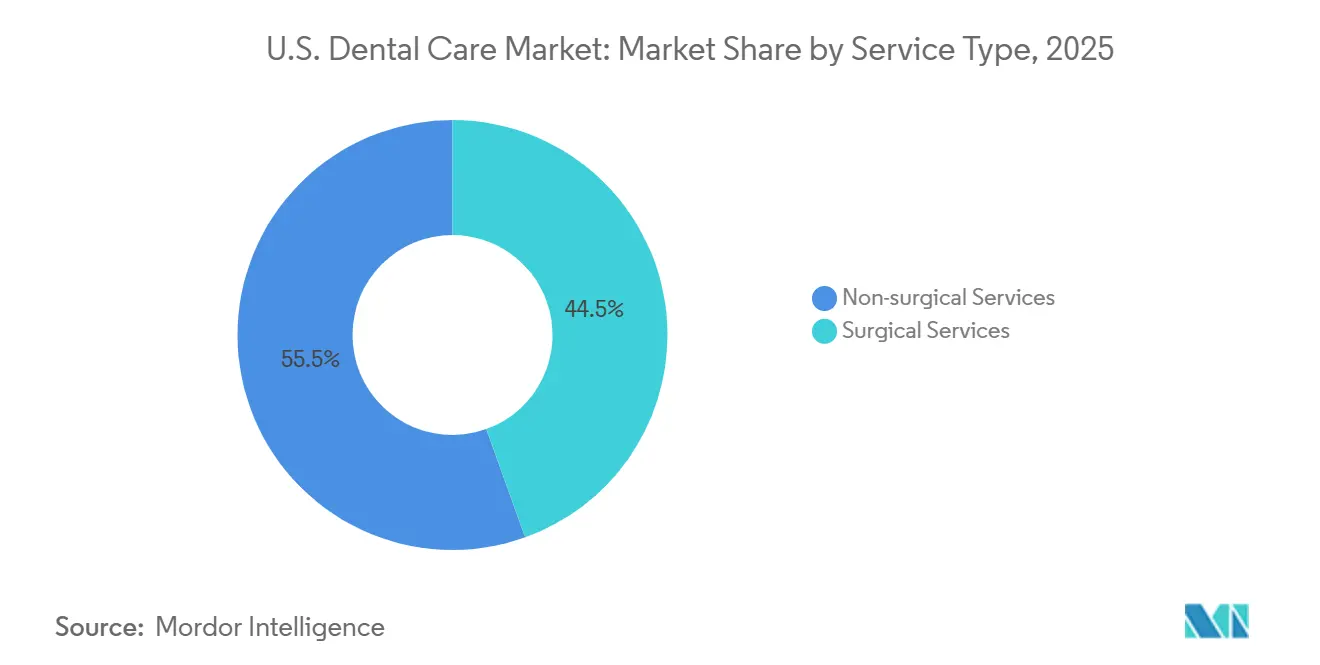

- By service type, non-surgical services held 55.46% revenue share in 2025, while surgical services are projected to expand at 6.15% CAGR through 2026-2031.

- By patient age group, adults aged 35-64 accounted for 52.53% of patient volume in 2025, while the 65-years-and-above cohort is projected to grow at 6.35% CAGR through 2026-2031.

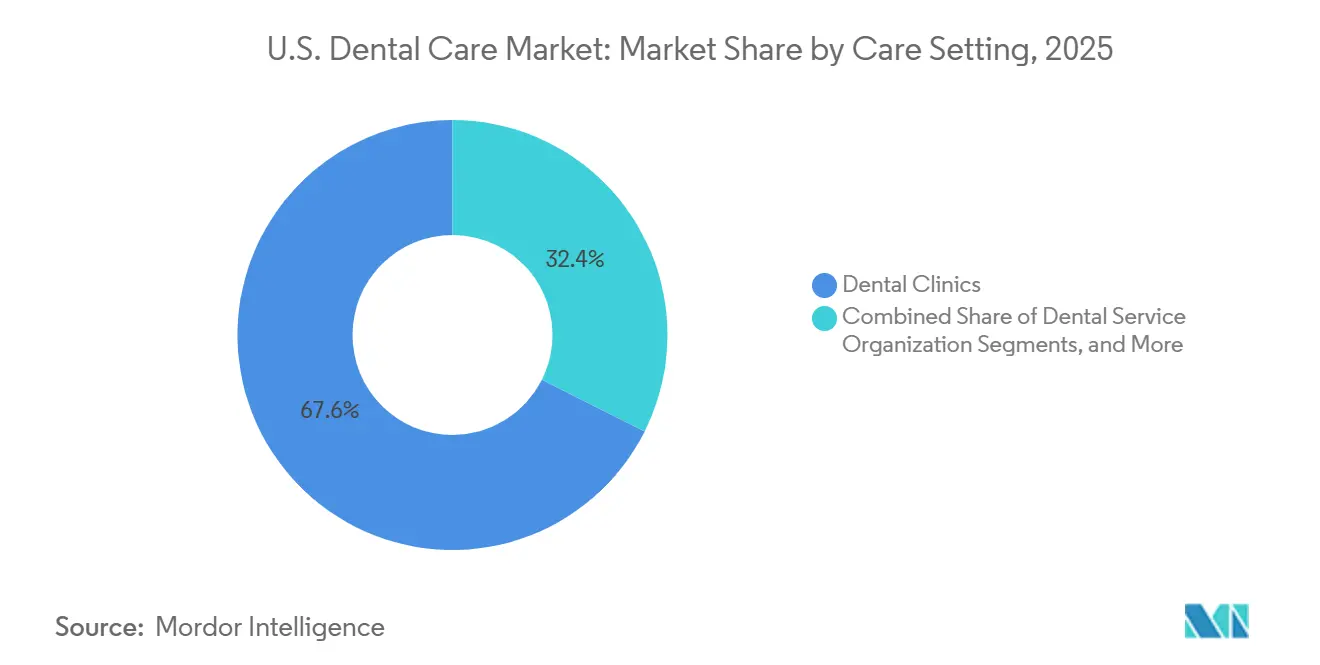

- By care setting, dental clinics captured 67.60% of revenue in 2025, while dental service organizations are expected to grow at 6.45% CAGR through 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Dental Care Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Medicare advantage dental benefit expansion | +0.8% | National, with concentrated gains in Florida, Arizona, California, and Texas where Medicare Advantage enrollment is highest | Medium term (2-4 years) |

| Adult medicaid dental benefit expansion and regulatory tailwinds | +0.7% | State specific but broadening nationally, with highest impact in Georgia, Indiana, Kansas, Kentucky, Utah, South Carolina, and Oklahoma | Medium term (2-4 years) |

| DSO consolidation and specialty rollout | +0.9% | National, with the strongest activity in California, Florida, New York, Pennsylvania, and Texas | Short term (≤ 2 years), Medium term (2-4 years) |

| Cosmetic, clear-aligner, and implant demand | +1.0% | National, with the strongest discretionary spend in urban and suburban markets in the Northeast and on the West Coast | Short term (≤ 2 years) |

| Ai diagnostics and dental-medical integration | +0.6% | National, with earlier adoption in larger DSO-operated networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Medicare Advantage Dental Benefit Expansion Fueling Senior Utilization

In 2025, Medicare Advantage enrollment reached 34.1 million, representing 54% of the eligible Medicare population, a 4% increase from the previous year. Projections indicate this share could grow to 64% by 2034, signaling continued expansion of senior dental coverage. Over 97% of Medicare Advantage plans included dental benefits in 2025, with supplemental dental benefits also widely available.[3]Centers for Medicare & Medicaid Services, “Medicare Advantage and Medicare Prescription Drug Programs to Remain Stable as CMS Implements Improvements to the Programs in 2025,” CMS Fact Sheet, cms.gov Special Needs Plans saw a 71% enrollment increase, driving demand for restorative, periodontal, and specialty procedures, resulting in higher revenue per senior patient.

Adult Medicaid Dental Benefit Expansion Broadening the Addressable Population

By the end of 2024, 11 states and Washington, D.C., offered extensive adult dental benefits under Medicaid, up from 4 states in 2020. Recent changes expanded service coverage, raised annual benefit limits, and targeted specific adult groups. This broadened the patient base, enabling more low-income adults to access dental care. Larger groups and DSO-backed practices are better positioned to manage lower reimbursements and higher volumes, making them key beneficiaries of this expansion.

DSO Consolidation And Specialty Rollout

DSO consolidation is transforming the U.S. dental market by centralizing revenue, referrals, and purchasing power. Dental service organizations are gaining share in complex procedures through efficient operations across multi-site networks. This model supports the rollout of specialty services like oral surgery and orthodontics, retaining more patient value within networks. DSOs are also better equipped to absorb Medicaid and Medicare Advantage growth, reshaping practice evaluations and private capital focus.

Cosmetic, Clear-Aligner, And Implant Demand Elevating Revenue Per Visit

Cosmetic dentistry has become a consistent revenue driver in the U.S. market. In 2024, adults accounted for 70% of clear-aligner starts, reflecting a shift in orthodontic demand. By 2026, 17% of U.S. adults had undergone cosmetic procedures, with whitening and clear-aligners leading. Intraoral scanners, used by 53% of dentists in 2024, enable same-day crowns and fewer visits. Products like LuxCreo's 4D Bright Aligner, launched in 2025, combine clinical correction with cosmetic whitening, boosting revenue per visit across premium services.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Hygienist and assistant shortages | -0.5% | National, most acute in rural areas and dental HPSAs, with heavier pressure across Southeast and South-Central states | Short term (≤ 2 years), Medium term (2-4 years) |

| Out-of-pocket burden and annual benefit caps | -0.4% | National, most pronounced in lower-income and uninsured populations, and stronger in states with limited Medicaid coverage | Medium term (2-4 years) |

| Low medicaid reimbursement and administrative burden | -0.3% | State specific, most acute where reimbursement remains far below dentist charges | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hygienist And Assistant Shortages Constraining Capacity At A Critical Growth Inflection

The U.S. dental care market faces capacity constraints as shortages of hygienists and assistants limit the conversion of insured demand into appointments. In 2025, 74% of dentists reported extreme difficulty in recruiting hygienists, with 57.2% of positions unfilled. A projected shortfall of 30,000 hygienists by 2037, driven by limited clinic space in training programs, further exacerbates the issue. These shortages have reduced practice capacity by 11%, increasing wait times, lowering visit throughput, and causing delays in treatment. Retention challenges, influenced by pay, workload, and scope-of-practice limits, remain a critical barrier to resolving this issue.

Out-Of-Pocket Burden And Annual Benefit Caps Suppressing Discretionary Demand

High out-of-pocket costs continue to suppress treatment completion in the U.S. dental care market, particularly for expensive procedures like crowns and implants. Many annual dental benefit caps remain near USD 1,000, with 32.8% of in-network maximums between USD 1,000 and USD 1,500, and 48.2% between USD 1,500 and USD 2,500. Once patients reach these caps, 39% delay care until benefits renew, while another 39% pay out of pocket. This dynamic reduces demand for high-revenue discretionary and restorative procedures, despite clear treatment needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Surgical Procedures Gaining Ground On A Large Non-Surgical Base

In 2025, non-surgical services accounted for 55.46% of the U.S. dental care market share, driven by preventive care such as cleanings and exams, which are repeatable across all age groups. Employer-sponsored dental insurance supports this category by offering broad reimbursements for preventive and restorative procedures, stabilizing routine utilization. Restorative services like fillings, crowns, and bridges, along with cosmetic dentistry options such as whitening and veneers, further enhance demand and revenue potential.

Surgical services are projected to grow at a 6.15% CAGR from 2026 to 2031, the fastest among service types. Implant adoption is a key driver, addressing both aging patients' tooth replacement needs and younger adults' demand for appearance-driven treatments. Orthodontics is expanding beyond adolescents to working adults, while advancements in endodontics and periodontics are increasing billable interventions, shifting the market toward higher-revenue specialty procedures.

By Patient Age Group: Middle-Aged Adults Hold Volume While Seniors Lead Growth

In 2025, adults aged 35-64 represented 52.53% of patient volume, driven by disposable income, employer-sponsored coverage, and demand for restorative and cosmetic procedures. The 35-54 age group is particularly valuable due to their willingness to combine elective upgrades with necessary treatments. Younger adults (18-34) focus more on preventive care but remain price-sensitive, with 32.2% not seeking dental care in the past year due to unaffordable copayments.

The 65-and-above age group is forecast to grow at a 6.35% CAGR from 2026 to 2031, supported by demographic aging and expanded Medicare Advantage dental coverage. However, 47% of adults aged 65-80 lacked dental insurance in 2025, limiting full market potential. Seniors often require complex restorative work, generating higher revenue per visit. Pediatric care remains stable, supported by programs like CHIP, though it has not fully recovered to pre-pandemic levels.

By Care Setting: Traditional Clinics Still Lead While DSOs Expand Faster

In 2025, dental clinics accounted for 67.60% of the U.S. dental care market, reflecting their role as the primary care point for routine preventive and restorative services. Hospital-based dentistry serves a smaller niche for patients with complex medical needs, while community health centers and mobile units are expanding access in underserved areas, shaping referral flows and market reach.

Dental service organizations (DSOs) are projected to grow at a 6.45% CAGR from 2026 to 2031, driven by centralized operations, broader specialist networks, and higher Medicaid participation. Their multi-state scale enables faster deployment of AI platforms and compliance systems, positioning DSOs as key players in the next growth phase, emphasizing scale and specialty access.

Geography Analysis

Regional performance in the U.S. dental care market is influenced by provider access, income distribution, insurance design, and local demographics rather than formal price regulations. A January 2025 study revealed that 24.7 million Americans live in areas with dental care shortages, highlighting the uneven distribution of services. Rural areas have one dentist per 3,850 residents compared to one per 1,470 in urban areas, creating significant access challenges. These gaps often delay preventive care, leading to more severe cases and impacting visit volumes, staffing, payer mix, and procedure complexity for operators.

The Northeast remains the region with the best access, with states like Connecticut, Delaware, Indiana, New Jersey, and Washington, D.C., identified as having no dental deserts. High provider density ensures smoother appointment availability, better preventive care adherence, and increased demand for elective cosmetic procedures. These factors support premium practice economics, as privately insured patients are more likely to pursue high-value treatments. The region’s dense population and established practice infrastructure have also driven active DSO expansions, making it more resilient compared to regions with workforce shortages.

The West and Southwest attract growth due to large populations, significant senior demographics, and high Medicare Advantage enrollments in states like California, Texas, Arizona, Nevada, and Florida. Florida and Arizona see strong demand for implants, restorative services, and periodontics due to aging populations. California and Texas remain key markets for DSO expansion, supported by large patient pools and scalable multi-site operations. The U.S. dental care market reflects a mixed landscape, with some regions constrained by access issues while others benefit from population growth, senior care needs, and consolidation.

Competitive Landscape

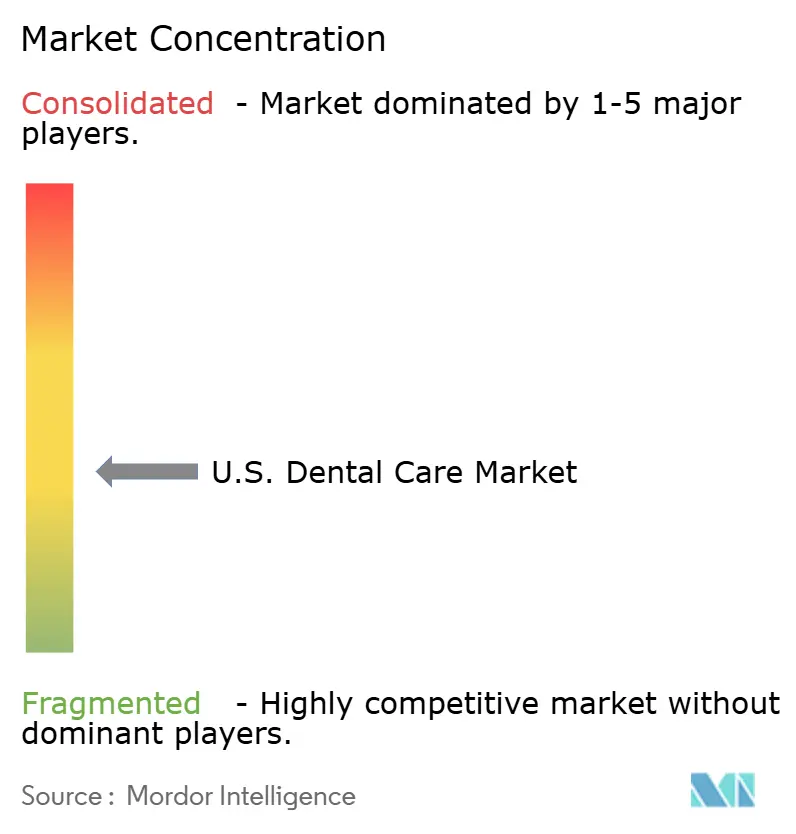

The U.S. dental care market remains moderately fragmented, with independent practices dominating most locations, even as larger groups gain revenue share in complex procedures. Heartland Dental, PDS Health, and The Aspen Group collectively support over 4,000 practices nationwide, positioning them as leading scaled operators. Their scale provides advantages such as better purchasing power, broader technology adoption, enhanced recruiting, and stronger payer negotiations. However, local practices continue to dominate preventive and restorative care, keeping the market open to acquisitions, affiliations, and selective specialty expansions.

Leading companies are leveraging strategic moves to strengthen their positions. Heartland Dental acquired Dentalogy in February 2026, marking its third transaction of the year and adding to a streak of 30 deals since early 2025. The Aspen Group deployed VideaHealth's Clinical Assist AI platform across 1,100+ Aspen Dental practices in early 2026 to standardize diagnoses and reduce missed pathologies. PDS Health expanded its collaboration with Pearl and announced plans to open over 100 new dental locations in 2026, signaling a shift from acquisitions to organic growth. Competitive advantage now hinges on M&A, AI integration, specialty depth, and network density.

Opportunities lie in Medicaid-accepting specialty practices, geriatric services, and integrated care models linking oral health with chronic disease management. Specialized Dental Partners and MAX Surgical Specialty Management are addressing premium implant and oral surgery demands, areas underutilized by general dentistry groups. Smaller operators can compete through strong referral networks, local brand trust, and consistent staffing but face challenges in capital access and digital capabilities. While ownership fragmentation persists, the market is becoming more concentrated in technology, specialty access, and payer-facing scale.

U.S. Dental Care Industry Leaders

Heartland Dental

Lightwave Dental Management LLC

Mortenson Dental Partners

North American Dental Group

Smile Doctors

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Heartland Dental completed its third transaction of 2026 by acquiring Dentalogy, marking its 30th acquisition since 2025. The DSO now supports over 3,000 doctors across 1,800+ locations in 39 states, aiming to reach 2,000 locations through organic and inorganic growth this fiscal year.

- January 2026: The Aspen Group deployed VideaHealth's Clinical Assist AI platform across 1,100+ Aspen Dental practices. This initiative enhances diagnostic consistency and reduces missed-pathology rates across its network.

- January 2026: PDS Health partnered with Pearl to expand AI-assisted diagnostics across its network and announced plans to open over 100 new dental locations in 2026, signaling a shift toward organic growth amid rising acquisition costs.

- September 2025: Heartland Dental acquired Smile Design Dentistry, adding 60 Florida-based practices to its network. This expanded its presence to over 1,880 practices across 39 states and the District of Columbia, strengthening its position in a key DSO market.

U.S. Dental Care Market Report Scope

As per the scope of the report, dental care is defined as the maintenance of healthy teeth, gums, and oral structures through the prevention, diagnosis, and treatment of oral diseases. It is a critical component of overall medicine that combines daily personal oral hygiene with professional clinical dentistry. Dental care services encompass professional, diagnostic, preventive, maintenance, and therapeutic treatments focused on the oral cavity, specifically the teeth, gums, and tongue.

The U.S. dental care market is segmented by service type, patient age group, and care setting. By service type, the market includes non-surgical services (preventive dentistry, restorative dentistry, and cosmetic dentistry) and surgical services (implants & oral surgery, orthodontics, and endodontics & periodontics). By patient age group, the market is categorized into 0-17 years, 18-34 years, 35-64 years, and 65 years and above. By care setting, the market is segmented into dental clinics, hospitals, dental service organizations, and others. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Non-surgical Services | Preventive Dentistry |

| Restorative Dentistry | |

| Cosmetic Dentistry | |

| Surgical Services | Implants & Oral Surgery |

| Orthodontics | |

| Endodontics & Periodontics |

| 0-17 years |

| 18-34 years |

| 35-64 years |

| 65 years and above |

| Dental Clinics |

| Hospital |

| Dental Service Organization |

| Others |

| By Service Type | Non-surgical Services | Preventive Dentistry |

| Restorative Dentistry | ||

| Cosmetic Dentistry | ||

| Surgical Services | Implants & Oral Surgery | |

| Orthodontics | ||

| Endodontics & Periodontics | ||

| By Patient Age Group | 0-17 years | |

| 18-34 years | ||

| 35-64 years | ||

| 65 years and above | ||

| By Care Setting | Dental Clinics | |

| Hospital | ||

| Dental Service Organization | ||

| Others | ||

Key Questions Answered in the Report

What is driving U.S. dental care demand through 2031?

The main demand drivers are broader insurance access, especially through Medicare Advantage and state Medicaid expansion, along with stronger uptake of implants, aligners, and other higher-value procedures. The U.S. dental care market is projected to rise from USD 224.56 billion in 2026 to USD 279.18 billion by 2031 at a 4.45% CAGR.

Which service area is growing the fastest in dental care?

Surgical services are the fastest-growing service segment, with a 6.15% CAGR through 2026-2031. Implant demand, adult orthodontics, endodontics, and periodontics are the main reasons this part of care is expanding faster than non-surgical treatment.

Why are seniors becoming more important for providers?

Patients aged 65 years and above are the fastest-growing age group, with a 6.35% CAGR through 2026-2031. Wider Medicare Advantage dental coverage and rising restorative need are increasing their importance for revenue growth.

How important are DSOs in the current competitive shift?

DSOs are the fastest-growing care setting, with a 6.45% CAGR through 2026-2031. Their scale helps them manage staffing, technology rollout, Medicaid participation, and specialty referrals more efficiently than many independent practices.

What is holding back treatment growth despite higher coverage?

Staffing shortages, annual benefit caps, and low Medicaid reimbursement remain the main barriers. These factors limit appointment capacity, raise patient out-of-pocket costs, and reduce provider willingness to accept lower-paying public plans.

Which U.S. regions face the biggest access challenges?

Rural areas remain the most constrained, with 1 dentist per 3,850 people versus 1 per 1,470 in urban areas. The Northeast has stronger provider density, while the West and Southwest are drawing growth interest because of large populations, older residents, and active DSO expansion.

Page last updated on: