United States Dental Elevator and Luxator Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

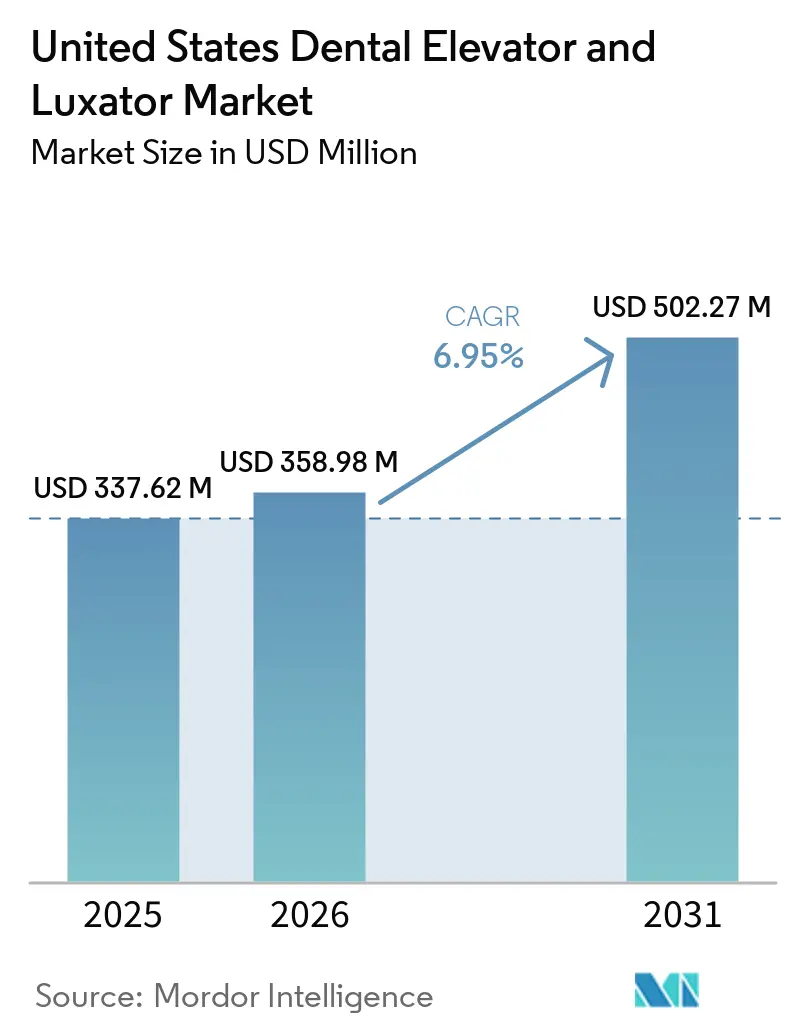

| Base Year Market Size (2025) | USD 337.62 Million |

| Market Size (2026) | USD 358.98 Million |

| Market Size (2031) | USD 502.27 Million |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dental Elevator and Luxator Market Analysis by Mordor Intelligence

The United States Dental Elevator And Luxator Market size is expected to increase from USD 337.62 million in 2025 to USD 358.98 million in 2026 and reach USD 502.27 million by 2031, growing at a CAGR of 6.95% over 2026-2031.

The United States dental elevator and luxator market is being supported by a structurally older patient base, and the United States had 61.2 million people aged 65 and older in 2024, equal to 18% of the population, with this cohort growing 3.1% from 2023 to 2024. The United States dental elevator and luxator market also benefits from the spread of group practice and outpatient dental networks, because DSO-affiliated dentists reached 16.1% of all U.S. dentists in 2024, and group settings now account for a large share of practice organization. Procedure demand remains firm because national dental expenditures reached USD 189 billion in 2024, and consumer dental spending is rising 4% year on year through January 2026, which keeps the United States dental elevator and luxator market tied to active clinical volumes rather than purely discretionary purchases. The United States dental elevator and luxator market is also being reshaped by immediate implant protocols, because minimally invasive extraction guidance increasingly favors socket-preserving instruments that protect bone volume before implant placement. A near-term limit remains input cost pressure, as tariff uncertainty and imported instrument inflation were identified as important concerns in late 2025, which may tighten margins and speed up consolidation among mid-tier suppliers serving the United States dental elevator and luxator market.

Key Report Takeaways

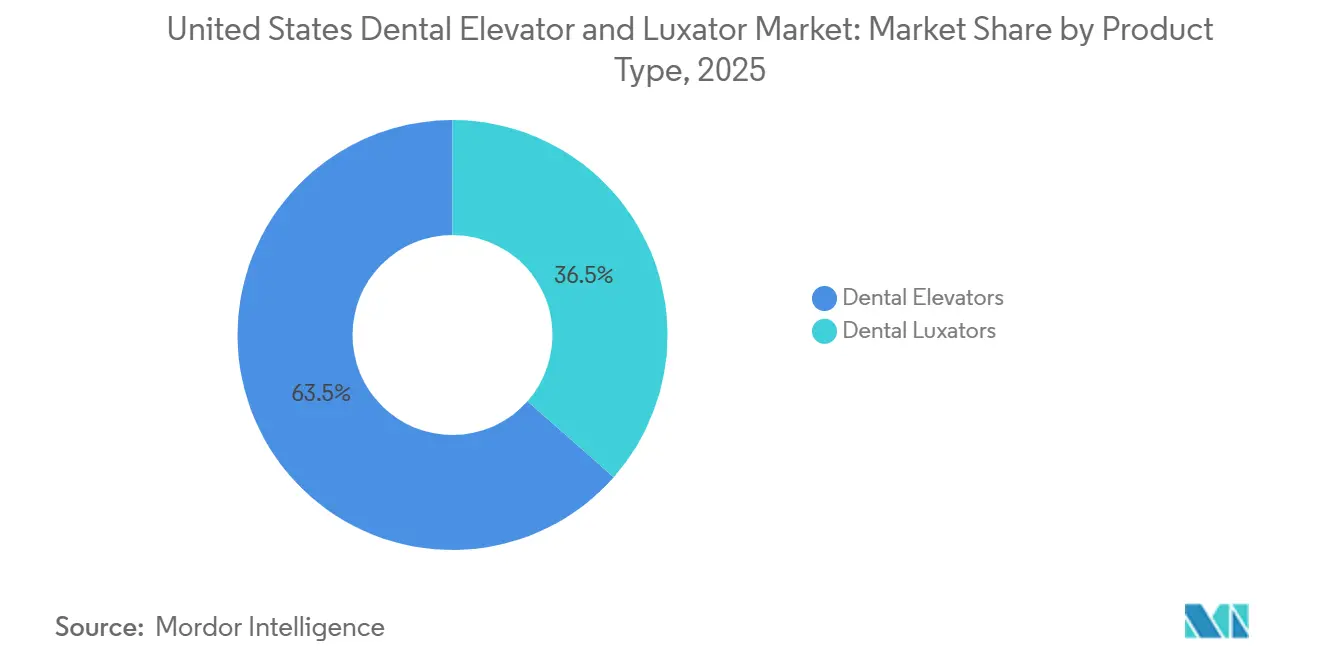

- By product type, dental elevators led with 63.48% revenue share in the United States dental elevator and luxator market in 2025, while dental luxators are forecast to expand at 7.36% CAGR through 2031.

- By size, 5 mm instruments accounted for 29.42% of 2025 value in the United States dental elevator and luxator market, while the 10 mm segment is projected to grow at 8.87% CAGR through 2031.

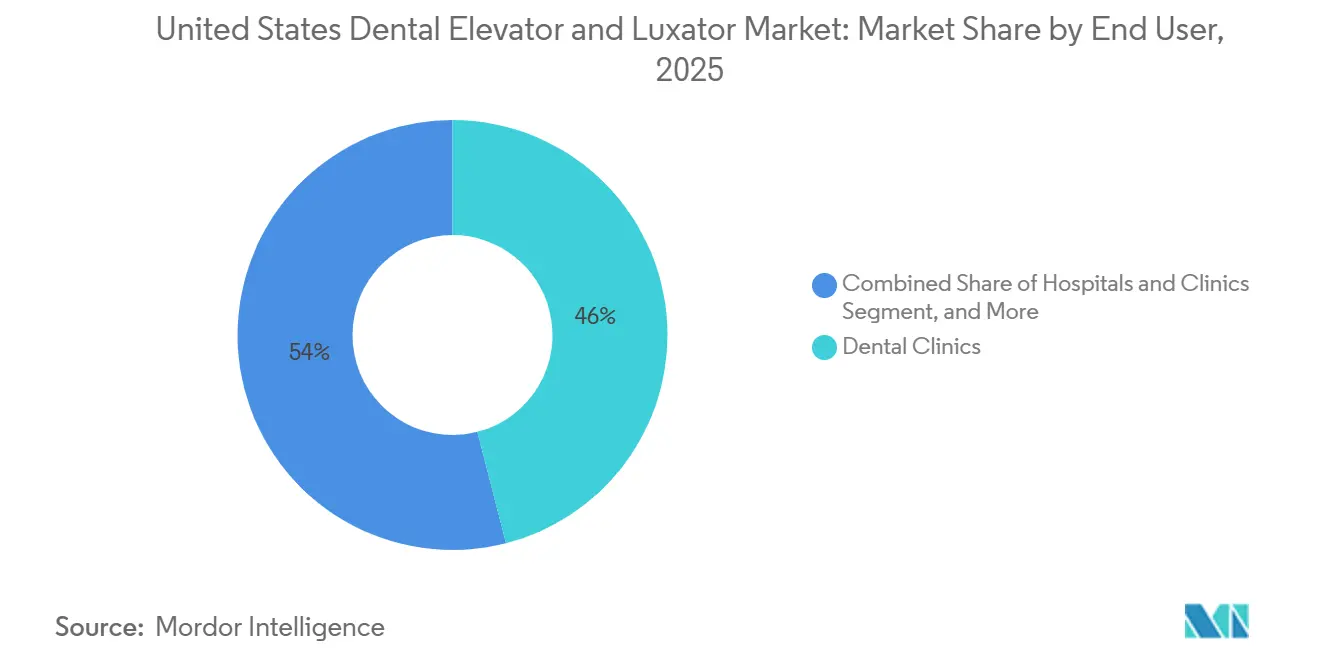

- By end user, dental clinics held 46.03% of the market in 2025, while hospitals and clinics are projected to advance at 7.97% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Dental Elevator and Luxator Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Geriatric Dental Extractions | +1.8% | National, with outsized concentration in Sun Belt states and the Northeast | Short term (≤ 2 years) |

| Expansion of Outpatient Dental Care Networks | +1.4% | National, with early gains in DSO-dense corridors in the Southeast, Midwest, and Southwest | Short term (≤ 2 years) |

| High Burden of Periodontal Disease and Tooth Loss | +1.2% | National, with elevated prevalence among lower-income, Hispanic, and Black adult populations in urban centers | Medium term (2-4 years) |

| Shift Toward Minimally Traumatic Extraction Techniques | +1.1% | National, with earlier adoption in academic dental centers and specialist group practices | Medium term (2-4 years) |

| Ergonomic Tool Design and Material Innovation | +0.7% | National, with concentration in high-volume DSO-managed practices and specialty oral-surgery clinics | Long term (≥ 4 years) |

| Sterile, Single-Use, and Clinic-Specific Instrument Bundling | +0.6% | National, with spillover to ambulatory surgical center settings in states with expanded Medicaid dental access | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Geriatric Dental Extractions: Aging Demographics Structurally Underpin Instrument Demand

The United States dental elevator and luxator market is closely linked to the fast rise in older adults across the country. The U.S. population aged 65 and older reached 61.2 million in 2024 and accounted for 18% of the total population, with annual growth of 3.1% from 2023 to 2024.[1]United States Census Bureau, “Older Adults Outnumber Children in 11 States, Nearly Half of Counties,” U.S. Census Bureau, census.gov Older adults carry heavier tooth loss burdens, and NIDCR reports that people aged 65 and older had 20.7 remaining teeth on average, while 17.3% were fully edentulous. Even among seniors who still retain teeth, the average of 10.7 missing teeth points to a continuing flow of difficult extractions that often involve roots, brittle bone, and periodontally compromised sites. This keeps demand in the United States dental elevator and luxator market tied to necessary procedures rather than optional spending. The long runway also matters because a 2025 article in Frontiers in Dental Medicine projects the U.S. population aged 65 and older to reach 98 million by 2060, which supports sustained extraction-related instrument demand well beyond the current forecast period.

Expansion of Outpatient Dental Care Networks: DSO Scale Generates Standardized Procurement Demand

The United States dental elevator and luxator market is also gaining from the growth of larger outpatient care networks. DSO-affiliated dentists represented 16.1% of all U.S. dentists in 2024, more than double the 7.4% recorded in 2015, and group practice participation has continued to rise.[2]American Dental Association Health Policy Institute, “The Dental Care Market,” American Dental Association, ada.org As DSOs expand, purchasing decisions move away from single-clinician choice and toward approved supplier lists, which creates repeatable order flows for oral-surgery hand instruments. Coverage expansion is widening the treatable patient base, because CMS finalized in 2024 that states may add routine adult dental services as an essential health benefit starting in January 2027. A December 2025 Medicaid dental benefits report showed that 38 states and the District of Columbia offered enhanced adult dental benefits in 2025, and 18 states had expanded adult dental benefits since 2021 without any state rolling back benefits. As outpatient care networks scale against this coverage backdrop, the United States dental elevator and luxator market is likely to see fewer minor brands on formularies and greater concentration in approved vendor lists that can support quality and volume at the same time.

High Burden of Periodontal Disease and Tooth Loss: Disease Prevalence Generates Recurring Procedure Volume

The United States dental elevator and luxator market draws steady support from the high national burden of periodontal disease. The latest nationally maintained prevalence figures show that 42.2% of U.S. adults aged 30 and older had periodontitis, while 59.8% of adults aged 65 and older were affected. Severe periodontitis affected 7.8% of adults aged 30 and older, and rates were much higher among smokers, adults with diabetes, and people below the federal poverty line. Periodontally compromised teeth often require slower socket dilation and controlled ligament separation, which favors elevators and luxators over a forceps-only approach when bone preservation matters. National dental expenditures reached USD 189 billion in 2024, which shows that disease burden is converting into active treatment rather than remaining only a latent care need. The United States dental elevator and luxator market also benefits when medical teams request dental clearance before dialysis or cardiovascular procedures, because patients with poor dentition often need extractions before broader treatment plans move ahead.

Shift Toward Minimally Traumatic Extraction Techniques: Socket Preservation Science Differentiates Luxators from Forceps

The United States dental elevator and luxator market is being shaped by the wider use of minimally traumatic extraction protocols. A 2024 expert consensus published in the Journal of Southern Medical University formalized indications, technique steps, and post-operative management for minimally invasive tooth extraction and placed periodontal ligament instruments among the preferred first-line tools. A 2025 comparative study in the Journal of Clinical Periodontology and Dental Research reported favorable biomechanical and clinical support for torsion-and-swing extraction methods over conventional socket expansion methods.[3]Journal of Clinical Periodontology and Dental Research, “Comparison of Biomechanics and Clinical Validation of Torsion and Swing Tooth Extraction Methods,” Journal of Clinical Periodontology and Dental Research, jocpd.com These findings matter because luxators cut the periodontal ligament with controlled rotational force and support cleaner socket preservation for immediate implant planning. That shifts purchasing logic away from simple extraction ease and toward downstream implant outcomes, which strengthens the premium tier in the United States dental elevator and luxator market. Piezosurgery studies also support this direction, yet they still position mechanical hand instruments as complementary rather than obsolete in mixed workflows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inconsistent Reimbursement for Routine Extraction Instruments | -0.8% | National, more acute in states with limited Medicaid dental benefits and rural areas with low private insurance penetration | Medium term (2-4 years) |

| Price Pressure From Standardized Low-Cost Imports | -0.7% | National, most acute in entry-level product tiers and among cost-sensitive independent dental practices | Short term (≤ 2 years) |

| Clinical Preference for Multi-Use Alternatives and Conventional Forceps | -0.5% | National, with greater resistance in rural and community health settings with limited training exposure | Medium term (2-4 years) |

| Limited Procedure Differentiation in a Mature Hand Instrument Category | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inconsistent Reimbursement for Routine Extraction Instruments: Coverage Gaps Constrain Facility Budgets

The United States dental elevator and luxator market still faces a reimbursement problem because procedure payment does not directly translate into instrument-specific recovery. CareQuest reported in 2025 that 26% of U.S. adults, equal to 69 million people, lacked dental coverage, which leaves many providers operating in unstable demand environments. Safety-net clinics and FQHCs usually manage budgets around reimbursable procedures, staffing, and essential consumables, so hand instruments compete for funds with more immediate operating needs. CMS policy changes improve the long-term coverage environment, but they do not reimburse the purchase of specific elevators or luxators as separate billable items. This creates uneven replacement cycles across states, because better-covered markets can refresh trays more regularly while low-coverage markets stretch instrument life. The result is slower premium adoption in the parts of the United States dental elevator and luxator market that are most budget-sensitive.

Price Pressure From Standardized Low-Cost Imports: Commodity Tier Erodes Pricing Power for Premium Manufacturers

The United States dental elevator and luxator market also faces persistent price pressure from imported standard-specification products. The ADA Health Policy Institute flagged tariff uncertainty and rising import costs as major concerns in its Q4 2025 dental economy survey, which showed that overhead pressure was influencing how practices viewed future expenses. At the same time, standardized elevator sets sourced from South and East Asia have appeared in catalogs at prices 25% to 40% below domestic-brand equivalents, which narrows the room for premium pricing in routine applications. Independent clinics and academic programs are especially exposed because they often weigh budget consistency more heavily than marginal ergonomic gains. This does not remove demand from the United States dental elevator and luxator market, but it does shift more volume toward the entry tier and forces premium manufacturers to justify price with durability, feel, and clinical handling. Margin compression is therefore likely to remain strongest where product substitution is easiest.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Dental Luxators Gaining Share as Implant-Preparatory Extraction Protocols Standardize

Dental elevators held 63.48% of the United States dental elevator and luxator market share in 2025, which reflected their long-standing role in routine extraction workflows across U.S. practices. Their wide use across incisor, premolar, and molar procedures keeps them as the default choice in many general dentistry and oral-surgery trays. Straight, cryer, and apical designs remain familiar to clinicians because they are deeply embedded in training, case setup, and basic inventory planning. This entrenched position gives elevators a stable demand base inside the United States dental elevator and luxator market, even as procedural techniques continue to evolve.

Dental luxators are forecast to grow at 7.36% CAGR through 2031, which is faster than the 7% overall pace of the United States dental elevator and luxator market. Their stronger growth reflects the fact that luxators sit closer to atraumatic extraction and implant-preparatory workflows, where bone preservation has direct financial and clinical value. The 2024 expert consensus on minimally invasive extraction specifically supported periodontal ligament instruments as first-line tools, which gives suppliers a clearer clinical basis for tray inclusion and premium positioning. This shift also improves product mix for manufacturers, because luxators, especially ergonomic and premium-finish variants, usually sell at higher average prices than standard elevators.

By Size: The 5 mm Segment Anchors Volume While 10 mm Growth Signals Rising Surgical Complexity

The 5 mm segment accounted for 29.42% of the United States dental elevator and luxator market size in 2025, which made it the leading size configuration. Its lead came from broad case versatility, because it fits a wide range of anterior and bicuspid extractions and supports routine tray standardization. Practices that want simple sterilization and restocking workflows often center routine case coverage around 3 mm to 5 mm sets, with 5 mm holding the broadest utility. The 2 mm, 3 mm, and 4 mm variants still remain important for narrow roots, pediatric cases, and intermediate anatomy, but they serve more selective procedural needs.

The 10 mm segment is projected to grow at 8.87% CAGR through 2031, which signals rising procedure intensity at the more difficult end of the case mix. Wider and longer working ends are relevant in third-molar impactions, multi-rooted molar extractions, and cases where stronger purchase and leverage are needed. Evidence on piezosurgery in third-molar work still supports a mixed-technique approach, where hand instruments continue to play a core role before or alongside osteotomy steps. That means the growth of larger-format instruments is less about replacing standard sizes and more about added demand from complex extractions that require higher mechanical control in the United States dental elevator and luxator market.

By End User: Dental Clinics Lead but Hospital-Setting Growth Reflects Systemic Integration

Dental clinics represented 46.03% of the United States dental elevator and luxator market size in 2025, which kept them as the largest end-user setting. This position reflects their role as the main site for routine and moderately complex extractions across independent practices, DSO-managed clinics, and community health centers. Their procedure base supports steady turnover for reusable hand instruments even when premium adoption differs by budget and case mix. Research and academic institutes remain a smaller but steady part of the United States dental elevator and luxator market because teaching needs and protocol development keep them active buyers.

Hospitals and clinics are projected to expand at 7.97% CAGR through 2031, which makes them the fastest-growing end-user group. This trend aligns with wider hospital outpatient dental access and more facility-based care for complex, medically managed, and pediatric cases. The American Academy of Pediatric Dentistry has continued to track state-level facility fee implementation for dental rehabilitation in operating rooms, and that supports restocking of surgical dental trays in outpatient and ambulatory settings. University of the Pacific’s Dugoni School also received approval for a USD 22 million ambulatory surgical center investment that is expected to lift patient volumes above 8,000 visits, which shows how hospital-linked capacity additions can translate into centralized procurement demand.

Geography Analysis

The United States dental elevator and luxator market is a single-country market in scope, but demand still varies meaningfully across the United States. Sun Belt states such as Florida, Texas, Arizona, and California carry some of the largest senior populations, which gives them the highest density of age-linked extraction demand. Florida has maintained a senior share above 21% in recent years, which helps explain its outsized role in procedure-heavy dental care. Consumer dental spending is also rising unevenly across regions, and the ADA Health Policy Institute confirmed 4% year-on-year growth through January 2026, with stronger activity in markets that combine better coverage, denser provider networks, and greater DSO presence.

Rural and underserved states remain the weakest demand pockets for premium products in the United States dental elevator and luxator market. CareQuest reported in 2025 that 69 million adults had no dental coverage, with the burden falling heavily on lower-income and underserved populations. FQHCs and community clinics in these regions usually favor durable reusable sets over premium single-use or titanium-enhanced variants because purchasing budgets are tightly managed. At the same time, the policy backdrop is improving, because 38 states and the District of Columbia offered enhanced adult Medicaid dental benefits in 2025 and 7 states expanded those benefits in 2025 alone. California adds another important example, as the California Health Facilities Financing Authority awarded USD 47.2 million for specialty dental clinic projects in 2025, which is expected to support 124 new or expanded operatories and surgery suites across 10 counties.

The Northeast corridor and West Coast metros remain early-adoption hubs for minimally traumatic extraction protocols in the United States dental elevator and luxator market. Their advantage comes from strong specialist density and the influence of major academic dental centers such as Harvard, Penn, UCSF, and Columbia, where luxator-first workflows are more likely to shape training norms. This training effect spreads outward over a 3-year to 5-year cycle as graduates move into private group practice and DSO settings. That diffusion pattern matters because premium vendors serving academic centers today may be shaping the approved formularies of tomorrow in nearby commercial markets.

Competitive Landscape

The United States dental elevator and luxator market is moderately fragmented, with specialized instrument makers competing alongside large national distributors. HuFriedyGroup and Medesy are well-positioned in the premium tier, while Titan Instruments and Nordent Manufacturing compete on domestic production credentials, customization, and oral-surgery set relevance. Henry Schein and Patterson Companies play an important amplification role because they move products through catalog, GPO, and DSO contract channels rather than relying only on direct manufacturer sales. This structure keeps the United States dental elevator and luxator market active, but it limits product-specific pricing battles because many suppliers sell elevators and luxators as one part of a broader hand-instrument portfolio.

A major opening in the United States dental elevator and luxator market lies in clinic-specific bundled extraction kits. Procedure-coded sterile sets for single-rooted anterior cases, multi-rooted molars, or third molars can reduce room setup time and fit the operating model of larger group practices. Materials science is also becoming a clearer differentiator, with titanium-alloy handles, harder blade coatings, and surface treatments being used to support grip, wear resistance, and procedural control. Young Innovations’ XP²-related surface treatment direction shows how adjacent hand-instrument categories are already normalizing premium performance claims in U.S. dentistry. Patent attention around handle design and working-end geometry suggests that product development is moving toward better-supported premium SKUs rather than digital disruption. Even so, no supplier has clearly locked in the assembled-kit niche for elevators and luxators, which leaves room for a specialist bundler or a scaled distributor to capture extra margin through curation.

Strategic moves in 2026 show that leading companies are widening influence around the United States dental elevator and luxator market rather than relying on this category alone. HuFriedyGroup introduced PWR Air at the Chicago Midwinter Meeting in February 2026, which reinforced its innovation profile and strengthened cross-category relationships with the same customers who buy oral-surgery instruments. In April 2026, HuFriedyGroup also announced a partnership with Seattle Study Club, which should strengthen education-linked prescribing behavior and brand visibility in procedure-driven settings. Dentsply Sirona and Siemens Healthineers received FDA clearance in March 2026 for the first dental-dedicated MRI system, which points to a dental care environment that is becoming more clinically sophisticated and more supportive of premium procedural tool adoption across adjacent categories.

United States Dental Elevator and Luxator Industry Leaders

3M

Dentsply Sirona Inc.

PLANMECA OY

Straumann Group

Zimmer Biomet Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: HuFriedyGroup and Seattle Study Club Strategic Partnership. HuFriedyGroup announced a strategic partnership with the Seattle Study Club, one of the world's most respected dental education networks, to integrate clinical instrument education with advanced curriculum delivery. The partnership positions HuFriedyGroup instruments within structured continuing education frameworks, directly influencing prescriptive behavior in surgical instrument categories including oral-surgery hand instruments.

- March 2026: Dentsply Sirona and Siemens Healthineers Receive FDA Clearance for First Dental-Dedicated MRI. Dentsply Sirona and Siemens Healthineers received US FDA clearance for the MAGNETOM Free.Max Dental Edition, the first dental-dedicated MRI system. While not directly related to extraction instruments, this milestone underlines the elevated clinical sophistication driving procedural volume in Dentsply Sirona's broader dental practice ecosystem, which includes surgical hand instruments under multiple brand lines.

- February 2026: HuFriedyGroup Debuts PWR Air at Chicago Midwinter Meeting. HuFriedyGroup introduced PWR Air, a new therapeutic air-polishing device, at the 2026 Chicago Midwinter Meeting. The launch reinforces HuFriedyGroup's continued investment in clinical innovations, supporting its presence across periodontal and surgical procedure categories that share instrument procurement relationships with elevator and luxator purchasing.

- January 2026: Dentsply Sirona and Benco Dental Expand Distribution Partnership. Dentsply Sirona and Benco Dental announced an expanded partnership enabling Benco to carry Dentsply Sirona's connected technology solutions in the US market. The partnership reflects Dentsply Sirona's strategy of deepening distribution reach, which applies to its surgical instrument lines as well as digital equipment.

United States Dental Elevator and Luxator Market Report Scope

Dental elevators and luxators are essential oral surgery instruments used to loosen and extract teeth. Luxators feature thin, sharp blades designed to cut periodontal ligaments. Elevators are thicker, wedge-shaped tools used to apply mechanical leverage, sever ligaments, and lift the tooth from its socket.

The United States Dental Elevator and Luxator Market is segmented into several categories. By Product Type, it includes Dental Elevators and Dental Luxators. By Size, the market is divided into instruments of 5 mm, 3 mm, 2 mm, 4 mm, and 10 mm. By End User, the segmentation covers Dental Clinics, Hospitals and Clinics, and Research and Academic Institutes.

| Dental Elevators |

| Dental Luxators |

| 5 mm |

| 3 mm |

| 2 mm |

| 4 mm |

| 10 mm |

| Dental Clinics |

| Hospitals and Clinics |

| Research and Academic Institutes |

| By Product Type | Dental Elevators |

| Dental Luxators | |

| By Size | 5 mm |

| 3 mm | |

| 2 mm | |

| 4 mm | |

| 10 mm | |

| By End User | Dental Clinics |

| Hospitals and Clinics | |

| Research and Academic Institutes |

Key Questions Answered in the Report

What is the 2026 value of the United States dental elevator and luxator market?

The United States dental elevator and luxator market stands at USD 358.98 million in 2026 and is projected to reach USD 502.27 million by 2031 at a 6.95% CAGR.

Which product type leads demand for dental elevators and luxators in the United States?

Dental elevators lead demand, with 63.48% of 2025 market value, because they remain the standard tool across routine extraction workflows.

Why are dental luxators growing faster than dental elevators?

Dental luxators are projected to grow at 7.36% CAGR through 2031 because minimally traumatic extraction and immediate implant workflows place greater value on socket preservation and periodontal ligament separation.

Which end-user setting is expanding fastest in this category?

Hospitals and clinics are the fastest-growing end-user group, with an 7.97% CAGR through 2031, supported by wider outpatient access and more facility-based dental care.

What is driving demand by instrument size in the United States?

The 5 mm size leads current demand with 29.42% of 2025 value because of its versatility, while the 10 mm segment is growing fastest at 8.87% CAGR as more complex molar and third-molar extractions increase.

What is the main risk affecting supplier margins in this space?

The main near-term risk is price pressure from imported low-cost instruments and tariff-linked cost inflation, which can squeeze margins for premium and mid-tier suppliers.

Page last updated on: