US Software Consulting Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

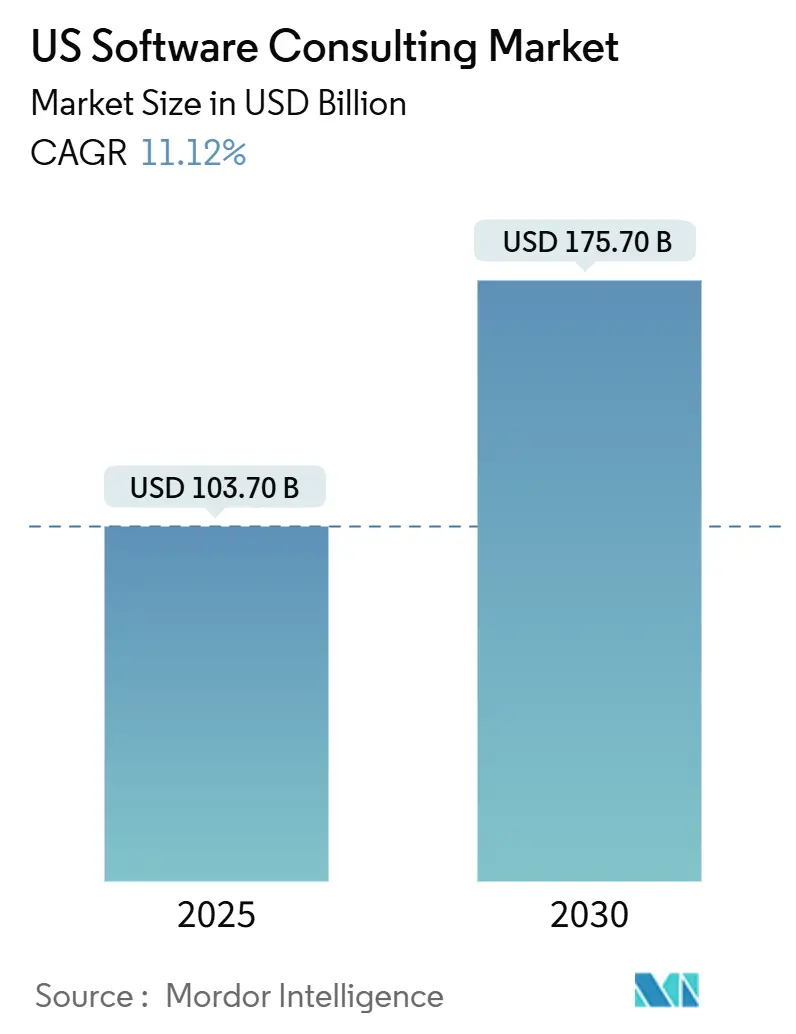

| Market Size (2025) | USD 103.70 Billion |

| Market Size (2030) | USD 175.70 Billion |

| Growth Rate (2025 - 2030) | 11.12% CAGR |

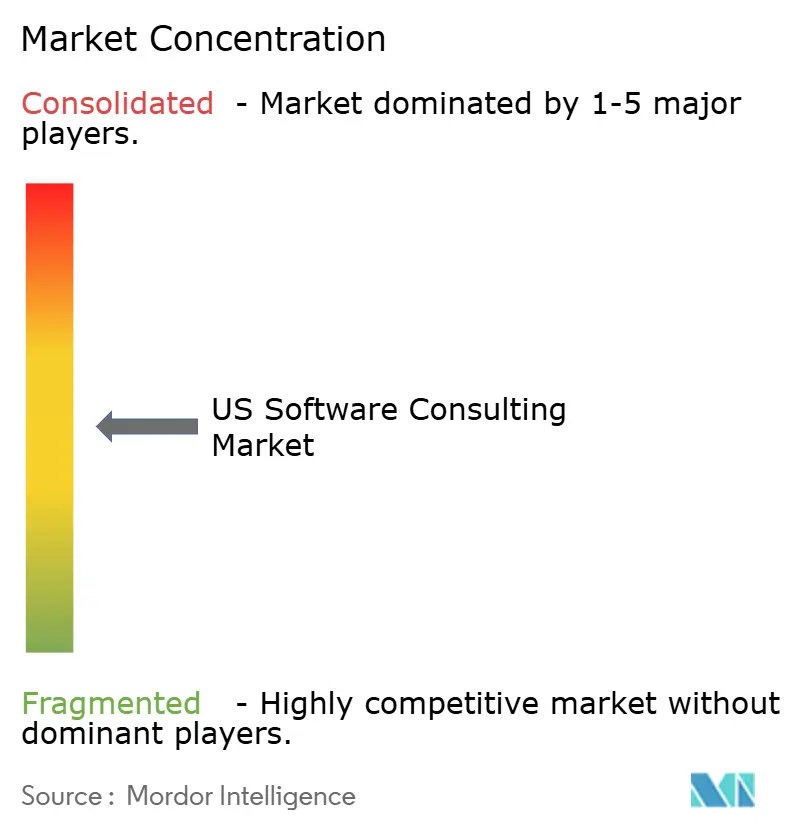

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Software Consulting Market Analysis by Mordor Intelligence

The 2025 software consulting market size in the United States stands at USD 103.70 billion and is forecast to climb to USD 175.70 billion by 2030, reflecting an 11.12% CAGR. The relentless modernization of aging platforms, the mainstreaming of artificial intelligence, and the adoption of cloud-native solutions keep consulting pipelines full as digital initiatives shift from elective projects to core strategy. With 88% of firms confirming tangible value from digital programs, engagements now focus on deep-rooted changes to their operating model rather than pilot experimentation.[1]Deloitte, “Digital Transformation Survey 2024: Accelerating Digital Transformation,” deloitte.com Post-pandemic hybrid work continues to reshape infrastructure choices, while federal defense modernization funding injects large, multiyear projects that reinforce demand stability. Enterprises are also reallocating budgets toward multi-cloud advisory services, responding to concerns about vendor lock-in and rising public cloud spending, which now averages USD 29 million annually per organization.

Key Report Takeaways

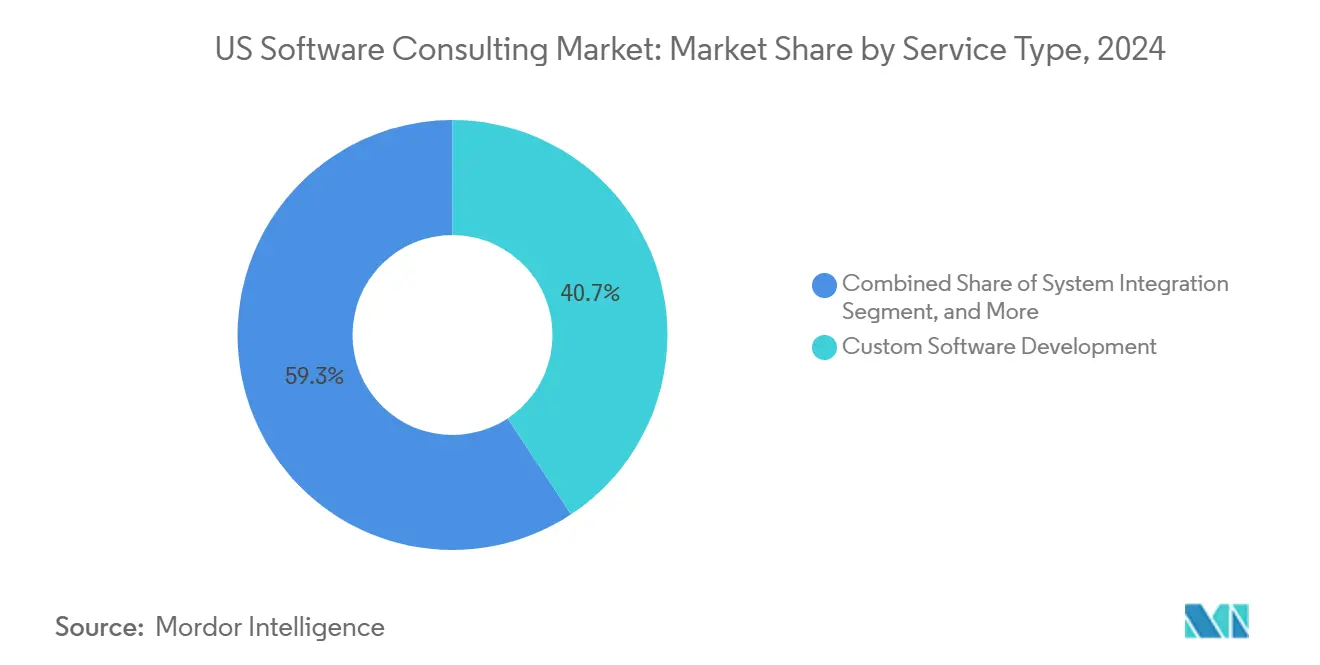

- By service type, custom software development led with a 40.7% share of the US software consulting market in 2024, while application modernization is projected to grow at a 13% CAGR through 2030.

- By end-use industry, BFSI commanded 30.8% of the US software consulting market size in 2024; the healthcare sector is projected to advance at a 13.9% CAGR through 2030.

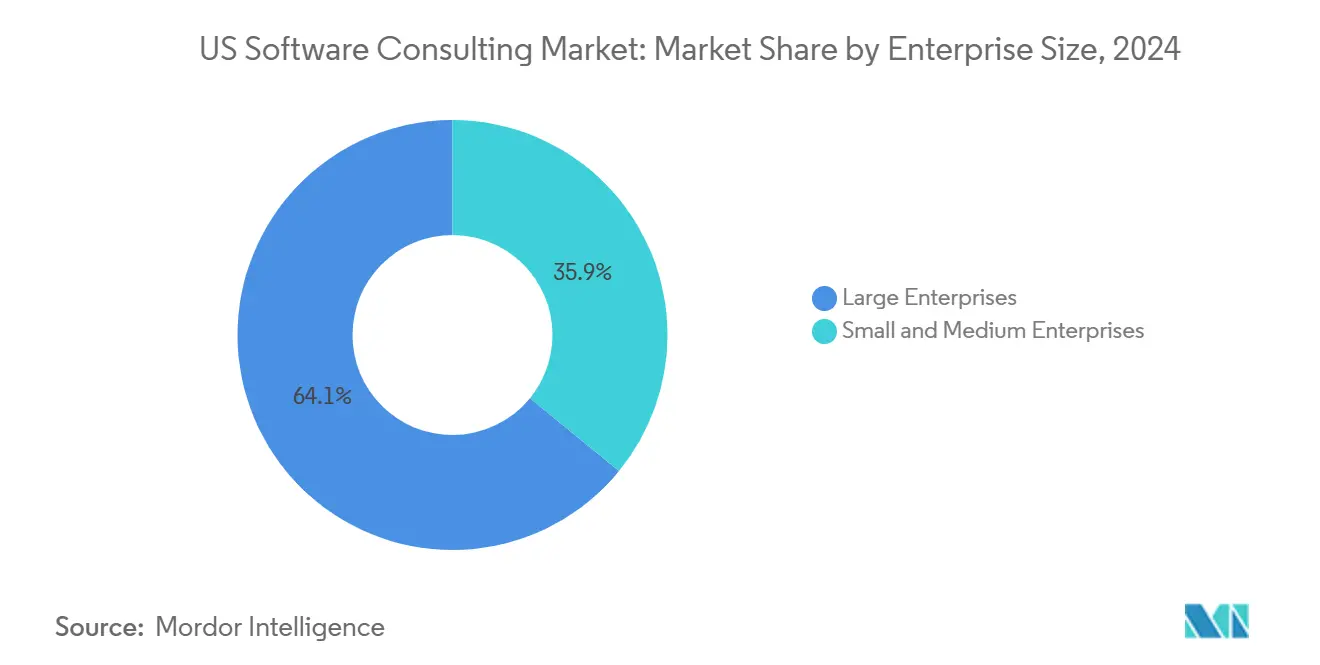

- By enterprise size, large enterprises retained a 64.1% share of the US software consulting market in 2024; however, the SME segment is projected to grow at a 12% annual rate through 2030.

- By deployment model, cloud-based approaches accounted for 55.02% of the US software consulting market share in 2024, while hybrid architectures are projected to expand at a 12.4% CAGR through 2030.

- By region, the South captured a 36.31% share of the US software consulting market size in 2024, while the West exhibits the fastest 12.8% CAGR through 2030.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on software consulting market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

US Software Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-first enterprise mandates | +2.8% | National, urban centers | Medium term (2-4 years) |

| Cloud-native transformation across legacy stacks | +2.5% | West and Northeast | Long term (≥ 4 years) |

| AI-driven productivity tooling integration | +2.2% | Tech and financial hubs | Short term (≤ 2 years) |

| Low-code platforms expanding developer capacity | +1.8% | SME-heavy regions | Medium term (2-4 years) |

| Post-pandemic hybrid work reshaping IT spend | +1.5% | Distributed-workforce regions | Short term (≤ 2 years) |

| Defense modernization funding spur | +1.2% | Virginia, California, Texas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-First Enterprise Mandates

Enterprises now view digital transformation as a survival imperative, replacing siloed modernization with holistic overhauls that demand end-to-end consulting engagements. API-first and microservices designs dominate new blueprints, and legacy-laden verticals such as manufacturing and healthcare depend on external specialists for refactoring. Public-sector momentum reinforces private activity; the Technology Modernization Fund authorized USD 2.1 billion for federal projects in 2024, guaranteeing baseline demand even in cyclical downturns.[2]U.S. General Services Administration, “Technology Modernization Fund,” gsa.gov Because digital capabilities now determine competitive parity, spending stays insulated from discretionary cuts, lengthening average contract tenures, and enlarging project scope.

Cloud-Native Transformation Across Legacy Stacks

Multi-cloud adoption, reported by 89% of enterprises, has matured from a risk mitigation strategy to a preferred architecture, intensifying the need for migration roadmaps tailored to decades-old mainframes. Financial services leaders exemplify scale: JPMorgan Chase commits USD 12 billion annually to technology, with cloud-native re-architecture topping the agenda.[3]JPMorgan Chase, “Annual Technology Investment Report,” jpmorganchase.com Consulting partners are increasingly shifting from lift-and-shift execution to ground-up rebuilds that leverage autoscaling, serverless, and managed AI. Such complexity inflates average deal value and expands recurring optimization workstreams after initial cut-over.

AI-Driven Productivity Tooling Integration

Seventy-four percent of organizations already register measurable returns from AI, yet only 8% run enterprise-wide deployments, underscoring a vast advisory gap. Generative AI and large language models raise technical, governance, and compliance questions that in-house teams rarely master. Microsoft’s USD 13 billion infusion into OpenAI and the subsequent Azure OpenAI Service have accelerated production pilots, creating a wave of demand for responsible-AI consulting, model fine-tuning, and data-privacy safeguards.

Low-Code Platforms Expanding Developer Capacity

Monthly active users on the Microsoft Power Platform surpassed 20 million in 2024, up 40% year-over-year, revealing management's urgency to offset developer shortages with citizen development. Consulting firms guide platform evaluation, establish guardrails, and integrate low-code output with core systems. Because every citizen application still relies on secure APIs, identity management, and data correctness, seasoned architects remain central, turning low-code from a threat into an additive revenue line.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acute shortage of senior full-stack architects | -1.8% | Major tech hubs | Long term (≥ 4 years) |

| Rising cybersecurity liability insurance premiums | -1.2% | Highly regulated sectors | Medium term (2-4 years) |

| Vendor lock-in concerns with hyperscalers | -0.8% | Large enterprises | Medium term (2-4 years) |

| Sustainability reporting costs for data centers | -0.6% | High-regulation states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acute Shortage of Senior Full-Stack Architects

Software developer employment is on a 25% growth path through 2032, but universities and bootcamps cannot mint architects at a comparable velocity. Scarcity inflates senior salaries to USD 180,000–250,000 in top metros, squeezing project margins and prolonging delivery cycles. Firms respond with reskilling academies and offshore talent hubs, yet attaining the requisite depth in AI, cloud, and security still requires years of mentorship, limiting near-term capacity expansion.

Rising Cybersecurity Liability Insurance Premiums

Cyber insurance premiums have increased by 50% annually since 2022, reflecting the rising frequency of breaches and heightened regulatory scrutiny. Healthcare and financial projects incur the steepest increases, occasionally forcing consultancies to absorb costs or pass them downstream. Tighter indemnity clauses now appear in master service agreements, demanding more rigorous security attestations. For smaller firms, premium spikes constrain bid competitiveness, prompting them to shift toward lower-risk verticals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Custom Development Drives Market Leadership

Custom development held 40.7% of 2024 revenue, underscoring the premium that enterprises place on differentiated functionality. The software consulting market size for custom solutions benefits from sector-specific compliance pressures that off-the-shelf software often fails to satisfy. High-regulation clients rely on proprietary code bases to execute unique workflows and encapsulate institutional IP. Application modernization is the fastest riser, with a 13% CAGR, propelled by cloud mandates and technical debt exposure. Modernization projects often transition into data-platform upgrades and DevOps enablement, thereby prolonging engagement lifecycles. System integration occupies an enduring niche as heterogeneous stacks proliferate. Implementation and support services grow in tandem, fueled by continuous delivery models that blur the lines between build and run. Regulatory frameworks such as SOX ensure sustained advisory demand around auditability and controls.

Consultancies refine accelerators to speed discovery, code refactoring, and automated testing. Pre-built microservice templates and domain-driven design artifacts compress timelines and increase margins. Vendors further monetize post-deployment through managed services and optimization sprints, anchoring annuity revenue.

By End-Use Industry: BFSI Leadership Meets Healthcare Acceleration

BFSI contributed 30.8% of 2024 revenue, securing leadership through digital banking rollouts, fintech partnerships, and open banking API strategies. Stringent regulatory obligations, such as Basel IV and real-time fraud monitoring, intensify reliance on advisory services. The software consulting market benefits from continual core-bank transitions and payment-rail upgrades as incumbents battle challenger banks. Healthcare races ahead at a 13.9% CAGR, energized by electronic health-record modernization, remote-care platforms, and AI-powered diagnostics. Pandemic-era telehealth adoption has created data interoperability challenges that only specialized consultancies can solve.

Retail and e-commerce assignments encompass omnichannel orchestration, inventory analytics, and personalization engines that enhance conversion rates. Manufacturing engagements focus on Industry 4.0, IoT data lakes, and predictive maintenance, while public-sector wins stem from grants from the Technology Modernization Fund. Diversification across verticals insulates revenue streams when individual sectors pause investment.

By Enterprise Size: Large Enterprises Dominate While SMEs Accelerate

Large enterprises accounted for 64.1% of 2024 spending, leveraging multi-year transformation roadmaps and board-level budgets. These clients demand full-stack capabilities, global delivery reach, and robust change-management frameworks. The software consulting market size for large-scale programs remains buoyant as AI and multi-cloud complexity deepens.

SMEs, expanding at a 12% CAGR, present shorter, outcome-based projects that capitalize on the affordability of SaaS and low-code solutions. Federal and state grants under SBA digital-readiness programs lower adoption barriers, further widening the SME pipeline. Consultancies respond with templated offerings, agile pods, and value-based pricing to preserve margins amid smaller ticket sizes.

By Deployment Model: Cloud-Based Dominance Yields to Hybrid Growth

Cloud deployments accounted for 55.02% of 2024 revenue, thanks to hyperscaler security certifications and usage-based economics. Yet, hybrid architectures, growing at a rate of 12.4% annually, increasingly address data-sovereignty and latency constraints, particularly in regulated or edge-heavy operations. The software consulting market share for hybrid scenarios expands as firms integrate colocation, private cloud, and edge nodes into cohesive management planes.

On-premise engagements persist where deterministic latency or classified data preclude the use of a public cloud. FedRAMP continues to shape deployment choices in the government, with consultancies required to certify their environments before being granted authority to operate. The rise of edge computing is closely tied to the rollout of 5G, opening up new avenues in distributed analytics and device orchestration.

Geography Analysis

The South accounted for 36.31% of the software consulting market share in 2024, driven by lower operating costs, business-friendly policies, and rapid corporate migration into hubs such as Austin, Atlanta, and Raleigh. State incentives, university pipelines, and quality-of-life advantages sustain hiring momentum. Major banks and cloud providers are deepening their local footprints, reinforcing consulting ecosystems that serve both relocated headquarters and regional startups.

The West projects the highest 12.8% CAGR through 2030, anchored by Silicon Valley’s concentration of hyperscalers, venture capital, and AI research. Seattle and Denver emerge as secondary poles, attracting consultancies eager to staff near cutting-edge client work. Early adoption of quantum computing, autonomous systems, and climate-tech solutions creates demand for frontier-tech advisory practices.

The Northeast’s financial services density fuels large-ticket, compliance-heavy implementations, while the Midwest’s manufacturing heritage drives Industry 4.0 and supply chain optimization projects. Federal engagements cluster around Washington D.C., leveraging Technology Modernization Fund allocations and defense initiatives to maintain a steady deal flow. Regional wage variations influence the placement of delivery centers, with firms balancing talent availability against cost pressures.

Competitive Landscape

Market concentration is moderate. Accenture, IBM, and Cognizant each hold sizable but not dominant positions, while Deloitte, TCS, Infosys, and Wipro round out a crowded top tier. These incumbents cross-invest in AI, cloud, and cybersecurity practices, often through acquisitions aimed at niche capability gaps. Accenture’s USD 3 billion AI program, IBM’s USD 6.4 billion HashiCorp acquisition, and Deloitte’s USD 800 million AI firm spree typify the arms race for talent and IP. Boutique specialists differentiate through deep AI, low-code, or industry-specific expertise, compressing cycles for proof-of-value and competing on agility.

Tool-based delivery is gaining traction as firms patent auto-code generation and AI testing frameworks, thereby lowering person-hour requirements and appealing to clients seeking faster ROI.[4]U.S. Patent and Trademark Office, “AI and Software Development Patent Trends,” uspto.gov Price competition remains tempered by talent scarcity and outcome-based contracting, which aligns fees with business metrics. Cyber-insurance premium hikes raise operating costs, encouraging joint risk-sharing models between clients and consultancies. Market entrants succeed by focusing on vertical depth or regional presence rather than full-stack breadth.

US Software Consulting Industry Leaders

Accenture plc

IBM Corporation

Cognizant Technology Solutions Corporation

Infosys Limited

Tata Consultancy Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Accenture committed USD 3 billion to AI over a three-year period, acquiring five specialist firms and adding 30,000 practitioners.

- August 2025: IBM has finalized its USD 6.4 billion purchase of HashiCorp, enhancing its hybrid-cloud consulting and DevOps automation capabilities.

- July 2025: Cognizant opened a USD 1 billion digital-engineering hub in Phoenix, creating 10,000 AI and cloud jobs.

- June 2025: TCS launched its largest North American delivery center in Austin with capacity for 5,000 consultants.

- May 2025: Deloitte Digital acquired three AI consultancies for USD 800 million, enhancing its depth in computer vision and MLOps.

US Software Consulting Market Report Scope

| Custom Software Development |

| Application Modernization |

| System Integration |

| Implementation and Support |

| Other Specialized Consulting |

| BFSI |

| Healthcare |

| Retail and E-commerce |

| Manufacturing |

| Government and Public Sector |

| Other End-Use Industries |

| Small and Medium Enterprises |

| Large Enterprises |

| On-Premise |

| Cloud-Based |

| Hybrid |

| Northeast |

| Midwest |

| South |

| West |

| By Service Type | Custom Software Development |

| Application Modernization | |

| System Integration | |

| Implementation and Support | |

| Other Specialized Consulting | |

| By End-Use Industry | BFSI |

| Healthcare | |

| Retail and E-commerce | |

| Manufacturing | |

| Government and Public Sector | |

| Other End-Use Industries | |

| By Enterprise Size | Small and Medium Enterprises |

| Large Enterprises | |

| By Deployment Model | On-Premise |

| Cloud-Based | |

| Hybrid | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

How large is the U.S. software consulting market in 2025?

The 2025 US software consulting market size is USD 103.70 billion, and it is projected to reach USD 175.70 billion by 2030.

What is the current CAGR outlook for software consulting through 2030?

The market is expected to expand at an 11.12% CAGR over the 2025–2030 period.

Which service type leads client spending today?

Custom software development holds the lead with 40.7% revenue share in 2024, driven by demand for differentiated functionality.

Which deployment approach is growing fastest?

Hybrid architectures are advancing at a 12.4% CAGR as firms blend cloud scalability with on-premises control.

Which region is forecast to grow the quickest?

The West is set for a 12.8% CAGR to 2030, buoyed by Silicon Valley’s innovation and expansion in Seattle and Denver.

What is the biggest challenge facing consulting providers?

A persistent shortage of senior full-stack architects, with demand outstripping supply by 30%, is inflating costs and elongating project timelines.

Page last updated on: