North America Strategic Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

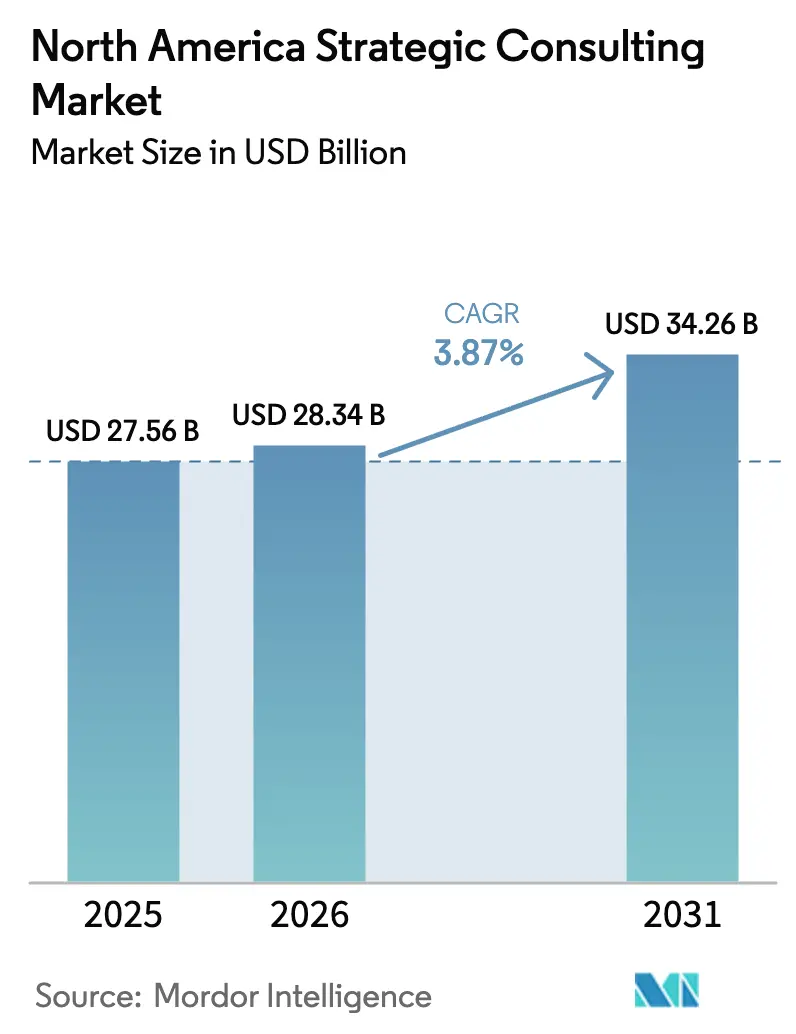

| Base Year Market Size (2025) | USD 27.56 Billion |

| Market Size (2026) | USD 28.34 Billion |

| Market Size (2031) | USD 34.26 Billion |

| Growth Rate (2026 - 2031) | 3.87% CAGR |

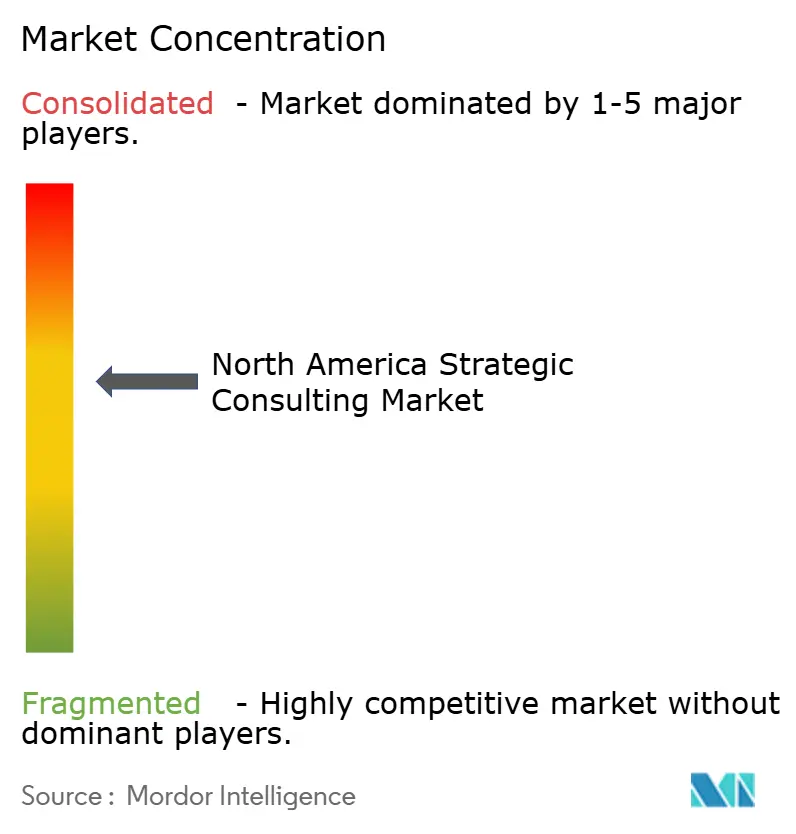

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Strategic Consulting Market Analysis by Mordor Intelligence

The North America strategic consulting market size is projected to be USD 27.56 billion in 2025, USD 28.34 billion in 2026, and reach USD 34.26 billion by 2031, growing at a CAGR of 3.87% from 2026 to 2031. Solid demand for external counsel persists even as clients develop in-house analytics teams and algorithm-driven decision platforms. Advisory firms are pivoting toward outcome-linked contracts, proprietary artificial intelligence toolkits, and deeper industry specialization to preserve pricing power. The result is a North America strategic consulting market that is growing steadily yet transforming rapidly in both service mix and delivery model. Competitive pressure is intensifying as boutique digital specialists court mid-market clients once served almost exclusively by global integrators.

Key Report Takeaways

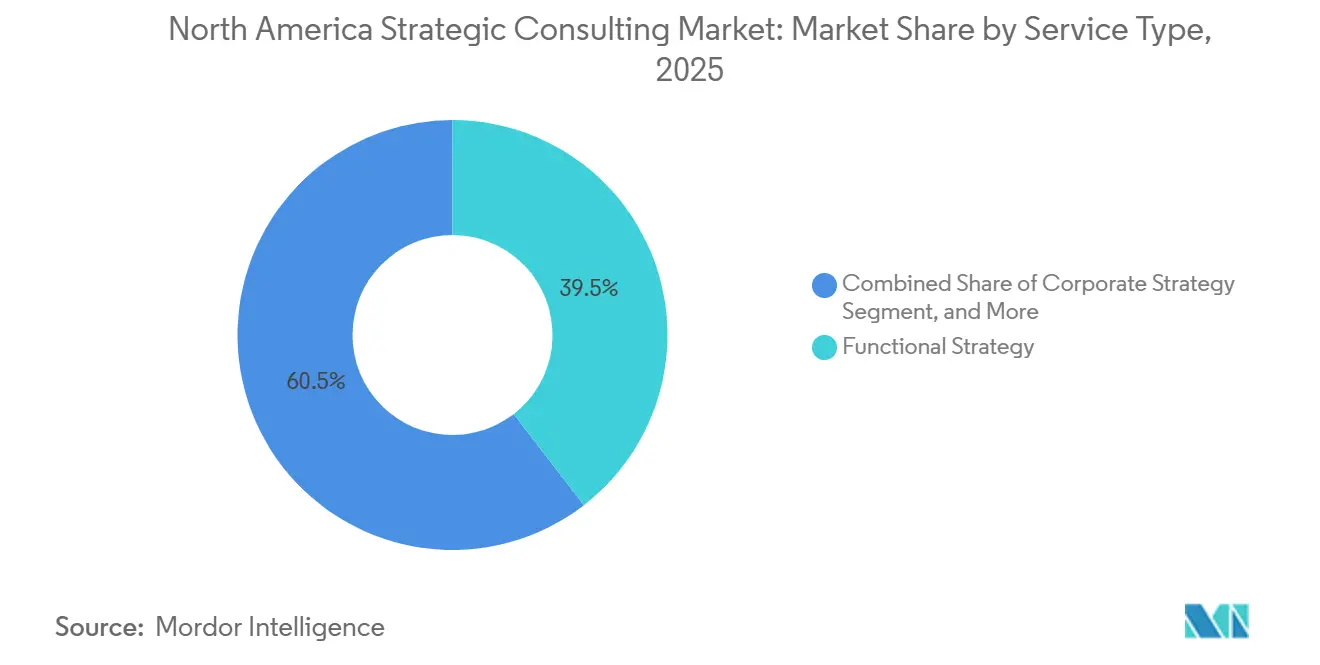

- By service type, functional strategy commanded 39.53% revenue share in 2025 while digital strategy and innovation is forecast to accelerate at a 4.65% CAGR through 2031.

- By organization size, large enterprises held 62.89% of the North America strategic consulting market share in 2025 whereas small enterprises are projected to expand at a 4.86% CAGR to 2031.

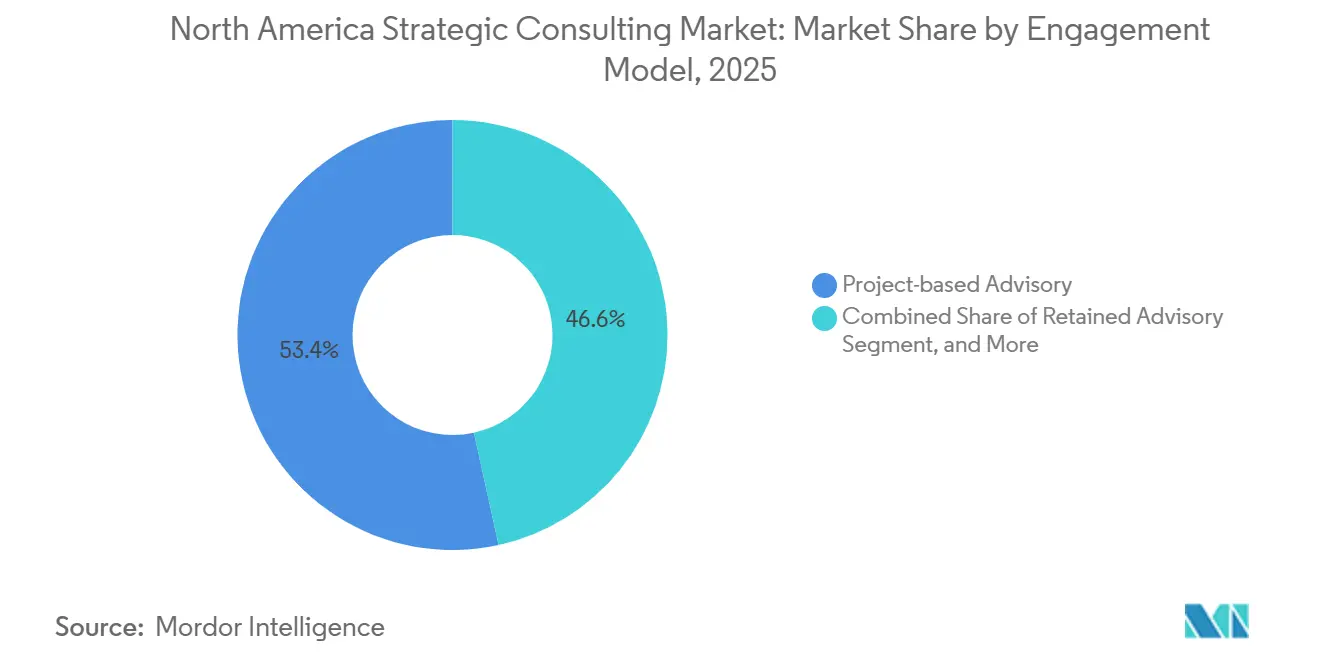

- By engagement model, project-based advisory delivered 53.43% of 2025 revenue and outcome-based consulting is advancing at a 4.78% CAGR during the outlook period.

- By end-user industry, financial services led with 28.92% share in 2025; life sciences and healthcare is set to grow at a 5.32% CAGR through 2031.

- By country, the United States captured 80.42% of 2025 revenue, while Mexico is poised for a 5.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Strategic Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Demand for Digital Strategy Consulting Among Corporates | +1.2% | United States, Canada, with early adoption in technology and financial services sectors | Medium term (2-4 years) |

| Growth of Mergers and Acquisitions Activity | +0.9% | United States dominance, spillover to Canada and Mexico cross-border transactions | Short term (≤ 2 years) |

| Rising Complexity in Regulatory Compliance | +0.7% | United States and Canada, particularly financial services and healthcare sectors | Long term (≥ 4 years) |

| Need for Cost Optimization and Operational Efficiency | +0.6% | North America-wide, with concentration in industrial and manufacturing segments | Medium term (2-4 years) |

| Accelerated Adoption of Advanced Analytics and AI-Powered Strategic Modeling | +0.8% | United States technology hubs, expanding to Canada and Mexico | Medium term (2-4 years) |

| Emergence of Sustainability-Linked Corporate Strategy Mandates | +0.5% | United States and Canada, driven by institutional investor pressure and SEC climate disclosure rules | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Demand For Digital Strategy Consulting Among Corporates

C-suite budgets earmarked 7.5% of 2024 revenue for digital transformation, yet only 22% of organizations shifted generative AI pilots into production, underscoring an execution gap that external advisors now monetize. Legacy technology stacks, dispersed data estates, and cautious governance impede scale-up, so engagements pivot toward organizational change, technical-debt remediation, and return-on-investment modeling. Financial institutions and healthcare providers lead demand because regulators require independent validation of cybersecurity resilience and data-privacy safeguards. [1]U.S. Securities And Exchange Commission Staff, “Proposed Climate Disclosure Rules,” U.S. Securities and Exchange Commission, sec.gov As digital road maps intertwine with compliance workflows, the North America strategic consulting market deepens its role inside enterprise governance structures. Advisory firms differentiate through proprietary accelerators that compress proof-of-concept cycles and quantify business impact within months.

Growth Of Mergers And Acquisitions Activity

North American deal value reached USD 2.04 trillion in 2025, a 63% jump over 2024, producing episodic but high-margin mandates for due diligence, valuation modeling, and synergy capture. Consultants remain embedded up to 24 months post-close to resolve integration bottlenecks around culture, systems, and operating cadence. Life sciences illustrates the pattern as pharmaceutical acquirers seek pipeline rejuvenation and require guidance on regulatory pathway viability and post-market evidence generation. Cross-border activity among the United States, Canada, and Mexico accelerates under the United States-Mexico-Canada Agreement, compelling advisors to interpret divergent tax regimes and labor codes. The North America strategic consulting market thereby links its own fee trajectory to the region’s M&A cycle.

Accelerated Adoption Of Advanced Analytics And AI-Powered Strategic Modeling

Consulting firms have armed their workforces with proprietary large language models that synthesize research, pre-populate scenario libraries, and draft deliverables at unprecedented speed. These internal platforms improve project margins while forming demonstration sandboxes for client AI initiatives. Advisory value now stems from algorithmic sophistication plus change-management rigor rather than generic frameworks that off-the-shelf AI can replicate. Clients demand pilot engagements that tie fees to realized gains, nudging the North America strategic consulting market toward outcome-linked contracts. The frontier emphasis on data-network effects and model governance cements long-term consultant involvement as businesses seek confidence in AI risk controls.

Rising Complexity In Regulatory Compliance

Financial institutions digested over 200 material rule changes during 2025, pushing compliance budgets up 18% year over year. Healthcare systems face parallel pressure as fast-track approval routes for gene therapies multiply documentation requirements.[2]U.S. Food And Drug Administration, “Accelerated Approval Pathways For Gene Therapies,” fda.gov Regulatory fragmentation across federal, state, and provincial lines prevents economies of scale, forcing executives to lean on specialists who translate statutes into operating policy. Advisory projects span risk-taxonomy redesign, reg-tech selection, and supervisory exam rehearsal. The North America strategic consulting market, thus secures an annuity stream tethered to perpetual rule churn.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of In-House Strategy Teams | -0.8% | United States, particularly among Fortune 500 companies and technology firms | Medium term (2-4 years) |

| Talent Shortages and High Consultant Turnover | -0.5% | North America-wide, with acute pressure in technology and digital strategy practices | Short term (≤ 2 years) |

| Commoditization of Traditional Strategy Frameworks via Generative AI Tools | -0.6% | United States and Canada, affecting mid-tier and boutique consultancies | Medium term (2-4 years) |

| Increasing Client Preference for Outcome-Based Pricing Models Reducing Margins | -0.4% | United States and Canada, driven by procurement sophistication and budget constraints | Long term (≥ 4 ye |

| Source: Mordor Intelligence | |||

Expansion Of In-House Strategy Teams

Fortune 500 enterprises hired former consultants en masse during 2025 to build internal centers of excellence that replicate traditional advisory methods and lower repeat spend.[3]Claire Bushey, “Corporates Build Internal Strategy Units To Shrink Consulting Spend,” Financial Times, ft.com Technology companies lead the shift, redeploying algorithmic talent across product lines without external procurement cycles. Routine planning, market scans, and competitor intelligence now migrate in-house, leaving external firms to fight for complex, high-stakes mandates. Advisory providers counter by embedding staff for multiyear transformation programs that blur boundaries between consulting and managed services, but margin profiles differ markedly from short-cycle project work.

Commoditization Of Traditional Strategy Frameworks Via Generative AI Tools

Freely available language models generate SWOT charts, market-entry matrices, and five-forces analyses within minutes, eroding the perceived value of slide-driven deliverables. Mid-tier and boutique consultancies are most exposed because proprietary data assets and implementation scale often differentiate larger rivals. To defend share, firms bundle analytics platforms, industry benchmarks, and change-management road maps that AI cannot fully automate, yet fee pressure persists. This dynamic restrains the North America strategic consulting market by shaving pricing power even as demand volumes hold steady.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Momentum Outpaces Legacy Functional Work

The functional strategy accounted for 39.53% of the North America strategic consulting market size in 2025, driven by human-resources redesign and supply-chain resilience mandates. Digital strategy and innovation, however, posts the swiftest 4.65% CAGR thanks to enterprise urgency around artificial intelligence deployment. Clients acknowledge that 65% of firms piloted generative AI yet only 22% scaled it, so advisors who can bridge experimentation and production enjoy pricing latitude. Functional advisory retains scale for cost-takeout programs, but digital teams now influence every redesign because cloud architectures and advanced analytics underpin modern process excellence. Corporate-strategy mandates still appear, but investors increasingly evaluate technology leverage when approving capital plans, blending digital imperatives into boardroom conversations. M&A advisory volumes fluctuate with macro conditions, supplying episodic upside yet exposing firms to rate-cycle volatility. Economic and policy engagements serve governments navigating infrastructure or trade reform, but procurement bureaucracy tempers expansion. In aggregate, digital’s rise signals that algorithmic capability eclipses classical economies-of-scale logic as the chief competitive weapon inside the North America strategic consulting market.

Second-order effects reinforce digital’s pull. Talent migration favors practices offering exposure to AI tool-building and data-science problems, thereby deepening capability gaps between digitally fluent consultancies and slower peers. Clients in life-sciences and financial services request dual-track projects that embed regulatory compliance into digital road maps, anchoring consultants for longer horizons. The North America strategic consulting market share held by functional advisory therefore slides gradually even as its absolute revenue grows, a testament to digital’s disproportionate contribution to incremental spend.

By Organization Size: Democratizing Access To Executive Insight

Large enterprises represented 62.89% of 2025 revenue, securing multiyear transformation road maps that require board-level sign-off. Governance norms oblige external validation, sustaining engagement flow to global integrators. Yet small enterprises, defined here as firms below USD 50 million in annual revenue, are projected to expand their spend at a 4.86% CAGR, the fastest across size tiers. Cloud collaboration suites and AI-assisted research have slashed minimum project economics, letting boutiques win deals once considered too small. As a result, the North America strategic consulting market penetrates entrepreneurial segments earlier in company life cycles.

Medium enterprises exhibit hybrid patterns, purchasing discrete growth diagnostics while lacking budgets for continuous retainers. Price sensitivity pushes these clients toward outcome-linked contracts, accelerating experimentation across the market. Consultants respond by curating modular service catalogs that scale with client maturity, from market-entry blueprints to implementation playbooks. This staircase approach lengthens customer lifetime value while expanding addressable volume. Margins, however, compress when serving smaller clients because delivery costs do not fall linearly with project size, reinforcing the premium positioning of enterprise programs inside the North America strategic consulting industry.

By Engagement Model: Risk-Sharing Becomes The New Normal

Project-based work delivered 53.43% of revenue in 2025, offering clarity on scope, timeline, and cost. Procurement teams value fixed deliverables, yet boards increasingly question fees not tied to observable impact. Consequently, outcome-based consulting is advancing at 4.78% CAGR and threatens to overtake traditional projects in new contract volume by decade-end. The pivot demands stronger data baselines, rigorous value-tracking, and deeper client integration, reshaping consultant operating models.

Retainer arrangements persist, especially in private-equity portfolios that need constant oversight, but growth is muted. Managed-services variants, where consultants run transformation offices for years, gain favor among clients lacking execution bandwidth, although talent retention challenges constrain scale. Platform-enabled advisory reduces cost-to-serve via automated analytics, unlocking mid-market penetration yet sparking skepticism over context depth. Overall, the mix shift forces every provider inside the North America strategic consulting market to balance delivery-risk appetite with profitability.

By End-User Industry: Life Sciences Becomes The Growth Engine

Financial services maintained a 28.92% revenue share in 2025 as banks, insurers, and asset managers contended with cybersecurity oversight and consolidation. Life sciences and healthcare, however, holds the highest forward CAGR at 5.32% through 2031, reflecting pharmaceutical M&A, gene-therapy regulation, and value-based reimbursement. Each theme demands bespoke insight into regulatory science and post-deal integration, capabilities that few in-house teams possess. Technology, media, and telecom contribute steady demand for platform monetization strategy, though major players increasingly internalize talent, tempering spend growth.

Energy and resources assignments grow around decarbonization road maps, yet project scope often centers on scenario analysis rather than multi-year implementation. Government consulting remains cyclical due to budget ceilings. Industrial and manufacturing engagements jump alongside nearshoring because footprint redesigns dictate supply-chain simulations, site labs, and workforce planning. As life sciences outpaces peers, its share of the North America strategic consulting market size could eclipse 15% by 2031 if the present deal pipeline closes as expected.

Geography Analysis

The United States generated 80.42% of 2025 revenue, underlining its dominance within the North America strategic consulting market. Fortune 500 density, private-equity capital, and intricate regulatory demands ensure steady advisory volume. Technology clusters in California, Washington, and Texas feed digital-transformation mandates, while financial hubs in New York and North Carolina sustain compliance-oriented consulting. Competitive pressure is high; over 200,000 management consultants operate nationally, but specialization around sustainability strategy, artificial intelligence deployment, and sector-specific regulation allows new entrants to thrive.

Canada follows with measured expansion. Financial-services consolidation, resource-sector diversification, and federal infrastructure spending anchor demand. Bilingual delivery requirements and provincial policy fragmentation complicate project staffing, thus domestic firms with French-language teams hold a structural advantage. Canadian boards increasingly link executive incentives to environmental, social, and governance metrics, driving recurring mandates in carbon accounting and transition planning. Although smaller than its southern neighbor, Canada contributes stable, margin-accretive work because clients favor long-term partnerships once cultural fit is proven.

Mexico is the region’s growth leader at a 5.41% CAGR through 2031, propelled by USD 40 billion of nearshoring-related foreign direct investment in 2024. Automotive, electronics, and medical-device makers relocating supply chains require counsel on industrial-park selection, supplier vetting, and trade-corridor optimization. Consulting capacity in Mexico remains nascent; therefore, global firms open local offices and blend on-site teams with offshore analytics hubs to manage cost. Talent scarcity presents a risk, yet first-mover advantage promises durable client relationships. The shift broadens the spatial footprint of the North America strategic consulting market, hedging providers against U.S. macro volatility while embedding them in resilient continental production networks.

Competitive Landscape

The North America strategic consulting market has a moderate concentration profile. Talent acquisition sits at the center of rivalry, with firms vying for experts in artificial intelligence, advanced analytics, and specialized regulation. High attrition challenges margins; many practitioners depart for technology vendors, private-equity operators, or corporate strategy roles promising better work-life equilibrium. Consulting firms respond by expanding recruitment beyond MBA pipelines to engineers, data scientists, and industry veterans, yet integrating heterogeneous talent pools strains culture cohesion.

Service innovation has become another battleground. Providers deploy proprietary large language models such as McKinsey Lilli or BCG generative-AI toolkits to speed hypothesis testing and deliverable drafting. Outcome-linked pricing further differentiates offerings but shifts risk onto consultants, compelling greater investment in change-management and implementation capabilities. Boutique specialists punch above their weight where deep domain expertise matters, such as sustainability mandates, policy navigation, or life-science regulation, forcing global integrators either to partner, acquire, or build niche teams organically.

Digital-native platforms also disrupt from below, automating research synthesis and democratizing strategy frameworks for small-enterprise consumers. While margins in that segment are thinner, volume growth attracts venture capital financing and pushes incumbents to develop low-touch productized services. The competitive outlook therefore balances consolidation at the top with fragmentation around niche and tech-enabled challengers, preserving client choice and driving continuous reinvention across the North America strategic consulting industry.

North America Strategic Consulting Industry Leaders

Accenture plc

A.T. Kearney Inc.

The Boston Consulting Group Inc.

Bain & Company Inc.

Deloitte Touche Tohmatsu Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Accenture acquired a Mexico-based supply-chain consultancy for over USD 50 million to deepen nearshoring advisory capability.

- December 2025: Deloitte launched a dedicated life-sciences regulatory strategy practice, onboarding 15 former U.S. FDA officials.

- November 2025: Boston Consulting Group introduced an AI-powered strategic-modeling platform that cuts delivery time by 30%.

- October 2025: McKinsey and Company opened a third Mexican office in Monterrey focused on supply-chain optimization.

North America Strategic Consulting Market Report Scope

Strategy consultants provide in-depth industry knowledge and impartial advice to provide organizations with the best outcomes for major decisions. The Strategic Consulting services Market forms a sub-set of overall consulting focused on developing corporate, functional, and organizational strategies.

The North America Strategic Consulting Market Report is Segmented by Service Type (Corporate Strategy, Business-Model Transformation, M&A and Corporate Finance Strategy, Digital Strategy and Innovation, Functional Strategy, and Economic and Policy Advisory), Organization Size (Large Enterprises, Medium Enterprises, and Small Enterprises), Engagement Model (Project-based Advisory, Retained Advisory, Managed/Implementation Services, Outcome-based/Success-fee Consulting, and Digital/Platform-enabled Consulting), End-user Industry (Financial Services, Life Sciences and Healthcare, Technology Media and Telecom, Energy and Resources, Government and Public Sector, Consumer and Retail, Industrial and Manufacturing, and Other End-user Industries), and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| Corporate Strategy |

| Business-Model Transformation |

| M&A and Corporate Finance Strategy |

| Digital Strategy and Innovation |

| Functional Strategy (HR, SCM, etc.) |

| Economic and Policy Advisory |

| Large Enterprises |

| Medium Enterprises |

| Small Enterprises |

| Project-based Advisory |

| Retained Advisory |

| Managed / Implementation Services |

| Outcome-based / Success-fee Consulting |

| Digital / Platform-enabled Consulting |

| Financial Services |

| Life Sciences and Healthcare |

| Technology, Media and Telecom |

| Energy and Resources |

| Government and Public Sector |

| Consumer and Retail |

| Industrial and Manufacturing |

| Other End-user Industries |

| United States |

| Canada |

| Mexico |

| By Service Type | Corporate Strategy |

| Business-Model Transformation | |

| M&A and Corporate Finance Strategy | |

| Digital Strategy and Innovation | |

| Functional Strategy (HR, SCM, etc.) | |

| Economic and Policy Advisory | |

| By Organization Size | Large Enterprises |

| Medium Enterprises | |

| Small Enterprises | |

| By Engagement Model | Project-based Advisory |

| Retained Advisory | |

| Managed / Implementation Services | |

| Outcome-based / Success-fee Consulting | |

| Digital / Platform-enabled Consulting | |

| By End-user Industry | Financial Services |

| Life Sciences and Healthcare | |

| Technology, Media and Telecom | |

| Energy and Resources | |

| Government and Public Sector | |

| Consumer and Retail | |

| Industrial and Manufacturing | |

| Other End-user Industries | |

| By Country | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large is the North America strategic consulting market in 2026?

It is valued at USD 28.34 billion and is on track to reach USD 34.26 billion by 2031.

Which service line is growing fastest?

Digital strategy and innovation consulting is forecast to post a 4.65% CAGR through 2031 as companies scale artificial intelligence initiatives.

Why is Mexico the fastest-growing geography for consulting demand?

Nearshoring has attracted USD 40 billion of foreign investment, prompting manufacturers to seek advisory on site selection, supplier networks, and trade-corridor design.

What engagement model is gaining favor with clients?

Outcome-based consulting, where fees align with measurable business results, is advancing at a 4.78% CAGR and reshaping risk-sharing norms.

Which end-user industry offers the highest future growth?

Life sciences and healthcare, supported by record pharmaceutical M&A and complex regulation, is projected to grow at a 5.32% CAGR to 2031.

How concentrated is the competitive landscape?

The top five firms control roughly 35% of revenue, giving the sector a moderate concentration score of 6.

Page last updated on: