North America Management Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

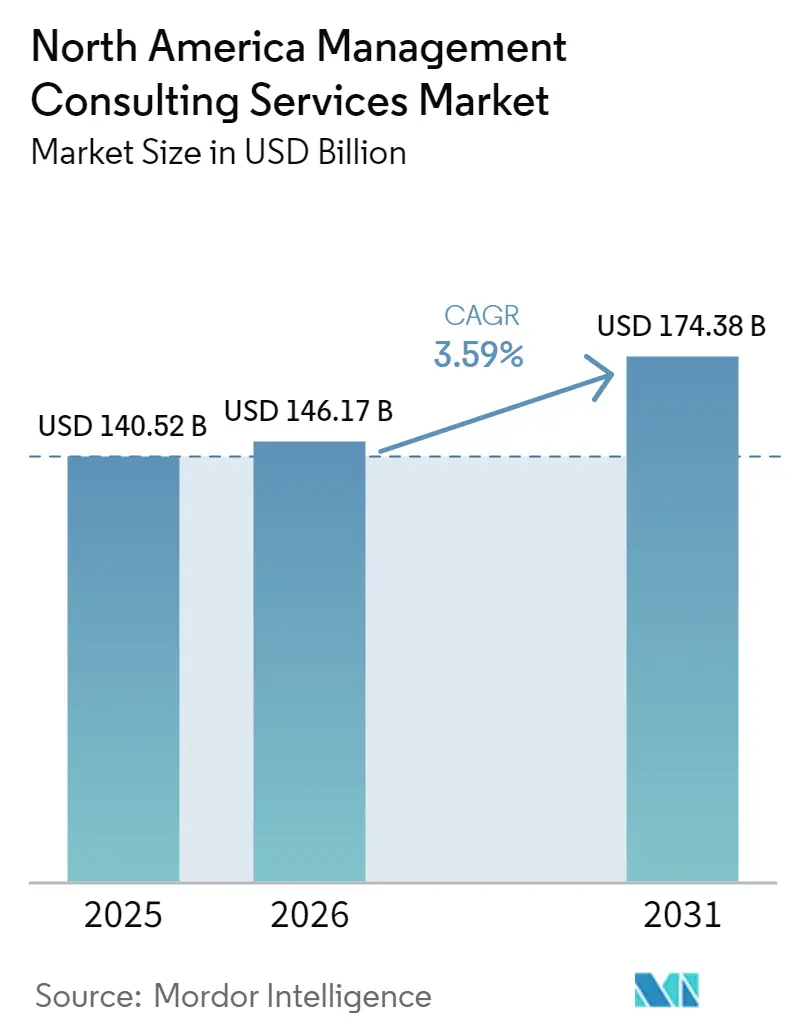

| Base Year Market Size (2025) | USD 140.52 Billion |

| Market Size (2026) | USD 146.17 Billion |

| Market Size (2031) | USD 174.38 Billion |

| Growth Rate (2026 - 2031) | 3.59% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Management Consulting Services Market Analysis by Mordor Intelligence

The North America management consulting services market size is projected to expand from USD 140.52 billion in 2025 and USD 146.17 billion in 2026 to USD 174.38 billion by 2031, registering a CAGR of 3.59% between 2026 to 2031. The region’s advisory budgets are tilting toward digital transformation, generative-AI enablement, and private-equity value creation, even as traditional strategy mandates remain relevant. Federal infrastructure and semiconductor stimulus is anchoring multi-year public-sector demand, while the near-universal experimentation with AI across United States enterprises is exposing gaps between pilot activity and scaled execution. Competitive intensity is rising because technology integrators and niche AI specialists are entering the field, but the consulting majors retain an edge in large, complex programs. Wage inflation and talent scarcity could modestly compress margins, yet the move to hybrid delivery and outcome-based pricing is helping firms protect profitability.

Key Report Takeaways

- By consulting service line, Strategy consulting led with 32.46% of North America management consulting services market share in 2025, whereas Digital transformation consulting is advancing at a 3.91% CAGR through 2031.

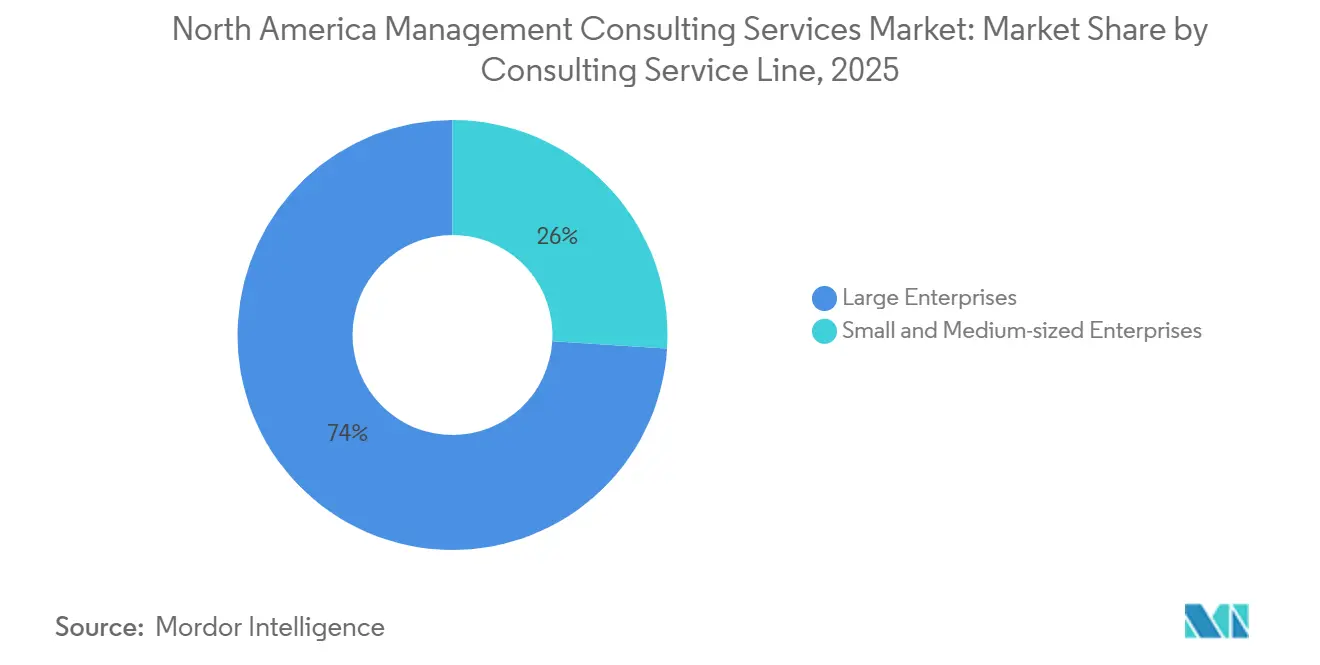

- By organization size, Large enterprises accounted for 67.63% of spending in 2025, while small and medium-sized enterprises are forecast to expand at a 3.64% CAGR to 2031.

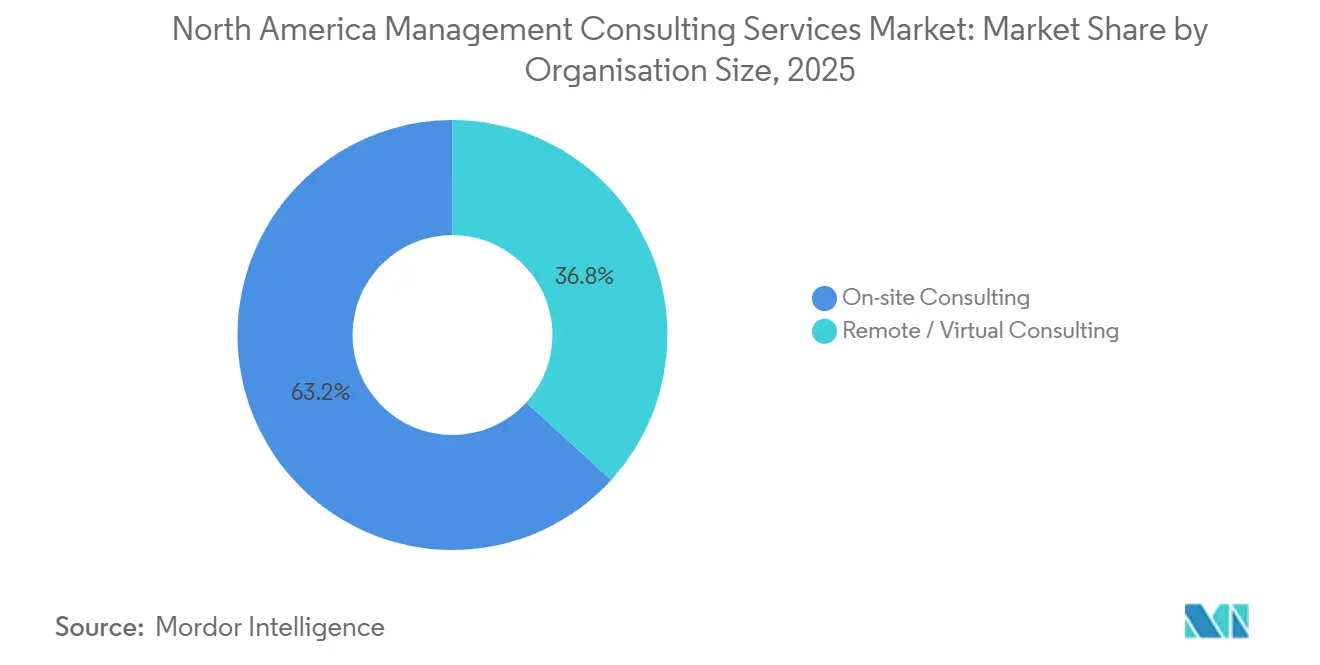

- By delivery model, On-site engagements held a 55.28% share of the North America management consulting services market size in 2025, and hybrid consulting is the fastest-growing format at a 3.87% CAGR.

- By end-user industry, Banking and insurance commanded 26.43% revenue share in 2025, yet IT and telecommunications is projected to grow at a 3.81% CAGR through 2031.

- By geography, the United States generated 78.13% of regional revenue in 2025, while Canada is poised for the highest growth at a 3.72% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Management Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DX-led cross-functional advisory demand surge | +0.9% | United States, Canada, Mexico | Medium term (2-4 years) |

| Generative-AI operating-model readiness audits | +0.8% | United States, Canada | Short term (≤ 2 years) |

| Federal infrastructure and CHIPS Act stimulus | +0.7% | United States, spillover to Canada and Mexico | Long term (≥ 4 years) |

| Private-equity portfolio value-creation playbooks | +0.6% | United States, Canada | Medium term (2-4 years) |

| ESG-centric consulting mandates | +0.3% | United States, Canada | Medium term (2-4 years) |

| Mid-market succession-planning boom | +0.2% | United States, Canada | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

DX-Led Cross-Functional Advisory Demand Surge

Digital modernization has evolved into enterprise-wide rewiring that links data strategy, talent architecture, and customer experience. Many companies report doubling the number of live generative-AI use cases between 2024 and 2025, yet fewer than one-third possess clear roadmaps for scale. This execution gap is prompting sustained demand for consultants that can align leadership agendas, redesign operating models, and oversee phased rollouts.[1]Bain and Company, “Survey: Generative AI’s Uptake Is Unprecedented Despite Roadblocks,” bain.com Regulated industries such as banking and healthcare add layers of compliance and security, increasing the premium on cross-functional expertise. The momentum explains why digital transformation consulting is projected to outpace the North America management consulting services market average growth rate.

Generative-AI Operating-Model Readiness Audits

Financial-services and healthcare providers must deploy generative-AI tools to remain competitive, but fragmented oversight and evolving standards slow progress. Many large banks still lack unified data-quality and governance foundations, while health systems wrestle with vendor selection and workflow integration. Consulting teams are therefore engaged in readiness audits that benchmark policies, map risks, and define governance frameworks.[2]Deloitte, “The Path to Sustainable Generative AI Value Balances Passion, Pragmatism and Patience,” deloitte.com Demand is sharply front-loaded into the next two years as boards push for visible returns on early AI investments. Success hinges on embedding risk management, security controls, and change-management protocols from the outset.

Federal Infrastructure and CHIPS Act Stimulus

Three landmark United States statutes, the Bipartisan Infrastructure Law, Inflation Reduction Act, and CHIPS and Science Act, authorized close to USD 2 trillion for transport, clean-energy, and semiconductor programs.[3]Deloitte, “Executing on the USD 2 Trillion Investment to Boost American Competitiveness,” deloitte.com Agencies are standing up hundreds of new grant mechanisms and performance offices, while private manufacturers have announced multibillion-dollar fab commitments. Execution complexity around portfolio tracking, fraud mitigation, supply-chain alignment, and workforce planning is fueling a pipeline of program-management and capital-delivery advisory work. Spillover opportunities extend into Canada and Mexico as cross-border corridors and supplier networks scale up over the decade, supporting long-term consulting demand.

Private-Equity Portfolio Value-Creation Playbooks

With exit windows constrained and holding periods stretching beyond seven years, private-equity sponsors are institutionalizing operating-improvement agendas. Value-creation offices are commissioning large-scale digital, pricing, and data-lake initiatives across portfolio companies to lift EBITDA rather than rely on leverage or multiple expansion. Consultants that can deliver repeatable playbooks, predictive analytics, and cross-portfolio benchmarking are seeing steady pipelines from New York and Toronto funds. Engagement intensity is expected to peak over the next four years as limited partners scrutinize distributions and require demonstrable operational alpha.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent Poaching and Wage Inflation | -0.5% | United States, Canada (major metro hubs) | Short term (≤ 2 years) |

| Internal Digital COEs Displacing External Advisory Spend | -0.4% | United States (large enterprises) | Medium term (2-4 years) |

| Consolidation Driven Fee Pressure | -0.2% | North America (cross-regional) | Medium term (2-4 years) |

| Generative AI DIY Strategy Tools | -0.1% | United States, Canada (tech-forward SMEs) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Talent Poaching and Wage Inflation

Competition for AI engineers, data scientists, and cloud architects is intense across New York, San Francisco, Toronto, and other technology corridors. Clients, hyperscalers, and private-equity operating teams are hiring directly from consulting benches, raising churn levels and bid-up compensation packages.[4]KPMG International, “Generative AI Adoption Index 2025,” kpmg.com Mid-tier firms with thinner margins are feeling the sharpest squeeze because they must match wage expectations without the scale advantages of the Big Four or strategy giants. Higher personnel costs, in turn, erode project profitability unless firms accelerate automation, near-shore delivery, or outcome-based pricing. Over the next two years the North America management consulting services market is expected to absorb this shock while experimenting with hybrid staffing models, talent academies, and AI-enabled productivity tools to offset salary pressure.

Internal Digital COEs Displacing External Advisory Spend

Large banks, insurers, and telecom operators have begun staffing internal centers of excellence that cover analytics, pricing science, and procurement digitization. Once COEs mature, repeatable diagnostic and dashboard work migrates in-house, reducing addressable spend for third-party advisors. Consulting demand therefore shifts toward higher-value services such as governance design, operating-model reconfiguration, and vendor-selection due diligence. The transition is unfolding over a two-to-four-year horizon, particularly in enterprises that already maintain robust IT and risk functions. To remain essential, consultancies are bundling managed services with intellectual-property assets, thereby keeping a foothold inside client COEs rather than ceding ground entirely.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Consulting Service Line: Strategy Dominates, Digital Transformation Accelerates

Strategy engagements generated 32.46% of North America management consulting services market share in 2025, underscoring persistent demand for portfolio realignment, cross-border M and A, and operating-model redesign. The segment remains the anchor for C-suite dialogue when macro uncertainty elevates the premium on scenario planning and capital allocation. Digital transformation consulting, however, is widening its footprint by growing at a 3.91% CAGR through 2031, the fastest among service lines and a direct beneficiary of enterprise AI road-mapping. The North America management consulting services market size attached to digital mandates is scaling because cloud migrations now bundle data-platform builds, automation workflows, and change-management programs into integrated scopes.

Operations consulting is gaining relevance in manufacturing and telecom where clients pursue supply-chain resilience and network automation. Risk and compliance specialists are also in demand as regulators tighten oversight on stablecoins, anti-money-laundering, and ESG disclosures. Smaller but high-growth niches include sustainability advisory and litigation readiness, each catalyzed by fragmented state-level rules and rising class-action exposure. Collectively, these dynamics indicate that multi-disciplinary firms capable of linking strategy, technology, and implementation are best positioned to expand wallet share in the North America management consulting services market.

By Organization Size: Large Budgets Lead, SMEs Accelerate

Large enterprises contributed 67.63% of the 2025 spending pool because they commission complex, multi-year transformations that require global delivery and deep domain knowledge. Many Fortune 1000 companies maintain evergreen master service agreements, keeping consulting teams embedded across strategy, finance, and technology work-streams. Even so, small and medium-sized enterprises are on track to post a 3.64% CAGR through 2031, nudged forward by subsidized compute-access programs and voucher schemes in Canada and select United States states. These incentives shrink the adoption gap and enlarge the North America management consulting services market size associated with mid-market digital projects.

SME buyers favor quick wins, phased rollouts, and shared-services economics rather than bespoke, open-ended engagements. Consequently, consulting firms are designing templated AI accelerators, fixed-fee pilots, and training bundles that align with constrained capital budgets. A secondary benefit for consultants is portfolio diversification, reducing reliance on a handful of mega-clients and spreading talent demand across a broader base.

By Delivery Model: On-Site Still Primary, Hybrid Rises

On-site work represented 55.28% of the 2025 North America management consulting services market size, reflecting client confidence in face-to-face workshops for high-stakes deal diligence and sensitive culture-change programs. However, hybrid delivery is projected to grow at a 3.87% CAGR because remote diagnostics, virtual collaboration suites, and generative-AI documentation tools have proven effective during extended private-equity hold periods. Hybrid approaches allow firms to allocate scarce experts across multiple clients, helping mitigate wage inflation while offering staff improved work-life balance.

Pure virtual consulting is gaining traction in analytics tuning, compliance testing, and HR policy refreshes where physical presence adds marginal value. Clients reap travel-cost savings, and consultants open regional talent pools unconstrained by relocation hurdles. The net result is a gradual rebalancing rather than a wholesale pivot: relationship-heavy strategy sprints will stay largely in person, whereas standardized build-operate-transfer work migrates toward remote or mixed modes.

By End-User Industry: Financial Sectors Command Spend, Telecom Outpaces Growth

Banking and insurance produced 26.43% of total fees in 2025 thanks to constant regulatory churn, stablecoin policy development, and post-merger integration after a wave of megadeals. Generative-AI adoption lags ambition in many banks, sustaining advisory demand for data-quality remediation and hub-and-spoke governance. IT and telecommunications, while smaller, is forecast to post the fastest 3.81% CAGR because operators must reinvent business models in a market where flanker brands and infrastructure carve-outs proliferate.

Manufacturing workloads are expanding due to federal reshoring incentives and the CHIPS Act, which collectively enlarge sourcing, site-selection, and workforce-planning assignments. Energy and resources clients require scenario modeling that juxtaposes fossil-inclusive and renewable pathways amid policy fluctuations. Public-sector buyers, flush with infrastructure allocations, account for a rising share of the North America management consulting services market share dedicated to program-management offices and grant-tracking modernization. Healthcare, retail, and other verticals round out the opportunity set, each adding niche digital and operational scopes as AI permeates workflows.

Geography Analysis

The United States generated 78.13% of the North America management consulting services market revenue in 2025, helped by an exceptional run of megadeals, substantial public-sector stimulus, and enterprise AI budgets that average about USD 10 million. Growth continues as financial-services, telecom, and public-sector clients expand multi-year programs that integrate strategy, implementation, and managed services. California remains the epicenter for software and semiconductor transactions, New York dominates private-equity buyouts, and Texas concentrates energy and household-product consolidation activity. Federal infrastructure and semiconductor laws are anchoring demand for program-management offices, capital-delivery transformation, and regulatory structuring support. State-level ESG fragmentation is simultaneously driving compliance and litigation-readiness work, adding another revenue stream for advisory firms. The United States therefore sets the pace for innovation in hybrid delivery and AI-enabled knowledge management that increasingly define competitive advantage in the North America management consulting services market.

Canada is forecast to record a 3.72% CAGR through 2031, the fastest among regional peers, propelled by CAD 2.4 billion in federal AI commitments and targeted SME voucher initiatives. Government programs that subsidize compute access and skills training are expanding the North America management consulting services market size linked to small and medium-sized enterprise digital projects. Canada’s telecom sector is restructuring as flanker brands claim close to one-third of subscribers, fibre lines overtake cable, and operators pivot toward managed enterprise services, all of which require brand architecture, pricing optimization, and operating-model redesign advisory. Financial centers in Toronto and Montreal are commissioning portfolio-wide value-creation playbooks for private-equity sponsors keen to lift EBITDA amid longer holding periods. Consulting firms that bundle domain expertise with bilingual delivery and regional compliance familiarity are advantaged in winning multi-province scopes.

Mexico benefits from near-shoring as United States manufacturers diversify supply chains to manage tariff exposure and geostrategic risk. Semiconductor incentives, clean-energy credits, and cross-border infrastructure corridors are generating mandates for site selection, vendor diversification, customs integration, and workforce planning. Banks and fintechs in Mexico are digitalizing products and modernizing core systems, creating fresh demand for technology-transformation and regulatory advisory. Manufacturing clients seeking supply-chain resilience are commissioning multi-plant footprint strategies that link northern industrial parks with central and southern logistics hubs. Together these trends lift the North America management consulting services market share attributable to Mexico, although absolute spending remains smaller than in the United States or Canada.

Competitive Landscape

The North America management consulting services market is moderately fragmented, with the top ten firms controlling about 40-45% of total revenue. Deloitte Consulting, PwC, EY, KPMG, Accenture, McKinsey, Boston Consulting Group, Bain, IBM Consulting, and Booz Allen Hamilton remain the dominant incumbents, each leveraging global scale, deep industry benches, and cross-border delivery centers. These firms secure most multibillion-dollar enterprise transformations and federal modernization contracts because they combine strategy design with technology implementation capabilities.

Competitive intensity is rising as technology integrators, offshore platforms, and boutique AI specialists blur traditional boundaries. OpenAI and its February 2026 Frontier Alliance embed vendor engineers inside consulting teams at Accenture, Capgemini, McKinsey, and BCG, accelerating enterprise AI deployments and signaling an integrated delivery model that fuses product and advisory. Accenture’s acquisitions of Faculty and DLB Associates illustrate an industry playbook of buying specialized talent pools to shore up engineering depth and sector knowledge. IBM Consulting, Capgemini, and Cognizant are differentiating through proprietary generative-AI toolkits that automate code generation, policy drafting, and workflow orchestration, thereby compressing delivery timelines.

Mid-tier and niche firms are countering scale disadvantages by specializing in growth pockets such as SME AI adoption, litigation readiness, and middle-market succession planning. Value propositions center on agility, domain focus, and outcome-based pricing that resonates with budget-constrained buyers. At the same time, large corporate clients are staffing internal centers of excellence that absorb repeatable analytics and data-engineering work, forcing consultancies to emphasize higher-value governance, operating-model, and risk-management scopes. Wage inflation and talent scarcity remain shared pain points, propelling greater use of offshore, near-shore, and hybrid staffing approaches across the North America management consulting services market.

North America Management Consulting Services Industry Leaders

McKinsey & Company, Inc.

Deloitte Consulting LLP

Accenture plc

PricewaterhouseCoopers Advisory Services LLC

The Boston Consulting Group, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: OpenAI launched the Frontier Alliance with Boston Consulting Group, McKinsey, Accenture, and Capgemini to embed engineers inside consulting teams and accelerate enterprise AI deployments.

- January 2026: Accenture completed the acquisition of a 65% stake in DLB Associates Consulting Engineers to deepen its Industry X engineering capabilities.

- January 2026: Accenture agreed to acquire Faculty, a United Kingdom AI startup with 400 employees, adding the Frontier data-synthesis platform and naming Faculty’s CEO as Accenture chief technology officer.

- November 2025: PwC reported 10,333 United States deals worth USD 1.6 trillion through November 2025, with 74 megadeals exceeding USD 5 billion and more than 20% driven by AI themes.

North America Management Consulting Services Market Report Scope

The North America Management Consulting Services Market Report is Segmented by Consulting Service Line (Strategy Consulting, Operations Consulting, HR Consulting, Financial Advisory Consulting, Digital Transformation Consulting, Risk and Compliance Consulting, and Other Consulting Service Lines), Organization Size (Large Enterprises, and Small and Medium-Sized Enterprises), Delivery Model (On-Site Consulting, Remote and Virtual Consulting, and Hybrid Consulting), End User Industry (IT and Telecommunications, Manufacturing, Energy and Resources, Public Sector, Healthcare, Banking and Insurance, and Other End User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Strategy Consulting |

| Operations Consulting |

| HR Consulting |

| Financial Advisory Consulting |

| Digital Transformation Consulting |

| Risk and Compliance Consulting |

| Other Consulting Service Lines |

| Large Enterprises |

| Small and Medium-Sized Enterprises |

| On-Site Consulting |

| Remote and Virtual Consulting |

| Hybrid Consulting |

| IT and Telecommunications |

| Manufacturing |

| Energy and Resources |

| Public Sector |

| Healthcare |

| Banking and Insurance |

| Other End User Industries |

| United States |

| Canada |

| Mexico |

| By Consulting Service Line | Strategy Consulting |

| Operations Consulting | |

| HR Consulting | |

| Financial Advisory Consulting | |

| Digital Transformation Consulting | |

| Risk and Compliance Consulting | |

| Other Consulting Service Lines | |

| By Organization Size | Large Enterprises |

| Small and Medium-Sized Enterprises | |

| By Delivery Model | On-Site Consulting |

| Remote and Virtual Consulting | |

| Hybrid Consulting | |

| By End User Industry | IT and Telecommunications |

| Manufacturing | |

| Energy and Resources | |

| Public Sector | |

| Healthcare | |

| Banking and Insurance | |

| Other End User Industries | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

What is the current size of the North America management consulting services market and its projected growth?

The market reached USD 140.52 billion in 2025 and is forecast to rise to USD 174.38 billion by 2031, reflecting a 3.59% CAGR.

Which consulting service line is expanding the fastest in the region?

Digital transformation consulting is advancing at a 3.91% CAGR as enterprises embed AI and cloud-native architectures.

Why are Canadian consulting revenues growing more quickly than those in the United States?

Federal AI funding and SME voucher programs are accelerating digital adoption, supporting a 3.72% CAGR through 2031.

How are talent shortages affecting consulting firm profitability?

Severe competition for AI and data talent is inflating wages, compressing margins, and prompting hybrid staffing and automation.

What industries are generating the strongest demand for consulting services?

Banking and insurance command the largest spend share, while IT and telecommunications are projected to grow the quickest through 2031.

How are consulting firms responding to the rise of internal centers of excellence?

They are shifting toward higher-value governance and operating-model redesign work, while bundling managed services to stay embedded with clients.

Page last updated on: