US Quality Management Software Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 4.05 Billion |

| Market Size (2030) | USD 6.83 Billion |

| Growth Rate (2025 - 2030) | 11.02% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Quality Management Software Market Analysis by Mordor Intelligence

The US Quality management software market size reached USD 4.05 billion in 2025 and is projected to climb to USD 6.83 billion by 2030, reflecting an 11.02% CAGR over the period. This expansion reflects how regulated industries now view quality management systems as strategic levers that enhance efficiency, mitigate risk, and sharpen competitive positioning. Investments are flowing toward cloud platforms that shorten deployment cycles, while risk-based validation rules from the U.S. Food and Drug Administration (FDA) are accelerating the rollouts of life sciences.[1]U.S. Food and Drug Administration, “Computer Software Assurance for Production and Quality System Software,” fda.gov Growth also stems from the surge in interconnected “digital-thread” architectures that link quality, design, and manufacturing data, as well as generative AI tools that predict defects before they occur. Together, these forces position the Quality management software market for persistent double-digit growth as organizations seek real-time insight across complex supply chains.

Key Report Takeaways

- By deployment model, cloud-based platforms captured 59.7% share of the Quality management software market in 2024 and are projected to register an 11.9% CAGR through 2030.

- By solution type, document control led with 34.8% revenue share of the Quality management software market in 2024, while supplier quality management is forecast to expand at a 13.05% CAGR to 2030.

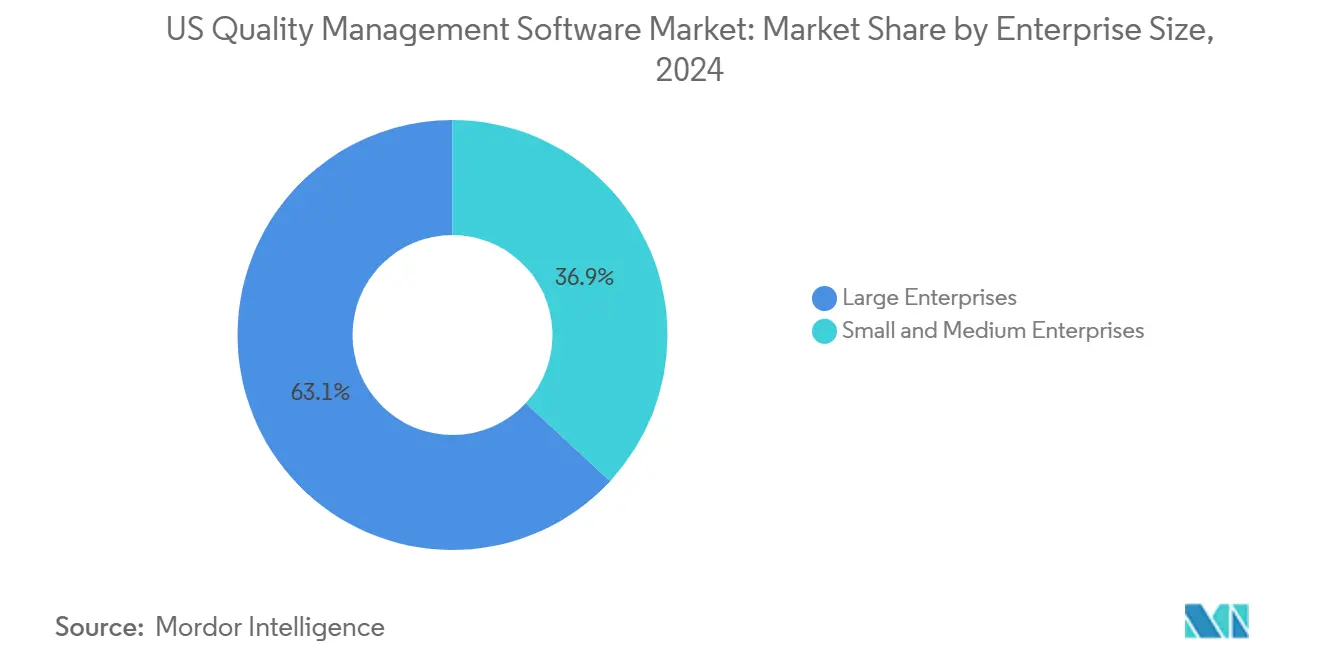

- By enterprise size, large enterprises held 63.1% share of the Quality management software market in 2024; small and medium enterprises represent the fastest segment with a 12.01% CAGR through 2030.

- By end-user industry, discrete manufacturing accounted for 32.02% of the 2024 spending in the Quality Management Software market, whereas healthcare and life sciences are poised to grow at a 13.81% CAGR through 2030.

- By region, the Midwest commanded a 38.88% share of the Quality management software market in 2024; the West Coast is set to deliver the highest regional growth at a 12.71% CAGR through 2030.

US Quality Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory-compliance burden in life-science and aerospace | +2.1% | Boston-Cambridge, San Francisco Bay Area, Seattle | Medium term (2-4 years) |

| Migration to cloud-based SaaS QMS platforms | +2.8% | West Coast tech corridors | Short term (≤ 2 years) |

| Digital-thread integration with ERP, PLM, MES | +1.9% | Midwest manufacturing belt, Southeast automotive corridor | Medium term (2-4 years) |

| Generative-AI predictive quality analytics | +1.6% | Technology and pharmaceutical hubs nationwide | Long term (≥ 4 years) |

| Reshoring-driven supply-chain transparency | +1.4% | Midwest and Southeast manufacturing regions | Medium term (2-4 years) |

| FDA Computer Software Assurance (CSA) final guidance | +1.2% | National life-sciences sector | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing regulatory-compliance burden in life-science and aerospace sectors

Medical-device makers must now align the FDA’s Quality Management System Regulation with ISO 13485, a convergence that prompts firms to adopt unified, enterprise-wide quality platforms. The FDA’s Medical Device Single Audit Program multiplies the need for harmonized processes, prompting manufacturers to replace fragmented tools with integrated systems that streamline audits and post-market surveillance. Aerospace suppliers face similar pressure from AS 9100 standards and cybersecurity mandates tied to defense programs. Quality data, therefore, plays a dual role: it meets compliance mandates and provides evidence for faster approval pathways. As a result, the Quality management software market gains momentum from sectors where quality spending represents 5-8% of operating budgets.

Accelerated migration to cloud-based SaaS QMS platforms

Cloud deployment trims implementation timelines from more than a year to as little as six months. Veeva Systems reports that 18 of the top 20 medical technology firms rely on its cloud Quality Suite, underscoring how subscription models shift quality from a capital expense to an operating expense.[2]Veeva Systems, “18 of the Top 20 MedTech Companies Partner with Veeva,” veeva.com Beyond lower up-front costs, cloud QMS offers automated upgrades that keep compliance current without IT disruption. For manufacturers with global plants, a single cloud instance also improves data integrity and ensures that audit trails remain intact during remote inspections. These factors explain the strong alignment between digital transformation roadmaps and the Quality management software market’s pivot to cloud delivery.

Digital-thread integration with ERP, PLM and MES ecosystems

Enterprises increasingly link design, production, and service data through a digital thread. When a QMS integrates with ERP and PLM, document retrieval time decreases, and training workflows become nearly frictionless. Siemens Digital Industries highlights U.S. growth driven by QMS modules that tie design verification directly to shop-floor execution. Such integration eliminates manual data re-entry and accelerates corrective-action cycles, enabling manufacturers to reduce quality-related costs to best-in-class levels, typically around 1.5% of revenue. The Quality management software market benefits as integration moves from “nice-to-have” to a purchasing requirement.

Generative-AI-powered predictive quality analytics

AI adoption leaped in 2024, with four in five manufacturers reporting measurable gains from machine-learning initiatives. Vendors such as ETQ embed algorithms that flag anomalies, automate root-cause analysis, and propose preventive actions before defects escape into the field. Cisco’s workforce study notes that quality-assurance roles now demand fluency in AI-assisted testing and prompt engineering skills.[3]Cisco, “AI-Enabled ICT Workforce Consortium Report,” cisco.com Early adopters credit AI modules with higher defect-detection accuracy and shorter inspection cycles, but they must also document algorithm performance for FDA scrutiny. These capabilities redefine quality as a forward-looking function, opening fresh addressable space for the Quality management software market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Up-front implementation and validation costs | -1.8% | SMEs in secondary manufacturing regions | Short term (≤ 2 years) |

| Data-security and IP-sovereignty concerns | -1.2% | Defense and pharmaceutical sectors | Medium term (2-4 years) |

| Shortage of certified quality-engineering talent | -0.9% | Specialized biotech and aerospace clusters | Long term (≥ 4 years) |

| Budget dilution from ESG-reporting overlap | -0.7% | Publicly traded manufacturing companies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Up-front implementation and validation costs

Even with SaaS pricing, mid-size manufacturers often spend 2-5% of their operating budgets on QMS projects that cover configuration, data migration, and validation. While the FDA’s CSA guidance eases paperwork, firms must still generate risk assessments and maintain evidence that software performs as intended. Costs scale with global scope, making enterprise rollouts a multi-million-dollar undertaking across diverse regulatory regimes.

Persistent data-security and IP-sovereignty concerns

Ransomware incidents have forced executives to weigh the risk of exposing proprietary process data in cloud environments. Manufacturing USA reported that more than half of U.S. plants faced cyberattacks in 2023.[4]Manufacturing USA, “Manufacturing USA 2023 Annual Report,” dodmantech.mil In sectors such as defense or biologics, data-location rules limit where quality data may reside, complicating global cloud strategies and slowing the Conversion of Quality management software markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Model: Cloud dominance accelerates digital transformation

Cloud platforms controlled 59.7% of the Quality management software market in 2024 and are forecast to log an 11.9% CAGR to 2030. This uptake comes from lower total cost of ownership, automatic version updates, and faster validation under the FDA’s CSA rule. On-premise installations persist where sovereignty or customization demands remain high, yet their share erodes as cybersecurity certifications and FedRAMP authorizations expand.

Cloud adoption also aligns with broader enterprise moves toward composable ERP, enabling APIs to pull high-quality data into finance and supply-chain dashboards in real-time. Vendors differentiate themselves by offering hybrid blueprints that stage gradual migrations, allowing plants to run on-premise modules while headquarters transition to multi-tenant SaaS. The Quality management software market benefits because each cloud upgrade introduces analytics add-ons and mobile apps that were cost-prohibitive in legacy environments.

By Solution Type: Document control leadership faces supplier-quality disruption

Document control remains essential, holding a 34.8% market share in the Quality Management software market in 2024. It anchors compliance by managing procedures, drawings, and controlled forms. Yet, supplier quality solutions outpace all other modules at a 13.05% CAGR, mirroring the rise of multi-tier supply chain oversight. Cloud portals now push corrective-action workflows directly to suppliers, shortening cycle times and cutting non-conformance risk.

Training management, audit management, and CAPA modules also expand as AI suggestions populate training curricula and auto-generate audit checklists. This convergence leads customers to favor integrated suites rather than best-of-breed point products. As suites spread, the Quality management software market size tied to cross-module packages grows faster than any single module alone.

By Enterprise Size: SME acceleration challenges large-enterprise dominance

Large enterprises commanded 63.1% of the Quality management software market revenue in 2024, aided by existing ERP links and global rollouts that routinely cross the USD 1 million mark. These projects incorporate advanced analytics and IoT sensor feeds, providing plants with near-real-time statistical-process-control dashboards.

Small and medium enterprises, however, are growing at a 12.01% CAGR as subscription pricing lowers entry barriers. Vendors offer guided implementation templates tailored to ISO 9001 and FDA Part 820, enabling SMEs to deploy in weeks without dedicated IT staff. ROI emerges quickly as defect rates fall and customer-audit scores climb, making word-of-mouth a potent catalyst within local supply chains.

By End-User Industry: Manufacturing strength meets healthcare innovation

Discrete manufacturing held 32.02% of 2024 spending, led by automotive, aerospace, and industrial equipment plants that require statistically rigorous records to satisfy both regulators and customers. High-mix production and electrification trends add complexity, prompting factories to adopt AI-driven inspections that plug directly into QMS dashboards.

Healthcare and life sciences will expand faster than all other verticals at a 13.81% CAGR. New combination-product rules and ISO 13485 harmonization fuel demand for unified platforms that consolidate design history files, validation evidence, and complaint trending. Technology and telecom firms also adopt QMS as code releases become continuous, necessitating automated software quality gates. Food and beverage manufacturers deploy modules that align with the Food Safety Modernization Act, while defense contractors integrate QMS with cybersecurity compliance records required by federal buyers.

Geography Analysis

The Midwest leads the Quality management software market with a 38.88% share in 2024. Michigan’s auto plants, Ohio’s machinery workshops, and Illinois’s food processors rely on integrated quality suites to safeguard complex, just-in-time supply chains. Manufacturers in this region leverage workforce upskilling grants and cybersecurity toolkits from Manufacturing USA programs to mesh QMS data with broader digital-factory platforms. At the same time, these strengths anchor adoption; however, aging facilities and workforce retirements may temper long-term momentum unless capital spending accelerates.

The West Coast posts the fastest growth, at 12.71% CAGR. Life sciences firms in California prefer cloud deployments that scale globally without local servers. Aerospace primes in Washington integrate generative AI modules that parse warranty data in real-time, gaining early-warning insight into field issues. Technology-sector norms promote API-first architectures, so quality events are instantly fed into service and product lifecycle dashboards. Venture funding further fuels the Quality management software market as investors mandate robust quality infrastructures before late-stage rounds.

The Northeast shows steady gains, given its high biotech density and the concentration of medical-device makers in Massachusetts and New Jersey. The South benefits from reshoring; new EV battery plants in Tennessee and Alabama deploy QMS suites that link directly to supplier portals. Together, these patterns illustrate how localized regulatory, supplier, and talent ecosystems direct the demand trajectories for quality management software markets.

Competitive Landscape

The Quality management software market features moderate concentration, with diversified enterprise platforms standing alongside niche specialists and AI-centric newcomers. Microsoft, SAP, and Oracle leverage their broad ERP footprints to bundle QMS into comprehensive digital core offerings. Veeva Systems, MasterControl, and ETQ maintain strongholds in the life sciences by delivering pre-configured templates that are validated to FDA and ISO standards.

Competition intensifies along three lines. First, platform consolidation: Clarivate’s April 2024 acquisition of Global QMS expanded its regulatory-intelligence portfolio into manufacturing quality workflows. Second, vertical specialization: Greenlight Guru caters solely to medical device startups that need quick ISO 13485 compliance. Third, technology differentiation: vendors release AI modules that recommend corrective actions or simulate defect propagation through digital twins.

Market share shifts as cloud adoption lowers switching costs and buyers place a higher weight on user experience, analytics depth, and validation speed. Partnerships with hyperscale cloud providers enable rapid regional expansion, while FedRAMP or HITRUST certifications open doors to government and healthcare customers. With mid-tier players capturing SMEs and global majors anchoring multi-plant rollouts, the Quality management software market rewards vendors that balance compliance rigor with agile product roadmaps.

US Quality Management Software Industry Leaders

AssurX Inc.

ComplianceQuest Inc.

Cority Software Inc.

Dassault Systèmes SE

Dot Compliance Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Microsoft launched a low-code QMS connector for Power Platform, enabling citizen developers to build quality dashboards that pull live data from Dynamics 365.

- September 2024: Veeva Systems expanded Vault QMS to include field-action and recall workflows for medical-technology firms, integrating device traceability with regulatory reporting.

- August 2024: Veeva Vault LIMS gained adoption as life sciences companies converged QA and QC data in one cloud workspace.

- August 2024: Clarivate acquired Global QMS, adding Optiqs360’s workflow engine and MediGPT AI to its life-sciences compliance suite.

US Quality Management Software Market Report Scope

| Cloud-Based |

| On-Premise |

| Document Control |

| Audit Management |

| CAPA / Non-conformance |

| Supplier Quality Management |

| Training Management |

| Large Enterprises |

| Small and Medium Enterprises |

| Discrete Manufacturing |

| Healthcare and Life Sciences |

| Aerospace and Defense |

| IT and Telecom |

| Food and Beverage |

| Other End-User Industries |

| Northeast |

| Midwest |

| South |

| West |

| By Deployment Model | Cloud-Based |

| On-Premise | |

| By Solution Type | Document Control |

| Audit Management | |

| CAPA / Non-conformance | |

| Supplier Quality Management | |

| Training Management | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Discrete Manufacturing |

| Healthcare and Life Sciences | |

| Aerospace and Defense | |

| IT and Telecom | |

| Food and Beverage | |

| Other End-User Industries | |

| By Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the 2025 value of the U.S. Quality management software market?

The market stands at USD 4.05 billion in 2025.

How fast is cloud deployment growing within quality systems?

Cloud solutions are projected to expand at an 11.9% CAGR through 2030.

Which solution segment is growing the quickest?

Supplier quality management modules lead with a 13.05% CAGR.

Why is the life-sciences sector adopting QMS rapidly?

New FDA regulations and ISO 13485 alignment require unified, validated quality platforms.

Which U.S. region shows the highest market growth?

The West Coast is forecast to grow at a 12.71% CAGR through 2030.

Page last updated on: