Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 77.53 Billion |

| Market Size (2031) | USD 95.49 Billion |

| Growth Rate (2026 - 2031) | 4.25% CAGR |

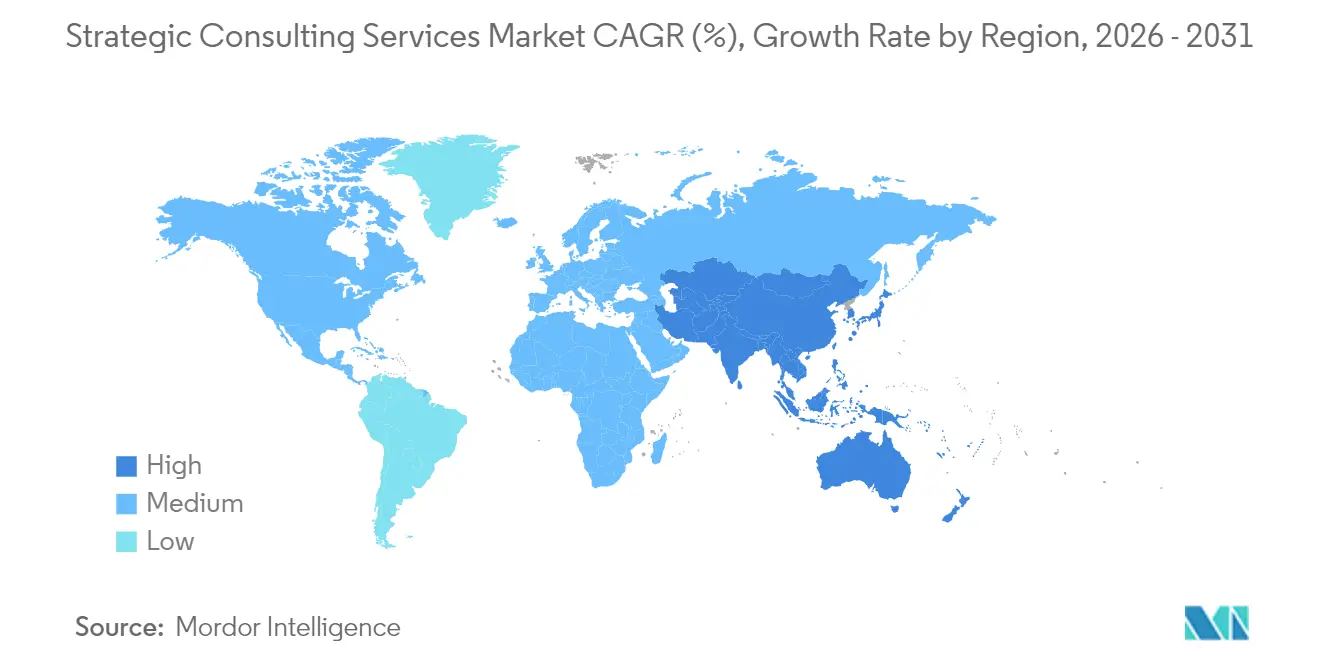

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Strategic Consulting Services Market Analysis by Mordor Intelligence

The strategic consulting services market size is expected to grow from USD 74.37 billion in 2025 to USD 77.53 billion in 2026 and is forecast to reach USD 95.49 billion by 2031 at 4.25% CAGR over 2026-2031. The measured growth reflects a maturing sector navigating widespread artificial-intelligence deployment, proliferating regulatory requirements, and rising client expectations for outcome-based engagements. Enterprise digital-transformation budgets remain the primary catalyst, with 72% of digital leaders planning higher 2025 spending that channels advisory demand toward AI governance and change-management roadmaps.[1]Marc Zao-Sanders, “How AI Can Change the Way Your Company Gets Work Done,” Harvard Business Review, hbr.org In parallel, the global M&A pipeline swelled to nearly USD 3.5 trillion in 2024, increasing complexity in cross-border integrations and fueling transaction advisory revenue streams.[2]Marc Zao-Sanders, “How AI Can Change the Way Your Company Gets Work Done,” Harvard Business Review, hbr.org Competitive intensity is elevated as boutique specialists, independent freelancers, and AI-powered platforms erode the historic dominance of large firms. These pressures are accelerating outcome-based pricing adoption, platform-enabled delivery, and talent model reinvention across the strategic consulting services market.

Key Report Takeaways

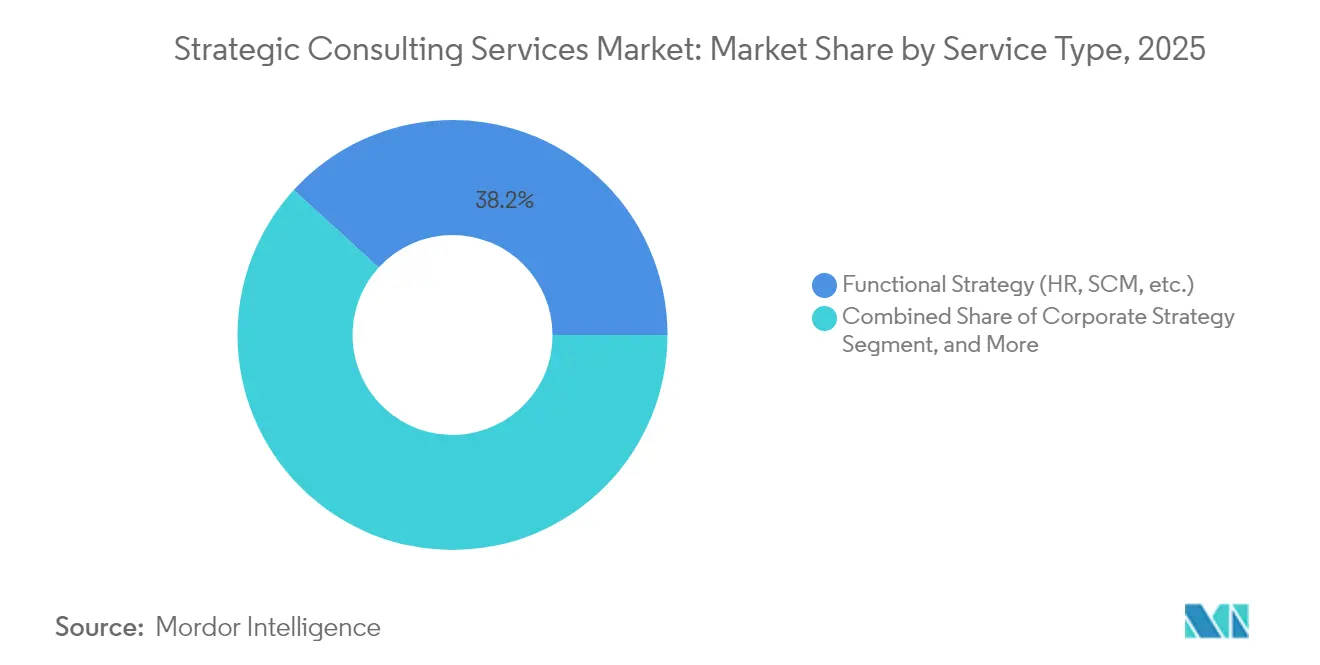

- By service type, functional strategy consulting commanded 38.22% of strategic consulting services market share in 2025, while digital strategy consulting recorded the fastest 4.67% CAGR through 2031.

- By organization size, large enterprises held 62.32% of the strategic consulting services market in 2025, whereas small enterprises are projected to grow at a 5.28% CAGR to 2031.

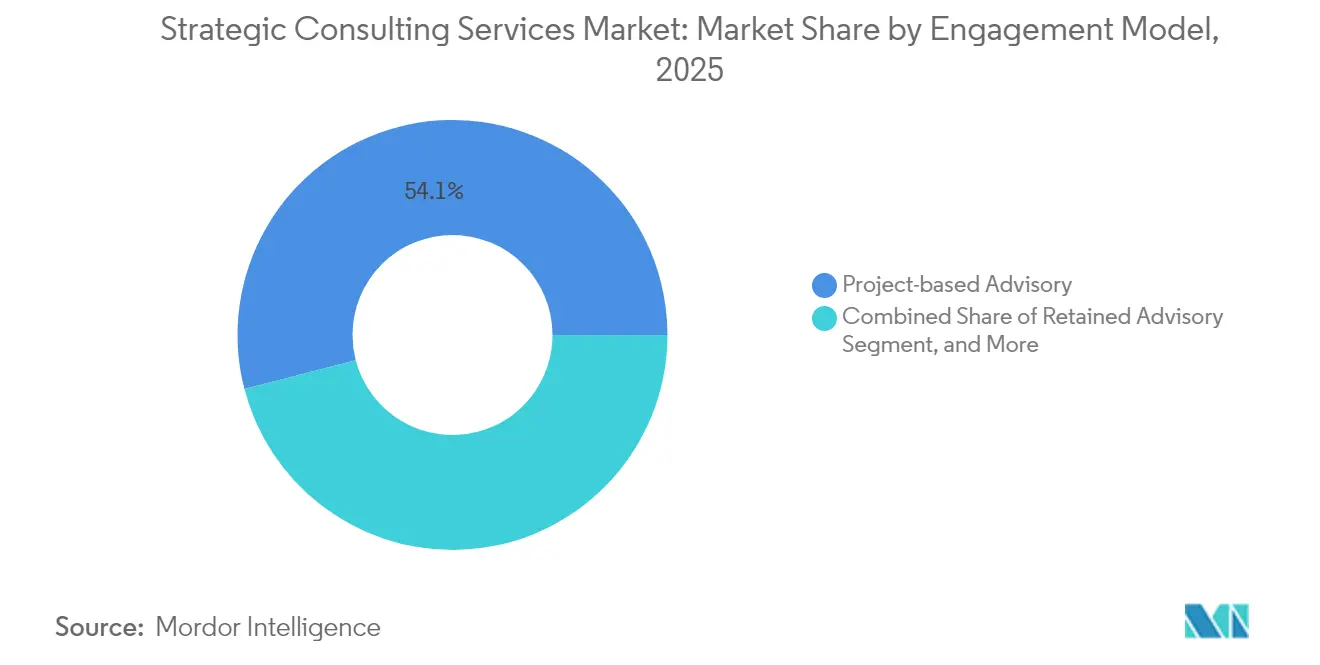

- By engagement model, project-based advisory accounted for 54.05% of the strategic consulting services market size in 2025, and outcome-based consulting is expanding at a 5.15% CAGR over the forecast period.

- By end-user industry, financial services led with 29.63% revenue share in 2025 in the strategic consulting services market and healthcare and life sciences is expected to exhibit the highest growth momentum through 2031.

- By geography, North America captured 36.55% share of the strategic consulting services market in 2025, while Asia Pacific is forecast to post the strongest 4.82% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Strategic Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital-transformation spend by enterprises | +1.2% | Global, with APAC and North America leading | Medium term (2-4 years) |

| Rising global M&A pipeline and integration complexity | +0.8% | North America and Europe, spill-over to APAC | Short term (≤ 2 years) |

| Regulatory and compliance proliferation across regions | +0.6% | Global, with EU and North America core | Long term (≥ 4 years) |

| SME demand for external strategic expertise | +0.5% | Global, with emerging markets acceleration | Medium term (2-4 years) |

| Generative-AI governance and strategy mandates | +0.4% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Geopolitical fragmentation driving near-shoring strategies | +0.3% | Global, with supply chain-dependent regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Digital-Transformation Spend by Enterprises

Enterprise investment in digital overhauls sustains advisory pipelines as organizations grapple with cloud migration, AI adoption, and broad operating-model redesign. IT services outlays climbed to USD 1.52 trillion in 2024, a 9.7% rise that translated into higher demand for consultants capable of bridging strategic road-mapping with implementation. Consulting firms are now monetizing premium AI-strategy engagements, coupling governance frameworks with workforce-reskilling programs. Digital leaders, those already capturing value from analytics, are 72% likelier to lift 2025 transformation budgets, ensuring recurring advisory revenue. Yet generative-AI tooling increasingly automates baseline research, compelling firms to shift junior talent toward synthesis, change-management, and client enablement. The dynamic pressures firms to elevate value-creation narratives while controlling cost structures through proprietary AI platforms.

Rising Global M&A Pipeline and Integration Complexity

Deal advisory momentum strengthened as worldwide transaction value neared USD 3.5 trillion in 2024, expanding 15% year over year and intensifying demand for strategy consultants skilled in diligence and integration. Cross-border deals face heightening regulatory scrutiny, data-sovereignty rules, and cultural integration hurdles, pushing firms to deploy AI-enabled diligence tools that compress document-review cycles by 30%. Geopolitical uncertainty adds strategic-scenario requests on antitrust clearances and stakeholder communications. Technology and healthcare deals, governed by specialized regulations, further boost advisory workloads among firms holding deep sector expertise. As private-equity dry powder persists, consultants expect a steady pipeline of carve-out and platform-roll-up assignments through 2026.

Regulatory and Compliance Proliferation Across Regions

Ever-evolving rulesets, spanning the EU’s AI Act, DORA resilience mandates, and Basel III capital standards, force organizations to seek external expertise. Consulting demand intensifies in financial services, where overlapping obligations necessitate risk-mitigation roadmaps and operational-resilience testing. Healthcare clients require navigation of FDA digital-therapeutics guidelines and value-based-care reimbursement frameworks. ESG reporting has become a compliance priority for energy and manufacturing players planning decarbonization and renewables investment. Firms with regulatory-focused practices monetize premium day rates and multi-year managed-compliance contracts. The fragmented regulatory landscape also raises barriers to entry, advantaging incumbents with established relationships across supervisory authorities.

SME Demand for External Strategic Expertise

Small and midsize companies now tap fractional consulting models to close capability gaps caused by accelerated technology disruption. SME-oriented engagements are forecast to grow at 5.45% CAGR, driven by AI adoption hurdles, digital-commerce pivots, and succession-planning needs that exceed in-house capacity. Independent consultants and specialized boutiques win share by offering bespoke solutions at competitively lower cost than large firms. Outcome-based pricing resonates with budget-constrained owners, aligning fees with realized performance improvements. Despite shorter project cycles and smaller ticket sizes, scalable delivery frameworks and SaaS-enabled toolkits allow providers to defend profitability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of in-house strategy teams | -0.7% | Global, with large enterprises in North America and Europe leading | Medium term (2-4 years) |

| Talent drain to the independent consultant economy | -0.4% | North America and Europe core, spill-over to APAC | Short term (≤ 2 years) |

| Procurement-led fee pressure and outcome pricing | -0.3% | Global, with mature markets experiencing highest pressure | Medium term (2-4 years) |

| DIY-strategy analytics enabled by Gen-AI tools | -0.2% | North America and Europe early adoption, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of In-House Strategy Teams

Large corporations increasingly recruit ex-consultants to head internal strategy units, reducing reliance on external advisors. AI-augmented analytics platforms now equip internal teams to replicate baseline market-research tasks, challenging firms to justify premium fees. Consultants respond by emphasizing implementation rigor, change-leadership expertise, and objective viewpoint. Hybrid engagement models that blend in-house capabilities with external specialization are emerging, though margins tighten as clients negotiate scope faster and insist on knowledge transfer.

Talent Drain to the Independent Consultant Economy

The freelance shift siphons seasoned principals and partners into the USD 1.5 trillion skilled-independent economy, where 54% claim advanced AI proficiency.[3]Upwork Research Institute, “Future Workforce Index 2025,” upwork.com Departing leaders leverage established relationships to compete directly, often undercutting legacy-firm pricing. Traditional firms counter with higher remuneration, equity schemes, and flexible work policies, but retention remains a structural risk. Client perception of equal expertise at lower cost further intensifies pricing pressure on bundled firm offerings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Strategy Drives Growth

Functional strategy services dominated 2025 revenue with 38.22% strategic consulting services market share, encompassing HR restructuring, supply-chain optimization, and lean-operations programs. Demand persists as core efficiency agendas remain board priorities. Digital strategy, however, is the fastest-expanding niche at a 4.67% CAGR, fueled by AI-integration roadmaps, data-monetization blueprints, and cloud-migration synchronization with business objectives. M&A and corporate-finance advisory also ride the elevated deal cycle, while economic-policy strategy grows as clients seek geopolitical risk hedging.

Digital-first work requires consultants to deliver technology and business acumen concurrently, changing talent mixes toward data scientists and product managers. Boutique specialists exploit the complexity by targeting single-domain pain points, challenging full-service incumbents. To protect share, global firms package multi-disciplinary “one-stop” offerings and invest in proprietary AI tools that compress research cycles and elevate synthesis quality.

By Organization Size: SME Growth Accelerates

Large enterprises retained a commanding 62.32% revenue contribution in 2025, leveraging consultants for global transformation, regulatory programs, and portfolio-diversification moves. Yet small enterprises are generating the strongest 5.28% CAGR as democratized access to cloud-based advisory platforms compresses traditional cost barriers. The strategic consulting services market size for SME engagements is projected to eclipse USD 20 billion by 2031, reflecting a broadening client base as digital literacy improves.

Providers now emphasize modular playbooks and templated project artifacts to keep scope lean and pricing transparent. Independent consultants thrive in this space, often partnering with SaaS vendors to blend technology and advisory into subscription bundles. The shift forces large firms to establish dedicated mid-market units with right-sized delivery models to preserve future growth.

By Engagement Model: Outcome-Based Models Gain Momentum

Project-based work still produced 54.05% of 2025 billings, sustaining its role as the standard contracting format for discrete strategy questions. The strategic consulting services market size for outcome-based agreements is, however, set to climb swiftly on a 5.15% CAGR, mirroring client insistence on measured value realization. Such contracts peg fees to EBITDA upticks, cost-savings milestones, or revenue-growth thresholds, transferring risk to advisors but offering upside when goals are exceeded.

Digital-platform delivery supplements both models by automating data collection, benchmarking, and progress tracking, enabling real-time visibility into engagement outcomes. Managed-services models also gain appeal as clients offload end-to-end functions, such as regulatory reporting, under multi-year contracts. Providers that mature measurement frameworks and accept variable compensation stand to capture loyalty premiums.

By End-User Industry: Financial Services Leads Demand

Financial institutions accounted for 29.63% of 2025 revenue as regulatory reforms, DORA, Basel III, and emerging AI mandates, mandated seasoned compliance counsel. The strategic consulting services industry is further buoyed by fintech disruptions and open-banking rollouts that require holistic digital-platform strategies. Healthcare and life sciences represent the fastest-advancing vertical on the back of accelerated R&D digitization, AI-supported clinical-trial orchestration, and value-based-care models.

Technology, media, and telecom assignments focus on platform-design and cybersecurity resilience, whereas energy clients seek ESG-aligned transition planning. Government demand grows around digital-services modernization and policy-impact assessment. Consultants with sector-specific data sets and regulatory credentials are best placed to secure repeat mandates.

Geography Analysis

North America retains leadership owing to deep client pockets, complex regulatory architectures, and record M&A activity that collectively sustain advisory pipelines. Financial-services firms pursue operational-resilience programs under DORA guidelines, while technology giants demand AI-ethics playbooks. Defense-sector contract scrutiny poses a downside threat, with federal reviews potentially curbing consulting spend.

Asia Pacific is the fastest-growing market, buoyed by government digitalization schemes, mid-market enterprise expansion, and infrastructure megaprojects. China drives demand through tech-sovereignty initiatives and diversification strategies, whereas India’s digital-payments and public-sector modernization create steady advisory flows. Japan and Australia sustain mature spend profiles emphasizing operational excellence and advanced-manufacturing transformation.

Europe offers resilient opportunity anchored in regulatory-compliance advisory, sustainability road-mapping, and cross-border integration support. Germany’s industrial base underpins Industry 4.0 consulting, the U.K. leverages financial-services depth, and France, Netherlands, and the Nordics add steady demand for digital-operations modernization. BCG’s 2024 launch of a dedicated Center for Geopolitics signals continued emphasis on macro-risk counsel

Competitive Landscape

Incumbent strategy houses, McKinsey, BCG, and Bain, maintain brand primacy but confront mounting share erosion from Big Four multifaceted offerings, sector-focused boutiques, and a surging independent-talent pool. Proprietary AI platforms, such as McKinsey’s “Lilli,” integrate a century of intellectual property to cut delivery cycles, improving margin leverage on fixed-fee contracts.[4]Mackenzie Ferguson, “McKinsey's Lilli: The AI Revolutionizing Consulting,” opentools.ai BCG’s “Deckster” automation engine and Bain’s Vector digital suite follow similar trajectories.

Boutiques differentiate through hyper-specialization, cyber-resilience, AI risk, climate-strategy, and capturing clients that favor depth over scale. Independent consultants generated USD 1.5 trillion in 2024, illustrating a meaningful wallet shift toward flexible expertise. Outcome-based contracting and digital-first delivery compress cost structures, placing further pressure on traditional billable-hour economics.

Firms expanding into the managed-services space secure annuity revenue while reinforcing technology partnerships across cloud, analytics, and cybersecurity vendors. Accenture’s acquisition of Maryville Consulting Group in July 2025 exemplifies portfolio deepening aimed at end-to-end transformation stewardship. As AI commoditizes baseline analysis, sustained differentiation will hinge on proprietary data assets, domain-specific accelerators, and measurable value delivery.

Strategic Consulting Services Industry Leaders

Ernst & Young Global Limited

Accenture plc

Deloitte Consulting LLP

Boston Consulting Group, Inc.

Bain & Company, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Business Insider warned of a potential decade-long reduction in consulting headcount across levels as AI automates foundational tasks.

- August 2025: The Economist assessed McKinsey’s strategic crossroads approaching its centenary, citing competitive and reputational challenges.

- July 2025: Accenture acquired Maryville Consulting Group, strengthening specialized strategic-advisory depth.

- June 2025: McKinsey introduced its proprietary AI platform “Lilli,” automating core research and presentation tasks.

Global Strategic Consulting Services Market Report Scope

The strategic consulting services market forms a sub-set of overall consulting that focuses on the development of corporate, functional, and organizational strategies. The scope of the study is limited to tracking the revenue generated through strategy consulting services in the domains of corporate strategy, business model transformation, economic policy, mergers and acquisitions, organizational strategy, functional strategy, strategy and operations, and digital strategy.

By Service Type

| Corporate Strategy |

| Business-Model Transformation |

| MandA and Corporate Finance Strategy |

| Digital Strategy and Innovation |

| Functional Strategy (HR, SCM, etc.) |

| Economic and Policy Advisory |

By Organization Size

| Large Enterprises |

| Medium Enterprises |

| Small Enterprises |

By Engagement Model

| Project-based Advisory |

| Retained Advisory |

| Managed / Implementation Services |

| Outcome-based / Success-fee Consulting |

| Digital / Platform-enabled Consulting |

By End-user Industry

| Financial Services |

| Life Sciences and Healthcare |

| Technology, Media and Telecom |

| Energy and Resources |

| Government and Public Sector |

| Consumer and Retail |

| Industrial and Manufacturing |

| Other End-user Industries |

By Geography

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Argentina | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Netherlands | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East and Africa | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Corporate Strategy | ||

| Business-Model Transformation | |||

| MandA and Corporate Finance Strategy | |||

| Digital Strategy and Innovation | |||

| Functional Strategy (HR, SCM, etc.) | |||

| Economic and Policy Advisory | |||

| By Organization Size | Large Enterprises | ||

| Medium Enterprises | |||

| Small Enterprises | |||

| By Engagement Model | Project-based Advisory | ||

| Retained Advisory | |||

| Managed / Implementation Services | |||

| Outcome-based / Success-fee Consulting | |||

| Digital / Platform-enabled Consulting | |||

| By End-user Industry | Financial Services | ||

| Life Sciences and Healthcare | |||

| Technology, Media and Telecom | |||

| Energy and Resources | |||

| Government and Public Sector | |||

| Consumer and Retail | |||

| Industrial and Manufacturing | |||

| Other End-user Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Argentina | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Netherlands | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East and Africa | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the strategic consulting services market?

The market stands at USD 77.53 billion in 2026 and is projected to hit USD 95.49 billion by 2031, growing at a 4.25% CAGR.

Which region is expanding the fastest in strategic consulting?

Asia Pacific is forecast to grow at a 4.82% CAGR through 2031 on the back of large-scale digital initiatives and rising mid-market adoption of advisory services.

Which service line is gaining the most traction?

Digital strategy consulting is the fastest-growing segment, advancing at a 4.67% CAGR as companies prioritize AI governance and technology-integration roadmaps.

How are engagement models evolving?

Outcome-based consulting is advancing on a 5.15% CAGR because clients favor fee structures tied to measurable business results.

What major factor restrains market growth?

The expansion of in-house strategy teams is eroding external spend, exerting a -0.7% drag on forecast CAGR.

Page last updated on: