Marketing Consulting Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 36.65 Billion |

| Market Size (2031) | USD 45.52 Billion |

| Growth Rate (2026 - 2031) | 4.42% CAGR |

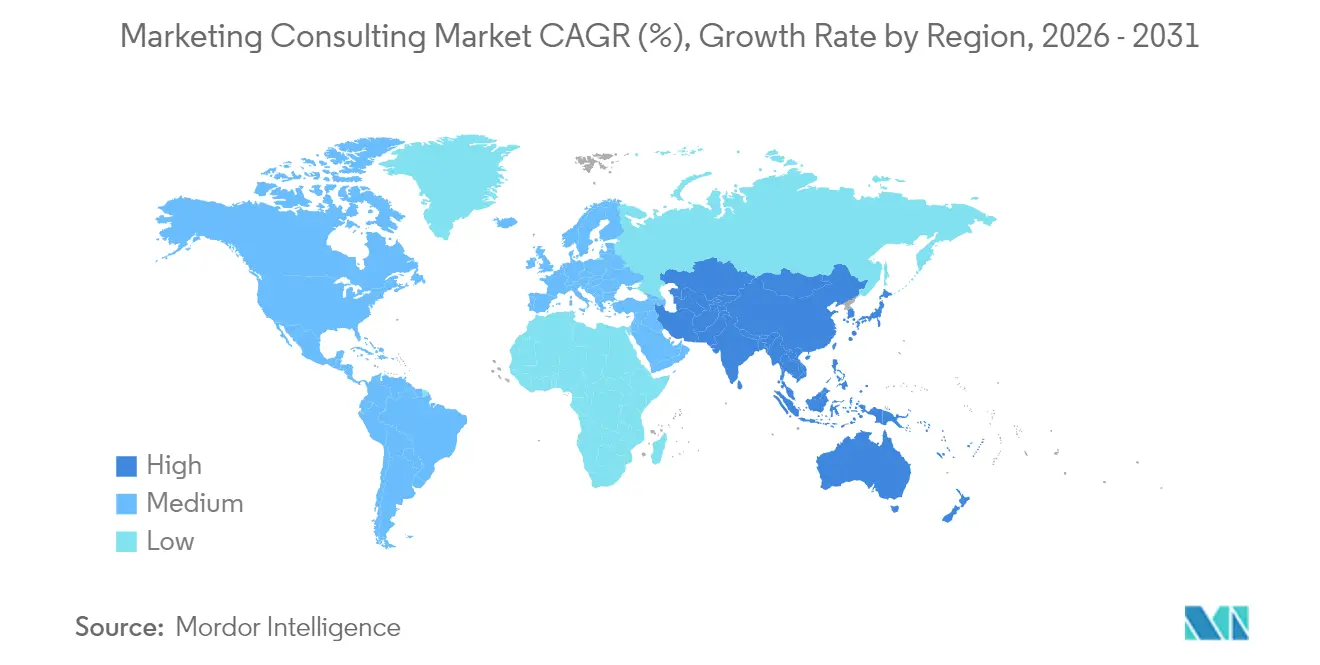

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

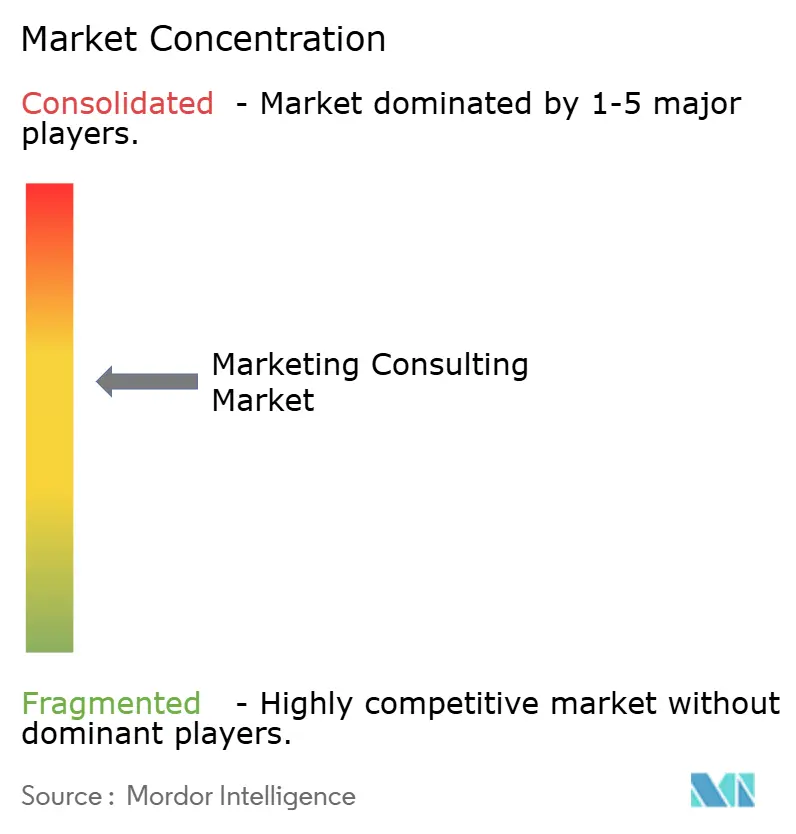

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Marketing Consulting Market Analysis by Mordor Intelligence

Marketing Consulting Market size in 2026 is estimated at USD 36.65 billion, growing from 2025 value of USD 35.10 billion with 2031 projections showing USD 45.52 billion, growing at 4.42% CAGR over 2026-2031. Demand is fueled by enterprises racing to integrate artificial intelligence into omnichannel strategies, comply with rapidly tightening privacy laws, and shift to outcome-based remuneration for agencies. Increasing reliance on zero-party data frameworks, the formalization of prompt-engineering advisory services, and widening adoption of hybrid consulting delivery models reinforce the market’s upward trajectory. Competitive intensity is rising as established management consultancies invest in proprietary martech stacks while AI-native specialists unlock new efficiencies for small and medium-sized clients. Despite budget vigilance in some verticals, consulting engagements tied to revenue accountability and compliance assurance continue to secure board-level sponsorship across geographies.

Key Report Takeaways

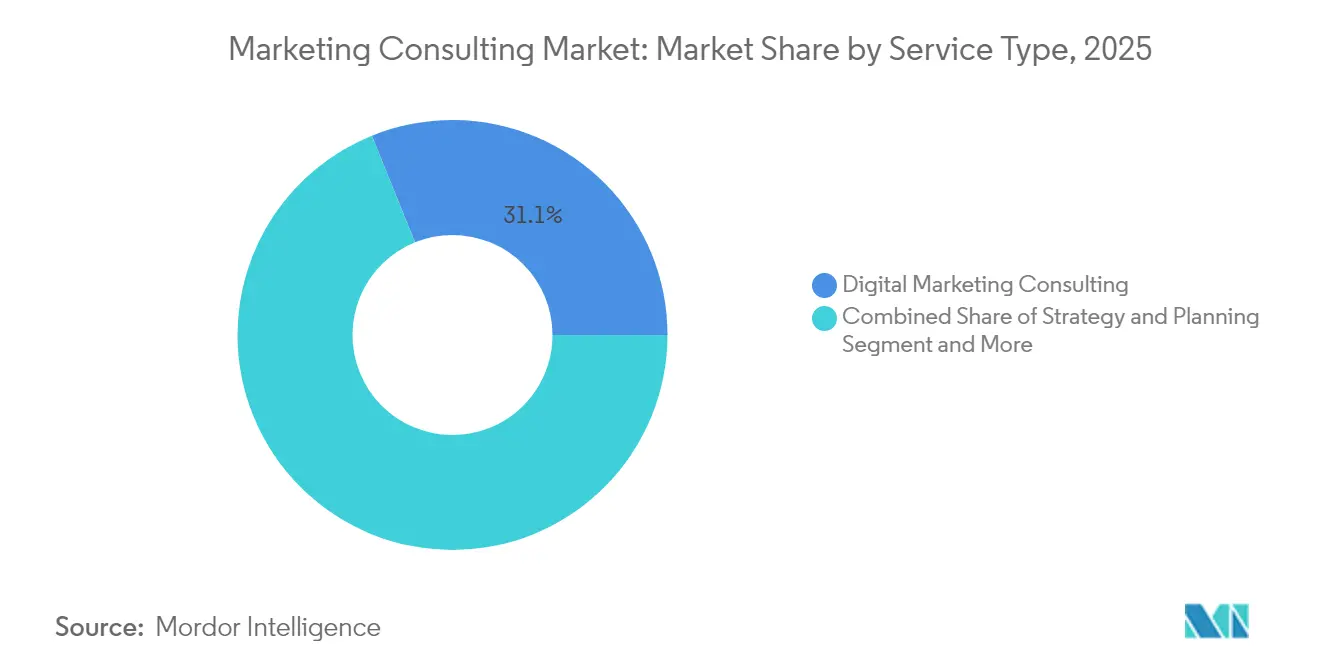

- By service type, digital marketing consulting led with 31.12% marketing consulting market share in 2025, while CX/personalization consulting is forecast to register the highest 6.39% CAGR through 2031.

- By end-user industry, retail and consumer goods dominated at 28.24% share in 2025; technology and media are projected to expand fastest at 6.23% CAGR to 2031.

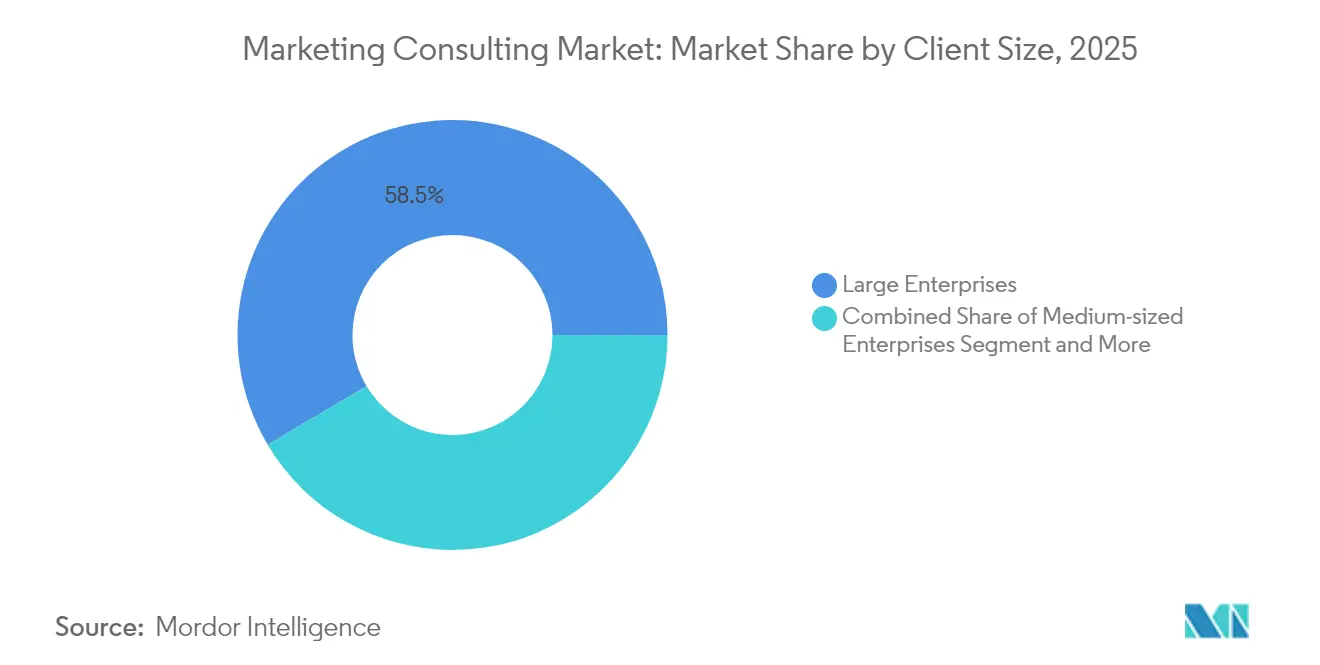

- By client size, large enterprises captured 58.53% of the marketing consulting market in 2025, whereas small and micro enterprises/start-ups are expected to grow at a 6.62% CAGR.

- By engagement model, project-based contracts held a 54.11% share in 2025, while outcome-based/risk-sharing agreements are set to climb at a 6.55% CAGR.

- By delivery mode, on-site consulting accounted for a 52.86% share in 2025; hybrid delivery is anticipated to progress at a 6.78% CAGR over the forecast period.

- By geography, North America contributed 37.21% of 2025 revenue, whereas Asia-Pacific is poised for the strongest 6.47% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Marketing Consulting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for digital transformation of marketing functions | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Increasing focus on customer personalization and data-driven decisions | +0.9% | Global, strongest in APAC and North America | Long term (≥ 4 years) |

| Rapid growth of omnichannel commerce ecosystems | +0.8% | Global, led by APAC retail markets | Medium term (2-4 years) |

| Emergence of zero-party data consulting post-privacy regulations | +0.7% | North America and EU primary, expanding globally | Short term (≤ 2 years) |

| CMOs adopting outcome-based remuneration models | +0.5% | North America and Europe, emerging in APAC | Long term (≥ 4 years) |

| Surge in AI prompt-engineering advisory for content generation | +0.4% | Global, technology sector leading adoption | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Digital Transformation of Marketing Functions

Enterprise marketing teams are restructuring their operating models to synchronize martech stacks, converge paid-owned-earned channels, and pivot from historical campaign calendars to always-on growth engines. Implementation of advanced customer data platforms, real-time attribution models, and privacy-compliant measurement frameworks requires external specialists with deep system-integration skills. Financial services firms in the United States now earmark up to 18% of total marketing spend for digital acceleration projects that demand third-party expertise. [1]Slaughter and May, “Why 2025 Is the Year to Refresh Your Marketing Compliance,” slaughterandmay.com Continuous platform upgrades and the growing complexity of consent-management tooling ensure that the marketing consulting market secures multi-year transformation mandates. As a result, consultants capable of unifying data, creative, and technology disciplines report stronger retention rates and higher project pipelines.

Increasing Focus on Customer Personalization and Data-driven Decisions

Organizations are transitioning from broad demographic segmentation toward algorithmic individualization that optimizes conversion in real time. Brands with diversified product portfolios manage millions of unique customer profiles that trigger personalized content across web, mobile, and in-store touchpoints. The technical lift involves identity resolution, predictive modeling, and creative automation that exceeds most in-house capabilities. Consulting firms assemble cross-functional squads combining data scientists, UX strategists, and performance media experts to design the underlying architecture. Heightened board-level scrutiny on first-party data governance further cements demand for external guidance on privacy-centric data activation, keeping the marketing consulting market ahead of purely in-house alternatives.

Rapid Growth of Omnichannel Commerce Ecosystems

Retailers, quick-service restaurants, and direct-to-consumer brands now treat physical locations as data-rich media assets. In 2025, a national pharmacy chain rolled out intent-based digital signage across 9,000 stores to boost basket size and shopper satisfaction. Replicating such initiatives at scale requires journey mapping, behavioral analytics, and edge-device orchestration skills that remain scarce internally. Consulting partners provide the playbooks to harmonize messaging, optimize inventory visibility, and integrate payment flows, thereby capturing incremental spend from omnichannel consumers. This structural shift supports sustained growth for firms that bridge store, mobile, and social commerce environments.

Emergence of Zero-party Data Consulting Post-privacy Regulations

The deprecation of third-party cookies in mainstream browsers and the enforcement of stringent opt-in regimes compel marketers to rethink data strategies. Advisories now guide clients through Privacy Sandbox API implementation, dynamic consent management, and new attribution logic absent cross-site identifiers. [2]Osano editorial team, “Google's Cookie Deprecation: What to Know About Chrome's Data Collection,” osano.com Engagement scopes often extend to customer-value-exchange design and governance audits that demonstrate compliance to regulators and audit committees. The accelerating patchwork of regional privacy laws underpins resilient demand for legal-technology crossover skill sets, reinforcing positive outlooks for the marketing consulting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing competition from in-house teams and automation platforms | -0.8% | Global, strongest impact in technology and retail sectors | Medium term (2-4 years) |

| Macroeconomic pressure on marketing consulting budgets | -0.6% | Global, with regional variations based on economic conditions | Short term (≤ 2 years) |

| Talent scarcity in advanced martech integration consulting | -0.4% | North America and Europe primarily | Long term (≥ 4 years) |

| Loss of cookie-based tracking disrupting legacy playbooks | -0.3% | Global, immediate impact in digital advertising | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Competition from In-house Teams and Automation Platforms

AI-enabled campaign orchestration, low-code data integration, and talent marketplaces empower enterprises to insource core marketing tasks that once required external agencies. Platforms matching vetted freelancers with businesses report that 85% of clients confirm the first recommended specialist, with contract values ranging between USD 5,000 and USD 20,000 per month. [3]MarketerHire, “Hire the World's Best Expert Marketing Talent,” marketerhire.com As functionality commoditizes, consulting firms must emphasize niche domain expertise, proprietary accelerators, and outcome-linked pricing to defend margins. Although automation dampens volume-based fee models, high-complexity transformation projects and regulatory advisory retain premium billing potential.

Macroeconomic Pressure on Marketing Consulting Budgets

Inflationary cost controls and cyclical softness in discretionary spending prompt marketing leaders to delay non-critical initiatives and renegotiate hourly rates. In 2024, leading Asia-Pacific networks experienced a double-digit decline in new business revenue as clients tightened procurement thresholds. [4]Robert Sawatzky, “APAC Agency Rankings: Zenith and Ogilvy Finish Atop New Business Leagues,” campaignasia.com Consultants counter this restraint by foregrounding ROI measurement, bundling cross-practice capabilities, and offering modular engagements that align with shorter planning horizons. While growth moderation will persist in the near term, structural demand drivers such as privacy compliance and AI augmentation temper the overall impact on the marketing consulting market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Marketing Dominance with CX Specialization Growth

Digital marketing consulting generated the largest service revenue, holding 31.12% of the marketing consulting market share in 2025, underscoring enterprises’ priority to future-proof media buying and measurement frameworks against cookie loss. The segment’s scale reflects continuing complexity in orchestrating paid search, programmatic display, and social commerce while maintaining compliance with region-specific privacy statutes. Consultants supply rapid enablement of server-side tagging, audience modeling, and creative automation, ensuring campaign effectiveness amid signal loss.

Customer experience and personalization consulting is projected to clock the fastest 6.39% CAGR as brands link individualized journeys to revenue growth. Engagements span data-layer audits, rules-based content decisioning, and tagging governance that underpin next-best-action engines. Strategy and planning remain foundational, accounting for steady retainer demand tied to roadmap development and vendor selection. Branding and advertising consulting evolves toward AI-assisted creative concepting that compresses ideation cycles. Market research and analytics practices integrate real-time first-party data ingestion, while emerging offerings such as prompt-engineering advisory and zero-party data strategy position firms at the frontier of martech innovation. The continued convergence of these competencies reinforces universal reliance on consulting support, anchoring a diversified revenue mix in the marketing consulting market.

By End-user Industry: Retail Leadership with Technology Sector Acceleration

Retail and consumer goods held 28.24% revenue in 2025, benefiting from consultancies’ ability to align store digitization, social commerce, and last-mile delivery messaging. Projects frequently revolve around unified product catalogs, dynamic pricing engines, and loyalty program recalibration to boost repeat purchase rates. Consultants also refine in-store analytics to optimize assortment and shelf adjacency, translating offline data into actionable insights that cascade across digital touchpoints.

Technology and media are set to register the highest 6.23% CAGR through 2031 as software publishers and streaming services scale global subscriber acquisition. Engagements emphasize machine-learning-driven experimentation, growth-marketing dashboards, and privacy-centric ad targeting rule sets. Healthcare and life sciences clients seek HIPAA-compliant omnichannel pathways that elevate patient engagement. BFSI players depend on advisory for consented data monetization and hyper-personalized product cross-selling within regulated boundaries. Manufacturing firms pursue B2B e-commerce enablement, and public-sector clients adopt citizen-centric communication architectures. Each vertical retains distinct compliance and experience mandates that sustain demand in the marketing consulting market.

By Client Size: Enterprise Dominance with SME Growth Acceleration

Large enterprises controlled 58.53% of total spend in 2025, affirming their reliance on multi-disciplinary advisory to coordinate martech stacks, global privacy programs, and brand governance frameworks. Engagement scopes often include enterprise-wide marketing cost optimization and change-management plans that stretch across business units and geographies.

Small and micro enterprises will, however, expand fastest at 6.62% CAGR, facilitated by fractional consulting models and AI-powered DIY toolkits that lower entry barriers. Subscription packages deliver modular guidance on demand generation, analytics, and funnel optimization without long-term retainers. Medium-sized organizations maintain incremental growth by outsourcing single-stack implementations or campaign transformations that exceed in-house bandwidth. As modular delivery platforms scale, SME engagement counts rise, further broadening the addressable marketing consulting market.

By Engagement Model: Project-based Prevalence with Outcome-based Evolution

Project-based contracts retained a 54.11% share in 2025, reflecting client preference for scoped deliverables such as CDP rollouts or campaign audits. These engagements facilitate clear budget control and milestone-based governance, yet increasingly incorporate agile sprints to adjust for real-time learnings.

Outcome-based and risk-sharing models will grow at 6.55% CAGR as CMOs link fee structures to revenue lift, cost-per-acquisition reductions, or compliant data-collection milestones. Consultants respond by investing in measurement frameworks, real-time dashboards, and contract clauses that delineate controllable variables. Subscription retainers remain relevant for ongoing optimization and advisory continuity, especially in heavily regulated verticals that require constant compliance monitoring. This evolution underscores rising maturity in value attribution across the marketing consulting market.

By Delivery Mode: On-site Traditional with Hybrid Acceleration

On-site delivery conserved a 52.86% share in 2025 because complex transformation programs benefit from embedded teams and direct collaboration with internal IT and finance stakeholders. Sensitive data environments and change-management workshops continue to favor physical presence.

Hybrid models combining periodic in-person workshops with virtual sprints will advance fastest at 6.78% CAGR. They leverage digital whiteboards, AI-assisted meeting transcripts, and collaborative code repositories to reduce travel costs while safeguarding relationship depth. Fully virtual engagements mature for analytics optimization, martech tuning, and performance reporting once foundational systems are live. The gradual rebalancing toward hybrid execution expands global talent pools and enhances scalability across the marketing consulting market.

Geography Analysis

North America commanded 37.21% of 2025 revenue, anchored by early adoption of privacy-compliant marketing architectures and enterprise investment in AI-enhanced omnichannel orchestration. State-level privacy statutes spur recurring advisory demand for consent-governed data pipelines. United States clients prioritize rapid integration of server-side tracking and predictive audiences to sustain performance marketing as traditional cookies vanish.

Europe contributes a sizable, mature revenue stream characterized by stringent GDPR enforcement that positions consultancies as compliance partners. Demand centers on streamlined consent management, lawful basis mapping, and post-Schrems II transfer risk mitigation. Firms fine-tune localized content within multilingual creative hubs to meet cultural preferences without breaching data boundaries.

Asia-Pacific posts the highest 6.47% CAGR owing to surging digital commerce penetration and rising automation investments among fast-growing enterprises. Regional conglomerates pursue data-lake consolidation and mobile-first experience design to capture digitally native consumers. Despite heterogenous privacy regulations, cross-border commerce growth stimulates advisory engagements on payment localization, cross-channel attribution ,and MarTech stack harmonization. South America, the Middle East and Africa exhibit nascent yet accelerating uptake as mobile broadband adoption climbs and consumer brands globalize. The variety of maturity levels across regions ensures sustained geographic expansion for the marketing consulting market.

Competitive Landscape

The marketing consulting market exhibits moderate concentration with a dynamic interplay between global professional-services giants and specialized boutiques. Accenture, Deloitte, and McKinsey leverage end-to-end digital capabilities and long-standing C-suite relationships to secure enterprise-wide transformation mandates. These firms continue to acquire martech specialists and integrate proprietary AI-driven analytics engines, enabling real-time personalization and efficient value delivery.

Boutique agencies differentiate through deep vertical specialization, agile engagement models, and prompt-engineering expertise that accelerates creative production. AI-native consultancies deploy low-code automation to reduce delivery cycles by up to 40%, unlocking cost advantages for mid-market clients. Talent marketplaces enhance competitive fluidity by matching vetted independent experts to projects, compressing engagement launch times, and expanding client access to niche capabilities.

Convergence between technology providers and strategic advisors intensifies. Software vendors embed advisory units to drive platform adoption, whereas consultancies develop accelerator IP that shortens implementation timelines. Market entrants focusing on privacy engineering, zero-party data orchestration, and outcome-based contracting attract venture backing, stimulating further innovation along the value chain. The evolving landscape underscores the need for differentiation through domain depth, proprietary tooling, and measurable impact within the marketing consulting market.

Marketing Consulting Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Limited

McKinsey & Company

Boston Consulting Group (BCG)

PwC (PricewaterhouseCoopers)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Gucci completed a global marketing transformation, reallocating 15% of its budget from underperforming regions to higher-conversion markets, achieving a 3% revenue uplift through data-driven optimization initiatives.

- March 2025: Slaughter and May published comprehensive guidance on the UK Data (Use and Access) Bill, emphasizing stricter penalties for non-compliant marketing practices and detailing new consent requirements.

- February 2025: CVS rolled out AI-powered in-store signage across 9,000 locations to personalize shopper engagement and improve product discovery.

- January 2025: MarketerHire reported an 85% client satisfaction rate for first-match marketer placements, validating AI-driven talent matching for marketing consulting engagements.

- November 2024: Google enhanced its Privacy Sandbox APIs to support cookieless advertising attribution, prompting new consulting engagements for implementation and optimization.

Global Marketing Consulting Market Report Scope

The marketing consulting market refers to the industry where firms provide expert advice and services to businesses on how to optimize their marketing strategies and achieve business goals. These services include market research, brand development, digital marketing, customer segmentation, and campaign management. Marketing consultants help organizations navigate the ever-evolving marketing landscape, focusing on customer engagement, data-driven decision-making, and innovative solutions. The market is driven by the growing need for companies to adapt to digital transformation and stay competitive in a crowded marketplace.

The Marketing Consulting Market is segmented by service type (strategy and planning, branding and advertising, digital marketing, market research and analysis, and other service types), end-use industry (retail and consumer goods, healthcare and life sciences, technology and media, banking, financial services, and insurance (BFSI), manufacturing, and other end-use industries), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Strategy and Planning |

| Branding and Advertising |

| Digital Marketing |

| Market Research and Analytics |

| CX/Personalization Consulting |

| Other Services |

| Retail and Consumer Goods |

| Technology and Media |

| Healthcare and Life Sciences |

| BFSI |

| Manufacturing |

| Government and Non-Profit |

| Other End-user Industries |

| Large Enterprises |

| Medium-sized Enterprises |

| Small and Micro Enterprises/Start-ups |

| Project-based |

| Subscription/Retainer |

| Outcome-based/Risk-sharing |

| On-site |

| Remote/Virtual |

| Hybrid |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Singapore | ||

| Malaysia | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Strategy and Planning | ||

| Branding and Advertising | |||

| Digital Marketing | |||

| Market Research and Analytics | |||

| CX/Personalization Consulting | |||

| Other Services | |||

| By End-user Industry | Retail and Consumer Goods | ||

| Technology and Media | |||

| Healthcare and Life Sciences | |||

| BFSI | |||

| Manufacturing | |||

| Government and Non-Profit | |||

| Other End-user Industries | |||

| By Client Size | Large Enterprises | ||

| Medium-sized Enterprises | |||

| Small and Micro Enterprises/Start-ups | |||

| By Engagement Model | Project-based | ||

| Subscription/Retainer | |||

| Outcome-based/Risk-sharing | |||

| By Delivery Mode | On-site | ||

| Remote/Virtual | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Singapore | |||

| Malaysia | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the marketing consulting market?

The marketing consulting market size stood at USD 36.65 billion in 2026 and is forecast to reach USD 45.52 billion by 2031.

Which service segment holds the largest share in the marketing consulting market?

Digital marketing consulting led with 31.12% marketing consulting market share in 2025, reflecting enterprises’ urgency to adapt to privacy-first advertising models.

Which region is expected to grow fastest through 2031?

Asia-Pacific is projected to record the highest CAGR at 6.47%, driven by expanding digital commerce and rising martech investment.

Why are outcome-based consulting engagements gaining popularity?

CMOs increasingly link fees to measurable business outcomes, incentivizing consultants to deliver quantifiable revenue lift or cost savings, which aligns incentives for both parties.

How are privacy regulations affecting marketing consulting demand?

Stricter data-protection laws drive sustained consulting needs for zero-party data strategy, consent management and compliant attribution frameworks.

What market concentration level characterizes the marketing consulting industry?

The market scores 6 out of 10 on the concentration scale, indicating that while global consultancies command a majority share, specialized boutiques and AI-native entrants maintain competitive pressure.

Page last updated on: