United States Oral Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

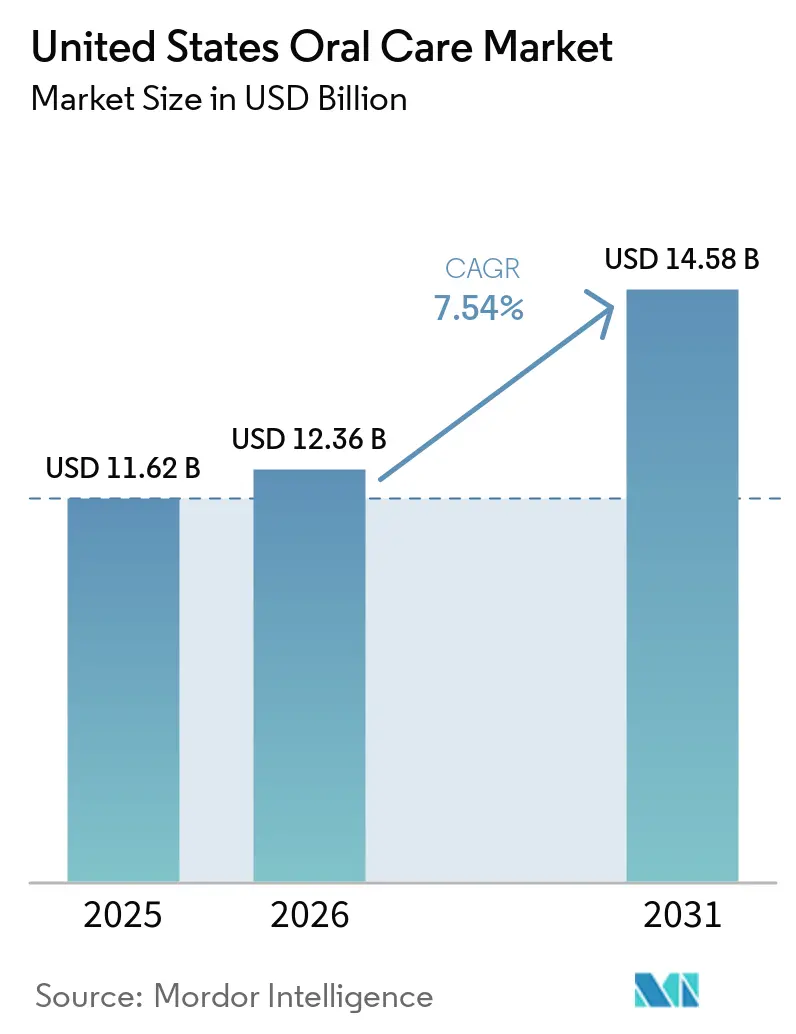

| Base Year Market Size (2025) | USD 11.62 Billion |

| Market Size (2026) | USD 12.36 Billion |

| Market Size (2031) | USD 14.58 Billion |

| Growth Rate (2026 - 2031) | 7.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Oral Care Market Analysis by Mordor Intelligence

The United States oral care market size was valued at USD 11.62 billion in 2025 and estimated to grow from USD 12.36 billion in 2026 to reach USD 14.58 billion by 2031, at a CAGR of 7.5% during the forecast period (2026-2031). The United States oral care market is expanding as consumers place more weight on preventive routines, and Delta Dental reported that 91% of U.S. adults saw oral health as a key part of overall health in 2026, while 94% of Gen Z respondents said it was very or extremely important, up from 89% in 2025. The United States oral care market is also moving toward higher-value products as buyers weigh clinical proof, digital functionality, and ingredient transparency more carefully than before. Competitive pressure remains centered on large consumer health companies, but direct-to-consumer challengers continue to gain traction by focusing on cleaner formulations, simpler messaging, and stronger social proof. Cost pressure still matters, and Colgate-Palmolive said in its Q1 2026 management remarks that raw material and packaging costs added USD 300 million, while regulatory attention around pediatric fluoride use is also shaping product decisions. The United States oral care market also has a clear opening in underserved Hispanic and Latino communities, where disease burden remains high and better bilingual communication, access support, and culturally adapted branding could lift category penetration over time.

Key Report Takeaways

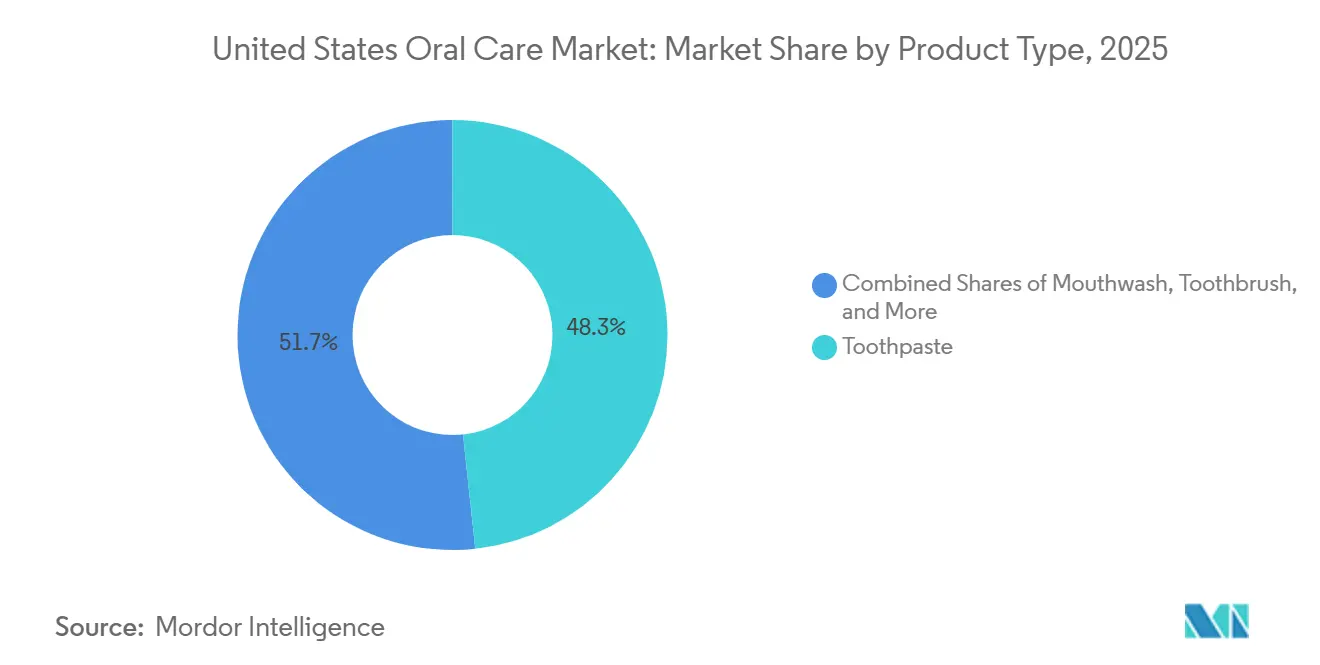

- By product type, toothpaste accounted for 48.32% of the United States oral care market size in 2025, while toothbrushes are projected to expand at an 8.25% CAGR through 2031.

- By ingredient, conventional formulations held 75.48% of the United States oral care market share in 2025, while natural and organic products are forecast to grow at an 8.38% CAGR through 2031.

- By end user, adults held 51.85% of the United States oral care market share in 2025, while kids and children are projected to advance at an 8.75% CAGR through 2031.

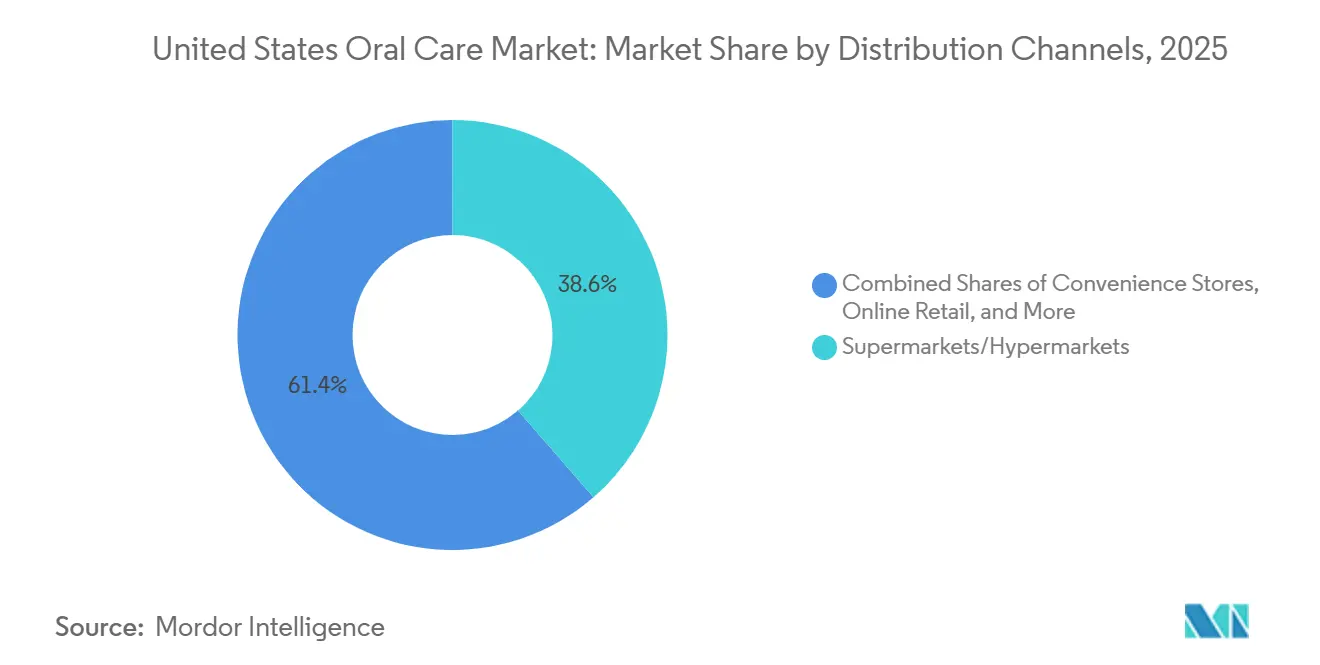

- By distribution channel, supermarkets and hypermarkets captured 38.62% share of the United States oral care market size in 2025, while online retail channels are forecast to grow at an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Oral Care Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Prevalence Of Dental Disorders | +1.5% | National, acute in Southern states and rural communities | Medium term (2-4 years) |

| Increasing Demand For Premium Oral Care Products | +1.3% | National, concentrated in Northeast and Pacific Coast metros | Medium term (2-4 years) |

| Expansion Of Natural And Organic Oral Care Products | +1.1% | National, concentrated in Pacific Coast and Northeast | Long term (≥ 4 years) |

| Product Innovation And Technological Advancements | +1.0% | National, with strongest uptake in high-income urban markets | Long term (≥ 4 years) |

| Growing Influence Of Dental Professionals And Preventive Care Programs | +0.8% | National | Medium term (2-4 years) |

| Increasing Consumer Awareness Of Preventive Oral Healthcare | +0.7% | National, with growing impact in underserved communities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Prevalence Of Dental Disorders

The United States oral care market continues to draw steady demand from a large and persistent disease burden across both adult and pediatric groups. The CDC reported in 2024 that 1 in 5 U.S. adults aged 20 to 64 had at least 1 untreated cavity, and 50% of children had experienced cavities by age 9[1]Source: Centers for Disease Control and Prevention, “Oral Health Facts,” cdc.gov. The same source showed that lower-income households faced more than twice the rate of untreated decay seen in higher-income households, which keeps demand broad but also highly uneven by price sensitivity. This pattern supports demand for everyday prevention products and also for higher-value therapeutic items such as gum-care, sensitivity, and antibacterial formulations. A 2025 BMC Oral Health study found that adults below 100% of the Federal Poverty Level had 2.4 times greater odds of untreated caries than adults at or above 400% of that level, which reinforces the need for targeted value and access strategies. A 2025 MDPI study also showed periodontal disease prevalence of 63% among Mexican-origin adults versus 43% among non-Hispanic White adults, which points to a sizable underserved demand pool inside the United States oral care market.

Increasing Demand For Premium Oral Care Products

The United States oral care market is seeing a stronger shift toward premium offerings as many consumers move away from standard mid-tier products. Buyers are showing a greater willingness to pay for whitening efficacy, digital coaching, specialized formats, and professional-style benefits when those claims are clearly explained. Colgate-Palmolive introduced Optic White Pro Series Toothpaste in March 2026 with 5% hydrogen peroxide and claimed visible whitening within 3 days at a USD 9.99 price point, which shows how brands are expanding the premium tier inside core categories. The premium shift also reaches beyond treatment into beauty-oriented positioning, as hello launched a whipped toothpaste format in January 2026 for Gen Z users who connect oral care with broader personal care routines. This change is narrowing the middle of the market because shoppers are increasingly choosing either value products or clearly differentiated premium items. That makes pricing discipline, brand storytelling, and visible product proof more important across the United States oral care market.

Expansion Of Natural And Organic Oral Care Products

The United States oral care market is also being reshaped by stronger interest in natural and organic formulations. Natural and organic products are projected to grow at an 8.4% CAGR through 2031, which is the fastest trajectory within the ingredient split and shows that this is not a short-term preference swing. Consumers who already check ingredient lists in food and skin care are now applying the same habit to toothpaste, rinses, and whitening products. This shift favors brands that make ingredient claims simple and easy to verify, especially in specialty retail and direct-to-consumer channels. Colgate-Palmolive’s management of the hello brand reflects how large companies are responding by keeping a naturally positioned label alongside their mainstream fluoride portfolios. Bond University research on Hismile noted that the brand reached AUD 700 million, or USD 462 million, in global gross sales by 2024, showing that natural-adjacent and ingredient-forward positioning can scale without traditional clinical heritage[2]Source: Bond University Research Portal, “Hismile, Bootstrapping an Oral Care Industry Disruptor,” bond.edu.au.

Product Innovation And Technological Advancements

The United States oral care market is relying heavily on innovation to create separation in categories where basic products are easy to compare. Connected electric toothbrushes, pressure sensors, and app-based coaching are turning devices into higher-value systems rather than simple tools. SuperMouth launched the Ultim8 SmartBrush Ortho-Edition in April 2026 for users in active orthodontic treatment, showing how design is moving toward narrower clinical use cases that were once ignored by broader device portfolios. Colgate-Palmolive also launched the Colgate Total Active Prevention System in February 2025 with patented stannous fluoride stabilization technology, which illustrates how formulation science remains a key tool for premium positioning in toothpaste. These developments support higher average selling prices and also create more reasons for consumers to stay within a brand ecosystem. The result is that the United States oral care market is shifting from single-product competition toward platform competition across devices, refills, and outcome-oriented daily care.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Compliance And Labeling Requirements | -0.6% | National | Medium term (2-4 years) |

| Concerns Regarding Certain Chemical Ingredients | -0.5% | National | Medium term (2-4 years) |

| Rising Raw Material And Packaging Costs | -0.4% | National | Short term (≤ 2 years) |

| High Consumer Price Sensitivity In Mass-Market Segments | -0.4% | National, acute in lower-income and rural communities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Regulatory Compliance And Labeling Requirements

The United States oral care market remains tightly shaped by federal compliance rules that affect how quickly brands can extend or revise products. The FDA’s monograph structure for anticaries and related products limits formulation flexibility and keeps ingredient and warning language under close scrutiny. The Federal Register notice issued in June 2025 on orally ingestible unapproved fluoride drug products in children also showed that pediatric oral care remains a particularly sensitive area for regulatory oversight[3]Source: U.S. Food and Drug Administration, “Use of Orally Ingestible Unapproved Prescription Drug Products Containing Fluoride in the Pediatric Population, Public Meeting,” federalregister.gov. These changes matter most for smaller and international brands because testing, registration, and label conformity absorb a larger share of their resources than they do for global incumbents. Compliance demands also slow line extensions in a category where brands often rely on new formats, flavors, and claims to maintain shelf interest. As a result, regulatory discipline tends to favor companies with larger in-house quality, legal, and formulation teams across the United States oral care market.

Concerns Regarding Certain Chemical Ingredients

The United States oral care market also faces a trust challenge as some consumers question the safety of fluoride in certain pediatric uses, sodium lauryl sulfate, titanium dioxide, and other synthetic ingredients. The FDA announced in 2025 that it was acting against unapproved ingestible fluoride drug products for children under age 3, which intensified public discussion even though topical fluoride toothpaste remains recognized as safe and effective for cavity prevention. This mixed message is difficult for brands because it requires careful explanation rather than simple advertising. Companies that communicate ingredient choices clearly are gaining credibility with consumers who already compare labels across food, beauty, and wellness categories. That communication gap creates room for alternative products that appear simpler even when their clinical support is less established. In practice, this pressure is pushing more of the United States oral care market toward transparent labeling, narrower claim sets, and cleaner product stories.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Toothpaste Anchors Volume While Powered Devices Drive Revenue

Toothpaste accounted for 48.32% of the United States oral care market in 2025, supported by very high household penetration and steady replenishment demand. Its position remains strong because brands continue to refresh the category with whitening, breath, gum-care, and antibacterial claims that keep consumers from treating it as a pure commodity. Mouthwash and rinses held the second-largest position, helped by multi-benefit formulas that combine cosmetic and therapeutic use cases. Procter & Gamble’s January 2026 launch of Crest Clean Breath showed how even a mature rinse and toothpaste environment can still support new premium claims tied to everyday consumer needs.

Toothbrushes are the fastest-growing product group, with the United States oral care market size for this segment projected to expand at an 8.25% CAGR through 2031. Growth is being driven by the shift from manual to electric formats, stronger consumer interest in guided brushing, and the growing appeal of refill-based recurring revenue models. Other product types such as floss, whitening strips, and accessories still add revenue, but their performance depends more heavily on education and routine-building than on automatic repeat purchase. This mix shows that the United States oral care market is being lifted more by category upgrading than by simple unit expansion. Companies that can link daily use products with device ecosystems are likely to capture more of the value created inside the broader United States oral care industry.

By Ingredient: Conventional Formulations Dominate As Natural Products Set The Growth Ceiling

Conventional formulations held 75.48% of the market in 2025, which reflected long-standing trust in fluoride-based and clinically positioned products across both retail and dental channels. That base remains important because consumers with active conditions such as sensitivity, gum irritation, or enamel concerns still prioritize proven efficacy over ingredient philosophy. Natural and organic products, however, are forecast to grow at an 8.38% CAGR through 2031, which is materially faster than the broader category pace. This split shows that the United States oral care market is not abandoning conventional chemistry, but it is giving more room to brands that simplify ingredient messaging.

The strongest demand for natural products is coming from younger buyers who compare oral care labels with the standards they use in skin care and food purchases. Brands such as Tom’s of Maine, Dr. Brite, The Humble Co., and Hismile benefit when shelf presentation and digital content make sourcing and formulation choices easy to understand. Large incumbents are responding by running dual architectures, with mainstream therapeutic brands on one side and more naturally positioned lines on the other. That approach helps preserve share in the legacy base while also participating in the faster-moving part of the United States oral care market. The tension going forward is not whether natural products matter, but whether large companies can scale them without weakening the authenticity that made them attractive in the first place.

By End User: Pediatric Products Accelerate As Parental Investment Rises

Adults held 51.85% of the market in 2025 because they consume the full range of oral care products, including preventive, therapeutic, whitening, and specialty items. This adult base remains critical because it supplies stable volume and also supports premium pricing in sensitivity relief, gum care, and cosmetic use cases. Kids and children are the fastest-growing end-user segment, with the United States oral care market size for pediatric products projected to rise at an 8.75% CAGR through 2031. Delta Dental reported in 2026 that 95% of parents prioritized their children’s oral health and that 78% rated it good or excellent, which helped support stronger household willingness to spend on prevention early in life.

That growth is being reinforced by broader product choice, including character-based designs, varied flavors, orthodontic-support tools, and different fluoride positioning. The United States oral care market also benefits from the fact that childhood brand choice can shape household replenishment behavior for years after the first purchase. The pediatric opportunity is especially important in fast-growing Hispanic and Latino communities, where disease burden remains elevated and communication barriers still affect preventive adoption. FDA attention to pediatric fluoride use adds another layer, which means brands need clear disclosure and credible parent education to keep trust high. For that reason, children’s products are becoming a long-term brand-building lever rather than just a niche extension inside the United States oral care market.

By Distribution Channels: Physical Retail Leads While Online Commerce Captures Value-Tier Spending

Supermarkets and hypermarkets held 38.62% of the market in 2025, reflecting their continued role in frequent replenishment purchases such as toothpaste, manual brushes, and mouthwash. Physical retail still matters because shoppers often buy these products as part of broader household trips and respond to in-store visibility and price promotions. Drug stores and pharmacies also remain important because the pharmacy setting supports trust for therapeutic and sensitivity-focused formulations. Online retail channels are growing fastest, with the United States oral care market size for this channel forecast to rise at an 8.55% CAGR through 2031.

Digital growth is being supported by easier product comparison, direct brand education, and subscription models for refills and routine replacement. Online channels are especially useful for premium electric devices and specialized formulas, where buyers often want more detail than a shelf tag can provide. Professional dental offices also matter because recommendation-based purchases tend to carry higher consumer confidence and lower switching rates. That creates a channel mix where broad volume still sits in stores, while a larger share of premium value creation moves online. The result is that the United States oral care market is becoming more dependent on coordinated pricing, fulfillment, and messaging across both physical and digital touchpoints.

Geography Analysis

The Northeast remains the largest regional revenue concentration within the United States oral care market, supported by higher household incomes, stronger dental insurance coverage, and greater willingness to buy premium and therapeutic products. California and the broader Pacific Coast also contribute outsized revenue because clean-label preferences, wellness spending, and direct-to-consumer adoption are all relatively strong there. The South and Southeast are expanding the addressable customer base through population growth, but unequal access to dental care still slows movement from basic hygiene into higher-value categories. Delta Dental reported that 53% of adults in urban areas had a preventive dental visit in 2025, compared with 40% in rural areas, and that gap helps explain why demand composition varies sharply across regions.

The Midwest shows steadier and more moderate expansion, with broad household penetration but stronger sensitivity to price. Private-label appeal is higher in this region because consumers are more likely to compare value when branded prices rise. Online ordering is becoming more relevant as delivery convenience improves and makes refill programs easier to adopt. Input costs also remain a live issue, and the U.S. Bureau of Labor Statistics producer price index for toothpastes, denture cleaners, and mouthwashes reached 181.1 in May 2026, which shows that cost pressure has not fully eased.

The Hispanic and Latino population, concentrated in California, Texas, Florida, and the Southwest, remains the clearest underaddressed growth opportunity in the United States oral care market. A 2025 MDPI study found periodontal disease prevalence of 63% among Mexican-origin adults, which was higher than the 43% reported for non-Hispanic White adults. A 2025 BMC Oral Health study also showed that adults below the Federal Poverty Level had 2.4 times greater odds of untreated caries, and this income effect overlaps with populations that already face access barriers. Language, insurance gaps, and a more reactive care pattern keep disease burden elevated in these communities. Brands that invest in bilingual communication, culturally adapted education, and stronger pediatric outreach should be better placed to outperform the national average as this population continues to grow.

Competitive Landscape

The United States oral care market remains concentrated at the top, with a small group of global consumer health companies controlling most shelf visibility, promotion budgets, and professional recommendation channels. That structure supports scale advantages in manufacturing, retail negotiations, and broad portfolio coverage. It also means category leaders can defend share even when growth slows in mass-market products. At the same time, challenger brands continue to gain attention by moving faster on ingredient clarity, distinct branding, and narrow use-case design.

Colgate-Palmolive’s February 2025 launch of the Active Prevention System showed how large incumbents are using proprietary science to refresh mature segments and support premium pricing. The company followed that with Optic White Pro Series in March 2026 and the hello whipped toothpaste format in January 2026, which together show a strategy that covers both clinical efficacy and beauty-adjacent product design. Haleon also signaled continued commitment to portfolio expansion through bolt-on acquisitions in its 2025 annual report, which supports the view that acquisition remains a practical tool for absorbing emerging brand equity before it scales further. Smaller brands are pushing hardest where the largest companies have been slower, especially in sustainability, transparent ingredient positioning, and culturally targeted communication. That pressure is forcing incumbents to respond across more dimensions than simple pricing or retailer promotion.

Bond University research showed that Hismile reached USD 462 million, in global gross sales by 2024, which confirms that social-native oral care brands can scale meaningfully without the same legacy trade structure as incumbents. SuperMouth’s April 2026 launch of an orthodontic-focused smart brush also showed how challengers can carve out narrow clinical niches that are too small for broad portfolios to prioritize early. Colgate-Palmolive’s disclosure of USD 300 million in added raw material and packaging costs in Q1 2026 further suggests that scale does not remove pressure, even for category leaders. The United States oral care market is therefore consolidated, but it is not static, because new growth is being contested in premium, natural, digital, and underserved demographic spaces.

United States Oral Care Industry Leaders

Colgate-Palmolive Company

The Procter and Gamble Company

Haleon plc

Church and Dwight Co., Inc.

Kenvue Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: SuperMouth launched the Ultim8 SmartBrush Ortho-Edition, identified as one of the first orthodontist-engineered electric toothbrush systems designed for users in active orthodontic treatment. The system is priced at USD 169.99-199.99, available via SuperMouth.com with Amazon availability announced imminently, targeting an underserved clinical sub-segment that established players had not addressed with purpose-built device design.

- March 2026: Colgate-Palmolive introduced the Optic White Pro Series Toothpaste, featuring 5% hydrogen peroxide and clinical substantiation for visible whitening within 3 days. The product launched nationally at Walmart, Amazon, and CVS at USD 9.99 MSRP and represents Colgate's most advanced at-home whitening formulation to date, extending the premium tier of the toothpaste category.

- January 2026: Procter & Gamble launched Crest Clean Breath, a daily-use toothpaste formulated to neutralize bad breath bacteria at the source and deliver 24-hour antibacterial protection, with national distribution across Target, Walmart, Walgreens, and CVS at USD 4.99-8.99 MSRP. The launch signals P&G's continued product line expansion within the functional toothpaste sub-segment.

United States Oral Care Market Report Scope

| Toothpaste |

| Mouthwash/Rinses |

| Toothbrush |

| Other Product Types |

| Conventional |

| Natural/Organic |

| Kids/Children |

| Adults |

| Supermarkets/Hypermarkets |

| Drug Stores/Pharmacies |

| Online Retail Channels |

| Other Distribution Channels |

| By Product Type | Toothpaste |

| Mouthwash/Rinses | |

| Toothbrush | |

| Other Product Types | |

| By Ingredient | Conventional |

| Natural/Organic | |

| By End User | Kids/Children |

| Adults | |

| By Distribution Channels | Supermarkets/Hypermarkets |

| Drug Stores/Pharmacies | |

| Online Retail Channels | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the 2031 outlook for United Sates oral care sales?

The United States oral care market is projected to reach USD 14.58 billion by 2031 from USD 12.36 billion in 2026, growing at a 7.54% CAGR over 2026-2031.

Which product category holds the largest share in oral care sales?

Toothpaste led the category in 2025 with a 48.32% share, supported by high household penetration and steady replenishment demand.

Which oral care segment is growing fastest by ingredient type?

Natural and organic formulations are forecast to grow at an 8.38% CAGR through 2031, outpacing the broader category and reflecting stronger interest in ingredient transparency.

Why are children’s oral care products expanding faster than the adult segment?

Kids and children are projected to grow at an 8.75% CAGR through 2031 because parents are spending more on prevention, broader pediatric product choices, and early routine building.

Page last updated on: