Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

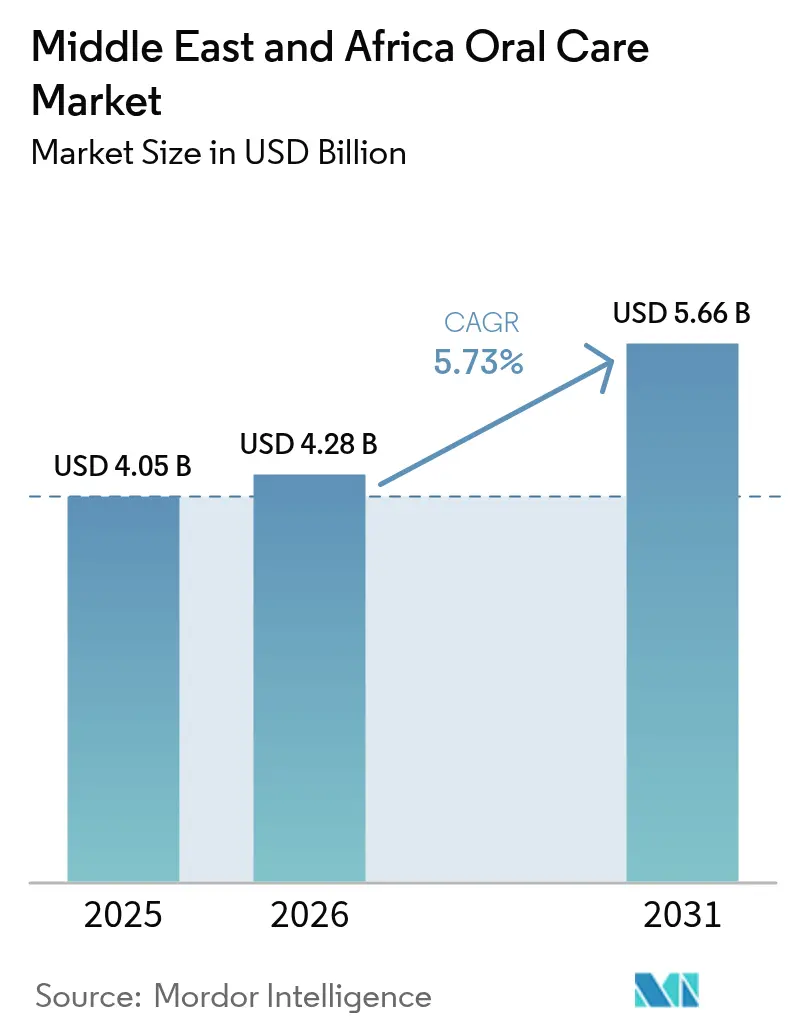

| Base Year Market Size (2025) | USD 4.05 Billion |

| Market Size (2026) | USD 4.28 Billion |

| Market Size (2031) | USD 5.66 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Middle East and Africa Oral Care Market Analysis by Mordor Intelligence

Middle East and Africa oral care market size in 2026 is estimated at USD 4.28 billion, growing from 2025 value of USD 4.05 billion with 2031 projections showing USD 5.66 billion, growing at 5.73% CAGR over 2026-2031. This growth is driven by rising disposable incomes, a burgeoning population under 30, and increased government spending on preventive healthcare. Highlighting the region's commitment to oral health, Morocco hosted its 6th International Exhibition of Dental Health in April 2025, drawing over 6,000 professionals. Organized under the Ministry of Health, the event featured educational conferences and showcased cutting-edge dental technologies. In the Gulf, high-income shoppers are gravitating towards premium innovations like electric toothbrushes, smart rinses, and halal-certified organic pastes. Simultaneously, staple toothpastes continue to dominate in more populous economies. Initiatives like school-based fluoride programs, targeted digital marketing, and the region's robust halal economy bolster the sector's resilience. As multinationals employ education campaigns and price-tier strategies to maintain brand leadership, agile local firms are capitalizing on cost advantages and cultural ties to enhance their market presence.

Key Report Takeaways

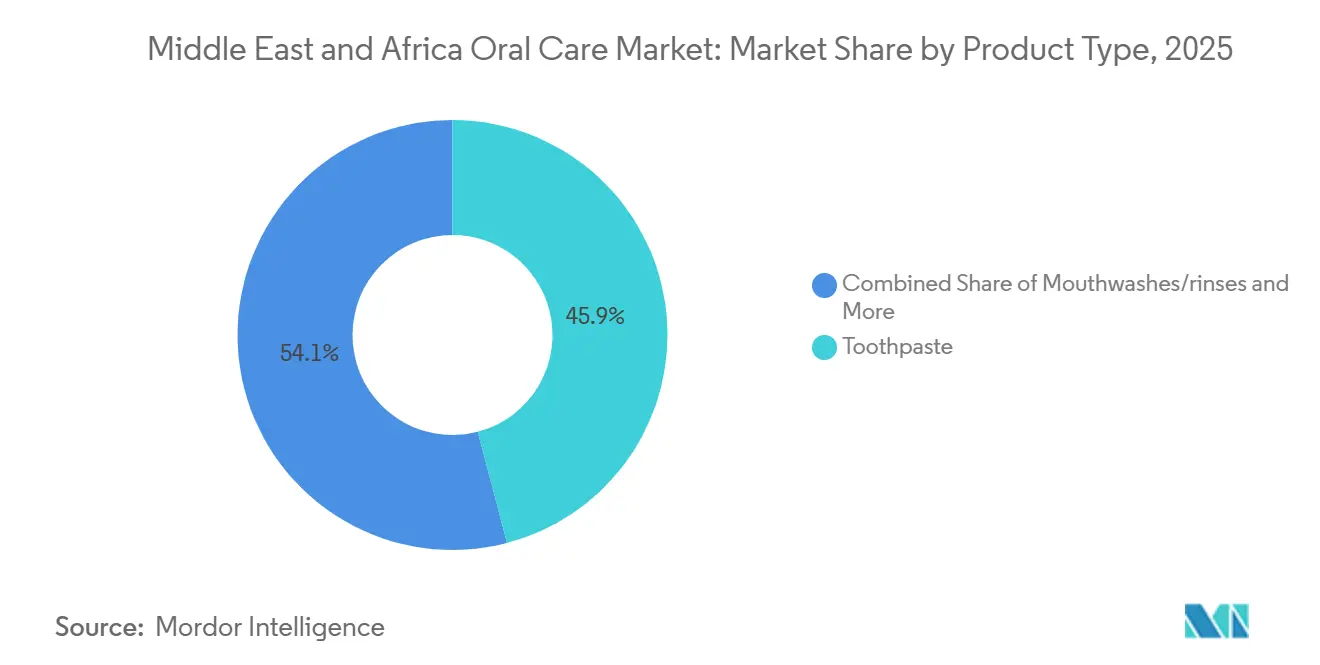

- By product type, toothpaste led with 45.92% of the Middle East Africa oral care market share in 2025, while mouthwashes/rinses are advancing at a 6.43% CAGR to 2031.

- By ingredient, conventional formulations held 82.23% share of the Middle East Africa oral care market in 2025; organic products are projected to grow at 6.76% CAGR through 2031.

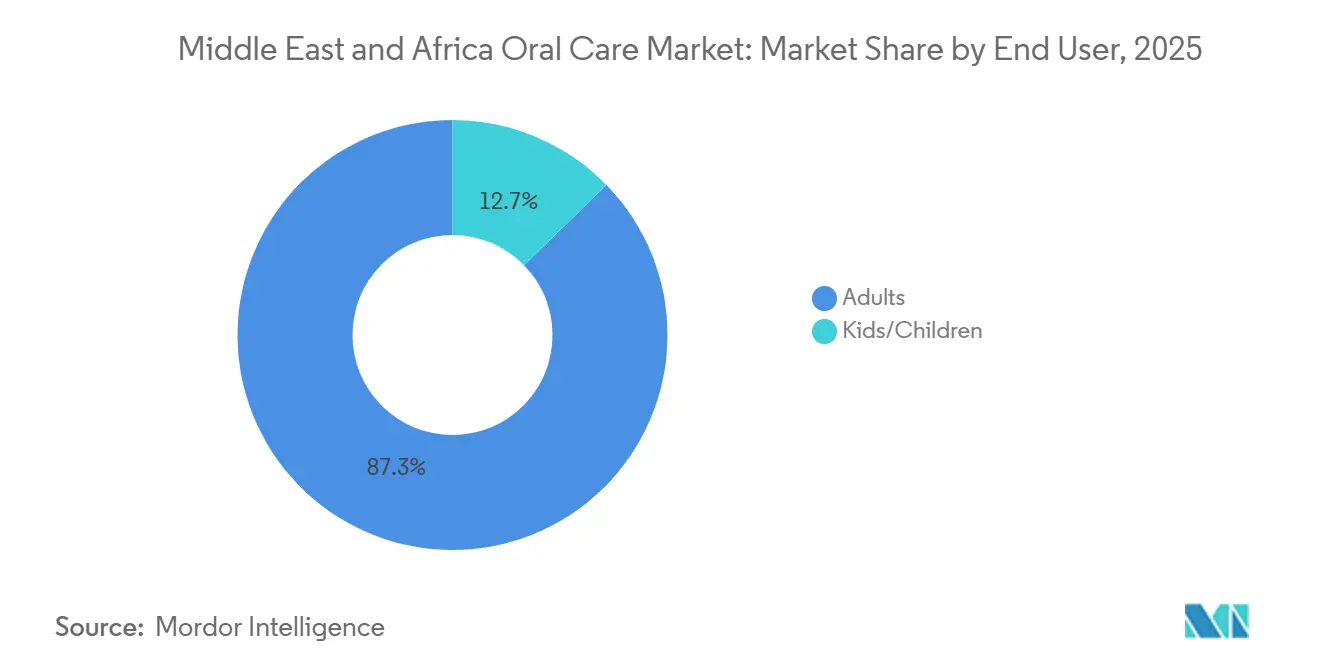

- By end user, adults accounted for 87.30% of 2025 sales, whereas the children’s segment is set to expand at 7.08% CAGR during 2026-2031.

- By distribution channel, supermarkets/hypermarkets commanded 33.42% share in 2025, and online retail is forecast to post a 7.58% CAGR to 2031.

- By geography, the United Arab Emirates contributed 32.18% revenue in 2025, while South Africa is poised for the fastest 7.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Middle East and Africa Oral Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing awareness of oral hygiene | +1.2% | Global, strongest in the United Arab Emirates, Saudi Arabia, South Africa | Medium term (2-4 years) |

| Product innovations and technology | +0.8% | Urban centers across Middle East and Africa, Gulf states leading adoption | Long term (≥ 4 years) |

| Rising prevalence of oral diseases | +0.9% | Sub-Saharan Africa, North Africa rural areas | Short term (≤ 2 years) |

| Consumer shift towards natural and organic products | +0.6% | The United Arab Emirates, Saudi Arabia, urban Egypt, Morocco | Medium term (2-4 years) |

| Government and NGO-led health campaigns | +0.7% | Kuwait, Uganda, Sudan, regional WHO initiatives | Medium term (2-4 years) |

| Digital marketing and social media influence | +0.5% | The Middle East and North Africa region, youth demographics 15-29 years | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Awareness of Oral Hygiene

Across the region, educational initiatives are reshaping consumer behavior and driving market demand. As of 2025, Kuwait's School Oral Health Program, active in all six governorates, caters to around 280,000 public school children. The program administers fluoride varnish applications biannually and imparts comprehensive oral health education. This proactive approach has led to a noticeable decline in disease levels and a reduced need for treatments. By emphasizing prevention, the program is steering long-term demand towards preventive products rather than curative treatments. In Sudan, similar educational programs not only boosted knowledge scores post-intervention but also led to tangible improvements in practices, underscoring the potential for education to drive market expansion. Corporate initiatives are bolstering these government-led efforts. Colgate's "Bright Smiles, Bright Futures" program, as of 2024, has reached over 1.6 billion children worldwide, with a notable presence in the MEA, thanks to collaborations with health and education ministries. The synergy between public and private educational endeavors is fostering a sustained growth in demand, influencing purchasing decisions at the household level. In 2024, WHO reported that around 44% of the African Region's population grappled with oral diseases, underscoring a significant market opportunity for preventive solutions[1]Source: World Health Organization, "World Oral Health Day 2024", www.afro.who.int.

Product Innovations and Technology

In the region, discerning consumers are increasingly investing in advanced oral care solutions, showcasing a trend in technology adoption that persists despite economic fluctuations. Philips Sonicare, a key player, offers a diverse range of products in the UAE and Kuwait. Their lineup spans from the entry-level Philips One, boasting a 90-day battery life, to the premium Sonicare 9900 Prestige, equipped with SenseIQ technology. This breadth underscores a robust demand for innovations in electric toothbrushes. The brand's technology, touting up to 62,000 brush movements per minute and clinically validated plaque removal, strikes a chord with health-conscious consumers who prioritize tangible benefits. As regional consumers align more closely with global beauty and wellness trends, oral care is increasingly adopting formats reminiscent of skincare – think serums, specialized applicators, and structured day/night routines. Furthermore, innovation isn't limited to hardware; it's also about integrating bioactive ingredients. Hydroxyapatite aids remineralization, peptides bolster periodontal health, and probiotics ensure a balanced microbiome. These additions cater to the region's sophisticated consumers, who demand clinically validated and dentist-endorsed formulations. With mobile usage in the region averaging over 4 hours daily and social media penetration notably high in the UAE and Saudi Arabia, there's a ripe opportunity for digital marketing and direct engagement strategies for these innovative products.

Rising Prevalence of Oral Diseases

Data on disease burdens in the Eastern Mediterranean Region highlights both challenges and market opportunities, as WHO estimates reveal significant unmet treatment needs. This region grapples with a high prevalence of dental caries, periodontal disease, and untreated decay. Vulnerable groups, notably children, economically disadvantaged individuals, and refugees, bear the brunt of these oral health challenges. The gravity of these oral health issues is underscored by proactive government initiatives. For example, in August 2025, African health ministers ratified a framework aimed at curbing oral diseases, targeting enhanced access to essential services and a reduction in major disease prevalence by 2030[2]Source: World Health Organization, African Region, "Regional framework for accelerating implementation of the Global oral health action plan", afro.who.int. While Saudi Arabia grapples with high rates of untreated tooth decay, both deciduous and permanent, Pakistan faces a rising prevalence of oral cancer. These disparities underscore the need for tailored product solutions. Furthermore, in conflict zones and areas with significant displacement, the deterioration of oral health is pronounced. This scenario amplifies the demand for oral care products that are both accessible and effective, even in challenging conditions. According to the WHO Global Health Observatory, in 2024, 3.5 billion individuals worldwide grappled with oral diseases, with about 75% residing in middle-income nations. This demographic closely mirrors the economic landscape of the MEA region. Given that basic restorative dental procedures cater to less than half of those in need across various regional markets, there's a burgeoning consumer demand for preventive self-care solutions and maintenance products.

Consumer Shift Towards Natural and Organic Products

In the UAE, the retail market is witnessing a surge in certified organic oral care products, underscoring a growing consumer preference for items that resonate with specific dietary and religious values. For instance, Jack n Jill's Organic Natural Raspberry Toothpaste, proudly halal-certified and free from SLS and fluoride, highlights this trend. As the halal economy is set to reach impressive valuations in 2024, there's a burgeoning market for oral care products that eschew alcohol and animal-derived ingredients. Companies like Fulijaya Manufacturing are capitalizing on this demand, rolling out EcoCert and ISO-compliant organic ranges, including natural antiseptic products aimed at conditions like gingivitis. Furthermore, as consumers become more informed about ingredient benefits, there's a noticeable shift towards alternatives to traditional fluoride. Innovations aren't limited to ingredients; the industry is also witnessing a pivot in packaging. Manufacturers are moving away from 100% plastic, introducing "Green Toothbrushes" and other sustainable solutions, catering to the eco-conscious consumer.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low awareness and education in certain segments | -0.8% | Rural areas across Sub-Saharan Africa, remote regions | Long term (≥ 4 years) |

| Influence of unorganized sector/counterfeit products | -1.1% | Nigeria, Kenya, Egypt, fragmented supply chains | Short term (≤ 2 years) |

| Preference for conventional/basic products | -0.6% | Rural and developing countries in the region | Medium term (≤ 3 years) |

| Fluctuating raw material prices | -0.9% | United Arab Emirates, Saudi Arabia, and Africa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low Awareness and Education in Certain Segments

In the Middle East and Africa (MEA), a significant market restraint stems from limited awareness and education regarding specific oral care products and advanced hygiene practices, especially in specialized or premium segments. While urban centers see a rise in awareness for basic products like toothpaste and toothbrushes, many remain oblivious to the advantages of items such as therapeutic mouthwashes, dental floss, and electric or smart toothbrushes. This knowledge gap hampers product adoption, stunting sales growth for manufacturers. For instance, in numerous rural and low-income regions, dental care is often a reactive endeavor, with individuals seeking treatment only after issues escalate, rather than proactively preventing them through a comprehensive oral care regimen. Such behavior directly influences the market for preventive products, like sensitive toothpaste or fluoride treatments. In light of this, government and dental associations have intensified their educational initiatives. In 2024–2025, several African nations marked World Oral Health Day with community and school outreach programs, emphasizing the importance of a holistic oral hygiene routine beyond mere brushing. Additionally, the FDI World Dental Federation's 2024–2026 initiative, "A Happy Mouth Is...", seeks to underscore the connection between oral and overall health, with the goal of fostering enduring behavioral changes. On the product development front, there's a noticeable shift towards natural and herbal ingredients in toothpaste, driving sales and brand recognition in certain regions. Simultaneously, advancements in electric and AI-powered toothbrushes target affluent urban segments, streamlining dental care routines. Yet, despite these innovations, the region grapples with a persistent challenge: a lack of awareness regarding the specific benefits and proper usage of these advanced products.

Influence of Unorganized Sector/Counterfeit Products

Counterfeit and substandard products pose a significant threat to market integrity and consumer safety in the region. As of June 2024, Dubai Customs recycled nearly 22 million counterfeit items over five years, underscoring the vast scale of illicit trade impacting consumer goods markets. Reports from the WHO highlight that a significant portion of global reports on substandard and falsified medicines come from Africa. In fact, an analysis of 7,508 samples in select markets revealed that 22.6% of medicines were either substandard or unregistered. The oral care sector is not immune, facing challenges with counterfeit toothpaste and mouthwash products. These fakes, funneled through informal distribution channels, not only undercut legitimate manufacturers on price but also jeopardize consumer safety. In March 2025, Kenya's Anti-Counterfeit Authority unveiled the AI-driven 'Bleep App' to tackle the counterfeit trade. They estimate that illicit trade drains over KSh 100 billion from Kenya's economy annually, highlighting the economic ramifications of competition from the unorganized sector. Enforcement challenges arise from the fragmented regulatory frameworks of 54 African authorities. Inconsistent national standards and feeble post-market surveillance further facilitate the circulation of counterfeit products. While brand owners like Colgate-Palmolive are proactive, reporting counterfeits to authorities and educating consumers, the enduring nature of the issue underscores the need for ongoing collaboration among multiple stakeholders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Toothpaste Leadership Faces Mouthwash Disruption

In 2025, toothpaste commands a dominant 45.92% market share, underscoring its entrenched consumer habits and widespread recognition across the MEA region. Meanwhile, mouthwashes and rinses are on a rapid ascent, projected to grow at a 6.43% CAGR through 2031. This surge is fueled by a more discerning consumer base that now seeks holistic oral care, moving beyond mere cleaning. This trend mirrors a broader wellness movement, with consumers adopting intricate oral care routines akin to skincare, targeting specific needs like sensitivity, whitening, and breath freshness. Electric toothbrushes are carving out a notable niche, especially in urban areas where tech-savvy consumers are willing to invest in advanced solutions that promise better plaque removal and added conveniences.

While mouth fresheners and denture care products cater to niche markets, each with its unique growth catalysts and consumer demographics, their trajectories diverge. Cultural inclinations and social habits drive the demand for mouth fresheners, whereas denture care products cater to the needs of an aging demographic in more mature markets. Despite its potential, dental floss remains underutilized, though growing awareness campaigns are spotlighting its importance for interdental cleaning. Regional dynamics reveal a spectrum of consumer maturity: Gulf markets are leaning towards premium and specialized products, while other regions, more price-sensitive, are gravitating towards basic functionality and value.

By Ingredient: Conventional Dominance Challenged by Organic Acceleration

In 2025, conventional products dominate with an 82.23% market share, underscoring a regional preference for established formulations and a price-sensitive consumer base. Yet, organic alternatives are on the rise, boasting a 6.76% CAGR through 2031, nearly double that of their conventional counterparts. This surge signals a pivotal shift in consumer inclinations towards natural and sustainable oral care. Such a trend is fueled by a growing health consciousness, especially among urban, educated demographics who value ingredient transparency and wellness-aligned products. Moreover, the organic segment is bolstered by cultural and religious factors: halal-certified organic offerings cater to specific dietary needs, steering clear of contentious elements like alcohol-based preservatives and animal-derived ingredients.

Regional manufacturing prowess champions organic product innovation. Companies roll out EcoCert and ISO-compliant natural formulations, marrying international quality benchmarks with local tastes. Ingredient segmentation paints a dual landscape: conventional products lead in volume, thanks to their affordability and accessibility, while organic variants, with their premium positioning and unique benefits, drive value growth. As consumer awareness and income levels rise in pivotal markets, regional regulatory bodies are increasingly backing organic product certification and labeling, setting the stage for further segment expansion.

By End User: Adult Dominance Masks Children's Growth Opportunity

In 2025, adults command a dominant 87.30% share of the market, underscoring their pivotal role in household oral care decisions across the MEA region. Yet, the children's segment is on a rapid ascent, boasting a 7.08% CAGR projected through 2031. This surge underscores the growing emphasis on instilling early oral care habits and the push for tailored pediatric products. The uptick in the children's segment can be attributed to effective educational campaigns, notably Kuwait's initiative reaching 280,000 children and Uganda's Unilever campaign, which, launched in March 2025, targeted 400,000 school-goers. Given the unique needs of children, from safety to taste, there's a burgeoning demand for innovative solutions in product formulation, packaging, and educational outreach.

With a significant portion of the region's population under 30, young families are increasingly prioritizing preventive healthcare, ensuring oral hygiene becomes a foundational routine in their children's lives. As of 2024, South Africa's population, nearing 63 million, boasts about 27.5 million individuals aged 0-24, according to Statistics South Africa. Major manufacturers, through corporate social responsibility initiatives, are heavily investing in children's oral health education, fostering brand loyalty that often carries into adulthood. Meanwhile, the adult segment is buoyed by a rising health consciousness and growing disposable incomes in key markets, leading to a trend towards premium products and specialized solutions for age-related oral health challenges.

By Distribution Channel: Traditional Retail Leads Digital Transformation

In 2025, supermarkets and hypermarkets dominate with a 33.42% market share, capitalizing on their vast physical presence and consumers' preference for hands-on product evaluation and instant access. Meanwhile, online retail stores are emerging as the fastest-growing channel, boasting a 7.58% CAGR projected through 2031. This surge underscores a swift digital adoption and a shift in consumer inclinations towards convenience and a broader product range. This upward trajectory is in sync with the regional e-commerce boom, hinting at significant growth potential. Drug stores and pharmacies hold their ground, bolstered by expert recommendations and niche product selections. In contrast, other channels, such as traditional retail and direct sales, cater primarily to price-sensitive consumers and rural demographics.

This evolution in distribution channels mirrors a wider retail metamorphosis in the region. As consumers increasingly demand fluid transitions between physical and digital platforms, omnichannel strategies have become paramount. Traditional distributors continue to play a crucial role in numerous markets. This is especially true in areas where unstructured grocery channels command significant market shares. Such dynamics compel manufacturers to strike a balance between digital advancements and time-honored distribution partnerships, all while leveraging insights from local market nuances.

Geography Analysis

In 2025, the United Arab Emirates accounted for 32.18% of total revenue, driven by high per-capita spending and a retail landscape that accelerates premium product launches. Duty-free zones introduce global travelers to flagship innovations, and Dubai's bustling tourist scene ensures rapid product trials. While domestic regulations enforce halal compliance, they also promote functional claims, allowing brands to stand out without protracted approval processes.

Saudi Arabia, a heavyweight in terms of volume, sees its Vision 2030 reforms spurring private healthcare investments and boosting consumption among the upper-middle class. Government-imposed sugar taxes have heightened public awareness of oral health, leading to a surge in demand for rinses and sensitivity care. South Africa, leading the growth with a 7.33% CAGR, is reaping benefits from an expanding middle class and broader medical aid coverage. Production hubs near Johannesburg are slashing logistics costs and speeding up shelf life for entry-level products.

While Nigeria and Egypt boast potential due to their large populations, challenges like currency fluctuations and a fragmented retail landscape temper immediate profit margins. E-commerce giants Jumia and Noon are broadening their last-mile delivery networks, addressing infrastructure challenges. Both Kenya and Morocco are witnessing a budding appetite for premium products, capitalizing on their growing urban middle classes and regional free-trade agreements. Navigating these diverse markets demands nimble strategies that harmonize affordability, halal compliance, and swift innovation.

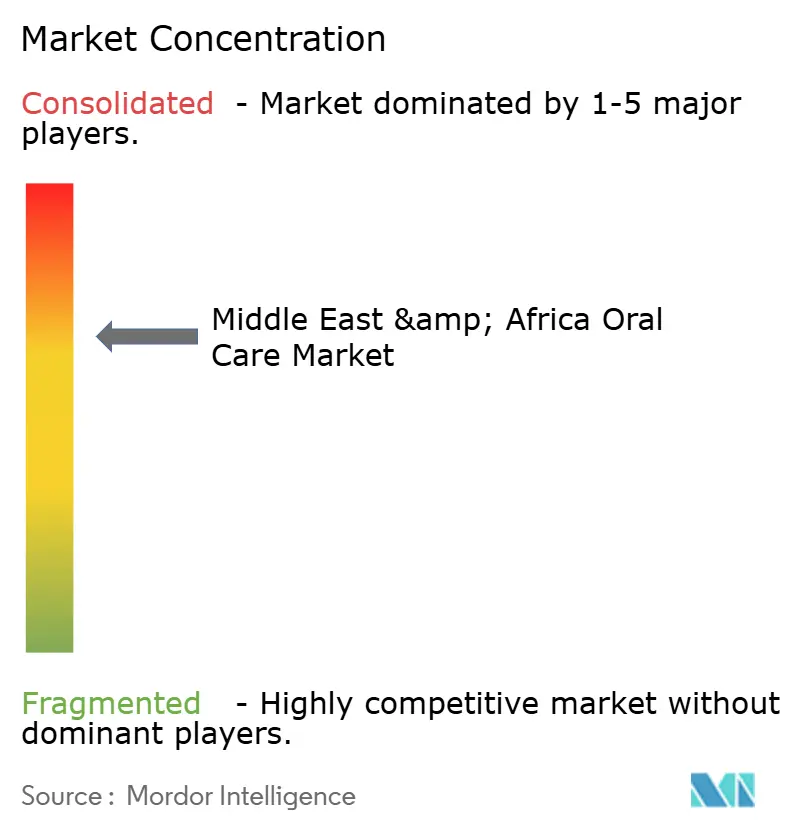

Competitive Landscape

In the fragmented oral care industry of the Middle East and Africa, global giants like Colgate-Palmolive, Unilever, and Procter & Gamble leverage scale marketing and endorsements from dentists to secure prime shelf positions. These brands also invest in school programs and subsidized check-ups, laying the groundwork for future brand loyalty. Philips, with its engineering expertise, has carved out a dominant position in the electric-brush segment. Meanwhile, emerging local brands are appealing to value-conscious shoppers by offering smaller pack sizes and halal certifications.

Innovation is centered around clinically proven ingredients, such as stannous fluoride, nano-hydroxyapatite, and zinc lactate, that command premium pricing. Start-ups are tapping into direct-to-consumer subscriptions, harnessing the power of social commerce and adaptable contract manufacturing. A collective effort is underway to combat counterfeiting; companies are teaming up with customs to implement AI-driven track-and-trace systems and are using tamper-evident holograms.

Regulatory hurdles, like halal accreditation, ISO 22716 GMP standards, and the newly introduced sustainability labeling in the GCC, elevate costs for smaller entrants. Yet, regional producers are turning this challenge into an opportunity. By customizing flavors and fragrances to suit local tastes, they're gradually capturing market share from multinationals in the mass-market paste segment. Furthermore, collaborations between device manufacturers and telecom companies are paving the way for Bluetooth-enabled oral health apps, signaling a blend with the larger digital health landscape.

Middle East and Africa Oral Care Industry Leaders

-

Procter & Gamble

-

Colgate-Palmolive Company

-

Unilever PLC

-

GlaxoSmithKline PLC

-

Johnson & Johnson

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Nature’s Renaissance International (NRI) introduced two new oral care products into the Nigerian market, UATD Eyi toothpaste for adults and UATD Eyi children’s toothpaste. The adult variant was produced with natural ingredients including charcoal and herbal extracts, while the children’s version comes in strawberry and grape flavours. NRI described the products as part of its commitment to providing locally sourced solutions to health challenges in Nigeria.

- November 2024: A toothpaste factory, the first of its kind, was launched in Rwanda by RK Industries Ltd., marking a significant step in the country's industrial development. The Pro Smile Toothpaste Factory was established in the Kigali Special Economic Zone with a USD 5 million investment, aiming to reduce the dependency on imported oral hygiene products and create local jobs.

- October 2024: Colgate introduced AI-powered toothbrushes into the MEA market. These smart toothbrushes featured real-time brushing feedback and personalized oral health analytics, targeting technologically adept consumers seeking advanced oral care solutions. This launch reflected a trend towards digital integration within the oral care sector, aiming to improve user experience and efficacy.

- January 2024: Laifen, a pioneer in personal care appliances introduced its revolutionary Laifen Wave Electric Toothbrush at CES 2024. The Wave boasts a handle crafted from durable materials such as aluminium, stainless steel, and ABS plastic. Featuring a cutting-edge servo system developed by Laifen, the Wave sets itself apart by seamlessly combining 60° oscillation and vibration, addressing a persistent challenge many electric toothbrushes face: the balance between powerful cleaning and gentle gum protection.

Middle East and Africa Oral Care Market Report Scope

The oral care market represents the products that are being used to maintain oral hygiene and oral health.

The report covers a range of products available in the market, including breath fresheners, dental floss, denture care, mouthwashes and rinses, toothbrushes and replacements, and toothpaste. Additionally, it covers the various channels, such as supermarkets/hypermarkets, convenience/grocery stores, pharmacies, drug stores, online retail stores, and other distribution channels through which the products are distributed. The study also covers the market analysis of major countries, such as Saudi Arabia, South Africa, and the Middle East and Africa.

The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Toothpaste | |

| Toothbrushes and accessories | Manual Toothbrushes |

| Electric Toothbrushes | |

| Mouth Fresheners | |

| Mouthwashes/rinses | |

| Denture care products | |

| Dental Floss |

By Ingredient

| Conventional |

| Organic |

By End User

| Kids/Children |

| Adults |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Drug Stores/Pharmacies |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| United Arab Emirates |

| South Africa |

| Saudi Arabia |

| Nigeria |

| Egypt |

| Kenya |

| Morocco |

| Turkey |

| Rest of Middle East and Africa |

| By Product Type | Toothpaste | |

| Toothbrushes and accessories | Manual Toothbrushes | |

| Electric Toothbrushes | ||

| Mouth Fresheners | ||

| Mouthwashes/rinses | ||

| Denture care products | ||

| Dental Floss | ||

| By Ingredient | Conventional | |

| Organic | ||

| By End User | Kids/Children | |

| Adults | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Drug Stores/Pharmacies | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | United Arab Emirates | |

| South Africa | ||

| Saudi Arabia | ||

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Middle East Africa oral care market in 2031?

The market is expected to reach USD 5.66 billion by 2031, expanding at a 5.73% CAGR.

Which product category is growing the fastest across Middle East and Africa?

Mouthwashes and rinses are posting the highest 6.43% CAGR on rising demand for multi-step oral routines.

How large is the children’s segment relative to adults?

Adults hold 87.30% of sales, but children’s lines are growing faster at 7.08% CAGR thanks to school-based education programs.

Why is online retail critical for future growth?

E-commerce, though only 5% of retail today, enjoys a 7.58% CAGR as mobile usage and social-media driven discovery accelerate direct-to-consumer sales.

Which geography is set for the quickest expansion?

South Africa leads regional growth with a forecast 7.33% CAGR through 2031, supported by an expanding middle class and better healthcare access.

Page last updated on: