Mouthwash Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 6.63 Billion |

| Market Size (2031) | USD 8.25 Billion |

| Growth Rate (2026 - 2031) | 4.47% CAGR |

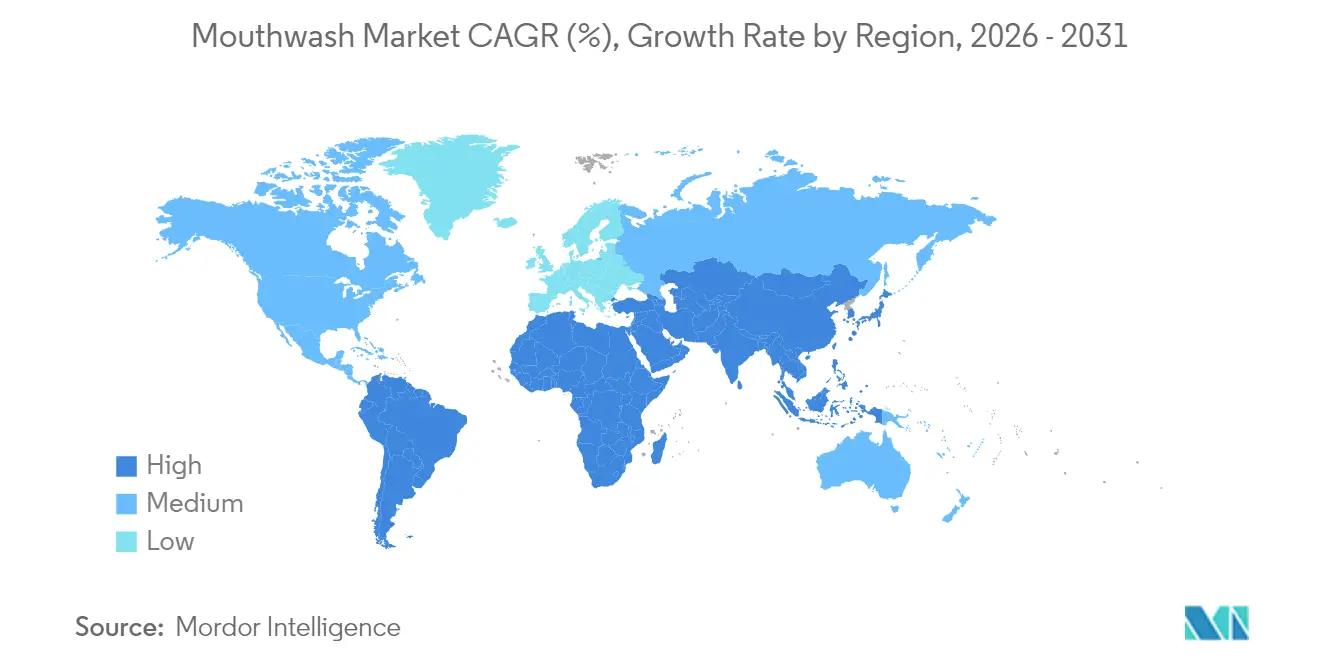

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

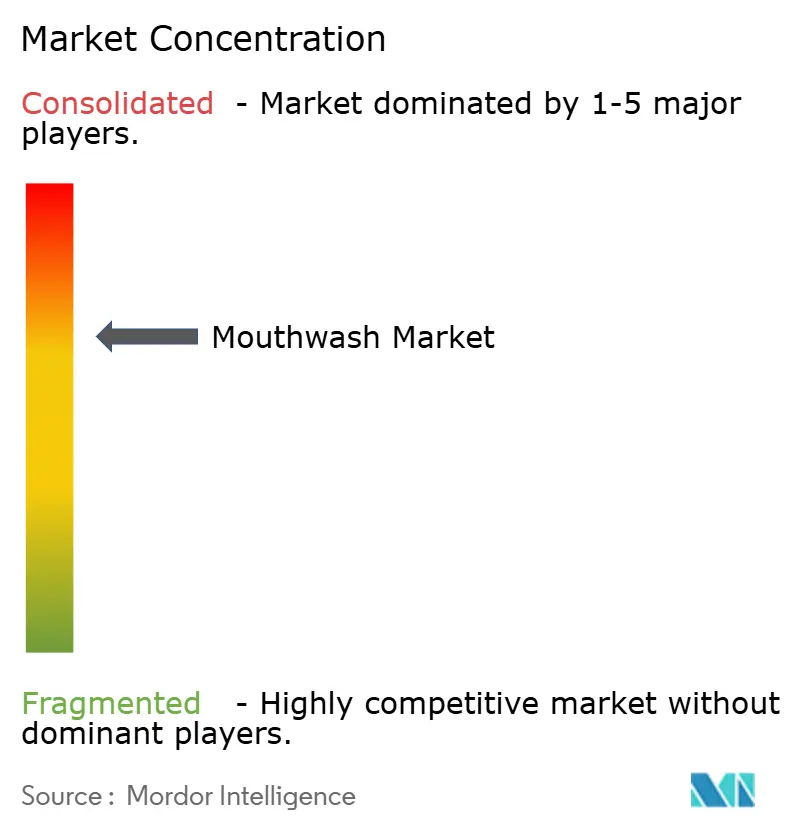

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mouthwash Market Analysis by Mordor Intelligence

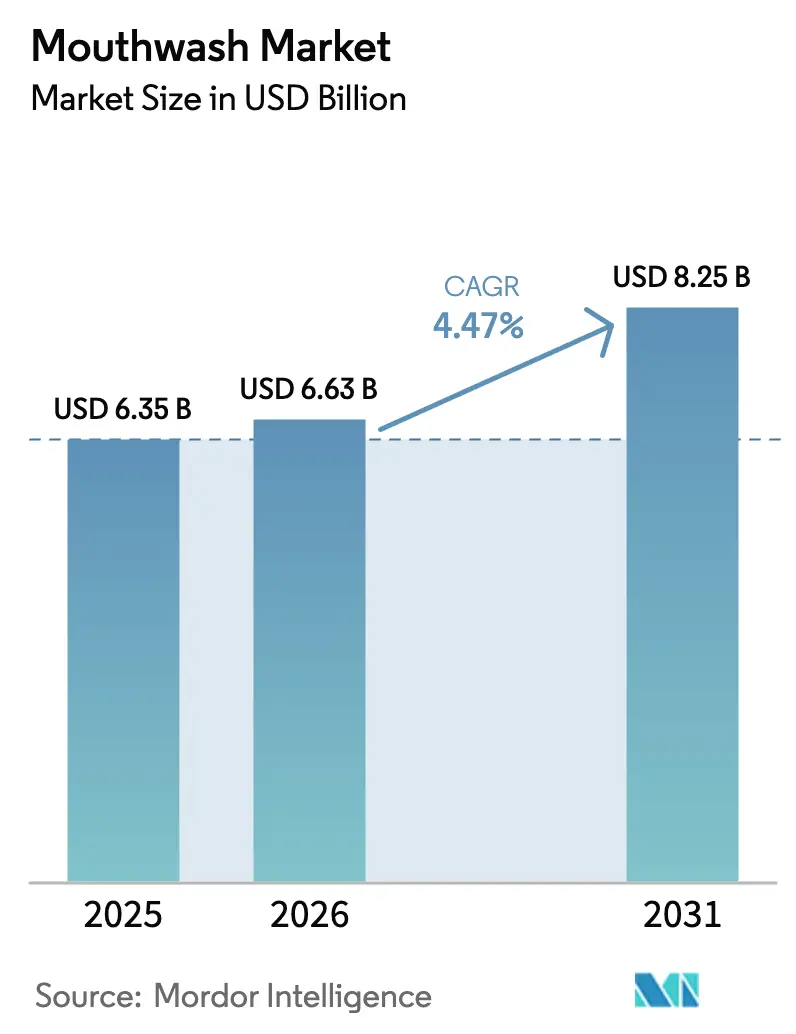

The mouthwash market size in 2026 is estimated at USD 6.63 billion, growing from 2025 value of USD 6.35 billion with 2031 projections showing USD 8.25 billion, growing at 4.47% CAGR over 2026-2031. This growth highlights the market's steady expansion, driven by changing consumer preferences and evolving regulations. Therapeutic mouthwash products are witnessing higher demand as government fluoride programs and increased endorsements from dental professionals encourage consumers to shift from cosmetic rinses to products with health benefits. The trend of premiumization is gaining momentum, with consumers increasingly opting for clinically proven formulations that offer benefits such as disease prevention, teeth whitening, and breath freshening. Research and development efforts are intensifying, focusing on innovations like alcohol-free formulations, natural ingredients, and advanced delivery systems. These advancements are reshaping the competitive landscape of the market. Global oral health campaigns are also playing a significant role in promoting daily mouthwash use as an essential part of overall wellness, rather than just an optional hygiene step. The mouthwash market is moderately consolidated, with key players driving innovation and competition.

Key Report Takeaways

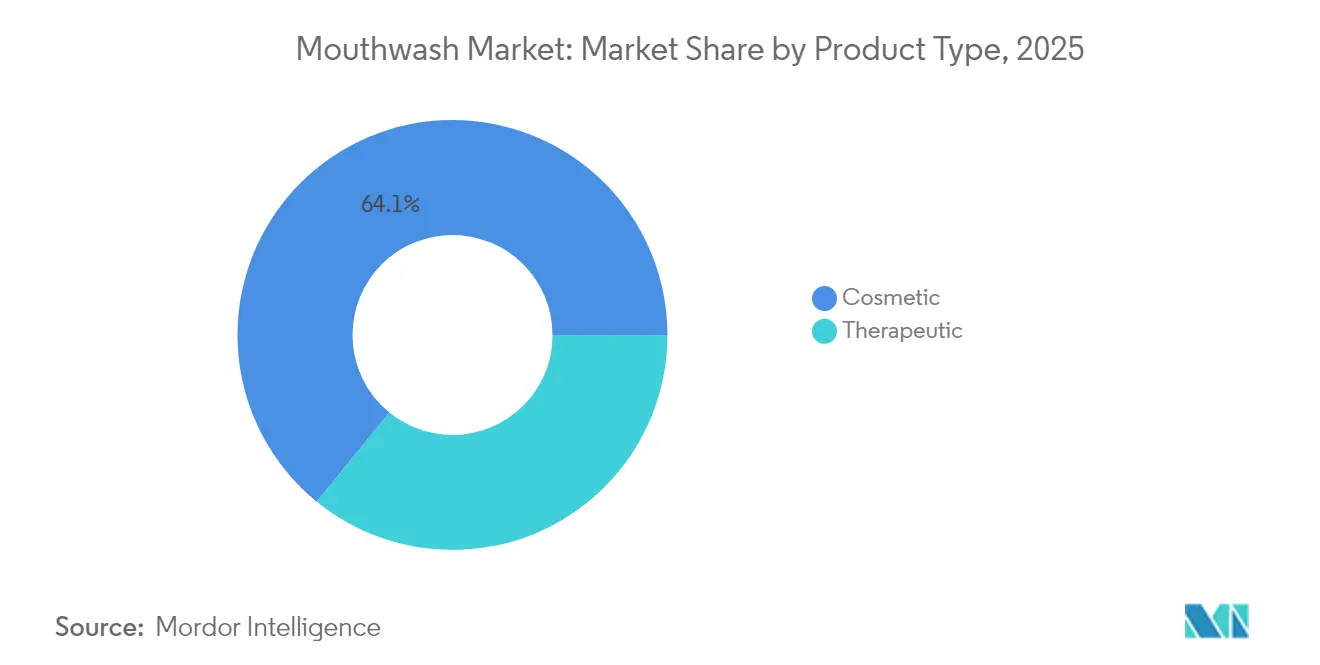

- By product type, cosmetic variants led with 64.12% of mouthwash market share in 2025, while therapeutic solutions are advancing at a 6.18% CAGR through 2031.

- By nature, conventional formulations accounted for 86.22% of the mouthwash market size in 2025; organic options are expanding at an 7.77% CAGR to 2031.

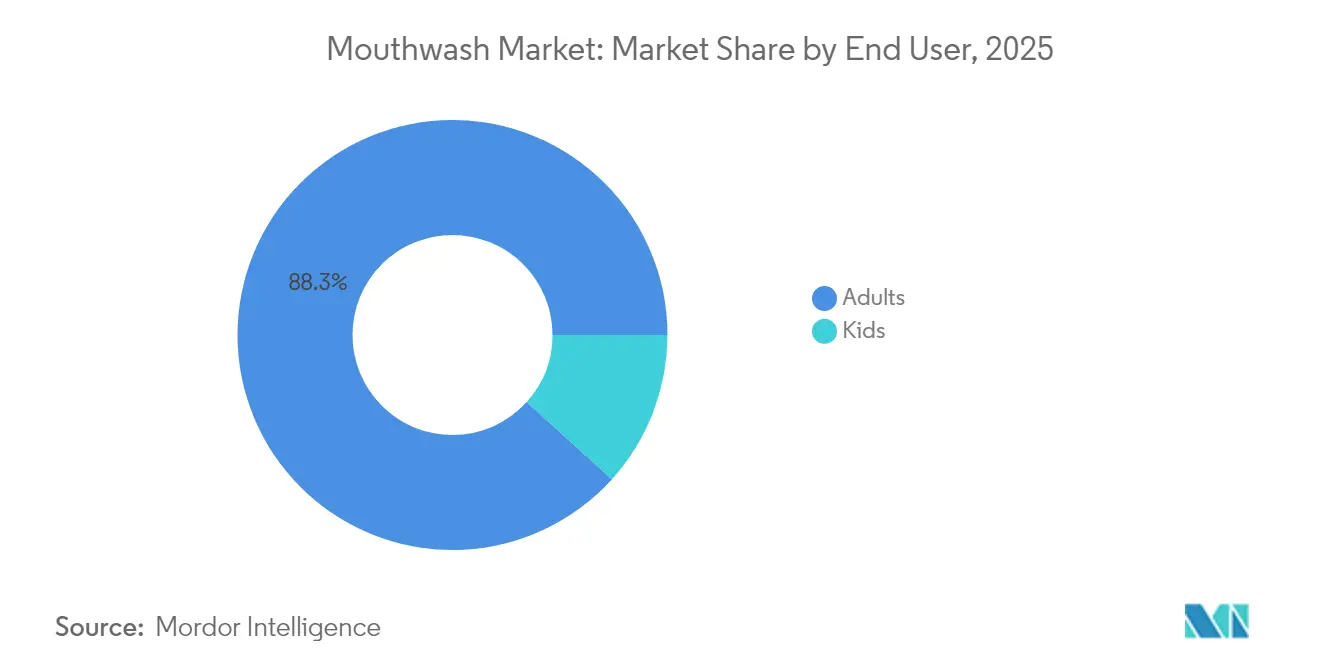

- By end user, adults captured 88.30% of the mouthwash market share in 2025, whereas kids’ formulations are forecast to rise at a 6.96% CAGR by 2031.

- By packaging, bottles retained 66.92% of the mouthwash market size in 2025; pouches deliver the fastest 5.44% CAGR through 2031.

- By distribution channel, supermarkets/hypermarkets commanded 36.10% mouthwash market share in 2025, but online retail is growing at 7.99% CAGR to 2031.

- By geography, North America accounted for 35.20% of the mouthwash market size in 2025; Asia-Pacific is expanding at an 6.72% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mouthwash Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising oral health awareness | +0.8% | Global, with stronger impact in North America and Europe | Medium term (2-4 years) |

| Government fluoride and oral-health initiatives in public schools | +0.6% | North America and Europe core, expanding to Asia-Pacific | Long term (≥ 4 years) |

| Growing demand for cosmetic and aesthetic oral care | +0.7% | Global, led by North America and urban Asia-Pacific markets | Short term (≤ 2 years) |

| Innovation in product formulation | +0.5% | Global, with Research and Development concentration in North America and Europe | Medium term (2-4 years) |

| Shift toward alcohol-free and herbal formulations | +0.4% | Global, strongest in Europe and urban Asia-Pacific | Medium term (2-4 years) |

| Uptick in professional dentist recommendations | +0.6% | North America and Europe core, spill-over to Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising oral health awareness

Awareness about oral health is steadily increasing, supported by various government programs and public health campaigns. These initiatives include training health workers with detailed guides that emphasize the importance of maintaining oral hygiene through practices like regular brushing and using mouthwash to prevent dental issues. On a global scale, oral diseases affect approximately 3.7 billion people every year, as reported by the World Health Organization, which highlights the urgent need for preventive oral care solutions[1]Source: World Health Organization, "Oral health," who.int. Consumer interest in oral health is growing, with recent data from the Oral Health Foundation revealing that 93% of United Kingdom adults in 2024 feel comfortable discussing their oral health with family and friends[2]Source: Oral Health Foundation, "New data reveals 93% of UK adults are willing to open up about their oral health," dentalhealth.org. This indicates a cultural shift where oral hygiene is becoming a key part of overall health and wellness. These combined efforts are helping people understand the importance of oral care.

Government fluoride and oral-health initiatives in public schools

Government fluoride programs are playing a key role in shaping the development and marketing of children's oral care products, especially mouthwashes. In the United States, public schools are required to implement fluoride mouth rinse programs with guidelines for age-appropriate fluoride concentrations. For example, Ohio's Revised Code mandates that school staff or volunteers cannot administer a fluoride mouth rinse to a student without receiving a signed consent form from the student's parent or guardian. This ensures that parents are involved in their child's oral care decisions. These regulations require companies to conduct clinical testing, which creates challenges for new brands trying to enter the market. Furthermore, in March 2025, the Food and Drug Administration (FDA) took action to remove unapproved ingestible fluoride prescription drug products for children from the market[3]Source: Food and Drug Administration, "FDA Begins Action To Remove Ingestible Fluoride Prescription Drug Products for Children from the Market," fda.gov. This move highlights the growing focus on safety and effectiveness in pediatric oral care.

Uptick in professional dentist recommendations

Recommendations from dentists play a significant role in increasing the use of therapeutic mouthwashes. Dentists often prescribe specific types of mouthwash, such as those targeting gum diseases, gingivitis, or providing fluoride protection, based on the unique needs of their patients. A survey conducted by Scientific Research Publishing, in May 2024, revealed that 49% of respondents used mouthwash to address bad breath, 37% to manage gum disease, and 10% for relief from throat discomfort[4]Source: Scientific Research Publishing, "Knowledge and the Attitude on the Use of Mouthwash among Two Selected Senior High Schools in Kumasi," scirp.org. Dentists often provide these recommendations, encouraging patients to prioritize therapeutic benefits over cosmetic features. Major brands invest in educational programs and clinical research to keep dentists informed and engaged. This ensures that dentists continue to recommend their products, helping these brands expand their market presence. Since consumers often rely on expert advice for oral care products, this professional influence significantly boosts the growth of the therapeutic mouthwash segment.

Innovation in product formulation

Innovation in product formulation is playing a significant role in driving the growth of the mouthwash market. Brands are focusing on advanced technologies to improve the effectiveness, safety, and overall appeal of their products. Techniques such as encapsulation, pH balancing, and multi-ion complexes like zinc–amine fluoride are being used to enhance the delivery of active ingredients, reduce irritation, and increase product shelf life. For example, in October 2023, Kenvue launched the Listerine® Clinical Solutions line, which uses Rapid Fusion Technology to boost fluoride absorption and strengthen teeth. Similarly, in April 2024, Lion Corporation introduced its OCH-TUNE mouthwash line, featuring pH-balancing formulations designed for personalized oral care. These advancements not only make products more effective but also create a competitive edge for established brands.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Strong competition from alternatives | -0.9% | Global, particularly intense in price-sensitive markets | Short term (≤ 2 years) |

| Concerns around alcohol-based formulas | -0.5% | Global, strongest impact in health-conscious demographics | Medium term (2-4 years) |

| Price sensitivity in developing regions | -0.7% | Asia-Pacific, Middle East and Africa, and Latin America core markets | Long term (≥ 4 years) |

| Perception of mouthwash as non-essential | -0.4% | Global, varying by cultural oral hygiene practices | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong competition from alternatives

The mouthwash market is experiencing growing competition from alternative oral care products such as water flossers and probiotic lozenges. These alternatives are becoming increasingly popular among consumers who are looking for innovative or natural ways to maintain oral hygiene. Many of these products are backed by clinical studies that demonstrate their effectiveness, which puts pressure on traditional cosmetic mouthwashes to prove their value. Products that lack therapeutic benefits or scientific backing are at risk of being perceived as less effective, especially in online marketplaces where consumers can easily compare features and reviews. To address this challenge and retain market share, companies are introducing bundled offerings that combine mouthwash with other oral care products like toothbrushes and floss. These bundles encourage brand loyalty by creating a comprehensive oral care solution within a single platform.

Concerns around alcohol-based formulas

Concerns about alcohol-based mouthwash formulas are slowing market growth, as research has linked excessive use to issues like irritation of the mouth lining and potential cancer risks. These findings have led to more cautious recommendations in professional guidelines. Retailers and insurance providers are also becoming hesitant to stock or promote mouthwashes with high alcohol content unless safer alternatives are available. To address these challenges, companies are increasingly focusing on creating alcohol-free mouthwash options. These alternatives use ingredients such as essential oils or quaternary ammonium compounds to provide similar antimicrobial benefits without the risks associated with alcohol. Brands are taking steps to educate consumers by including clear and transparent labeling on product packaging. They are also launching dedicated educational websites to raise awareness about the safety and benefits of alcohol-free formulations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Therapeutic Gains Ground Despite Cosmetic Dominance

Cosmetic mouthwashes led the mouthwash market in 2025, accounting for 64.12% of the total market share. This segment's popularity is driven by consumer preferences for products that offer teeth-whitening benefits and long-lasting fresh breath. The wide availability of these products through offline and online retail channels, combined with appealing flavors and attractive packaging, makes them a convenient choice for many. Marketing campaigns emphasizing aesthetic benefits further boost their demand. Despite growing awareness of oral health, cosmetic mouthwashes remain a preferred option for consumers seeking quick and visible results in their daily oral care routines.

Therapeutic mouthwashes are rapidly gaining traction and are expected to be the fastest-growing segment, with a projected CAGR of 6.18% between 2026 and 2031. This growth is primarily driven by increasing dentist recommendations for products containing antimicrobial and fluoride-based ingredients to address issues like gingivitis, plaque, and periodontal diseases. Consumers are increasingly trusting advanced formulations with clinically proven benefits, which is encouraging adoption. Rising health awareness, tele-dentistry consultations, and oral health campaigns are promoting the use of therapeutic mouthwashes. This shift highlights a growing trend of consumers viewing mouthwash as an essential part of preventive oral care rather than just a cosmetic product.

By Nature: Organic Segment Surges Despite Conventional Leadership

Conventional mouthwash formulations dominated the market in 2025, accounting for 86.22% of the total market share. Their popularity is largely due to their widespread availability in retail stores, established brand reputation, and consumer familiarity with traditional flavors and ingredients. These products are often marketed as reliable and effective solutions for daily oral hygiene, which resonates with a broad audience. Their affordability and ease of use make them a convenient choice for consumers looking for basic oral care. Despite the emergence of new trends, conventional mouthwashes continue to be the go-to option for many households worldwide.

On the other hand, organic mouthwashes are rapidly gaining traction and are expected to grow at a robust CAGR of 7.77% through 2031. This growth is fueled by increasing consumer interest in natural and sustainable products, as well as a preference for alcohol-free and chemical-free formulations. Organic mouthwashes often feature plant-based ingredients and eco-friendly packaging, appealing to environmentally conscious buyers. Health-focused consumers are also drawn to these products for their gentle yet effective oral care benefits. As awareness of clean-label and sustainable practices grows, organic mouthwashes are carving out a significant niche in the market, attracting both new and existing users.

By End User: Adult Market Stability Contrasts with Kids Segment Innovation

In 2025, adults represented the largest segment in the mouthwash market, accounting for 88.30% of the total market share. This dominance is primarily due to the widespread use of mouthwash as part of daily oral care routines among adults. The availability of various products catering to specific oral health needs, such as gum care and fresh breath, has further boosted this segment. Trusted brands, familiar flavors, and effective marketing campaigns emphasizing convenience and oral health benefits continue to attract adult consumers. The growing awareness of maintaining long-term oral hygiene has solidified the importance of mouthwash in adult oral care practices.

The kids' mouthwash segment, on the other hand, is expected to grow significantly, with a projected CAGR of 6.96% through 2031. This growth is fueled by increasing parental awareness of the importance of early oral hygiene habits. Pediatric dentists are actively recommending mouthwash for children to prevent cavities and promote healthy teeth. To cater to this demand, companies are introducing products with kid-friendly flavors, colorful packaging, and interactive designs to make oral care more appealing to children. These efforts aim to encourage children to adopt good oral hygiene practices early, while also addressing the rising demand for safe and effective products specifically designed for younger users.

By Packaging Type: Sustainability Drives Pouches Growth Despite Bottles Dominance

Bottled mouthwash formats were the leading choice in the market in 2025, holding 66.92% of the total market share. Their popularity stems from their ease of use, durability, and availability in retail outlets like supermarkets and pharmacies. Consumers find bottled mouthwash convenient for daily oral care, as the design allows for easy dosing and consistent application. The sturdy packaging also ensures product quality and builds trust in established brands. These factors make bottled formats a reliable and preferred option for a wide range of users looking for effective oral hygiene solutions.

Pouch formats, meanwhile, are rapidly gaining popularity and are projected to grow at a CAGR of 5.44% through 2031. Their lightweight and compact design makes them cost-effective for shipping and aligns with the growing demand for sustainable packaging. Many brands are marketing pouches as eco-friendly alternatives, appealing to environmentally conscious consumers. Their refillable nature offers a practical and budget-friendly option for users, reducing waste while maintaining oral hygiene. This emerging segment provides brands with an opportunity to cater to consumers seeking both convenience and sustainability in their oral care products.

By Distribution Channel: E-Commerce Disrupts Traditional Retail Patterns

Supermarkets/hypermarkets were the leading distribution channels in the mouthwash market in 2025, holding 36.10% of the total market share. These outlets attract a large number of customers due to their convenience and accessibility. Products are strategically placed on shelves to encourage impulse buying, making it easier for consumers to pick up mouthwash during routine shopping trips. Promotions, discounts, and in-store advertisements further boost sales in these retail formats. The trust and familiarity associated with supermarkets and hypermarkets make them a preferred choice for purchasing oral care products.

Online retail, however, is growing rapidly and is expected to achieve a CAGR of 7.99% by 2031. This growth is fueled by the increasing popularity of subscription services, which ensure regular delivery of products, and targeted online advertisements that cater to individual preferences. E-commerce platforms also offer convenience, allowing consumers to shop from home and access a wider range of products, including exclusive deals and bundles. Manufacturers are utilizing these platforms to directly engage with customers, offering personalized promotions and enhancing brand loyalty. As a result, online retail is becoming an essential channel for expanding the reach of mouthwash products.

Geography Analysis

North America held a significant 35.20% share of the mouthwash market in 2025, driven by high consumer spending, strong dentist recommendations, and clear regulatory guidelines on fluoride usage and product claims. While the market in this region continues to grow, the pace has slowed due to widespread adoption and market saturation. To address this challenge, companies are introducing innovative therapeutic products, such as solutions for dry mouth (xerostomia) and peri-implant care, to cater to specific consumer needs and unlock new revenue opportunities.

The Asia-Pacific region is witnessing the fastest growth, with a projected CAGR of 6.72%. This growth is supported by the rising middle-class population in urban areas, increasing access to dental insurance, and the influence of social media in promoting better oral care habits. Countries like China and India are driving this demand, with China's expanding tier-2 cities and India's school-based oral health initiatives playing a significant role. Consumer preferences for alcohol-free and herbal formulations, such as green tea or clove-based flavors, are encouraging global brands to tailor their products to meet local tastes and preferences.

In Europe, the market is growing steadily as environmentally conscious consumers increasingly prefer recyclable packaging and organic ingredients, in line with strict European Union cosmetic regulations. In the Middle East and Africa, adoption rates vary widely. Wealthier Gulf Cooperation Council countries are adopting premium products similar to those in Western markets, while rural areas in Africa still consider mouthwash a non-essential product. In Latin America, the market shows mixed trends. Brazil's growing orthodontic treatments are boosting demand for therapeutic mouthwash, but economic challenges and currency fluctuations in other countries are limiting price flexibility and overall market growth.

Competitive Landscape

The mouthwash market is moderately consolidated, with the top 5 companies accounting for approximately 70% of the total market share. Large multinational companies benefit from economies of scale in research, development, and marketing. For example, Church & Dwight’s acquisition of TheraBreath for USD 580 million expanded its portfolio of therapeutic products, strengthening its market position. Similarly, Colgate-Palmolive focuses on developing proprietary ingredients, such as cetylpyridinium-fluoride blends, to enhance partnerships with dentists and reduce competition from private-label brands.

Innovation in the market is increasingly focused on specialized mouthwash products designed for specific conditions, such as post-implant healing, plaque detection, or salivary diagnostics. Start-ups are leveraging faster clinical trials to introduce these niche products. E-commerce-focused brands are using subscription models and data analytics to customize flavor options and dosage recommendations, challenging the dominance of traditional retail players. Sustainability is also becoming a key focus, with companies like Lion committing to fully recyclable packaging by 2026, as environmental responsibility is now seen as a standard expectation rather than a unique selling point.

Capital investments in the industry are directed toward advanced technologies, such as micro-encapsulation for better ingredient delivery, AI-driven flavor development, and facilities for packaging with post-consumer recycled (PCR) content. Companies are also prioritizing the validation of product claims through peer-reviewed studies and real-world evidence, as consumers increasingly demand transparency and scientific backing. To build trust with informed and research-oriented buyers, firms are strengthening collaborations with universities and publishing open-access studies, which are becoming more critical than traditional advertising in gaining a competitive edge.

Mouthwash Industry Leaders

-

Colgate-Palmolive Company

-

Kenvue Inc.

-

Procter & Gamble Company

-

GlaxoSmithKline plc

-

Unilever plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: David's Health Lifesciences launched "Fresh Breath Mouthwash," which featured Hydroxi, a fluoride-free and alcohol-free formula developed with nano hydroxyapatite to promote gum detoxification and enamel health.

- February 2025: Colgate-Palmolive launched "Colgate Total Active Prevention" mouthwash in North America. The product focused on comprehensive oral health by targeting multiple dental concerns and providing advanced protection against bacteria and plaque buildup.

- February 2024: Sensodyne launched first mouthwash in India with the introduction of "Complete Protection+" variant. The alcohol-free formulation was designed to protect against tooth sensitivity, enamel wear, and cavities, while delivering a refreshing cool mint flavor without causing any burning sensation.

- March 2023: TheraBreath expanded its product portfolio by introducing its first children's mouthwash to the market. The company developed the product with fluoride as an active ingredient offering it in three certified organic flavors - Wacky Watermelon, Grapes Galore, and Strawberry Splash.

Global Mouthwash Market Report Scope

Mouthwash is an antibacterial liquid solution used for oral hygiene in terms of cleaning and rinsing the mouth, gums, and teeth. Antibacterial mouthwash provides long-lasting freshness and complete protection. Along with that, it prevents periodontitis, gingival bleeding, and bad breath with the medicated ingredients present in it that penetrate every corner of the mouth.

The global mouthwash market is segmented by type, distribution channel, and geography. By type, the market is segmented into conventional and therapeutic. Based on the distribution channel, the market studied is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. It provides an analysis of emerging and established economies across the world, comprising North America, Europe, South America, Asia-Pacific, the Middle East, and Africa.

For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Therapeutic |

| Cosmetic |

| Organic |

| Conventional |

| Kids |

| Adults |

| Bottles |

| Pouches |

| Others |

| Supermarkets/Hypermarkets |

| Pharmacies/Drug Stores |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Colombia | |

| Chile | |

| Peru | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Therapeutic | |

| Cosmetic | ||

| By Nature | Organic | |

| Conventional | ||

| By End User | Kids | |

| Adults | ||

| By Packaging Type | Bottles | |

| Pouches | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Pharmacies/Drug Stores | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Colombia | ||

| Chile | ||

| Peru | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the global mouthwash market in 2026?

The mouthwash market stands at USD 6.63 billion in 2026 and is projected to reach USD 8.25 billion by 2031 at a 4.47% CAGR.

Which region is growing fastest for mouthwash sales?

Asia-Pacific records the highest 6.72% CAGR through 2031, fueled by urbanization and rising oral-health awareness.

What segment shows the quickest growth within mouthwash?

Therapeutic formulations expand at a 6.18% CAGR owing to dentist endorsements and preventive-care positioning.

How is e-commerce reshaping the category?

Online retail grows at 7.99% CAGR as subscription models, personalized recommendations, and direct-to-consumer strategies gain popularity.

Page last updated on: