United States Menopause Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

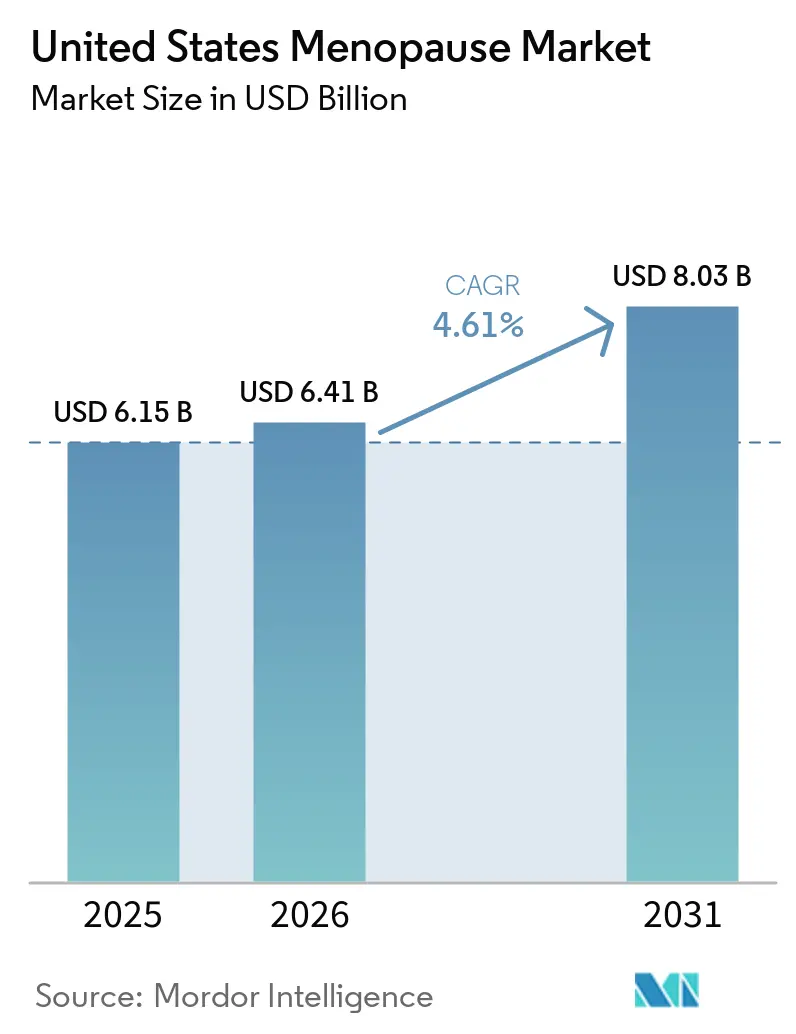

| Base Year Market Size (2025) | USD 6.15 Billion |

| Market Size (2026) | USD 6.41 Billion |

| Market Size (2031) | USD 8.03 Billion |

| Growth Rate (2026 - 2031) | 4.61% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Menopause Market Analysis by Mordor Intelligence

The United States Menopause Market size is expected to increase from USD 6.15 billion in 2025 to USD 6.41 billion in 2026 and reach USD 8.03 billion by 2031, growing at a CAGR of 4.61% over 2026-2031.

The United States menopause market is supported by steady demand because nearly 1.3 million women enter menopause each year in the country, and close to 6,000 women cross that threshold each day. This demand base is becoming more active in seeking treatment as menopause care is discussed more openly in clinical settings and in public health conversations. Prescribing confidence has also improved after the FDA removed the long-standing black-box warning on menopausal hormone therapies in November 2024 and then held a formal expert panel on hormone replacement therapy in July 2025. A large share of symptomatic women still remains untreated, which leaves room for further conversion across prescription, over-the-counter, and digitally enabled care models. The United States menopause market is also seeing stronger competition from pharmaceutical companies, virtual care providers, and consumer wellness brands, even as legacy safety concerns, reimbursement barriers for newer therapies, and input cost pressure continue to moderate the pace of adoption.

Key Report Takeaways

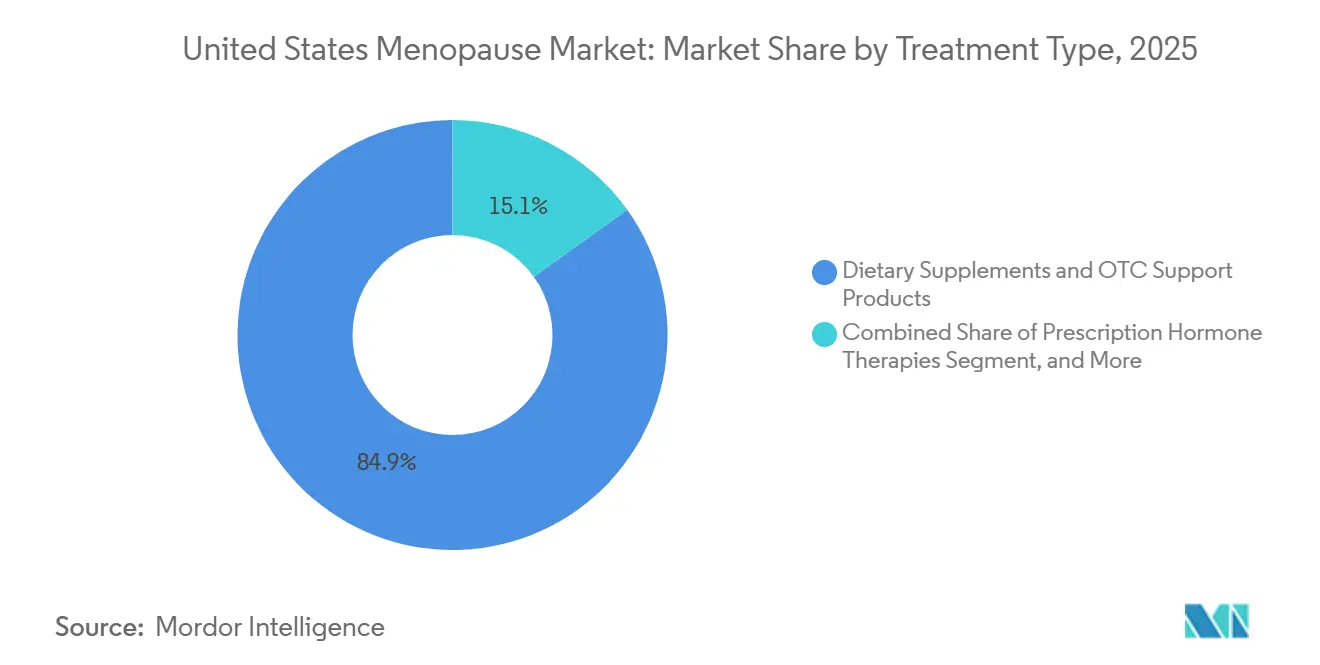

- By treatment type, dietary supplements & OTC support products led with 84.87% share in 2025, while prescription non-hormonal therapies are forecast to expand at a 5.06% CAGR through 2031.

- By primary symptom focus, vasomotor symptoms accounted for 53.83% share in 2025, while genitourinary syndrome of menopause is projected to grow at a 6.12% CAGR through 2031.

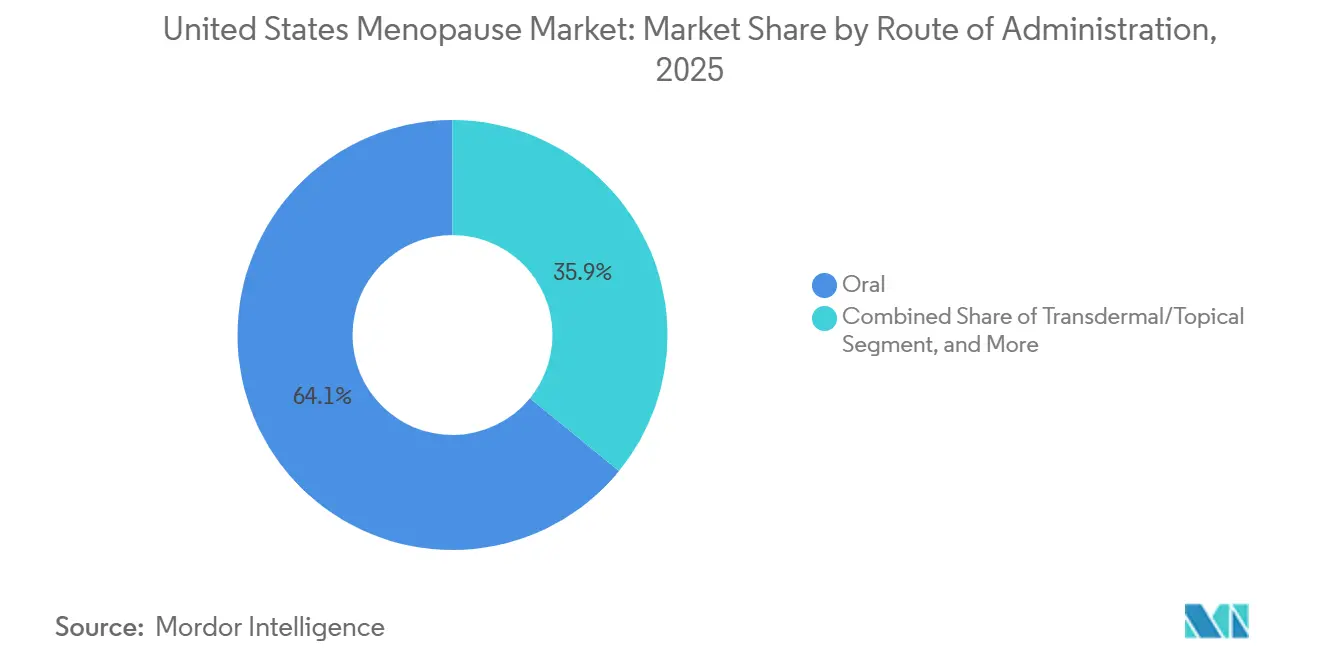

- By route of administration, oral formulations held 64.12% share in 2025, while transdermal and topical delivery are expected to advance at a 5.94% CAGR through 2031.

- By distribution channel, retail pharmacies and drugstores retained 47.23% share in 2025, while online pharmacies and direct-to-consumer platforms are projected to grow at a 6.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Menopause Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Large Symptomatic Female Cohort Entering Menopause | +1.2% | National, with elevated concentration in Sun Belt states such as Florida, Texas, and Arizona, and in coastal metros | Long term (≥ 4 years) |

| Rising Awareness and Destigmatization of Menopause Care | +0.9% | National, amplified in urban and suburban markets with high telehealth penetration | Medium term (2-4 years) |

| Non-Hormonal Prescription Innovation | +1.0% | National, with faster uptake in states with higher gynecologist density such as New York, California, and Massachusetts | Medium term (2-4 years) |

| Preference for Hormone-Free and Natural Symptom Relief | +0.7% | National, strongest in West Coast and Pacific Northwest markets | Short term (≤ 2 years) |

| Large Untreated Population With Conversion Runway | +0.6% | National, with rural and underserved markets representing the largest conversion opportunity | Long term (≥ 4 years) |

| Employer-Sponsored and Virtual Menopause Care | +0.5% | National, concentrated in states with large self-insured employer bases such as New York, California, Texas, and Illinois | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Large Symptomatic Female Cohort Entering Menopause

The United States menopause market is supported by a dense demographic wave as later Baby Boomers and early Generation X women move through menopause at the same time. The country adds nearly 1.3 million new menopause entrants each year, which keeps the care pool expanding even when broader health spending becomes cautious. This population is entering menopause with greater familiarity with digital care tools and with a stronger willingness to ask for treatment instead of accepting symptoms without support. That combination raises the likelihood of multi-modal care, including supplements, prescriptions, and virtual consultations, rather than one-time symptom management. The result is a durable demand base for the United States menopause market that is tied more to population structure and symptom burden than to discretionary spending.

Rising Awareness and Destigmatization of Menopause Care

The United States menopause market is benefiting from a clear change in how menopause is discussed at work, in clinics, and across consumer health channels. Awareness is improving through employer education, women’s health advocacy, and a broader media focus on symptoms that were often minimized in the past. The Society for Women’s Health Research found that 64% of employees want menopause-related workplace benefits, which shows that treatment demand is now visible inside employer settings as well as in physician offices.[1]Society for Women’s Health Research, “Roadmap to Menopause-Friendly Workplaces,” Society for Women’s Health Research, swhr.org This change is especially important in areas such as GSM, sleep disruption, and mood symptoms, where women often delay care or never raise the issue at all. The FDA’s July 2025 expert panel added further legitimacy to active treatment by focusing directly on hormone therapy risk and benefit communication.

Non-Hormonal Prescription Innovation

The United States menopause market is being reshaped by a new prescription class that gives women an alternative to hormone therapy for vasomotor symptoms. The approval of fezolinetant in 2023 and elinzanetant in October 2025 established neurokinin receptor targeting as the leading non-hormonal drug pathway in this space.[2]Bayer AG, “Lynkuet® (Elinzanetant), the First and Only Neurokinin 1 and Neurokinin 3 Receptor Antagonist, Receives FDA Approval for Moderate to Severe Hot Flashes Due to Menopause,” Bayer, bayer.com Bayer positioned elinzanetant as the first dual NK1 and NK3 receptor antagonist in the United States, supported by Phase 3 OASIS 1, 2, and 3 data showing meaningful reductions in the frequency and severity of moderate to severe hot flashes over both short and longer treatment periods. Astellas also showed the commercial traction of this class when VEOZAH generated JPY 46.6 billion, or USD 303 million, in global revenue in FY2025, with the United States as the primary driver. These launches matter beyond one symptom because the same pathway is being assessed for sleep and mood benefits, which could widen the prescribing base over time.

Employer-Sponsored and Virtual Menopause Care

The United States menopause market is also changing in the way care is delivered and paid for. Virtual clinics and employer-linked programs are making menopause support easier to access for women who do not have a local specialist or who prefer ongoing digital follow-up. Midi Health expanded its employer-linked virtual menopause clinic to all 50 states in 2024 and announced plans to add 150 clinicians, which showed how quickly these care models can scale when payer and employer channels open up.[3]Midi Health, “Midi Health Accelerates Mission, Closing USD 60M Series B Round,” Midi Health, joinmidi.com CVS Health added weight to this shift in March 2025 when it became the first company in the United States to earn Menopause Friendly Accreditation for its workforce support program. As more employers recognize menopause-related productivity loss and retention issues, the United States menopause market is likely to see more recurring demand flow through institutional channels rather than only through retail purchases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Hormone Therapy Safety Overhang | -0.9% | National, most pronounced in primary care settings with lower women’s health specialization | Long term (≥ 4 years) |

| Stringent Evidence and Regulatory Burden | -0.6% | National, affecting new entrants and the supplement category seeking clinical validation | Medium term (2-4 years) |

| Liver-Monitoring and Reimbursement Friction for NK-Targeted Therapies | -0.7% | National, concentrated in markets with restrictive formulary management | Short term (≤ 2 years) |

| Import-Cost Pressure on Hormone Formulations | -0.5% | National, with sharper impact on generic manufacturers reliant on active ingredient imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Legacy Hormone Therapy Safety Overhang

The United States menopause market still carries the effects of older hormone therapy risk perceptions, especially in general practice settings. A recent JAMA Internal Medicine reanalysis of Women’s Health Initiative trial data showed that hormone therapy can offer a net cardiovascular benefit for women aged 50-59 with vasomotor symptoms when timing and age at initiation are considered. Even so, prescribing behavior remains uneven because not all clinicians interpret current evidence in the same way. The American Academy of Family Physicians published guidance in July 2025 that continued to frame menopausal hormone therapy as having limited benefits and significant harms, which shows that professional messaging still differs across care settings. This leaves many eligible women untreated or delayed in treatment, which slows the conversion of clinical demand into realized sales across the United States menopause market.

Liver-Monitoring and Reimbursement Friction For NK-Targeted Therapies

The newer neurokinin-targeted prescription products add growth to the United States menopause market, but they also introduce practical barriers to broad use. The prescribing information for LYNKUET requires baseline liver function testing and continued monitoring for elevated liver enzymes, which makes access less frictionless than standard telehealth prescribing models. That requirement adds time, follow-up burden, and extra clinical coordination before treatment can begin. These therapies also carry a pricing premium over generic hormone options, while formulary access remains uneven across commercial and public plans. As a result, uptake is strongest among women with better insurance coverage or a willingness to self-pay, which narrows the near-term addressable pool even as clinical interest grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Prescription Innovation Erodes Supplement-Market Lock

Dietary supplements & OTC support products held 84.87% of the United States menopause market share in 2025, which reflects the long-standing habit of self-directed symptom management through easily accessible products. Their reach is broad because these products are sold through retail pharmacies, grocery outlets, and direct online subscriptions, which gives them a visibility advantage that prescription therapies cannot match. This leadership position, however, does not mean the category is secure from disruption. Prescription non-hormonal therapies are projected to grow at a 5.06% CAGR through 2031, which points to a gradual but meaningful shift in the United States menopause market toward clinically guided treatment options.

That shift is visible in how prescription and OTC boundaries are starting to blur. Bonafide Health launched Thermella in September 2024 as an OTC NK3R antagonist supplement priced at USD 40-45 per month, using the same broad biological pathway that has attracted strong interest in prescription vasomotor care. Within hormonal prescriptions, companies with broad portfolios still hold an important place because they cover both systemic and local treatment needs. Pfizer’s menopause hormone therapy portfolio includes Premarin, Prempro, Estring, Premarin Vaginal Cream, and Duavee, which gives it coverage across multiple patient profiles and symptom settings. Mayne Pharma also reported USD 178.4 million in FY2025 revenue from its women’s health business, with strong growth from IMVEXXY and BIJUVA, supported in part by a more favorable regulatory tone toward local estrogen therapies.

By Primary Symptom Focus: GSM Emerges as the Next Clinical Frontier

Vasomotor symptoms accounted for 53.83% of the United States menopause market size in 2025, which reflects how hot flashes and night sweats remain the main triggers for women to seek treatment. The leading drug launches in recent years have centered on this symptom group, and that focus has reinforced both physician attention and commercial investment. The approval of newer NK-targeted therapies has strengthened the prescription pathway for women who want relief without hormone use or who cannot take hormone therapy. That said, the United States menopause market is not staying limited to vasomotor care alone, because untreated symptoms in other categories are now drawing more clinical focus.

Genitourinary syndrome of menopause is forecast to expand at a 6.12% CAGR through 2031, making it the fastest-growing symptom segment in the United States menopause market. This growth reflects better recognition of GSM as a chronic and progressive condition rather than a narrow or optional quality-of-life issue. The segment had been held back by patient reluctance to discuss vaginal symptoms and by uneven provider familiarity with diagnosis and long-term management. Growth is also being supported by local estrogen options and by broader awareness that menopause care often requires treatment across multiple symptom clusters rather than in one isolated complaint. Sleep and mood symptoms could also become more commercially important if ongoing work around elinzanetant confirms benefits beyond vasomotor control, because that would widen the practical treatment scope for a single prescription class.

By Route of Administration: Transdermal Gains from Safety Repositioning

Oral formulations represented 64.12% of the United States menopause market size in 2025, reflecting the deep familiarity that prescribers and consumers have with tablets and capsules across both prescription and OTC categories. Oral delivery has benefited from convenience, established prescribing habits, and a product base that ranges from supplements to non-hormonal medicines. Even so, route choice is becoming a more active clinical issue within the United States menopause market because providers are paying closer attention to safety, tolerability, and adherence. This is especially relevant in hormone therapy, where the route can affect how patients and clinicians weigh benefit and risk.

Transdermal and topical delivery is projected to grow at a 5.94% CAGR through 2031, which makes it the fastest-rising route in the United States menopause market. Its momentum is tied to growing awareness that transdermal estrogen avoids first-pass liver metabolism and is often seen as a more favorable option for certain patients. The FDA’s late 2024 label change and its 2025 expert discussion around local estrogen therapies helped reinforce confidence in these formulations. The vaginal route is also gaining relevance as a focused choice for GSM, while injectable and other formats remain niche and largely limited to narrower clinical use. Overall, route innovation is pushing the United States menopause industry toward more individualized therapy selection rather than default reliance on oral products alone.

By Distribution Channel: DTC Platforms Challenge Retail Pharmacy Primacy

Retail pharmacies and drugstores held 47.23% of the United States menopause market share in 2025, supported by the volume strength of supplements and OTC products sold through large national chains. This channel still matters because it offers visibility, convenience, and immediate access for women who want symptom relief without scheduling a clinical visit. Retail also remains important for familiar hormone therapy brands and for broad consumer trust in pharmacy-based care. However, the United States menopause market is showing clear movement away from exclusive dependence on physical store networks.

Online pharmacies and direct-to-consumer platforms are expected to grow at a 6.79% CAGR through 2031, the fastest pace among all channel segments in the United States menopause market. Their appeal comes from combining consultation, prescription fulfillment, recurring product delivery, and ongoing symptom support within a single process. Bonafide’s expansion into more than 1,800 Target stores in 2025 also shows that successful digital-first brands are now moving both ways across the channel divide, using retail presence to widen reach while keeping direct relationships intact. Virtual menopause platforms such as Midi Health and other specialist care models are proving that bundled care plus dispensing can hold patients longer than channel-only retail models. This leaves the United States menopause industry with a more competitive distribution structure, where convenience, continuity of care, and insurance integration matter as much as shelf access.

Geography Analysis

The United States menopause market operates as a single national market, but treatment uptake still differs meaningfully by region. The Northeast and West Coast remain the most developed pockets for clinically guided menopause care. California, New York, and Massachusetts stand out because they combine higher specialist density, stronger telehealth use, and earlier adoption of newer prescription options. These regions were among the first to convert interest in NK-targeted therapies into sustained prescribing after the launch of VEOZAH and later LYNKUET. They also tend to show better alignment between patient awareness and provider readiness, which supports quicker treatment conversion in the United States menopause market.

The South is the largest volume opportunity in the United States menopause market because it has the biggest concentration of women in menopause age bands across fast-growing states such as Texas, Florida, and Georgia. Large metro areas such as Dallas, Houston, Miami, and Atlanta give both branded drug makers and digital platforms a wide patient base to target. Florida is especially important because it combines a large retiree population with a growing working-age female base, which broadens demand across both symptom intensity and treatment affordability levels. At the same time, this region still shows wider unmet need because menopause care is often handled by primary care physicians instead of specialists. That gap limits prescribing depth, but it also leaves meaningful room for telehealth-led expansion across the United States menopause market.

The Midwest is becoming a more active secondary growth zone in the United States menopause market because large self-insured employers in states such as Illinois and Michigan are helping normalize menopause care within benefit structures. Institutional support can lift uptake across supplements, prescriptions, and virtual consultations at the same time. Rural parts of the Midwest and Mountain West remain underserved because pharmacy closures, fewer specialists, and lower telehealth adoption still restrict access. Those same barriers create longer-term conversion potential as virtual infrastructure and employer-linked care continue to scale nationally.

Competitive Landscape

The United States menopause market has a split competitive structure. The supplement and OTC end is highly fragmented, with many brands competing on ingredients, symptom positioning, price, and digital engagement. No single consumer brand has reached a level that defines the category across the full market. The prescription side is more concentrated, with companies such as Pfizer, Bayer, Mayne Pharma, and Padagis holding stronger positions through regulated products, physician relationships, and access to pharmacy formularies. This creates a market where fragmentation remains high overall, but the prescription core is becoming more strategically important inside the United States menopause market.

One of the clearest competitive contests is in non-hormonal vasomotor therapy. Astellas established the category with VEOZAH, and its FY2025 global revenue of JPY 46.6 billion, or USD 303 million, showed that demand is real and scalable when a non-hormonal option wins physician acceptance. Bayer then entered with LYNKUET in October 2025 and positioned the drug around a dual NK1 and NK3 mechanism supported by the OASIS Phase 3 program. In hormonal therapy, Pfizer continues to compete through breadth of portfolio, while Mayne Pharma is strengthening its place through focused women’s health brands and momentum in local estrogen and combination products. These moves show that leadership in the United States menopause market now depends on portfolio depth, route choice, and the ability to serve multiple symptom needs.

Digital care companies are changing the competition in a different way. Midi Health expanded nationwide in 2024 and tied its virtual clinic model to employer and insurance-linked access, which helped move it beyond a niche direct-pay offer. Bonafide showed another path by launching Thermella in 2024 and then entering Target stores in 2025, which turned a digital-first menopause brand into a broader omnichannel player. The remaining white space is concentrated in rural populations, women with lower coverage, and patients who need multilingual or lower-friction care. Companies that can combine clinical credibility, pharmacy access, and ongoing patient engagement are likely to hold the strongest positions as the United States menopause market matures.

United States Menopause Industry Leaders

Astellas Pharma Inc.

Bayer AG

Flo Health Inc.

Pfizer Inc.

SPD Swiss Precision Diagnostics GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: FDA hosted an expert panel on menopause and hormone replacement therapy, where clinicians urged the agency to ease warning labels on low-dose estrogen treatments. Mayne Pharma cited this event as a key commercial catalyst, noting the panel's endorsement of removing the black-box warning on menopausal hormone therapies, particularly local and low-dose vaginal estrogen

- October 2025: Bayer received FDA approval for Lynkuet (elinzanetant) 60mg capsules for moderate to severe hot flashes due to menopause, making it the first and only dual neurokinin-1 and neurokinin-3 receptor antagonist approved in the US. Approval was supported by data from the Phase 3 OASIS 1, 2, and 3 trials, and the drug was made available in November 2025.

- September 2025: Bonafide Health expanded into retail, launching four products in over 1,800 Target stores and on Target.com for the first time, marking the first major retail move for this historically DTC-focused menopause supplement brand.

United States Menopause Market Report Scope

The menopause market encompasses the global ecosystem of medical treatments, pharmaceuticals, dietary supplements, and lifestyle products designed to manage symptoms and health risks associated with perimenopause, menopause, and postmenopause.

The United States menopause market report is segmented across several dimensions to capture the full scope of treatment and delivery options. By treatment type, the market includes prescription hormonal therapies, non‑hormonal therapies, and dietary supplements & OTC products. In terms of symptom focus, the segmentation covers vasomotor symptoms, genitourinary syndrome of menopause (GSM), sleep & mood disturbances, and bone & sexual health. The route of administration is divided into oral, transdermal/topical, vaginal, and injectable options. Finally, the distribution channels include retail pharmacies, online/DTC platforms, hospital pharmacies, and specialty clinics. Market forecasts are provided in terms of value (USD), offering insights into growth trends across all these segments.

| Prescription Hormone Therapies | Systemic Estrogen-Only Therapies |

| Estrogen-Progestogen Combination Therapies | |

| Local Vaginal Estrogen Therapies | |

| Prescription Non-Hormonal Therapies | NK-Targeted Therapies |

| SSRI / SNRI and Other Symptom-Targeted Prescriptions | |

| SERM and Other Non-Estrogen Therapies | |

| Dietary Supplements & OTC Support Products |

| Vasomotor Symptoms |

| Genitourinary Syndrome of Menopause |

| Sleep and Mood Symptoms |

| Bone, Sexual Health, and Healthy Aging Support |

| Oral |

| Transdermal / Topical |

| Vaginal |

| Injectable / Other |

| Retail Pharmacies & Drugstores |

| Online Pharmacies & Direct-to-Consumer |

| Hospital / Health-System Pharmacies |

| Specialty Clinics & Virtual Menopause Platforms |

| By Treatment Type | Prescription Hormone Therapies | Systemic Estrogen-Only Therapies |

| Estrogen-Progestogen Combination Therapies | ||

| Local Vaginal Estrogen Therapies | ||

| Prescription Non-Hormonal Therapies | NK-Targeted Therapies | |

| SSRI / SNRI and Other Symptom-Targeted Prescriptions | ||

| SERM and Other Non-Estrogen Therapies | ||

| Dietary Supplements & OTC Support Products | ||

| By Primary Symptom Focus | Vasomotor Symptoms | |

| Genitourinary Syndrome of Menopause | ||

| Sleep and Mood Symptoms | ||

| Bone, Sexual Health, and Healthy Aging Support | ||

| By Route of Administration | Oral | |

| Transdermal / Topical | ||

| Vaginal | ||

| Injectable / Other | ||

| By Distribution Channel | Retail Pharmacies & Drugstores | |

| Online Pharmacies & Direct-to-Consumer | ||

| Hospital / Health-System Pharmacies | ||

| Specialty Clinics & Virtual Menopause Platforms | ||

Key Questions Answered in the Report

What is the forecast value of menopause care in the United States by 2031?

The United States menopause market is forecast to reach USD 8.03 billion by 2031, up from USD 6.41 billion in 2026, at a 4.61% CAGR over 2026-2031.

Which treatment category currently leads spending in the United States?

Dietary supplements & OTC support products led in 2025 with 84.87% share, showing how strong self-directed care still is in this space.

Which symptom area is growing the fastest through 2031?

Genitourinary syndrome of menopause is the fastest-growing symptom segment, with a projected 6.12% CAGR through 2031.

Why are non-hormonal prescription therapies gaining traction?

Growth is being driven by recent FDA approvals for NK-targeted therapies such as fezolinetant and elinzanetant, which offer an alternative for women who prefer not to use hormones or cannot use them.

Which route of administration is gaining the most momentum?

Transdermal and topical delivery is growing the fastest at a 5.94% CAGR, helped by stronger clinical preference for routes that avoid first-pass liver metabolism in hormone therapy.

How are distribution channels changing in menopause care?

Retail pharmacies still led with 47.23% share in 2025, but online pharmacies and DTC platforms are expanding faster at a 6.79% CAGR because they combine consultation, fulfillment, and recurring engagement.

Page last updated on: