Progesterone Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

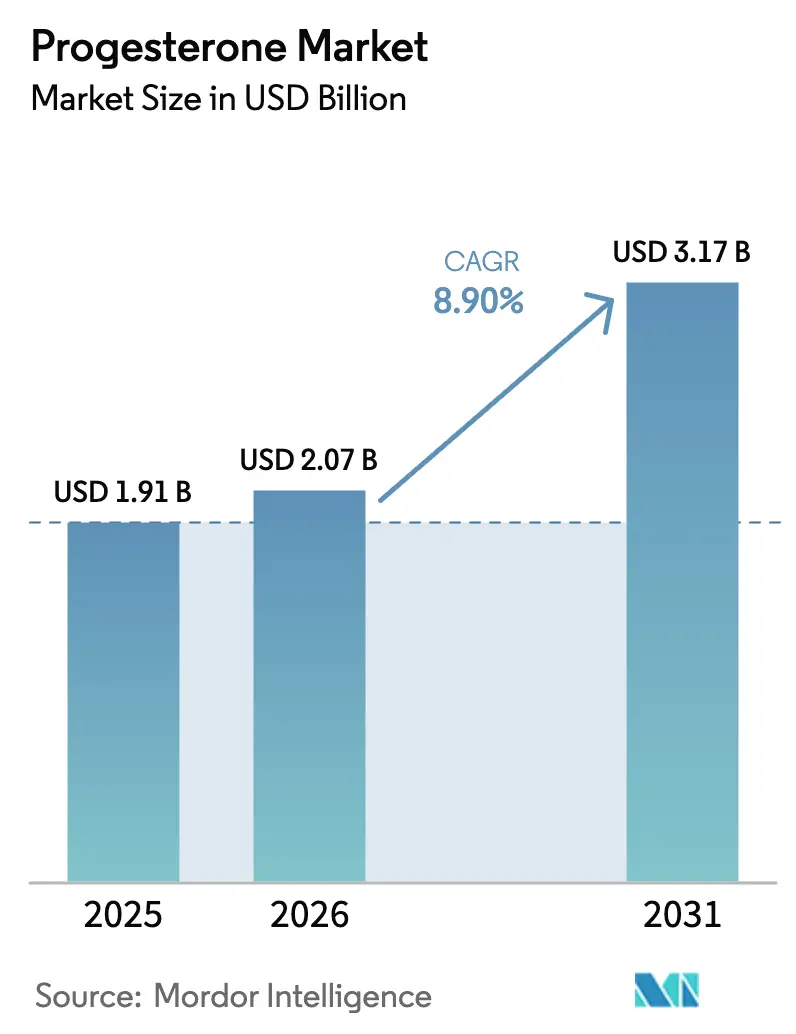

| Market Size (2026) | USD 2.07 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 8.90% CAGR |

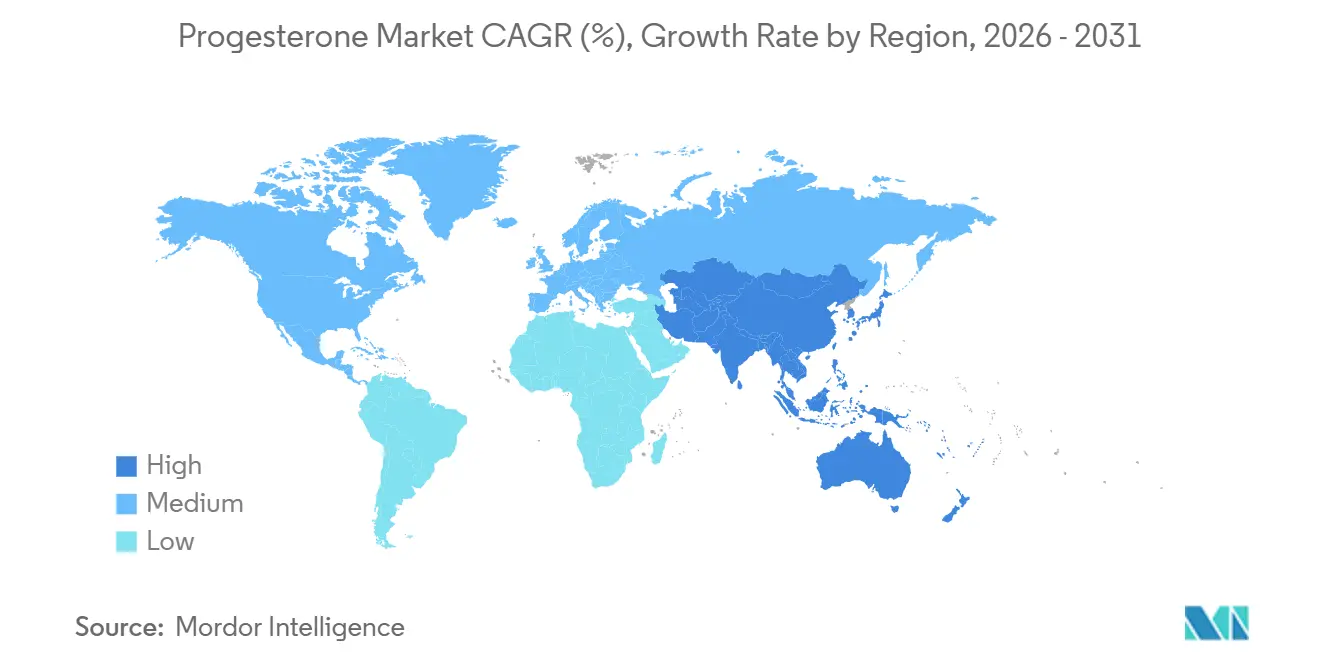

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

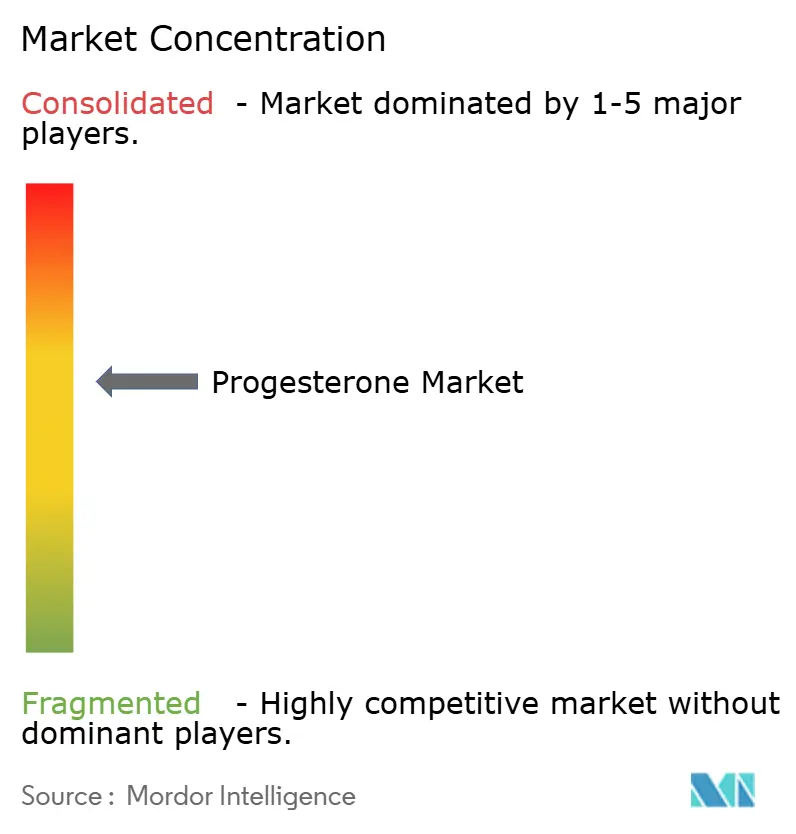

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Progesterone Market Analysis by Mordor Intelligence

The Progesterone Market size is projected to expand from USD 1.91 billion in 2025 and USD 2.07 billion in 2026 to USD 3.17 billion by 2031, registering a CAGR of 8.90% between 2026 to 2031.

Growing IVF cycle volumes, wider adoption of menopause therapy, and evolving clinical preferences for bioidentical hormone formulations are the core demand catalysts. Manufacturers are investing in micronization and sustained-release technologies to enhance convenience, while insurers are increasingly reimbursing frozen-embryo transfer protocols that require luteal-phase support. Regulatory agencies on both sides of the Atlantic are tightening quality oversight of compounded hormones, which is steering prescribers toward FDA- and EMA-approved products. Competitive dynamics are equally shaped by vertically integrated Indian producers that leverage diosgenin feedstock advantages to undercut branded prices in price-sensitive regions. Delivery-platform innovation, especially subcutaneous autoinjectors and biodegradable implants, remains a white-space opportunity as stakeholders aim to reduce clinic visits and improve adherence in resource-constrained settings.

Key Report Takeaways

- By product type, synthetic progesterone led with 64.34% of progesterone market share in 2025, while natural formulations are projected to expand at a 10.45% CAGR to 2031.

- By mode of delivery, injectables commanded 47.65% share of the progesterone market size in 2025, and oral formulations are advancing at a 10.67% CAGR through 2031.

- By application, menopause accounted for a 34.78% share of the progesterone market size in 2025, whereas endometrial cancer protocols are projected to grow at an 11.55% CAGR through 2031.

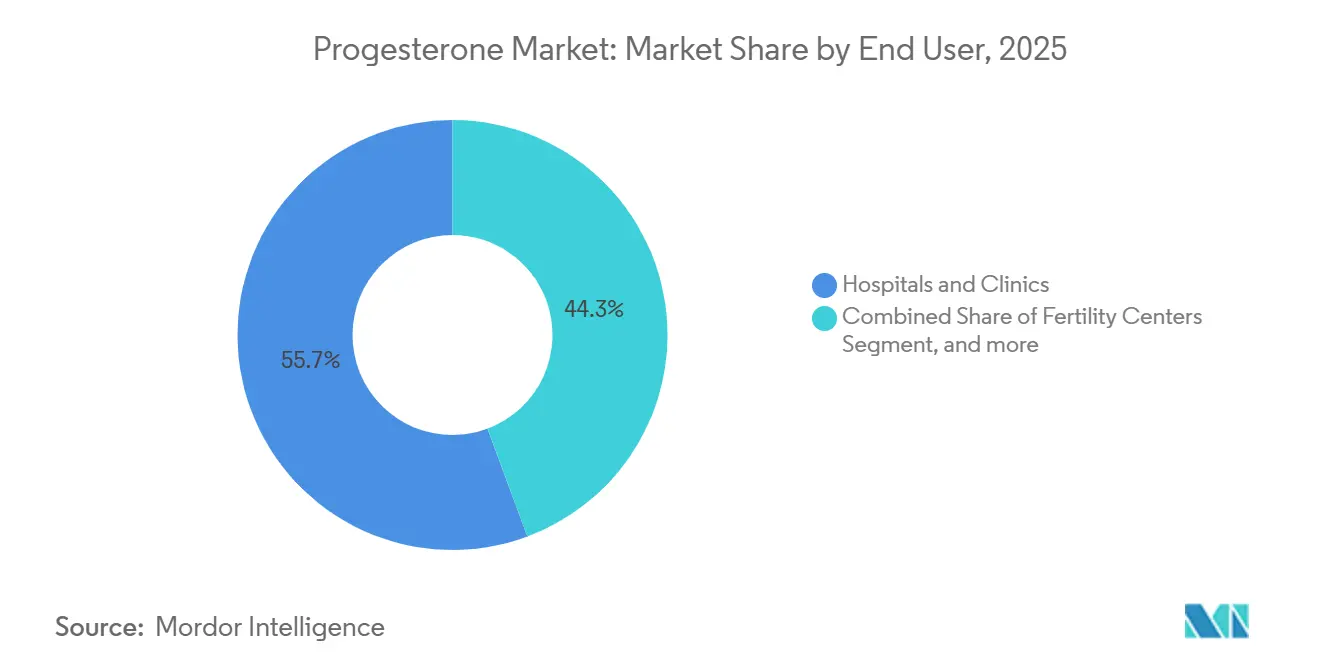

- By end user, hospitals and clinics held 55.67% of the progesterone market share in 2025, yet fertility centers are projected to rise at an 11.67% CAGR between 2026 and 2031.

- By distribution channel, prescription pathways captured 58.65% of 2025 value, but OTC products are expanding at an 11.43% CAGR through 2031.

- By geography, North America contributed 40.34% of the revenue in 2025; the Asia-Pacific region is forecast to post the highest regional CAGR of 9.54% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Progesterone Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Hormone-Related Disorders | +1.8% | Global, with concentration in North America & Europe | Long term (≥ 4 years) |

| Growing IVF & Assisted Reproductive Technology Procedures | +2.3% | Global, APAC core with spill-over to MEA | Medium term (2-4 years) |

| Expanding Use of Progesterone in Menopause Hormone Therapy | +1.5% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Increasing Adoption of Micronized Progesterone in Neuroprotective Clinical Trials | +0.7% | North America & Europe | Long term (≥ 4 years) |

| Shift Toward Bio-Identical Plant-Derived Progesterone in Compounding Pharmacies | +1.2% | North America, selective European markets | Medium term (2-4 years) |

| Emerging Demand for Sustained-Release Progesterone Drug-Delivery Implants in Low-Income Settings | +0.9% | Sub-Saharan Africa, South Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hormone-Related Disorders

Polycystic ovary syndrome, endometriosis, and dysfunctional uterine bleeding affect roughly 10-15% of women of reproductive age, generating durable demand for progesterone therapy. Rising obesity and metabolic syndrome exacerbate these conditions, especially in urbanizing Asian economies. Medical guidelines advocate progesterone to oppose unopposed estrogen and prevent endometrial hyperplasia, delaying surgical escalation[1]American College of Obstetricians and Gynecologists, “Management of Abnormal Uterine Bleeding,” acog.org. Strengthening diagnostic awareness, along with better access to gynecologic services in middle-income countries, is expanding the progesterone market. Pharmaceutical brands capitalize by positioning micronized formulations as first-line options with favorable safety profiles.

Growing IVF & Assisted Reproductive Technology Procedures

Luteal-phase progesterone supplementation is mandatory in frozen-embryo transfer protocols. The United States completed 435,426 ART cycles in 2022, a 33% jump over 2020. China already surpasses 1 million cycles annually, and fertility clinic chains are scaling rapidly across India and Southeast Asia. Subcutaneous and oral routes are gaining popularity because equivalence studies show no live-birth disadvantage compared to intramuscular injectables[2]Cochrane Collaboration, “Routes of progesterone administration for luteal-phase support in assisted reproduction,” cochrane.org. This patient-centric shift fuels double-digit demand for micronized and lipid-encapsulated oral capsules.

Expanding Use of Progesterone in Menopause Hormone Therapy

Reappraisal of Women’s Health Initiative data indicates benefits outweigh risks when therapy starts within 10 years of menopause. Clinical societies now recommend micronized progesterone over synthetic progestins for endometrial protection alongside estrogen[3]National Academies of Sciences, Engineering, and Medicine, “The Clinical Utility of Compounded Bioidentical Hormone Therapy,” nationalacademies.org. Uptake is strong in North America and Western Europe, and guidelines in Australia and parts of Asia are aligning. Branded products, such as Prometrium, are experiencing higher prescription renewals as prescribers shift away from medroxyprogesterone acetate.

Increasing Adoption of Micronized Progesterone in Neuroprotective Trials

Progesterone’s GABA‐A modulation and anti-inflammatory effects prompt ongoing trials in traumatic brain injury and Alzheimer’s disease. National Institute on Aging-funded programs are studying allopregnanolone derivatives in Phase II cohorts. Although prior large-scale TBI studies fell short, subgroup signals are encouraging continued investment. Success would open non-gynecologic revenue streams for the progesterone market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse Events & Safety Concerns With Long-Term Hormone Therapy | -1.4% | Global, particularly North America & Europe | Medium term (2-4 years) |

| Availability of Cost-Effective Generic Hydroxyprogesterone Alternatives | -0.8% | Emerging markets in APAC, Latin America, MEA | Short term (≤ 2 years) |

| Supply Chain Constraints in Plant Steroid Feedstock | -1.1% | Global, with acute impact in North America & Europe | Short term (≤ 2 years) |

| Regulatory Scrutiny on Compounded Hormone Therapy Quality Standards | -0.6% | North America, selective European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Events & Safety Concerns with Long-Term Hormone Therapy

Residual fears about breast cancer and thromboembolic risk persist despite data showing micronized progesterone’s favorable profile compared with synthetic progestins. EMA mandates cardiovascular warnings on labels, amplifying patient apprehension. This caution curbs penetration among high-risk cohorts, slowing prescription growth in developed markets.

Availability of Cost-Effective Generic Hydroxyprogesterone Alternatives

Indian manufacturers market hydroxyprogesterone caproate at discounts of up to 70% compared to micronized progesterone. Public hospitals in Africa, Southeast Asia, and Latin America often opt for the cheaper option despite emerging safety concerns. Until regulatory convergence tightens control, low-priced generics will temper the pricing power of premium brands.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Natural Formulations Gain Share Amid Safety Reappraisals

Synthetic molecules still dominate revenue, yet natural formulations are growing faster as clinicians respond to safety and patient-preference signals. The segment’s 10.45% CAGR will lift natural products from a minority position toward parity by 2031. Many U.S. and EU prescribers now view micronized progesterone as the default choice for menopause therapy, and IVF protocols increasingly accept it for luteal support without efficacy compromise. Emerging economies remain price-sensitive; however, regulatory alignment and larger production runs are expected to narrow cost differentials, thereby fostering broader adoption. This evolution positions natural products to capture incremental progesterone market share in premium reimbursed indications, while synthetics retain footholds in cost-constrained public tenders.

By Mode of Delivery: Oral and Subcutaneous Routes Challenge Injectable Dominance

Injectables remain entrenched in IVF and oncology settings; however, patient discomfort and clinic-visit burden are prompting protocol revisions. Oral micronized capsules achieve comparable pregnancy rates and command double-digit growth in menopause and dysfunctional-bleeding indications. Subcutaneous autoinjectors have entered U.S. fertility programs, allowing self-administration and reducing nursing workload - vaginal inserts balance efficacy and lower systemic exposure but face adherence issues due to application inconvenience. Transdermal and implantable systems, which are still investigational, could further erode the injectable share within the progesterone market, particularly in low-resource settings that require autonomy from cold-chain logistics.

By Application: Endometrial Cancer Protocols Drive Fastest Growth

Menopause therapy supplies the largest revenue pool, yet fertility-sparing oncology uses are expanding quickest. Consensus guidelines now position high-dose progesterone as first-line treatment for early-stage, receptor-positive endometrial carcinoma in women desiring pregnancy. Supported by growing cancer screening in younger cohorts, this application underscores double-digit expansion. Dysfunctional uterine bleeding and hyperplasia management remain steady, benefiting from rising obesity-linked estrogen excess. Neuroprotection and psychiatric uses sit in the experimental pipeline; successful trials could diversify indications and lift the overall progesterone market size over the next decade.

By End User: Fertility Centers Outpace Hospitals in Adoption Velocity

Hospitals still prescribe the highest aggregate volume, yet specialized fertility centers are leading the growth. Rising ART cycles, especially frozen-embryo transfers, require consistent luteal support, fueling demand for subcutaneous and vaginal products optimized for outpatient use. Clinics invest in patient-experience enhancements, preferring formulations that minimize pain and monitoring. Ambulatory surgical centers manage a stable share, while retail pharmacies benefit from rising OTC cream sales. Research institutes contribute marginal volume but drive future indication expansion through trials.

By Distribution Channel: OTC Segment Expands as Consumers Seek Autonomy

Prescription channels stay dominant due to regulatory control over high-dose formulations, yet OTC progesterone creams and gels record the fastest CAGR at 11.43%. Consumer marketing emphasizes “natural” symptom relief, despite inconsistent serum levels achieved. FDA warning letters have not quelled demand, indicating strong patient desire for self-directed hormone management. Compounding pharmacies occupy a middle ground; stricter oversight raises costs but simultaneously legitimizes accredited operators. Net effect: distribution diversification increases complexity for manufacturers, necessitating multi-channel strategies to capture full progesterone market potential.

Geography Analysis

North America remains the revenue leader, with a 40.34% share, supported by insurance mandates for fertility treatments and mature demand for bioidentical hormones. The U.S. market benefits from high ART procedural volumes and relatively permissive state rules for compounded products, though FDA oversight of quality is tightening. Canada’s coverage varies provincially, yet private clinics absorb unmet demand. Mexico’s growing medical tourism sector and competitive pricing attract U.S. patients, thereby expanding regional volumes.

Europe contributes roughly 28-30% of sales. EMA centralizes regulatory approval, but reimbursement and pricing are national prerogatives. Germany’s reference-price system and France’s centralized tenders intensify generic competition, while NICE guidelines in the U.K. endorse micronized progesterone for menopause therapy. Eastern European countries experience faster percentage growth from a lower base as access to IVF broadens and middle-class incomes rise.

Asia-Pacific is the growth engine, advancing at a 9.54% CAGR. China’s one million-plus annual ART cycles and India’s expanding private fertility chains dominate volume. The Japanese and South Korean markets prioritize premium, branded drugs within rigorous regulatory frameworks. Southeast Asian nations are liberalizing ART regulations, and rising disposable income supports the expansion of clinics. Cost-competitive generics from Indian API clusters penetrate both domestic and export markets, widening access.

The Middle East and Africa hold smaller shares but show selected high-growth pockets. GCC governments, notably Saudi Arabia and the UAE, subsidize IVF, stimulating demand for high-quality branded products. Donor-funded family-planning initiatives in sub-Saharan Africa prioritize progesterone implants, presenting volume opportunities once sustained-release natural formulations clear regulatory hurdles. South America, led by Brazil and Argentina, is experiencing steady growth despite currency headwinds and import tariffs that favor local generic production.

Competitive Landscape

Market concentration is moderate. Besins Healthcare, Ferring Pharmaceuticals, Pfizer, and Bayer anchor the branded segment, leveraging global distribution and clinical data portfolios. Besins dominates the natural micronized capsules market across Europe and Asia, while Ferring secures partnerships with specialized fertility centers that utilize vaginal inserts. Pfizer maintains a share in synthetic molecules for oncology. Indian companies—Cipla, Lupin, Sun Pharma, and Alkem—integrate diosgenin supply with API synthesis to deliver aggressive price points, eroding premium margins in emerging markets.

Pipeline innovation centers on sustained-release implants, autoinjector devices, and nanoparticle-enhanced oral forms. Partnerships between device specialists and hormone manufacturers aim to commercialize 6-month depots, particularly appealing for contraceptive programs in resource-limited regions. Regulatory compliance is a persistent battleground; quality lapses can rapidly remove competitors, as illustrated by FDA import alerts on substandard batches. Strategic differentiation increasingly hinges on supply-chain resilience, pharmacovigilance data, and clinician-education initiatives to reinforce the safety advantages of approved products over compounded alternatives.

Progesterone Industry Leaders

Cadila Pharmaceuticals

Alkem Labs

Cipla Limited

Lupin Limited

Glenmark Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: The Food and Drug Administration approved a new medication called Lynkuet for alleviating hot flashes and night sweats in menopausal women. Lynkuet contains the compound elinzanetant, offering a nonhormonal treatment option.

- August 2025: Gedeon Richter UK launched Nalvee (10mg dydrogesterone), reintroducing a dydrogesterone-only HRT option after over 17 years. The oral tablet provides clinicians with a new progestogen choice for non-hysterectomised women on oestrogen therapy.

- June 2025: Xiromed launched its progesterone vaginal insert 100mg, a generic version of Endometrin. This product is the first generic approved by the FDA with a Competitive Generic Therapy (CGT) designation. It qualifies for 180 days of market exclusivity under the CGT program.

Global Progesterone Market Report Scope

As per scope of the report, progesterone is the naturally occurring steroid hormone that is produced in the adrenal glands, ovary, and placenta. Progesterone is mainly involved in the maintenance of pregnancy, the regulation of the menstrual cycle, and embryogenesis. Low progesterone levels may lead to constant breast tenderness, abdominal pain, fatigue, and even miscarriage or fetal death. During this phase, progesterone is given to the patient to prevent the aforementioned conditions.

The Progesterone Market Report is Segmented by Product Type (Natural Progesterone and Synthetic Progesterone), Mode of Delivery (Injectable, Suspended Form, Oral, and Other Modes), Application (Menopause, Dysfunctional Uterine Bleeding, Endometrial Cancer, Contraception, Hyperplastic Precursor Lesions, and Other Applications), End User (Hospitals & Clinics, Fertility Centers, Ambulatory Surgical Centers, Retail & Online Pharmacies, and Research & Academic Institutes), Distribution Channel (Prescription, Over-The-Counter, and Compounding Pharmacies), and Geography (North America, Europe, Asia-Pacific, Middle East And Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Natural Progesterone | Plant-Sterol-Derived |

| Animal-Source-Derived | |

| Synthetic Progesterone | Steroidal (17-?-Hydroxyprogesterone Caproate, etc.) |

| Non-Steroidal (Norethindrone, etc.) |

| Injectable |

| Suspended Form |

| Oral |

| Other Modes Of Delivery |

| Menopause |

| Dysfunctional Uterine Bleeding |

| Endometrial Cancer |

| Contraception |

| Hyperplastic Precursor Lesions |

| Other Applications |

| Hospitals & Clinics |

| Fertility Centers |

| Ambulatory Surgical Centers |

| Retail & Online Pharmacies |

| Research & Academic Institutes |

| Prescription (Rx) |

| Over-The-Counter (OTC) |

| Compounding Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East And Africa | GCC |

| South Africa | |

| Rest Of Middle East And Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Product Type | Natural Progesterone | Plant-Sterol-Derived |

| Animal-Source-Derived | ||

| Synthetic Progesterone | Steroidal (17-?-Hydroxyprogesterone Caproate, etc.) | |

| Non-Steroidal (Norethindrone, etc.) | ||

| By Mode Of Delivery | Injectable | |

| Suspended Form | ||

| Oral | ||

| Other Modes Of Delivery | ||

| By Application | Menopause | |

| Dysfunctional Uterine Bleeding | ||

| Endometrial Cancer | ||

| Contraception | ||

| Hyperplastic Precursor Lesions | ||

| Other Applications | ||

| By End User | Hospitals & Clinics | |

| Fertility Centers | ||

| Ambulatory Surgical Centers | ||

| Retail & Online Pharmacies | ||

| Research & Academic Institutes | ||

| By Distribution Channel | Prescription (Rx) | |

| Over-The-Counter (OTC) | ||

| Compounding Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East And Africa | GCC | |

| South Africa | ||

| Rest Of Middle East And Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the current value of the progesterone market?

The progesterone market size stands at USD 2.07 billion in 2026 and is forecast to reach USD 3.17 billion by 2031.

Which application is growing fastest for progesterone products?

Endometrial cancer protocols are the fastest-growing application, advancing at an 11.55% CAGR through 2031.

Why are natural formulations gaining preference over synthetic progesterone?

Clinical guidelines favor micronized, plant-derived progesterone due to a more favorable safety profile and patient perception of bioidentical hormones.

Which region will post the highest growth in progesterone demand?

Asia-Pacific is projected to record the strongest regional CAGR at 9.54% between 2026-2031.

How is the distribution landscape changing for progesterone products?

While prescriptions remain dominant, over-the-counter creams and gels are expanding at an 11.43% CAGR as consumers seek self-directed hormone options.

Page last updated on: