Homeopathy Product Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

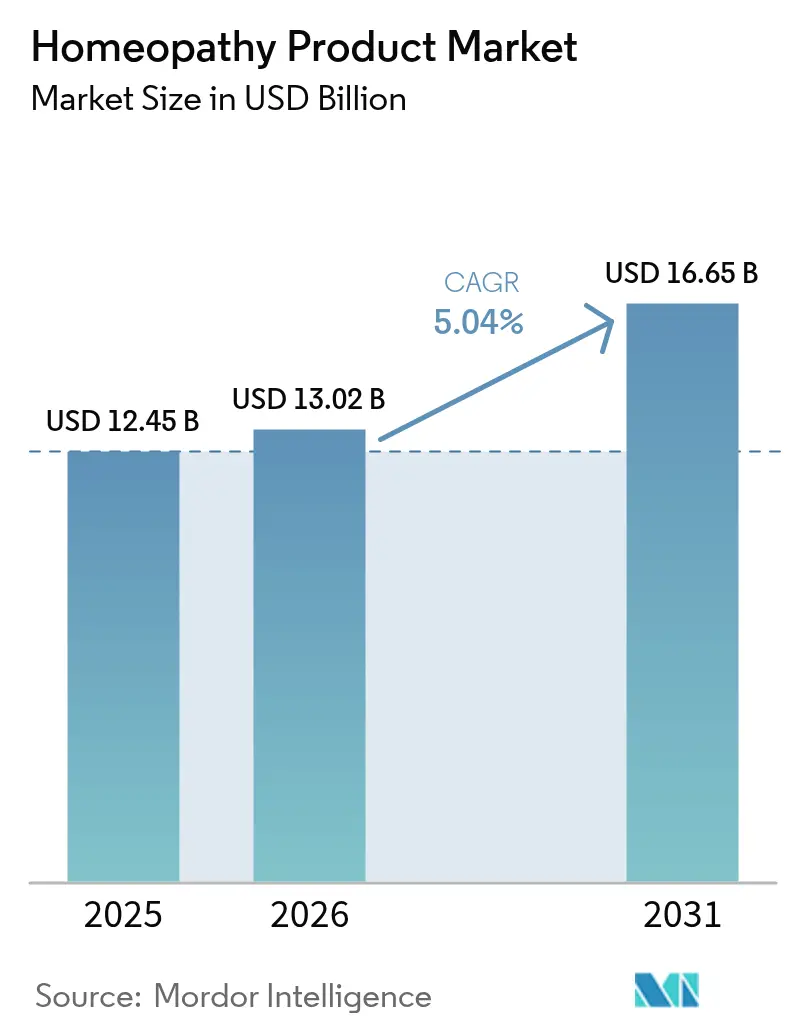

| Market Size (2026) | USD 13.02 Billion |

| Market Size (2031) | USD 16.65 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

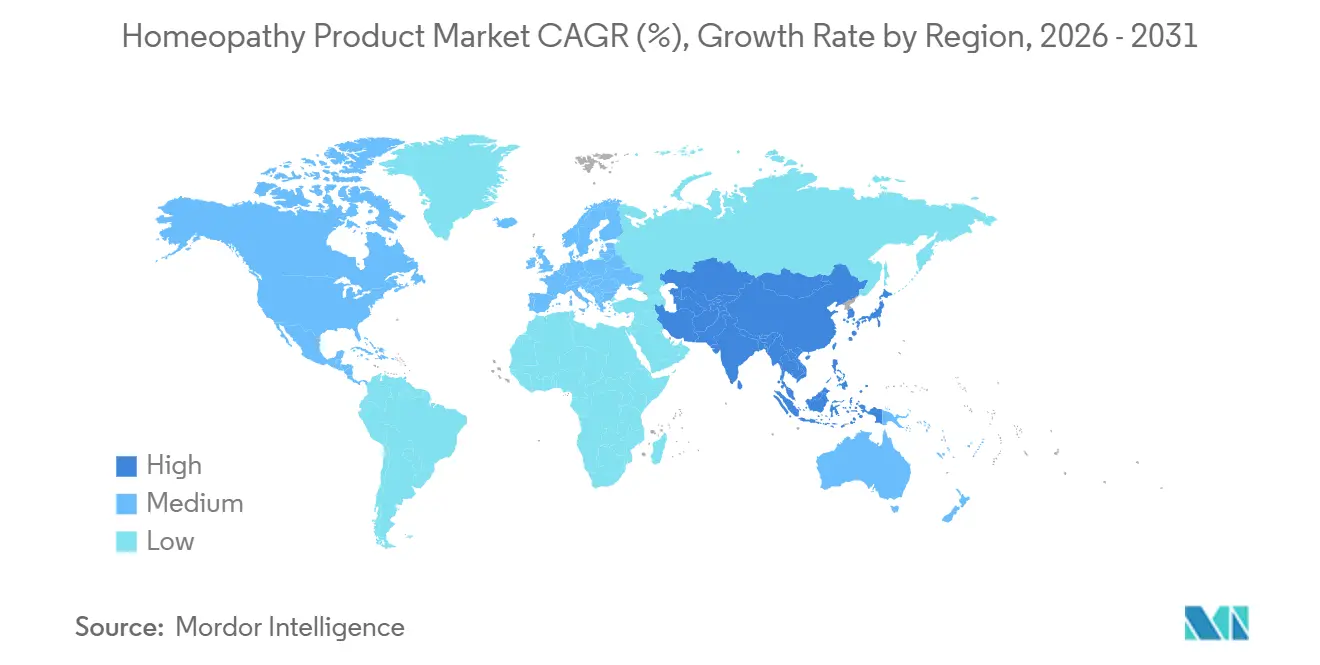

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Homeopathy Product Market Analysis by Mordor Intelligence

The Homeopathy Product Market size was valued at USD 12.45 billion in 2025 and is estimated to grow from USD 13.02 billion in 2026 to reach USD 16.65 billion by 2031, at a CAGR of 5.04% during the forecast period (2026-2031).

Demand is propelled by aging populations seeking gentler chronic-disease options, rising regulatory recognition in India, Canada, and parts of Europe, and e-commerce models that bypass skeptical pharmacy gatekeepers. OTC dominance masks fast growth in self-care combination remedies, while drops and tinctures gain favor for faster absorption. Competitive intensity remains moderate; regional leaders Boiron, Heel, and Schwabe defend share as digital-native entrants deploy direct-to-consumer subscriptions that cut margins yet deepen loyalty. Regulatory fragmentation poses downside risks, but the WHO’s Traditional Medicine Strategy and India’s National Commission for Homoeopathy Act offer durable upside for resource-constrained health systems.

Key Report Takeaways

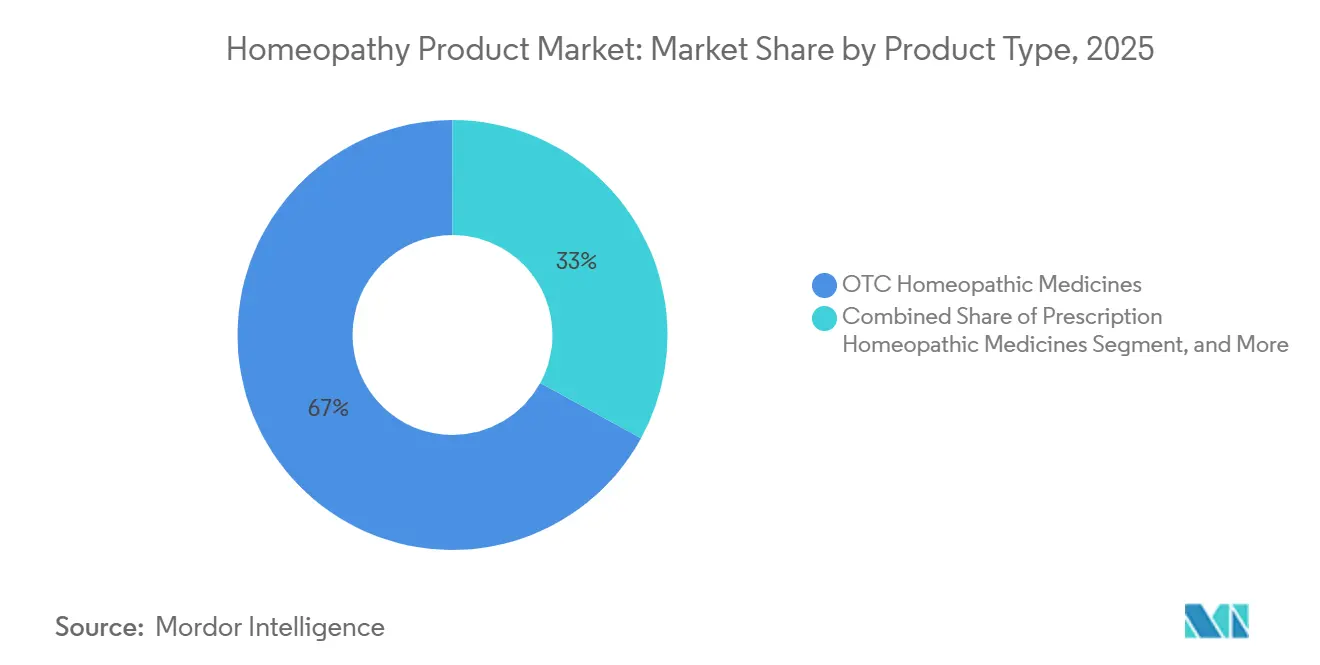

- By product type, over-the-counter homeopathic medicines led with 67.02% revenue share in 2025, and self-care combination remedies are advancing at a 6.85% CAGR through 2031.

- By source, plant-based sources commanded 60.34% of the homeopathy product market share in 2025, and animal-based formulations are projected to expand at a 9.33% CAGR through 2031.

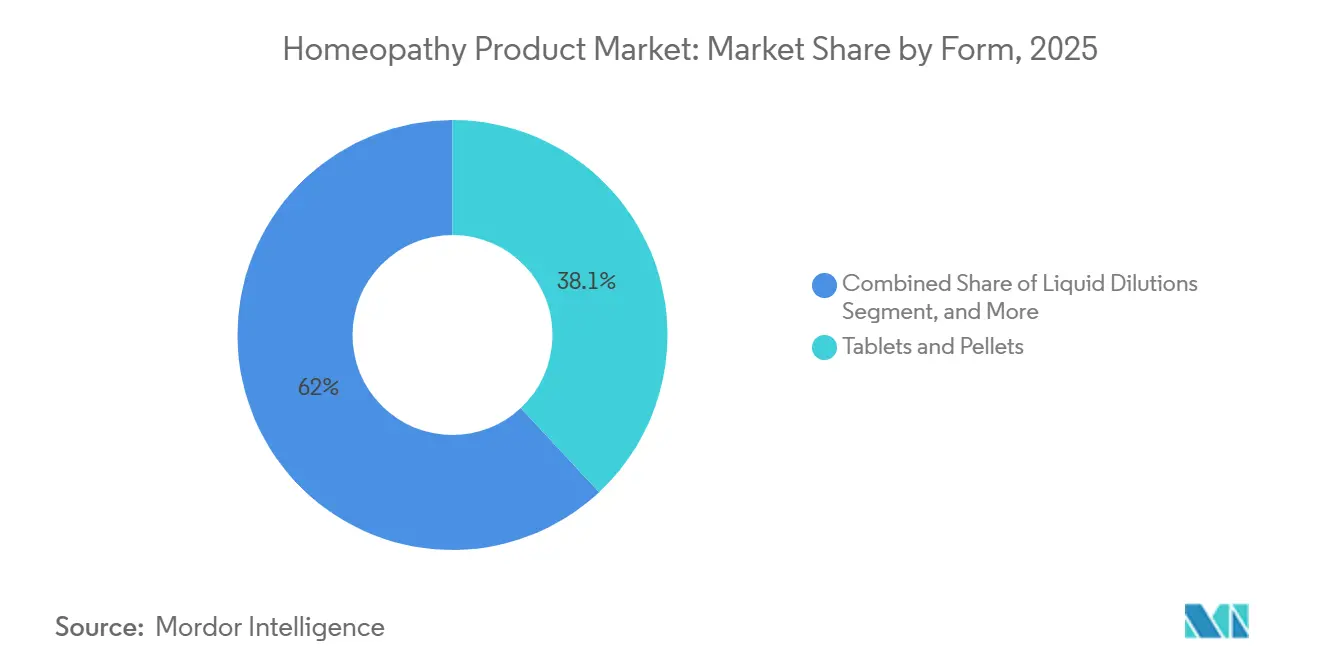

- By form, tablets & pellets commanded 38.05% of the homeopathy product market share in 2025, drops and tinctures are set to grow at a 10.93% CAGR, outpacing all other dosage forms.

- By distribution channel, retail pharmacies held a 46.28% share in 2025, while homeopathic clinics are growing at an 8.93% CAGR.

- By geography, North America accounted for 37.78% of the homeopathy product market size in 2025; Asia-Pacific is forecast to be the fastest region at a 7.03% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Homeopathy Product Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Consumer shift toward natural and holistic medicine | +1.2% | Global with strength in North America, Europe, India | Medium term (2-4 years) |

| Self-care and preventive health adoption | +0.9% | Global, urban Asia-Pacific and North America | Short term (≤ 2 years) |

| Aging population and chronic disease prevalence | +0.8% | North America, Europe, Japan, China | Long term (≥ 4 years) |

| Regulatory recognition and healthcare integration | +0.7% | India, Brazil, select EU markets | Medium term (2-4 years) |

| E-commerce and digital distribution expansion | +0.6% | Global led by North America and Asia-Pacific | Short term (≤ 2 years) |

| Personalized formulation and combination remedies | +0.5% | North America, Europe, Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Shift Toward Natural and Holistic Medicine

Escalating preference for plant-based and mineral-derived remedies is reshaping portfolios as 80% of surveyed consumers express interest in natural health products, yet familiarity with homeopathy lingers at 60%. Boots’ June 2025 release of 300 wellness SKUs, including homeopathic lines, signals mainstream confidence in category growth.[1]Boots UK, “Wellness Product Expansion,” boots.com Millennials and Gen Z emphasize transparency and sustainability, prompting brands to spotlight botanical sourcing. Retail shelf gains coexist with knowledge gaps around potentization, inviting scrutiny over efficacy claims. Firms investing in omnichannel education capture outsized share as they translate curiosity into repeat purchase.

Self-Care and Preventive Health Adoption

Combination OTC remedies, expanding at a 6.85% CAGR, illustrate consumer demand for simplified multi-symptom control. Boiron’s Oscillococcinum and Hyland’s Cold’n Cough target flu-like syndromes without consultation, a habit reinforced by pandemic-era telehealth autonomy. Classical practitioners caution that a one-size-fits-all approach dilutes an individualized philosophy. Manufacturers straddle this divide through tiered portfolios that place single remedies in clinic channels and blends in mass retail.

Aging Population and Chronic Disease Prevalence

Geriatric cohorts gravitate to gentler modalities for arthritis, diabetes, and allergies, elevating drops and tinctures that enable precise dosing. India’s 300,000 registered homeopaths often serve as frontline providers in rural areas where allopathic care is scarce.[2]Ministry of AYUSH, “AYUSH Budget Allocation 2024-25,” ayush.gov.in Western insurers mostly exclude coverage, constraining uptake among cost-sensitive seniors, though Germany maintains high familiarity despite funding debates. Long-run growth hinges on longitudinal evidence demonstrating the cost-effectiveness of the approach over polypharmacy.

Regulatory Recognition and Healthcare Integration

India’s National Commission for Homoeopathy Act and the WHO 2025-2034 strategy embed the modality in public health, spurring procurement and insurance pilots. Brazil’s ANVISA code supplies similar clarity. Countervailing forces include Canada’s 2025 front-of-pack disclaimer rule that may cool demand.[3]Health Canada, “Labelling Provisions for Homeopathic Products,” canada.ca The net effect remains positive as emerging-market tailwinds outweigh headwinds, though global rollouts must navigate disparate labelling and reimbursement regimes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited clinical evidence and scientific skepticism | -0.6% | Global, most acute in North America and Western Europe | Medium term (2-4 years) |

| Regulatory fragmentation and reimbursement rollbacks | -0.4% | Europe (France, Germany), North America (Canada, US) | Short term (≤ 2 years) |

| High upfront capital cost for mid-size clinics | -0.3% | Asia-Pacific, Latin America, emerging markets | Medium term (2-4 years) |

| Shortage of qualified practitioners and technicians | -0.2% | North America, Europe, select Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Clinical Evidence and Scientific Skepticism

The absence of large-scale placebo-controlled trials limits hospital and insurer adoption. FDA’s 2022 risk-based guidance sidelines efficacy considerations, focusing on safety while maintaining a watchlist. Canada’s 2025 disclaimer mandate codifies doubt on retail shelves, and advocacy groups challenge the policy in court. Heel undertakes the rare rigorous program yet faces methodology critiques. Without compelling data, many brands stay confined to OTC aisles and practitioner scripts.

Regulatory Fragmentation and Reimbursement Rollbacks

France halted reimbursement in 2021, shrinking Boiron’s domestic revenue base, while Germany debates statutory coverage, creating uncertainty. The UK ended NHS funding in 2017. Such moves push firms toward self-pay retail where volumes persist but margins narrow. Emerging markets like India and Brazil grant opposite momentum through supportive acts and clear product codes, though average unit prices are lower. Global players juggle premium branding for Western consumers and mass-value SKUs for Asia and Latin America.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: OTC Leadership and Combination-Remedy Momentum

Over-the-counter medicines accounted for 67.02% of the homeopathic product market share in 2025. The segment thrives on mass distribution through Walgreens, Walmart and Boots, reinforced by Hyland’s 2025 rollout into 7,400 new U.S. outlets. OTC expansion aligns with digital education campaigns that deepen shopper confidence and raise basket sizes.

Self-care combination remedies underpin forecast acceleration, advancing at 6.85% CAGR as time-pressed consumers embrace multi-symptom relief. Boiron devoted USD 6.6 million to pediatric cold-and-flu advertising, lifting U.S. channel sales 11.4% year on year. Prescription lines persist in Germany and India where practitioner ecosystems remain influential, but their contribution to the homeopathy product market size shrinks as reimbursement wanes.

By Source: Plant Dominance and Emerging Animal-Derived Niche

Plant-based inputs accounted for 60.34% of the value in 2025, thanks to familiarity with Arnica, Belladonna, and Chamomilla. Sustainability narratives and clean-label cues reinforce share across Europe and North America. Mineral remedies maintain a stable demand through practitioner prescriptions.

Animal-based nosodes and sarcodes, though a minority today, are projected to grow at a 9.33% CAGR. Brands like Dr. Reckeweg educate clinicians on chronic-disease protocols, widening acceptance. Ethical sourcing and EU traceability rules introduce cost and reputational hurdles that could moderate growth but have not yet derailed momentum.

By Form: Liquid Formats Accelerate on Bioavailability

Tablets and pellets accounted for 38.05% of 2025 revenue, favored for their portability and long shelf life. Nonetheless, drops and tinctures will outpace all other forms with a 10.93% CAGR, expanding their share of the homeopathy market. Caregivers value rapid absorption and adjustable dosage, key for pediatric and geriatric segments.

Canada’s March 2026 GMP upgrade for liquids raises compliance costs, likely consolidating share among capitalized manufacturers. Hyland’s leverages subscription logistics to sell higher-priced tinctures, offsetting tighter margins in retail tablets.

By Distribution Channel: Retail Scale Versus Clinic Personalization

Retail pharmacies retained a 46.28% share in 2025, driven by strong foot traffic and impulse buys, with Boots’ 300-SKU wellness push emblematic of banner confidence. Yet homeopathic clinics are forecast to grow 8.93% CAGR, bolstered by India’s 215 colleges pumping new practitioners into tier-2 and tier-3 cities.

Hybrid models integrate teleconsults and e-commerce fulfilment, blending personalized care with delivery convenience. Direct-to-consumer websites now account for a double-digit share in the United States as subscription economics defeat shelf-space fees.

Geography Analysis

North America led 2025 revenue at 37.78%, anchored by mature OTC channels and digital subscriptions. United States retailers stock broad assortments, while Canada balances opportunity with a 2025 disclaimer that could mute growth. Mexico remains nascent but benefits from rising wellness spend.

Europe shows mixed prospects. Germany’s population familiarity of 95.1% sustains baseline demand despite the coverage debate, and France’s reimbursement cut forces a retail pivot for Boiron. Spain, Italy, and Eastern Europe offer mid-single-digit growth under lighter regulation. Weleda’s Cell Longevity debut in prestige boutiques illustrates premium repositioning.

Asia-Pacific is set to climb at 7.03% CAGR, the highest regional rate. India dominates with 300,000 practitioners and INR 3,050 crore federal backing. China sees cautious interest beyond TCM, while Australia’s strict TGA oversight supports premium pricing. Southeast Asian markets open white-space through smartphone-driven telehealth adoption.

Competitive Landscape

Market structure is moderately concentrated. Boiron, Heel, and Schwabe retain regional strongholds but face fragmentation from India’s multi-hundred-player ecosystem. Digital disruptors raise the bar; Hyland’s USD 40 million funding scaled its Subscribe & Save engine and delivered 15% customer savings, improving stickiness. Weleda’s science-adjacent Cell Longevity line taps affluent wellness seekers.

Clinical validation remains a weak flank; Heel’s Traumeel studies help hospital acceptance yet confront methodological critiques. Tightening GMP rules in Canada and anticipated copycats in Europe signal impending consolidation favoring well-capitalized manufacturers with ISO certifications such as SBL. Blockchain provenance pilots aim to combat the proliferation of counterfeits in open e-commerce channels.

Homeopathy Product Industry Leaders

A Nelson & Co Ltd.

Biologische Heilmittel Heel GmbH

Boiron

Dr. Willmar Schwabe GmbH

SBL World Pharmaceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Hyland’s expanded Baby Oral Pain Relief tablets into 5,900 Walgreens and 1,500 Walmart stores after reformulating to exclude belladonna and benzocaine

- August 2024: Boiron USA confirms a new logistics centre in Newtown Square, Pennsylvania, to streamline warehousing and nationwide delivery.

Global Homeopathy Product Market Report Scope

As per the scope of the report, homeopathy is a medical system based on the principle that the body can cure itself. Those who practice it use tiny amounts of natural substances, like plants and minerals. They believe these stimulate the healing process. The Homeopathy Product Market is Segmented by Product Type (Tincture, Dilutions, Tablets, and Others), Application (Analgesic and Antipyretic, Respiratory, Neurology, and Others), Source (Plants, Animals, and Minerals), and Geography (North America, Europe, Asia-Pacific, Middle East, and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value (in USD million) for the above segments.

| OTC Homeopathic Medicines |

| Prescription Homeopathic Medicines |

| Self-care Combination Remedies |

| Plant-based |

| Mineral-based |

| Animal-based |

| Biochemic |

| Liquid Dilutions |

| Tablets & Pellets |

| Drops & Tinctures |

| Ointments & Creams |

| Powders |

| Retail Pharmacies |

| Homeopathic Clinics |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | OTC Homeopathic Medicines | |

| Prescription Homeopathic Medicines | ||

| Self-care Combination Remedies | ||

| By Source | Plant-based | |

| Mineral-based | ||

| Animal-based | ||

| Biochemic | ||

| By Form | Liquid Dilutions | |

| Tablets & Pellets | ||

| Drops & Tinctures | ||

| Ointments & Creams | ||

| Powders | ||

| By Distribution Channel | Retail Pharmacies | |

| Homeopathic Clinics | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large will the homeopathy product market be by 2031?

It is projected to reach USD 16.65 billion by 2031 at a 5.04% CAGR.

Which product type is growing fastest?

Drops and tinctures are forecast to expand at 10.93% CAGR on bioavailability advantages.

Why is Asia-Pacific considered the most attractive region?

India’s practitioner density, supportive regulation and rising disposable incomes push the region toward a 7.03% CAGR.

What is driving OTC dominance?

Retail accessibility and consumer comfort with self-medication keep OTC products at 67.02% market share in 2025.

How are companies addressing evidence gaps?

Leaders like Heel invest in clinical trials, while others focus on consumer education and regulatory compliance to build credibility.

Page last updated on: