Bioidentical Hormones Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

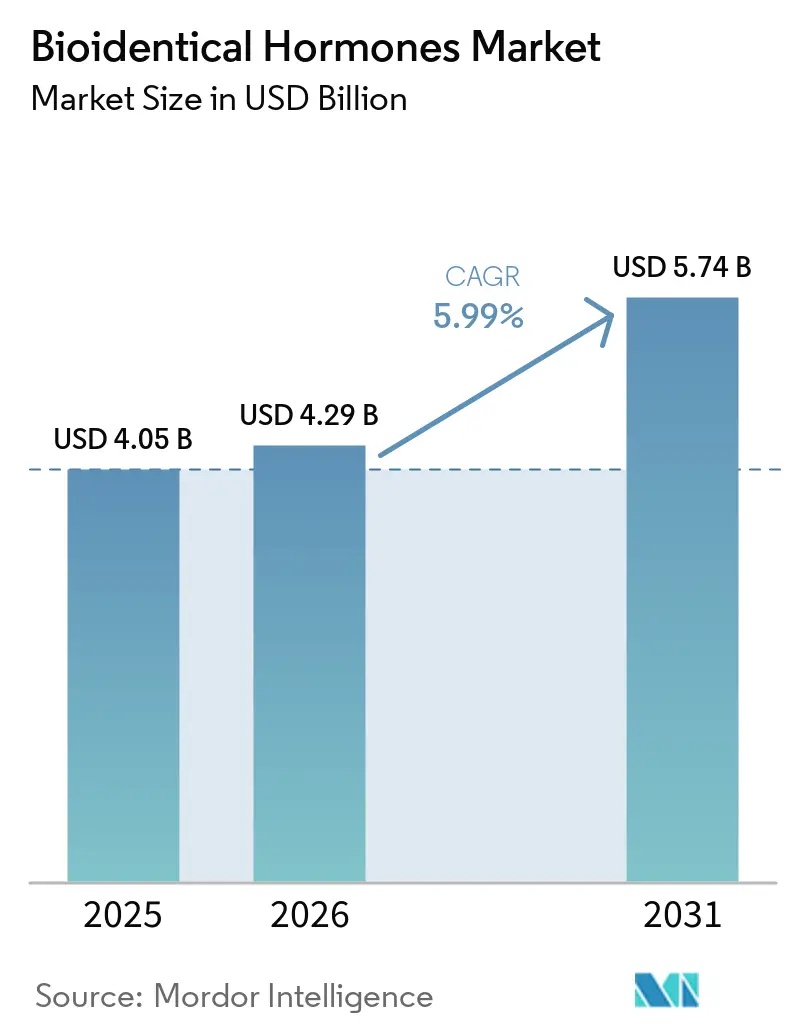

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 5.74 Billion |

| Growth Rate (2026 - 2031) | 5.99% CAGR |

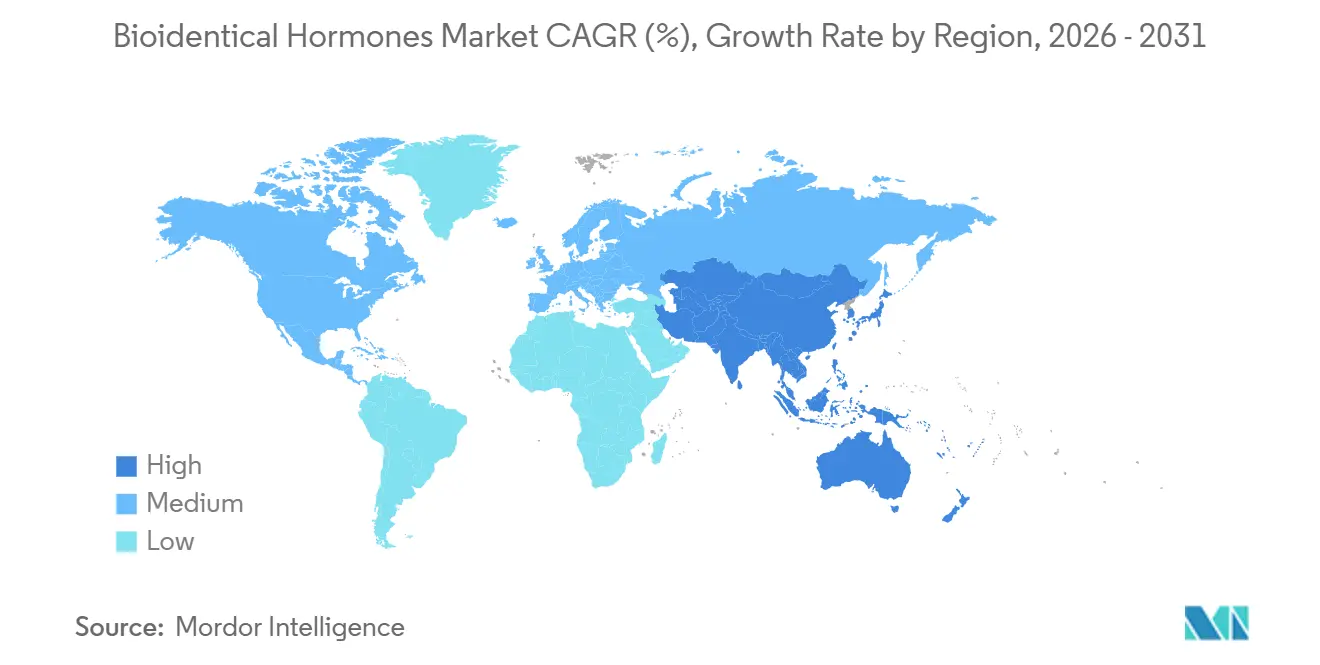

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

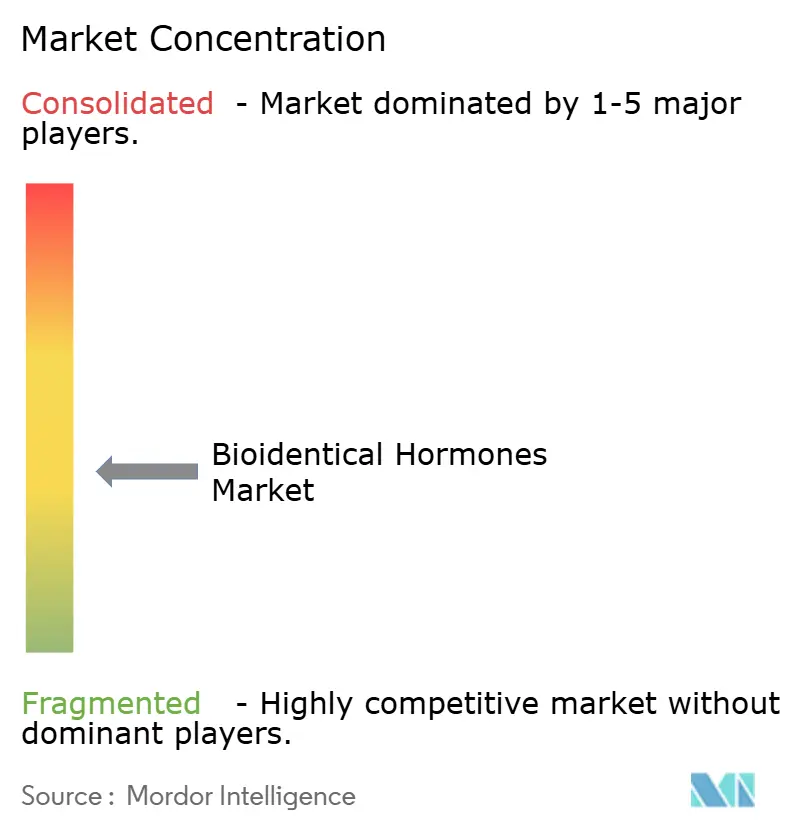

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bioidentical Hormones Market Analysis by Mordor Intelligence

The Bioidentical Hormones Market size is expected to grow from USD 4.05 billion in 2025 to USD 4.29 billion in 2026 and is forecast to reach USD 5.74 billion by 2031 at 5.99% CAGR over 2026-2031.

In late 2025, the FDA removed the boxed warning from several menopausal hormone therapy products, leading to a rapid increase in prescribing patterns by early 2026. By February 2026, estrogen patch prescriptions surged, and the use of estrogen-based hormone therapy among women aged 45 to 54 rose to nearly 5%, up from 2.5% in 2023, signaling recovery after years of underuse following the 2002 WHI study. The bioidentical hormones market is gaining momentum due to growing patient interest in transdermal delivery, personalized dosing, and increased awareness of menopause care gaps, which telehealth platforms are addressing at scale. Competition in the bioidentical hormones market is being driven by acquisition-led growth, compliant compounding capabilities, and digital prescribing models that streamline the process from consultation to fulfillment. This environment creates opportunities for companies that can secure supply chains, support non-oral delivery formats, and serve patients in both institutional and home care settings.

Key Report Takeaways

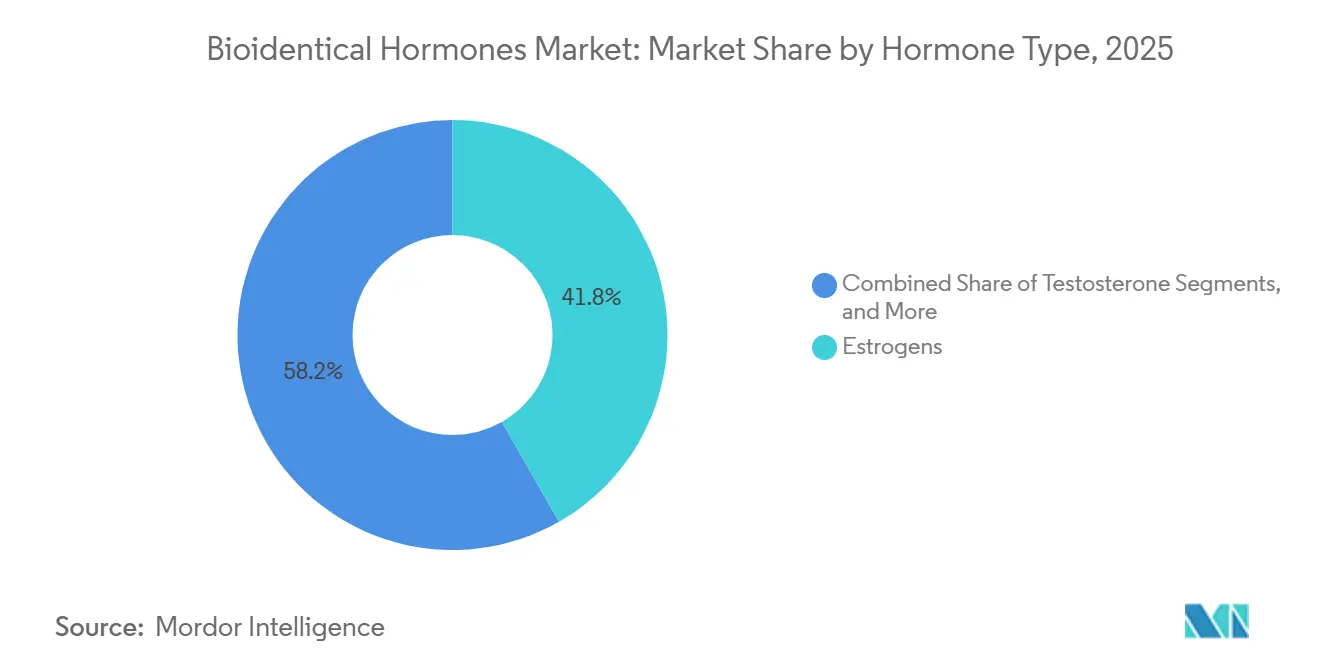

- By hormone type, estrogens led with a 41.75% share in 2025, while testosterone is projected to record the fastest CAGR of 6.30% through 2031.

- By product type, patches and implants held a 41.6% share in 2025 and are also projected to post the highest CAGR of 7.10% through 2031.

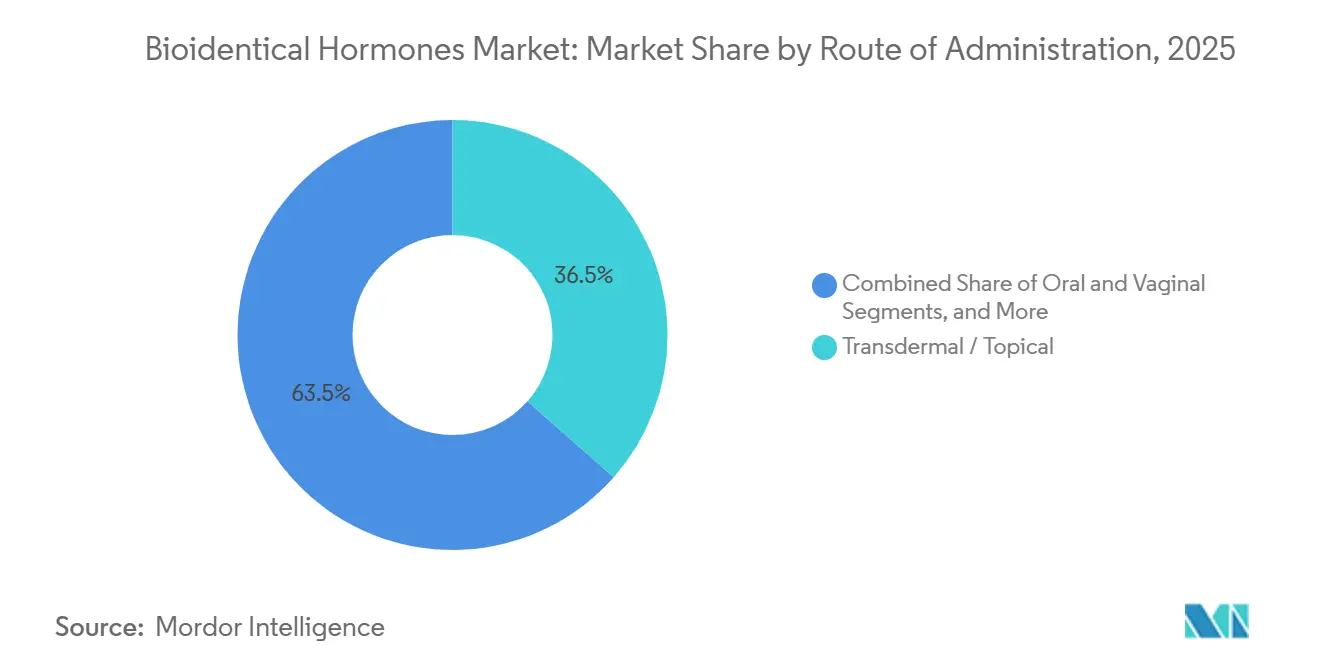

- By route of administration, transdermal and topical delivery accounted for a 36.50% share in 2025 and is expected to expand at the fastest CAGR of 7.75% through 2031.

- By application, menopause management and vasomotor symptoms commanded a 61.66% share in 2025, while andropause and male hypogonadism is projected to grow at the fastest CAGR of 6.25% through 2031.

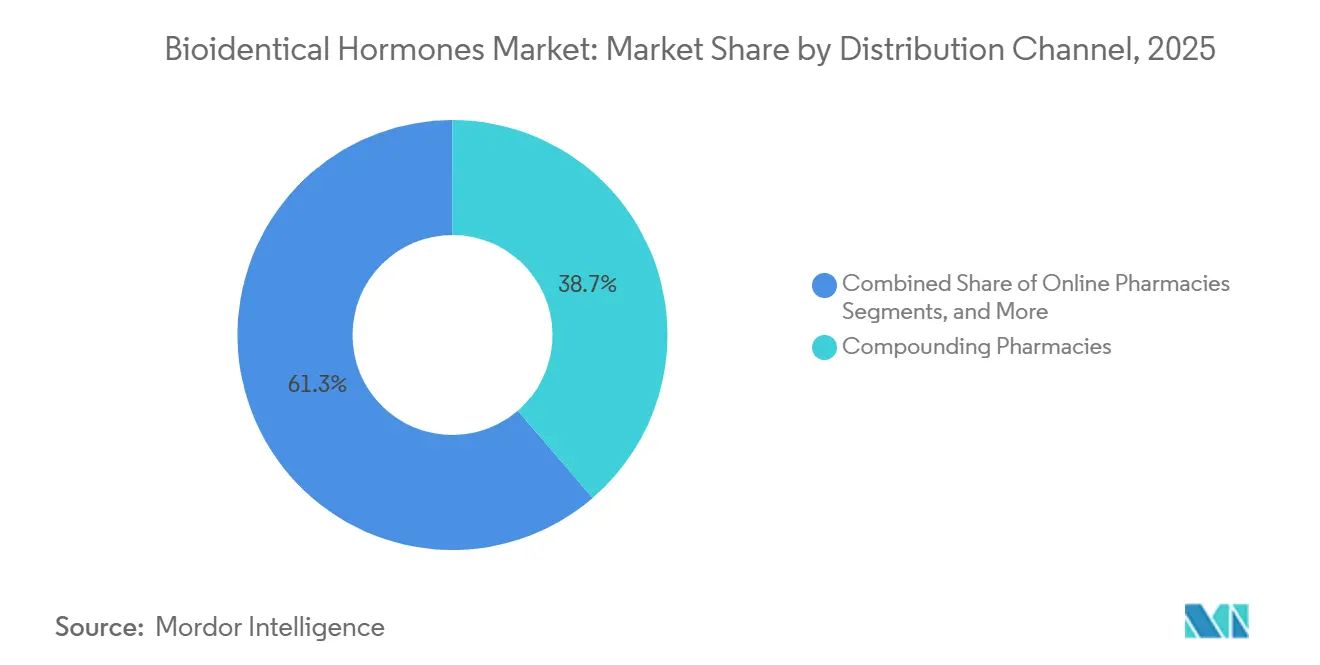

- By distribution channel, compounding pharmacies held a 38.70% share in 2025, while online pharmacies is projected to register the fastest CAGR of 7.55% through 2031.

- By end user, hospitals contributed a 58.55% share in 2025, while homecare and self-administered care is expected to advance at the fastest CAGR of 6.98% through 2031.

- By geography, North America retained the largest regional share at 41.67% in 2025, while Asia-Pacific is projected to grow at the fastest CAGR of 7.15% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bioidentical Hormones Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising menopause and age-related hormone deficiency demand | +1.8% | Global, strongest in North America and Europe | Short term (≤ 2 years) |

| Demand for personalized and natural-feeling hormone products | +1.2% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Shift toward transdermal and non-oral delivery | +0.9% | Global, strongest in North America and Western Europe | Medium term (2-4 years) |

| Telehealth-enabled hormone care pathways | +0.8% | North America, with spillover into Asia-Pacific and Middle East and Africa | Short term (≤ 2 years), Medium term (2-4 years) |

| Reappraisal of menopause hormone therapy risk-benefit profile | +1.0% | North America and Europe, with early gains in Australia and South Korea | Short term (≤ 2 years) |

| Unmet need for female testosterone options | +0.5% | North America, the United Kingdom, and Australia | Medium term (2-4 years), Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Menopausal and Age-Related Hormone Deficiency Demand

The bioidentical hormones market is experiencing significant growth due to the increasing postmenopausal population. By 2025, over 1.1 billion women globally are expected to be postmenopausal, with more than 1.3 million women in the U.S. entering menopause annually.[1]Women’s Health Issues, “Compounded Bioidentical Hormone Therapy and Care Access Trends,” Women’s Health Issues, whijournal.com The financial impact of untreated symptoms is substantial, with annual productivity losses reaching USD 1.8 billion and combined medical and productivity costs at USD 26.6 billion in the U.S. Additionally, the market is recovering from a decline in hormone therapy usage caused by risk concerns from the WHI study, which reduced uptake from 27% to under 5% over two decades.[2]Canadian Agency for Drugs and Technologies in Health, “Comparative Evidence Between Transdermal and Oral Menopausal Hormone Therapy,” NCBI Bookshelf, ncbi.nlm.nih.gov Companies that can rapidly scale supply are well-positioned to capitalize on this rebound.

Demand for Personalized and Natural-Feeling Hormone Products

The market is shifting from standardized treatments to personalized approaches, focusing on individualized dosing, route selection, and symptom-specific management. Patients today are more informed and actively involved in treatment decisions, favoring options that mimic natural hormone patterns. However, approved products like BIJUVA, which introduced two-dose strengths in February 2026, are narrowing this gap. The market is moving toward regulated personalization, benefiting branded products that combine flexibility with the credibility of formal approval.

Shift Toward Transdermal and Non-Oral Delivery for Better Outcomes

The bioidentical hormones market is seeing a shift toward transdermal and non-oral delivery methods, driven by clinical recommendations favoring these options. Transdermal estrogen has been shown to reduce the risk of venous thromboembolism by 56% compared to oral estrogen, without the stroke risk associated with oral routes. NICE guidance supports transdermal therapy for women with a BMI over 30 kg/m² or elevated VTE risk. This trend is influencing manufacturing priorities and increasing demand for patches, gels, sprays, and pellets. Companies with strong capabilities in non-oral formats are better positioned to benefit from this safety-driven and convenience-focused shift.

Telehealth-Enabled Hormone Care Pathways Expanding Access

Telehealth is transforming the bioidentical hormones market, becoming a primary channel for patient prescriptions. Platforms such as Hers, Eden Health, Evernow, Rixa Health, Winona, and Carrot Fertility have expanded access to menopause and hormone care across the U.S., addressing long wait times and limited specialist availability. A 2025 survey revealed that over 50% of Millennials prefer telehealth over office visits, with 77% of Americans viewing remote care as the future of medicine. The care gap is significant, as nearly 80% of OB-GYN and internal medicine residents report inadequate training in menopause care. Employer-linked services, like Carrot Fertility's virtual menopause clinic launched in 2025, further enhance access, with prescriptions often directed to mail-order or specialty pharmacies.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Guideline skepticism toward compounded bioidentical hormone therapy | -0.7% | Global, strongest in North America and Western Europe | Short term (≤ 2 years), Medium term (2-4 years) |

| Limited reimbursement and self-pay affordability barriers | -0.5% | North America, core Asia-Pacific markets, with spillover into Middle East and Africa | Medium term (2-4 years), Long term (≥ 4 years) |

| Estradiol patch and menopause therapy supply shortages | -0.4% | North America, with potential spillover into Europe | Short term (≤ 2 years) |

| Higher compliance burden for compounders and outsourcing facilities | -0.3% | United States, with early regulatory relevance in Europe and Australia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Guideline Skepticism Toward Compounded Bioidentical Hormone Therapy

Clinical skepticism continues to challenge the growth of the bioidentical hormones market, particularly regarding compounded bioidentical hormone therapy. The Endocrine Society and ACOG have highlighted the lack of evidence supporting the safety of compounded products over FDA-approved alternatives. ACOG also noted that compounded estradiol could test 26% below labeled content, while progesterone could test 31% above. This scrutiny is significant as the market has relied on compounding pharmacies to address dose and route needs unmet by approved products. In September 2025, the VA classified compounded bioidentical hormone therapy as investigational and unnecessary for menopause, male hypogonadism, and low libido, removing a key institutional prescribing pathway and potentially influencing other health systems. While demand remains strong, the market faces a stricter evidence and reimbursement environment.

Limited Reimbursement and Self-Pay Affordability Barriers

High out-of-pocket costs and inconsistent reimbursement continue to limit the bioidentical hormones market, particularly for branded products and female testosterone options. BIJUVA's monthly cash price ranged from USD 257 to USD 351, with uninsured or underinsured patients bearing the full cost despite copay support for insured users. The challenge is more acute for women, as no FDA-approved testosterone product exists in the U.S. or Brazil, leaving patients reliant on off-label male formulations or compounded products, often requiring cash payment. In the UK, testosterone prescriptions for menopausal women were three times higher in affluent GP practices compared to deprived ones. These affordability gaps hinder adoption, but a future FDA approval of a female-specific testosterone could improve reimbursement and prescribing confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Hormone Type: Testosterone Gains Ground as Estrogen Anchors Revenue

In 2025, estrogens accounted for 41.75% of the bioidentical hormones market, maintaining their position as a key revenue driver. Their dominance is due to their established role in treating vasomotor symptoms, genitourinary syndrome of menopause, and osteoporosis prevention. The 2025 Korean Society of Menopause guidelines highlighted the reduced risk of VTE and stroke with transdermal estradiol compared to oral routes, reinforcing estrogen products as the market's cornerstone.

Progesterone remains critical for women with an intact uterus, mitigating endometrial risks associated with unopposed estrogen therapy. Micronized progesterone and combination products continue to support prescription trends. DHEA, including FDA-approved vaginal prasterone, is a smaller but growing segment addressing genitourinary symptoms. Testosterone, with a projected CAGR of 6.30% through 2031, is the fastest-growing segment, driven by increased awareness of HSDD and androgen therapy, despite the absence of a female-specific approved product.

By Product Type: Patches and Implants Drive Adoption Across Demographics

Patches and implants held a 41.6% market share in 2025 and are projected to grow at a 7.10% CAGR through 2031. Transdermal patches offer consistent estradiol delivery, bypass hepatic first-pass metabolism, and provide a safer option for women with thrombotic risks. Prescribers increasingly favor patches for balancing symptom control and cardiovascular risk.

Implants are gaining traction due to their long-acting hormone delivery and alignment with rising testosterone use in both genders. Subdermal pellets, offering sustained release and minimal daily intervention, have expanded the implant segment. Manufacturers with expertise in patch production or pellet systems are well-positioned to benefit from the shift away from oral products.

By Route of Administration: Transdermal Dominates and Widens Its Lead

Transdermal and topical delivery methods accounted for 36.50% of the bioidentical hormones market in 2025, with the highest projected CAGR of 7.75% through 2031. These methods bypass hepatic first-pass metabolism, ensuring stable serum profiles and reducing metabolic disruptions. Transdermal estrogen is preferred for addressing sexual function and libido concerns, further solidifying its market position.

Transdermal formats like patches, gels, creams, and sprays align with home-based treatment models and telehealth care pathways, enabling remote dose adjustments and follow-ups. While oral routes remain relevant for specific patient needs, the market increasingly favors non-oral formats for their convenience and clinical benefits.

By Application: Menopause Management Leads but Andropause Redefines the Growth Narrative

Menopause management dominated the market with a 61.66% share in 2025, driven by the high prevalence of vasomotor symptoms among U.S. women and renewed confidence in hormone therapy following FDA labeling changes. The 2025 Korean Society of Menopause guidelines support standard-dose therapy for significant symptom reduction, reinforcing menopause care as the primary revenue driver.

Andropause and male hypogonadism are the fastest-growing applications, with a projected CAGR of 6.25% through 2031. Growth is fueled by increased testosterone adoption, awareness of hormone deficiencies in aging men, and the use of pellets and transdermal formats. Hospitals and specialist clinics remain pivotal in diagnosis and treatment initiation.

By Distribution Channel: Compounding Pharmacies Lead as Online Channels Scale Fastest

Compounding pharmacies held a 38.70% market share in 2025, driven by their ability to create patient-specific formulations that commercial products cannot fully address. Section 503A compounding pharmacies operate under state board oversight, offering flexibility for individualized estrogen-progesterone combinations and off-label testosterone treatments. Fagron’s acquisition of UCP in 2026 expanded its dual-channel reach in California.

Online pharmacies are the fastest-growing channel, with a projected CAGR of 7.55% through 2031. This growth is tied to telehealth, where virtual consultations drive prescriptions to mail-order and specialty fulfillment models, enhancing convenience for refills and subscription-based care.

By End User: Hospitals Lead While Homecare Signals Structural Decentralization

Hospitals accounted for 58.55% of the bioidentical hormones market in 2025, reflecting their role in specialist care, structured diagnostics, and complex case management. They remain central to gynecology, endocrinology, and testosterone-related treatments, supported by specialty hormone and wellness clinics for patient-centric care.

Homecare and self-administered treatments are the fastest-growing segment, with a projected CAGR of 6.98% through 2031. This growth is driven by telehealth-to-pharmacy pathways and the suitability of transdermal and pellet therapies for remote management, enabling stable patients to adhere to treatment with minimal clinical intervention.

Geography Analysis

In 2025, North America accounted for 41.67% of the bioidentical hormones market, maintaining its leadership position. The U.S. drives this dominance due to regulatory changes, rising menopause treatment demand, robust telehealth infrastructure, and increased treatment awareness. Estrogen-based hormone therapy prescriptions among women aged 45 to 54 nearly doubled between 2023 and early 2026, reaching 5% of this demographic. Estrogen patch prescriptions also rose by 184% from 2018 to February 2026, reflecting a shift toward non-oral delivery methods. In Canada, Knight Therapeutics began commercializing IMVEXXY and BIJUVA in 2024 under its license from TherapeuticsMD, introducing institutional branding in a market previously dominated by compounded hormones.

Europe holds a mature yet evolving position in the bioidentical hormones market. Menopausal hormone therapy prevalence in Northern and Western Europe remains higher than the post-WHI U.S. levels, ranging from 4% to 10% in most EU markets. A joint statement by The British Menopause Society, the Royal College of Obstetricians and Gynaecologists, and the Society for Endocrinology supports no arbitrary age or duration limits on hormone therapy for symptomatic women. This provides a stable prescribing base, although compounded products face challenges related to evidence and reimbursement. The region combines strong clinical acceptance of therapy with stringent quality and evidence expectations.

Asia-Pacific is the fastest-growing region in the bioidentical hormones market, with a projected CAGR of 7.15% through 2031. Growth is driven by increased diagnoses, stronger guideline support, improved affordability of select products, and rising commercial investments. In China, menopausal hormone therapy prescriptions rose by 86.08% from 2019 to 2023, with prescription value increasing by 126.58%, despite a pandemic-related decline in 2020. The country also shows strong use of estrogen-progestogen compound preparations, supported by centralized procurement policies improving progesterone affordability.

Competitive Landscape

The bioidentical hormones market is moderately fragmented, with competition spanning three layers. The first layer includes global compounders such as Fagron, Empower Pharmacy, and Compounding Pharmacy of America. The second layer comprises branded women’s health specialists like Mayne Pharma, Besins Healthcare, and AbbVie. The third layer involves telehealth-linked clinics and pharmacies, including AnazaoHealth, Defy Medical, The biostation, and BioTE Medical. No single company holds more than a low-to-mid single-digit market share, making factors like positioning, compliance strength, route specialization, and channel control more critical than scale.

Fagron has been a prominent strategic player in the market, completing 14 acquisitions globally by early 2026, including University Compounding Pharmacy for USD 41.5 million in January 2026 and Amber Compounding Pharmacy in Singapore and Malaysia in December 2025. The company’s USD 225 million credit facility in November 2025 supported North American growth, while its Wichita expansion is expected to generate nearly USD 25 million in additional annual revenue.

The market still offers significant opportunities, such as the need for a female-specific testosterone product to meet rising demand and the development of integrated digital care models combining consultation, personalized dispensing, refill management, and ongoing monitoring. Asia-Pacific and Latin America remain underpenetrated, with treatment levels below clinical needs and commercial infrastructure still evolving.

Bioidentical Hormones Industry Leaders

TherapeuticsMD Inc.

SottoPelle Therapy

BioTE Medical

AbbVie Inc.

Besins Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Radix Regenerative announced its role as a provider of bioidentical hormone replacement therapy, professional-grade peptides, and regenerative medicine solutions, catering to functional medicine clinics, OB/GYN practices, medical spas, and weight loss clinics across the United States.

- February 2026: Mayne Pharma reported a 26% increase in BIJUVA prescriptions and a 16% rise in NEXTSTELLIS demand cycles, alongside plans to launch an integrated digital platform in late Q3 FY2026 to streamline the patient-prescriber-fulfillment process.

- February 2026: The FDA introduced labeling updates for six menopausal hormone therapy products, while Rixa Health expanded its national telehealth services for women’s hormone replacement therapy, citing the FDA update as a key driver for improved access.

- July 2025: Texas Star Pharmacy launched a new line of bio-identical hormone pellets, emphasizing improved safety, consistency, and convenience for hormone replacement therapy users.

Global Bioidentical Hormones Market Report Scope

As per the scope of the report, bioidentical hormones are chemical substances identical in molecular structure to the hormones produced by the human body. Derived from plant sources like soy and yams, they are primarily used in hormone replacement therapy (BHRT) to relieve symptoms caused by low or unbalanced hormone levels, such as during menopause.

The bioidentical hormones market is segmented by hormone type, product type, route of administration, application, distribution channel, end-user, and geography. By hormone type, the market includes estrogens, progesterone, testosterone, DHEA, and other hormones. By product type, the market is segmented into tablets & capsules, creams & gels, patches and implants, injectables, vaginal inserts, rings & suppositories, and others. By route of administration, the market is categorized into oral, transdermal/topical, vaginal, injectable/parenteral, and subdermal implant/pellet. By application, the market includes menopause management/vasomotor symptoms, genitourinary syndrome of menopause/vaginal atrophy, andropause/male hypogonadism, sexual wellness/HSDD and related use cases, thyroid disorders, and other hormonal imbalance indications. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, compounding pharmacies, and direct clinic dispensing. By end-user, the market includes hospitals, gynecology clinics, endocrinology clinics, specialty hormone and wellness clinics, and homecare/self-administered care. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Estrogens |

| Progesterone |

| Testosterone |

| DHEA and Other Hormones |

| Tablets & Capsules |

| Creams & Gels |

| Patches and implants |

| Injectables |

| Vaginal Inserts, Rings & Suppositories |

| Other |

| Oral |

| Transdermal / Topical |

| Vaginal |

| Injectable / Parenteral |

| Subdermal Implant / Pellet |

| Menopause Management / Vasomotor Symptoms |

| Genitourinary Syndrome of Menopause / Vaginal Atrophy |

| Andropause / Male Hypogonadism |

| Sexual Wellness / HSDD and Related Use Cases |

| Thyroid Disorders |

| Other Hormonal Imbalance Indications |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Compounding Pharmacies |

| Direct Clinic Dispensing |

| Hospitals |

| Gynecology Clinics |

| Endocrinology Clinics |

| Specialty Hormone and Wellness Clinics |

| Homecare / Self-administered Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Hormone Type | Estrogens | |

| Progesterone | ||

| Testosterone | ||

| DHEA and Other Hormones | ||

| By Product Type | Tablets & Capsules | |

| Creams & Gels | ||

| Patches and implants | ||

| Injectables | ||

| Vaginal Inserts, Rings & Suppositories | ||

| Other | ||

| By Route of Administration | Oral | |

| Transdermal / Topical | ||

| Vaginal | ||

| Injectable / Parenteral | ||

| Subdermal Implant / Pellet | ||

| By Application | Menopause Management / Vasomotor Symptoms | |

| Genitourinary Syndrome of Menopause / Vaginal Atrophy | ||

| Andropause / Male Hypogonadism | ||

| Sexual Wellness / HSDD and Related Use Cases | ||

| Thyroid Disorders | ||

| Other Hormonal Imbalance Indications | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| Compounding Pharmacies | ||

| Direct Clinic Dispensing | ||

| By End User | Hospitals | |

| Gynecology Clinics | ||

| Endocrinology Clinics | ||

| Specialty Hormone and Wellness Clinics | ||

| Homecare / Self-administered Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in bioidentical hormone therapy through 2031?

Growth is being driven by stronger menopause treatment uptake, the FDA's 2025 labeling reset, wider telehealth access, and the shift toward transdermal delivery. The category is projected to grow from USD 4.29 billion in 2026 to USD 5.74 billion by 2031 at a 5.99% CAGR.

Which hormone category generates the most revenue today?

Estrogens remain the largest revenue contributor, with a 41.75% share in 2025. Their position is supported by first-line use in vasomotor symptoms, GSM, and related menopause management needs.

Why are patches and topical products gaining share so quickly?

Patches, implants, and transdermal formats are benefiting from better safety perception, avoidance of hepatic first-pass metabolism, and easier home use. Transdermal and topical delivery held 36.50% share in 2025 and is forecast to grow at 7.75% CAGR through 2031.

What is the biggest application area for hormone treatment demand?

Menopause management and vasomotor symptoms remains the largest application, with a 61.66% share in 2025. That reflects the large untreated symptom burden and improving physician willingness to prescribe therapy again.

How important are compounding pharmacies in current distribution?

Compounding pharmacies remain central, holding 38.70% of distribution in 2025 because they can tailor dose, route, and hormone combinations. At the same time, online pharmacies are growing faster at 7.55% CAGR as telehealth prescriptions increasingly flow into mail-order fulfillment.

Page last updated on: