Menopausal Hot Flashes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.12 Billion |

| Market Size (2031) | USD 10.34 Billion |

| Growth Rate (2026 - 2031) | 4.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

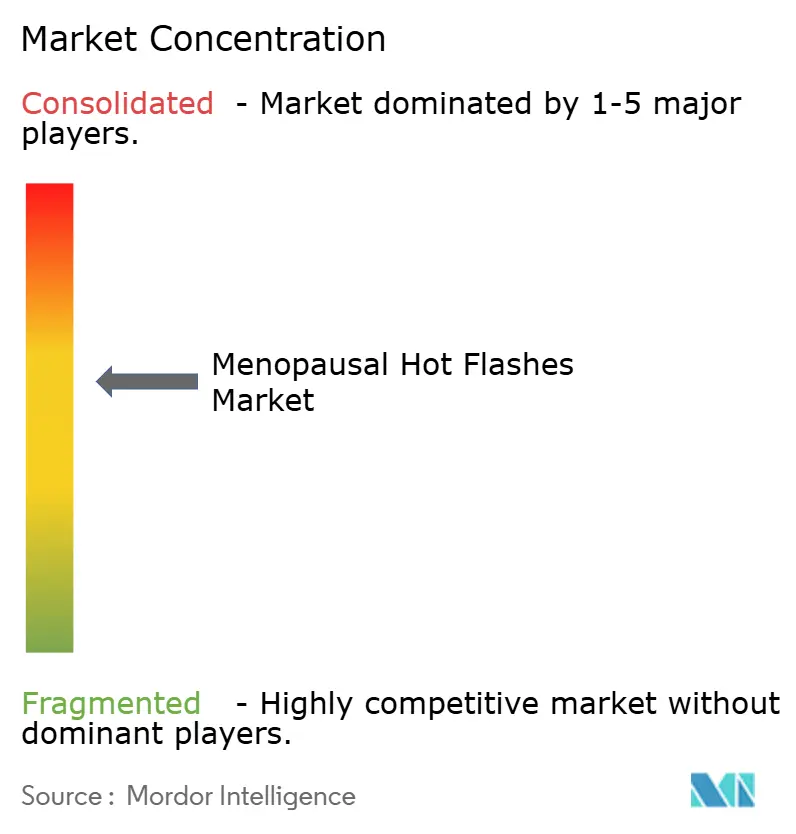

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Menopausal Hot Flashes Market Analysis by Mordor Intelligence

The menopausal hot flashes therapeutics market size is projected to be USD 7.62 billion in 2025, USD 8.12 billion in 2026, and reach USD 10.34 billion by 2031, growing at a CAGR of 4.95% from 2026 to 2031. Neurokinin-3 (NK-3) receptor antagonists such as fezolinetant are steadily capturing demand from legacy hormone replacement therapy (HRT) because they offer an estrogen-free mechanism for oncology survivors and women at thromboembolic risk. Still, mandatory baseline and periodic liver-enzyme testing introduced through a December 2024 FDA boxed warning raises per-patient costs and constrains adoption in resource-limited settings. Policy momentum is growing: the White House Office of Science and Technology Policy directed USD 113 million to women’s-health projects in February 2024, accelerating investigative programs that shorten clinical timelines for next-generation formulations. Employer-sponsored menopause benefits, ubiquitous tele-consultations, and rapid approvals of NK-3 assets are catalyzing earlier intervention, particularly among perimenopausal women who previously delayed care.

Key Report Takeaways

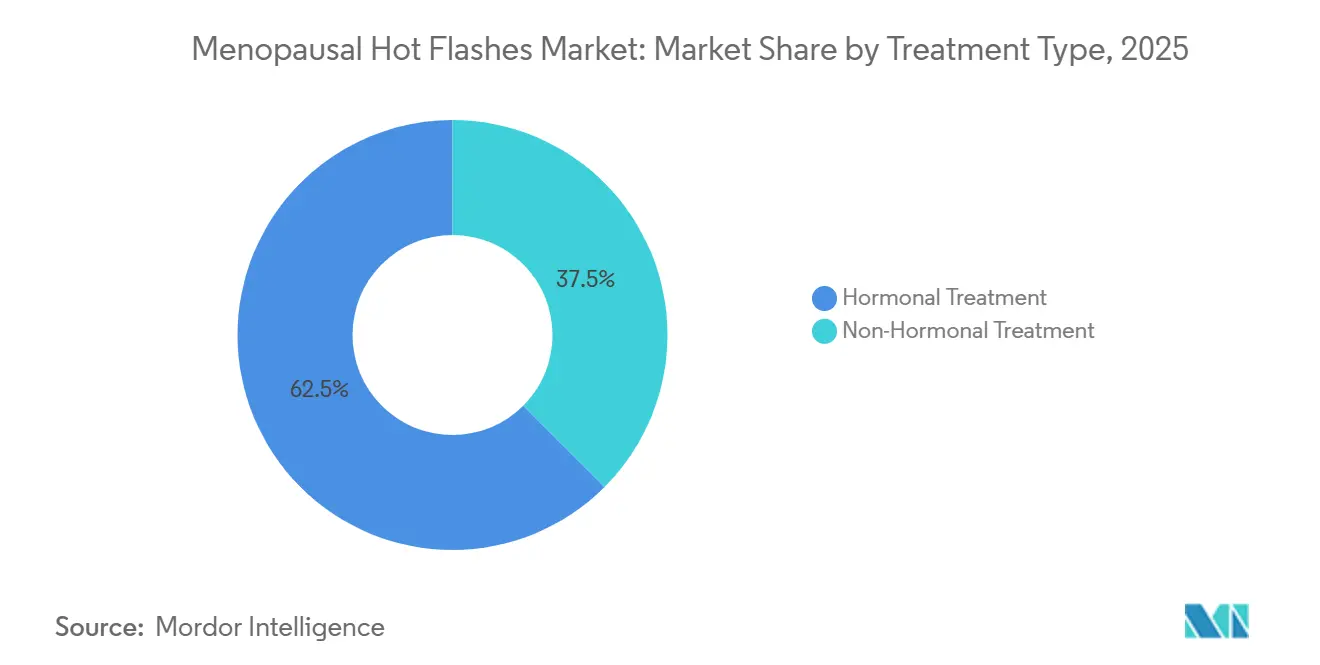

- By treatment type, hormonal options led with 62.55% of menopausal hot flashes therapeutics market share in 2025. Non-hormonal options are forecast to expand at a 7.25% CAGR between 2026-2031.

- By route of administration, oral formulations held 57.53% share of menopausal hot flashes therapeutics market size in 2025. Transdermal gels and sprays are projected to grow at 7.75% CAGR through 2031.

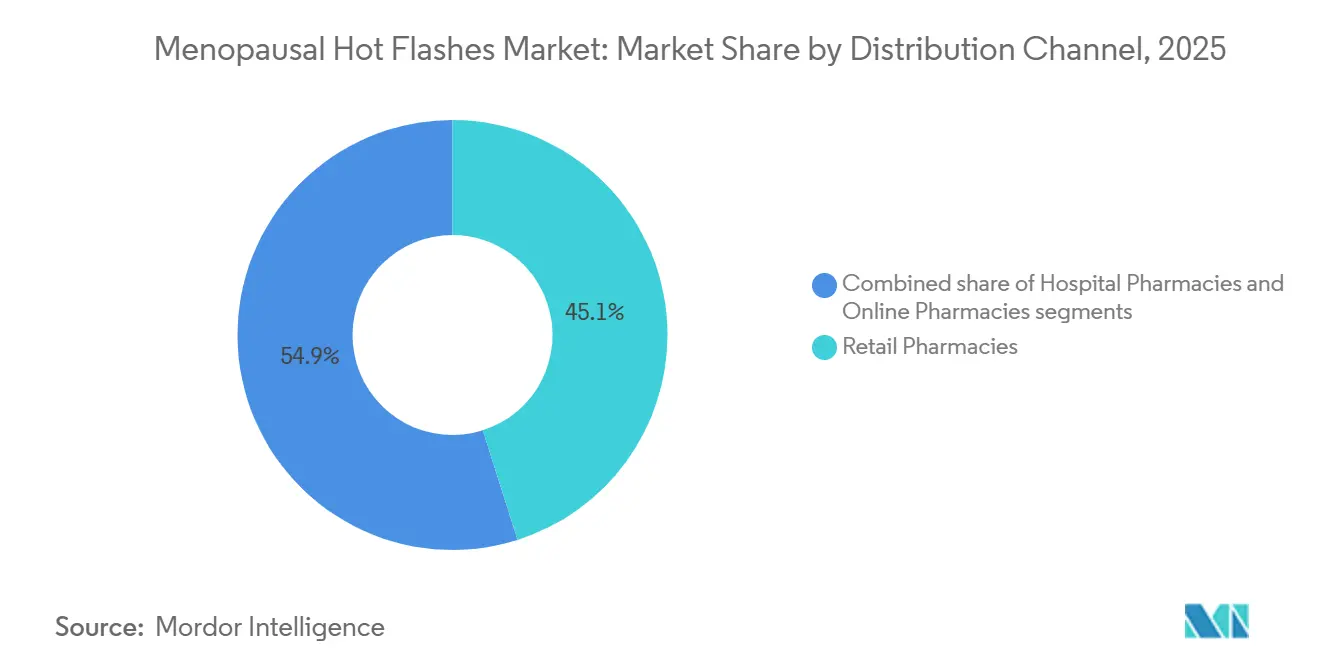

- By distribution channel, retail pharmacies captured 45.15% of global volume in 2025. Online pharmacies are advancing at an 8.82% CAGR during 2026-2031.

- By menopausal stage, early post-menopause represented 44.65% of demand in 2025. Perimenopause is the fastest-growing cohort at 8.32% CAGR to 2031.

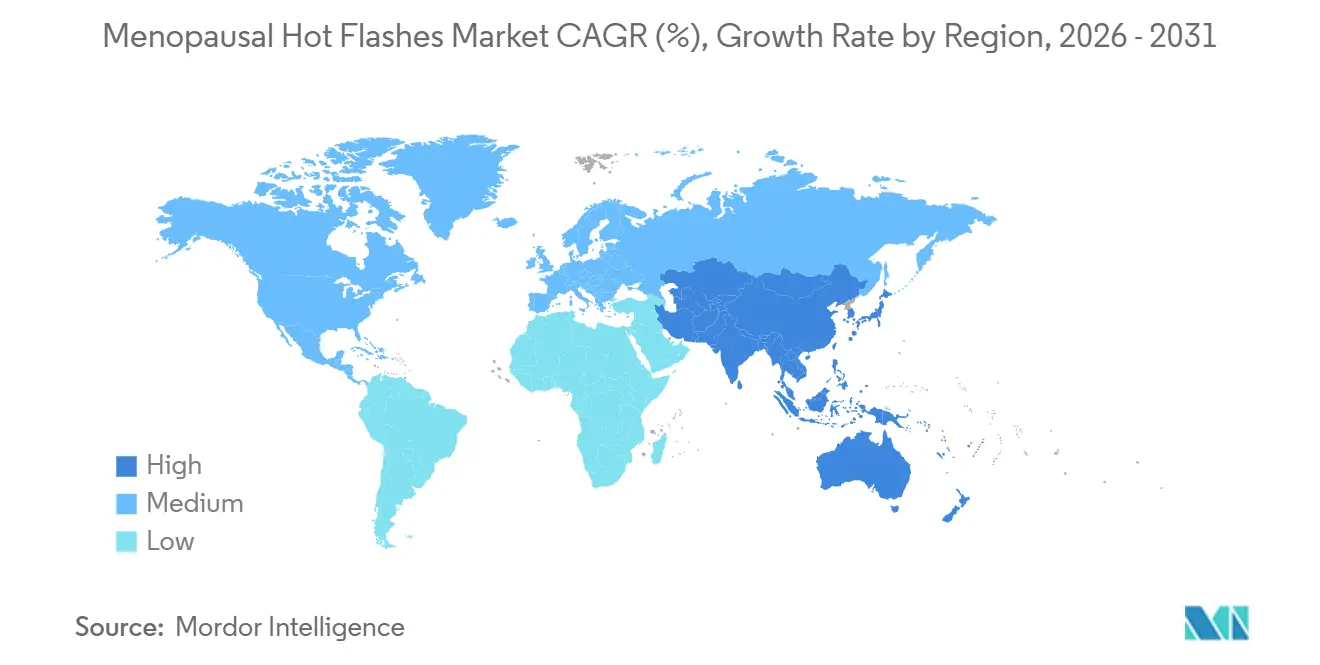

- By geography, North America captured 42.23% of global revenue in 2025; Asia-Pacific is the fastest region with a 7.42% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Menopausal Hot Flashes Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in post-menopausal female population base | +1.2% | Global, with peak impact in Japan, South Korea, Italy | Long term (≥ 4 years) |

| Growing pharmaceutical investment in women's health portfolios | +0.9% | North America & EU, spillover to APAC urban centers | Medium term (2-4 years) |

| Rapid approvals of neurokinin-3 receptor antagonists | +1.5% | North America, EU; regulatory review underway in China, Brazil | Short term (≤ 2 years) |

| Employer adoption of menopause benefits platforms | +0.7% | United States, Canada, United Kingdom | Short term (≤ 2 years) |

| AI-enabled precision dosing & companion diagnostics | +0.5% | North America & EU; pilot deployments in Singapore, UAE | Medium term (2-4 years) |

| Expansion of tele-menopause virtual clinics in underserved regions | +0.8% | APAC (India, Indonesia), Latin America (Brazil, Mexico), Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rise in Post-Menopausal Female Population Base

Longer life expectancy is lengthening the post-menopausal window, generating sustained prescription need. Japan expects its 65+ female cohort to expand by 1.8 million between 2024-2030, while the United States projects more than 58 million women aged 50+ by 2030. These population shifts persuaded Medicare Part D to list fezolinetant in January 2025, albeit with prior-authorization hurdles that reference prior HRT failure. Similar demographic curves in South Korea and Italy motivate payer reviews that gradually widen reimbursement for both transdermal HRT and NK-3 antagonists.

Growing Pharmaceutical Investment in Women’s-Health Portfolios

Global venture funding for women’s health touched USD 3.1 billion in 2024, a 42% jump year over year. Bayer is spending EUR 150 million on additional Climara patch capacity in Finland, targeting 25% output growth by 2027. Organon disclosed USD 680 million menopause-related revenue in 2024, 18% of total sales, and guided to double-digit expansion for 2025[1]Organon & Co., “2024 Annual Report,” organon.com. ARPA-H’s newly funded projects include AI-driven symptom-tracking and novel NK-3 delivery systems, potentially trimming development cycles by up to two years.

Rapid Approvals of Neurokinin-3 Receptor Antagonists

Fezolinetant secured FDA approval in 2023 followed by Health Canada and the U.K.’s MHRA in 2024. Bayer’s elinzanetant submitted an NDA in August 2024 with a June 2026 target action date; Phase 3 OASIS trials showed a 2.5-point greater reduction in symptom severity versus placebo. China’s NMPA placed elinzanetant on priority review in January 2025, suggesting a late-2026 launch that could unlock a vastly undertreated population of 120 million menopausal women.

Employer Adoption of Menopause Benefits Platforms

Fifteen percent of U.S. employers offered menopause-specific benefits in 2024, with services ranging from tele-consultations to subsidized prescriptions. Maven Clinic, covering 15 million women globally, reports that 68% of enrolled users commence therapy within one month of sign-up, compressing historical delays that exceeded six months. In the United Kingdom, NHS pilots cutting wait times from 14 weeks to under five days are further validating virtual-first pathways.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-term hepatic safety concerns for NK-3 antagonists | -0.8% | Global, with heightened scrutiny in North America & EU | Short term (≤ 2 years) |

| Limited reimbursement outside OECD markets | -1.1% | APAC (excluding Japan, South Korea), Latin America, MEA | Long term (≥ 4 years) |

| Cultural stigma suppressing care-seeking in Asia & MENA | -0.6% | India, China, Saudi Arabia, UAE, Indonesia | Medium term (2-4 years) |

| Regulatory ambiguity for botanical OTC supplements | -0.4% | Global, with fragmented enforcement in APAC & Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Long-Term Hepatic Safety Concerns for NK-3 Antagonists

The FDA recorded three acute liver-injury cases among roughly 2,400 fezolinetant users, prompting a boxed warning that now mandates serial liver tests valued at USD 150-200 per patient. Astellas noted a 22% sequential prescription decline after the warning, especially in Medicare Advantage plans tightening prior authorization. The EMA is midway through a parallel safety review due in Q2 2026, and potential restrictions could echo across Europe.

Limited Reimbursement Outside OECD Markets

In India, neither ESIC nor CGHS lists menopause therapies, leaving 92% of spending out of pocket; a three-month course of fezolinetant can equal 40% of median monthly household income in tier-2 cities[2]Employees’ State Insurance Corporation, “Essential Medicines List,” esic.gov.in. Brazil’s SUS supplies generic estradiol tablets but excludes patches and NK-3 antagonists, fostering inequity between public and private patients. Gulf insurers routinely classify menopause as “lifestyle,” and 61% of expatriate women in the UAE report never discussing symptoms with clinicians because of cost concerns.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Non-Hormonal Gains on Safety Profile

Hormonal therapy controlled 62.55% of menopausal hot flashes therapeutics market share in 2025, anchored by broad familiarity and strong efficacy data. Non-hormonal agents, primarily NK-3 antagonists, selective serotonin reuptake inhibitors (SSRIs) and gabapentinoids, are poised for a 7.25% CAGR, benefiting estrogen-contraindicated segments and oncology survivors. The menopausal hot flashes therapeutics market size for non-hormonal products is projected to expand faster than HRT as payers increasingly reimburse fezolinetant following Medicare Part D listing. Progesterone monotherapy is emerging with supportive evidence from a 2024 Cochrane review, while herbal supplements remain marginal due to inconsistent potency and weak clinical validation.

Price erosion in legacy HRT is inevitable as biosimilar estradiol patches proliferate across Europe and India. FDA approval of estetrol-drospirenone, a fetal estrogen with lower clotting propensity, may slow attrition in the hormonal segment, yet oncology survivors and high-risk cardiovascular patients will likely bypass estrogen entirely, reinforcing non-hormonal momentum. Real-world data from 1.2 million U.S. charts indicate that NK-3 antagonist usage skews toward women with absolute HRT contraindications, suggesting additive rather than cannibalistic demand.

By Route of Administration: Transdermal Innovation Accelerates

Oral therapies held 57.53% of 2025 volume, favored for lower list prices and prescribing inertia. Transdermal gels, sprays and patches are on a 7.75% CAGR trajectory through 2031, capitalizing on lower venous-thromboembolism risk and the convenience of dose titration. A meta-analysis of 14 cohort studies found a 2.1-fold reduction in VTE incidence for patches versus tablets. Microneedle and iontophoretic delivery systems trialed in 2024 achieved therapeutic estradiol levels within two hours without skin irritation, hinting at next-generation adherence solutions.

While transdermal patches dominate non-oral formulations, dissolving microneedle arrays could disrupt share by offering painless, discreet applications ideal for tropical climates where patches detach with sweat. Oral estetrol may partly offset transdermal gains in price-sensitive markets, but cold-chain-independent microneedle systems are likely to lift transdermal penetration across APAC and Africa as logistics improve.

By Distribution Channel: Online Platforms Reshape Access

Retail pharmacies delivered 45.15% of 2025 global prescriptions, yet online channels are racing ahead at an 8.82% CAGR as direct-to-consumer (D2C) models bundle teleconsultation and doorstep delivery. Hims & Hers recorded 110% year-over-year growth in menopause subscriptions in Q4 2024. Amazon Pharmacy lists estradiol patches among its top 10 items by volume and offers same-day fulfillment in 12 U.S. metros. CVS Health counters with in-store menopause kiosks where 34% of visitors initiate therapy within two weeks.

Digital pharmacies also chip away at stigma: nearly 40% of women reported preferring online conversations to avoid perceived judgment from in-person clinicians. Regulatory shifts are helping—U.K. guidance since January 2025 permits paperless HRT dispensing by online pharmacies, shrinking the compliance gap with brick-and-mortar outlets.

By Menopausal Stage: Perimenopause Intervention Gains Traction

Early post-menopause generated 44.65% of 2025 demand, reflecting symptom peak after the final menstrual period. Perimenopause, however, is racing ahead at an 8.32% CAGR through 2031 owing to guideline updates encouraging earlier HRT commencement for cardiovascular and cognitive benefit. Ultra-low-dose estradiol patches and dual-indication estetrol-drospirenone contraception are resonating among women aged 42-48 who balance symptom management with pregnancy prevention.

Employer benefits platforms skew toward younger cohorts: 54% of Maven Clinic’s menopause users were in their early forties, and early intervention reduced subsequent sleep-disorder claims by 23% over 18 months. Late post-menopause patients gravitate to NK-3 antagonists due to cumulative estrogen exposure limits and contraindications for older age groups, sustaining a lift for fezolinetant in the 60-65 bracket.

Geography Analysis

North America maintained 42.23% of 2025 revenue and will grow at 4.2% CAGR to 2031, amplified by Medicare Part D listing of fezolinetant and a robust network of specialty clinics. Canadian provinces adopted favorable reimbursement in late 2024, while Mexico’s private sector imports transdermal patches from the United States to compensate for limited IMSS offerings. Corporate menopause programs are most mature here, cutting median therapy-initiation times to one month. FDA guidance released in 2024 that lowers trial burdens for symptomatic relief drugs should further energize pipeline velocity.

Asia-Pacific is projected to register a 7.42% CAGR—the fastest globally—as regulatory pathways converge and aging accelerates. Japan’s 65+ female share rose to 28.9% in 2024, driving sustained patch usage[3]Japan Ministry of Health, “Demographic Statistics 2024,” mhlw.go.jp. China’s NMPA fast-tracked estradiol-progesterone combinations in 2025 and is reviewing elinzanetant under priority status, but cultural delay persists: fewer than 2% of symptomatic women seek prescription care. India’s tele-medicine surge, headlined by Veera Health, shows rural engagement when language-localized virtual care is offered. South Korea’s insurance co-pay reset to 30% for patches in 2024 caused a 47% utilization jump.

Europe’s centralized EMA approvals streamline launches; fezolinetant gained clearance in November 2024, and biosimilar patches slashed prices up to 35% in Germany and France. NHS England’s pilot cut wait times to under five days, spurring 31% higher HRT initiation rates. Italy and Spain remain fully out-of-pocket markets for vasomotor indications, hamstringing adoption. Eastern Europe lags in awareness, although EU cohesion funds back education drives in Poland and Romania.

Middle East & Africa expands from a small base. Saudi Arabia’s insurance package now mandates HRT coverage, and the SFDA fast-tracked fezolinetant in January 2025. In the UAE, expatriate women commonly pay cash because private plans exclude menopause care, while South Africa’s reimbursement ceiling of ZAR 120 limits branded product reach. Telehealth pilots in Kenya and Nigeria demonstrate early promise in circumventing cultural resistance and provider shortages. South America is dominated by Brazil, where SUS funds generic estradiol tablets yet omits patches and NK-3 antagonists. Cold-chain limitations complicate patch logistics across Amazonian states, and most advanced therapies are confined to private-pay urban markets.

Regulatory Landscape

Regulatory oversight for menopausal hot flashes therapeutics is increasingly shaped by benefit-risk scrutiny around hepatic safety for neurokinin-pathway drugs and by expanded labeling that recognizes vasomotor symptoms beyond natural menopause. In the United States, the FDA approval of fezolinetant (Veozah) in 2023 established the leading non-hormonal pathway, and subsequent labeling updates (including a December 2024 boxed warning referenced in the report context) reinforced baseline and periodic liver-function monitoring as a practical compliance standard for NK-3 prescribing and payer coverage.

Across Europe, EMA actions have widened the regulated therapeutic toolkit and indications relevant to oncology-linked vasomotor symptoms. Lynkuet (elinzanetant) received EU marketing authorization in November 2025 for moderate-to-severe vasomotor symptoms associated with menopause, including hot flashes caused by adjuvant endocrine therapy, aligning regulatory language with breast cancer care pathways. In early 2026, EMA momentum also extended to hormonal options, with CHMP issuing a positive opinion for Fylrevy (estetrol) in January 2026, followed by EU marketing authorization in March 2026, supporting continued product refresh in HRT alongside newer non-hormonal entrants.

Competitive Landscape

The menopausal hot flashes therapeutics market features moderate concentration: the top five companies account for a notable but not majority share. Astellas’ Veozah generated USD 180 million in the first nine months of 2025, below target after hepatotoxicity warnings tightened payer criteria. Bayer’s dual NK-1/NK-3 antagonist elinzanetant is positioned as a sleep-and-mood differentiator and is under FDA and EMA review, backed by a EUR 150 million capacity investment in Turku. Generic manufacturers such as Teva, Lupin and Cipla pressured HRT pricing by 25-35% with biosimilar patches across Europe and India.

Digital differentiation is critical: Organon integrates its HRT line with Ovia Health’s symptom-tracking app, improving six-month adherence by 19 percentage points. Pfizer is trialing wearable-triggered sublingual estradiol micro-doses, while small biotechs KaNDy Therapeutics and Mithra Pharmaceuticals advance combination NK-3 plus SERM candidates through Phase 2, aiming to address bone-density needs unmet by stand-alone antagonists. D2C platforms such as Hims & Hers and Midi Health are reshaping demand origination, especially among tech-savvy perimenopausal consumers.

Menopausal Hot Flashes Industry Leaders

Astellas Pharma Inc.

Bayer AG

Pfizer Inc.

AbbVie Inc. (Allergan)

Organon & Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace centers on non-hormonal therapies for women who avoid or cannot use estrogen, including oncology survivors and patients at thromboembolic risk, where neurokinin antagonists provide an alternative mechanism. The competitive set has broadened from NK-3-only therapy (Astellas, Veozah) to dual NK1/NK3 therapy (Bayer, Lynkuet), with FDA approval of Lynkuet in October 2025 and earlier U.K. MHRA approval in July 2025 adding a branded option that manufacturers and prescribers can position for symptom clusters such as sleep and mood. At the same time, mandated liver-enzyme monitoring tied to fezolinetant safety labeling increases the total cost of care and creates room for differentiated safety and monitoring workflows that reduce testing friction.

Geographic and channel expansion opportunities also track areas where access and reimbursement remain uneven. Canada added a non-hormonal option when Health Canada approved Veozah in December 2024, and Astellas subsequently made it available in pharmacies in March 2025. In many non-OECD markets, payer lists still favor low-cost oral estradiol and exclude patches and NK-pathway drugs, leaving large out-of-pocket segments underpenetrated. Digital-first care and dispensing models provide another route to earlier intervention, supported by employer menopause-benefits adoption and tele-consult pathways highlighted in the report context; scaling these models alongside specialty-pharmacy distribution can reduce stigma and appointment delays that suppress diagnosis and treatment initiation.

Recent Industry Developments

- April 2026: Sun Pharmaceutical Industries signed a definitive agreement to acquire Organon & Co. for USD 11.75 billion in an all-cash transaction. The deal targets scale in womens health and can reshape commercialization focus and portfolio prioritization across menopause therapies and adjacent womens health categories.

- March 2025: Astellas announced that VEOZAH (fezolinetant) became available in pharmacies across Canada for treatment of moderate to severe vasomotor symptoms associated with menopause. Commercial availability following approval expanded North American access to a non-hormonal NK-3 option and reinforced specialty and retail pharmacy pathways for branded, monitoring-linked therapies.

- December 2024: Health Canada approved VEOZAH (fezolinetant) as the first non-hormonal treatment for moderate to severe vasomotor symptoms associated with menopause. The decision broadened the regulated non-hormonal category outside the United States and supported payer and provider adoption discussions around estrogen-free management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the value of therapies used to reduce menopausal hot flashes in peri and postmenopausal women, counted at the level of products delivered through standard healthcare and pharmacy channels across major regions.

Scope exclusions: We exclude diagnosis services, routine gynecology visits, and broader menopause care not directly linked to hot flash symptom control.

Segmentation Overview

- By Treatment Type

- Hormonal Treatment

- Estrogen

- Progesterone

- Estrogen-Progesterone Combination

- Non-Hormonal Treatment

- NK-3 Receptor Antagonists

- SSRIs

- SNRIs

- Gabapentinoids

- Herbal & Dietary Supplements

- Hormonal Treatment

- By Route of Administration

- Oral

- Transdermal Patch

- Transdermal Gel/Spray

- Parenteral (Injectable)

- Topical (Vaginal/Derma)

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- By Menopausal Stage

- Perimenopause

- Early Post-Menopause (?5 yrs)

- Late Post-Menopause (>5 yrs)

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by mapping the patient pool and treatment environment, so our assumptions have a clear anchor. We reviewed public health sources such as the US CDC, the US NIH and its PubMed index, the World Health Organization, and the US FDA drug labels and safety communications to track epidemiology, treatment guidance, and approvals.

To keep regional trends consistent, we also referred to sources such as OECD health statistics, national health ministries, and peer reviewed journals that report vasomotor symptom prevalence and treatment patterns. Additional context comes from company annual reports, investor presentations, reputable medical news, and, when helpful, paid subscriptions covering company financials and intelligence, along with patent databases used as a signal for innovation activity. The examples above are illustrative, and many other public and paid sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test the desk assumptions and translate them into practical sizing inputs, especially around treatment mix, typical duration of therapy, access pathways, and price behavior by channel. We spoke with a spread of respondents across prescribers, pharmacy and distribution stakeholders, and industry experts, covering the major regions so regional uptake and reimbursement differences were not averaged away.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 15% | APAC: 38% |

| Mid tier: 55% | Functional/Unit leaders: 34% | EMEA: 36% |

| Smaller Players: 19% | Managers: 51% | Americas: 26% |

Market-Sizing & Forecasting

Sizing is built using a top down approach where prevalence and treated share are translated into demand, then converted into value using therapy mix and average annual treatment cost by route and channel. Once the demand pool is formed, we check it with selective bottom-up approximations, including sampled price points by channel, supplier and distributor checks on mix shifts, and a sanity roll up across key therapy classes to confirm that no single category is overstated.

Key model inputs include the menopausal population by age band, prevalence of moderate to severe vasomotor symptoms, diagnosis and treatment seeking rates, split between hormonal and non-hormonal use, and persistence or discontinuation patterns that affect annualized demand. We track route shifts (oral versus transdermal) and channel mix (hospital, retail, and online pharmacies) because these factors move the blended price and realized market value. Forecasts are produced using scenario analysis supported by trend lines on treatment adoption, policy and label changes, and expert views on how newer non-hormonal options can change uptake. When country level data is thin, we use proxy indicators from similar markets and then correct them through interviews before finalizing totals.

Data Validation & Update Cycle

Outputs are cross checked against independent signals such as approval timelines, prescription behavior commentary in public filings, and reported pricing changes in major markets. We then review results for outliers at the country and therapy class level. If a large variance appears, we re-check the patient pool build, treatment duration assumptions, and currency conversion timing, followed by targeted re-contacts to close gaps.

Before sign-off, the model and narrative go through multi-step analyst reviews to keep arithmetic, logic, and scope boundaries consistent across sections. The study is refreshed annually, and interim updates are made when a material event occurs such as a major approval, safety update, or reimbursement change. Right before delivery, a final pass is completed to confirm the numbers and assumptions reflect the latest available evidence.

Mordor Intelligence's Menopausal Hot Flashes Market Size Versus Other Published Estimates

Published numbers for menopausal hot flashes often do not match because the underlying counting logic is not the same, even when the market title looks identical. Differences usually come from what gets included as a therapy, which pricing level is used, and whether the model is tied to a treated patient pool or to product revenue definitions.

Key gap drivers in this market are common, but they are also easy to miss in headlines. Some estimates fold in broader menopause management or adjacent symptom products, and others use factory gate revenue concepts that can inflate totals versus demand-based patient spending in end markets. Currency conversion timing and the refresh cadence around newer non-hormonal launches can also shift the reported year value, even if long-term growth rates look similar.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.62 B (2025) | |

| Trade Publisher A | USD 15.92 B (2025) | Uses a revenue accounting view that references factory gate values and can count related services differently, which tends to expand the value base beyond treated-patient demand spending in end markets. |

| Industry Research Outlet B | USD 8.76 B (2024) | Uses a 2024 base year with a longer horizon and broader segment framing, and the included product perimeter is not always explicit by route and channel, which can shift what is counted as hot flash treatment. |

Approval and label evidence, plus observed adoption signals by route and channel, are the checks that keep Mordor Intelligence's estimate tied to the treated hot flash population rather than a broad revenue bucket. Taken together, the spread in the table mostly reflects how wide the therapy boundary is drawn and which price layer is used, and our approach stays repeatable because each step maps back to patient counts, treatment mix, and annualized cost.

Key Questions Answered in the Report

What is the projected value of the menopausal hot flashes therapeutics market by 2031?

It is forecast to reach USD 10.34 billion by 2031.

Which treatment class is growing fastest within menopause hot-flash therapy?

Non-hormonal products, especially NK-3 antagonists, are expanding at 7.25% CAGR through 2031.

Why are transdermal patches attracting interest versus oral estrogen?

They bypass first-pass metabolism, cut thrombosis risk by roughly half, and offer steadier hormone levels.

How are virtual clinics influencing therapy uptake?

Platforms such as Maven Clinic reduce initiation delays to under one month and boost adherence via remote monitoring.

Page last updated on: