Postmenopausal Osteoporosis Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

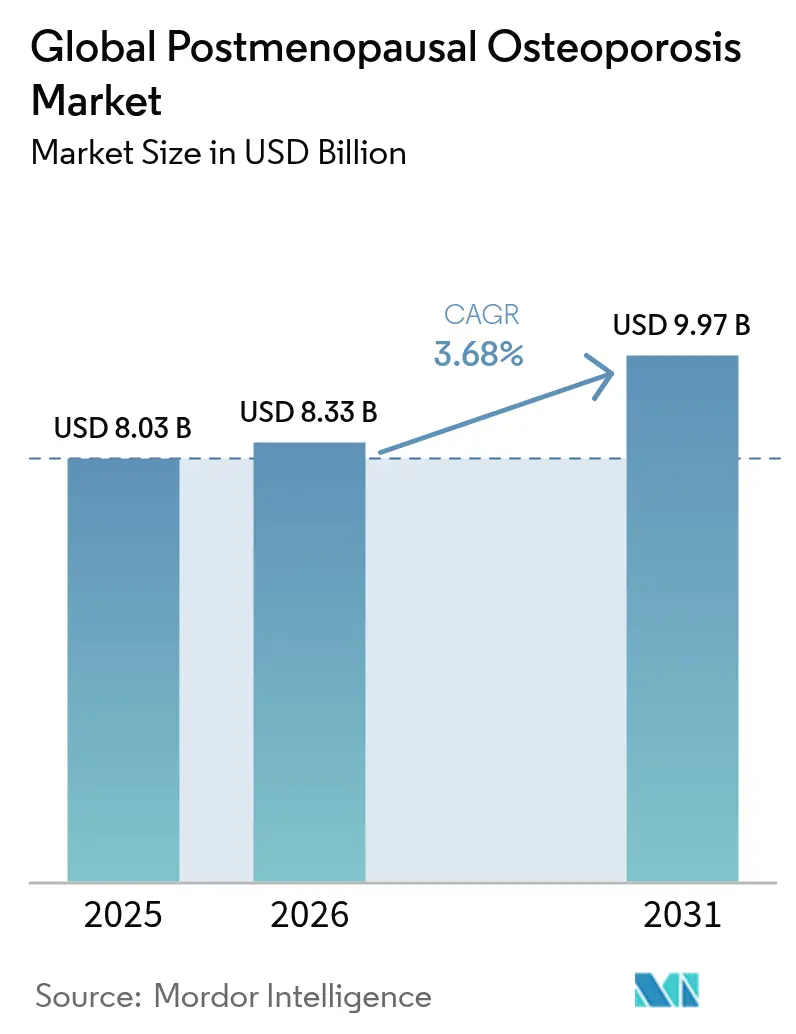

| Market Size (2026) | USD 8.33 Billion |

| Market Size (2031) | USD 9.97 Billion |

| Growth Rate (2026 - 2031) | 3.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

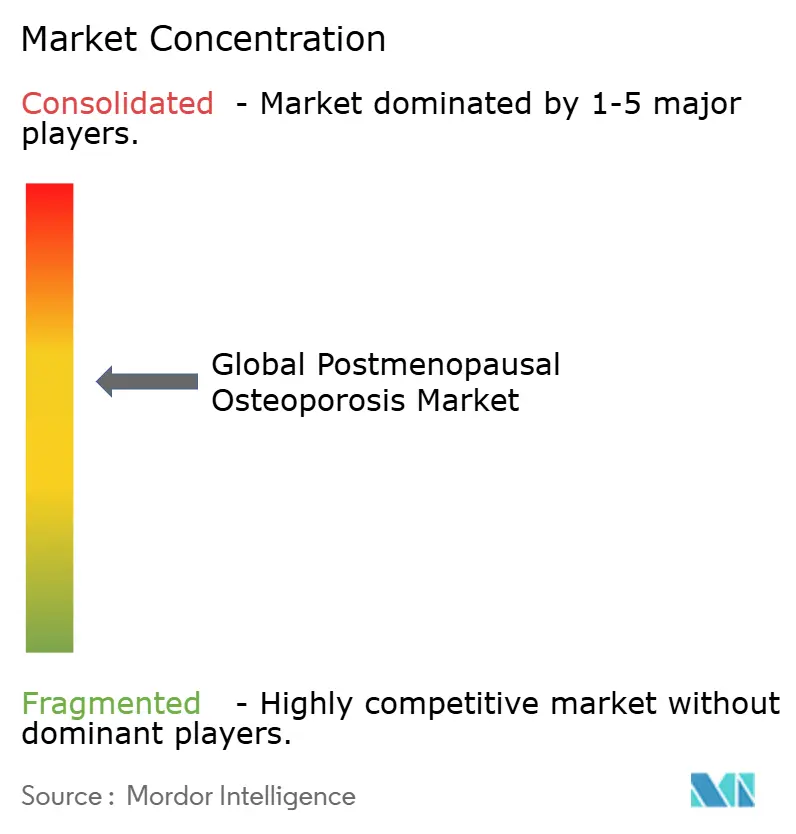

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Postmenopausal Osteoporosis Market Analysis by Mordor Intelligence

The Postmenopausal Osteoporosis Market size is expected to grow from USD 8.03 billion in 2025 to USD 8.33 billion in 2026 and is forecast to reach USD 9.97 billion by 2031 at 3.68% CAGR over 2026-2031.

Competitive dynamics are shifting as denosumab’s primary patent expiry in early 2025 opened the door for biosimilars such as Wyost and Jubbonti, bringing price pressure and forcing originator brands to emphasise service-based differentiation. Rising life expectancy, particularly among post-menopausal women, keeps underlying demand firm, with vertebral fractures already affecting millions of patients each year despite advances in prevention. Bisphosphonates still account for nearly half of global sales, yet their dominance is eroding as generic entries broaden access while concerns over rare long-term adverse effects temper repeat prescribing. RANKL inhibitors are expanding the fastest, supported by denosumab’s strong adherence profile and a widening biosimilar field that is attracting cost-conscious payers. North America remains the largest revenue generator, yet Asia-Pacific is emerging as the principal growth engine thanks to rapid population ageing and improving reimbursement frameworks

Key Report Takeaways

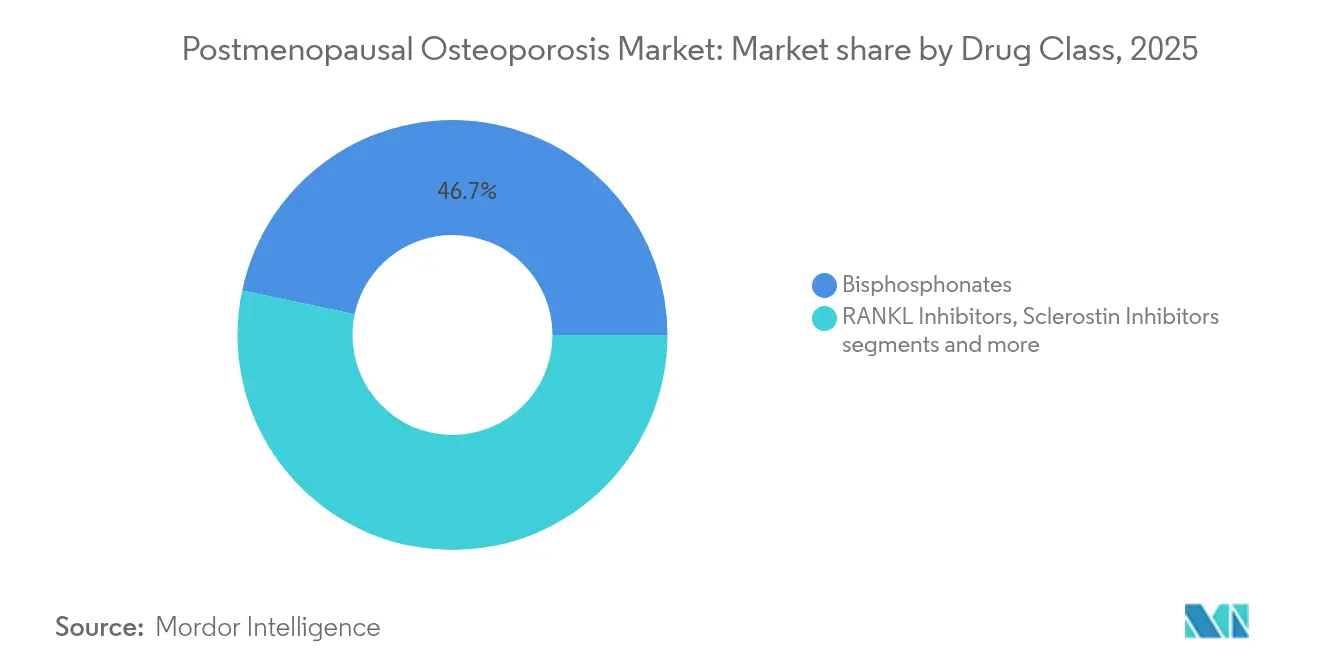

- By drug class, bisphosphonates led with 46.68% of osteoporosis drugs market share in 2025, whereas RANKL inhibitors are projected to expand at 5.04% CAGR to 2031.

- By route of administration, oral agents accounted for 60.12% share of the osteoporosis drugs market size in 2025; subcutaneous delivery posts the fastest 5.76% CAGR between 2026-2031.

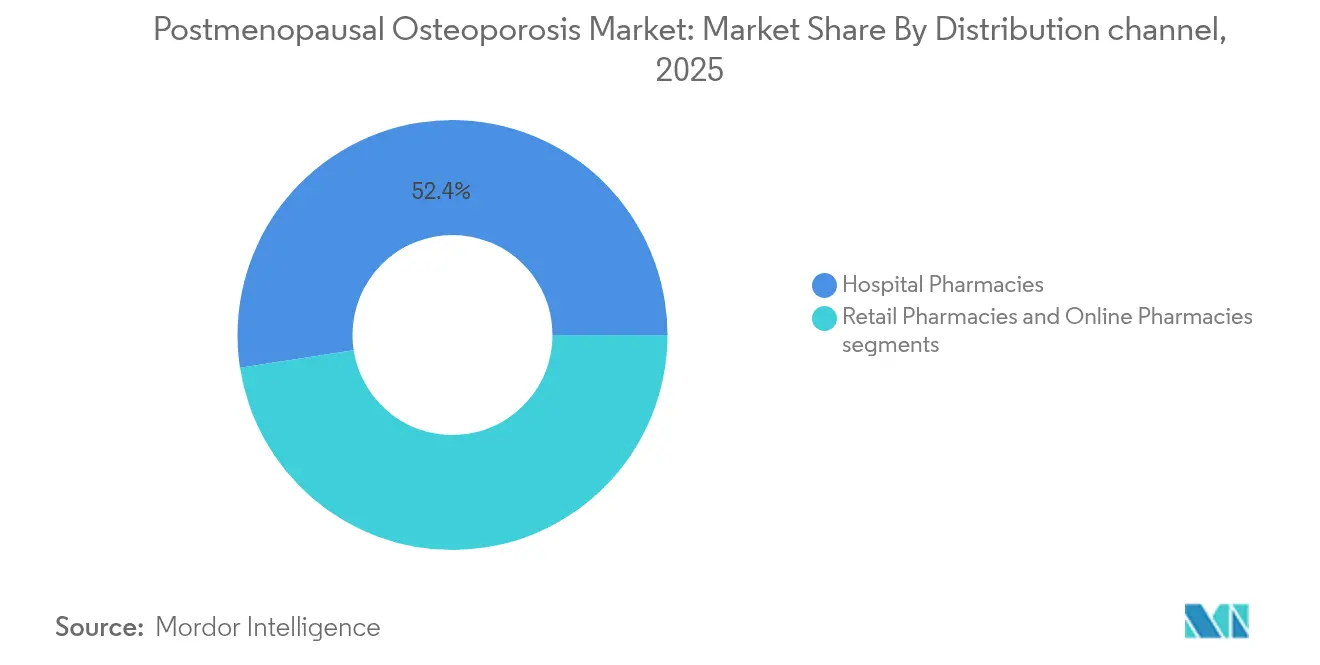

- By distribution channel, hospital pharmacies dominated with 52.43% revenue share in 2025, while online pharmacies are set to grow at 5.49% CAGR through 2031.

- By geography, North America held 37.28% of osteoporosis drugs market share in 2025, and Asia-Pacific registers the highest 6.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Postmenopausal Osteoporosis Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing ageing female population base | +1.20% | Global, concentrated in developed economies | Long term (≥ 4 years) |

| Fracture-cost containment programs by insurers | +0.80% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Bisphosphonate patent expiries boosting generics | +0.60% | Global, early gains in US, EU, Japan | Short term (≤ 2 years) |

| Launch of anabolic agents with superior BMD efficacy | +0.90% | North America & EU core, spill-over to APAC | Medium term (2-4 years) |

| AI-based fracture-risk screening in primary care | +0.40% | Developed markets, pilot programs in emerging | Long term (≥ 4 years) |

| Integration of digital adherence tools with injectables | +0.30% | Global, higher adoption in tech-savvy demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Ageing Female Population Base

The number of women aged 50 years and older is projected to climb 30% globally by 2030, driving first-line screening and therapy use. Recent studies in China reveal significant regional variations, with Shanghai reporting osteoporosis prevalence of 12.5% among middle-aged adults, while Sichuan Province demonstrates 19.42% overall prevalence, with 32.1% of postmenopausal women and 6.9% of men over 50 affected. Longer life expectancy positions high-risk women for extended pharmacologic exposure, increasing demand for agents with proven fracture-risk reduction. Consequently, manufacturers are prioritising once-yearly or biannual dosing regimens to align with geriatric adherence needs.

Fracture-Cost Containment Programs by Insurers

US and EU payers intensify post-fracture programs after economic analyses show that treating high-risk patients early saves direct medical costs compared with managing subsequent fractures. Mexican modelling demonstrated that romosozumab can reduce lifetime costs by USD 51,363 per patient while improving outcomes relative to teriparatide. Belgium followed with favourable health-economic findings supporting reimbursement for anabolic treatment in very high-risk postmenopausal women. Insurers therefore steer formularies toward injectable therapies showing 92.5% adherence versus 63.5% for oral alendronate.

Bisphosphonate Patent Expiries Boosting Generics

Alendronate, risedronate and ibandronate lost exclusivity in major markets, and generic uptake now exceeds 80% of prescriptions in many EU states, lowering annual therapy cost by up to 70%. Lower prices widen access in emerging economies, prompting guidelines to favour initiating generics when fracture risk is moderate. This generic shift also frees payer budgets to fund premium anabolic agents for very high-risk patients. Manufacturers respond through reformulated weekly or monthly tablets to defend brand loyalty. Digital reminder apps bundled with generics aim to curb the 35% discontinuation observed during the first treatment year.

Launch of Anabolic Agents with Superior BMD Efficacy

Romosozumab’s dual mechanism yields 73% relative reduction in new vertebral fractures versus placebo, reshaping osteoporosis treatment sequences. The 2024 ASBMR/BHOF guidance now recommends anabolic-first therapy in very high-risk patients before antiresorptive maintenance. NICE’s 2024 green light for abaloparatide opened NHS reimbursement to 14,000 women deemed at imminent fracture risk. Real-world satisfaction tops 86% among abaloparatide users, with 83% adherence at 12 months, reinforcing payer confidence. Sequential protocols combining 12 months of anabolic therapy followed by denosumab are moving into mainstream clinical routines.

Restraints Impact Analysis of Postmenopausal Osteoporosis Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Safety concerns around long-term bisphosphonate use | -0.70% | Global, heightened awareness in developed markets | Medium term (2-4 years) |

| Declining DXA scanner reimbursement in Europe | -0.50% | Europe primary, secondary effects in other regions | Short term (≤ 2 years) |

| Low therapy adherence beyond 12 months | -0.80% | Global, particularly acute in oral therapy segments | Long term (≥ 4 years) |

| Limited payer coverage for bone-building biologics | -0.40% | Emerging markets, selective coverage in developed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Safety Concerns around Long-Term Bisphosphonate Use

Emerging evidence links extended bisphosphonate courses with atypical femoral fractures and osteonecrosis of the jaw, prompting clinicians to opt for drug holidays after 3–5 years. Awareness campaigns in the US and EU shifted 12-month persistence from 54% in 2020 to 47% in 2024 as cautious patients discontinued therapy, dampening sales. Regulatory agencies now require class-wide labelling updates describing rare fracture risks. These safety dialogues accelerate physician adoption of injectables that deliver comparable or superior BMD gains without prolonged skeletal retention. Nevertheless, payers weigh the higher acquisition cost of biologics against long-term fracture avoidance benefits.

Declining DXA Scanner Reimbursement in Europe

Cuts in national tariffs have forced many private radiology centres to retire DXA services, stretching wait times for bone density tests beyond 6 months in parts of Italy and Spain. Hospital-based scanners absorb overflow but create scheduling bottlenecks. Limited diagnostic capacity delays therapy initiation, especially in rural settings. Policymakers consider boosting tariffs or funding mobile DXA units to prevent missed fracture-prevention opportunities. AI-driven CT opportunistic screening is a potential workaround, yet payers remain cautious about reimbursement until large-scale validation confirms cost-effectiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Postmenopausal Osteoporosis Market Segment Analysis

By Drug Class:

Biosimilar Competition Reshapes Market LeadershipBisphosphonates commanded 46.68% of the osteoporosis drugs market share in 2025, buoyed by decades of clinician familiarity and low pricing. However, the osteoporosis drugs market size for RANKL inhibitors is projected to expand as biosimilar denosumab variants roll out worldwide. Sandoz introduced Wyost and Jubbonti in May 2025 in the US, and Samsung Bioepis, Celltrion and Teva will follow through 2026. First-to-market biosimilars launched at price discounts of 20-30%, accelerating adoption in cost-sensitive health systems.

Sequential anabolic-antiresorptive therapy is becoming standard in very high-risk cohorts, sustaining demand for both classes. Parathyroid hormone analogs gain renewed momentum after NICE endorsed abaloparatide, and experts predict double-digit uptake in Europe once reimbursement cascades through other markets. SERMs and calcitonin maintain niche usage among patients contra-indicated for frontline agents. Generic pipelines remain active across all small-molecule classes, and reformulation strategies such as effervescent tablets aim to retain market share against low-cost copies. Overall, innovation and biosimilar economics intertwine to create a two-tier competitive field where value-based pricing dominates purchasing.

By Route of Administration:

Injectable Therapies Gain PreferenceOral options still accounted for 60.12% of the osteoporosis drugs market size in 2025, driven by weekly or monthly bisphosphonate dosing and mature generic lines. Yet subcutaneous agents are on track for a 5.76% CAGR through 2031 as patients and providers gravitate toward biannual injections such as denosumab or monthly romosozumab. Randomised trials confirm superior femoral-neck BMD gains with denosumab versus alendronate, fuelling confidence in biologic delivery routes. Patient-reported studies show that 88% of elderly users prefer at-home injection devices over clinic-based infusions.

Intravenous zoledronic acid retains a role for those seeking annual dosing convenience, with pivotal studies documenting 70% spinal-fracture risk reduction. Wearable ultrasound device Osteoboost became the first non-pharmacologic prescription option cleared by FDA in May 2025, signalling technology’s capacity to complement pharmacotherapy. Digital adherence add-ons integrated into autoinjectors now transmit dosing confirmation to cloud dashboards, lifting 12-month persistence rates from 65% to 92% in pilot cohorts. Collectively, delivery innovation aligns with the broader trend toward personalising therapy according to fracture risk and lifestyle practicality

By Distribution Channel:

Digital Transformation Accelerates Online GrowthHospital pharmacies generated 52.43% of global revenue in 2025 because injectable biologics require cold-chain management and nurse-led counselling. Integrated Fracture Liaison Services inside hospitals further reinforce this channel by linking post-fracture patients to immediate therapy initiation. Online outlets achieved the fastest 5.49% CAGR projection as pandemic-era habits normalised mail-order fulfilment and digital refill reminders. Retail chains still command a meaningful footprint but feel price pressure from internet competitors offering auto-ship discounts and telepharmacy support.

Payers increasingly contract directly with specialty pharmacies for biosimilar denosumab, bundling medication with virtual adherence coaching to maximise cost savings. In emerging markets, e-commerce pharmacy apps are bridging geographic gaps by delivering generics to underserved rural zones within 48 hours. Regulatory agencies tighten oversight of online sales to reduce counterfeit risk, mandating track-and-trace serialisation for biologics. Overall, distribution evolves toward omnichannel models that place patient convenience and data-driven adherence at the centre of commercial strategy.

Geography Analysis

North America Postmenopausal Osteoporosis Market

North America captured 37.28% of 2025 revenue for the osteoporosis drugs market. Broad insurance coverage and rapid adoption of novel agents underpin leadership, while the FDA’s clearance of digital therapeutic Osteoboost exemplifies the region’s openness to breakthrough solutions. Biosimilar pressure escalates after February 2025, yet Amgen’s Prolia still posted 10% sales growth in Q1 2025 pre-erosion, signalling resilience through brand loyalty programs. Policy moves such as CMS removing prior-authorisation hurdles on select bone stimulators further smooth treatment pathways .

Europe Postmenopausal Osteoporosis Market

Europe shows steady, value-driven uptake of biosimilars after EMA approvals of Wyost, Jubbonti, Stoboclo and Osenvelt through 2024-2025. NICE’s economic endorsement of abaloparatide in England set a precedent for wider EU funding, covering 14,000 high-risk women in its first year. Nonetheless, shrinking DXA reimbursement narrows diagnostic capacity, prompting Italian experts to petition AIFA for algorithm-based fracture-risk assessment upgrades. Health ministries weigh mobile scanning vans and AI-enhanced CT analytics to mitigate bottlenecks.

APAC Postmenopausal Osteoporosis Market

Asia-Pacific posts the fastest 6.41% CAGR as shifting demographics swell the patient base; prevalence already affects up to 30% of women over 40 in developed regional economies. Multinationals pursue local licensing; Radius granted Pharmanovia rights to abaloparatide for China and ASEAN markets in March 2025, aiming to leverage escalating fracture rates. Regional guidelines increasingly acknowledge ethnicity-specific BMD norms to prevent misclassification, highlighting the need for device calibration research.

Competitive Landscape

Leading players collectively held about more tha half of osteoporosis drugs market revenue in 2024, indicating moderate concentration. Amgen anchors the field with Prolia and romosozumab; the company booked USD 1.1 billion and USD 442 million respectively in Q1 2025, and is cross-promoting digital adherence apps to defend share against biosimilars. Sandoz became the first biosimilar entrant, pricing Wyost and Jubbonti at double-digit discounts and bundling nurse-coach services to accelerate switching. Samsung Bioepis, Celltrion, Teva and Amneal are lining up phased launches through 2026, leveraging manufacturing scale and risk-sharing contracts.

Innovation remains vibrant: UCB licensed its BoneBot AI software to ImageBiopsy Lab in June 2024, aiming to detect silent vertebral fractures on routine imaging and funnel untreated patients into therapy. Novartis maintains a differentiated niche with zoledronic acid’s once-yearly dosing, while exploring subcutaneous long-acting sclerostin inhibitors. Lilly’s USD 650 million alliance with Juvena Therapeutics targets muscle anabolism in GLP-1 users at fracture risk, underscoring convergence between bone and metabolic segments. Several Chinese biotech firms have entered Phase 1 programmes for oral RANKL inhibitors, signalling future disruption.

Successful strategies increasingly couple pharmacology with software: Amgen links Prolia with smartphone reminders, and Sandoz bundles remote nurse outreach in its biosimilar starter kits. Specialty pharmacies deliver cold-chain tracked biologics while feeding adherence metrics back to manufacturers under value-based contracts. In parallel, generics suppliers differentiate through effervescent or chewable tablets to capture aging patients with dysphagia. The interplay of price competition and digital service layering is expected to recalibrate margins but enlarge patient reach, particularly in emerging economies.

Postmenopausal Osteoporosis Industry Leaders

Amgen Inc.

Eli Lilly and Co.

F. Hoffmann-La Roche Ltd

Merck & Co., Inc.

Allergan plc

- *Disclaimer: Major Players sorted in no particular order

Postmenopausal Osteoporosis Market Companies Covered in this Report

- Amgen

- Eli Lilly and Company

- Pfizer

- Procter & Gamble

- Novartis

- Clonz Biotech

- Ligand Pharmaceuticals

- Merck

- BiologicsMD

- Enteris BioPharma

- Oncobiologics

- Abbvie

Recent Industry Developments in Postmenopausal Osteoporosis Market

- June 2025: Wyost and Jubbonti launched as the first US denosumab biosimilars, introducing biosimilar price competition for a USD 5 billion reference franchise.

- May 2025: FDA cleared Osteoboost, the first prescription wearable for low bone density, positioning a non-drug option for 60 million Americans.

- January 2025: Pharmanovia secured rights to commercialise abaloparatide in China and selected Asia-Pacific markets.

Postmenopausal Osteoporosis Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the postmenopausal osteoporosis market as the global revenue generated from prescription medicines, physician-administered biologics, and reimbursed supplements that are clinically indicated to prevent or treat osteoporosis arising after natural or surgical menopause. This encompasses bisphosphonates, RANKL and sclerostin inhibitors, SERMs, parathyroid hormone analogs, calcitonin, and emerging anabolic agents supplied through hospital, retail, and online pharmacies.

Scope exclusion: sales linked to male, pediatric, or steroid-induced osteoporosis therapies remain outside the present analysis.

Segments Covered in This Report

- By Treatment

- Vitamin D

- Bisphosphonates

- Hormone Replacement Therapy

- Parathyroid Hormone Therapy

- Others

- By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Primary Research

Mordor analysts interviewed endocrinologists, hospital pharmacists, and payor formulary managers across North America, Europe, China, and Brazil. These conversations validated dose-switch patterns (sequential anabolic to anti-resorptive), real-world adherence, and biosimilar discount curves, allowing us to refine assumed average selling prices and eligible patient pools.

Desk Research

We began with publicly available epidemiology from bodies such as WHO, IOF, and CDC, treatment-guideline adoption data from NICE and USPSTF, customs codes for denosumab and zoledronic acid accessed via UN Comtrade, and prescription volume snapshots from IQVIA's open dashboards. Company 10-Ks and investor decks helped us benchmark brand erosion after biosimilar entry, while scholarly databases (PubMed, ClinicalTrials.gov) clarified pipeline attrition rates. Paid repositories from D&B Hoovers and Dow Jones Factiva strengthened revenue cross-checks. The sources cited here illustrate the wider range we reviewed; many additional datasets informed gap filling and triangulation.

Market-Sizing & Forecasting

A top-down prevalence-to-treated cohort build-up starts with the female population aged 50+, fracture risk incidence, diagnosis and treatment penetration, then applies region-specific ASPs. Supplier roll-ups of key brands and channel checks supply a selective bottom-up lens to stress-test totals. Key variables modeled include DXA scan rates, patent expiry timing, biosimilar uptake velocity, estrogen-level linked fracture elasticity, and regional reimbursement ceilings. Multivariate regression projects these drivers through 2030, with scenario analysis around patent cliffs and guideline updates to bound uncertainty. Data gaps in bottom-up estimates are bridged using analog markets and sensitivity ranges reviewed with clinical KOLs.

Data Validation & Update Cycle

Outputs undergo variance checks against import data and historic launch curves before a two-step analyst review. We refresh each model annually; material events such as price caps or landmark trial results trigger interim revisions, ensuring clients always access the latest view.

How Mordor Intelligence's Postmenopausal Osteoporosis Market Size Compares to Other Published Estimates

Published estimates often diverge because analysts choose dissimilar patient cohorts, price bases, and refresh cadences. In this therapy area, differences in whether consumer-priced calcium combos or male osteoporosis drugs are folded in can widen gaps noticeably.

Key gap drivers include scope creep beyond postmenopausal cases, use of wholesale-to-retail mark-ups without validation, limited country coverage, and infrequent updates that miss 2025 biosimilar discounts. Mordor's disciplined scope, annual refresh, and dual validation with treated-cohort math and brand roll-ups yield a balanced baseline for decision makers.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 8.03 B (2025) | Mordor Intelligence | - |

| USD 10.9 B (2025) | Global Consultancy A | Includes perimenopausal and male osteoporosis; uses consumer retail prices |

| USD 5.18 B (2025) | Industry Journal B | Excludes several Asia-Pacific markets; relies on limited hospital sample data |

These comparisons show that when the right scope, variables, and timely data are combined, Mordor Intelligence delivers a dependable, transparent market baseline that clients can retrace and replicate with confidence.

Key Questions Answered in the Report

What is the current value of the osteoporosis drugs market?

The osteoporosis drugs market size reached USD 8.33 billion in 2026 and is projected at USD 9.97 billion by 2031.

Which drug class is growing the fastest?

RANKL inhibitors, led by denosumab and its biosimilars, are forecast to post a 5.04% CAGR through 2031.

Why are biosimilars important for osteoporosis treatment costs?

Denosumab biosimilars launched in 2025 at 20–30% price discounts, allowing payers to treat more patients within fixed budgets.

Which region offers the highest future growth?

Asia-Pacific leads with a projected 6.41% CAGR as aging populations and expanding insurance coverage raise therapy uptake.

How do injectable therapies compare with oral bisphosphonates for adherence?

Real-world studies show injectable denosumab achieves 92.5% adherence versus 63.5% for oral alendronate, supporting its preference in high-risk patients.

Page last updated on: