Male Breast Cancer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.65 Billion |

| Market Size (2031) | USD 5.63 Billion |

| Growth Rate (2026 - 2031) | 3.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Male Breast Cancer Market Analysis by Mordor Intelligence

The Male Breast Cancer Market size is expected to grow from USD 4.49 billion in 2025 to USD 4.65 billion in 2026 and is forecast to reach USD 5.63 billion by 2031 at 3.92% CAGR over 2026-2031.

Male breast cancer represented less than 1% of all breast cancer cases globally, yet absolute incidence rose from 9,777 cases in 1990 to 38,827 cases in 2021, which kept demand rising across diagnosis, surgery, radiation, drug therapy, and supportive services in the male breast cancer market. The male breast cancer market is also moving toward more standardized and biomarker-led care, as guideline updates now support routine BRCA1 and BRCA2 testing and more consistent receptor profiling in men at diagnosis. North America remained the largest contributor because reimbursement systems are mature and evidence pathways for targeted drugs are better established, while the Asia-Pacific region is expanding faster as China and other large countries convert a rising disease burden into higher treatment volumes in the male breast cancer market. Competition in the male breast cancer market remains moderate, with large drug makers holding strong positions in branded systemic therapy and a broad generics base continuing to supply much of the endocrine treatment volume in earlier-stage care.

Key Report Takeaways

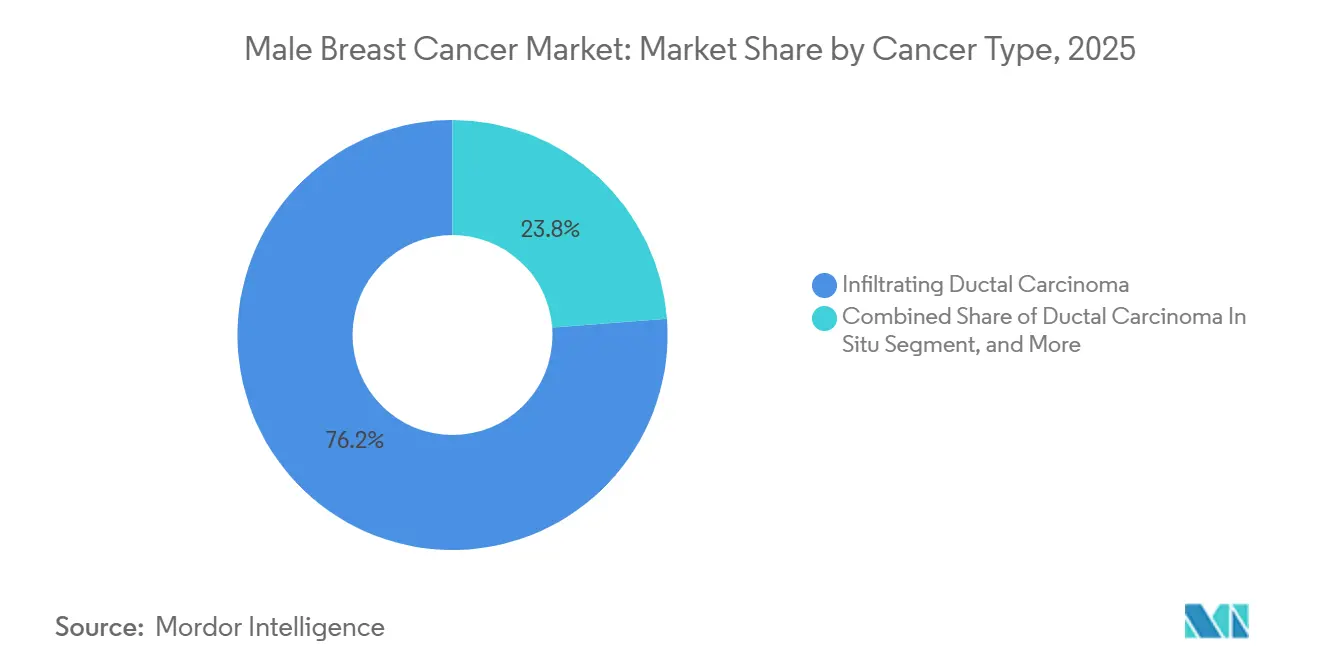

- By cancer type, infiltrating ductal carcinoma held 76.23% of the male breast cancer market share in 2025, while ductal carcinoma in situ is projected to expand at 4.48% CAGR through 2031.

- By diagnosis, imaging accounted for 38.28% share in 2025, while pathology is forecast to grow at 5.22% CAGR through 2031.

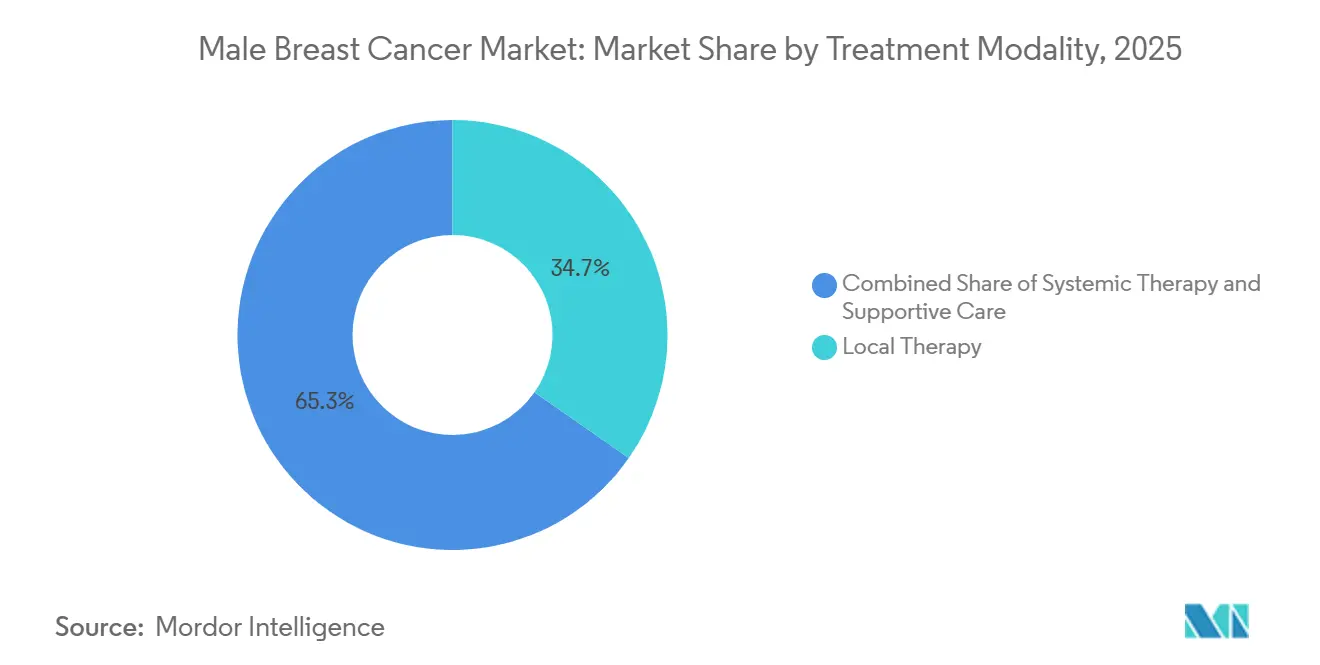

- By treatment modality, local therapy accounted for 34.68% share of the male breast cancer market size in 2025, while systemic therapy is advancing at 5.56% CAGR through 2031.

- By end user, hospitals held 56.23% share in 2025, while cancer specialty clinics are projected to record the highest CAGR at 6.19% through 2031.

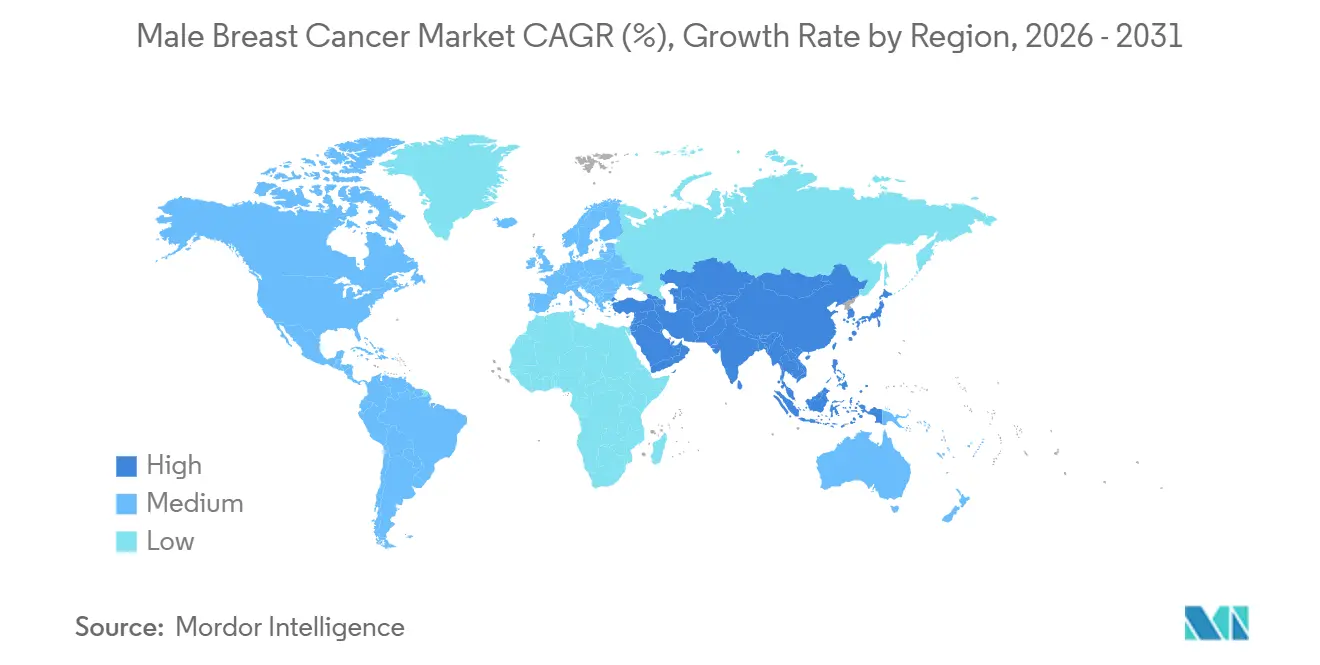

- By geography, North America held 42.39% share in 2025, while Asia-Pacific is projected to expand at 5.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Male Breast Cancer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diagnosis And Awareness | +0.8% | Global, with early gains in North America and Western Europe | Medium term (2-4 years) |

| Expansion Of CDK4/6, PARP, And HER2-Targeted Options | +1.2% | North America, Europe, and high-income Asia-Pacific | Medium term (2-4 years) |

| Wider Germline BRCA And Tumor Biomarker Testing | +0.7% | North America, Europe, Japan, South Korea, Australia | Short term (≤ 2 years) |

| Better Oncology Access In Emerging Markets | +0.6% | APAC core, with spill-over to MEA and South America | Long term (≥ 4 years) |

| Male-Inclusion Pressure In Breast Cancer Trials | +0.3% | Global, led by US and EU trial infrastructure | Long term (≥ 4 years) |

| Real-World-Evidence Label Expansion For Men | +0.4% | North America and EU, with regulatory influence from FDA and EMA-linked review pathways | Short term (≤ 2 years) to Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Diagnosis And Awareness

Male breast cancer has long been identified later than female breast cancer, and published evidence placed average diagnostic delay in men at 14 to 21 months compared with 1 to 4 months in women.[1]Shayan Raeisi Dehkordi, Samantha K. F. Kennedy, Malika Peera, et al., “Examining Stigma in Experiences of Male Breast Cancer Patients and Its Impact as a Barrier to Care: A Narrative Review,” Annals of Palliative Medicine, ovid.com That delay has direct commercial implications for the male breast cancer market because late recognition pushes patients into more resource-intensive treatment pathways after symptoms have already advanced. Clinical reports also showed that male presentation is still often triggered by self-detection rather than structured examination, which keeps imaging and biopsy demand closely tied to awareness efforts among the public and frontline physicians. As more general practitioners recognize the disease earlier, referral volumes move faster into imaging, pathology, and endocrine therapy, and that broadens demand across the male breast cancer market rather than in one care setting alone. Earlier diagnosis also changes the treatment mix over time, because patients identified before wide metastatic spread are more likely to receive longer courses of guided systemic care and monitored follow-up.

Expansion Of CDK4/6, PARP, And HER2-Targeted Options

The treatment range in the male breast cancer market has widened since real-world evidence first helped extend CDK4/6 inhibitor use to men with HR-positive, HER2-negative metastatic disease.[2]Srikavya Pasumarthy, Peggy Miller, Cheri Ambrose, Patricia Washburn, and Lopamudra Das Roy, “High Mortality in the Male Breast Cancer Community: A Report on Its Drivers and a Demand for Change in Healthcare Policy,” Cureus, pmc.ncbi.nlm.nih.gov Ribociclib then moved further into early disease after the September 2024 FDA approval for adjuvant use in high-risk early breast cancer, and that label explicitly included men in the NATALEE trial population. Real-world clinical data from Turkey also supported class performance in men, with overall response rates of 84.0% for palbociclib and 76.2% for ribociclib in first-line treatment of metastatic HR-positive, HER2-negative disease. PARP inhibitors add another growth layer because a German registry found that 12.6% of men with early breast cancer met adjuvant olaparib eligibility criteria under the OlympiA framework, which is meaningful in a rare-disease setting. New approvals, such as inavolisib in October 2024 and datopotamab deruxtecan in January 2025, show that the male breast cancer market is gradually gaining access to the same targeted treatment architecture that already shapes female breast cancer care.

Wider Germline BRCA And Tumor Biomarker Testing

The 2024 ASCO and Society of Surgical Oncology guideline update changed the testing baseline in the male breast cancer market by recommending BRCA1 and BRCA2 testing for all men newly diagnosed with breast cancer, regardless of age or stage.[3]Isabelle Bedrosian, Mark R. Somerfield, Maria Isabel Achatz, et al., “Germline Testing in Patients With Breast Cancer: ASCO-Society of Surgical Oncology Guideline,” Journal of Clinical Oncology, ascopubs.org That recommendation is commercially important because pathogenic BRCA2 variants were reported in 11% of male patients undergoing multigene panel testing, which makes male diagnosis more likely to produce actionable germline findings than many routine female pathways. Canada reinforced the same direction in 2025 through recommendations that called for multigene next-generation sequencing panels and identified men as a distinct high-priority testing group. Tumor profiling is also becoming more relevant as targeted therapy choices increasingly depend on PIK3CA and related pathway information, which is reflected in the ongoing MALPELO study for male patients with PIK3CA-mutant advanced disease. The January 2026 CMS reimbursement decision for Illumina’s TruSight Oncology Comprehensive panel at USD 2,989.6 per test further lowers access barriers and helps move comprehensive profiling closer to routine practice in the U.S. segment of the male breast cancer market.

Better Oncology Access In Emerging Markets

Emerging markets are becoming more important to the male breast cancer market because disease burden is rising faster in several Asian countries than in many mature systems. China recorded 16,956 new male breast cancer cases in 2021, and its age-standardized incidence rate rose at an estimated annual percentage change of 6.2 since 1990, which points to a much larger treatment base than in earlier decades. India is also projected to see further increases in both incidence and mortality through 2036, which supports the case for wider diagnostic access and broader generic therapy distribution. Japan already has a stronger structural base because national health insurance covers BRCA1 and BRCA2 germline testing for male patients, and the Japanese Breast Cancer Society includes male disease within its patient guidance. These shifts do not remove access gaps in lower-income settings, but they steadily widen the addressable patient pool for imaging, pathology, and endocrine treatment across the male breast cancer market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tiny Patient Pool Constrains Trials And ROI | -0.5% | Global, most pronounced in MEA and South America | Long term (≥ 4 years) |

| Stigma And Low Clinical Suspicion Delay Diagnosis | -0.4% | Global, accentuated in Asia and MEA | Medium term (2-4 years) |

| Tamoxifen Side Effects And Poor Adherence | -0.3% | Global, particularly North America and Europe | Short term (≤ 2 years) to Medium term (2-4 years) |

| Women-Centric Reimbursement And Evidence Pathways | -0.3% | North America and EU, with compliance factors tied to health technology assessment bodies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tiny Patient Pool Constrains Trials And ROI

The rare nature of the disease remains a structural drag on the male breast cancer market because the United States is expected to record only 2,670 new male cases in 2026, compared with 316,950 female cases. That gap makes male-only interventional trials difficult to recruit, and weak recruitment then limits the amount of sex-specific evidence available for regulators, payers, and guideline writers. A German registry analysis showed how wide that gap remains, since men represented only 0.3% to 0.6% of participants in major adjuvant trials even though 12.6% to 47.6% of men in the registry would have met trial eligibility criteria. This keeps the male breast cancer market dependent on extrapolated female data and real-world evidence rather than direct male Phase III programs, which can slow reimbursement decisions for newer drugs. The same limitation is especially relevant for PARP inhibitors, next-generation endocrine agents, and newer combination approaches, where male-specific outcome evidence is still limited as of 2026.

Stigma And Low Clinical Suspicion Delay Diagnosis

Social stigma still limits how quickly men enter the male breast cancer market because many patients delay reporting symptoms when breast cancer is viewed as a female disease. A narrative review also found that 64.2% of male patients reported moderate-to-high embarrassment during symptom presentation, which helps explain why diagnosis often occurs later than it should. Low suspicion among clinicians adds a second barrier, and registry evidence from Austria showed that men received adjuvant chemotherapy, radiotherapy, and hormonal therapy less often than stage-matched women despite comparable tumor biology. That under-treatment reduces utilization per patient and limits how fully the male breast cancer market can convert clinical need into actual spending. Progress will depend on both public awareness and stronger training for frontline physicians, because they remain the first gateway to referral, biopsy, and treatment initiation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cancer Type: Ductal Dominance Shapes Revenue While Earlier Detection Supports Pre-Invasive Growth

Infiltrating ductal carcinoma accounted for 76.23% share in 2025, which made it the central revenue base for the male breast cancer market by cancer type. That concentration is consistent with broader clinical literature showing that infiltrating ductal tumors make up most male breast cancer cases and are usually estrogen receptor positive. Because this subtype is usually hormone-driven, the care pattern in the male breast cancer market stays closely tied to endocrine therapy, CDK4/6 inhibitors, and long follow-up periods rather than to chemotherapy alone. The dominance of ductal disease also makes pathology and receptor testing more important, because treatment selection depends on defining ER, PR, and HER2 status clearly at diagnosis. Rare subtypes such as inflammatory breast cancer and Paget disease represent small revenue pools, but they still create high-intensity treatment episodes because they often present with more aggressive clinical behavior.

Ductal carcinoma in situ is forecast to expand at 4.48% CAGR through 2031, making it the fastest-growing cancer type within the male breast cancer market. The key reason is that wider germline testing and surveillance in BRCA carriers are increasing the chance of detection before invasive transformation. This earlier-stage mix supports more imaging, biopsy, and planned surgery, and it gradually shifts part of the male breast cancer industry toward controlled early intervention rather than late-stage rescue treatment. Invasive lobular carcinoma remains uncommon in men because lobular tissue is sparse in normal male breast anatomy, so its commercial weight stays limited in the male breast cancer market. Even so, these less common forms still matter clinically because they broaden the need for specialized pathology review and hormone-focused management in selected patients.

By Diagnosis: Imaging Holds Present Volume While Pathology Builds Future Value

Imaging captured 38.28% of the diagnosis segment in 2025, which gave it the largest position within diagnostic spending in the male breast cancer market. In practice, mammography and ultrasound remain the main first-line tools, and U.S. surgical oncology guidance supports ultrasound first for men under 25 with indeterminate palpable masses and mammography for men aged 25 or older. That structure keeps imaging volume steady because most patients still present after noticing a lump or local change rather than through organized screening. PET and MRI occupy smaller positions, but they remain important for staging and treatment response assessment in advanced disease, especially when clinicians need a broader disease map. As awareness improves, imaging demand in the male breast cancer industry will continue to be supported by earlier referral rather than only by metastatic workup.

Pathology is the fastest-growing diagnostic category at 5.22% CAGR through 2031, reflecting the move toward biomarker-led decisions across the male breast cancer market. Receptor profiling for ER, PR, and HER2 is now fundamental to therapy choice, and germline BRCA testing has also shifted from selective use to a standard recommendation for newly diagnosed men. Companion diagnostics are also deepening revenue per patient episode, as shown by the approval of FoundationOne Liquid CDx alongside inavolisib for PIK3CA mutation detection. The January 2026 CMS decision on TruSight Oncology Comprehensive gave the male breast cancer market another push by making broader genomic profiling more accessible to Medicare beneficiaries. Over time, this means more of the value in diagnosis will come from interpretation and molecular stratification rather than from imaging alone.

By Treatment Modality: Surgery Keeps the Largest Base While Systemic Therapy Expands Faster

Local therapy held 34.68% share in 2025 and remained the largest treatment category in the male breast cancer market because mastectomy is still the standard surgical approach for many men. The basic reason is anatomical, since limited male breast tissue often makes breast-conserving surgery less practical than in women. Sentinel lymph node biopsy has improved the quality of local management by giving clinically node-negative men a less morbid staging option when compared with routine full axillary dissection. Radiation also remains relevant after surgery in selected higher-risk cases, which keeps local therapy broader than surgery alone within the male breast cancer industry. This part of the male breast cancer market remains stable because every diagnosed patient moves through local control decisions, even when later treatment differs by biomarker profile.

Systemic therapy is projected to grow at 5.56% CAGR through 2031, which makes it the fastest-moving treatment segment in the male breast cancer market. The growth driver is not one product. It is the steady build-out of endocrine backbones, CDK4/6 inhibitors, PARP candidates, PI3K-pathway drugs, oral SERDs, and HER2-directed options. The ETHAN Phase II study is especially important because it is one of the few prospective endocrine comparisons designed specifically for men, which could sharpen treatment sequencing over time. Treatment nuance also matters in men, since aromatase inhibitors require concurrent gonadal suppression to avoid inferior outcomes, and that makes specialist oversight more valuable in the male breast cancer market. As this complexity rises, revenue growth shifts steadily toward drug classes that depend on molecular selection and longitudinal management rather than on one-time intervention.

By End User: Hospitals Remain the Core Channel While Specialty Clinics Gain Share

Hospitals captured 56.23% share in 2025, which kept them at the center of service delivery across the male breast cancer market. That lead reflects their role in surgery, pathology coordination, inpatient chemotherapy, imaging access, and multidisciplinary decision-making for newly diagnosed patients. Hospitals also act as the main referral destination when men present with delayed or advanced disease, which remains common in many health systems. Academic and research centers overlap with this hospital base because they host many male-inclusive studies and see a larger share of complex metastatic cases. For that reason, institutional care continues to anchor the male breast cancer industry even as outpatient oncology models expand.

Cancer specialty clinics are projected to grow at 6.19% CAGR through 2031, which makes them the fastest-growing end-user category in the male breast cancer market. Their advantage is clinical focus, because biomarker-led treatment selection, genetic counseling, endocrine toxicity management, and targeted therapy monitoring are easier to coordinate in dedicated oncology settings. A German claims analysis showed that 59% of adjuvant endocrine therapy prescriptions for male patients came from general practitioners, which highlights a governance gap that specialty clinics are better placed to address. Ambulatory surgical centers are also gaining a modest role in outpatient procedures such as sentinel node biopsy and diagnostic workup, although they remain smaller than hospital and specialty oncology channels. The result is a channel mix in the male breast cancer market that still starts in hospitals but is gradually moving more toward ongoing management and specialized outpatient oncology care.

Geography Analysis

North America accounted for 42.39% share of the male breast cancer market size in 2025, which kept it in the lead among all regions. The region’s strength comes from established oncology infrastructure, broad reimbursement for advanced therapies, and a stronger real-world evidence ecosystem that supports male use even when randomized male-only data remain limited. The 2024 ASCO and Society of Surgical Oncology update on universal germline testing for men with breast cancer also supports more consistent biomarker identification and downstream treatment use in the U.S. segment of the male breast cancer market. Real-world evidence from the POLARIS study further strengthened this base, with male patients treated with palbociclib showing a median real-world progression-free survival of 19.8 months. Canada adds to the region’s depth through aligned germline testing recommendations and regulatory support for ribociclib in male patients, which keeps North America the most developed regional cluster in the male breast cancer market.

Europe remained the second-largest regional grouping in the male breast cancer market, led by Germany, France, the United Kingdom, and Italy. The region gained an important boost when ribociclib was approved in Europe for adjuvant early breast cancer after a trial program that explicitly included men, which improved the credibility of male access in earlier-stage disease. Germany’s registry data also showed that 47.6% of men with early breast cancer met ribociclib eligibility criteria under NATALEE, which points to sizable untreated or undertreated opportunity within the regional male breast cancer market. Even with this progress, Europe still faces a translation gap between trial eligibility and routine uptake, which means growth depends as much on implementation discipline as on new approvals.

Asia-Pacific is projected to grow at 5.87% CAGR through 2031, making it the fastest-expanding regional block in the male breast cancer market. China is the main driver because it recorded 16,956 new male cases in 2021 and has seen incidence rise much faster than the global average over the last 3 decades. East Asia also has a reported HER2 positivity rate of 17% in male breast cancer, which is materially higher than the 8% level reported for Europe and the United States, and that creates stronger regional demand for HER2-directed therapy. Japan supports uptake through national insurance coverage for BRCA1 and BRCA2 germline testing and through clinical guidance that includes male disease in practice frameworks. Middle East and Africa as well as South America are smaller today, but they remain part of the longer runway for the male breast cancer market as GCC infrastructure investment, awareness programs, and insurance expansion gradually improve diagnosis and treatment access despite persistent late-stage presentation in several lower-resource settings.

Competitive Landscape

The male breast cancer market is moderately consolidated in branded systemic therapy, but it is much less concentrated when diagnosis, surgery, radiation, supportive care, and generic endocrine drugs are included in the full value chain. Pfizer and Novartis remain the clearest branded leaders in CDK4/6-based treatment for men because palbociclib and ribociclib both have established regulatory pathways that explicitly support male use in major Western markets. Eli Lilly also remains highly relevant as abemaciclib continues to post large global breast cancer sales, and the company strengthened its position again with the September 2025 approval of imlunestrant for ESR1-mutated advanced disease after a trial that included male participants. AstraZeneca and Daiichi Sankyo remain strong in HER2-directed care because Enhertu continued to expand clinically and commercially, supported by Phase III data showing a 53.0% reduction in the risk of disease recurrence or death versus T-DM1 in high-risk HER2-positive early breast cancer. The result is a male breast cancer market where the branded therapy race is active, but no single company controls the broader care pathway across all service categories.

Competition is also moving toward next-generation endocrine and pathway-directed therapies in the male breast cancer market. Lilly’s approval of imlunestrant in 2025, AstraZeneca’s positive SERENA-6 readout for camizestrant in 2025, and Genentech’s 2024 inavolisib approval all show that the market is widening beyond first-generation endocrine combinations. Pfizer also signaled class defense in March 2026 with positive topline Phase II data for atirmociclib, a selective CDK4 inhibitor being advanced after prior CDK4/6 therapy. These moves matter because the male breast cancer market has limited room for male-only blockbuster franchises, so companies compete by extending broader breast cancer platforms into male care rather than building isolated male portfolios.

Diagnostics is another active front in the male breast cancer market, even though it is less visible than drug competition. Illumina strengthened its position in January 2026 when CMS reimbursement for TruSight Oncology Comprehensive improved the commercial case for broad genomic profiling in routine oncology workups. GE HealthCare also took a visible step in April 2026 by expanding its collaboration with RadNet’s DeepHealth to widen access to AI-powered screening workflows that showed a 21.0% improvement in detection in a U.S. real-world analysis. Together, these developments show that the male breast cancer market is being shaped not only by drug launches, but also by better molecular testing and smarter imaging infrastructure that influence who gets diagnosed, stratified, and treated earlier.

Male Breast Cancer Industry Leaders

Bristol Myers Squibb Company

Eli Lilly and Company

Merck & Co., Inc.

Novartis AG

Sanofi S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: GE HealthCare expanded its mammography collaboration with RadNet's DeepHealth subsidiary to extend global access to AI-powered breast cancer screening, with a real-world US analysis showing a 21% increase in detection rates using DeepHealth's Breast Suite, this expansion directly enhances detection capacity for male breast cancer in high-volume imaging centers worldwide.

- March 2026: Pfizer announced positive topline Phase 2 results for atirmociclib, an investigational selective CDK4 inhibitor, in the FOURLIGHT-1 study, showing a 40% reduction in risk of disease progression or death in HR-positive, HER2-negative advanced breast cancer after prior CDK4/6 inhibitor therapy, the drug targets patients including males, and Pfizer is advancing a Phase 3 registrational study in first-line metastatic disease.

- January 2026: Illumina secured CMS reimbursement for its FDA-approved TruSight Oncology Comprehensive NGS panel, effective January 1, 2026, at USD 2,989.55 per test under the Clinical Laboratory Fee Schedule, this expands access to comprehensive genomic profiling for male breast cancer patients within the US Medicare population, supporting BRCA and PIK3CA-guided treatment decisions.

- October 2025: AstraZeneca and Daiichi Sankyo reported that Enhertu reduced the risk of disease recurrence or death by 53% versus T-DM1 in high-risk HER2-positive early breast cancer in the DESTINY-Breast05 Phase III trial, 3-year IDFS was 92.4% versus 83.7%, supporting potential standard-of-care replacement for T-DM1 in post-neoadjuvant settings applicable to male HER2-positive patients.

Global Male Breast Cancer Market Report Scope

The Male Breast Cancer Market refers to the global economic sector comprising the drugs, medical devices, diagnostics, and therapeutic services used to prevent, identify, and treat breast cancer in men.

The Male Breast Cancer Market is Segmented by Cancer Type (Infiltrating Ductal, DCIS, Paget Disease, Inflammatory, Invasive Lobular), Diagnosis (Imaging, Pathology, Biomarker and Genetic Testing), Treatment Modality (Local Therapy, Systemic Therapy, Supportive Care), End User (Hospitals, Specialty Clinics, Academic Centers, ASCs), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Forecasts are in Value (USD).

| Infiltrating Ductal Carcinoma |

| Ductal Carcinoma In Situ |

| Paget Disease of the Nipple |

| Inflammatory Breast Cancer |

| Invasive Lobular Carcinoma |

| Imaging | Mammography |

| Ultrasound | |

| Magnetic Resonance Imaging | |

| Computed Tomography | |

| Positron Emission Tomography | |

| Pathology | Core Needle Biopsy |

| Fine Needle Aspiration Biopsy | |

| Excisional Biopsy | |

| Biomarker and Genetic Testing | Estrogen Receptor / Progesterone Receptor Testing |

| HER2 Testing | |

| Germline BRCA and Hereditary Cancer Panel Testing | |

| Tumor Genomic Profiling |

| Local Therapy | Surgery | Mastectomy |

| Breast-Conserving Surgery | ||

| Sentinel Lymph Node Biopsy | ||

| Axillary Lymph Node Dissection | ||

| Radiation Therapy | ||

| Systemic Therapy | Endocrine Therapy | Tamoxifen |

| Aromatase Inhibitor Plus GnRH Analogue | ||

| Fulvestrant | ||

| Chemotherapy | Neoadjuvant Chemotherapy | |

| Adjuvant Chemotherapy | ||

| Metastatic-Line Chemotherapy | ||

| Targeted Therapy | CDK4/6 Inhibitors | |

| HER2-Targeted Therapy | ||

| PARP Inhibitors | ||

| PI3K / AKT / mTOR-Pathway Therapies | ||

| Immunotherapy | ||

| Supportive Care | ||

| Hospitals |

| Cancer Specialty Clinics |

| Academic and Research Centers |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Cancer Type | Infiltrating Ductal Carcinoma | ||

| Ductal Carcinoma In Situ | |||

| Paget Disease of the Nipple | |||

| Inflammatory Breast Cancer | |||

| Invasive Lobular Carcinoma | |||

| By Diagnosis | Imaging | Mammography | |

| Ultrasound | |||

| Magnetic Resonance Imaging | |||

| Computed Tomography | |||

| Positron Emission Tomography | |||

| Pathology | Core Needle Biopsy | ||

| Fine Needle Aspiration Biopsy | |||

| Excisional Biopsy | |||

| Biomarker and Genetic Testing | Estrogen Receptor / Progesterone Receptor Testing | ||

| HER2 Testing | |||

| Germline BRCA and Hereditary Cancer Panel Testing | |||

| Tumor Genomic Profiling | |||

| By Treatment Modality | Local Therapy | Surgery | Mastectomy |

| Breast-Conserving Surgery | |||

| Sentinel Lymph Node Biopsy | |||

| Axillary Lymph Node Dissection | |||

| Radiation Therapy | |||

| Systemic Therapy | Endocrine Therapy | Tamoxifen | |

| Aromatase Inhibitor Plus GnRH Analogue | |||

| Fulvestrant | |||

| Chemotherapy | Neoadjuvant Chemotherapy | ||

| Adjuvant Chemotherapy | |||

| Metastatic-Line Chemotherapy | |||

| Targeted Therapy | CDK4/6 Inhibitors | ||

| HER2-Targeted Therapy | |||

| PARP Inhibitors | |||

| PI3K / AKT / mTOR-Pathway Therapies | |||

| Immunotherapy | |||

| Supportive Care | |||

| By End User | Hospitals | ||

| Cancer Specialty Clinics | |||

| Academic and Research Centers | |||

| Ambulatory Surgical Centers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East & Africa | GCC | ||

| South Africa | |||

| Rest of Middle East & Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the expected value of male breast cancer by 2031?

The male breast cancer market is projected to reach USD 5.63 billion by 2031, up from USD 4.65 billion in 2026, at a CAGR of 3.92%.

Which region leads revenue today?

North America led with 42.39% share in 2025 because reimbursement systems, targeted therapy access, and biomarker testing pathways are more established there.

Which region is growing the fastest?

Asia-Pacific is forecast to grow at 5.87% CAGR through 2031, supported by rising incidence in China and improving oncology infrastructure across major Asian countries.

Which cancer type drives the largest portion of spending?

Infiltrating ductal carcinoma held 76.23% share in 2025, which reflects its dominant clinical prevalence among male patients and its heavy dependence on long-course endocrine and targeted therapy.

Why is pathology growing faster than imaging?

Pathology is projected to grow at 5.22% CAGR because treatment selection now depends more on receptor profiling, BRCA testing, and genomic assays that guide targeted therapy use.

Page last updated on: