United States Dermatological Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

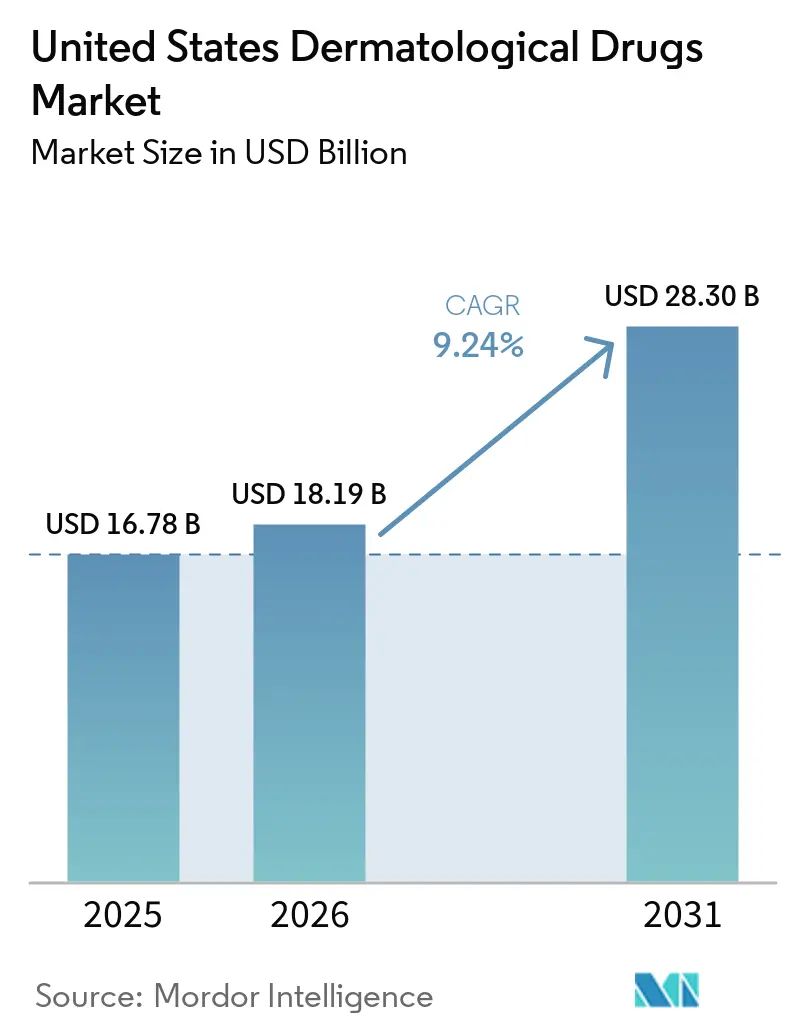

| Base Year Market Size (2025) | USD 16.78 Billion |

| Market Size (2026) | USD 18.19 Billion |

| Market Size (2031) | USD 28.30 Billion |

| Growth Rate (2026 - 2031) | 9.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dermatological Drugs Market Analysis by Mordor Intelligence

The United States Dermatological Drugs Market size is expected to grow from USD 16.78 billion in 2025 to USD 18.19 billion in 2026 and is forecast to reach USD 28.30 billion by 2031 at 9.24% CAGR over 2026-2031.

Medicare Part D redesign is improving affordability for high-cost specialty therapies from 2025 onward, and the USD 2,000 out-of-pocket cap is helping more patients move from prescription approval to actual treatment use in the United States dermatological drugs market. Growth is also being supported by a durable consumer care layer, with over-the-counter products rising faster than prescription products and creating a wider revenue base beyond specialist biologics. Psoriasis remains the largest revenue pool, while hidradenitis suppurativa is expanding faster because new therapies are entering an area that still has a large untreated population, which gives the United States dermatological drugs market two very different growth engines at the same time. Topical products still anchor volume because acne, eczema, and mild psoriasis are often managed without systemic therapy, but oral and injectable innovation is changing brand competition by giving companies more ways to differentiate treatment choice. Distribution is also shifting, as retail pharmacy remains the leading channel while online fulfillment accelerates, and large manufacturers are already responding to access pressure with direct pricing and patient access strategies such as Novartis’s discounted Cosentyx platform.

Key Report Takeaways

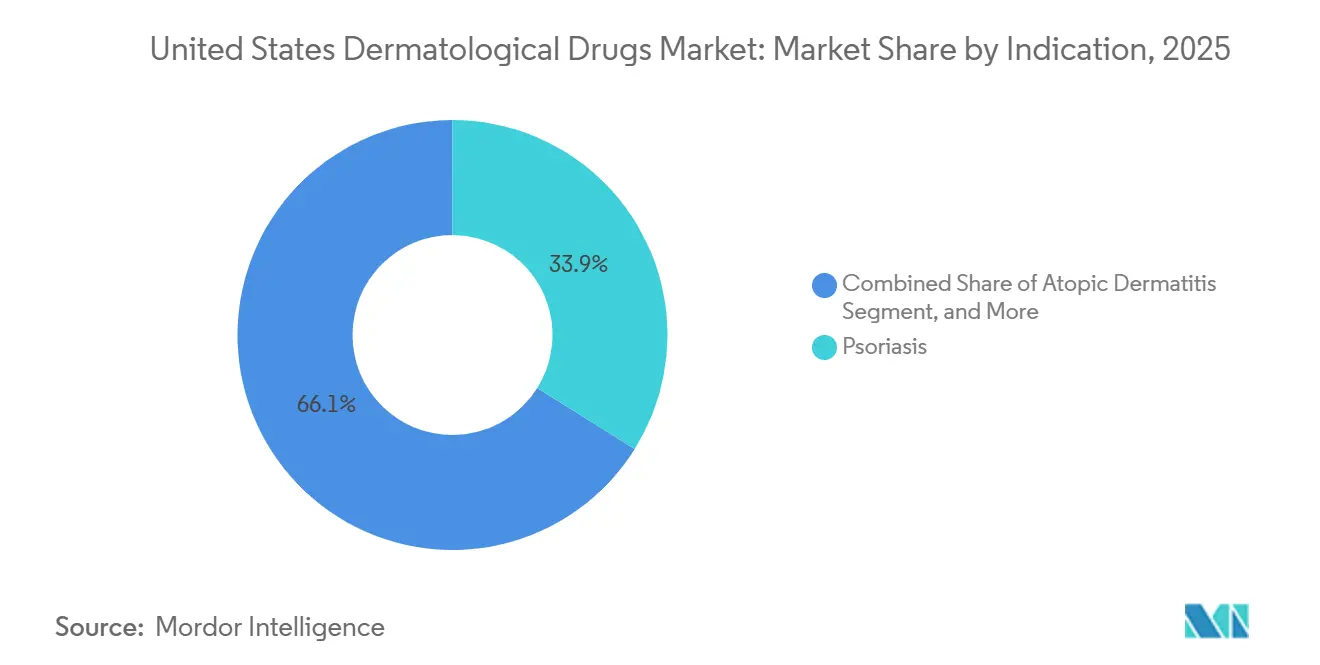

- By indication, psoriasis held 33.87% share in 2025, while hidradenitis suppurativa is forecast to expand at 9.97% CAGR through 2031.

- By prescription status, prescription products held 73.42% share in 2025, while OTC products are projected to grow at 10.06% CAGR through 2031.

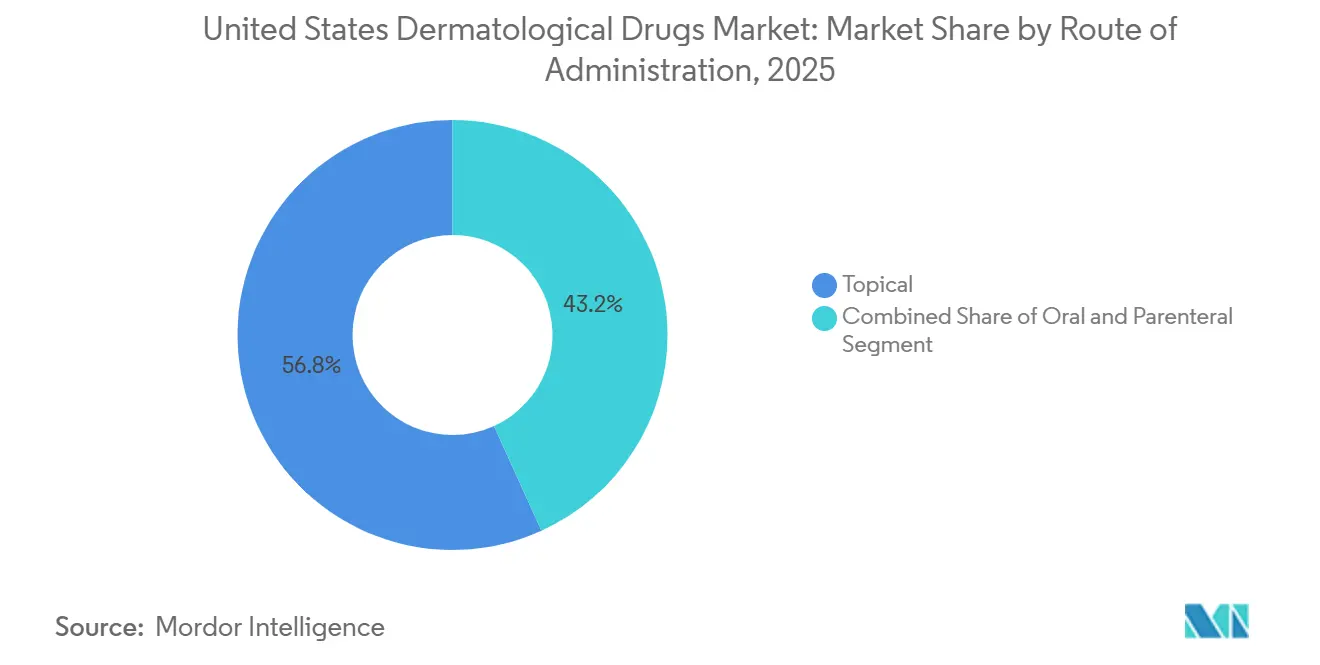

- By route of administration, topical products accounted for 56.81% share in 2025, while parenteral products are projected to rise at 9.44% CAGR through 2031.

- By drug class, corticosteroids led with 26.74% share in 2025, while PDE-4 inhibitors are expected to grow at 11.13% CAGR through 2031.

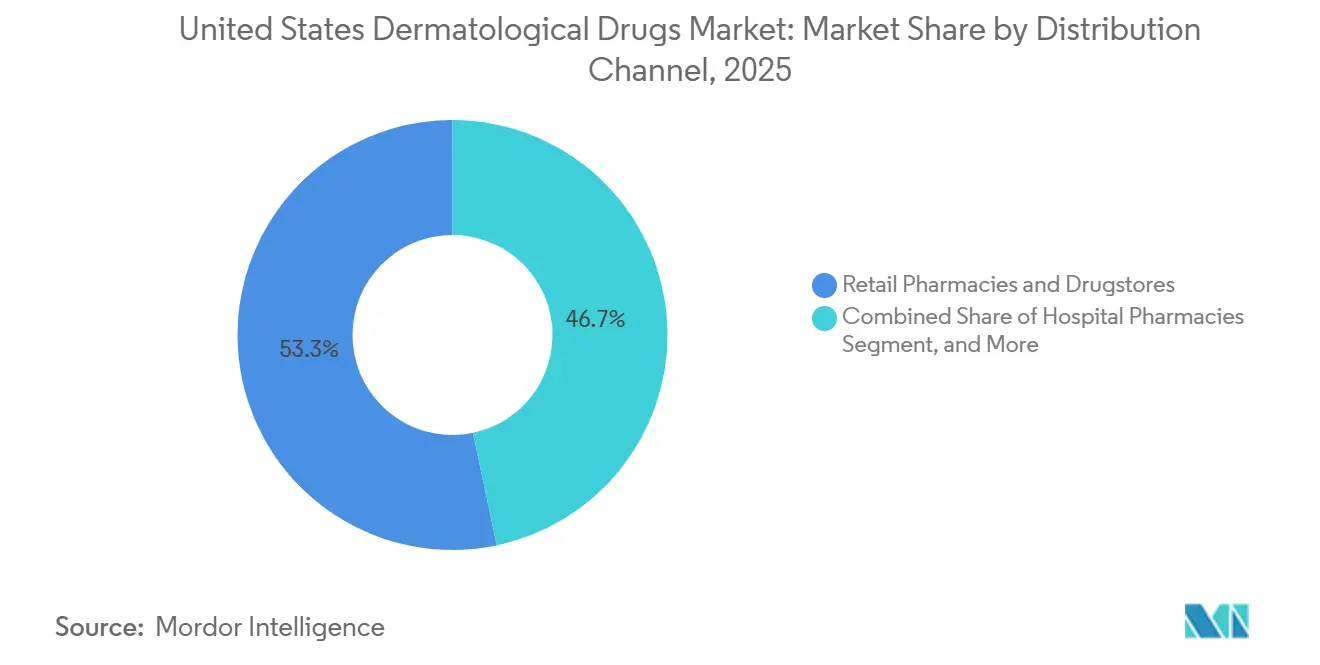

- By distribution channel, retail pharmacies and drugstores held 53.27% share in 2025, while online pharmacies are projected to expand at 10.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Dermatological Drugs Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Biologic Uptake In Psoriasis | +2.3% | National, concentrated in Northeast and West Coast specialty centers | Medium term (2-4 years) |

| Expanding Moderate-To-Severe Atopic Dermatitis Treatment Pool | +2.0% | National, with higher pediatric uptake in Sun Belt and suburban markets | Medium term (2-4 years) |

| Strong FDA Approval Cadence In Medical Dermatology | +1.4% | National | Short term (≤ 2 years) |

| Persistent Acne Burden Sustaining Rx And OTC Demand | +1.1% | National | Short term (≤ 2 years) |

| Teledermatology And Digital Pharmacy Integration Accelerating Conversion | +0.8% | National, with spillover to underserved rural states | Medium term (2-4 years) |

| Medicare Part D Redesign Improving Specialty-Drug Affordability | +0.7% | National, with early gains in high-Medicare-enrollment states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Biologic Uptake in Psoriasis

Psoriasis remains the main specialty revenue engine in the United States dermatological drugs market because biologic therapy has moved treatment expectations closer to high skin-clearance outcomes rather than partial disease control. AbbVie reported Skyrizi global revenue of USD 17.6 billion in 2025, which shows how large the commercial psoriasis pool has become for leading immune therapies.[1]AbbVie Inc., “AbbVie Reports Full-Year and Fourth-Quarter 2025 Financial Results,” AbbVie Investor Relations, abbvie.com Johnson & Johnson also received FDA approval in March 2026 for Icotyde, described as the first oral IL-23R antagonist for plaque psoriasis in adults and adolescents, which adds a meaningful non-injectable option to a class that had been led by subcutaneous biologics. That shift matters because prescribing competition is starting to depend less on basic efficacy differences and more on dosing convenience, patient preference, and whether a brand can hold patients through switching cycles. As penetration matures, the United States dermatological drugs market is likely to see more value migrate through brand switching and line extension rather than through first-time diagnosis alone.

Expanding Moderate-To-Severe Atopic Dermatitis Treatment Pool

Atopic dermatitis has become one of the most important specialty segments in the United States dermatological drugs market because treatment now spans biologics, oral immunomodulators, and newer non-steroidal topicals. Dupixent generated USD 17.8 billion in global net sales in 2025, and Regeneron reported more than 1.4 million patients on treatment globally with first-quarter 2026 sales of USD 4.9 billion, which shows how large and durable this treatment base has become.[2]Regeneron Pharmaceuticals, “2025 Annual Report,” Regeneron Investor Relations, regeneron.com Sanofi also reported positive Phase 3 data in March 2026 for amlitelimab across the COAST 1, COAST 2, and SHORE trials, which adds another late-stage biologic candidate for moderate-to-severe disease. The category is therefore widening at both ends, with severe disease pulling in high-value specialty biologics and milder disease moving toward more durable non-steroidal topical management. This broader treatment ladder is helping the United States dermatological drugs market expand without depending on a single mechanism or one patient severity band.

Strong FDA Approval Cadence in Medical Dermatology

The United States dermatological drugs market continues to benefit from a steady pace of regulatory activity, which keeps the country at the center of dermatology product innovation. FDA records show that novel dermatology-related approvals in 2025 included delgocitinib cream, and the agency noted that the total number of approved JAK inhibitors had risen to 12, which signals that immune pathway expansion is continuing beyond older inflammatory categories.[3]U.S. Food and Drug Administration, “Novel Drug Approvals for 2025,” FDA Center for Drug Evaluation and Research, fda.gov That pace carried into 2026 through additional label and product advances, such as Icotyde in plaque psoriasis and Cosentyx in pediatric hidradenitis suppurativa. Companies are also using the same development engines to widen brands into adjacent and rare skin diseases, as shown by Dupixent approvals in bullous pemphigoid and chronic spontaneous urticaria during 2025. This pattern supports longer product life cycles and gives the United States dermatological drugs market more revenue depth without requiring every growth step to come from a brand-new launch.

Persistent Acne Burden Sustaining Rx and OTC Demand

Acne remains one of the largest volume categories in the United States dermatological drugs market because it affects both adolescents and adults and is usually managed with high-frequency topical use. That large patient base supports recurring demand for retinoids, antibiotics, washes, and other topical regimens even when investor attention is centered on specialty biologics. It also creates a stable revenue floor for both prescription and OTC products, which is why topical categories continue to matter even as new immune therapies gain share. Recent category movement toward self-care and retail access is reinforcing this pattern, because many mild cases can be managed without escalation into specialist therapy. As a result, acne helps the United States dermatological drugs market keep broad consumer participation while specialty indications drive higher-value prescription growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Biologic Prices And Prior-Authorization Friction | -1.6% | National, amplified in states with restrictive Medicaid prior authorization rules | Medium term (2-4 years) |

| Biosimilar Interchangeability And PBM Switching Friction | -1.2% | National, most acute for ustekinumab and adalimumab biosimilar markets | Short term (≤ 2 years) |

| JAK Safety Monitoring And Label-Related Caution | -0.9% | National | Long term (≥ 4 years) |

| Dermatologist Workforce Maldistribution | -0.7% | Non-metropolitan and rural regions, with the South and Midwest most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Biologic Prices and Prior-Authorization Friction

Access barriers remain a major brake on the United States dermatological drugs market, even when clinical demand is strong. A JAMA Dermatology analysis available through PMC found that 87% of biologic prescriptions required prior authorization and that a typical dermatology practice faced an average monthly administrative cost of USD 3,454 from this process. That burden means treatment delays are often driven by paperwork and payer review rather than by physician reluctance or lack of patient need. It also pushes practices to spend time on access management that could otherwise support faster initiation or follow-up care. Even with reimbursement reform moving in a favorable direction, prior authorization keeps slowing real conversion in the United States dermatological drugs market.

Biosimilar Interchangeability and PBM Switching Friction

Biosimilar competition is increasing pricing pressure in the United States dermatological drugs market, especially for mature biologic brands nearing or crossing exclusivity thresholds. The core issue is that formulary strategy can change revenue timing very quickly once a payer or pharmacy benefit manager has more substitution leverage. Novartis signaled this pressure in November 2025 when it launched a direct-to-patient Cosentyx platform at a 55% reduction from list price for uninsured and underinsured patients, which showed that manufacturers are willing to bypass parts of the traditional channel to protect unit demand. That kind of response suggests price defense and channel control are becoming just as important as clinical positioning. For the United States dermatological drugs market, the main risk is not lower clinical need, it is faster commercial resetting of brand economics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Indication: Psoriasis Leads, HS Pipeline Reshapes Treatment Priorities

Psoriasis held 33.87% of United States dermatological drugs market share in 2025, which kept it as the largest therapeutic revenue pool in this report. That lead reflects strong biologic penetration and high annual treatment value in moderate-to-severe disease. AbbVie’s Skyrizi posted USD 17.6 billion in global revenue in 2025, which shows how much scale psoriasis-targeted biologics can reach once they become embedded in specialist practice. March 2026 also brought FDA approval for Icotyde as the first oral IL-23R antagonist for plaque psoriasis, adding a non-injectable systemic option that may widen reach among patients reluctant to use injectable therapy. Atopic dermatitis remained the second-largest indication, supported by the continued scale of Dupixent and by a broader pipeline that is widening treatment choice in the United States dermatological drugs industry.

Hidradenitis suppurativa is the fastest-growing indication, with projected growth of 9.97% through 2031, and it stands out because class expansion is starting from a lower commercial base. UCB received FDA approval in November 2024 for Bimzelx in adults with moderate-to-severe hidradenitis suppurativa, introducing the first dual IL-17A and IL-17F inhibitor for the condition, and UCB reported 2025 net sales of EUR 2.2 billion, equivalent to USD 2.4 billion, for the product. Novartis then expanded the treatment pool further in March 2026 with FDA approval of Cosentyx for pediatric patients aged 12 and older with moderate-to-severe hidradenitis suppurativa. Rosacea and fungal skin infections continue to rely more on affordable topical therapy and stable volume, while alopecia areata has become more visible after the arrival of FDA-approved JAK options. The broader “other” group is also gaining relevance, because Dupixent added dermatology-adjacent approvals in chronic spontaneous urticaria and bullous pemphigoid during 2025.

By Prescription Status: OTC Momentum Challenges Rx Dominance

Prescription products accounted for 73.42% of 2025 revenue, which shows how much value is still concentrated in branded specialty therapies and prescription topicals. This part of the United States dermatological drugs market is led by psoriasis, atopic dermatitis, and hidradenitis suppurativa treatments that require specialist evaluation, payer review, or continued clinical monitoring. Prescription demand is also sustained by route complexity, since injectable biologics and monitored oral agents cannot be replaced by self-care in moderate-to-severe disease. Even so, the revenue mix is beginning to shift because OTC products are forecast to grow at 10.06% CAGR through 2031, which is faster than the prescription tier. That faster pace suggests the United States dermatological drugs market is widening through consumer-directed management rather than relying only on high-cost prescription escalation.

The OTC side benefits from several forces moving at the same time, including stronger consumer skincare awareness, easier digital consultation, and better retail and online availability. These factors matter most in acne, mild eczema, and other lower-complexity conditions where patients often start treatment before entering specialist care. Telehealth and digital pharmacy tools also support this shift, because patients can move from symptom review to product recommendation and purchase more quickly than in a traditional office-led pathway. From a payer perspective, OTC migration can reduce reimbursement pressure in categories where outcomes do not always require a covered prescription. The result is a more layered United States dermatological drugs industry, where prescription products keep revenue leadership, but OTC products continue to pull share through convenience and access.

By Route of Administration: Topical Franchise Stable as Injectables Advance

Topical formulations represented 56.81% share of the United States dermatological drugs market size in 2025, which shows the durability of non-systemic treatment across acne, mild psoriasis, and mild-to-moderate eczema. This large base is supported by disease prevalence and by the fact that many patients can be managed without systemic therapy for long periods. It also reflects how broad the topical category has become, since innovation now extends beyond older corticosteroids into non-steroidal creams and foams. FDA records show that Arcutis received approval in May 2025 for Zoryve foam 0.3% for plaque psoriasis of the scalp and body in patients aged 12 and older, which illustrates how topical formats are still being upgraded rather than merely defended. That kind of product improvement helps the United States dermatological drugs market protect its highest-volume route even while severe disease care becomes more systemic.

Parenteral products are projected to grow at 9.44% CAGR through 2031 because psoriasis, atopic dermatitis, and hidradenitis suppurativa biologics still depend heavily on self-injection or supervised administration. This route keeps gaining importance as newer immune therapies move earlier in the treatment pathway and into younger patient populations. Oral therapy sits between topical convenience and injectable potency, which is why brands like JAK inhibitors and new oral pathway modulators are being positioned as a middle-ground option. FDA boxed warnings for JAK inhibitors continue to affect route selection by raising concerns around infections, malignancy, major cardiovascular events, thrombosis, and death in relevant inflammatory settings. This means route competition in the United States dermatological drugs market is being shaped not only by efficacy, but also by monitoring burden, risk tolerance, and patient willingness to accept chronic administration.

By Drug Class: PDE-4 Innovation Disrupts Corticosteroid Dominance

Corticosteroids led with 26.74% share in 2025 because they still cover a wide set of skin conditions and remain familiar, low-cost options across both prescription and OTC use. Their position in the United States dermatological drugs market is supported by decades of prescriber comfort and by the breadth of generic supply. At the same time, their long-term share is under pressure because chronic steroid use carries well-known limitations, especially in pediatric use and on sensitive skin areas. Severe disease is also moving toward biologics and targeted oral agents, which reduces the part of the treatment spectrum that once depended more heavily on repeated corticosteroid use. This makes the category durable in the near term, but less protected as targeted alternatives gain wider clinical acceptance.

PDE-4 inhibitors are projected to grow at 11.13% CAGR through 2031, which makes them the fastest-growing drug class in the report and the clearest disruptive force in moderate disease management. A 2025 review in Pharmaceutics identified 7 structurally distinct PDE-4 chemical scaffolds under dermatological development and noted that LEO Pharma had the broadest proprietary scaffold coverage, which suggests that companies are building platform-level intellectual property rather than relying on one topical asset. Retinoids, antibiotics, calcineurin inhibitors, and antifungals continue to serve stable roles in acne, bacterial skin infections, mild atopic dermatitis, and fungal disease without the same near-term disruption seen in immune-mediated segments. JAK inhibitors are still expanding, but class-level caution from the FDA keeps prescribing more selective and slows broad-based uptake. That gives PDE-4 inhibitors an important opening in the United States dermatological drugs market, especially where physicians want long-term non-steroidal topical use without the same safety overhang.

By Distribution Channel: Digital Channels Erode Retail Pharmacy Share

Retail pharmacies and drugstores held 53.27% of United States dermatological drugs market share in 2025, which reflects their role in both high-volume OTC purchases and routine prescription fulfillment. Their position is also supported by specialty pharmacy relationships that help move biologics through established dispensing and reimbursement pathways. Hospital pharmacies remain important for complex dermatology cases and for therapies that need tighter clinical supervision or infusion support. Even so, the channel mix is changing because same-day and digitally enabled dispensing is reducing the convenience advantage that physical stores once held. This means the United States dermatological drugs market is moving from a store-led refill model toward a more blended model that combines local pickup, specialty coordination, and direct digital delivery.

Online pharmacies are expected to advance at 10.67% CAGR through 2031, which gives them the fastest growth rate among distribution channels and makes them a major watch point for future share shifts. Amazon’s planned same-day expansion to nearly 4,500 US cities and towns by year-end 2026 gives digital dispensing a national logistics footprint that is well-suited to repeat dermatology purchases. Miiskin’s 2025 partnership with Photon Health also shows how consultation, visual assessment, prescribing, and fulfillment can now sit in one digital pathway. Retail incumbents therefore face their biggest risk not in the most complex biologics, but in refill-heavy topicals, oral agents, and OTC products that are easier to migrate online. The United States dermatological drugs market is still led by retail today, but digital execution is steadily narrowing the gap.

Geography Analysis

Specialist supply remains heavily concentrated in metropolitan areas, and that shapes where high-value biologic prescribing can scale fastest. Archives of Dermatological Research reported that the dermatologist supply-demand adequacy ratio was 108% in metropolitan areas in 2021 and only 39% in non-metropolitan areas, which shows how uneven treatment capacity remains. The same research found that national dermatologist supply is projected to rise 12.45% by 2036, compared with demand growth of 12.70%, and that non-metropolitan shortfalls become much larger under improved access assumptions. In practical terms, biologic growth in the United States dermatological drugs market is still concentrated in urban and suburban areas where specialists, specialty pharmacies, and referral systems are already present.

Sun Belt states such as Texas, Florida, California, and Arizona remain large treatment pools because of their population scale and steady demand across acne, rosacea, and other high-volume skin conditions. These states also carry meaningful Medicaid and low-income patient populations, so access to advanced therapies can vary sharply with state-level prior authorization rules and formulary design. The Northeast, including New York, New Jersey, Massachusetts, and Pennsylvania, remains a high-value region for specialist launches because it concentrates academic dermatology centers, clinical trial recruitment, and specialty infrastructure. CMS Part D redesign is also especially relevant in older patient markets such as Florida, Pennsylvania, and Michigan, where the USD 2,000 out-of-pocket cap improves access to specialty therapies from 2025 onward.

Digital care is becoming the main bridge between these dense specialist hubs and underserved regions. The workforce study projected that rural markets could face 157% excess dermatology demand by 2036 under improved access assumptions, which leaves significant room for tele-triage and remote prescribing models to fill basic treatment gaps. Tools that combine image-based assessment with e-prescribing and home delivery are therefore becoming commercially meaningful in the United States dermatological drugs market, especially for topicals and lower-complexity prescriptions. Near-term rural growth is still more favorable for OTC products and lower-complexity prescription topicals than for biologics, because specialist initiation remains a real constraint for advanced immune therapies.

Competitive Landscape

The United States dermatological drugs market is concentrated in the specialty biologic tier but remains much more dispersed across generics, corticosteroids, and OTC topicals. AbbVie holds a leading position in psoriasis through Skyrizi, while the Regeneron and Sanofi partnership remains central to atopic dermatitis through Dupixent’s scale. UCB, Novartis, and Johnson & Johnson are using newer indications and administration-route differentiation to challenge these established revenue pools. That has created a split strategy across the market, with large incumbents defending mature franchises while more focused players push into underpenetrated categories such as hidradenitis suppurativa, pediatric atopic dermatitis, and upgraded topical therapy. The result is a United States dermatological drugs market where concentration is high in a few specialty niches, but competitive intensity is broad because adjacent categories are still open.

Strategic moves over the past 2 years show how competition is evolving. Novartis launched a direct-to-patient pharmacy platform for Cosentyx in November 2025 at a 55% reduction from list price, signaling a more aggressive response to payer and substitution pressure. Arcutis used focused dermatology execution to win FDA approval for Zoryve foam in psoriasis in 2025, which strengthened its position as a specialist topical innovator rather than a broad primary care player. Sanofi advanced amlitelimab with positive Phase 3 data in March 2026, which shows that large companies are still investing heavily to widen the next wave of specialty treatment options in atopic dermatitis. These moves show that pricing, lifecycle extension, and targeted label expansion are now as important as first-launch novelty.

Topical innovation is also becoming more structured at the intellectual property level. The 2025 Pharmaceutics review noted that LEO Pharma had registered 4 distinct PDE-4 scaffold families between 2011 and 2024, which suggests that multi-scaffold platform design is becoming a durable way to defend future topical franchises. Digital channels are changing how brands reach physicians and patients at the same time, because image-based care, e-prescribing, and direct delivery reduce dependence on the older rep-driven sequence. This keeps the United States dermatological drugs market competitive even where a few products dominate sales, because execution now depends on channel design, access support, and label depth as much as on molecule quality alone.

United States Dermatological Drugs Industry Leaders

AbbVie Inc.

Bristol Myers Squibb

Eli Lilly and Company

Galderma

Sanofi SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Novartis received FDA approval for Cosentyx (secukinumab) in pediatric patients aged 12 and older with moderate-to-severe HS, extending the IL-17A inhibitor franchise to the fastest-growing therapeutic indication in dermatology and into the pediatric patient population.

- March 2026: Sanofi disclosed positive Phase 3 data for amlitelimab across three trials (COAST 1, COAST 2, SHORE) in moderate-to-severe atopic dermatitis at the AAD Annual Meeting, advancing an IL-33 receptor antibody toward potential US regulatory submission and further intensifying competition in the biologic AD segment.

- September 2025: Incyte received FDA approval for Opzelura (ruxolitinib cream) in children aged 2 to 11 with mild-to-moderate atopic dermatitis, becoming the third US approved indication for the ruxolitinib cream formulation and further expanding the non-steroidal topical option for pediatric patients.

- May 2025: Arcutis Biotherapeutics received FDA approval for Zoryve (roflumilast foam 0.03%) for plaque psoriasis of the scalp and body in patients 12 and older, extending the non-steroidal topical psoriasis franchise into a new foam vehicle with improved application compliance for hard-to-reach areas.

United States Dermatological Drugs Market Report Scope

The dermatological drugs market involves the development and sale of medications, including topical creams, oral pills, and biologics, used to treat diseases of the skin, hair, nails, and genital membranes. It excludes purely cosmetic products.

The United States Dermatological Drugs Market Report, presented in terms of value (USD), is segmented across several dimensions that define its therapeutic and commercial landscape. By indication, the market covers acne, psoriasis, atopic dermatitis, rosacea, alopecia areata, hidradenitis suppurativa (HS), and other dermatological conditions. In terms of prescription status, products are divided into prescription drugs and over‑the‑counter (OTC) formulations. By route of administration, therapies are delivered topically, orally, or via parenteral methods. From a drug class perspective, the market includes corticosteroids, retinoids, antibiotics, PDE‑4 inhibitors, JAK inhibitors, biologics, and other emerging classes. Finally, by distribution channel, dermatological drugs are supplied through hospital pharmacies, retail outlets, and online pharmacies.

| Acne |

| Psoriasis |

| Atopic Dermatitis |

| Rosacea |

| Alopecia Areata |

| Hidradenitis Suppurativa |

| Fungal Skin Infections |

| Other Dermatological Indications |

| Prescription |

| Over-the-Counter |

| Topical |

| Oral |

| Parenteral |

| Corticosteroids |

| Retinoids |

| Antibiotics |

| Antifungals |

| Calcineurin Inhibitors |

| PDE-4 Inhibitors |

| JAK Inhibitors |

| Biologics |

| Other Drug Classes |

| Hospital Pharmacies |

| Retail Pharmacies & Drugstores |

| Online Pharmacies |

| By Indication | Acne |

| Psoriasis | |

| Atopic Dermatitis | |

| Rosacea | |

| Alopecia Areata | |

| Hidradenitis Suppurativa | |

| Fungal Skin Infections | |

| Other Dermatological Indications | |

| By Prescription Status | Prescription |

| Over-the-Counter | |

| By Route of Administration | Topical |

| Oral | |

| Parenteral | |

| By Drug Class | Corticosteroids |

| Retinoids | |

| Antibiotics | |

| Antifungals | |

| Calcineurin Inhibitors | |

| PDE-4 Inhibitors | |

| JAK Inhibitors | |

| Biologics | |

| Other Drug Classes | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies & Drugstores | |

| Online Pharmacies |

Key Questions Answered in the Report

What is the size of the United States dermatological drugs market in 2025 and 2031?

The United States dermatological drugs market was valued at USD 16.78 billion in 2025 and is forecast to reach USD 28.30 billion by 2031, growing at a 9.24% CAGR during 2026-2031.

Which indication leads revenue in United States dermatology therapeutics?

Psoriasis was the leading indication in 2025 with 33.87% revenue share, supported by the scale of biologic therapies and strong commercial performance from major brands.

Which indication is growing the fastest through 2031?

Hidradenitis suppurativa is projected to expand at 9.97% CAGR through 2031, helped by new approvals and a still underpenetrated treatment base.

Why are OTC products gaining ground in skin therapy sales?

OTC products are forecast to grow at 10.06% CAGR through 2031 because consumer skincare awareness, digital consultation, and easy retail or online availability are widening self-care demand.

Which route of administration still dominates treatment volume?

Topical products led with 56.81% share in 2025 because acne, mild psoriasis, and mild-to-moderate eczema are still commonly managed without systemic therapy.

Page last updated on: