United States Urea Cycle Disorder Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

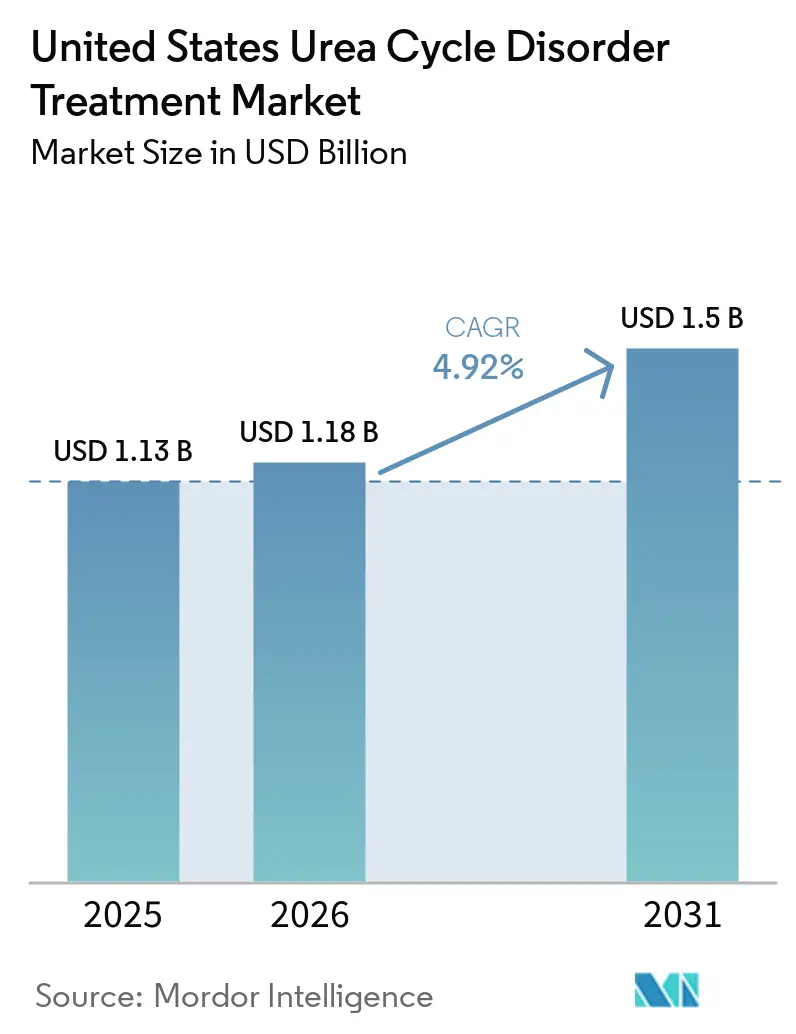

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.5 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Urea Cycle Disorder Treatment Market Analysis by Mordor Intelligence

The United States Urea Cycle Disorder Treatment Market size was valued at USD 1.13 billion in 2025 and is estimated to grow from USD 1.18 billion in 2026 to reach USD 1.5 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031).

Three powerful yet counterbalancing forces shape the current landscape: as tandem mass-spectrometry panels broaden, diagnosis rates rise; orphan-drug approvals accelerate, expanding therapeutic choices; and generic erosion mounts, compressing margins for legacy products. While the first-to-market edge of glycerol phenylbutyrate diminishes, its palatable liquid formulation still drives over half of all prescriptions. Meanwhile, step-therapy rules solidify sodium phenylbutyrate's position as the first-line, cost-effective care. Gene-editing advancements for deficiencies in ornithine transcarbamylase and carbamoyl phosphate synthetase 1 hint at a future shift towards one-time, potentially curative treatments. However, immediate adoption faces hurdles from CDMO capacity constraints and payers' scrutiny over multimillion-dollar launch prices.

Key Report Takeaways

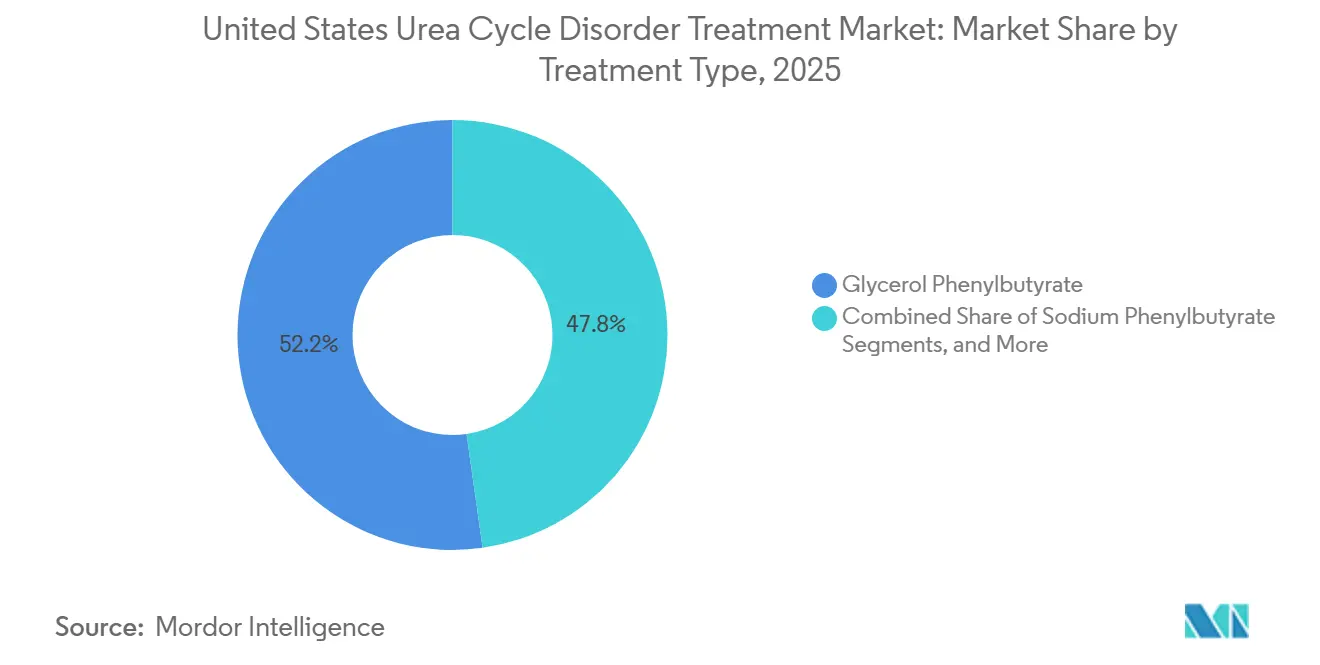

- By treatment type, glycerol phenylbutyrate led with 52.24% of the United States Urea Cycle Disorder Treatment market share in 2025. Amino-acid supplements and specialized medical formulas are advancing at a 4.62% CAGR through 2031, the fastest pace among treatment categories.

- By enzyme deficiency, ornithine transcarbamylase accounted for 58.04% of the segment’s United States Urea Cycle Disorder Treatment market size in 2025 and is expanding at a 4.55% CAGR to 2031.

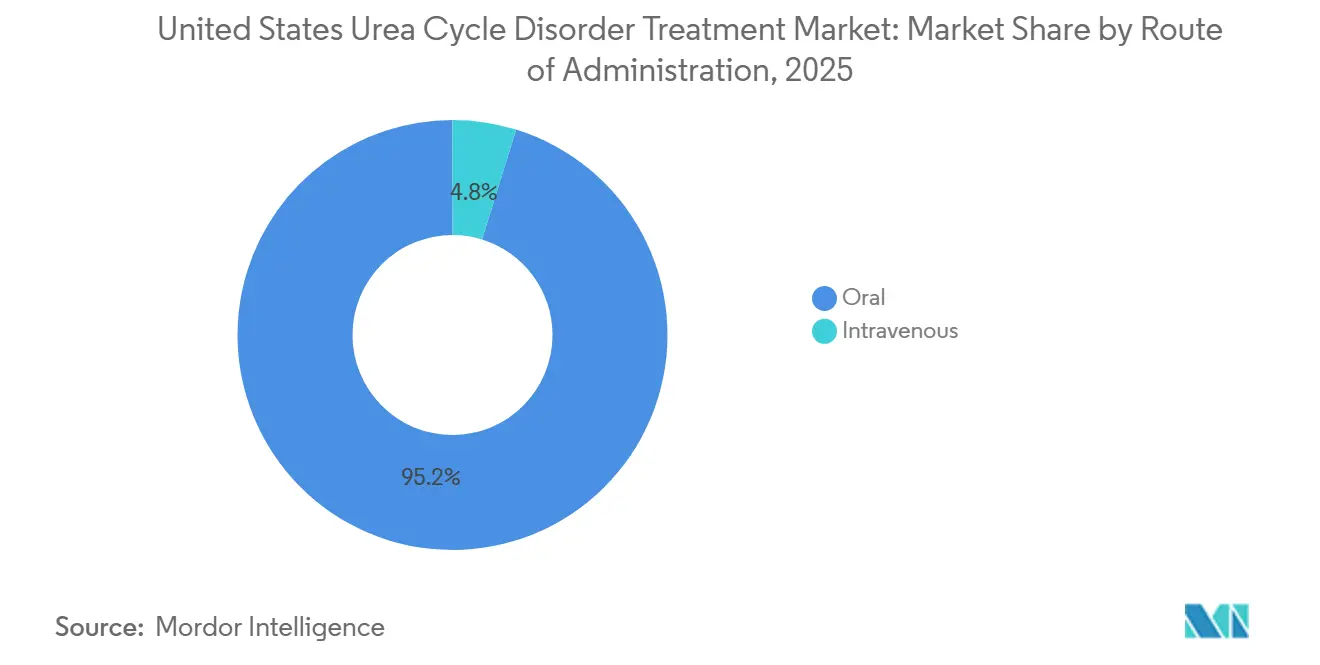

- Intravenous formulations commanded only 4.78% of 2025 revenue yet are growing at 5.1% CAGR as emergency departments standardize hyperammonemia protocols.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global United States Urea Cycle Disorder Treatment Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising incidence & newborn-screening expansion | +1.2% | National, state variability | Medium term (2-4 years) |

| FDA orphan-drug incentives & recent approvals | +1.5% | National | Short term (≤ 2 years) |

| Adoption of glycerol phenylbutyrate orals | +0.8% | National, metabolic specialty centers | Short term (≤ 2 years) |

| Patient-advocacy & awareness campaigns | +0.5% | National, UCDC network hubs | Medium term (2-4 years) |

| Wearable ammonia-monitoring integration | +0.3% | National, early academic adopters | Long term (≥ 4 years) |

| Taste-masked micro-encapsulated NaPB | +0.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence & Newborn-Screening Expansion

In the U.S., approximately 1 in 35,000 births, equating to about 113 infants annually, are born with a urea-cycle defect.[1]Newborn Screening Technical Assistance and Evaluation Program, “Recommended Uniform Screening Panel Update,” newsteps.org Historically, tandem mass-spectrometry programs only identified distal enzyme blocks. However, with the July 2024 addition of argininosuccinic aciduria and citrullinemia type I to the Recommended Uniform Screening Panel, diagnostic delays for these conditions have been reduced by up to three months. While proximal defects like ornithine transcarbamylase remain undetected by routine panels due to a drop in plasma citrulline levels, this oversight leaves around 300 newborns each year at risk of a hyperammonemic crisis before diagnosis. There's notable state-to-state variability: Texas prioritizes ASA and CIT-I, while Illinois screens all four distal disorders but lacks an algorithm for OTC confirmation. In 2025, the National Urea Cycle Disorders Foundation introduced The Partner Network, which now directs positive screens to a metabolic center within 72 hours, bridging a historical care-coordination gap. Despite early diagnoses, 40% of cases still face mortality, highlighting the urgent need for panel enhancements.[2]UnitedHealthcare Services Inc., “Prior Authorization Criteria – Ravicti,” uhcprovider.com

FDA Orphan-Drug Incentives & Recent Approvals

In February 2026, pegzilarginase received accelerated approval, achieving an 80% reduction in arginine levels and demonstrating clear functional benefits. This set a significant benchmark for using biochemical surrogate endpoints.[3]Securities and Exchange Commission, “Aeglea BioTherapeutics Announces FDA Approval of Loargys (pegzilarginase) for Arginase 1 Deficiency,” sec.gov Following this, Ultragenyx’s DTX301 gene therapy and iECURE’s ECUR-506 were both fast-tracked, now benefiting from priority FDA guidance under the Regenerative Medicine Advanced Therapy status. Additionally, Satellite Bio’s SB-101 clinched the Rare Pediatric Disease designation in May 2026, earning a transferable voucher potentially worth up to USD 150 million. While orphan-drug exclusivity provides a buffer against competition for biologics, the swift price erosion of small-molecule nitrogen scavengers, exemplified by glycerol phenylbutyrate post-exclusivity, serves as a cautionary tale. This underscores the importance for gene-therapy sponsors to tether pricing to lasting outcome data rather than fleeting statutory monopolies.

Adoption of Glycerol Phenylbutyrate Orals

Pediatric and adult patients favor liquid glycerol phenylbutyrate over sodium phenylbutyrate, primarily due to the latter's bitter taste. Randomized crossover studies validate that both have similar 24-hour ammonia exposure. Moreover, while ten-year observational cohorts suggest fewer crises with glycerol, formal superiority remains unproven. In May 2025, UnitedHealthcare and Regence rolled out step-therapy algorithms, mandating a trial of generic sodium phenylbutyrate before granting approval for Ravicti. This shift steered prescribing patterns towards generics. Amgen’s “By Your Side” initiative offers prior-authorization templates, adherence apps, and co-pay caps aligned with Federal Poverty Levels. This strategic move helps counterbalance a 15-20% price undercut by generics from Endo and Aurobindo.

Patient-Advocacy & Awareness Campaigns

Co-sponsored by the National UCD Foundation and Zevra Therapeutics, "Check Ammonia Month" distributed handheld analyzers to 200 emergency rooms. This initiative reduced the average time to the first ammonia reading to under 15 minutes and heightened clinician awareness. The UCD-ECHO telementoring series, initiated in 2025, shares monthly case discussions with 200 community hospitals, extending expertise beyond the 54 specialized metabolic centers in the country. In February 2026, the MyRareDiet mobile app introduced a two-way alert system: patients can log their protein intake, and care teams receive color-coded trend lines for ammonia levels. With registry enrollment now encompassing 65% of all diagnosed Americans, this vast dataset is instrumental for adaptive trial designs and payer dossiers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High therapy cost & reimbursement hurdles | -0.9% | National, Medicaid variability | Short term (≤ 2 years) |

| Scarcity of metabolic specialty centers | -0.6% | Rural and underserved regions | Medium term (2-4 years) |

| Supply-chain fragility for niche excipients | -0.3% | National | Short term (≤ 2 years) |

| Viral-vector CDMO capacity bottlenecks | -0.5% | National, global dependencies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Therapy Cost & Reimbursement Hurdles

Ravicti, priced at a wholesale pack rate of USD 5,785, results in an annual expenditure exceeding USD 300,000 for adults on standard dosing. This significant cost has led commercial and Medicaid plans to implement blanket prior authorizations. UnitedHealthcare's 2025 policy requires established users to follow the same step-therapy protocol as new patients, necessitating repeated trials with generics and potentially delaying access by up to three months. By late 2025, philanthropic copay assistance programs from organizations like HealthWell and NORD reached their enrollment limits, removing critical financial support for underinsured families. With gene-therapy prices expected to exceed USD 2 million per infusion, payers are likely to impose stricter access controls. To address this, sponsors may need to adopt outcome-based guarantees or staged payment models tied to the durability of ammonia-control outcomes.

Scarcity of Metabolic Specialty Centers

In the U.S., only 54 facilities provide the full range of services, including biochemical genetics, metabolic dietetics, and dialysis-capable ICUs. This limited availability leaves large rural areas underserved. By 2025, wait times for initial appointments extended to 120 days. Additionally, emergency transfers from community hospitals added 4-6 hours before ammonia-lowering treatments could begin, a delay associated with the risk of permanent neurological damage. While UCD-ECHO has expanded access, it cannot provide critical on-site assays such as glutamine and orotic acid, which are essential for managing crises. The American College of Medical Genetics projects a 25% shortage of biochemical geneticists by 2030. Without rapid advancements in telehealth reimbursement and point-of-care diagnostics, these regional access challenges are expected to worsen.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Generic Competition Narrows Price Gaps

In 2025, Glycerol phenylbutyrate held a 52.24% share of the U.S. market for Urea Cycle Disorder treatments. However, generics from Endo and Aurobindo have reduced branded list prices by nearly 20%. Following the 2024 Mead Johnson supply shock, the U.S. market for amino-acid supplements and medical formulas is expanding at a 4.62% CAGR, driven by neonatal protocols favoring protein-free calories. While step-therapy rules maintain sodium phenylbutyrate's lead for new starts, adherence challenges often lead patients back to glycerol phenylbutyrate within a year. Meanwhile, Carglumic acid continues to serve a niche but stable group with NAGS deficiency.

Second-order effects are influencing procurement strategies: children’s hospitals are broadening dual-sourcing contracts to mitigate single-supplier risks, and specialty pharmacies are offering adherence analytics as a billable service. Formulation R&D is now focusing on taste-masked microcapsules of sodium phenylbutyrate, aiming to counter glycerol phenylbutyrate’s palatability advantage as price differences diminish.

By Enzyme Deficiency Type: OTC Dominates Owing to Screening Blind-Spots

In 2025, ornithine transcarbamylase deficiency accounted for 58.04% of segment revenue, underscoring gaps in newborn screening for proximal enzyme blocks. The U.S. market for Urea Cycle Disorder treatments related to OTC cases is projected to grow at a 4.55% CAGR through 2031, as late-diagnosed adults increasingly enter chronic therapy. Distal disorders, such as citrullinemia type I and argininosuccinic aciduria, benefit from earlier therapy, reducing neonatal mortality rates to below 20%. Although arginase 1 deficiency saw the introduction of its first disease-modifying agent, pegzilarginase, in 2026, commercial forecasts remain cautious due to a prevalent base of fewer than 80 U.S. patients.

Forward pipelines are concentrated on AAV and mRNA constructs for OTC and CPS1. If durable ammonia control is demonstrated, the market could shift from lifelong scavengers to single-dose cures after 2029, altering the revenue mix across the U.S. Urea Cycle Disorder Treatment market.

By Route of Administration: IV Use Climbs in Emergency Algorithms

In 2025, oral agents dominated spending with a 95.22% share, reflecting routine outpatient management. However, intravenous treatments like Ammonul and dialysis are growing at a 5.1% CAGR. This growth is driven by emergency departments implementing protocols that prioritize IV scavenger loading when ammonia levels exceed 300 µmol/L. Additionally, point-of-care analyzers, introduced during Check Ammonia Month, have halved decision-making times, increasing demand for IV stock in community hospitals. While the market size for IV formulations in U.S. Urea Cycle Disorder treatments remains modest, the inclusion of standardized hyperammonemia bundles in 37 state Medicaid manuals ensures baseline utilization growth.

In the long term, wearable ammonia sensors could enable earlier outpatient interventions, potentially reducing emergency IV volumes. Until then, heightened awareness of rapid neurologic injuries will ensure hospital pharmacies continue to stock Ammonul, sodium benzoate, and disposables for continuous renal replacement.

Geography Analysis

Regional disparities divide a single country's landscape into distinct micro-markets. States like Illinois and Massachusetts, which quickly implemented the 2024 screening update, have achieved a 40% reduction in distal UCD diagnostic delays. In contrast, states that adopted the update later continue to experience historical lag times. Medicaid formularies further complicate this landscape: fourteen states designate glycerol phenylbutyrate as the preferred agent for patients on sodium restrictions, while twenty-three states require two documented failures of sodium phenylbutyrate before approval. These regulations influence dispensing channels, with southern states demonstrating a higher ratio of generics to branded medications compared to New England.

Workforce maldistribution intensifies access inequities. While academic centers in Philadelphia, Boston, and Houston serve as hubs for tertiary care, vast rural regions from the Dakotas to the Mountain West lack access to biochemical geneticists. Although telehealth coverage parity laws enacted in California and New York in 2025 improved follow-up adherence, they did not resolve critical transport challenges. In Texas, mobile ECMO and rapid-transfer networks have successfully reduced door-to-dialysis intervals by two hours, and this operational model is now being evaluated in five other states with Medicaid waivers.

Supply-chain disruptions create periodic regional shortages. A 2024 fire at Mead Johnson’s Indiana plant disrupted formula availability across the Midwest, prompting five hospital systems to source amino-acid mixes from European suppliers under FDA enforcement discretion. Gulf Coast compounding facilities, which are vulnerable to hurricanes, are proactively planning similar contingency measures for specialized excipients like phenylacetic acid.

Competitive Landscape

Competition is moderately concentrated, with the top five manufacturers accounting for approximately 70% of 2025 sales. Amgen’s Ravicti remains the largest single product; however, generics from Endo and Aurobindo now represent one-third of glycerol phenylbutyrate prescriptions, reducing branded revenue by 18%. Competitive strategies are shifting toward services, such as Amgen’s nurse hotlines and Endo’s adherence dashboards, rather than focusing solely on pricing. Sodium phenylbutyrate suppliers leverage step-therapy mandates to secure first-line positioning, although challenges with palatability continue to hinder long-term patient adherence.

The future of the market lies in genetic medicines. Ultragenyx’s DTX301 demonstrated statistically significant reductions in mean 24-hour ammonia levels during its Phase 3 results in March 2026. Meanwhile, iECURE’s ECUR-506 employs a twin-AAV cassette to integrate OTC cDNA at the ApoA1 locus, enabling lifelong expression under physiologic promoters. Korro Bio’s RNA-editing candidate KRRO-121, backed by an $85 million funding round in March 2026, aims to eliminate the need for immunogenic capsids. The acceptance of upfront multimillion-dollar pricing by payers will depend on real-world data showing reduced hospitalizations, which the NIH-funded UCD Consortium is collecting through 2027.

Legacy manufacturers are responding by developing taste-masked sodium phenylbutyrate formulations and testing digital pill bottles that record ingestion timestamps. These incremental innovations may help maintain market share until curative platforms demonstrate long-term viability. However, market dynamics are expected to evolve into a bifurcated structure, where chronic scavenger therapies coexist with one-time treatments, catering to varying levels of risk tolerance and insurance coverage.

United States Urea Cycle Disorder Treatment Industry Leaders

Abbott Laboratories

Bausch Health Companies Inc.

Amicus Therapeutics Inc.

Recordati Rare Diseases Inc.

Ultragenyx Pharmaceutical Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Satellite Bio received Rare Pediatric Disease designation for SB-101, unlocking a transferrable priority-review voucher worth up to USD 150 million.

- April 2026: Aurobindo launched generic glycerol phenylbutyrate at USD 4,479-4,929 per 25 mL pack, discounting branded Ravicti by 15-20%.

- March 2026: Korro Bio raised USD 85 million in private placement to fund KRRO-121 clinical milestones through 2028.

- February 2026: FDA granted accelerated approval to pegzilarginase (Loargys) for arginase 1 deficiency based on the PEACE Phase 3 trial.

- January 2026: iECURE’s ECUR-506 earned Regenerative Medicine Advanced Therapy designation, positioning it for priority review.

Global United States Urea Cycle Disorder Treatment Market Report Scope

As per the scope of the report, urea cycle disorders (UCDs) are rare genetic metabolic conditions in the United States that prevent the liver from breaking down nitrogen (ammonia) into waste, causing toxic buildup in the brain. Treatment focuses on lowering ammonia through strict low-protein diets, arginine/citrulline supplements, and nitrogen-scavenging medications, with liver transplants as a potential cure.

The United States Urea Cycle Disorder Treatment Market is segmented by treatment type, enzyme deficiency type, and route of administration. By treatment type, the market includes sodium phenylbutyrate, glycerol phenylbutyrate, sodium benzoate/phenylacetate, carglumic acid, and amino-acid supplements & specialized formulas. By enzyme deficiency type, the market is categorized into ornithine transcarbamylase deficiency, carbamoyl phosphate synthetase 1 deficiency, argininosuccinate synthetase deficiency/citrullinemia I, argininosuccinate lyase deficiency, arginase 1 deficiency, N-acetylglutamate synthase deficiency, and others. By route of administration, the market is segmented into oral and intravenous. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Sodium Phenylbutyrate |

| Glycerol Phenylbutyrate |

| Sodium Benzoate / Phenylacetate |

| Carglumic Acid |

| Amino-acid Supplements & Specialized Formulas |

| Ornithine Transcarbamylase Deficiency |

| Carbamoyl Phosphate Synthetase 1 Deficiency |

| Argininosuccinate Synthetase Def. / Citrullinemia I |

| Argininosuccinate Lyase Deficiency |

| Arginase 1 Deficiency |

| N-Acetylglutamate Synthase Deficiency |

| Others |

| Oral |

| Intravenous |

| By Treatment Type | Sodium Phenylbutyrate |

| Glycerol Phenylbutyrate | |

| Sodium Benzoate / Phenylacetate | |

| Carglumic Acid | |

| Amino-acid Supplements & Specialized Formulas | |

| By Enzyme Deficiency Type | Ornithine Transcarbamylase Deficiency |

| Carbamoyl Phosphate Synthetase 1 Deficiency | |

| Argininosuccinate Synthetase Def. / Citrullinemia I | |

| Argininosuccinate Lyase Deficiency | |

| Arginase 1 Deficiency | |

| N-Acetylglutamate Synthase Deficiency | |

| Others | |

| By Route of Administration | Oral |

| Intravenous |

Key Questions Answered in the Report

How large is the United States Urea Cycle Disorder Treatment market in 2026?

The market stood at USD 1.18 billion in 2026 and is forecast to reach USD 1.50 billion by 2031, reflecting a 4.92% CAGR.

Which product holds the highest share in current therapy?

Glycerol phenylbutyrate accounted for 52.24% of the 2025 market, though generics launched in 2025-2026 are eroding branded revenue.

Which enzyme deficiency represents the largest treated cohort?

Ornithine transcarbamylase deficiency captured 58.04% of enzyme-specific revenue in 2025 and remains the fastest-growing subtype at 4.55% CAGR to 2031.

How are step-therapy rules affecting prescribing?

Policies from UnitedHealthcare and other payers require failure on generic sodium phenylbutyrate before approving glycerol phenylbutyrate, delaying access by up to three months and shifting initial prescriptions toward generics.

What is the outlook for gene-therapy entrants?

Ultragenyx, iECURE, and Satellite Bio each hold priority designations, and if they demonstrate durable ammonia control, single-dose treatments could begin displacing chronic nitrogen scavengers after 2028.

Are intravenous formulations gaining traction?

Yes, IV agents are growing at 5.1% CAGR as emergency departments adopt standardized hyperammonemia protocols specifying IV Ammonul for ammonia above 300 µmol/L.

Page last updated on: