U.S. Women's Health Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 72.86 Billion |

| Market Size (2026) | USD 76.21 Billion |

| Market Size (2031) | USD 92.42 Billion |

| Growth Rate (2026 - 2031) | 4.60% CAGR |

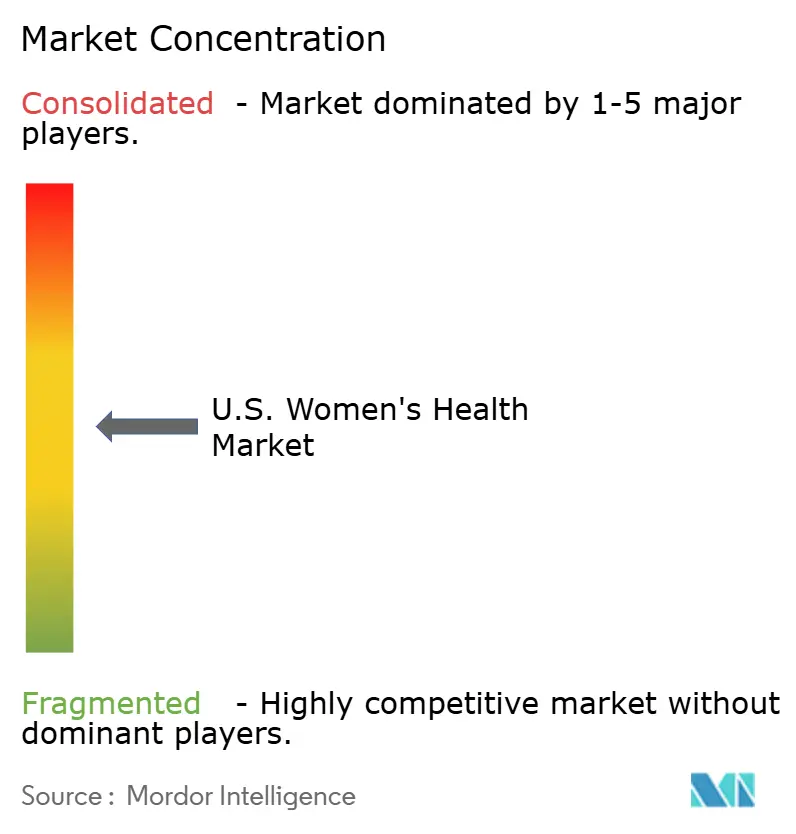

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Women's Health Market Analysis by Mordor Intelligence

The U.S. Women's Health Market size is expected to increase from USD 72.86 billion in 2025 to USD 76.21 billion in 2026 and reach USD 92.42 billion by 2031, growing at a CAGR of 4.60% over 2026-2031.

The United States women's health market is shifting towards comprehensive care that addresses contraception, fertility, menopause, chronic gynecological conditions, and preventive screenings. A significant driver is the FDA's February 2026 decision to remove cardiovascular and breast cancer warnings from six menopausal hormone therapy product labels, reducing barriers to treatment adoption and reshaping menopause care discussions. The market is also advancing with in-office procedures, virtual care, and home-based diagnostics, improving convenience and accelerating the transition from symptoms to treatment. Proposed federal changes to fertility benefits and employer-linked plan models are expanding access beyond traditional reimbursement pathways, ensuring steady utilization across reproductive and midlife care.

Key Report Takeaways

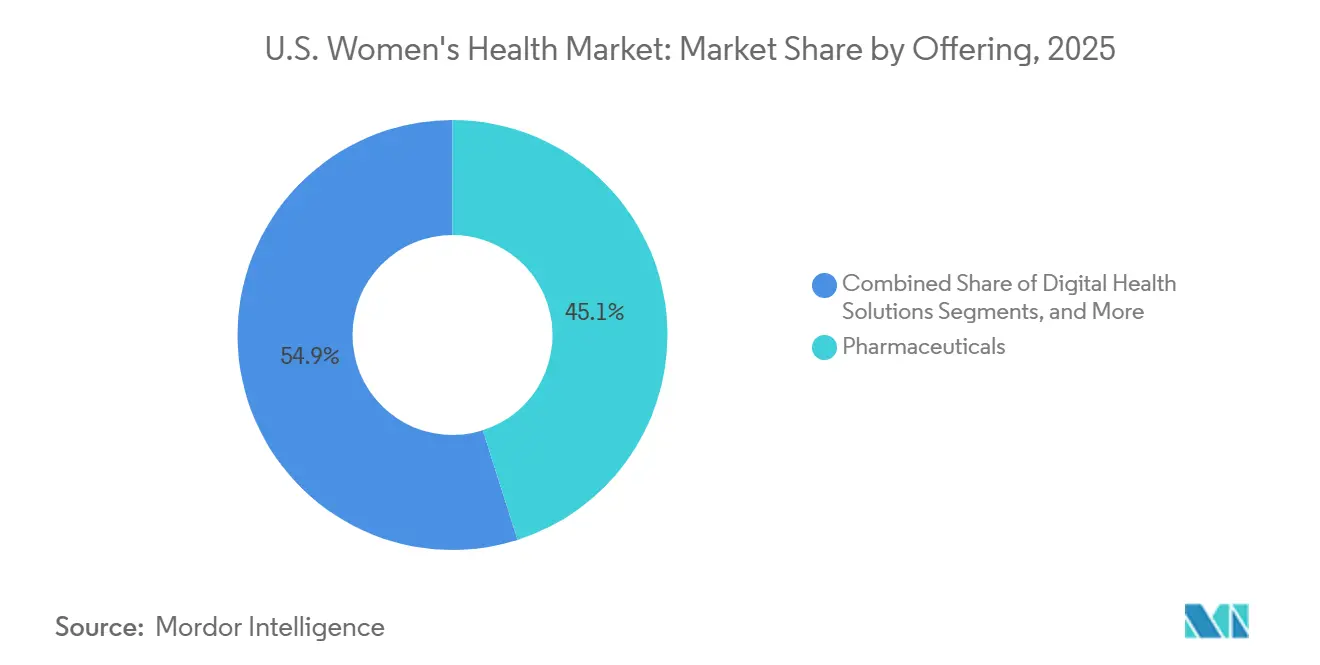

- By offering, pharmaceuticals held 45.12% of the US women's health market share in 2025, while digital health solutions are projected to record the highest CAGR at 7.25% through 2031.

- By application, contraception and family planning accounted for 36.76% of the US women's health market size in 2025, while menopause management is forecasted to expand at a 6.56% CAGR through 2031.

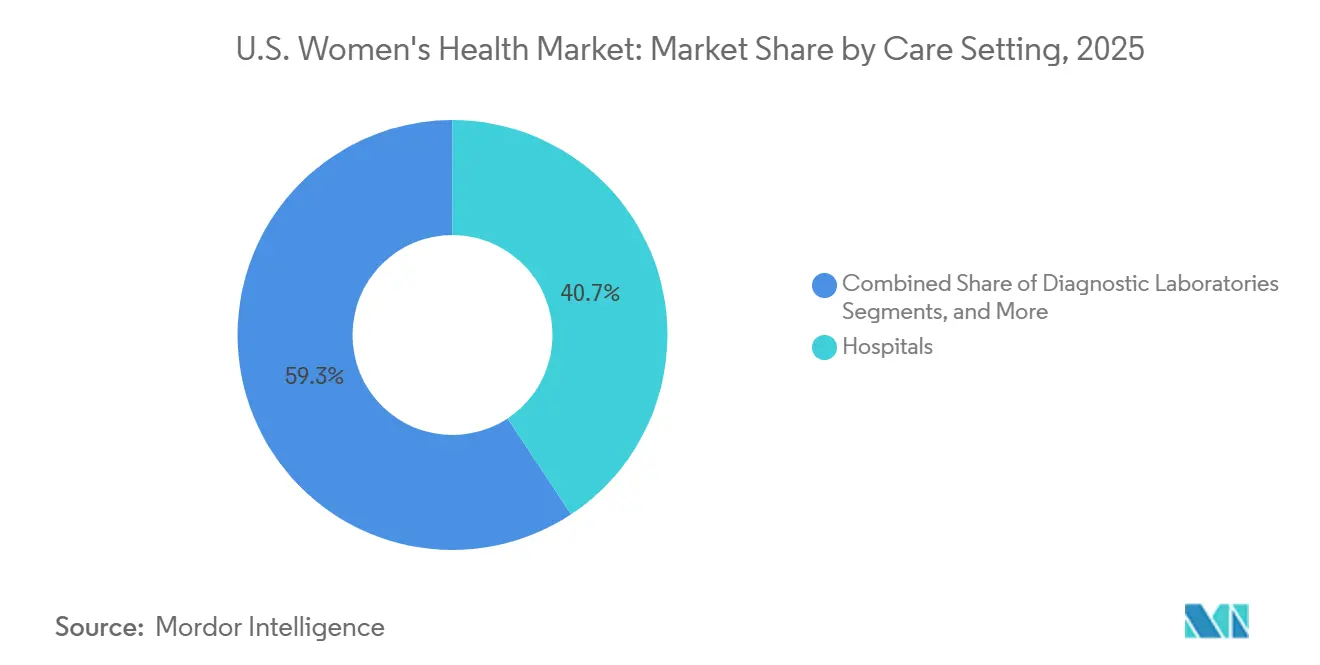

- By care setting, hospitals captured 40.67% share in 2025, while telehealth and virtual women's health platforms are projected to grow at a 7.35% CAGR through 2031.

- By age group, reproductive-age women represented 51.34% share in 2025, while postmenopausal women are expected to advance at a 6.92% CAGR through 2031.

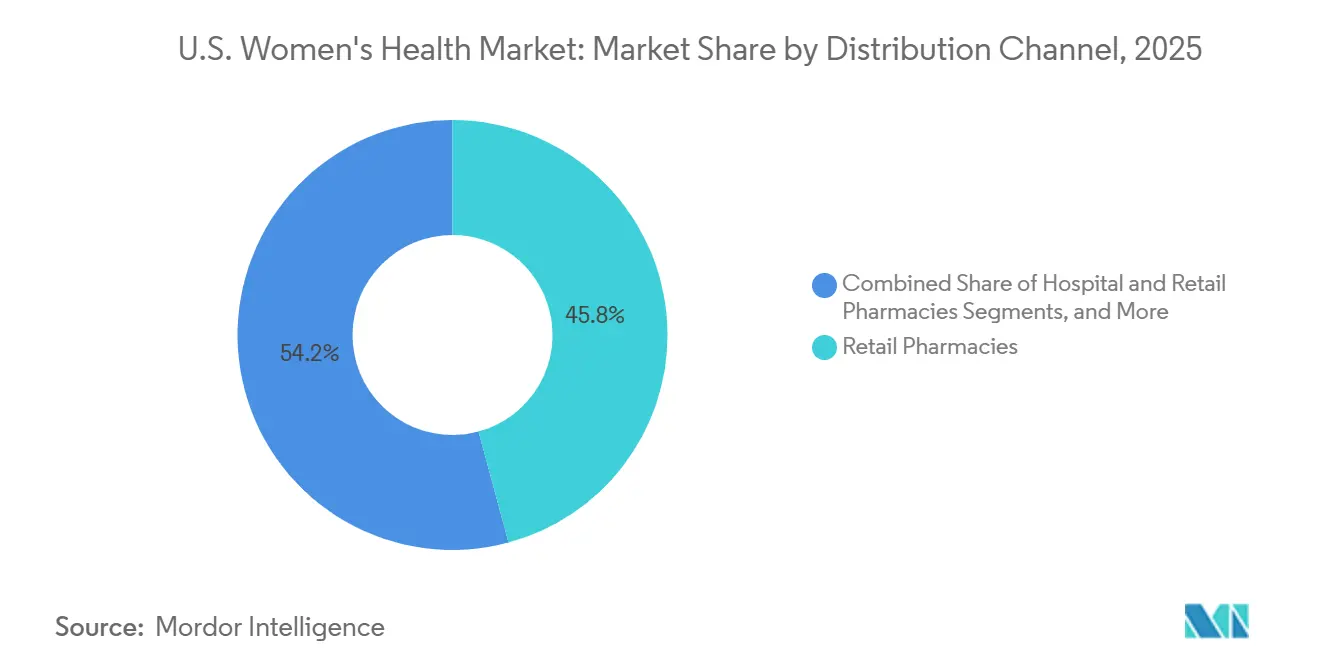

- By distribution channel, retail pharmacies held 45.78% share in 2025, while online pharmacies and direct-to-consumer channels are projected to expand at a 7.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Women's Health Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising demand for noninvasive and in-office women's health procedures | +1.0% | National, with early adoption concentrated in high-density metropolitan areas such as New York City, Los Angeles, Chicago, and Dallas | Medium term (2-4 years) |

| Expanding clinical recognition of menopause as a treatable condition | +1.2% | National, with strongest impact in states with established HRT prescribing infrastructure across the Northeast, California, and the Pacific Northwest | Short term (≤ 2 years) |

| Higher utilization of fertility diagnostics and assisted reproductive technologies | +0.9% | National, with volume concentrated in states with stronger fertility coverage frameworks including New York, Illinois, California, and New Jersey | Medium term (2-4 years) |

| Payor and employer interest in women's health benefits | +0.8% | National, with early gains in large employer markets such as Texas, New York, California, and Illinois | Short term (≤ 2 years) |

| Wider adoption of specialty women's health diagnostics | +0.6% | National, with particular strength in academic medical center clusters such as Boston, Houston, and San Francisco | Long term (≥ 4 years) |

| State-level policy support for family planning and prevention | +0.5% | State-specific, with early gains in mandate-active states such as California, New York, Illinois, and Massachusetts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Noninvasive and In-Office Women's Health Procedures

The United States women's health market is increasingly adopting procedures in lower-acuity settings. In April 2026, Femasys introduced FemaSeed Complete, enabling OB-GYNs to perform first-line inseminations and in-office sperm preparations, reducing reliance on external labs. This innovation simplifies fertility care access and lowers patient costs. Additionally, the approval of a new Category III CPT code for FemaSeed intratubal insemination in early 2026 strengthens reimbursement pathways, accelerating treatment adoption and patient participation.

Expanding Clinical Recognition of Menopause as a Treatable Condition

Menopause care is becoming a mainstream focus in the United States women's health market, driving increased demand. The FDA approved elinzanetant in October 2025, expanding non-hormonal treatment options for menopause-related hot flashes. In February 2026, the FDA removed boxed warnings from six hormone therapy products, addressing long-standing prescribing concerns. These developments are fostering evidence-based care and encouraging more women to seek diagnosis and treatment during midlife.[1]Food and Drug Administration, “FDA Approves Labeling Changes to Menopausal Hormone Therapy Products,” FDA, fda.gov

Higher Utilization of Fertility Diagnostics and Assisted Reproductive Technologies

Fertility care is gaining prominence in the United States women's health market. A 2025 NCHS report revealed that 13.7% of women aged 20 to 49 used fertility services, with 6.9% undergoing infertility testing, highlighting strong demand.[2]National Center for Health Statistics, “Use of Fertility Services in the United States,” CDC Data Brief 542, cdc.gov In May 2026, the U.S. Department of Labor proposed a rule capping fertility benefits at USD 120,000, simplifying employer-sponsored coverage. Progyny reported serving over 600 employers and 7.2 million covered lives in 2026, improving access to fertility diagnostics and treatments.[3]U.S. Department of Labor, “Excepted Benefits Relating to Certain Fertility and Reproductive Health Benefits,” U.S. Department of Labor, dol.gov

Payor and Employer Interest in Women's Health Benefits

Employer and payor initiatives are strengthening the United States women's health market. The Department of Labor's proposed rule on fertility benefits provides employers with a clearer framework for coverage. In April 2026, Progyny launched Progyny Select, a fully insured supplemental fertility plan for small employers, addressing affordability challenges. These efforts are expanding employer-linked coverage, creating a stable reimbursement base and driving treatment uptake across fertility and related services.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent underdiagnosis and late treatment initiation across key conditions | -0.6% | National, with disproportionate burden in rural and underserved states across the South and Midwest | Long term (≥ 4 years) |

| Coverage friction for long-acting contraception and fertility treatments | -0.8% | National, with highest impact in non-mandate states and states with weaker Medicaid support | Medium term (2-4 years) |

| Clinical hesitancy and safety-label sensitivity around women's therapeutics | -0.5% | National, with legacy hesitancy concentrated in geographies with older provider cohorts | Medium term (2-4 years) |

| Fragmented care pathways across primary care, ob-gyn, and specialty settings | -0.7% | National, broad across all markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Underdiagnosis and Late Treatment Initiation

Underdiagnosis limits the United States women's health market from converting clinical needs into treatment volumes. Polycystic ovary syndrome affects 6% to 12% of women of reproductive age, yet many remain undiagnosed for extended periods. Endometriosis in the United States faces an average diagnostic delay of 4.4 years, leading to economic burdens as care often begins after symptoms worsen. Uterine fibroids and endometriosis remain underdiagnosed across care settings, creating a gap between prevalence and documented treatment. Late diagnoses reduce early-stage pharmaceutical use and shift patients toward complex, less scalable interventions.

Coverage Friction for Long-Acting Contraception and Fertility Treatments

Coverage gaps slow access in the United States women's health market. Ten states that have not adopted Medicaid expansion leave 1.4 million eligible individuals without government-sponsored insurance, limiting access to contraception and preventive care. Twenty percent of uninsured women of reproductive age stopped using contraception due to costs, compared to 5% of Medicaid-covered women. Self-funded employer plans, exempt from state IVF mandates under ERISA, create uneven access even in states with coverage requirements. These gaps hinder uptake in high-need groups and slow the market's ability to convert demand into revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Pharmaceuticals Anchor the Market While Digital Health Reshapes Delivery

In 2025, pharmaceuticals accounted for 45.12% of the United States women's health market, driven by their role in managing contraception, menopause, endometriosis, and PCOS. Prescription therapies remain the primary treatment for high-volume conditions. The FDA's approval of elinzanetant in October 2025 expanded non-hormonal menopause treatment options. Organon reported a 16% decline in women's health revenue in Q1 2026, emphasizing the need for portfolio renewal alongside scale.

Digital health solutions are projected to grow at a 7.25% CAGR through 2031, making them the fastest-growing segment. Maven expanded its virtual clinic in May 2026, integrating GLP-1 care, hormone therapy, and over 30 women's health specialties. Diagnostics and device-led offerings, such as the Onclarity HPV Self-Collection Kit and BD Onclarity HPV Assay, are enhancing access to less invasive care pathways.

By Application: Contraception Leads, but Menopause and Specialty Conditions Gain Faster Momentum

Contraception and family planning represented 36.76% of the United States women's health market in 2025, reflecting their broad role across retail, provider, and public coverage channels. This segment benefits from recurring prescriptions, long-acting products, and preventive care, supported by digital platforms for consultations and renewals.

Menopause management is projected to grow at a 6.56% CAGR through 2031, driven by new non-hormonal treatments and updated hormone therapy labels. Endometriosis and PCOS remain key growth areas due to high disease burden and unmet needs, with diagnosis improvements expected to boost medication use and specialist referrals.

By Care Setting: Hospitals Retain Core Volume While Virtual Channels Expand Faster

Hospitals held 40.67% of the United States women's health market in 2025, reflecting their role in complex procedures and high-acuity reproductive services. Their importance lies in procedural intensity and multidisciplinary care, which cannot easily shift to lower-cost settings.

Telehealth and virtual platforms are projected to grow at a 7.35% CAGR through 2031. Twentyeight Health launched a nationwide virtual clinic in April 2026, partnering with over 100 insurers to reach approximately 16 million women. Femasys is enabling first-line fertility treatments in OB-GYN offices, redistributing routine care while maintaining hospital relevance for complex cases.

By Age Group: Reproductive-Age Women Hold the Largest Base While Postmenopausal Care Drives Growth

Reproductive-age women accounted for 51.34% of the United States women's health market in 2025, driven by frequent care needs such as contraception, fertility, prenatal services, and diagnostic testing. This segment benefits from recurring touchpoints that ensure steady demand.

Postmenopausal women are projected to grow at a 6.92% CAGR through 2031, supported by increased clinical acceptance of menopause treatments and new therapeutic options like elinzanetant. This growth highlights the rising importance of midlife and later-life care in the market.

By Distribution Channel: Retail Pharmacies Lead, but Online and DTC Access Is Growing Faster

Retail pharmacies held a 45.78% share of the United States women's health market in 2025, supported by prescription refill continuity, insurance-linked access, and geographic reach. They remain critical for long-term therapies requiring adherence.

Online pharmacies and direct-to-consumer channels are projected to grow at a 7.66% CAGR through 2031. Twentyeight Health and Maven Clinic are streamlining consultation, prescribing, and delivery, while employer-linked channels are driving scalability and convenience, challenging traditional distribution models to enhance service and efficiency.

Geography Analysis

The women's health market in the United States operates nationally but varies significantly by state due to differences in coverage rules, specialist availability, and delivery models. States with stronger insurance support for family planning and fertility services see higher utilization rates due to reduced coverage barriers and clearer referral pathways. Regions with established provider networks for menopause care, fertility treatments, and diagnostics benefit more quickly. Major metropolitan areas lead in adoption due to specialist density, employer coverage, and faster rollout of clinical services, making access more about efficiency than population size.

The South and Midwest face the most challenges in the United States women's health market due to coverage gaps and provider shortages. Ten non-expansion states leave 1.4 million eligible individuals without government-sponsored insurance, creating concentrated access risks. In 2025, 20% of uninsured women of reproductive age stopped using contraception due to cost, highlighting financial barriers. Virtual care is critical in these regions, reducing reliance on local specialists. Twentyeight Health addresses these gaps by providing nationwide access to approximately 16 million women, including Medicaid members.

Large commercial states dominate the upper tier of the United States women's health market due to advanced employer-sponsored benefits. In 2026, Progyny served over 600 employer clients and approximately 7.2 million covered lives, reflecting concentrated demand in major employment hubs. The market operates through a mix of state policies, employer benefit designs, and provider availability, favoring platforms capable of managing multi-state compliance while ensuring consistent care experiences across locations.

Competitive Landscape

The United States women's health market is moderately concentrated at the top but remains diverse across pharmaceuticals, diagnostics, devices, telehealth, and benefit management. Major players like AbbVie, Pfizer, Merck, Organon, and Bayer dominate the prescription segment, while diagnostics leaders and digital innovators are reshaping adjacent categories. Bayer strengthened the menopause therapy segment with the 2025 FDA approval of elinzanetant, introducing a non-hormonal option in a growing treatment area.

In 2026, leading companies focused on controlling broader care pathways rather than just selling products. Abbott's USD 21 billion acquisition of Exact Sciences expanded its cancer screening and precision diagnostics portfolio, enhancing its position in women's oncology testing. Waters and BD received FDA clearance for an at-home HPV self-collection solution in April 2026, advancing cervical screening into home-based diagnostics. Femasys launched FemaSeed Complete in April 2026 and secured a new Category III CPT code for reimbursement, showcasing how device makers are driving adoption through workflow changes rather than product differentiation. These developments highlight increasing competition centered on access, convenience, and integration.

Digital and benefit-focused companies are adding complexity to the United States women's health market. Maven expanded its direct-to-consumer platform nationwide in May 2026, while Twentyeight Health broadened insured virtual care access for a large population. Progyny introduced a fully insured supplemental fertility product for small employers, improving access for groups previously excluded from premium fertility coverage. Scale remains critical, but companies must now prioritize distribution reach, reimbursement alignment, and patient access to maintain their market position.

U.S. Women's Health Industry Leaders

AbbVie Inc.

Bayer AG

Pfizer Inc.

Organon & Co.

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Maven Clinic launched a nationwide direct-to-consumer platform, integrating GLP-1 management, hormone care, and over 30 women's health specialties.

- May 2026: Aspira Women's Health entered into a Master Collaboration and License Agreement with Cleveland Clinic to develop AI-powered, noninvasive diagnostics utilizing novel biomarker signatures.

- April 2026: Progyny launched Progyny Select, the first fully insured supplemental fertility and family-building plan designed for small employers.

- April 2026: Waters Corporation received FDA clearance for the Onclarity HPV Self-Collection Kit and approval for the BD Onclarity HPV Assay for at-home use.

- April 2026: Femasys launched FemaSeed Complete for OB-GYNs, and the AMA CPT Editorial Panel approved a new Category III CPT code for FemaSeed intratubal insemination.

- April 2026: Twentyeight Health introduced Complete Care, a nationwide insurance-enabled virtual clinic in partnership with over 100 insurance providers, covering approximately 16 million women, including Medicaid beneficiaries, with copays starting as low as USD 0.

- March 2026: Femasys commenced patient enrollment for the pivotal FINALE clinical trial of FemBloc following FDA IDE approval.

U.S. Women's Health Market Report Scope

As per the scope of the report, women's health focuses on the diagnosis, treatment, and prevention of diseases uniquely or disproportionately affecting women. The women’s health market is the commercial ecosystem that provides the pharmaceuticals, medical devices, and digital solutions required to support women’s physical and emotional well-being across their entire life cycle.

The U.S. women's health market is segmented by offering, application, care setting, age group, and distribution channel. By offering, the market includes pharmaceuticals, medical devices, diagnostics, digital health solutions, and nutraceuticals & wellness products. By application, the market is segmented into contraception and family planning, fertility and reproductive endocrinology, menopause management, osteoporosis prevention and treatment, endometriosis and uterine fibroids, PCOS management, and breast health & screening. By care setting, the market is categorized into hospitals, OB-GYN clinics, fertility centers, diagnostic laboratories, retail & mail-order pharmacies, and telehealth & virtual platforms. By age group, the market is segmented into adolescents & young adults, women of reproductive age, perimenopausal women, and postmenopausal women. By distribution channel, the market includes hospital pharmacies, retail pharmacies, online pharmacies, specialty pharmacies, and direct-to-consumer & employer channels. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Pharmaceuticals |

| Medical Devices |

| Diagnostics |

| Digital Health Solutions |

| Nutraceuticals and Wellness Products |

| Contraception and Family Planning |

| Fertility and Reproductive Endocrinology |

| Menopause Management |

| Osteoporosis Prevention and Treatment in Women |

| Endometriosis and Uterine Fibroids |

| PCOS Management |

| Breast Health and Screening-Linked Care |

| Hospitals |

| OB-GYN Clinics |

| Fertility Centers |

| Diagnostic Laboratories |

| Retail and Mail-Order Pharmacies |

| Telehealth and Virtual Women's Health Platforms |

| Adolescents and Young Adults |

| Reproductive Age Women |

| Perimenopausal Women |

| Postmenopausal Women |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Specialty Pharmacies |

| Direct-to-Consumer and Employer Channels |

| By Offering | Pharmaceuticals |

| Medical Devices | |

| Diagnostics | |

| Digital Health Solutions | |

| Nutraceuticals and Wellness Products | |

| By Application | Contraception and Family Planning |

| Fertility and Reproductive Endocrinology | |

| Menopause Management | |

| Osteoporosis Prevention and Treatment in Women | |

| Endometriosis and Uterine Fibroids | |

| PCOS Management | |

| Breast Health and Screening-Linked Care | |

| By Care Setting | Hospitals |

| OB-GYN Clinics | |

| Fertility Centers | |

| Diagnostic Laboratories | |

| Retail and Mail-Order Pharmacies | |

| Telehealth and Virtual Women's Health Platforms | |

| By Age Group | Adolescents and Young Adults |

| Reproductive Age Women | |

| Perimenopausal Women | |

| Postmenopausal Women | |

| By Distribution Channel | Hospital Pharmacies |

| Retail Pharmacies | |

| Online Pharmacies | |

| Specialty Pharmacies | |

| Direct-to-Consumer and Employer Channels |

Key Questions Answered in the Report

What is the size of the US women's health market in 2026 and 2031?

The US women's health market size is USD 76.21 billion in 2026 and is projected to reach USD 95.42 billion by 2031, at a CAGR of 4.60%.

Which offering segment leads revenue generation?

Pharmaceuticals lead with a 45.12% share in 2025 because they cover high-volume needs across contraception, menopause, endometriosis, and PCOS treatment.

Which application area is growing the fastest?

Menopause management is the fastest-growing application, with a projected CAGR of 6.56% through 2031, supported by new treatment approvals and updated FDA labeling.

Which care setting is expanding the fastest?

Telehealth and virtual women's health platforms are growing the fastest at a 7.35% CAGR through 2031 as providers expand insured and nationwide access models.

Which age group has the strongest growth outlook?

Postmenopausal women are expected to grow the fastest at a 6.92% CAGR through 2031, helped by broader acceptance of active menopause treatment.

Which distribution channel is changing the fastest?

Online pharmacies and direct-to-consumer channels are expanding the fastest at a 7.66% CAGR through 2031 as digital consultation, prescribing, and delivery become more integrated.

Page last updated on: