United States Medical Cold Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

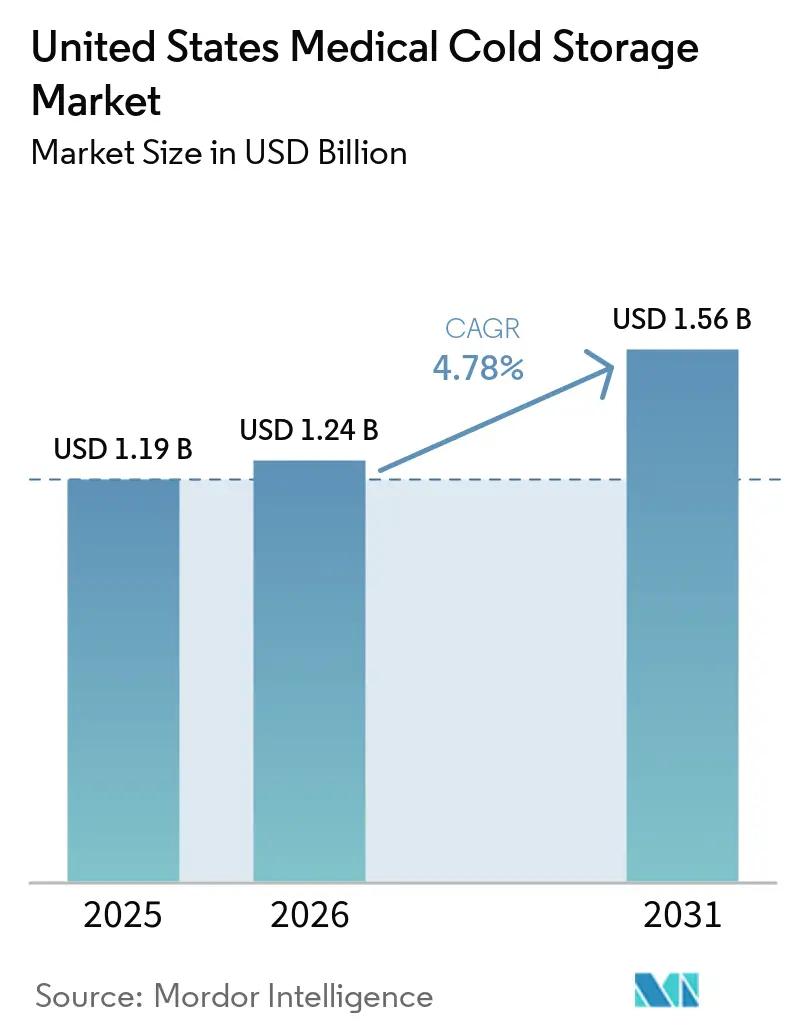

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.56 Billion |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Medical Cold Storage Market Analysis by Mordor Intelligence

The United States Medical Cold Storage Market size is expected to grow from USD 1.19 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.56 billion by 2031 at 4.78% CAGR over 2026-2031.

The United States medical cold storage market is being shaped by demand that comes from biologics expansion, storage compliance, and cryogenic handling needs rather than short-term equipment cycles. Facilities are moving from standard pharmacy refrigeration toward layered temperature management that includes ambient, ultra-low, and cryogenic conditions, which is changing how hospitals, laboratories, and outsourced biomanufacturing sites plan capital spending. The post-pandemic vaccine infrastructure buildout created a larger installed base, but the next stage of the United States medical cold storage market is being defined by cell and gene therapy commercialization, connected monitoring, and tighter refrigerant rules. Replacement demand is also becoming more compliance-driven because blood banking, vaccine storage, and biologics handling increasingly require purpose-built equipment, continuous monitoring, and audit-ready records. That combination gives the United States medical cold storage market a steadier demand floor, even as procurement teams face higher complexity around energy use, refrigerant transitions, and backup resilience requirements.

Key Report Takeaways

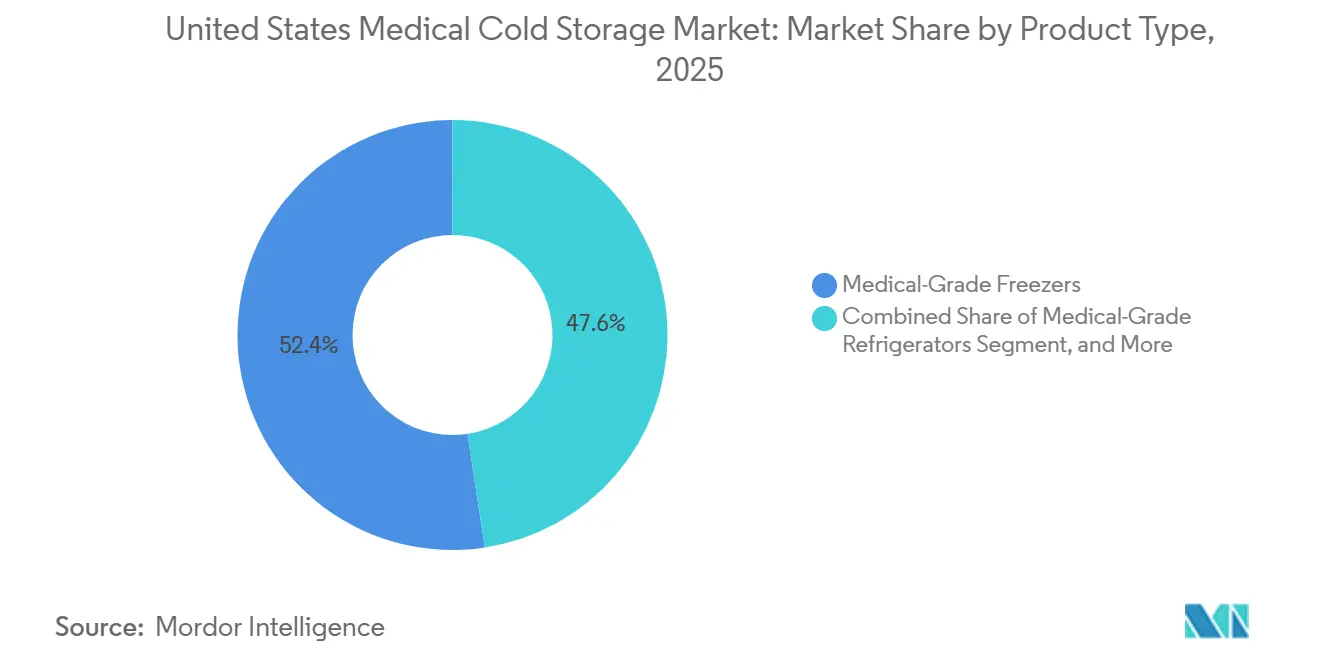

- By product type, medical-grade freezers led with 52.43% revenue share in 2025, while monitoring systems and accessories are forecast to expand at a 6.36% CAGR through 2031.

- By storage temperature range, ultra-low storage held 43.21% share in 2025, while cryogenic storage is projected to record the fastest growth at 5.87% CAGR through 2031.

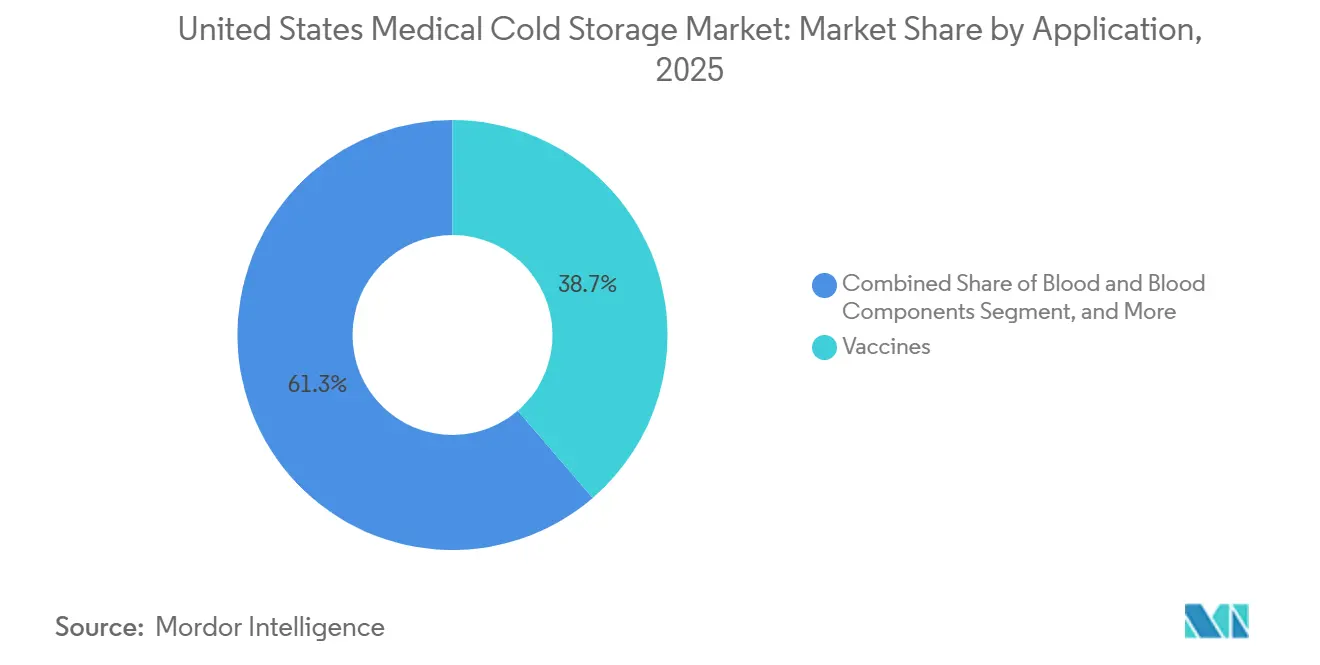

- By application, vaccines accounted for 38.72% share in 2025, while cell and gene therapies are advancing at the highest projected CAGR of 6.97% through 2031.

- By end user, hospitals and health systems held 45.82% share in 2025, while CROs, CMOs, and cell therapy processing sites are projected to grow fastest at 7.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Medical Cold Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Biologics And Specialty-Drug Cold Storage Demand | +1.2% | National, concentrated in Northeast corridor, Boston/Cambridge, and San Francisco Bay Area biotech hubs | Long term (≥ 4 years) |

| Rising Vaccine Inventory Complexity Across Care Settings | +0.8% | National, with early gains in suburban, rural, and safety-net care settings | Medium term (2-4 years) |

| Tighter FDA, CDC, And Accreditation Compliance Requirements | +0.7% | National | Short term (≤ 2 years) |

| Cell And Gene Therapy Scale-Up Requiring Cryogenic Capacity | +1.0% | Northeast, Mid-Atlantic, California, Southeast, concentrated in CGT manufacturing hubs | Long term (≥ 4 years) |

| ENERGY STAR-Led Replacement Of Aging Installed Base | +0.5% | National, with institutional concentration at academic medical centers | Medium term (2-4 years) |

| Decentralized Clinical Trials Creating Distributed Storage Nodes | +0.4% | National, geographically distributed to patient home and local clinic locations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expanding Biologics and Specialty-Drug Cold Storage Demand

The United States medical cold storage market is gaining durable support from the growing number of biologics that need validated handling across manufacturing, distribution, and care delivery sites. Biocon Biologics received FDA approval in 2025 for Kirsty, an interchangeable rapid-acting insulin aspart, which widened cold chain requirements across pharmacies, hospital outpatient departments, and specialty care settings.[1]Biocon Biologics, “Biocon Biologics Expands Diabetes Portfolio With FDA Approval of Kirsty,” Biocon Biologics, biocon.com Each new biologic launch adds storage needs beyond the manufacturer because the same product must move through distribution nodes, hospital pharmacies, and monitored clinical inventories before administration. That pattern matters for the United States medical cold storage market because it creates repeat replacement demand across the full chain instead of tying equipment sales to a single launch event. Storage validation standards also keep procurement tied to compliance, which makes purpose-built refrigeration and freezer capacity harder to postpone than general equipment purchases. As biologics portfolios widen, the United States medical cold storage market continues to shift toward regulated assets that must meet documentation, temperature uniformity, and monitoring expectations in daily operations.

Cell and Gene Therapy Scale-Up Requiring Cryogenic Capacity

The United States medical cold storage market is also being lifted by the expansion of commercial cell and gene therapy programs that depend on cryogenic handling. Cryoport stated in its first quarter 2026 results that it supports 21 commercially approved CGTs and 766 active clinical trials globally, with 569 in the Americas, which shows the scale of programs requiring specialized storage and logistics. BioLife Solutions reported in May 2026 that its biopreservation media were embedded in 17 approved CGT products, with 9 additional approvals or expansions anticipated within 12 months, which points to continuing demand for validated cryogenic workflows. Unlike vaccine inventories, autologous therapies need a dedicated labeled cryogenic position for each patient lot, so storage demand rises with every treatment slot rather than only with bulk batch volumes. That patient-specific model gives the United States medical cold storage market a strong growth layer in cryogenic systems, especially at outsourced manufacturing and processing sites where chain-of-custody controls are most intensive. It also keeps procurement concentrated among vendors that can pair physical storage with validation support, remote diagnostics, and documented audit trails.

Tighter FDA, CDC, and Accreditation Compliance Requirements

The United States medical cold storage market benefits from a compliance environment that is steadily becoming more integrated across blood, vaccine, medication, and biologics storage. AABB continued to tighten expectations around digital traceability through its September 2025 FDA Blood Establishment Registration Toolkit and its proposed 35th edition standards for blood banks and transfusion services. The Joint Commission’s 2026 National Performance Goals added explicit backup refrigeration expectations for designated medication refrigerators and freezers, which directly link storage decisions to survey readiness and operational continuity. Facilities now face a setting where temperature performance, electronic records, alarm response, and power continuity are increasingly reviewed together rather than as separate issues. That makes the United States medical cold storage market more replacement-driven because legacy units without integrated monitoring or documented backup plans create broader accreditation risk. The result is a procurement bias toward systems that combine hardware, alarms, remote oversight, and validation documentation in a single platform.

Rising Vaccine Inventory Complexity Across Care Settings

The United States medical cold storage market still carries a strong vaccine infrastructure base, but product handling has become more complex across pharmacies, primary care sites, and public health settings. Merck’s ENFLONSIA received FDA approval for the 2025-2026 RSV season, which added another cold-chain product to pediatric and preventive care workflows. Bavarian Nordic’s freeze-dried JYNNEOS approval in March 2025 introduced a different storage profile from the earlier liquid-frozen formulation, which required updates to storage protocols and documentation. Many care sites now hold products with different stability windows and temperature bands inside the same limited footprint, which raises the need for dedicated vaccine units and stronger monitoring discipline. That supports the United States medical cold storage market because providers enrolled in institutional immunization programs must keep continuous, traceable temperature records rather than relying on general-purpose equipment. It also strengthens demand for monitoring systems and accessories, since digital logging and deviation reporting are becoming standard for mixed vaccine inventories across distributed care settings.[2]AABB, “Proposed 35th Edition of Standards for Blood Banks and Transfusion Services,” AABB, aabb.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Lifecycle Energy Costs Of ULT Assets | -0.7% | National, with disproportionate impact on critical access hospitals and rural health systems | Long term (≥ 4 years) |

| Calibration, Monitoring, And Audit Burden Across Facilities | -0.4% | National | Short term (≤ 2 years) |

| Refrigerant-Transition Procurement Complexity | -0.3% | National, amplified in California-based facilities subject to additional CARB standards | Medium term (2-4 years) |

| Backup-Power And Disaster-Resilience Requirements | -0.2% | Southeast, Gulf Coast, and Atlantic hurricane belt, Pacific Northwest seismic zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Energy Costs of ULT Assets

The United States medical cold storage market still faces a real cost barrier from ultra-low temperature equipment, especially in settings with tight capital approval cycles. Purchase prices remain high for compliance-grade -80°C systems, and the cost burden rises further when facilities add calibration, service contracts, backup power integration, and future refrigerant-related adjustments. The University of California, Santa Barbara, estimated a 6 to 13 year payback period for ENERGY STAR ULT replacements, even with strong energy savings, which shows why many facilities delay upgrades despite clear operating benefits.[3]University of California Santa Barbara Engineering, “Funding Available to Replace Old Energy-Inefficient Equipment, Including ULT Freezers,” UCSB Engineering, ucsb-engr.atlassian.net This slows parts of the United States medical cold storage market because smaller hospitals, independent laboratories, and rural health systems often cannot replace aging units on the same timetable as large academic centers. Even when energy-efficient alternatives are available, procurement teams must weigh upfront premiums against long replacement cycles and site-specific budget limits. The result is a market where replacement intent is present, but actual conversion can move slowly outside well-funded institutions.

Refrigerant-Transition Procurement Complexity

The United States medical cold storage market is also being restrained by refrigerant transition uncertainty during the 2026 to 2032 compliance window. The EPA Technology Transitions Program set an interim GWP limit of 700 for new cold storage warehouse installations from January 1, 2026, with further reductions to 150 to 300 required by January 1, 2032. That timeline forces buyers to consider whether a unit purchased now could face retrofit pressure before the end of its expected service life. Facilities Dive reported that natural refrigerant options can require added ventilation and electrical modifications, which raises installation costs at sites that were not designed for flammable refrigerants. Deep-freeze systems need more complex refrigerant architectures, which narrows the supplier pool and lengthens procurement decisions for high-specification installations. This issue is most visible in walk-in cold rooms and large-capacity ULT systems, where refrigerant charge and site engineering requirements are harder to standardize across multi-facility networks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Freezers Anchor Volume, Monitoring Systems Accelerate

Medical-grade freezers accounted for 52.43% of the United States medical cold storage market size in 2025, which made them the largest product category by revenue. Their lead came from wide use across blood components, specialty biologics, and research sample preservation, where -20°C to -90°C performance is routine. The United States medical cold storage market continues to rely on this category because freezers serve the broadest mix of healthcare, research, and biopharma applications. Procurement activity within the category is centered on units that can combine temperature stability, alarm systems, and documented compliance features in one platform. The VA Long Beach 2025 solicitation for TSX Universal Series -80°C freezers showed how buyers are now specifying dual-cascade refrigerants and extended warranty expectations, which favors established suppliers with validated product lines.

Medical-grade refrigerators remain the installed volume base for pharmacy, vaccine, blood bank, and laboratory use, but the demand pattern is more mature, and replacement-led rather than expansion-led. These units still matter because broad ambulatory and hospital use gives them a large installed footprint across the United States medical cold storage market. Walk-in cold rooms and cryogenic systems serve narrower but higher-intensity use cases, especially where GMP biorepository functions or advanced therapy handling are involved. Monitoring systems and accessories are forecast to grow at a 6.36% CAGR through 2031, which makes them the fastest-growing product grouping as digital compliance shifts from optional to expected. That growth reflects a practical change in buying behavior, because facilities increasingly need traceable logs, automated alerts, and audit-ready dashboards rather than manual temperature records alone.

Cryogenic storage is still smaller in current revenue terms, but it represents the highest-intensity capital deployment area inside this product mix. The main reason is that cell and gene therapy workflows require purpose-built storage conditions and documented chain-of-custody controls that cannot be served by standard freezer platforms. Cryoport’s MVE Biological Solutions introduced the Fusion 800 Series self-sustaining cryogenic freezer in the first quarter of 2026, which addressed one of the main operational limits of cryogenic adoption by reducing dependence on continuous liquid nitrogen supply. That type of product development shows how the US medical cold storage industry is responding to operational pain points, not just temperature targets. It also means product competition is moving toward integrated system design, where safety, remote oversight, and cryogenic workflow fit matter as much as pure cabinet performance.

The monitoring category is gaining from the same compliance shift, but with a different value proposition. Buyers increasingly want storage assets that can produce documentation without relying on manual intervention, which supports remote diagnostics and easier survey preparation. PHC’s TwinGuard ECO 703VXH launch in January 2026 reflected this shift by pairing ultra-low performance with remote diagnostics and optional identity-based access control. In the United States medical cold storage market, that combination turns monitoring from an accessory purchase into a core part of product qualification. Over time, this is likely to widen the gap between vendors selling compliant platforms and vendors competing mainly on cabinet hardware.

By Storage Temperature Range: Ultra-Low Dominates, Cryogenic Tier Reshapes Demand Structure

Ultra-low storage represented 43.21% of the United States medical cold storage market size in 2025, which made it the largest temperature band by value. This range remains central because many biologics, research samples, and advanced therapy materials are stabilized at very low temperatures under validated handling protocols. The United States medical cold storage market depends heavily on ultra-low systems because they sit at the intersection of research, blood-related applications, specialty therapeutics, and outsourced biomanufacturing. Demand here is not only broad but also specification-heavy because buyers increasingly want energy efficiency, redundancy, and audit support in the same unit. That is why product launches in this band carry outsized weight in competitive positioning.

PHC Corporation of North America launched the TwinGuard ECO 703VXH in January 2026 with 7.3 kWh per day consumption at a -80°C setpoint, natural refrigerants, and inverter-controlled dual compressor redundancy. The launch matters because it addressed three purchase criteria at once, which were energy costs, backup protection, and low-GWP transition readiness. In the United States medical cold storage market, vendors that solve all three issues together are better placed than those that treat them as separate procurement decisions. Refrigerated storage at 2°C to 8°C remains a stable and large installed base because vaccines, medications, and blood-related applications continue to need it every day. Frozen storage at -20°C to -40°C also stays relevant for plasma products, vaccine variants, and specimen archiving, but it does not face the same degree of capital intensity as the ultra-low tier.

Cryogenic storage at or below -150°C is projected to grow at a 5.87% CAGR through 2031, which is the fastest rate across temperature sub-segments. That pace reflects the spread of advanced therapy workflows that need vapor-phase liquid nitrogen conditions and tighter chain-of-custody requirements. The United States medical cold storage market is therefore being reshaped by a two-speed temperature structure where ultra-low remains the core revenue base and cryogenic storage defines the highest strategic growth. This split is important because it changes vendor priorities, site planning, and service needs at the same time. Buyers are no longer looking only for temperature performance, but also for documentation, energy profile, facility fit, and refrigerant compliance within each range.

That shift has wider implications for competition and replacement cycles. Ultra-low systems face immediate pressure from operating cost concerns and refrigerant transitions, while cryogenic systems face stronger pressure from workflow design and patient-specific handling. Cryometrix’s T-90 platform illustrates the push toward closed-loop, LN2-free cryogenic approaches that address containment and compliance needs in a differentiated way. In practical terms, the US medical cold storage industry is moving toward more specialized product stacks inside each temperature band. The deeper the storage requirement, the more likely equipment qualification becomes tied to end-use process design rather than only to generic capacity needs.

By Application: Vaccines Lead by Volume, Cell Therapies Lead by Strategic Value

Vaccines held 38.72% share in 2025, which made them the largest application area in the United States medical cold storage market. Their lead came from breadth, because institutional immunization programs, retail pharmacy participation, and distributed provider networks create a wide base of monitored storage demand. This application remains resilient because vaccine programs require purpose-built units and continuous temperature tracking across thousands of care sites. The installed vaccine base gives the United States medical cold storage market steady replacement demand, even when growth in other therapeutic categories is more concentrated. It also reinforces demand for monitoring systems because mixed product inventories raise the cost of temperature excursions and documentation gaps.

Recent product approvals show why this category remains operationally complex. Merck’s ENFLONSIA approval for the 2025-2026 RSV season added another cold-chain product to pediatric and preventive care workflows. Bavarian Nordic’s freeze-dried JYNNEOS approval in March 2025 also changed storage protocol requirements relative to the previous liquid-frozen formulation. These examples show that even established vaccine categories can reset equipment specifications and handling procedures. In the United States medical cold storage market, that makes vaccine demand stable in volume but still active in replacement and monitoring upgrades.

Cell and gene therapies are forecast to grow at a 6.97% CAGR through 2031, which makes them the fastest-expanding application. This segment is smaller today, but it carries much higher strategic value because each patient-specific workflow places greater demands on storage precision, labeling, and custody control. The United States medical cold storage market is gaining disproportionate value from this application because cryogenic storage demand can rise faster than patient volume in autologous therapy models. Cryoport reported support for more than 250 commercially sponsored CGT clinical trials in the United States in 2026, which underlines the scale of advanced therapy activity feeding storage demand. Blood and blood components remain a large adjacent application with monitoring needs shaped by blood bank standards, while medications, biologics, and laboratory specimens form a steady middle layer across the United States medical cold storage market.

What separates the advanced therapy category is the structure of demand, not only the growth rate. A vaccine refrigerator can serve multiple products and many doses at once, but autologous cell therapy storage often reserves a specific cryogenic position for an individual patient lot. That creates a non-linear demand pattern for cryogenic capacity, especially at outsourced manufacturing sites and treatment networks. The result is that the application mix in the United States medical cold storage market is shifting toward higher-value storage positions even before advanced therapies dominate total volume. This is why the segment has become central to long-term product strategy among specialized vendors and biopharma-linked equipment suppliers.

By End User: Hospitals Anchor Volume, Outsourced Biomanufacturers Drive Cryogenic Growth

Hospitals and health systems held 45.82% of United States medical cold storage market share in 2025, which made them the largest end-user group. Their lead reflects the breadth of storage needs across pharmacy refrigerators, blood bank units, laboratory freezers, and walk-in cold rooms inside a single organization. The United States medical cold storage market remains anchored by this segment because hospitals combine routine clinical demand with high compliance exposure. Joint Commission requirements around emergency refrigeration continuity reinforce this position by turning storage performance into an operational readiness issue, not just a facilities purchase. Pharmacies and vaccination sites also form a large volume tier, but their specifications are more standardized, and their capital intensity is lower than that of large acute care systems.

Academic and research laboratories make up another important layer of demand. Their buying behavior is shaped by a mix of research continuity, sustainability policies, and temperature documentation expectations. The UCSB TGIF program, which offered a USD 4,000 rebate for replacing aged ULT freezers with ENERGY STAR models, shows how institutions are using policy-linked incentives to accelerate selective replacement. In the United States medical cold storage market, this segment does not grow as fast as advanced therapy outsourcing, but it supports a broad installed base of ultra-low equipment and monitoring upgrades. Blood banks and transfusion centers add a stable compliance-led demand stream because equipment replacement there is closely tied to traceability and continuous monitoring expectations.

CROs, CMOs, and cell therapy processing sites are projected to grow at a 7.35% CAGR through 2031, which is the fastest pace among end users. This reflects the outsourcing shift in advanced therapy manufacturing, where cryogenic and ultra-low capacity is being concentrated in specialized facilities instead of being dispersed across many smaller in-house sites. The United States medical cold storage market is therefore gaining a new growth center in facilities that pair bioprocessing with tightly controlled storage and chain-of-custody systems. Thermo Fisher Scientific’s 2026 investments in biologics development infrastructure and process-linked manufacturing support that direction because they deepen the tie between cold storage and outsourced therapy production. As this outsourced layer expands, the United States medical cold storage market is likely to see a larger share of capital flow toward specialized high-density sites rather than evenly across traditional healthcare buyers.

This shift also affects how pharmaceutical and biotechnology companies use storage capacity. More of these companies are aligning storage decisions with development and manufacturing partners instead of building every layer of biorepository infrastructure internally. That reduces the need for broad in-house duplication while increasing the need for validated partner networks. In the US medical cold storage industry, this favors vendors and service providers that can serve multi-site outsourced models with consistent documentation and performance. It also strengthens the role of cryogenic and remote-monitoring solutions in end-user segments that are already growing faster than the hospital base.

Geography Analysis

The United States medical cold storage market shows its heaviest demand concentration in the Northeast corridor, where Greater Boston, New York and New Jersey, Philadelphia, and the Research Triangle host dense clusters of academic medicine, biologics activity, and advanced therapy processing. This region matters because it combines high research intensity with a large number of facilities that face constant accreditation, documentation, and cold-chain performance expectations. Thermo Fisher Scientific opened its flagship U.S. Bioprocess Design Center in Plainville, Massachusetts, in April 2026, which reinforced the region’s role as a center for biologics-linked infrastructure and cold-storage-integrated process development. The Northeast also fits the growth profile of the United States medical cold storage market because advanced therapy programs there depend on both ultra-low and cryogenic capacity. Dense provider networks and specialized research sites make this region especially supportive of monitoring systems, validated storage, and higher-specification replacement cycles.

The Midwest and Sun Belt form the next demand tier, but the mix is different. These geographies combine large hospital networks, research institutions, and steadily growing life science activity with a stronger focus on cost discipline and resilience planning. In the United States medical cold storage market, there are opportunities for the replacement of aging installed bases as well as new capacity tied to biomanufacturing expansion. Disaster resilience requirements are more important in Gulf Coast and hurricane-exposed states, where backup refrigeration and continuity planning carry greater operational weight under hospital standards.

California is a distinct demand pole inside the United States medical cold storage market because it combines a major biopharmaceutical presence with more careful environmental considerations. Cryoport said in its first quarter 2026 results that it plans to open a Global Supply Chain Center in Santa Ana in the fourth quarter of 2026, which reflects growing cryogenic logistics and storage requirements on the West Coast. California buyers also face more direct pressure from refrigerant transition planning because compliance timing and low-GWP product availability have become central parts of capital decisions. That raises procurement complexity in the state, but it also pulls forward the adoption of newer systems that align with future refrigerant rules. The result is that the United States medical cold storage market has three clear geographic patterns, which are a compliance-intensive Northeast, a replacement and resilience-oriented Midwest and Sun Belt, and a California market shaped by both biopharma density and faster refrigerant transition pressure.

Regional demand is therefore not uniform, even though the market is national in scope. The same core drivers operate across the country, but their weight changes with research concentration, weather risk, advanced therapy exposure, and site engineering requirements. This is why geography in the United States medical cold storage market is better understood through end-use intensity and compliance complexity than through simple population measures. Regions with stronger biologics and CGT ecosystems are more likely to accelerate cryogenic and ultra-low deployment, while broader healthcare regions remain more tied to refrigeration, vaccine storage, and replacement-led upgrades.

Competitive Landscape

The United States medical cold storage market shows moderate concentration, with a leading group that includes Thermo Fisher Scientific and PHC Holdings Corporation, alongside specialized participants such as Helmer Scientific, Eppendorf SE, Haier Biomedical, Cryoport, and niche cryogenic providers. Competition is not based on cabinet supply alone, because buyers increasingly want compliance support, remote diagnostics, energy efficiency, and workflow fit in the same purchase decision. That gives larger and better-established vendors an advantage in the United States medical cold storage market, especially in regulated applications where qualification risk is high. Thermo Fisher Scientific strengthened its position in April 2026 by opening its flagship U.S. Bioprocess Design Center in Massachusetts, which linked cold-storage capability more directly with end-to-end biologics development infrastructure. The company also completed the acquisition of Clario Holdings in March 2026, which added data and trial support capabilities that can complement compliance-heavy cold-chain environments.

PHC Holdings Corporation is differentiating through product architecture rather than scale alone. Its TwinGuard ECO 703VXH combines natural refrigerants, dual-compressor redundancy, remote diagnostics, and optional identity-based access controls, which aligns with energy, audit, and chain-of-custody requirements in one product line. That matters in the United States medical cold storage market because procurement teams increasingly prefer systems that reduce the need for separate compliance and monitoring add-ons after installation. Cryoport is taking a different route, expanding through cryogenic specialization and connected platforms. Its Fusion 800 Series and MVE HE line, both highlighted in the first quarter 2026 disclosures, show how the company is targeting facilities that need advanced cryogenic storage with remote oversight and operational continuity. Specialized vendors such as Cryometrix add another layer of competition by focusing on differentiated technologies like closed-loop cryogenic systems that address containment and compliance concerns in narrower but high-value niches.

The most open space in the United States medical cold storage market sits where traditional product categories do not fully solve emerging workflow problems. One gap is cryogenic capability at distributed hospital administration sites for autologous therapies, where receiving and short-duration holding needs are rising faster than installed vapor-phase capability. A second gap sits in decentralized clinical trial support, where storage verification and documentation must extend beyond large facilities into local delivery settings under the FDA’s 2024 final guidance. A third gap is lower-total-cost replacement for aging ULT assets in budget-constrained hospitals and rural health systems, where need is clear but conversion remains slow. These gaps explain why the United States medical cold storage market is competitive, but not commoditized, because growth is favoring vendors that can align equipment with real-world compliance, energy, and workflow constraints.

Entry barriers remain meaningful. Standards and qualification expectations keep buyers focused on vendors with known validation histories, dependable service, and documented monitoring capability. That supports pricing power for established manufacturers even though the field still includes several credible specialists. As a result, the United States medical cold storage market continues to reward breadth and compliance depth, while leaving focused room for cryogenic and digital-monitoring innovators.

United States Medical Cold Storage Industry Leaders

BioLife Solutions, Inc.

Eppendorf SE

Haier Biomedical

PHC Holdings Corporation

Thermo Fisher Scientific Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Thermo Fisher Scientific opened its flagship United States Bioprocess Design Center in Plainville, MA, expanding cold-storage-integrated biologics development infrastructure for CDMOs and biopharmaceutical customers.

- April 2026: BioLife Solutions won the INTERPHEX 2026 Biotech Innovation Award for its CellSeal CryoCase, a rigid cryogenic containment system purpose-built for frozen biologics, supporting visual inspection for container integrity under GMP frameworks.

- March 2026: Thermo Fisher Scientific completed the acquisition of Clario Holdings for USD 8.8 billion, adding endpoint data solutions for clinical trials, with direct relevance to cold-chain compliance documentation requirements for decentralized and traditional clinical settings

United States Medical Cold Storage Market Report Scope

The Medical Cold Storage Market encompasses the industry providing temperature-controlled infrastructure like medical-grade refrigerators, ultra-low temperature (ULT) freezers, and refrigerated warehouses used to safely preserve and transport temperature-sensitive healthcare goods. It ensures the efficacy of vaccines, biologics, and pharmaceuticals by preventing degradation.

The United States Medical Cold Storage Market is Segmented by Product Type (Refrigerators, Freezers, Cryogenic Storage, Walk-ins, Monitoring Systems), Temperature Range (CRT, Refrigerated, Frozen, Ultra-Low, Cryogenic), Application (Vaccines, Blood Components, Biologics, Cell/Gene Therapies, Lab Specimens, Organs/Tissues), End User (Hospitals, Pharmacies, Blood Banks, Labs, Pharma/Biotech, CROs/CMOs), Geography (US). Forecasts in Value (USD).

| Medical-Grade Refrigerators | Pharmacy / Vaccine Refrigerators |

| Blood Bank Refrigerators | |

| Laboratory / General-Purpose Refrigerators | |

| Medical-Grade Freezers | Low-Temperature Freezers (-20°C to -40°C) |

| Ultra-Low Temperature Freezers (-60°C to -90°C) | |

| Cryogenic Storage Systems (≤-150°C) | |

| Walk-in Cold Rooms & Chambers | |

| Monitoring Systems & Accessories |

| Controlled Room Temperature / Ambient |

| Refrigerated (+2°C to +8°C) |

| Frozen (-20°C to -40°C) |

| Ultra-Low (-60°C to -90°C) |

| Cryogenic (≤-150°C) |

| Vaccines |

| Blood & Blood Components |

| Medications & Biologics |

| Cell & Gene Therapies |

| Laboratory / Diagnostic Specimens |

| Organs & Tissues |

| Hospitals & Health Systems |

| Pharmacies & Vaccination Sites |

| Blood Banks & Transfusion Centers |

| Academic & Research Laboratories |

| Pharmaceutical & Biotechnology Companies |

| CROs, CMOs & Cell Therapy Processing Sites |

| By Product Type | Medical-Grade Refrigerators | Pharmacy / Vaccine Refrigerators |

| Blood Bank Refrigerators | ||

| Laboratory / General-Purpose Refrigerators | ||

| Medical-Grade Freezers | Low-Temperature Freezers (-20°C to -40°C) | |

| Ultra-Low Temperature Freezers (-60°C to -90°C) | ||

| Cryogenic Storage Systems (≤-150°C) | ||

| Walk-in Cold Rooms & Chambers | ||

| Monitoring Systems & Accessories | ||

| By Storage Temperature Range | Controlled Room Temperature / Ambient | |

| Refrigerated (+2°C to +8°C) | ||

| Frozen (-20°C to -40°C) | ||

| Ultra-Low (-60°C to -90°C) | ||

| Cryogenic (≤-150°C) | ||

| By Application | Vaccines | |

| Blood & Blood Components | ||

| Medications & Biologics | ||

| Cell & Gene Therapies | ||

| Laboratory / Diagnostic Specimens | ||

| Organs & Tissues | ||

| By End User | Hospitals & Health Systems | |

| Pharmacies & Vaccination Sites | ||

| Blood Banks & Transfusion Centers | ||

| Academic & Research Laboratories | ||

| Pharmaceutical & Biotechnology Companies | ||

| CROs, CMOs & Cell Therapy Processing Sites | ||

Key Questions Answered in the Report

What is the projected value of United States medical cold storage by 2031?

The United States medical cold storage market is projected to reach USD 1.56 billion by 2031, rising from USD 1.24 billion in 2026 at a 4.8% CAGR over 2026 to 2031.

Which product category leads revenue in United States medical cold storage?

Medical-grade freezers were the largest product type in 2025 with 52.43% share, reflecting broad demand across blood, biologics, and research preservation needs.

Which application is growing fastest in United States medical cold storage?

Cell and gene therapies are forecast to expand at a 6.97% CAGR through 2031, supported by rising cryogenic handling needs and patient-specific storage requirements.

Why are monitoring systems becoming more important in medical cold storage?

Monitoring systems and accessories are projected to grow at a 6.36% CAGR because facilities need automated logs, alarms, and audit-ready records under tighter compliance expectations.

How are refrigerant rules affecting equipment purchases in the United States?

EPA transition rules are raising procurement complexity because buyers must balance current needs with lower-GWP requirements that tighten further by 2032, especially for large cold rooms and ULT systems.

Page last updated on: