United States Patient Temperature Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

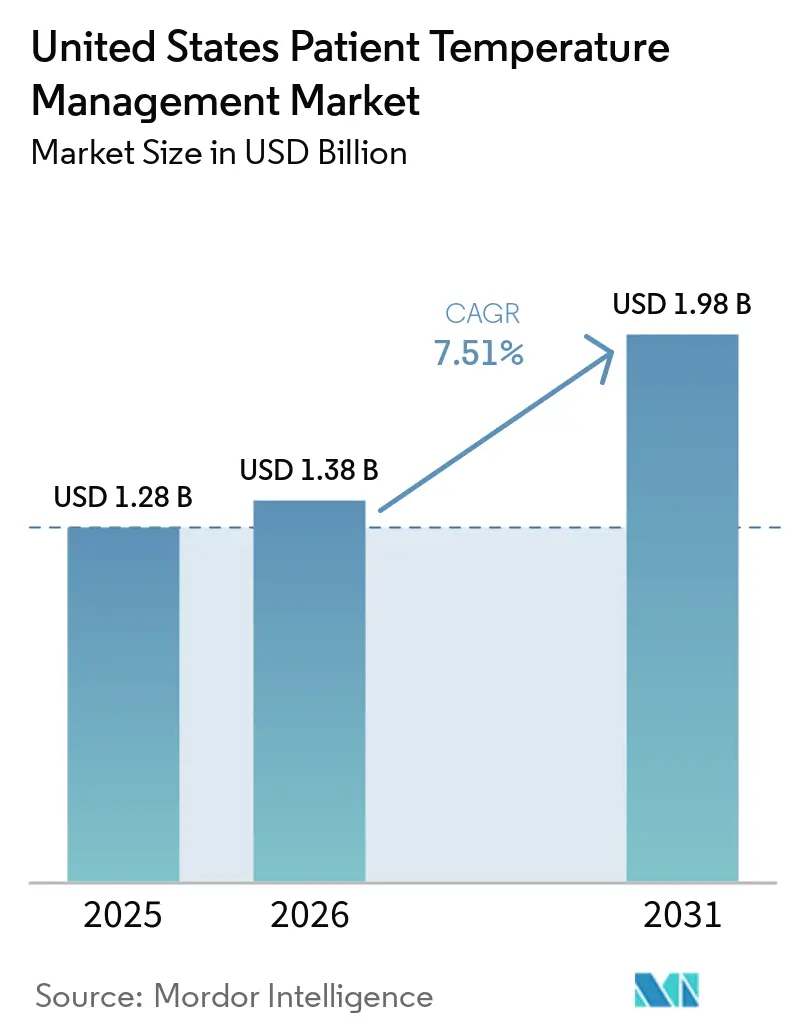

| Base Year Market Size (2025) | USD 1.28 Billion |

| Market Size (2026) | USD 1.38 Billion |

| Market Size (2031) | USD 1.98 Billion |

| Growth Rate (2026 - 2031) | 7.51% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Patient Temperature Management Market Analysis by Mordor Intelligence

The United States Patient Temperature Management Market size was valued at USD 1.28 billion in 2025 and is estimated to grow from USD 1.38 billion in 2026 to reach USD 1.98 billion by 2031, at a CAGR of 7.51% during the forecast period (2026-2031).

Growth in the United States (US) patient temperature management market is being supported by the steady shift of higher-acuity procedures into ambulatory and outpatient settings, where compact warming systems fit faster case turnover and tighter room layouts. The US patient temperature management market is also benefiting from stronger enforcement of perioperative normothermia protocols, which is making active temperature control a routine part of quality-linked care pathways in surgery and recovery settings. A second layer of demand is coming from cardiac ICU and neurocritical care pathways, where guideline-driven fever avoidance now requires continuous and automated temperature control rather than occasional manual intervention. Hospital replacement demand is also becoming more selective, with buyers favoring closed-loop and dual-mode platforms that can support both warming and cooling workflows on the same control architecture. Smaller hospitals and independent outpatient operators are still absorbing the reimbursement and compliance effect of these changes, which is likely to keep procurement discipline high even as the US patient temperature management market expands.

Key Report Takeaways

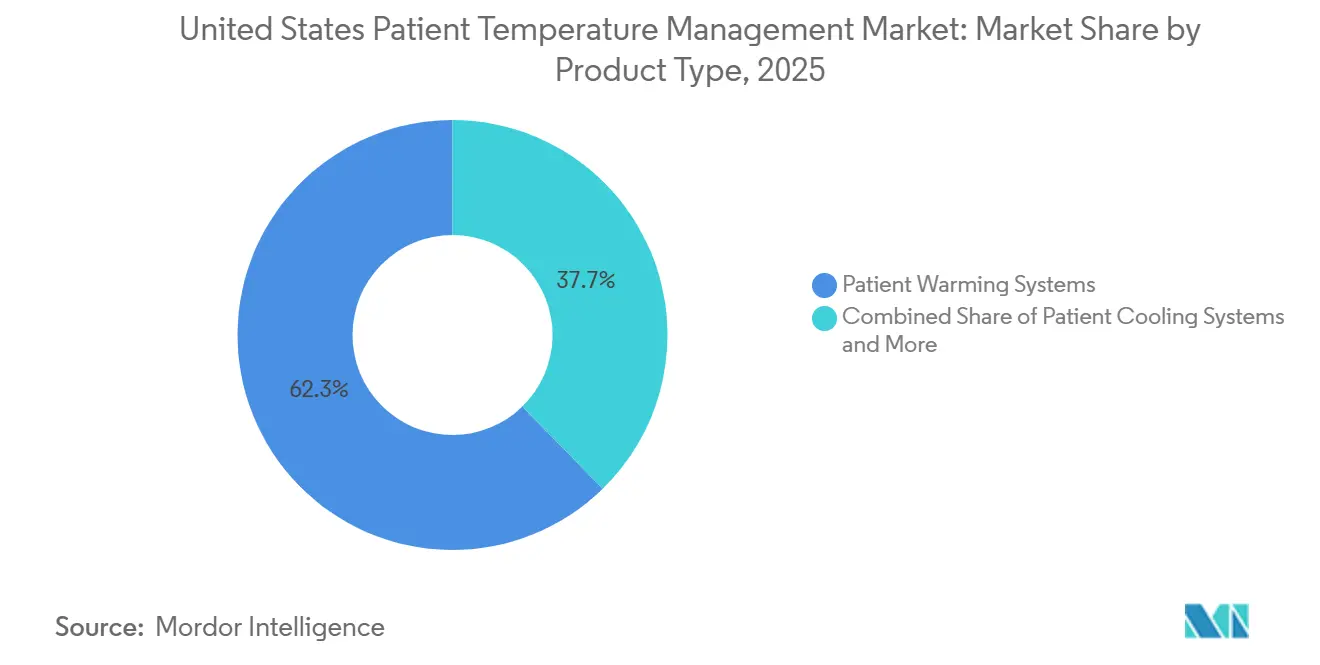

- By product type, Patient Warming Systems held 62.31% of 2025 revenue and also recorded the highest projected CAGR at 8.38% through 2031.

- By application, Perioperative Care accounted for 53.24% of 2025 revenue, while Neurology and Neurocritical Care is forecast to expand at an 8.52% CAGR through 2031.

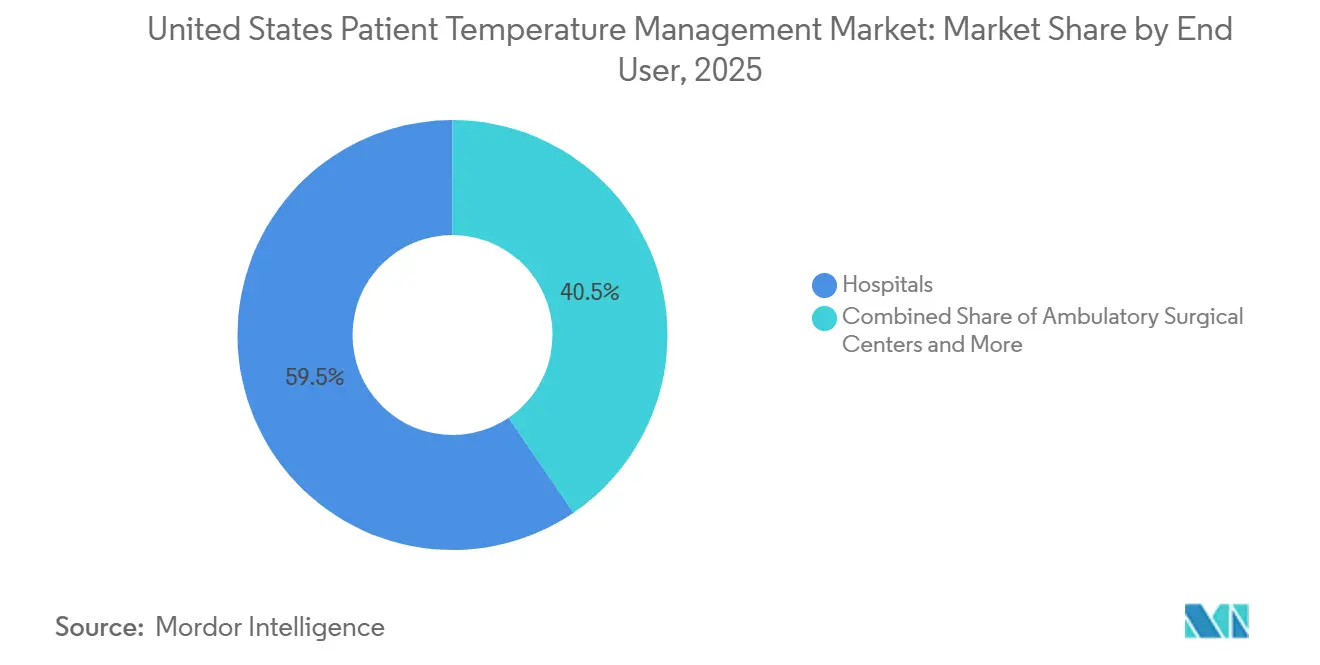

- By end user, Hospitals held 59.52% of 2025 revenue, while Ambulatory Surgical Centers are projected to grow at a 9.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Patient Temperature Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Surgical Volumes And Perioperative Normothermia Protocols | +1.8% | National, with early concentration in high-ASC states including Texas, Florida, and California | Short term (≤ 2 years) |

| Higher Cardiac-Arrest And Neurocritical-Care Temperature-Control Use | +1.2% | National, with above-average uptake in academic medical centers | Medium term (2-4 years) |

| Closed-Loop And Dual-Mode Platform Upgrades | +1.5% | National, hospital-centric, strongest in urban tertiary centers | Medium term (2-4 years) |

| NICU Thermoregulation Monitoring Upgrades | +0.8% | National, concentrated in Level III-IV NICUs | Medium term (2-4 years) |

| ASC Migration Favoring Compact Rapid-Turnover Warming Workflows | +1.2% | National, accelerating in Sun Belt and Midwest ASC clusters | Short term (≤ 2 years) |

| Portable Blood And Fluid Warming In EMS And Military Transport | +0.6% | Federal procurement channels, with civilian EMS demand concentrated in rural trauma corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes And Perioperative Normothermia Protocols

The US patient temperature management market is seeing broad support from rising surgical activity in outpatient settings, where portable and rapid-cycle warming systems are easier to deploy than fixed hospital-style equipment. Outpatient facilities now handle more than 80% of surgical procedures in the United States, which has shifted a larger share of device demand toward smaller footprints and faster room turnover. MedPAC reported that ASC procedure volume per Medicare beneficiary grew 3.4% in 2024, which was well above the 2019-2023 average annual rate of 1.0%[1]MedPAC, “Ambulatory Surgical Center Services: Status Report,” MedPAC, medpac.gov.. That migration is changing procurement behavior because many ASC locations now weigh per-case cost and operational simplicity more heavily than feature density. AORN reported in 2025 that 90.35% of outpatient facility respondents used forced-air warming systems, which shows how deeply warming devices are embedded in perioperative workflows even amid litigation noise. The US patient temperature management market is also gaining from stronger compliance pressure around perioperative temperature control, which supports recurring disposable demand as much as capital equipment placement.

Higher Cardiac-Arrest And Neurocritical-Care Temperature-Control Use

The US patient temperature management market is also being lifted by updated post-resuscitation guidance that requires active fever prevention after cardiac arrest rather than simple observation. The 2025 American Heart Association guidance recommends preventing fever at or below 37.5°C for at least 72 hours in adults who remain comatose after return of spontaneous circulation. European guidance published in Intensive Care Medicine in 2025 aligns with that approach, which keeps device demand intact even as the clinical focus shifts away from routine deep hypothermia[2]Robert Greif et al., “European Resuscitation Council and European Society of Intensive Care Medicine Guidelines 2025, Post-Resuscitation Care,” Intensive Care Medicine, springer.com.. In neurocritical care, updated consensus recommendations continue to favor automated feedback-controlled temperature management for intracerebral hemorrhage, subarachnoid hemorrhage, and acute ischemic stroke patients who require ICU admission. Severe traumatic brain injury care is following the same pattern, with controlled normothermia recognized as a therapeutic option in advanced ICU protocols. This widens the addressable pool for the US patient temperature management market beyond surgical warming and ties growth more closely to critical care pathways.

Closed-Loop And Dual-Mode Platform Upgrades

The US patient temperature management market is moving toward platform upgrades that let clinicians manage more than one temperature-control modality through a single system. Hospitals are increasingly favoring units that can shift between surface and intravascular treatment without changing the controller, which reduces hardware duplication and simplifies staff training. ZOLL received FDA clearance and CE Mark in January 2024 for its Thermogard HQ platform expansion, which combined intravascular catheter-based and surface pad-based temperature control in one platform. Gentherm reinforced the same direction in February 2026 when it submitted a 510(k) notification for ThermAffyx, a system that combines patient warming and securement for robotic-assisted surgery. These launches show that procurement is shifting toward devices that solve multiple clinical tasks rather than offering stand-alone temperature control alone. For the US patient temperature management market, that shift raises the advantage of vendors that can connect data into hospital dashboards and quality workflows while also reducing room-level equipment clutter.

NICU Thermoregulation Monitoring Upgrades

The US patient temperature management market is also gaining from NICU upgrades, where hospitals are moving from single-step warming approaches toward broader thermoregulation systems. A 2026 multicenter randomized clinical trial in JAMA Network Open reported that many very preterm infants still arrived outside the normal thermal range of 36.5-37.5°C despite current bundle interventions. ILCOR’s 2025 neonatal life support recommendations continued to support wraps, thermal mattresses, heated humidified gases, and radiant warmers in combination for preterm infants below 34 weeks’ gestation. That clinical direction is pushing Level III and Level IV NICUs toward incubator, radiant warmer, servo-control, and humidification combinations rather than single-device solutions. A 2025 quality improvement study in the Journal of Perinatology Practices and Quality Standards found better normothermia compliance after standardizing open-crib transition protocols that included thermostat calibration and servo-controlled temperature weaning. As a result, the US patient temperature management market is seeing a steadier replacement cycle in neonatal care, especially for hybrid systems that also support monitoring and transport.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital And Disposable Costs | -0.9% | National, with greater pressure on rural hospitals and independent ASCs | Medium term (2-4 years) |

| Recalls And Fluid-Warmer Safety Risks | -0.7% | National, most acute in facilities with high fluid-warming volumes | Short term (≤ 2 years) |

| Forced-Air Infection-Control Litigation In Implant-Heavy ORs | -0.8% | National, concentrated in orthopedic and joint-replacement ORs | Long term (≥ 4 years) |

| Legacy Controller Footprints And Service Complexity | -0.5% | National, most acute in community and critical-access hospitals | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital And Disposable Costs

Capital intensity remains a real brake on the US patient temperature management market, especially for dual-mode and closed-loop platforms that require a larger up-front commitment. Smaller hospitals and independent ASCs have to balance those capital costs against narrower budgets and lower qualifying case volumes. The burden does not stop at the controller because intravascular catheters, gel pads, warming blankets, and fluid-warming sets create recurring spend with every case. That pressure is harder to absorb when facilities are paid through bundled outpatient structures instead of separate reimbursement for temperature-control products. Independent ASC operators are especially price sensitive, which often pushes them toward single-vendor disposable contracts and slows adoption of newer systems from smaller suppliers. Leasing and subscription models help in some cases, but uptake has been uneven, so cost remains a clear restraint on the US patient temperature management market.

Recalls And Fluid-Warmer Safety Risks

The US patient temperature management market also faces pressure from recalls and product safety events, which can delay purchasing even when clinical demand remains firm. The FDA posted a Class 1 recall in 2025 for the 3M Ranger Blood and Fluid Warming High Flow Set because of concerns tied to flow rate and inlet fluid temperature labeling. The agency also posted Class 2 recalls in 2025 for rapid infuser disposable sets with connector issues that could lead to fluid leaks during priming. In 2024, the BD Arctic Sun Temperature Management System was subject to a Class 2 recall related to a software issue that could prevent an alert when target water temperature was not reached. These events make biomedical teams more cautious and increase the amount of documentation they seek during contract reviews. The short-term effect on the US patient temperature management market is slower ordering and more scrutiny, even though the longer-term result can favor established vendors with stronger post-market support records.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Warming Holds The Lead While Higher-Value Cooling Platforms Gain Depth

Patient Warming Systems held 62.31% of the US patient temperature management market share in 2025, and the segment is also projected to grow at an 8.38% CAGR through 2031. That combination shows that warming remains the operational backbone of the US patient temperature management market across perioperative care, critical care, and neonatal use. The installed base is expanding in 2 ways at the same time, with higher disposable pull-through at existing accounts and new placements in ASCs and specialty clinics. Forced-air warming remains the most common modality by installed base, supported by the 2025 AORN survey showing use in 90.35% of outpatient facilities[3]Association of periOperative Registered Nurses, “2025 Patient Warming Survey,” Outpatient Surgery Magazine, aorn.org.. Conductive and resistive warming systems are also gaining traction where infection-control concerns are changing preference in orthopedic operating rooms, and a 2026 study in Scientific Reports found conductive warming could achieve outcomes comparable to forced-air warming when pre-warming was used.

Blood and IV-fluid warmers continue to serve a separate but important role in delivering normothermic fluids to hemorrhage and hypothermia-risk patients. That niche is supported by military trauma guidance that specifies warmed blood products at 38-42°C in battlefield and prehospital resuscitation scenarios. Neonatal warmers and hybrid incubator-warmer platforms are also benefiting from the broader NICU quality push, which is expanding the US patient temperature management industry into more integrated thermoregulation workflows. On the cooling side, patient cooling systems remain smaller by revenue, but they are gaining value in cardiac arrest and neurocritical care because precision servo-control and multimodality treatment are becoming more important in ICU practice.

By Application: Perioperative Care Drives Volume While Neurology Expands Faster

Perioperative Care accounted for 53.24% of the US patient temperature management market size in 2025, which made it the largest application segment by value. Its scale comes from the wide range of procedures that now require active temperature support across hospital operating rooms, ASC procedure rooms, and post-anesthesia care units. The clinical case for active warming remains strong because temperature loss begins early under anesthesia, and 2025 consensus work on perioperative thermoprotection again favored active warming over passive insulation across the care pathway. This broad procedural base gives the US patient temperature management market a large recurring demand pool that is less exposed to one specialty alone. Cardiac Arrest and Critical Care remains the second-largest application, and it is being reshaped by the shift from routine deep hypothermia toward controlled fever avoidance and normothermia maintenance.

Neurology and Neurocritical Care is the fastest-growing application at an 8.52% CAGR through 2031, which reflects growing use in stroke, hemorrhage, and traumatic brain injury pathways. Updated consensus recommendations support continuous automated feedback-controlled devices for major neurocritical conditions that require ICU admission. The same pattern appears in traumatic brain injury protocols, where controlled normothermia now sits inside structured ICP management approaches. Neonatal and pediatric care is also advancing as hospitals pursue better compliance with thermal targets at admission and during crib transition, while other applications provide a steady but slower tail for the US patient temperature management industry.

By End User: Hospitals Keep The Spending Base While ASCs Set The Growth Pace

Hospitals retained 59.52% of 2025 revenue in the US patient temperature management market, reflecting their role as the main buyers of capital-intensive warming and cooling platforms. Large hospital systems can spread device use across operating rooms, ICUs, PACUs, and NICUs, which supports broader platform standardization and steadier disposable demand. Their scale also gives them an advantage in negotiating blanket and accessory contracts, which tends to favor integrated vendors over narrower specialists. Accreditation expectations around surgical temperature monitoring reinforce this behavior and help protect baseline demand for active warming equipment in acute care settings. For that reason, hospitals remain the anchor customer group for the US patient temperature management market even when procurement becomes more selective.

Ambulatory Surgical Centers are forecast to grow at a 9.25% CAGR through 2031, making them the fastest-growing end-user category. MedPAC showed continued expansion in the number of Medicare-certified ASCs, with 6,436 facilities in 2024 and 6,566 by Q4 2025, which confirms the widening procedural base for outpatient warming demand. ASC buyers typically want compact systems with quick setup and simple turnover, which aligns well with forced-air warming and single-use resistive pad designs. Specialty clinics and other users, including transport operators and military medical settings, remain smaller in value but add targeted demand for portable fluid-warming products outside fixed care environments.

Geography Analysis

The US patient temperature management market shows a clear regional split between outpatient surgery growth, critical care burden, and neonatal service concentration. High-ASC states such as Texas, Florida, and California continue to shape demand for compact warming systems because outpatient facilities in those markets need faster turnover and lower equipment footprints. That gives the US patient temperature management market a strong base for portable and room-efficient warming products outside traditional hospital campuses. The Northeast shows a different profile because academic and teaching hospitals in states such as New York and Massachusetts have stronger demand for advanced cooling and closed-loop normothermia systems used in cardiac and neurocritical care. This makes regional demand less uniform and keeps product mix sensitive to local care settings rather than national averages alone.

The South carries the highest cardiac arrest age-adjusted mortality rate among U.S. Census regions at 6.9 per 100,000 population, while the West recorded 2.2 per 100,000 in the 2025 Journal of Clinical Medicine analysis. Alabama had the highest state-level rate at 36.5 per 100,000 in the same analysis. The CARES 2024 Annual Report also showed out-of-hospital cardiac arrest survival at 9.7%-11.0% across covered populations, with major state-level variation in bystander CPR rates from 23.4% to 79.7%. These differences matter because they shape how many patients reach facilities that can use controlled temperature management after resuscitation. In parts of the South, community hospitals still represent a larger refresh opportunity for the US patient temperature management market because device penetration in advanced normothermia systems appears lower than in large academic centers.

Neonatal demand follows another map that is tied to the distribution of higher-level NICUs. A study of 1,424 operational NICUs found that the Southeast held 26% of all units, while the Midwest and West each held 22%. A JAMA Network Open cohort study found that 74.4% of urban birth hospitals offered higher-level neonatal care by 2022, compared with only 16.9% of rural birth hospitals. That rural gap creates a practical need for transport-capable neonatal warming systems, while urban academic centers are more likely to upgrade to hybrid incubator-warmer platforms with integrated monitoring and transfer capability. This leaves the US patient temperature management market with distinct urban replacement demand and rural transport-related demand rather than one uniform neonatal purchasing pattern.

Competitive Landscape

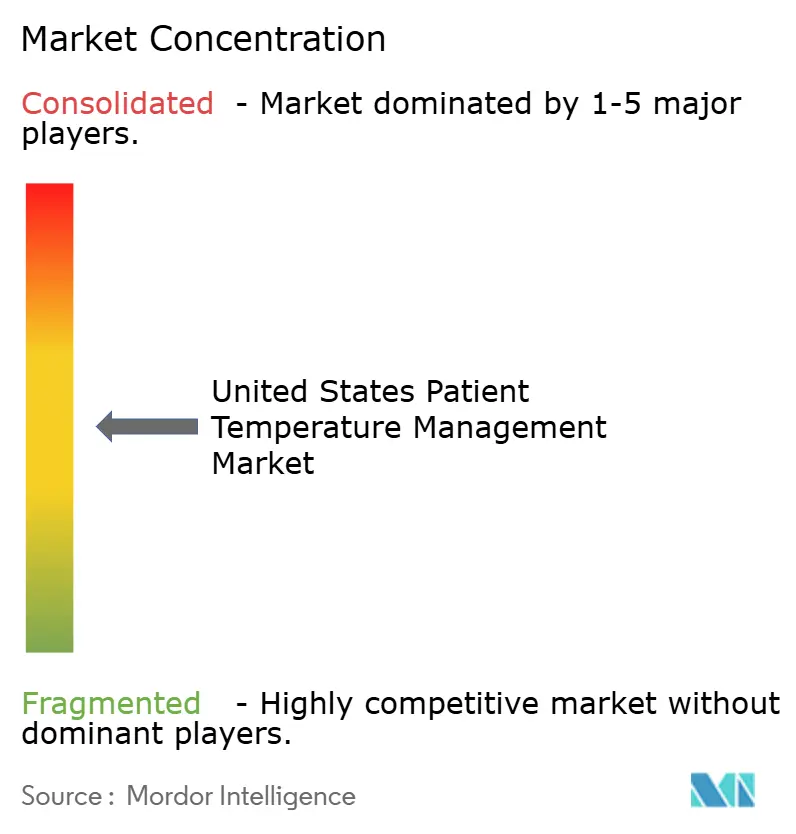

The US patient temperature management market is moderately concentrated, with a small group of global medtech companies holding strong positions across the main warming and cooling categories. Solventum, through the Bair Hugger franchise, and Gentherm, through Blanketrol and ASTOPAD, remain central to the warming side of the US patient temperature management market. ZOLL and BD lead much of the advanced cooling and targeted temperature management segment through Thermogard and Arctic Sun, especially in critical care settings. This structure leaves room for specialized companies, but the core platform business still sits with vendors that can support controllers, disposables, service, and clinician training at scale. The result is a competitive field where broad portfolios matter more than single-product presence.

Strategic differentiation is shifting from basic device performance toward platform flexibility and workflow fit. ZOLL’s Thermogard HQ expansion is a good example because it lets providers use intravascular and surface modalities on the same platform, which supports ICU standardization and reduces equipment switching. Gentherm’s February 2026 ThermAffyx submission also points to a different form of competition in the US patient temperature management market, where warming is being combined with securement and robotic surgery workflow needs rather than sold as a stand-alone function. Xodus Medical moved in the same direction with the Hot Pink Pad, which combines conductive warming and anti-slide positioning in a single-use format aimed at operating room efficiency. These moves show that vendors are trying to win clinical workflows, not just device tenders.

The competitive picture is also being shaped by litigation, recalls, and the need for stronger post-market support. Ongoing forced-air warming litigation has kept infection-control concerns visible in implant-heavy operating rooms, which has helped conductive and resistive alternatives gain more attention. At the same time, FDA recall activity across warming and cooling categories has made procurement teams more cautious and has raised the value of established service organizations. In the US patient temperature management market, this favors companies that can show platform reliability, safety follow-up, and a clearer upgrade path rather than relying on price alone.

United States Patient Temperature Management Industry Leaders

Solventum Corporation

Gentherm Incorporated

ZOLL Medical Corporation (Asahi Kasei Corporation)

Stryker Corporation

Smiths Medical (ICU Medical)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Xodus Medical launched the Hot Pink Pad following FDA 510(k) clearance, combining carbon-based conductive underbody warming with clinically proven anti-slide positioning technology in a single-use surgical pad. The product addresses two simultaneous surgical risks, inadvertent perioperative hypothermia and hospital-acquired pressure injuries, reducing the number of separate devices needed per procedure and accelerating OR turnaround workflows.

- February 2026: Gentherm Incorporated submitted a 510(k) premarket notification to the FDA for the ThermAffyx Patient Safety System, a first-of-its-kind integrated patient warming and securement platform designed for robotic-assisted surgery. Gentherm plans market launch in the third quarter of 2026, targeting the expanding robotic surgery segment where positioning and warming have historically been managed by separate, incompatible devices.

United States Patient Temperature Management Market Report Scope

As per the scope of the report, patient temperature management refers to the practice of monitoring and regulating a patient's body temperature to maintain it within a normal or desired range. This involves the use of various techniques and devices to prevent hypothermia (abnormally low body temperature) or hyperthermia (abnormally high body temperature), thereby supporting optimal physiological functioning and improving clinical outcomes.

The segmentation for the United States patient temperature management market is categorized by product type, application, and end user. By product type, the market includes patient warming systems, such as forced-air warming systems, conductive and resistive warming systems, blood and IV-fluid warmers, neonatal warmers and hybrid incubator-warmer platforms, and integrated table-based and dual-mode warming systems. It also includes patient cooling systems, such as surface cooling systems, intravascular cooling systems, and selective and targeted cooling systems, along with accessories and disposables. By application, the market is segmented into perioperative care, cardiac arrest and critical care, neurology and neurocritical care, neonatal and pediatric care, and other applications. By end user, the market is divided into hospitals, ambulatory surgical centers, specialty clinics, and other end users. For each segment, the market size and forecast are provided in terms of value (USD).

| Patient Warming Systems | Forced-air Warming Systems |

| Conductive and Resistive Warming Systems | |

| Blood and IV-Fluid Warmers | |

| Neonatal Warmers and Hybrid Incubator-Warmer Platforms | |

| Integrated Table-based and Dual-mode Warming Systems | |

| Patient Cooling Systems | Surface Cooling Systems |

| Intravascular Cooling Systems | |

| Selective and Targeted Cooling Systems | |

| Accessories & Disposables |

| Perioperative Care |

| Cardiac Arrest and Critical Care |

| Neurology and Neurocritical Care |

| Neonatal and Pediatric Care |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| Other End Users |

| By Product Type | Patient Warming Systems | Forced-air Warming Systems |

| Conductive and Resistive Warming Systems | ||

| Blood and IV-Fluid Warmers | ||

| Neonatal Warmers and Hybrid Incubator-Warmer Platforms | ||

| Integrated Table-based and Dual-mode Warming Systems | ||

| Patient Cooling Systems | Surface Cooling Systems | |

| Intravascular Cooling Systems | ||

| Selective and Targeted Cooling Systems | ||

| Accessories & Disposables | ||

| By Application | Perioperative Care | |

| Cardiac Arrest and Critical Care | ||

| Neurology and Neurocritical Care | ||

| Neonatal and Pediatric Care | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| Other End Users | ||

Key Questions Answered in the Report

What is driving growth in U.S. patient temperature management through 2031?

Growth is being supported by expanding outpatient surgery, stronger perioperative normothermia compliance, wider use in cardiac arrest and neurocritical care, and hospital upgrades to closed-loop platforms. The market is projected to reach USD 1.98 billion by 2031 at a 7.51% CAGR.

Which product category leads spending in patient temperature management in the United States?

Patient Warming Systems lead the category with 62.31% of 2025 revenue, and they are also the fastest-growing product type with an 8.38% CAGR through 2031.

Why are ambulatory surgical centers becoming important buyers of warming systems?

ASCs are the fastest-growing end-user segment at a 9.25% CAGR through 2031. Their growth is tied to rising outpatient surgical volumes and a preference for compact systems that support fast room turnover.

Which clinical application is growing the fastest in this field?

Neurology and Neurocritical Care is the fastest-growing application segment, with an 8.52% CAGR through 2031, supported by guideline-based use of automated temperature control in stroke, hemorrhage, and brain injury care.

Why do hospitals still account for the largest share of spending?

Hospitals held 59.52% of 2025 revenue because they use temperature management across operating rooms, ICUs, PACUs, and NICUs, and they are the main buyers of capital-intensive intravascular cooling and large warming fleets.

What are the main risks affecting supplier performance in this space?

The main risks are high capital and disposable costs, device recalls, fluid-warmer safety concerns, and litigation pressure around forced-air warming in implant-heavy operating rooms. These factors can slow purchasing even when clinical demand stays firm.

Page last updated on: