Pharmaceutical Stability & Storage Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

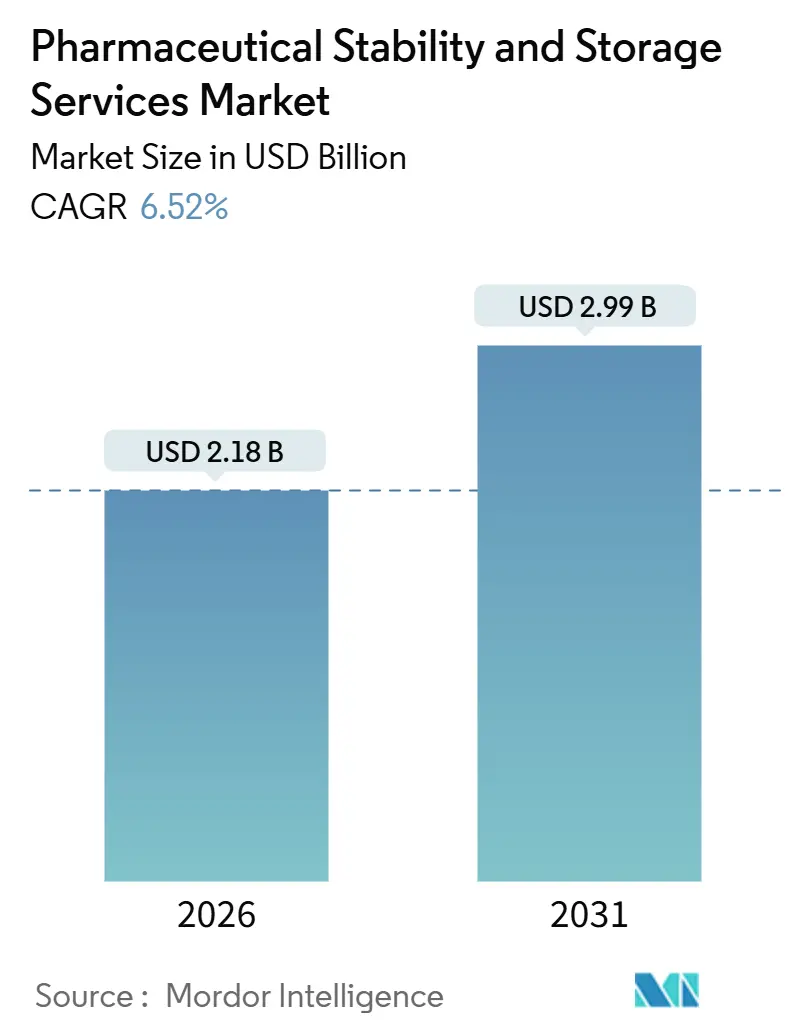

| Market Size (2026) | USD 2.18 Billion |

| Market Size (2031) | USD 2.99 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

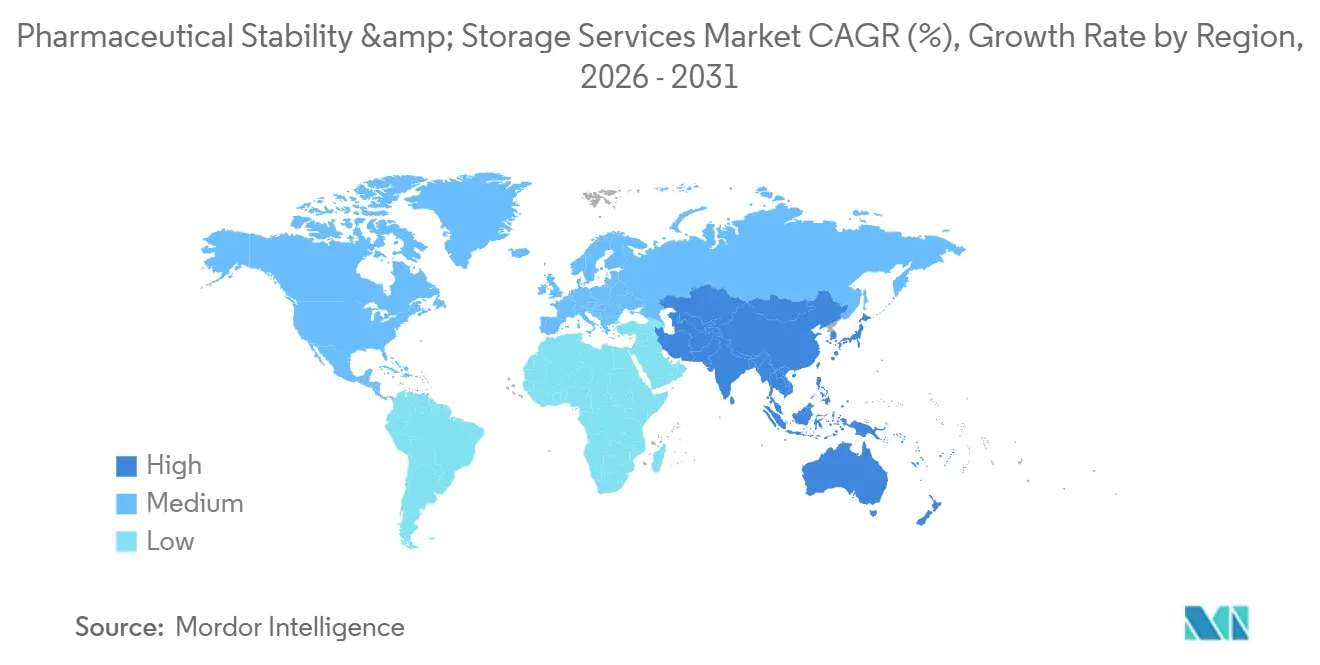

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pharmaceutical Stability & Storage Services Market Analysis by Mordor Intelligence

The Pharmaceutical Stability & Storage Services Market size is estimated at USD 2.18 billion in 2026, and is expected to reach USD 2.99 billion by 2031, at a CAGR of 6.52% during the forecast period (2026-2031).

Major providers are retrofitting chambers to meet the growing demand for facilities capable of handling biologics at minus 80 °C, cell therapies, and mRNA vaccines, while smaller labs are exiting these capital-intensive segments. Regulatory convergence, driven by the 2025 draft consolidation of ICH Q1 guidelines, enables a single stability dossier to fulfill the requirements of the FDA, EMA, and NMPA. This development reduces redundant long-term studies and shortens global filing timelines by up to 18 months. Enhanced operational visibility, supported by IoT sensors and AI-driven analytics, allows for the prediction of degradation events, streamlining accelerated studies and minimizing sample pulls. However, the European energy shock of 2024–2025 has increased cold-room operating costs, accelerating the adoption of high-efficiency freezers and renewable energy contracts.

Key Report Takeaways

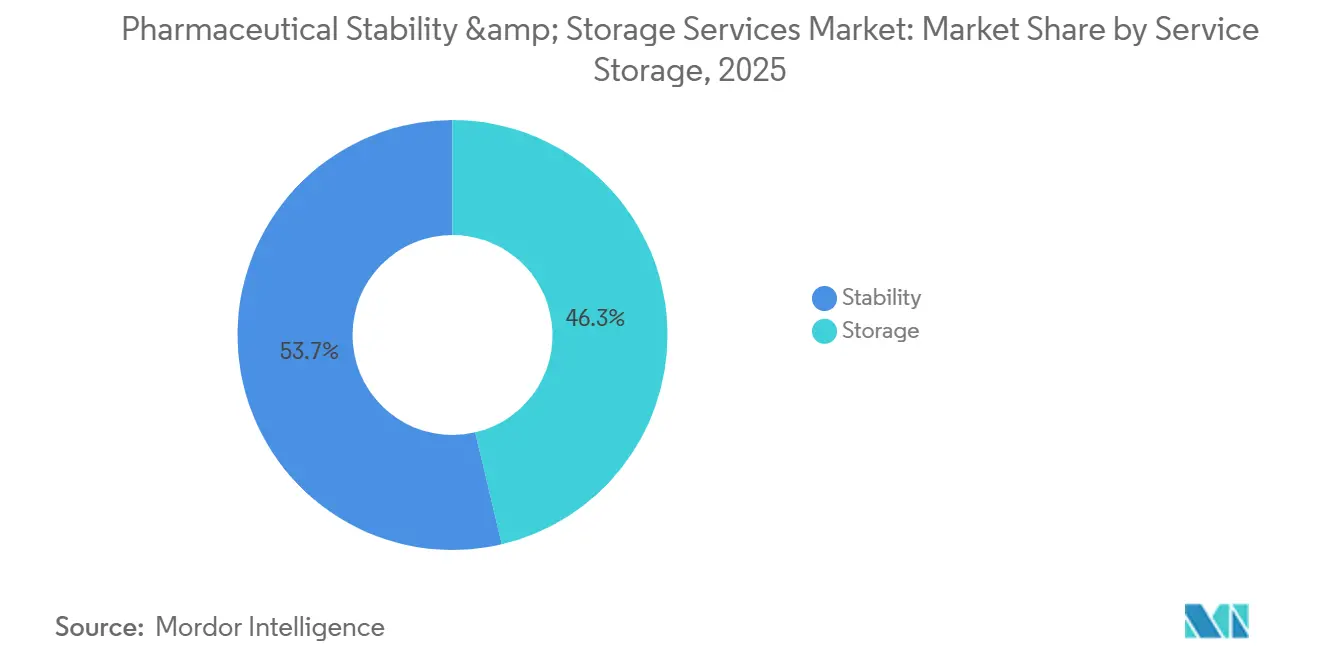

- By service, stability testing held 53.67% of the pharmaceutical stability & storage services market share in 2025, while storage is advancing at an 8.54% CAGR through 2031.

- By molecule type, large molecules captured 47.65% of the pharmaceutical stability & storage services market in 2025 and are expanding at a 8.87% CAGR through 2031.

- By geography, North America contributed 42.56% revenue in 2025; Asia-Pacific is the fastest-growing region with a 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pharmaceutical Stability & Storage Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global pharmaceutical production volumes | +1.2% | Global, with concentration in APAC and North America | Medium term (2–4 years) |

| Proliferation of temperature-sensitive biologic therapies | +1.8% | North America & EU core, expanding to APAC | Long term (≥ 4 years) |

| Intensifying regulatory focus on product quality and integrity | +0.9% | Global, led by FDA, EMA, NMPA | Short term (≤ 2 years) |

| Outsourcing trend across drug development and manufacturing | +1.3% | Global, strongest in North America and Europe | Medium term (2–4 years) |

| Advancements in cold-chain storage and monitoring technology | +0.7% | North America & EU early adoption, APAC following | Medium term (2–4 years) |

| Growing complexity of worldwide distribution networks | +0.6% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Pharmaceutical Production Volumes

Worldwide drug-manufacturing output rose 7.2% year-over-year in 2025, driven by biosimilar launches and shifts in generic production to India and Southeast Asia[1]United Nations Industrial Development Organization, “Pharmaceutical Production Index 2025,” unido.org. Each new drug substance requires at least three ICH-compliant long-term studies, plus accelerated and intermediate protocols, resulting in 18–24 data points per product. Eurofins responded by commissioning 12 new walk-in chambers across Europe in 2024, boosting capacity 14%. Continuous-manufacturing lines further heighten testing frequency because real-time release hinges on ongoing stability verification. As batch volumes climb, contract labs are adding modular suites that can be validated in weeks rather than months, keeping pace with production surges.

Proliferation of Temperature-Sensitive Biologic Therapies

Biologic entities accounted for 38% of FDA approvals in 2025, and nearly all require storage at 2–8 °C or colder. mRNA vaccines and many cell therapies require minus-80 °C freezers, an infrastructure gap that legacy small-molecule labs cannot fill without multimillion-dollar upgrades. Cryoport reported a 41% jump in validated shipper deployments during 2025, underscoring the surge in ultra-cold logistics. A single walk-in freezer at minus 80 °C can cost USD 150,000–250,000, and redundancy doubles that outlay, creating a barrier that favors established providers. The FDA’s 2024 draft on temperature management now mandates real-time electronic monitoring, lifting compliance costs yet raising service quality standards.

Intensifying Regulatory Focus on Product Quality and Integrity

Global regulators issued 1,847 quality-related letters in 2024, a 19% jump from 2023. The FDA now requires 6-month interim stability updates for new applications, accelerating sample throughput demands. China’s tiered inspection framework assigns facilities to risk categories that trigger unannounced audits every 18 months for top-tier sites. EMA adoption of ICH Q12 in 2025 permits post-approval stability-protocol changes without prior approval if a robust quality system is in place. Continuous monitoring systems compliant with ISO 17025 are thus becoming a baseline expectation, forcing small labs either to invest or exit.

Outsourcing Trend Across Drug Development and Manufacturing

Virtual biotech firms and mid-cap pharma lack internal stability infrastructure, so they increasingly outsource to CDMOs that bundle testing with manufacturing services. Catalent’s 2024 bankruptcy and subsequent USD 16.5 billion acquisition by Novo Holdings highlighted the strategic value of integrated stability capabilities. Sponsors can avoid USD 2–4 million in capital outlay per Phase II program by using third-party chambers, preserving cash for trials. Outsourcing is most pronounced in rare-disease pipelines where low patient numbers render in-house suites uneconomical. Improved regulatory acceptance of third-party electronic records, codified by the FDA in 2024, removed a longstanding friction point.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure for cGMP stability infrastructure | -0.8% | Global, acute in emerging markets (India, Latin America, MEA) | Medium term (2–4 years) |

| Rising operational costs of energy-intensive cold storage | -0.6% | Europe & North America primary, spreading to APAC | Short term (≤ 2 years) |

| Limited availability of specialized technical workforce | -0.5% | Global, most severe in North America and Europe | Medium term (2–4 years) |

| Fragmented regulatory requirements across regions | -0.4% | Global, particularly affecting sponsors in multi-region trials (FDA, EMA, NMPA, ANVISA jurisdictions) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure for cGMP Stability Infrastructure

Building a compliant stability suite costs USD 3–7 million and includes walk-in chambers, HVAC with ±2 °C tolerance, backup power, and electronic monitoring. Photostability chambers alone can reach USD 120,000 each, and operators often keep five units online to avoid study delays. Annual requalification costs USD 25,000 per chamber, while any deviation triggers a root-cause analysis that can idle capacity for weeks. Emerging-market labs average 2 chambers, compared with more than 6 in U.S. peers, limiting throughput and deterring multinational sponsors. Financing remains tough because lenders assign low collateral values to specialized chambers, leading to higher interest rates than for general commercial loans.

Rising Operational Costs of Energy-Intensive Cold Storage

Cold facilities consume 150–200 kWh per m² annually, triple ambient requirements, and European energy prices jumped 22% during 2024–2025. A bank of 20 freezers at -80 °C can rack up a monthly electricity bill of USD 40,000. The EU carbon border tax introduced in 2024 added 8% to operating costs for German and Dutch providers[2]European Commission, “Carbon Border Adjustment Mechanism Guidance,” europa.eu. Upgrading to vacuum-insulated panels and variable-speed compressors cuts power draw by 28% but needs USD 0.5–1.2 million per site. California’s 2025 Title 24 code now mandates an 85 kBtu/ft² ceiling for new pharmaceutical cold stores, pushing firms toward on-site solar or long-term green-energy contracts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Storage Segment Accelerates as Sponsors Defer Capital

The storage segment of the pharmaceutical stability & storage services market is advancing at an 8.54% CAGR through 2031 as sponsors defer in-house cold-room investments[3]Parenteral Drug Association, “Cold Chain Outsourcing Survey 2025,” pda.org. Stability testing still accounts for 53.67% of 2025 revenue because every regulatory dossier requires ICH-compliant data, yet its mature profile limits incremental expansion. Outsourced cold facilities offer contingency inventory buffers against temperature excursions, an urgent need for cell and mRNA products that spoil within hours outside the 80 °C range. A 2025 Parenteral Drug Association survey showed 68% of biotech firms now outsource at least half of their cold storage, up from 42% in 2022. Within storage, ultra-low chambers claim the largest capital influx, while ambient generics continue to use conventional warehouses.

Accelerated stability tests conducted at 40 °C and 75% relative humidity are in greater demand following the FDA's 2025 approval of interim approvals based on such data. Photostability protocols increased by 14% year over year as packaging scrutiny intensified. Analytical-method validation workloads rose with complex combination products, stretching project timelines by up to 12 weeks. AI models that predict degradation could reduce physical sample volumes and reshape long-term capacity planning if regulators accept in-silico data, as early pilots with Sanofi suggest.

By Molecule: Large Molecules Drive Premium Services

Large molecules led the pharmaceutical stability & storage services market with 47.65% revenue in 2025 and are projected to grow at 8.87% annually through 2031. Their demanding minus-80 °C or vapor-phase nitrogen profiles command service fees 40–60% higher than for small-molecule testing. Monoclonal antibodies require aggregation monitoring via size-exclusion chromatography and dynamic light scattering, consuming more analyst hours than typical HPLC assays. Cell and gene therapies, though fewer in approvals, require cryogenic storage at temperatures below -150 °C with redundant alarm systems, which boost infrastructure costs.

Small molecules still generate high sample counts, driven by the volume of generic approvals—782 ANDAs cleared in 2024. Forced-degradation studies for poorly soluble oncology actives can run USD 80,000 per compound and extend 16 weeks. Once three years of real-time data are logged, many commercial small molecules qualify for reduced testing, easing annual budgets by up to 30%. The FDA’s 2024 gene-therapy guidance, which mandates potency assays at every time point, widens the price gulf between molecule categories.

Geography Analysis

North America generated 42.56% of 2025 revenue in the pharmaceutical stability & storage services market, supported by 48% of global Phase III trials and a dense biomanufacturing base. The FDA’s new semi-annual stability reporting has made proximity to domestic labs more attractive, curbing cold-chain risks. Canada and Mexico are adding capacity as manufacturers diversify supply chains; Mexico’s pharma exports rose 11% in 2024, fueling stability demand in Nuevo León and Jalisco. Energy incentives in Texas and North Carolina are drawing new cold-storage foot-prints, while California’s strict energy code raises build-out costs but appeals to firms targeting sustainability benchmarks.

Europe remains a mature but dynamic contributor. EMA adoption of ICH Q12 in 2025 allows protocol changes without prior review, favoring providers that can update digital records in real time. Germany, France, and the United Kingdom account for 58% of regional revenue thanks to legacy manufacturing sites near Frankfurt, Lyon, and Cambridge. Energy inflation after the 2024 gas-price spike pushed operators to invest in vacuum-panel freezers and on-site photovoltaics, lowering operating costs over five-year horizons. Cryoport’s Paris hub, inaugurated in August 2024, filled a critical ultra-cold gap for EU cell-therapy developers.

Asia-Pacific is the fastest-growing region at 7.54% CAGR. China’s 68 innovative drug approvals in 2024 generated fresh long-term stability obligations, expanding domestic demand. India remains cost-competitive; Eurofins added 8 chambers across Bangalore and Hyderabad in 2025 to address backlogs in bioequivalence studies. Japan and South Korea are scaling cryogenic sites to manage regenerative-medicine approvals, whereas Australia supports global Phase I trials through rapid-turnaround programs under the TGA notification route. The Middle East, Africa, and South America combined account for under 15% of revenue but show strategic investments, such as Saudi Arabia’s USD 1.2 billion biopharma plan and Brazil’s tropical-condition chambers calibrated to 30 °C and 75% RH.

Competitive Landscape

The pharmaceutical stability & storage services market exhibits moderate concentration. The top five providers accounted for 38% of revenue in 2025, leaving room for regional specialists. Thermo Fisher’s AI-assisted stability models, co-developed with Sanofi, aim to cut accelerated studies in half and could reset service benchmarks if regulators endorse predictive outputs. Eurofins and SGS continue expanding their footprints in India and Brazil to capture cost-sensitive generic pipelines. Charles River implemented robotic sample handlers in Massachusetts in 2024, trimming labor costs by 19% and reducing contamination incidents.

Catalent’s 2024 bankruptcy and Novo Holdings’ USD 16.5 billion takeover temporarily displaced USD 400 million in annual stability contracts, which mid-tier players like PCI Pharma Services and Recipharm quickly absorbed. Cryoport dominates global cell-therapy logistics but serves only 28 countries, creating opportunities for local cold-chain specialists. Patent activity remains low—14 USPTO filings in 2024–2025—so competitive advantage relies on operational quality, geographic reach, and digital transparency rather than proprietary hardware. ISO 17025 and FDA readiness pose high fixed costs, and annual compliance spending above USD 100,000 discourages small entrants.

Pharmaceutical Stability & Storage Services Industry Leaders

Catalent

Charles River Laboratories

Eurofins Scientifi

SGS

Almac Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Astoriom expanded its sample management capabilities in the US with the acquisition of Precision Stability Storage. This acquisition marks a strategic expansion of Astoriom’s footprint in North America, strengthening its presence in high-growth regions for biopharmaceutical, biotechnology, and medical technology innovation.

- November 2024: Novo Holdings finalized a USD 16.5 billion acquisition of Catalent, adding 120 stability chambers to its network

Global Pharmaceutical Stability & Storage Services Market Report Scope

As per the scope of the report, pharmaceutical stability & storage services involve specialized testing and monitoring to ensure the quality, efficacy, and safety of pharmaceutical products over time. These services include stability testing, storage condition management, and data analysis to comply with regulatory standards. They help manufacturers verify product shelf life and maintain optimal storage conditions throughout the supply chain.

The Pharmaceutical Stability & Storage Services Market is Segmented by Service (Stability: Drug Substance, Stability-Indicating Method Validation, Accelerated Stability Testing, Photostability Testing, and Other Stability Testing Methods, and Storage: Cold and Non-Cold), Molecule (Small Molecule: Research Products and Commercial Products, and Large Molecule: Research Products and Commercial Products), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Stability | Drug Substance |

| Stability-Indicating Method Validation | |

| Accelerated Stability Testing | |

| Photostability Testing | |

| Other Stability Testing Methods | |

| Storage | Cold |

| Non-Cold |

| Small Molecule | Research Products |

| Commercial Products | |

| Large Molecule | Research Products |

| Commercial Products |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest Of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest Of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest Of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest Of South America |

| By Service | Stability | Drug Substance |

| Stability-Indicating Method Validation | ||

| Accelerated Stability Testing | ||

| Photostability Testing | ||

| Other Stability Testing Methods | ||

| Storage | Cold | |

| Non-Cold | ||

| By Molecule | Small Molecule | Research Products |

| Commercial Products | ||

| Large Molecule | Research Products | |

| Commercial Products | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest Of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest Of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest Of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest Of South America | ||

Key Questions Answered in the Report

What is the forecast value of the pharmaceutical stability & storage services market in 2031?

The pharmaceutical stability & storage services market is projected to reach USD 2.99 billion by 2031.

Which service category is growing fastest?

Outsourced storage, particularly ultra-cold rooms, is expanding at an 8.54% CAGR through 2031.

Why are large molecules driving higher service fees?

Monoclonal antibodies and cell therapies demand minus 80 ¡C or colder storage plus specialized analytical methods that raise unit costs.

How are regulations changing stability-testing timelines?

The FDA now requires 6-month interim data, and the 2025 ICH consolidation reduces redundant regional studies, accelerating submissions.

What technology trends are reshaping stability services?

IoT sensors, AI-based predictive models, and vacuum-insulated freezers are cutting energy use and shortening accelerated studies.

Which regions present the highest growth potential?

Asia-Pacific leads with a 7.54% CAGR due to manufacturing expansion in China and India alongside streamlined regulatory pathways.

Page last updated on: