Community Acquired Pneumonia Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

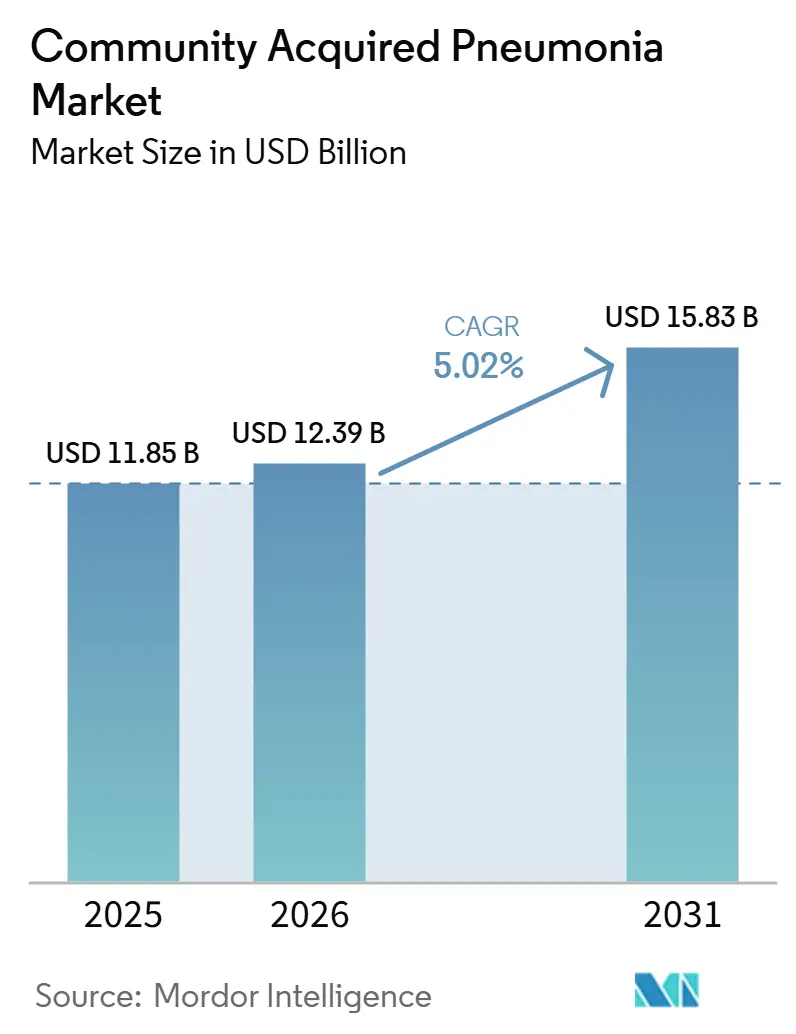

| Market Size (2026) | USD 12.39 Billion |

| Market Size (2031) | USD 15.83 Billion |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Community Acquired Pneumonia Market Analysis by Mordor Intelligence

The Community Acquired Pneumonia Market size was valued at USD 11.85 billion in 2025 and is estimated to grow from USD 12.39 billion in 2026 to reach USD 15.83 billion by 2031, at a CAGR of 5.02% during the forecast period (2026-2031).

The community-acquired pneumonia market is being supported by a rising disease burden in older adults and immunocompromised patients, who face higher hospitalization risk, longer recovery, and higher post-discharge mortality than the general population. The community-acquired pneumonia market is also benefiting from broader use of molecular respiratory panels, which shorten the time needed to identify pathogens and help clinicians move faster toward targeted treatment choices. Vaccine policy is adding another layer of support because adult pneumococcal recommendations have widened, and next-generation pediatric candidates are moving through pivotal development, which keeps prevention programs active across age groups. The community-acquired pneumonia market is also seeing more selective competition, with novel antibiotics, vaccines, and decentralized diagnostics shaping different parts of the value chain at the same time. At the same time, delayed diagnosis, resistance pressure, and the high cost of severe care continue to limit access and slow the pace at which newer products convert clinical value into broader commercial uptake.

Key Report Takeaways

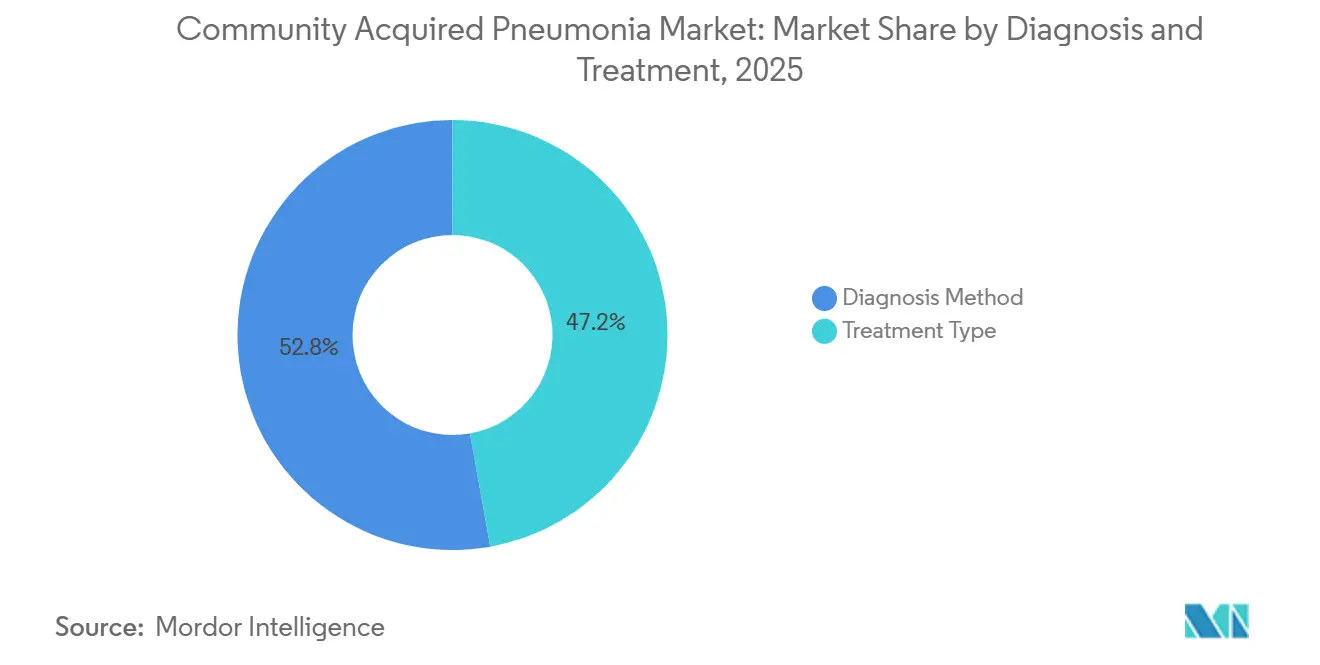

- By diagnosis and treatment, the diagnosis method held 52.83% of the community-acquired pneumonia market share in 2025, while the treatment type recorded the highest projected CAGR at 5.54% through 2031.

- By pathogen type, bacterial pneumonia accounted for 60.38% of the community-acquired pneumonia market size in 2025, while viral pneumonia is projected to expand at a 6.76% CAGR through 2031.

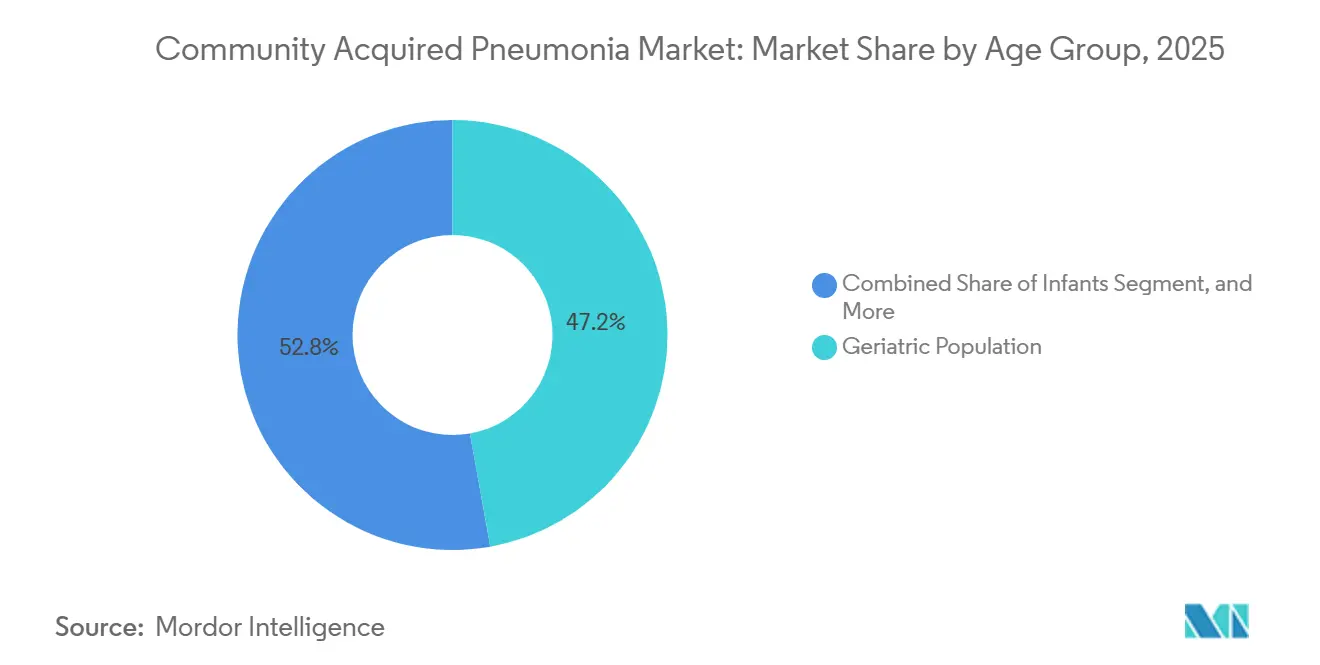

- By age group, the geriatric population led with a 47.16% share in 2025, while Infants posted the fastest growth at a 7.57% CAGR through 2031.

- By risk factors, chronic diseases captured 39.63% share in 2025, while weakened immune system is forecast to grow at a 5.94% CAGR through 2031.

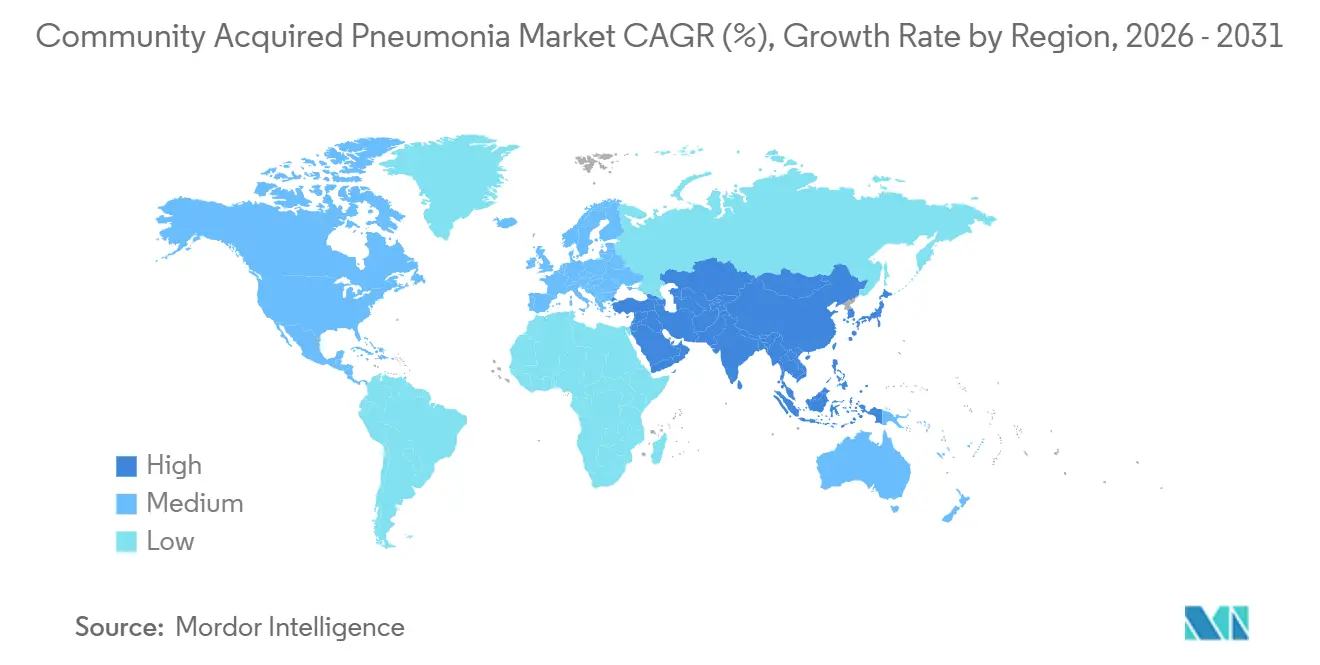

- By geography, North America led with 35.63% share in 2025, while Asia-Pacific is advancing at a 6.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Community Acquired Pneumonia Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising CAP burden in older and immunocompromised patients | +1.4% | Global, concentrated in North America, Western Europe, and major aging markets in Asia-Pacific | Long term (≥ 4 years) |

| Increasing antibiotic innovation for resistant respiratory pathogens | +0.9% | North America and Europe first, followed by Japan, South Korea, and Australia | Medium term (2-4 years) |

| Wider use of rapid diagnostics and imaging in early CAP workup | +0.8% | Global, with North America leading adoption and Asia-Pacific scaling fastest | Medium term (2-4 years) |

| Broader pneumococcal and respiratory vaccination adoption | +0.7% | Global, strongest in North America and Europe, with policy expansion in Asia-Pacific and South America | Long term (≥ 4 years) |

| Underuse of novel agents in outpatient step-down therapy | +0.6% | North America and Europe | Medium term (2-4 years) |

| Expansion of outpatient and home-based management pathways | +0.5% | North America, Europe, and selected Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising CAP Burden in Older and Immunocompromised Patients

The community-acquired pneumonia market is expanding with the steady rise in elderly and immunocompromised patients who face a higher risk of severe disease and repeat care episodes. A 2025 study in JAMA Network Open showed that adults aged 65 and older carried the heaviest hospitalization burden in the United States, and Streptococcus pneumoniae still caused 14% of cases despite broad vaccine use.[1]American Medical Association, “All-Cause and Pneumococcal Community-Acquired Pneumonia Hospitalizations Among Older US Adults,” JAMA Network Open, jamanetwork.com A 2025 meta-analysis in the European Journal of Internal Medicine found that 1 in 3 adults hospitalized for CAP died within the following year, with mortality rising from 5% in patients under 65 to 14% in those over 80 and reaching 43% in patients with multiple comorbidities.[2]Elsevier, “Comprehensive Management of Pneumonia in Older Patients,” European Journal of Internal Medicine, doi.org These outcomes keep demand strong for prevention, early diagnosis, inpatient treatment, and post-discharge management rather than limiting spending to the acute episode alone. The same pattern is reinforcing the role of the community-acquired pneumonia market in long-cycle care planning because transplant recipients, patients on immunosuppressive therapy, and people living with cancer or HIV present with broader pathogen diversity and higher treatment failure risk.

Increasing Antibiotic Innovation for Resistant Respiratory Pathogens

The community-acquired pneumonia market is also being shaped by antibiotic innovation as resistance weakens the reliability of older empiric regimens. A 2026 pooled analysis of the Phase 3 OPTIC and OPTIC-2 trials confirmed that omadacycline remained noninferior to moxifloxacin across a microbiologically diverse CABP population, including patients with pathogens showing reduced fluoroquinolone susceptibility. A 2026 paper in Antibiotics explained that newer agents such as lefamulin and omadacycline were designed to bypass resistance pathways that have reduced the utility of macrolides and fluoroquinolones in lower respiratory infections. Basilea Pharmaceutica started Phase 1 dosing for BAL2420 in 2026, and the added CARB-X funding showed continued support for first-in-class approaches against gram-negative resistance gaps that current approved agents do not fully address. As a result, the community-acquired pneumonia market is moving beyond simple class replacement and toward targeted therapies that can justify premium positioning when standard therapies fail.

Wider Use of Rapid Diagnostics and Imaging in Early CAP Workup

The community acquired pneumonia market is gaining from faster diagnostics because pathogen confirmation is moving closer to the initial care encounter. Roche received FDA clearance in 2025 for the cobas Respiratory 4-flex assay, which runs on existing cobas systems and supports broader high-throughput respiratory testing without requiring a full instrument replacement cycle.[3]Roche Diagnostics, “Roche's First Respiratory Test Powered by TAGS Technology Receives FDA Clearance,” Roche Diagnostics, diagnostics.roche.com bioMérieux received IVDR CE marking in 2026 for the BIOFIRE SPOTFIRE R/STplus panels, which extended near-patient respiratory testing options in Europe and strengthened the move toward quicker differentiation of respiratory etiologies.[4]bioMérieux S.A., “bioMérieux Receives IVDR CE-Marking for Two BIOFIRE SPOTFIRE Panels,” bioMérieux, biomerieux.com Faster identification changes treatment selection, reduces unnecessary broad-spectrum use, and makes outpatient care more practical for selected patients when clinicians can rule out uncertainty earlier. This keeps the community-acquired pneumonia market closely tied to molecular testing adoption because better diagnostics improve the commercial case for branded therapies that depend on timely pathogen recognition.

Broader Pneumococcal and Respiratory Vaccination Adoption

The community-acquired pneumonia market continues to benefit from vaccination policy because adult and pediatric prevention programs are widening at the same time. In 2024, ACIP expanded age-based pneumococcal conjugate vaccine recommendations to all adults aged 50 years and older, replacing a more selective framework that had limited routine uptake in practice. The same CDC-backed evidence showed that 90% of adults aged 50 to 64 who were hospitalized with pneumococcal pneumonia or invasive pneumococcal disease had at least 1 underlying risk condition, which supports the logic of earlier adult coverage. A 2025 review in Frontiers in Public Health found that herd protection from infant PCV programs did not fully cover older adults against important serotypes such as 3 and 19A, which keeps room open for adult-focused vaccine strategies. This is strengthening the community-acquired pneumonia market on the prevention side while also sustaining downstream use of diagnostics and therapeutics in settings where coverage gaps remain.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Antibiotic resistance reducing efficacy of standard regimens | -0.8% | Global, most acute in South Asia, Southeast Asia, and Sub-Saharan Africa | Long term (≥ 4 years) |

| Delayed or inaccurate diagnosis leading to non optimal treatment | -0.7% | Global, strongest in Asia-Pacific, the Middle East and Africa, and South America, with spillover into rural developed markets | Medium term (2-4 years) |

| High cost of severe care management and newer antibiotics | -0.6% | Global, especially restrictive in emerging markets | Long term (≥ 4 years) |

| Limited personalized treatment approaches for CAP subtypes | -0.4% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Antibiotic Resistance Reducing Efficacy of Standard Regimens

The community-acquired pneumonia market still faces a major barrier because resistance continues to erode the effectiveness of standard first-line regimens. A 2026 cross-sectional study of CAP isolated bacteria documented resistance across beta-lactams, macrolides, and fluoroquinolones, and prior antibiotic exposure closely tracked with those resistance patterns. When first-line therapy becomes less predictable, clinicians escalate more quickly to reserve agents, which increases treatment cost and creates more pressure on stewardship systems. Reimbursement pathways in many countries still move more slowly than resistance patterns, so newer branded drugs do not always gain commercial traction at the same pace as their clinical value. This keeps the community-acquired pneumonia market under pressure because demand for better treatment exists, but access rules, budget limits, and stewardship safeguards still slow broad adoption.

Delayed or Inaccurate Diagnosis Leading to Non-Optimal Treatment

The community-acquired pneumonia market is also constrained by the gap between diagnostic capability in hospitals and the reality of primary and outpatient care. France's HAS updated outpatient guidance in 2025 and continued to rely on probabilistic antibiotic prescribing in ambulatory CAP care, which showed that even advanced health systems still cannot confirm pathogens quickly in routine practice. A 2025 epidemiological study published through Epidemiology & Infection followed a large Chinese community cohort over more than 309,000 person-years and found a CAP incidence rate of 42.1 per 1,000 per year, with 39.2 cases managed only in outpatient settings, where confirmation is rarely performed before treatment begins. This pattern favors low-cost empiric antibiotics, delays use of advanced diagnostics, and reduces the share of cases that move toward targeted therapy. In lower resource parts of Asia-Pacific, the Middle East and Africa, and South America, the community-acquired pneumonia market remains limited by uneven imaging access and laboratory capacity, which makes diagnostic upgrade paths slower.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diagnosis & Treatment: Molecular Platforms Reshape CAP Workup

Diagnosis method held 52.83% share in 2025, which made it the largest part of this segmentation and a core spending anchor in the community-acquired pneumonia market. Chest X-ray remains the standard entry point because it is widely available, familiar to clinicians, and cost-efficient in both inpatient and outpatient settings. CT scanning is used more often in complex, recurrent, or immunocompromised presentations where plain imaging does not settle the differential diagnosis. Blood tests such as procalcitonin and C-reactive protein continue to support bacterial versus viral differentiation, while sputum culture remains important for resistance surveillance, and pulse oximetry supports fast severity stratification at triage. These tools keep the community-acquired pneumonia market grounded in established workflows even as higher-value molecular methods move into routine use.

Treatment type is projected to grow at a 5.54% CAGR through 2031, giving it the fastest growth profile within this category and linking more future value to care delivery than to test confirmation alone. Antibiotics still account for the largest share of treatment spending, and newer agents such as omadacycline and lefamulin are widening their role as hospitals respond to resistance risk and formulary needs. Oxygen therapy demand is also rising because more elderly patients present with greater severity and because home oxygen devices now support ambulatory management in selected lower acuity cases. Hospitalization is facing more cost pressure, which encourages wider use of severity scoring, remote follow-up, and ambulatory compatible therapies that reduce avoidable admissions.

By Pathogen Type: Viral Recognition Gaining Ground on Bacterial Dominance

Bacterial pneumonia held 60.38% of the community-acquired pneumonia market size in 2025, which kept it well ahead of every other pathogen category. Streptococcus pneumoniae remained the best-known single pathogen, and a 2025 study in JAMA Network Open found that it accounted for 14% of hospitalized CAP cases among older adults in the United States. A 2025 systematic review in the journal Pneumonia reported that non-vaccine serotypes, especially serotype 3, have re-emerged among elderly CAP patients since 2020, which keeps demand in place for broader vaccine coverage and pathogen-specific testing. Gram-negative pathogens such as Klebsiella pneumoniae and resistant Haemophilus influenzae are also taking a larger role in elderly and immunocompromised patients, which supports continued antibiotic innovation against harder-to-treat bacterial disease. For this reason, the community-acquired pneumonia market continues to derive a large share of commercial value from bacterial management even while the pathogen mix is gradually broadening.

Viral pneumonia is forecast to grow at a 6.76% CAGR through 2031, making it the fastest expanding pathogen group in the community-acquired pneumonia market. Better respiratory surveillance since the COVID period has increased the number of viral infections that are specifically identified rather than left in an unspecified CAP category. The spread of multiplex respiratory panels has also improved differentiation between viral, bacterial, and mixed infections, which is changing treatment decisions and epidemiological reporting patterns. Fungal Pneumonia remains smaller in volume but higher in value because immunocompromised patients need specialized diagnosis and treatment, especially for Aspergillus and Pneumocystis jirovecii. Atypical Pneumonia remains clinically important because organisms such as Legionella, Mycoplasma pneumoniae, and Chlamydophila pneumoniae respond poorly to beta lactams, which keeps accurate pathogen identification central to treatment quality in the community acquired pneumonia market.

By Age Group: Geriatric Priority Meets Accelerating Infant Immunization

The geriatric population held 47.16% of the community-acquired pneumonia market share in 2025, which made older adults the main commercial focus across vaccines, therapeutics, diagnostics, and supportive care. Older patients face a higher burden of hospitalization, more severe disease, and more difficult recovery, which keeps care intensity elevated even after discharge. A 2025 Frontiers in Medicine study found that malnutrition in elderly hospitalized CAP patients was independently associated with longer hospital stay, higher in-hospital mortality, and greater 30 day readmission risk, with low serum albumin and hemoglobin acting as independent predictors. Adults aged 18 to 64 still contribute a large outpatient volume because the cohort is broad, even though per capita severity is lower than in the geriatric group. Children remain a separate clinical group in the community-acquired pneumonia market because their protocols, vaccine patterns, and treatment choices differ materially from adult practice.

Infants are projected to grow at a 7.57% CAGR through 2031, which gives this sub-segment the fastest pace of expansion among age groups in the community-acquired pneumonia market. That growth is being supported by pediatric immunization policy, stronger clinical recognition of neonatal and infant respiratory infections, and the wider policy focus on reducing under-5 mortality. Pfizer advanced its 25-valent pediatric pneumococcal conjugate vaccine candidate into pivotal Phase 3 development in May 2026, with a trial that is recruiting around 3,230 infant participants against the currently licensed 20-valent standard. Pediatric management is also being shaped by the updated 2026 IDSA and PIDS guidance for infants and children older than 3 months, which helps standardize treatment expectations in major markets. As prevention programs broaden and clinical attention rises, the community-acquired pneumonia market is likely to see more sustained investment around infant vaccines, testing, and early treatment pathways.

By Risk Factors: Chronic Comorbidities Define Treatment Complexity

Chronic diseases accounted for 39.63% share in 2025, making comorbidity the largest risk linked to commercial clusters in the community-acquired pneumonia market. COPD, diabetes, and cardiovascular disease remain central because they increase susceptibility, complicate recovery, and often place CAP inside broader chronic care pathways rather than in isolation. CDC-backed evidence used by ACIP showed that 90% of adults aged 50 to 64 who were hospitalized with pneumococcal pneumonia or invasive pneumococcal disease had at least 1 underlying risk condition, which reinforces the close link between upstream chronic disease burden and downstream CAP demand. This creates workflow advantages for products that fit into existing respiratory, diabetes, or cardiac management systems instead of operating as standalone CAP tools. Smoking and alcoholism remain relevant in the community-acquired pneumonia market because they raise aspiration risk, impair mucociliary clearance, and increase vulnerability in specific adult patient groups, even where smoking prevalence is trending down.

Weakened immune system is expected to rise at a 5.94% CAGR through 2031, which makes it the fastest-growing risk factor group in the community-acquired pneumonia market. Growth in immunosuppressive therapy for cancer, autoimmune disease, transplantation, and HIV management is expanding the number of patients who present with atypical organisms, broader pathogen diversity, and higher treatment failure risk. APTARION Biotech AG completed enrollment in January 2026 for its Phase 2 ADCAP trial of AON-D21 in severe CAP across 5 European countries and the United States, and that program reflects growing interest in adjunct immune response management rather than pathogen targeting alone. This kind of immunomodulatory approach could create a new treatment layer for severe disease, especially where standard antibiotic escalation alone does not address the inflammatory burden. In practical terms, the community-acquired pneumonia industry is becoming more clinically complex in this group, and that complexity supports premium testing and treatment models that are harder to replicate with generic care pathways.

Geography Analysis

North America held 35.63% of the community-acquired pneumonia market share in 2025, which kept it in the lead among all regional groupings. The United States remains the key revenue engine because it combines advanced hospital infrastructure, strong vaccine policy, and active clinical development across therapeutics and diagnostics. ACIP expanded pneumococcal conjugate vaccine eligibility to all adults aged 50 years and older, which strengthened the long-term prevention base for adult disease management. Merck's CAPVAXIVE also added momentum after FDA approval, and the company stated that the vaccine covered 83% to 85% of invasive pneumococcal disease-causing serotypes in adults within this age group. Canada supports steady demand through universal coverage and cost-focused care models, while Mexico adds volume but remains less even in advanced diagnostics penetration.

Europe remained the second largest regional block in the community-acquired pneumonia market, supported by strong stewardship frameworks and steady vaccine and diagnostics demand. France updated outpatient CAP antibiotic guidance in 2025 and limited uncomplicated treatment to a maximum of 7 days, which reinforced faster de-escalation and sharper antibiotic selection. This can limit unit volumes for standard regimens, but it also strengthens the value proposition for rapid respiratory testing and better targeted therapies. Germany, the United Kingdom, Spain, and Italy continue to add meaningful demand across molecular diagnostics, adult vaccination, and hospital-based antibiotic use.

Asia-Pacific is forecast to grow at a 6.04% CAGR through 2031, making it the fastest expanding geography in the community-acquired pneumonia market. India remains important because of the high incidence, and broad public health programs keep both disease burden and treatment access initiatives elevated. A 2025 community study in China found a CAP incidence of 42.1 per 1,000 person-years, with most cases managed in outpatient settings without pathogen confirmation, which points to a large opening for point-of-care diagnostics. The Middle East and Africa, along with South America, still represent earlier-stage opportunities in the community-acquired pneumonia market because better laboratory networks, public procurement, and vaccine access are gradually improving the base for future diagnostics and treatment growth.

Competitive Landscape

The community acquired pneumonia market is moderately consolidated in therapeutics and more fragmented in diagnostics, so competitive intensity differs by product type. A smaller set of specialty drug companies holds differentiated antibiotic assets, while larger companies such as Merck, Pfizer, and GSK compete more visibly through vaccine portfolios and broader respiratory programs. In diagnostics, the field is wider, with Roche, bioMérieux, Thermo Fisher Scientific, QuidelOrtho, and other platform vendors competing on speed, breadth, and ease of deployment. This means the community acquired pneumonia market does not reward scale in the same way across every segment, because antibiotic, vaccine, and diagnostic economics remain structurally different. Companies that can connect faster testing to more confident treatment selection are gaining an advantage because hospitals increasingly value workflow efficiency along with clinical performance.

Recent strategic moves show how the community acquired pneumonia market is evolving around platform depth rather than single product launches alone. bioMérieux received IVDR CE marking in March 2026 for the BIOFIRE SPOTFIRE R/STplus Panel and R/STplus Panel Mini, which strengthened its near-patient respiratory testing presence in Europe. QuidelOrtho completed its acquisition of LEX Diagnostics in June 2026, adding the Velo multiplex RT-PCR point of care platform and reinforcing consolidation pressure in decentralized diagnostics. Pfizer also moved its 25-valent pediatric pneumococcal vaccine candidate into pivotal Phase 3 testing in 2026, which could sharpen competitive positioning in infant prevention over the medium term.

White space remains visible in host response management, severe disease adjuncts, and resistance-focused gram-negative coverage within the community-acquired pneumonia market. APTARION's AON-D21 is one example because it targets hyperinflammatory response in severe CAP instead of attacking the pathogen directly, which gives it a different competitive position from standard antibiotics. Basilea's BAL2420 is another example because it is being developed against gram-negative bacteria, including strains resistant to colistin, where approved CABP options do not fully cover the gap. As guideline alignment becomes more important in hospital purchasing and payer decisions, the community-acquired pneumonia market is likely to keep favoring companies that combine differentiated evidence with easier integration into routine respiratory care pathways.

Community Acquired Pneumonia Industry Leaders

AbbVie Inc.

Novartis AG

AstraZeneca plc

bioMérieux S.A.

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Pfizer initiated its pivotal Phase 3 pediatric trial for PF-07872412 (25vPnC), a 25-valent pneumococcal conjugate vaccine candidate, recruiting approximately 3,230 infant participants and comparing the candidate directly against the licensed 20-valent standard-of-care vaccine. This Phase 3 program follows robust Phase 2 immunogenicity results and positions Pfizer to challenge the infant pneumococcal vaccine segment.

- April 2026: Basilea Pharmaceutica dosed the first patient in its Phase 1 clinical study of BAL2420, a first-in-class LptA inhibitor antibiotic targeting gram-negative bacteria including carbapenem- and colistin-resistant strains. CARB-X awarded Basilea an additional USD 6 million in non-dilutive funding to support the trial, bringing total CARB-X commitment to USD 8.2 million.

- March 2026: bioMérieux received IVDR CE-marking for the BIOFIRE SPOTFIRE R/STplus Panel and R/STplus Panel Mini for near-patient respiratory and sore-throat diagnostics in Europe. Both products became available to countries recognizing CE marking in Q2 2026.

- January 2026: APTARION Biotech AG completed enrollment in its international Phase 2 ADCAP trial of AON-D21 in severe CAP. The trial enrolled 150 patients across 5 European countries and the United States, testing the first L-aptamer immunomodulatory candidate for severe respiratory infection.

Global Community Acquired Pneumonia Market Report Scope

The Community-Acquired Pneumonia (CAP) market comprises the global market for the prevention, diagnosis, treatment, and management of pneumonia acquired outside of hospital or healthcare settings. It includes pharmaceutical therapies such as antibiotics, antivirals, and adjunctive treatments; diagnostic products including laboratory tests, imaging technologies, and point-of-care diagnostic tools; as well as vaccines and supportive care products used to prevent and manage CAP.

The Community-Acquired Pneumonia (CAP) market is segmented based on diagnosis & treatment, pathogen type, age group, risk factors, and geography. By diagnosis & treatment, the market is categorized into diagnosis methods and treatment types. Diagnosis methods include chest X-ray, CT scan, sputum culture, blood tests, and pulse oximetry, while treatment types comprise antibiotics, oxygen therapy, hospitalization, and supportive care. By pathogen type, the market is divided into bacterial pneumonia, viral pneumonia, fungal pneumonia, and atypical pneumonia. Based on age group, the market is segmented into infants, children, adults, and the geriatric population. By risk factors, the market includes patients with chronic diseases, smoking history, alcoholism, and weakened immune systems. Geographically, the market is analyzed across North America (United States, Canada, and Mexico), Europe (Germany, the United Kingdom, France, Italy, Spain, and the Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, and the Rest of Asia-Pacific), Middle East & Africa (GCC, South Africa, and the Rest of the Middle East & Africa), and South America (Brazil, Argentina, and the Rest of South America).

| Diagnosis Method | Chest X-Ray |

| CT Scan | |

| Sputum Culture | |

| Blood Tests | |

| Pulse Oximetry | |

| Treatment Type | Antibiotics |

| Oxygen Therapy | |

| Hospitalization | |

| Supportive Care |

| Bacterial Pneumonia |

| Viral Pneumonia |

| Fungal Pneumonia |

| Atypical Pneumonia |

| Infants |

| Children |

| Adults |

| Geriatric Population |

| Chronic Diseases |

| Smoking |

| Alcoholism |

| Weakened Immune System |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diagnosis & Treatment | Diagnosis Method | Chest X-Ray |

| CT Scan | ||

| Sputum Culture | ||

| Blood Tests | ||

| Pulse Oximetry | ||

| Treatment Type | Antibiotics | |

| Oxygen Therapy | ||

| Hospitalization | ||

| Supportive Care | ||

| By Pathogen Type | Bacterial Pneumonia | |

| Viral Pneumonia | ||

| Fungal Pneumonia | ||

| Atypical Pneumonia | ||

| By Age Group | Infants | |

| Children | ||

| Adults | ||

| Geriatric Population | ||

| By Risk Factors | Chronic Diseases | |

| Smoking | ||

| Alcoholism | ||

| Weakened Immune System | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the expected value of the community acquired pneumonia space by 2031?

The community acquired pneumonia market size is projected to reach USD 15.83 billion by 2031 from USD 12.39 billion in 2026, with a 5.02% CAGR over 2026 to 2031.

Which product area leads current spending in CAP care?

Diagnosis method led its category with 52.83% share in 2025, which shows how strongly current spending still depends on imaging, lab confirmation, and early workup tools.

Which pathogen category is growing fastest?

Viral pneumonia is the fastest-growing pathogen segment and is projected to expand at a 6.76% CAGR through 2031 as multiplex diagnostics identify more viral cases.

Which patient group matters most commercially?

Older adults remain the largest age-based group, with the geriatric population holding 47.16% share in 2025, reflecting higher severity, hospitalization, and follow-up care needs.

Which region offers the strongest growth opportunity?

Asia-Pacific is the fastest-growing geography at a 6.04% CAGR through 2031 because disease burden remains high and diagnostics penetration still has room to improve.

What is the main competitive theme shaping vendor strategy?

The main theme is integration, with companies combining faster diagnostics, differentiated antibiotics, and vaccine programs to fit more tightly into routine respiratory care pathways.

Page last updated on: