Market Overview

| Study Period | 2020 - 2031 |

|---|---|

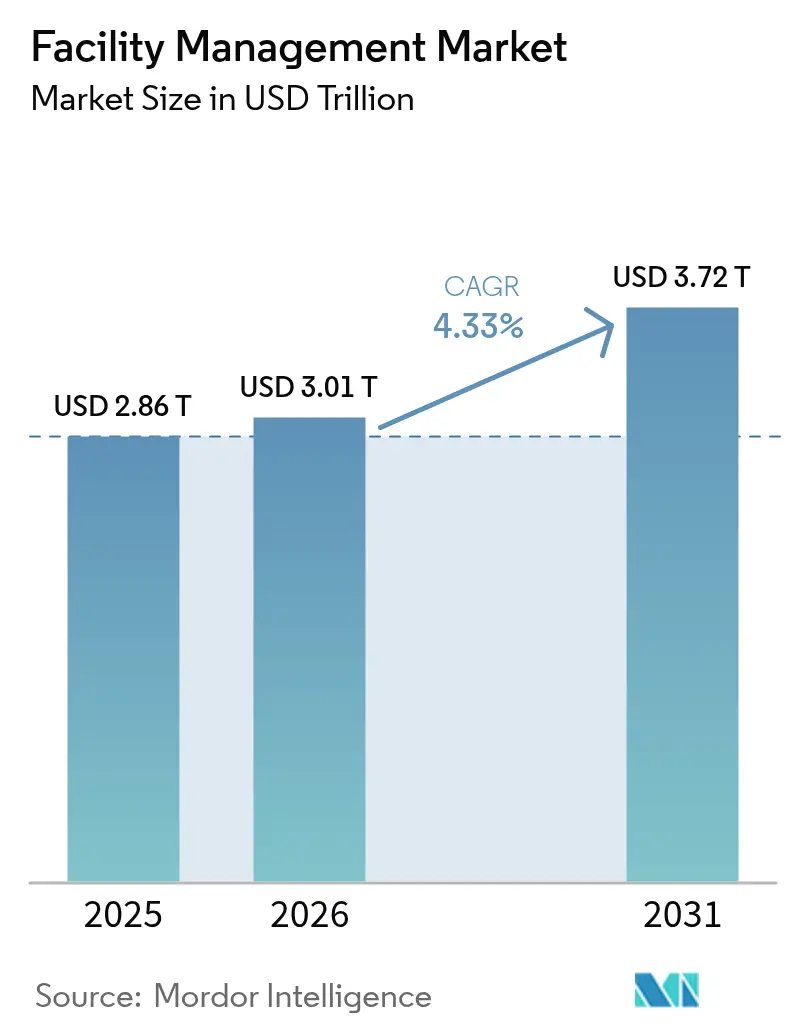

| Market Size (2026) | USD 3.01 Trillion |

| Market Size (2031) | USD 3.72 Trillion |

| Growth Rate (2026 - 2031) | 4.33% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Facility Management Market Analysis by Mordor Intelligence

The Facility Management Market size is projected to be USD 2.86 trillion in 2025, USD 3.01 trillion in 2026, and reach USD 3.72 trillion by 2031, growing at a CAGR of 4.33% from 2026 to 2031. Growth momentum reflects the repositioning of facility management from a support cost to a strategic lever for operational resilience, digital integration, and employee productivity. Heightened outsourcing appetite, rapid cloud migration despite cybersecurity incidents, and the steady pull of ESG mandates are collectively widening addressable demand. Rising infrastructure spending in emerging markets, particularly Asia-Pacific, is reinforcing a multi-regional expansion cycle for the facility management market. Providers that blend technology platforms with outcome-based models are capturing premium contracts as clients seek transparent cost control and measurable efficiency.

Key Report Takeaways

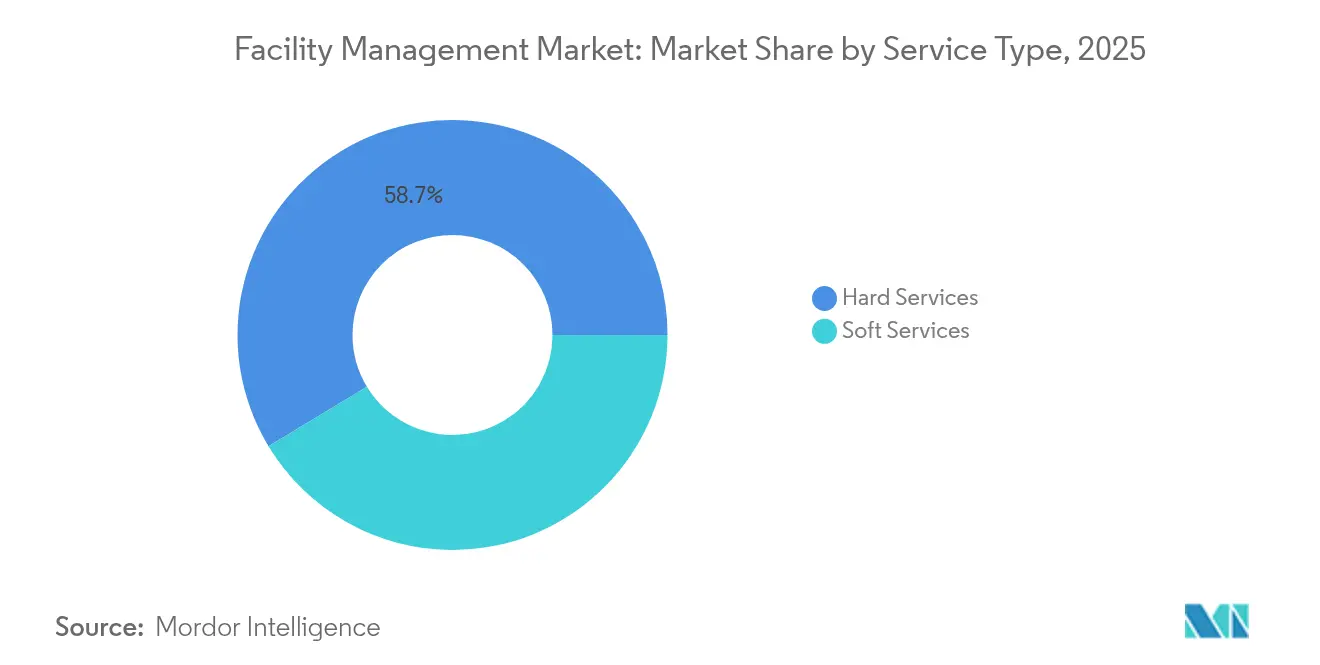

- By service type, Hard Services accounted for 58.65% of facility management market share in 2025, while Soft Services are projected to expand at a 6.05% CAGR through 2031.

- By offering type, In-house models retained 53.20% share of the facility management market size in 2025; Outsourcing operations are forecast to grow at 5.71% CAGR to 2031.

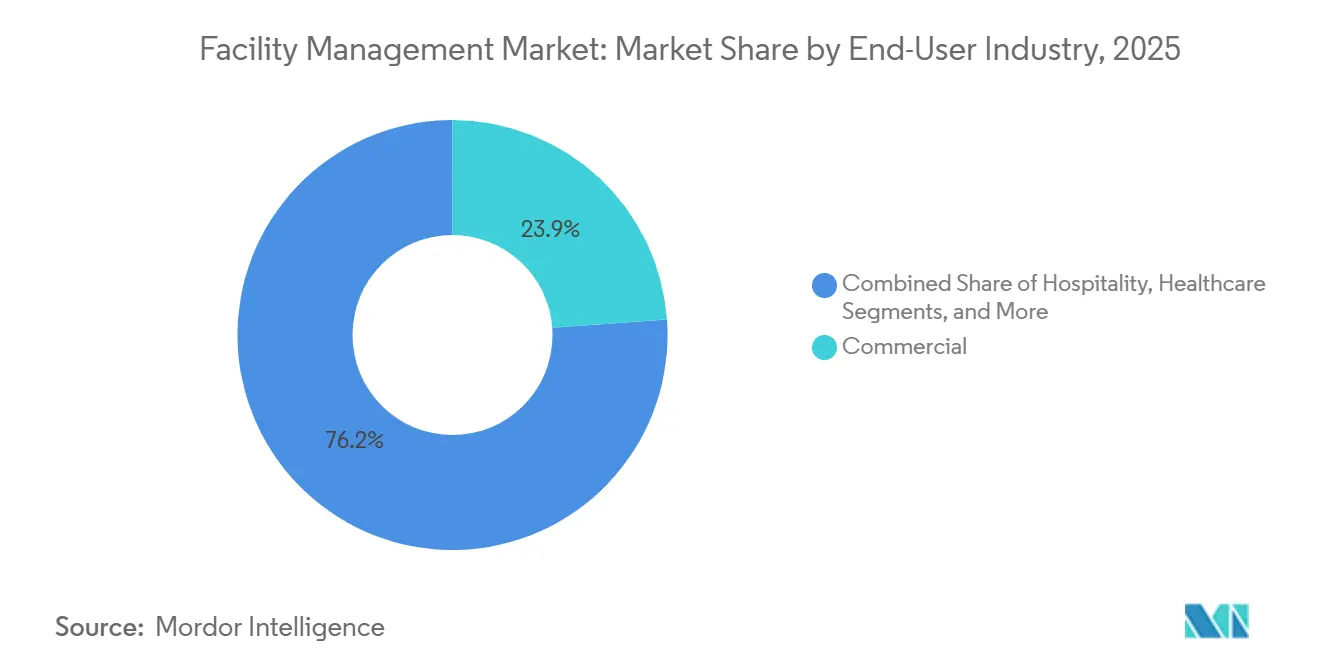

- By end-user industry, the Commercial segment led with 23.85% of facility management market share in 2025, whereas Healthcare facilities are growing fastest at 7.78% CAGR on smart-hospital investments.

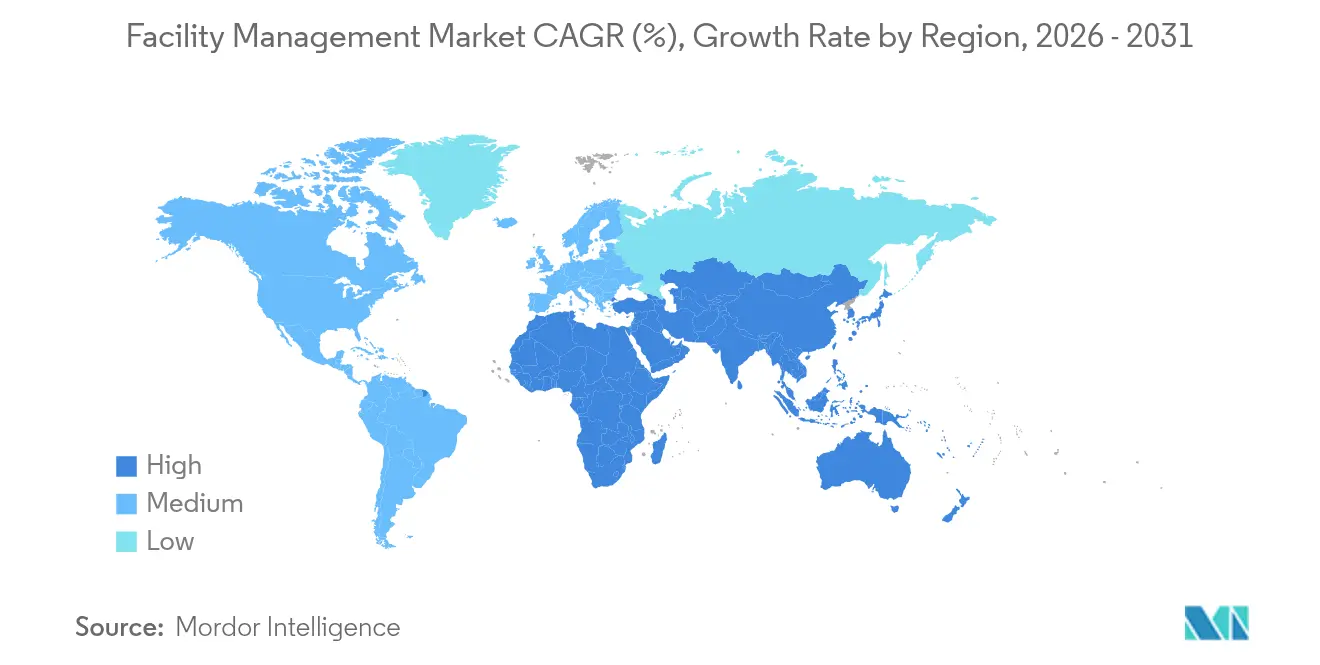

- By geography, Asia-Pacific held 41.10% of the facility management market in 2025 and Middle East and Africa advancing at 7.05% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing emphasis on outsourcing non-core operations | +2.8% | Global, with strongest adoption in North America & Europe | Medium term (2-4 years) |

| Facility digitisation via IoT-enabled predictive maintenance | +2.1% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Sustainability and ESG-linked FM contracting | +1.9% | Europe & North America, expanding to APAC | Long term (≥ 4 years) |

| Post-pandemic hybrid workplace re-design needs | +1.4% | Global, with emphasis on developed markets | Short term (≤ 2 years) |

| Public–private infrastructure pipelines in EMs | +1.2% | Asia-Pacific, Middle East & Africa | Long term (≥ 4 years) |

| AI-led energy optimisation mandates | +0.9% | North America & Europe, early adoption in APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing emphasis on outsourcing non-core operations

Corporations are channeling capital toward core innovation by transferring facilities responsibilities to specialist partners, with 35% of enterprises boosting FM budgets in 2024 to curb operational complexity.[1]CBRE Research, “Global FM Budget Outlook 2024,” cbre.com The facility management market is benefiting from scale effects that let providers absorb supply-chain shocks and provide diversified labor pools. Demand is pronounced in technology and healthcare, supporting CBRE’s 16% net revenue rise from facilities contracts during Q1 2025. The practice also mitigates supplier-risk exposure—29% of firms flagged disruption fears—fueling preference for FM partners with fortified logistics. As outsourcing volume mounts, providers are reinvesting margin gains into automation, predictive analytics, and workforce upskilling, reinforcing a virtuous growth cycle across the facility management market.

Facility digitisation via IoT-enabled predictive maintenance

Predictive maintenance platforms worth USD 5.5 billion in 2025 and expanding 17% annually underpin a structural shift from reactive repairs to condition-based care.[2]Buildings Media, “Predictive Maintenance Market Update 2025,” buildings.com Healthcare adopters report 10-15% facility cost savings through automated work-order generation.[3]Medxcel, “Smart Hospital Case Studies,” medxcel.com The software layer—44% of spend—packages pre-trained algorithms that democratize access for midsize sites inside the facility management market. Early pilots in industrial plants reveal 25% faster waste-heat recovery, highlighting tangible ESG payoffs. As anomaly-detection models mature, data prerequisites shrink, enabling smaller assets to participate without dense historical logs, thereby broadening market penetration across geographies.

Sustainability and ESG-linked FM contracting

Evolving green-building codes such as LEED v5 compel comprehensive decarbonisation strategies, pushing FM providers to embed renewable power, waste diversion, and indoor-air targets into contracts. ENERGY STAR NextGen demands 30% renewable-energy sourcing, raising performance bars and differentiating tech-savvy vendors. ISS Guckenheimer’s #1 protein-sustainability ranking illustrates how service portfolios now integrate food-supply ethics with energy management. Compass Group’s pledge to cut Scope 1 and 2 emissions 46% by 2030 positions the group to win ESG-driven tenders. Collectively, these dynamics enlarge the facility management market by turning sustainability into a revenue-generating capability rather than a compliance cost.

Post-pandemic hybrid workplace re-design needs

Hybrid work is reshaping space allocation, driving uptake of AI-enabled occupancy tools such as IBM TRIRIGA, which adjusts portfolios in real time. CBRE’s Industrious acquisition extends the firm’s reach into flexible offices, evidencing a shift toward experiential service bundles within the facility management market. Healthcare operators like Guthrie Clinic saved USD 7 million in labor and cut turnover after launching remote-care hubs. Demand for healthy indoor environments is fostering investment in air-quality sensors and touchless controls, reinforcing convergence between employee well-being and facilities strategy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High wage inflation in custodial labour | -1.8% | Global, with acute pressure in North America & Europe | Short term (≤ 2 years) |

| Fragmented vendor base in emerging markets | -1.2% | Asia-Pacific, Middle East & Africa | Medium term (2-4 years) |

| Cyber-security risk in cloud-based FM platforms | -0.9% | Global, with heightened concern in developed markets | Short term (≤ 2 years) |

| Capital lock-in for IFM platforms among SMEs | -0.7% | Global, with particular impact on emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High wage inflation in custodial labour

Average hourly earnings in facilities support soared 4.1% in 2024, lifting median pay to USD 21.74 and compressing margins for labour-intensive contracts. Skilled-trade shortages, especially HVAC and electrical, intensify bidding wars, while events such as Cornell University’s facilities-worker strike underscore rising union activism. Hidden contract fees and backend surcharges further strain budgets, pushing buyers to reconsider outsourcing economics. Providers respond by accelerating robotics and autonomous-cleaning pilots, but up-front capital and retraining requirements weigh on near-term adoption across the facility management market.

Fragmented vendor base in emerging markets

In Asia-Pacific and parts of MEA, FM suppliers are numerous yet sub-scale, complicating procurement and quality assurance for multinational occupiers. Disparate standards challenge integrated service rollouts, inflating coordination costs and slowing the facility management market’s maturation. Large incumbents are deploying consolidation playbooks, but regulatory barriers and local-labor mandates prolong integration timelines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Drive Infrastructure Modernization

Hard Services generated 58.65% of the facility management market size in 2025, buoyed by mandatory mechanical, electrical, and plumbing (MEP) maintenance that safeguards asset integrity. Regulatory codes and rising asset complexity necessitate certified technicians, reinforcing demand stability. Over the forecast horizon, convergence with Soft Services will intensify as clients seek unified experience management, creating cross-selling avenues for integrated vendors.

Soft Services, though smaller, accelerate at a 6.05% CAGR, reflecting heightened focus on hygiene, security, and occupant well-being. Cleaning contracts embed anti-microbial protocols and robotic vacuums, while security shifts toward AI video analytics. As ESG scorecards widen to include indoor air and catering sustainability, Soft Services gain board-level visibility. Providers that fuse Hard and Soft data streams can proactively adjust preventive schedules, creating tangible operational gains and broadening wallet share within the facility management market.

By Offering Type: In-house Accelerates Despite Outsourcing Growth

In-house models held 53.20% of the facility management market share in 2025, underpinned by integrated FM (IFM) contracts that streamline accountability. Multisite firms appreciate single-invoice transparency, propelling uptake. Simultaneously, Outsourcing FM expands 5.71% CAGR as cyber-sensitive industries retain critical controls. Hybrid structures are proliferating: strategic planning stays internal, while field execution shifts to partners, balancing flexibility and risk.

As IFM scope widens, vendors embed analytics portals that surface cost-to-serve by location, enabling data-driven renewals. Single-service options erode as clients insist on total-value propositions, nudging smaller contractors toward mergers or specialisation niches. CBRE’s USD 1.6 billion Industrious acquisition underscores strategic re-positioning toward experiential subscriptions that bundle facilities, hospitality, and space analytics, thereby redefining competitive contours of the facility management market.

By End-User Industry: Healthcare Leads Growth Through Smart Infrastructure

The Commercial category contributed 23.85% of revenue in 2025, spanning IT hubs, retail, and warehousing that require stringent uptime and environmental controls. Healthcare, the fastest-growing vertical, exhibits an 7.78% CAGR to 2031, catalysed by IoT-enabled smart hospitals demanding round-the-clock critical-equipment monitoring. Industrial campuses embrace AI-guided energy efficiency, achieving up to 18.75% lower consumption and 20% CO2 cuts.

Hospitality operators invest in guest-experience technologies automated check-in kiosks and predictive HVAC to differentiate in a competitive landscape. Public infrastructure facilities benefit from sovereign spending, such as China’s USD 51.4 trillion construction program, enlarging the facility management market footprint. Residential complexes adopt smart-home integrations, foreshadowing fresh service bundling opportunities for FM providers.

Geography Analysis

Asia-Pacific accounted for 41.10% of the facility management market in 2025 and is set to expand at a 6.05% CAGR, sustained by government stimulus and urban migration. China’s USD 51.4 trillion fixed-asset push, including 5.9% growth in infrastructure placements, underpins long-run service pipelines. India’s commercial real estate surge adds demand for remote monitoring, while ASEAN smart-city programs embed FM contracts into master planning stages. Providers scaling localized supply chains and multilingual platforms will gain early-mover advantage.

North America maintains a mature yet innovative landscape where cloud penetration and ESG compliance drive premium fees. The facility management market in the region contends with tight labor pools, spurring automation adoption. Energy-optimisation mandates and the Inflation Reduction Act’s incentives incentivize retrofits managed by FM specialists. Europe exhibits similar digital sophistication but is distinguished by stringent carbon regulations such as EPBD, steering contracts toward performance-linked remuneration. Pan-European vendors leverage cross-border governance frameworks to standardise service quality.

The Middle East and Africa witness accelerating adoption through public-private partnerships in transport, healthcare, and education infrastructure. Gulf Cooperation Council megaprojects integrate FM provisions from the design stage, anchoring lifecycle value. South America experiences steady demand tied to logistics and manufacturing expansion, though currency volatility necessitates flexible pricing. Across all emerging regions, fragmented supplier landscapes encourage consolidation plays, broadening the facility management market for global majors adept at merger integration.

Competitive Landscape

The facility management market remains fragmented, yet consolidation momentum is unmistakable. Global leaders—CBRE, JLL, ISS, and Sodexo—collectively command significant but not dominant share, keeping competitive pressure high. CBRE’s USD 1.6 billion purchase of Industrious extends its suite to flexible workspaces, illustrating strategic pivot toward high-growth experiential services. JLL registered 20% Workplace Management growth in 2025, partly through AI-enhanced service orchestration.

Technology investment is the primary battleground. Providers deploy IoT sensors and machine-learning predictive engines to cut downtime and prove ROI, bolstering contract renewals. ISS leverages its sustainability track record—such as Guckenheimer’s protein-sustainability leadership—to win ESG-centric bids. Patent activity around building automation and occupancy analytics is rising, granting first-mover IP moats.

In emerging regions, indigenous firms hold relational capital but lack scale, prompting acquisition interest from multinationals eager to deepen local portfolios. Outcome-based pricing, where providers guarantee utility baselines or uptime targets, redistributes risk and rewards operational excellence. As clients demand single-pane dashboards for property, energy, and experience metrics, platform interoperability becomes a decisive differentiator, steering winners in the facility management market toward open-API ecosystems.

Facility Management Industry Leaders

Emeric Facility Services

SMI Facility Services

AHI Facility Services Inc.

Sodexo SA

ISS A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: JLL delivered USD 5.7 billion Q1 2025 revenue, beating consensus by 13% despite EPS pressure from fair-value adjustments; reaffirmed outlook signals resilience in transaction-adjacent FM demand.

- March 2025: Klickitat Valley Health invested in hydrogen-fuel-cell systems, exemplifying healthcare’s shift to resilient, low-carbon energy under FM stewardship.

- January 2025: Sodexo generated EUR 6.4 billion (USD 7.1 billion) Q1 2025 revenue, acquiring CRH Catering to fortify U.S. food-services adjacencies and strengthen cross-selling within FM accounts.

- January 2025: CBRE closed the USD 1.6 billion acquisition of Industrious, forming a Building Operations & Experience division forecast to produce USD 20 billion revenue. The move secures CBRE a ready-made flexible-workspace network while monetising synergies with its integrated FM platform, positioning the firm to upsell bundled occupancy services.

Global Facility Management Market Report Scope

Facility management (FM) services involve the management of building upkeep, utilities, maintenance operations, waste services, security, etc. These services are further segmented by hard facility management services and soft facility management services. The adoption of FM solutions and services is likely to be driven by several factors, including an increase in demand for cloud-based FM solutions and a rise in demand for FM systems linked to intelligent software.

The facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others), and by geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC | |

| Fire and Safety | |

| Other Hard Services | |

| Soft Services | Cleaning |

| Security and Office Support | |

| Catering | |

| Other Soft Services |

By Offering Type

| In-house | |

| Outsourced | Single-service FM |

| Bundled FM | |

| Integrated FM (IFM) |

By End-User Industry

| Commercial (IT and Telecom, Retail, Warehousing) |

| Hospitality (Hotels, Eatries, Restaurants) |

| Institutional and Public Infrastructure (Government, Education, Transport) |

| Healthcare (Public Facilities, and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-house Residential, Entertainment, Sports and Leisure) |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Benelux (Belgium, Netherlands, Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland) | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America | |

| Middle East | GCC (Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain) |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Kenya | |

| Rest of Africa |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC | ||

| Fire and Safety | ||

| Other Hard Services | ||

| Soft Services | Cleaning | |

| Security and Office Support | ||

| Catering | ||

| Other Soft Services | ||

| By Offering Type | In-house | |

| Outsourced | Single-service FM | |

| Bundled FM | ||

| Integrated FM (IFM) | ||

| By End-User Industry | Commercial (IT and Telecom, Retail, Warehousing) | |

| Hospitality (Hotels, Eatries, Restaurants) | ||

| Institutional and Public Infrastructure (Government, Education, Transport) | ||

| Healthcare (Public Facilities, and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-house Residential, Entertainment, Sports and Leisure) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Benelux (Belgium, Netherlands, Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland) | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Rest of South America | ||

| Middle East | GCC (Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain) | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Kenya | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the facility management market?

The facility management market stands at USD 3.01 trillion in 2026 and is projected to reach USD 3.72 trillion by 2031 at a 4.33% CAGR.

Which region leads the facility management market?

Asia-Pacific holds 41.10% share and shows the fastest 6.05% CAGR, buoyed by large-scale infrastructure investments and rapid urbanization.

Why are Soft Services growing faster than Hard Services?

Soft Services benefit from heightened focus on occupant health, ESG targets, and automated cleaning and security technologies, driving a 6.05% CAGR through 2031.

Which end-user industry is the fastest-growing within the facility management market?

Healthcare facilities are advancing at 7.78% CAGR thanks to smart-hospital initiatives and strict regulatory compliance needs.

How are leading FM providers differentiating themselves?

Market leaders invest heavily in IoT, AI-driven predictive maintenance, and ESG-linked service models, while pursuing acquisitions that broaden experiential and flexible-workspace offerings.

Page last updated on: