United States (US) MEP Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

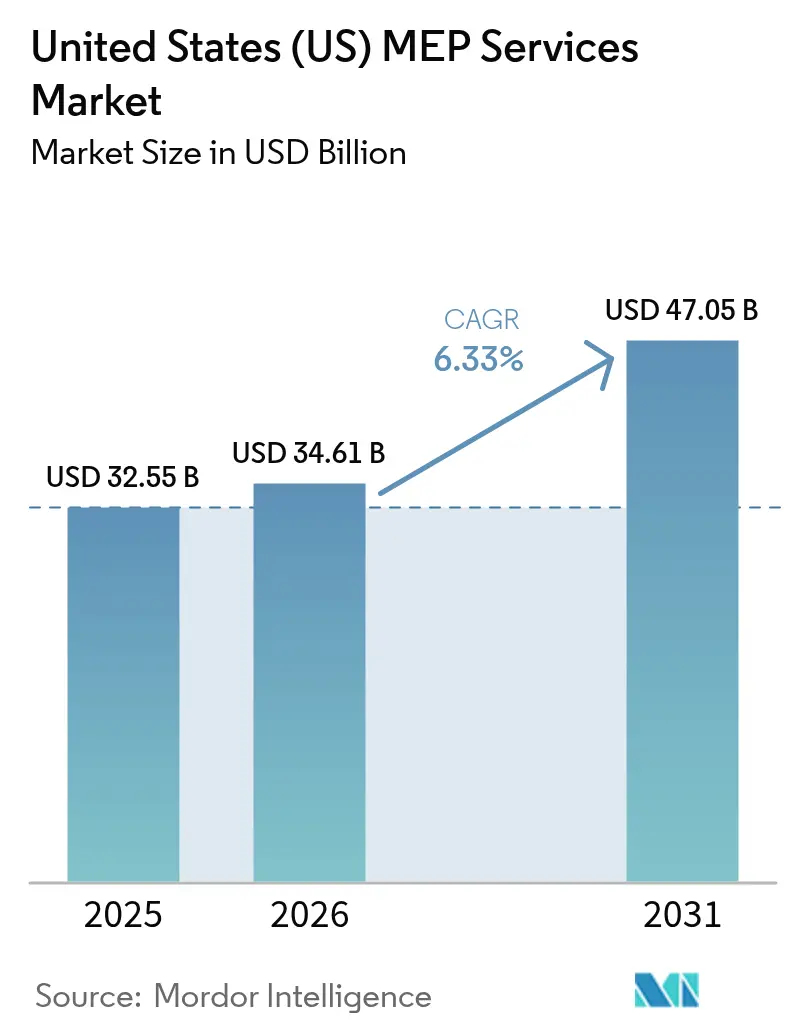

| Base Year Market Size (2025) | USD 32.55 Billion |

| Market Size (2026) | USD 34.61 Billion |

| Market Size (2031) | USD 47.05 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

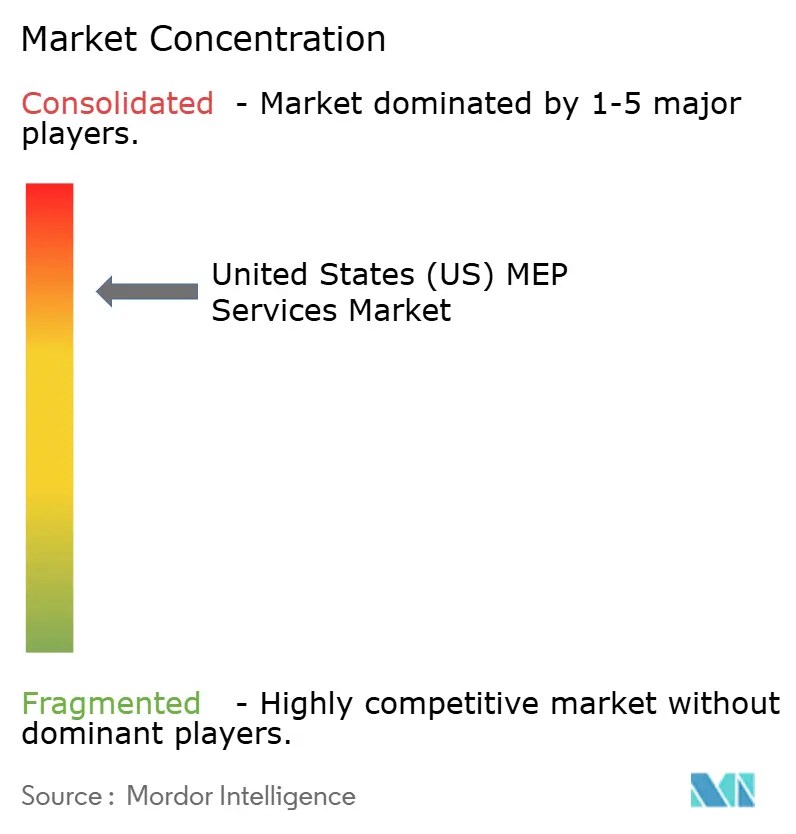

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States (US) MEP Services Market Analysis by Mordor Intelligence

The United States MEP services market size is expected to grow from USD 32.55 billion in 2025 to USD 34.61 billion in 2026 and is forecast to reach USD 47.05 billion by 2031 at 6.33% CAGR over 2026-2031. Contractors report that retrofit activity accelerated after the IRA’s launch, with heat-pump and energy-efficient HVAC retrofits up 40% since 2024. Healthcare expansions, semiconductor fabs, and hyperscale data centers are shaping procurement cycles, while skilled-labor scarcity continues to inflate wages and extend project lead times.[1]Contracting Business, “Industry Econ Forecast 2025,” contractormag.com Material cost volatility, especially copper surpassing USD 5 per pound, complicates pricing strategies for the mechanical services industry. Digitalization deepens competitive gaps as 77% of new projects already require BACnet-compatible building-automation infrastructure that favors firms with proven BIM and AI capabilities.[2]BACnet International, “BACnet’s Future in Building Automation,” bacnetinternational.org

Key Report Takeaways

- By type, retrofit and renovation led with 46.72% revenue share of the mechanical services market in 2025; commissioning and re-commissioning are advancing at a 7.35% CAGR through 2031.

- By end-user vertical, healthcare facilities commanded 28.74% of the mechanical services market share in 2025; data centers are rising at an 7.86% CAGR to 2031.

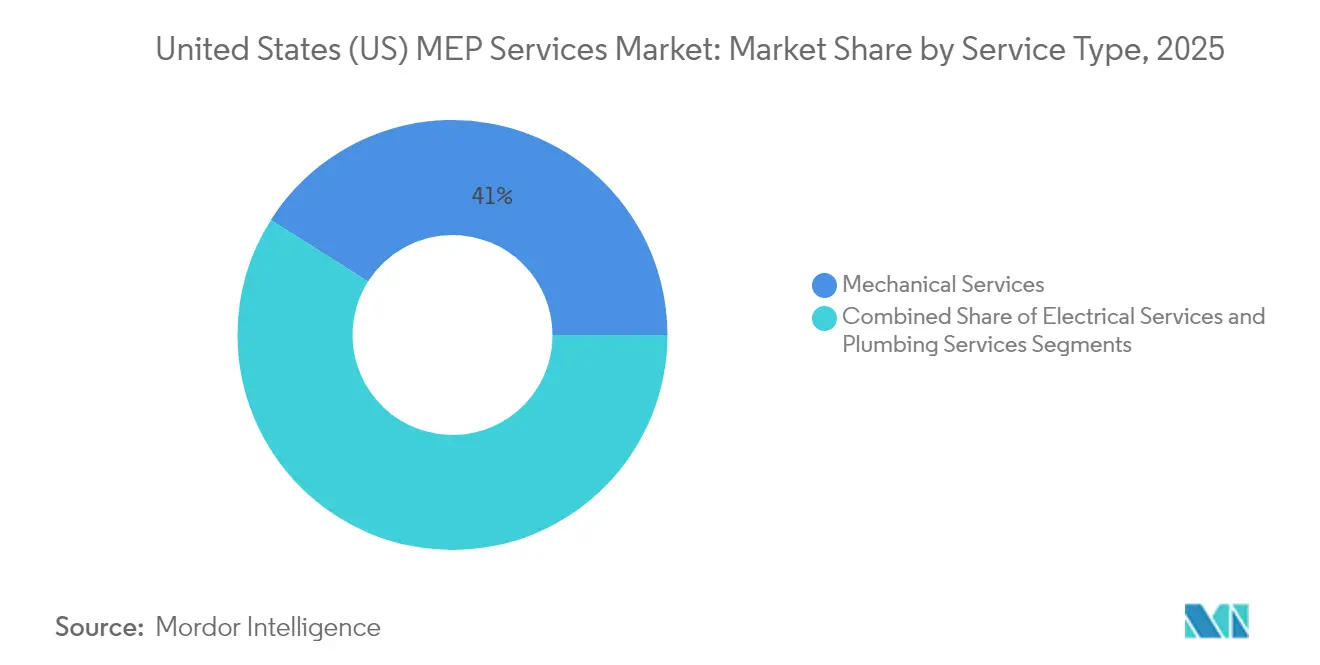

- By service type, Mechanical Services accounted for a 41.02% share of the mechanical services market size in 2025, while electrical services are forecast to expand at a 7.47% CAGR.

- By US region, the South held 36.12% of the mechanical services market size in 2025; the West is projected to post the fastest regional CAGR at 7.55% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States (US) MEP Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Outsourcing focus on core competencies | +1.2% | Global, with concentration in South and West regions | Medium term (2-4 years) |

| Sustained demand from healthcare construction | +1.5% | National, with early gains in Texas, California, Arizona | Long term (≥ 4 years) |

| Electrification and HVAC efficiency retrofits | +1.8% | California, New York, Northeast states leading adoption | Short term (≤ 2 years) |

| Inflation Reduction Act tax-credit pull-through | +1.1% | National, with higher uptake in high-income metropolitan areas | Short term (≤ 2 years) |

| Grid-interactive buildings and DER integration needs | +0.9% | California, Texas, Northeast grid-constrained markets | Medium term (2-4 years) |

| Growing VC funding for AI-driven MEP design tools | +0.2% | Technology hubs: Silicon Valley, Boston, Seattle | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Outsourcing Focus on Core Competencies

Mechanical systems now form 40–60% of building energy loads, encouraging owners to outsource to specialist firms rather than carry in-house teams. Technology platforms such as ServiceTitan help contractors build direct relationships that bypass general-contractor markups, evidenced by Southland Industries’ productivity gains after adopting the platform. Healthcare networks allocate higher portions of capital budgets to specialized partners, with facilities-management spending on non-hospital projects up 27% in 2025. Contractors like Limbach report recurring revenue increases from building-systems solution contracts that improve lifecycle performance.

Sustained Demand from Healthcare Construction

Healthcare construction reached USD 65 billion in 2024 as infection-control protocols and negative-pressure ventilation drove complex mechanical specifications. Projects such as Mayo Clinic’s 1.4 million sq ft expansion in Arizona require redundant HVAC, filtration, and emergency power systems with 24/7 uptime. Hospital owners now specify commissioning on 80% of projects to certify operational readiness, expanding demand for specialized MEP consultants.

Electrification and HVAC Efficiency Retrofits

IRA rebates and state codes are accelerating electrification, with the Department of Energy projecting 900,000 new contractor roles linked to heat-pump rollouts. California’s 2025 Energy Code mandates electric-ready kitchens and higher heat-pump efficiencies, pushing contractors into advanced refrigerant management and electrical-coordination scopes.[3]California Energy Commission, “2025 California Energy Code Fact Sheet,” energy.ca.gov Smart HVAC integration delivers 36.8 kW average power savings per facility when coupled with IoT-driven predictive maintenance algorithms.

Inflation Reduction Act Tax-Credit Pull-Through

Section 25C permits homeowners to recover 30% of qualified mechanical expenditures up to USD 3,200 annually, driving a wave of residential retrofits. Commercial owners leverage uncapped 25D credits for solar-plus-storage that require sophisticated HVAC load management, while states like New York add workforce grants that subsidize heat-pump installer training.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Talent scarcity and wage escalation | -1.8% | National, with acute shortages in Midwest and Northeast | Long term (≥ 4 years) |

| Small-firm margin squeeze from design-build consolidation | -0.9% | Regional markets with high general contractor concentration | Medium term (2-4 years) |

| Cyber-security liability on smart-building projects | -0.4% | Urban markets with high smart building adoption | Medium term (2-4 years) |

| Volatile HVAC/R material pricing risk transfer | -0.6% | National, with higher impact in copper-intensive regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Talent Scarcity and Wage Escalation

The sector faces a gap of 650,000 skilled workers as baby-boom retirements accelerate, leading to 20% wage growth since 2020.[4]Autodesk, “Can Better MEP Solve Construction’s Skilled Labor Shortage?,” autodesk.com Apprentice compensation in energy trades averages USD 77,000 in year one, pressuring bid margins for public-sector contracts. Mechanical contractors in the Midwest report 68% difficulty filling mechanical-engineering positions, forcing 49% of firms to decline projects despite strong pipelines.

Small-Firm Margin Squeeze from Design-Build Consolidation

Strategic acquisitions among national players continued in 2024, exemplified by WSP’s USD 1.78 billion purchase of Power Engineers and Michael Baker International’s takeover of Infinity MEP+S Consultants. Consolidators leverage bulk-buying power to mitigate copper and equipment price spikes, leaving independents vulnerable to material cost inflation that has hit 40% for HVAC equipment since 2020. Smaller entities increasingly pivot toward niches such as hospital retro-commissioning or liquid-cooling integration to preserve pricing power.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Retrofits Dominate IRA-Driven Growth

Retrofit and renovation captured 46.72% of the mechanical services market share in 2025 as building owners raced to secure federal incentives ahead of potential rule changes. Commissioning and re-commissioning are projected to generate USD 4.58 billion of additional mechanical services market size by 2031, posting a 7.35% CAGR as performance verification becomes mandatory for healthcare and public-sector projects.

Performance-based contracts are reshaping service scopes; eighty percent of hospital projects now bundle commissioning, energy modeling, and maintenance analytics into single awards. Digital-twin adoption accelerates verification accuracy, with IFC-based workflows reducing corrective-action lists by 28%.

By End-User Vertical: Healthcare Leads Mission-Critical Expansion

Healthcare accounted for 28.74% of the mechanical services market size in 2025, underpinned by USD 2.5 billion in announced medical-campus expansions. Data centers hold a modest 10.34% revenue slice today, but are the fastest-growing vertical at 7.86% CAGR as AI workloads escalate liquid-cooling adoption.

Commercial-office demand remains resilient as owners upgrade indoor air quality to win back tenants, while educational institutions unlock deferred-maintenance budgets through infrastructure grants. Industrial and warehousing clients invest in high-volume ventilation and process piping to comply with Occupational Safety and Health Administration (OSHA) air-quality limits. Mission-critical campuses, a blended category of hospitals, labs, and hyperscale compute sites, are projected to contribute USD 49 billion to the mechanical services market size by 2025.

By Service Type: HVAC Systems Drive Electrification

HVAC retained 41.02% of the mechanical services market share in 2025, reflecting the technical intensity of heat-pump rollouts and smart controls integration. Electrical Services is expanding at a 7.47% CAGR as jurisdictions adopt outcome-based codes that oblige predictive performance assurance.

Electrical-service demand climbs in parallel, driven by panel upgrades for EV chargers and rooftop solar interconnections. Plumbing and fire protection maintain a steady share because hospital and industrial projects need specialized piping, medical-gas systems, and code-driven sprinkler designs. ASHRAE’s 2024 standards emphasize whole-building system efficiency, compelling mechanical contractors to coordinate envelope, lighting, and HVAC decisions from schematic stages.

Geography Analysis

Non-residential spending in the South grew 8.3% year over year, outpacing national averages as corporate capital moved toward right-to-work states with lower energy costs. Data-center developers cluster near high-capacity transmission lines, driving demand for chilled-water plants and high-density power distribution. Population inflows sustain a 4.6% uptick in multifamily starts, providing retrofit opportunities for centralized hot-water and HVAC upgrades across residential towers.

The West posts the highest mechanical services market CAGR at 7.55% as California mandates electric-ready builds and advanced heat-pump coefficients. Rural counties in Oregon and Utah attract hyperscale campuses seeking cool climates for liquid-cooling systems that reduce PUE ratios. Solar-plus-storage microgrids proliferate in wildfire-prone areas, requiring mechanical contractors to coordinate battery thermal-management units and smoke-control fans that meet revised air-quality rules.

The Northeast and Midwest struggle with acute labor gaps yet benefit from healthcare and infrastructure outlays. New York’s clean-energy workforce grants subsidize heat-pump installer certifications, while Illinois’ apprenticeship programs fortify pipefitter and electrician pipelines. Midwest megaprojects, including bio-fuels refineries and small-modular reactor test sites, create specialty work packages for mechanical firms offering combined process and HVAC expertise.

Competitive Landscape

Innovation and Adaptability Drive Future Success

Despite 25% of top firms completing acquisitions in 2024, the mechanical services market remains fragmented. WSP’s USD 1.78 billion integration of Power Engineers vaulted it to the top tier in energy-sector MEP, while Michael Baker International expanded geographical reach by acquiring Infinity MEP+S Consultants. Digital maturity has become a wedge; 77% of winning bids in 2025 specified BIM-level 3 coordination, and contractors advertising AI-based clash detection report bid-hit ratios 15% above peers.

White-space opportunities revolve around specialized liquid-cooling for AI data halls, hospital-grade filtration, and grid-interactive building retrofits. Independent specialists secure premium pricing in these domains, even as generalists chase volume contracts. Sustainability credentials also influence selection; more than 90 organizations have signed the MEP 2040 pledge, signaling that carbon-footprint transparency may soon be table stakes for federal and Fortune 500 clients.

Labor scarcity shapes strategy: tier-one firms invest in prefabrication and robotics to compress field hours, while mid-sized contractors form joint ventures to meet union-mandated manpower thresholds. Wage escalation prompts some companies to open in-house training academies; AECOM’s 2025 backlog hit USD 23.9 billion, partly on the strength of workforce-development programs that de-risk delivery schedules.

United States (US) MEP Services Industry Leaders

Jacobs Engineering Group Inc.

WSP USA

HDR Inc.

Arup Group

AECOM Technology Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: WSP Global completed its USD 1.78 billion acquisition of Power Engineers Inc., creating the largest energy-focused engineering platform in North America.

- January 2025: NYSERDA awarded USD 2.5 million to three clean-energy workforce projects targeting heat-pump installation and HVAC system testing.

- January 2025: The US DOE released the Distributed Energy Resource Interconnection Roadmap outlining new grid-integration protocols.

- February 2025: AECOM reported a record Q1 FY 2025 net service revenue of USD 1.8 billion, citing robust demand for MEP services across infrastructure and water segments.

United States (US) MEP Services Market Report Scope

MEP Services encompasses the design, engineering, consulting, and maintenance-related activities provided by engineering firms across a wide range of end-user verticals. The study's scope encompasses MEP services provided to new and renovated installations across a wide range of end-user verticals, including healthcare, industrial facilities, commercial offices, public buildings, educational institutions, and other relevant sectors.

The United States MEP Services Market Report is Segmented by Type (New Construction, Retrofit and Renovation, Commissioning/Re-commissioning, Facility Assessment), End-user Vertical (Healthcare, Commercial Offices, Educational Institutions, Public Facilities, Industrial and Warehousing, Data Centers), Service Type (Mechanical Services, Electrical Services, Plumbing Services), and Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

| New Construction |

| Retrofit and Renovation |

| Commissioning / Re-commissioning |

| Facility Assessment and Other Services |

| Healthcare |

| Commercial Offices |

| Educational Institutions |

| Public Facilities (Govt, Transport, Museums) |

| Industrial and Warehousing |

| Data Centers and High-Tech |

| Mechanical Services |

| Electrical Services |

| Plumbing Services |

| By Type | New Construction |

| Retrofit and Renovation | |

| Commissioning / Re-commissioning | |

| Facility Assessment and Other Services | |

| By End-user Vertical | Healthcare |

| Commercial Offices | |

| Educational Institutions | |

| Public Facilities (Govt, Transport, Museums) | |

| Industrial and Warehousing | |

| Data Centers and High-Tech | |

| By Service Type | Mechanical Services |

| Electrical Services | |

| Plumbing Services |

Key Questions Answered in the Report

How large is the United States MEP services Industry market in 2026?

The MEP services Industry market size is USD 34.61 billion in 2026.

What is the forecast CAGR for US MEP services Industry from 2026 to 2031?

The market is projected to expand at a 6.33% CAGR through 2031.

Which project type holds the largest share of spending?

Retrofit and renovation projects account for 46.72% of 2025 revenue.

Which end-user vertical is growing the fastest?

Data centers are advancing at an 7.86% CAGR through 2031

Page last updated on: