Canada Integrated Facility Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

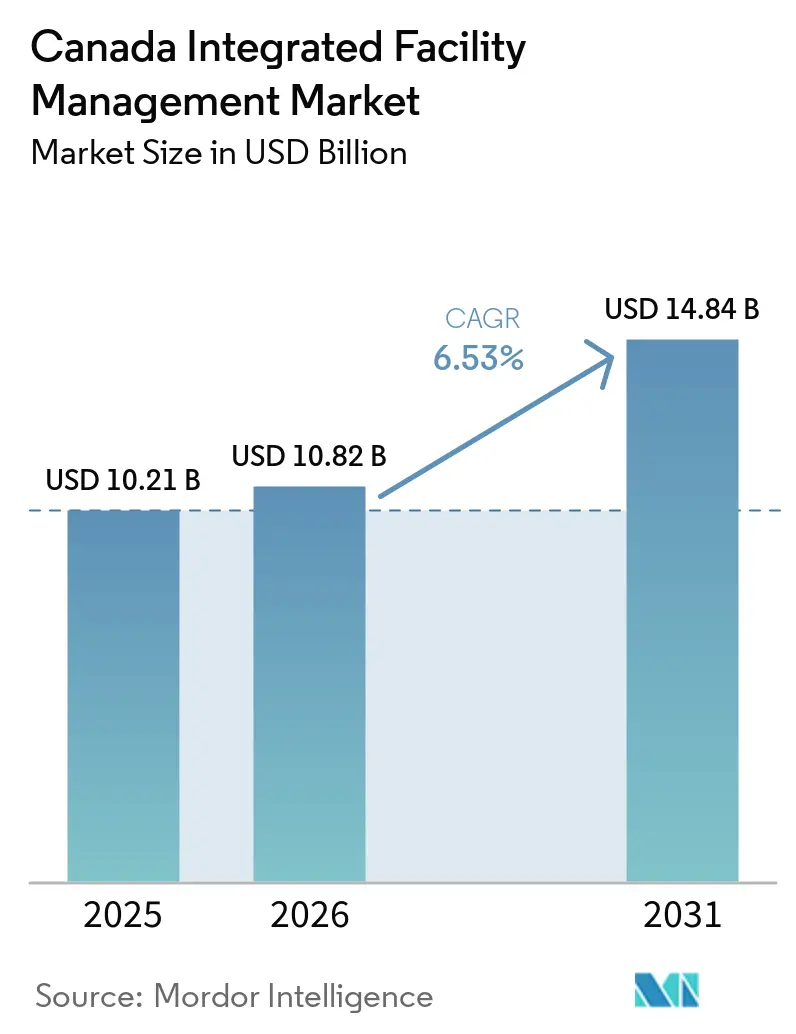

| Base Year Market Size (2025) | USD 10.21 Billion |

| Market Size (2026) | USD 10.82 Billion |

| Market Size (2031) | USD 14.84 Billion |

| Growth Rate (2026 - 2031) | 6.53% CAGR |

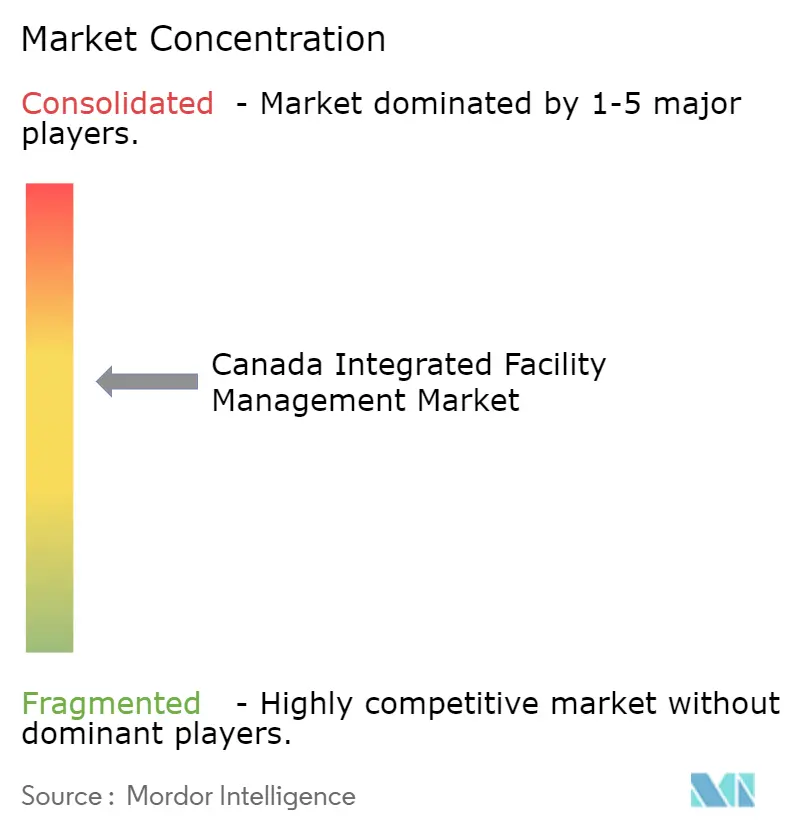

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Integrated Facility Management Market Analysis by Mordor Intelligence

The Canada integrated facility management market size is projected to be USD 10.21 billion in 2025, USD 10.82 billion in 2026, and reach USD 14.84 billion by 2031, growing at a CAGR of 6.53% from 2026 to 2031. The Canada integrated facility management market is benefiting from a broad shift toward consolidated, outcome-based contracts as occupiers adjust to hybrid work, wider site networks, and the rising cost of managing older buildings. Demand is also being reinforced by the need to meet certification and compliance requirements tied to LEED, BOMA BEST, and Canada Green Building Council Zero Carbon Building Standards across office, institutional, and mixed-use assets. Federal sustainability policy is making facility management more central to building operations because carbon reporting, energy benchmarking, and electrification project support are now part of many public sector property programs. That policy layer makes the Canada integrated facility management (IFM) market less tied to short property cycles than earlier outsourcing waves because spending is now linked to compliance, asset resilience, and operating performance. Competition remains active but disciplined, with large global providers leading complex national contracts while regional and niche operators continue to win in remote, community, and specialized settings.

Key Report Takeaways

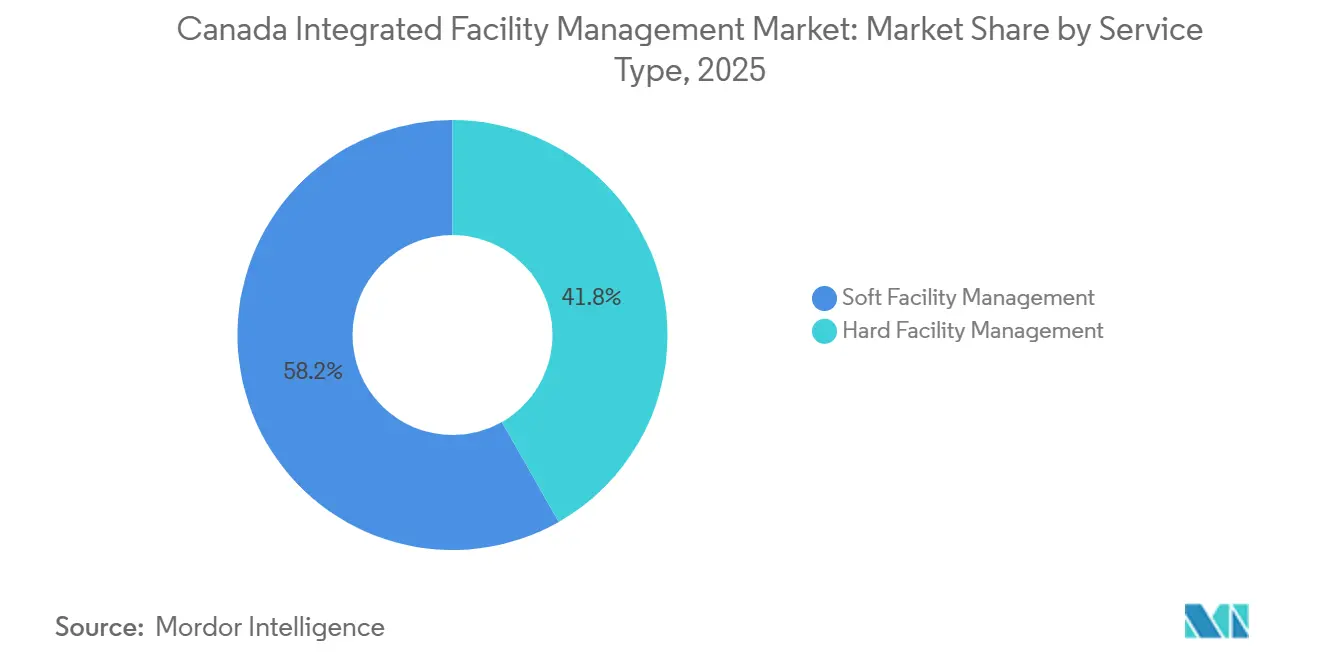

- By service type, soft facility management led with 58.23% share of the Canada integrated facility management market in 2025, while hard facility management is forecast to post the highest growth at 7.12% CAGR through 2031.

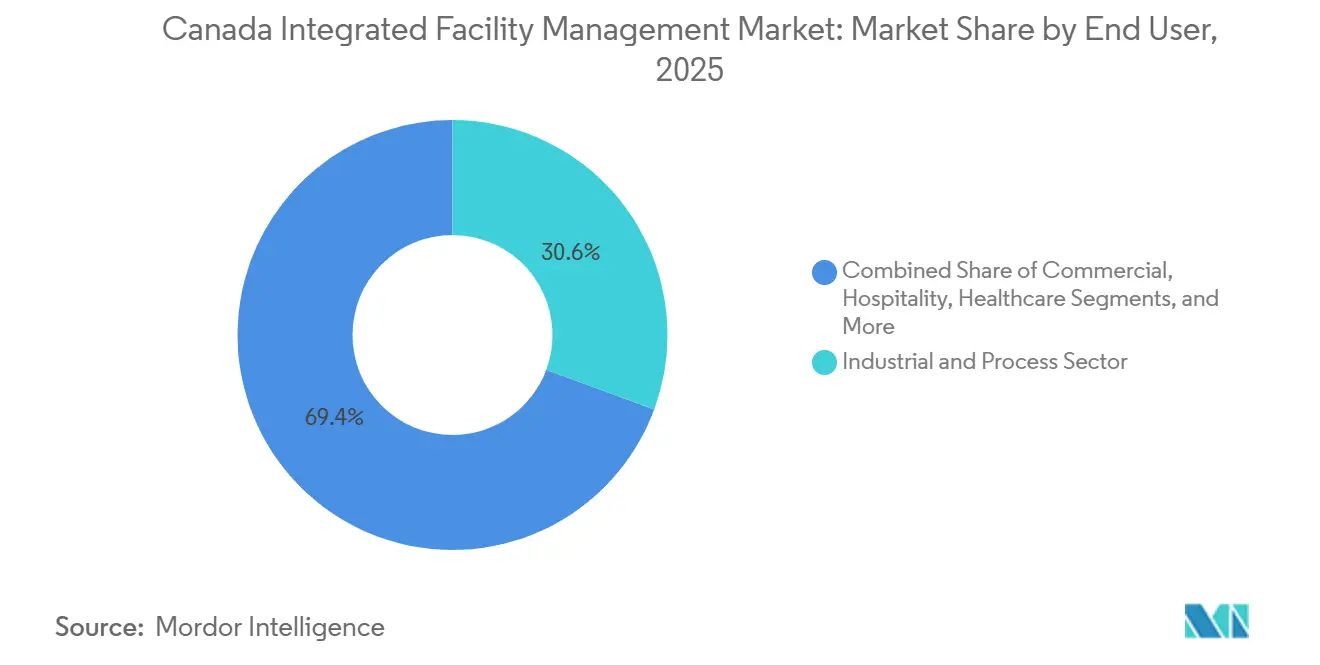

- By end-user, industrial and manufacturing held the largest share at 30.63% of the Canada IFM market in 2025, while commercial is projected to expand at the fastest pace with a 5.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Canada Integrated Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digitization of FM Operations Using AI, Advanced Analytics, and Predictive Maintenance | +1.6% | Canada-wide, early adoption concentrated in Ontario and British Columbia | Medium term (2-4 years) |

| Growing Demand for Outsourced Integrated FM Services | +1.4% | National, concentrated in major metropolitan areas - Toronto, Vancouver, Calgary, Montreal | Short term (≤ 2 years) |

| Sustainability Targets Driving Energy-Efficient FM Programs | +1.3% | National, strongest regulatory pull in British Columbia, Ontario, and Quebec | Long term (≥ 4 years) |

| Aging Commercial Real Estate Base Requiring Integrated Facilities | +0.9% | Ontario, Quebec, and Alberta urban cores, spill-over to Atlantic provinces | Medium term (2-4 years) |

| Workplace Experience Platforms Boosting Employee Productivity | +0.8% | Metropolitan areas, Toronto, Vancouver, Montreal, Calgary, early gains in secondary cities | Short term (≤ 2 years) |

| Procurement Efficiency Gaining Prominence Towards Total FM Lifecycle | +0.5% | National, public-sector concentration in Ontario and Western Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Digitization of FM Operations Using AI, Advanced Analytics, and Predictive Maintenance

Digital adoption is moving from pilot activity to mainstream procurement in the Canada integrated facility management (IFM) market because Canadian real estate operators are planning software upgrades at a faster pace than they were in 2024. Statistics Canada data showed that 18.6% of real estate rental and leasing firms planned AI software adoption in 2025, up from 10.9% in 2024, which signals a stronger appetite for platform-led operations across commercial portfolios. BOMA Canada reported in September 2025 that AI was actively used in only 23% of surveyed buildings, which shows that adoption intent is still ahead of day-to-day deployment.[1]Building Owners and Managers Association Canada, “BOMA Canada Member Research On Building Technology Adoption,” BOMA Canada, bomacanada.ca The same survey found that 63% of respondents cited limited internal expertise and 44% pointed to legacy integration problems, which helps explain why outsourced partners are gaining influence in digital retrofits. That gap is creating a practical opening in the Canada IFM market for providers that can combine computerized maintenance systems, building automation, sensor data, and service workflows inside one operating model. Providers that can deliver predictive maintenance and analytics without a difficult transition are likely to improve renewal rates because building owners want visible savings and fewer operational handoffs in the Canada integrated facility management market.

Growing Demand for Outsourced Integrated FM Services

The Canada integrated facility management market is expanding as organizations move away from fragmented vendor structures and toward a single operating partner that can manage risk, reporting, and service delivery across entire portfolios. Dexterra stated that IFM accounted for more than 20% of the outsourced FM market in North America, which supports the view that bundled contracts are becoming a more established part of enterprise facilities strategy. The appeal of outsourcing is increasingly tied to better data use because one provider can connect asset condition records, maintenance history, energy performance, and labor scheduling inside a common platform. Public institutions are an important part of this demand because federal properties, healthcare networks, and post-secondary campuses manage dispersed assets that are difficult to oversee through separate local contracts. The same logic is reaching mid-market owners, especially where tenants are expecting better waste handling, stronger energy performance, and clearer service accountability across shared spaces. This is keeping the Canada IFM market active in large cities where portfolio complexity is highest and where owners need operating models that can scale across multiple locations.

Sustainability Targets Driving Energy-Efficient FM Programs

Sustainability targets are widening the service scope in the Canada integrated facility management market because energy management, carbon reporting, and retrofit support are becoming part of normal contract expectations rather than optional add-ons. Natural Resources Canada released the Green Buildings Strategy in July 2024 and tied national building retrofit goals to broader infrastructure and code adoption efforts, which strengthened the policy base for long-cycle FM demand.[2]Natural Resources Canada, “Canada’s Green Buildings Strategy,” Government of Canada, natural-resources.canada.ca National Energy Code of Canada for Buildings 2025 introduced operational greenhouse gas limits for new buildings and a more aligned framework for energy performance in existing-building alterations, which makes technical compliance a larger part of facility delivery. Quebec's annual energy reporting rules and British Columbia's Zero Carbon Step Code add a province-level compliance layer that favors providers with bilingual teams, energy expertise, and multi-province coverage. These rules are shifting HVAC electrification, envelope reviews, ISO 50001-linked reporting, and ENERGY STAR Portfolio Manager benchmarking into standard contract discussions across the Canada IFM market. The carbon pollution price reached CAD 110 (USD 80.01) per tonne in 2026 and is scheduled to rise further by 2030, which gives owners a direct financial reason to use FM programs to cut building energy waste.

Aging Commercial Real Estate Base Requiring Integrated Facilities

Older building stock is increasing service intensity in the Canada integrated facility management (IFM) market because many assets now face overlapping equipment replacement, safety, accessibility, and energy upgrade needs. Statistics Canada reported CAD 52.9 billion (USD 38.50 billion), in non-residential building permits in 2025, while the institutional segment grew by CAD 1.9 billion (USD 1.38 billion) year over year, which shows that upgrade and expansion activity remained strong in hospitals, campuses, and care facilities. Much of Canada's commercial stock dates from the 1960s through the 1990s, so owners are now dealing with simultaneous lifecycle renewal across HVAC systems, fire and life safety infrastructure, and building controls. Natural Resources Canada stated that ENERGY STAR Portfolio Manager is used to benchmark more than 42,000 Canadian buildings, or close to one-third of commercial floor space, which gives owners a clearer view of underperforming properties.[3]Natural Resources Canada, “ENERGY STAR Portfolio Manager In Canada,” Government of Canada, natural-resources.canada.ca That visibility is supporting a shift from reactive maintenance to performance-based service contracts because asset owners can now link building condition, energy use, and occupant comfort more directly to operating outcomes. As a result, the Canada IFM market is seeing stronger demand from financial services, post-secondary, and process-driven sites where aging assets now affect both compliance and workplace performance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Integration and Transition Costs | -1.8% | National, most pronounced in smaller markets and owner-managed portfolios | Medium term (2-4 years) |

| Skilled Labor Shortages in Technical FM Roles | -1.5% | National, acutest in Ontario, Alberta, and British Columbia | Long term (≥ 4 years) |

| Data Privacy and Cybersecurity Concerns in Smart Buildings | -1.2% | National, concentrated in federal buildings and financial district assets | Short term (≤ 2 years) |

| Connected Assets and Digitizing in Brownfield Buildings | -0.9% | National, older commercial stock in Montreal, Toronto, Ottawa, and Calgary | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Initial Integration and Transition Costs

Transition costs remain a clear barrier in the Canada integrated facility management market because a shift from multiple contractors to one integrated model often requires new software, data migration, control system connectivity, and process redesign. That burden is most visible among owner-managed portfolios and public institutions where capital approval cycles are shorter than the operational payback period of a full integration program. The transition also creates service continuity concerns because several incumbent contracts may need to be transferred at the same time, which raises the risk of disruption during mobilization. Buyers therefore place more value on providers that can self-deliver through technical and non-technical services, since heavy subcontracting can weaken the control benefits that justify integration in the first place. This restraint is more pronounced in secondary cities where workforce depth is thinner and where large providers may not have the same operating density as they do in Toronto, Montreal, Calgary, or Vancouver. Even so, the Canada IFM market continues to move forward where clients can stage implementation, link scope changes to compliance needs, and prove service continuity early in the transition period.

Skilled Labor Shortages in Technical FM Roles

Labor availability is one of the most persistent limits on the Canada integrated facility management (IFM) market because demand for skilled technicians is rising faster than the supply of workers qualified to maintain complex building systems. The Future Skills Centre estimated that skilled trades shortages cost the Canadian economy USD 2.6 billion in lost GDP in 2024 and identified more than 10,250 excess vacancies in technical trades occupations.[4]Future Skills Centre, “Skilled Trades Shortages And Economic Impact In Canada,” Future Skills Centre, fsc-ccf.ca Employment and Social Development Canada projected 16,500 job openings for facility operation and maintenance managers across 2024 to 2033, with 76% of openings tied to retirement replacement rather than net new growth. The same labor pressure is particularly important because 49% of facility maintenance managers in Canada were aged 50 and over, which means succession pressure is already built into the workforce profile. Providers are responding with more remote monitoring, more automation, and more technician training, but those measures have not fully matched the pace of attrition in HVAC, electrical, fire systems, and building automation roles. This keeps execution risk elevated in the Canada IFM market at the same time that decarbonization retrofits and compliance-heavy Hard FM programs are becoming more central to contract growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Soft FM Leads Scale While Hard FM Gains From Technical Upgrades

Hard FM is projected to grow at a 7.12% CAGR from 2026 to 2031, which places it ahead of the overall pace of the Canada integrated facility management (IFM) market and shows how technical building operations are becoming more central to contract value. The main drivers are predictive maintenance, building automation system upgrades, HVAC electrification, and tighter fire and life safety obligations across institutional and commercial portfolios. BOMA Canada found in September 2025 that more than 70% of surveyed building operators planned to implement smart building automation, advanced analytics, predictive maintenance, and sustainability monitoring within the next 2 years, which supports a near-term pipeline for technical services. This demand is significant for the Canada integrated facility management industry because owners increasingly want one provider that can connect equipment performance, energy goals, and compliance work under a single operating framework. Sodexo Canada showed the return potential of this approach through a lighting upgrade project for a pharmaceutical client that generated annual energy savings of USD 266,000, reinforcing the case for folding efficiency measures into technical FM scope.

Soft FM held 58.23% of the Canada integrated facility management market share in 2025, reflecting the breadth of security, workplace, hygiene, catering, and support services embedded in large outsourced contracts. Security monitoring and access management are gaining more weight as AI-enabled surveillance and integrated control platforms are bundled into broader service packages instead of being handled as separate technology contracts. Workplace services are also adjusting to hybrid occupancy patterns, which is pushing operators toward cleaning and support programs that can change with real-time use levels rather than fixed schedules. This part of the Canada IFM market remains the largest by volume because it touches daily building experience across offices, hospitals, industrial campuses, and public facilities, while also creating recurring touchpoints that support wider contract retention.

By End-User: Industrial And Manufacturing Holds The Lead While Commercial Builds Momentum

Industrial and process sector accounted for 30.63% of the Canada integrated facility management market size in 2025, which reflects the service intensity of oil and gas, mining, food processing, automotive, and advanced manufacturing sites. These facilities depend on continuous technical maintenance, safety compliance, workforce support, and in many cases remote accommodation services, which makes integrated delivery more practical than fragmented local contracting. Dexterra reported FY2025 revenue of CAD 1.04 billion (USD 744.6 million), largely from IFM and workforce accommodation activities connected to Canada's industrial base, illustrating the scale of spending tied to these assets. Activity in the Montney and Duvernay corridors continued to support demand for camp management, maintenance, environmental services, and food programs that need to operate in difficult logistics settings. The segment is also raising the technical bar within the Canada IFM industry because listed industrial clients are embedding carbon reporting, water management, waste reduction, and safety performance into contract KPIs.

Commercial is forecast to expand at a 5.93% CAGR through 2031, supported by office portfolio rationalization, retail redevelopment into mixed-use sites, and the rapid build-out of data center capacity. ABB Canada stated that AI-related data center investment is increasing demand for smart building technologies and higher-voltage electrical infrastructure management, which fits directly with Hard FM and broader IFM delivery. This makes Commercial the most dynamic end-user group in the Canada integrated facility management market, even though it started from a smaller base than Industrial and Manufacturing. Healthcare, labs, and life sciences are also gaining steady momentum because aging demographics and major hospital and long-term care programs are expanding the need for technically demanding facility support. Government, infrastructure, post-secondary, hospitality, and retail users continue to sustain the wider Canada integrated facility management (IFM) market through large public contracts, campus outsourcing, and food-service consolidation trends that are broadening integrated service scope.

Geography Analysis

Ontario anchors the Canada integrated facility management market because it combines the country's largest office base, a major concentration of federal and provincial property, and a large stock of hospitals, campuses, and transportation-linked assets. BGIS's Infrastructure Ontario real property services relationship, effective from April 2024, covered more than 4,400 buildings and 194,000 acres of provincial property, which makes it one of the most significant IFM mandates in the country. Statistics Canada reported that Ontario's institutional segment led non-residential permit growth in late 2025, which points to continued facility demand from hospitals and post-secondary projects in the Greater Toronto Area and Ottawa. Ontario's updated building code took effect in January 2025 and required at least a 13% improvement in energy efficiency over the prior standard, which is widening retrofit work tied to HVAC and envelope upgrades. Quebec forms the second major cluster in the Canada integrated facility management market because annual energy reporting rules, bilingual service needs, and Montreal's industrial, pharmaceutical, and aerospace assets create a distinct operating environment for multi-province providers.

British Columbia and Alberta represent the next clear growth centers in the Canada integrated facility management market, but each is being shaped by a different demand pattern. British Columbia's Zero Carbon Step Code set measurable emissions expectations for most new buildings from March 2025, which made sustainability capability a more direct procurement requirement for owners in Vancouver and Victoria. The province's technology sector and port-driven logistics base are also creating opportunities in data centers and distribution facilities that need higher technical service content. Alberta remains the most industrial of the large provincial markets, with energy corridor activity supporting workforce accommodation, site maintenance, and specialized support services at remote and semi-remote assets. Dexterra's August 2025 acquisition of Right Choice Camps and Catering showed the continuing scale of this demand in Western Canada's gas regions, while Alberta's updated building code framework is starting to influence institutional and commercial FM procurement.

The rest of Canada is smaller in absolute value, but it still matters to the Canada integrated facility management market because public procurement, remote operations, and community-based delivery models remain active across several provinces. In the Prairies, Indigenous partnership structures are becoming more relevant in community and government facility programs, which is opening a more localized route to market for selected providers. Atlantic Canada continues to generate demand through long-running federal real property and facility management arrangements, including Public Services and Procurement Canada contract activity that remained active through 2025 and 2026. The territories and remote communities add a specialized layer to the Canada integrated facility management market because harsh logistics, accommodation needs, and technical service demands favor operators with established northern delivery infrastructure and dependable field execution.

Competitive Landscape

The Canada integrated facility management market has a moderately consolidated structure in which BGIS, Dexterra Group, JLL, Sodexo, CBRE Global Workplace Solutions, ISS, Aramark, Compass Group, and Cushman and Wakefield hold a strong position in large outsourced contracts, while regional specialists stay relevant in narrower verticals and local service areas. Technology is the main point of differentiation in this cycle because buyers want fewer operating silos and better visibility across work orders, asset condition, procurement, and energy performance. CBRE stated that its fmPilot platform manages 120,000 locations and processes 4.1 million annual work orders across its North American network, which shows the scale advantage that platform-based providers can bring to enterprise clients. JLL used Corrigo, Azara, JAGGAER, and Avetta in its WestJet mandate, which highlights how digital procurement and workflow tools are now part of the competitive discussion rather than a separate systems decision. Johnson Controls has also expanded the competitive standard through OpenBlue and outcome-based energy programs linked to Canada Infrastructure Bank project activity, while BGIS has continued to strengthen its position through smart building and clean technology capability.

Acquisition-led platform building is becoming a major feature of the Canada integrated facility management market because scale now matters in workforce coverage, technology spending, and the ability to self-deliver across multiple provinces. Dexterra reported Q1 2026 revenue of USD 275.5 million, up 15% year over year, which shows that inorganic expansion is being matched by solid operating momentum. Its July 2025 purchase of a 40% stake in Pleasant Valley Corporation added a U.S. IFM platform with proprietary technology, while the August 2025 acquisition of Right Choice Camps and Catering deepened its position in Western Canada's resource corridors. Dexterra also expanded and extended its revolving credit facility to CAD 425 million (USD 304.3 million), which underlines how much balance-sheet support is now being directed toward growth in the Canada integrated facility management market. These moves matter because large clients increasingly prefer partners that can combine national account management with local delivery density, technical depth, and a credible M&A-backed route to wider service coverage.

Several opportunity pockets are still open in the Canada integrated facility management market even with strong competition at the top of the supplier base. Life sciences and healthcare facilities are one such area because clean environments, validation-heavy systems, uptime requirements, and carbon targets all raise the need for specialized operating processes. JLL's April 2026 appointment of a Head of Life Sciences Canada points to further investment in this niche and signals that high-specification delivery is becoming a more deliberate growth lane. AI data center support is another developing space because smart electrification, cooling performance, backup power reliability, and higher-voltage infrastructure management are becoming more important to both owners and equipment vendors in the Canada integrated facility management market.

Canada Integrated Facility Management Industry Leaders

BGIS Global Integrated Solutions Canada LP

CBRE Group, Inc.

Dexterra Group Inc.

GDI Integrated Facility Services Inc.

Jones Lang LaSalle Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Elevate Service Group announced the acquisition of Think Green Solutions, establishing a stronger national lighting platform across Canada. The deal expands Elevate’s LED lighting, electrical, and maintenance services while increasing its presence in key Canadian markets. The acquisition also adds recurring revenue opportunities and supports Elevate’s strategy of building an integrated nationwide facilities services platform.

- March 2026: Bouygues Energies & Services Canada rebranded as Equans Services to unify its operations under one identity. The transition strengthened its presence in integrated facilities management, technical services, and sustainability solutions across Canada while aligning the company with Equans’ global branding strategy after Bouygues Group acquired Equans in 2022.

- September 2025: JLL announced that Canadian airline WestJet selected the firm as its integrated facilities manager for a 1.9-million-square-foot portfolio, including its Calgary headquarters and 17 airport locations nationwide. JLL will manage maintenance, safety, janitorial, HVAC, landscaping, and waste services while using advanced technology solutions to improve efficiency, reduce costs, and enhance employee and passenger experiences across WestJet’s operations.

- September 2025: Johnson Controls and Concordia University, Montreal, signed a 10-year outcome-based partnership for the net-zero retrofit of the Guy-De Maisonneuve Building, targeting a 50% reduction in energy consumption through air-sourced heat pumps, heat recovery, and occupancy controls. The project is designed to achieve LEED Existing Buildings, WELL Certified, and Canada Green Building Council Zero-Carbon Building Standards certifications.

Canada Integrated Facility Management Market Report Scope

The Canada Integrated Facility Management Market Report is Segmented by Service Type (Hard Facility Management [Asset Management, MEP and HVAC Services, Fire Systems and Safety, and Other Hard Facility Management Services], and Soft Facility Management [Office Support and Security, Cleaning Services, Catering Services, and Other Soft Facility Management Services]), End User (Commercial (includes BFSI, IT and Telecom, Retail and Warehouses, etc.), Hospitality (includes Eateries, Restaurants and Large-Scale Hotels),Institutional and Public Infrastructure (includes Government Establishments, Education, Transportation such as Airports and Railways, etc.), Healthcare (includes Public and Private Healthcare Facilities), Industrial and Process Sector (includes Manufacturing, Energy including Oil and Gas Exploration, Mining, etc.), and Other End-User Industries (Multi-House Residential, Entertainment, Sports and Leisure)). The Market Forecasts are Provided in Terms of Value (USD).

| Hard Facility Management | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard Facility Management Services | |

| Soft Facility Management | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft Facility Management Services |

| Commercial |

| Hospitality |

| Institutional and Public Infrastructure |

| Healthcare |

| Industrial and Process Sector |

| Other End-User Industries |

| Segmentation by Service Type | Hard Facility Management | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard Facility Management Services | ||

| Soft Facility Management | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft Facility Management Services | ||

| Segmentation by End User | Commercial | |

| Hospitality | ||

| Institutional and Public Infrastructure | ||

| Healthcare | ||

| Industrial and Process Sector | ||

| Other End-User Industries | ||

Key Questions Answered in the Report

What is driving growth in Canada integrated facility management services through 2031?

Growth is being supported by consolidated outsourcing, sustainability compliance, digitized building operations, and the need to manage older building stock more efficiently. The market is expected to reach USD 14.84 billion by 2031 at a 6.5% CAGR.

Which service type leads demand in Canada?

Soft FM led in 2025 with a 58.23% share because security, workplace, hygiene, catering, and support services remain deeply embedded in large, outsourced contracts across offices, healthcare, and industrial sites.

Why is Hard FM growing faster than Soft FM in Canada?

Hard FM is projected to grow at 7.12% CAGR through 2031 because predictive maintenance, BAS upgrades, HVAC electrification, and fire and life safety compliance are increasing the technical content of contracts.

Which end-user group contributes the most revenue?

Industrial and Manufacturing led with 30.63% share in 2025, reflecting the complexity of oil and gas, mining, food processing, automotive, and advanced manufacturing facilities that require integrated technical and support services.

Why is the Commercial segment gaining traction in facility management contracts?

Commercial is the fastest-growing end-user at 5.93% CAGR, supported by office portfolio changes, data center expansion, and retail redevelopment into mixed-use formats that need more advanced operating support.

What is the biggest operational risk for service providers in Canada?

Skilled labor shortages remain the main execution risk because technical roles in HVAC, electrical systems, fire systems, and building automation are under pressure from retirements and broader trades demand.

Page last updated on: