United States Hospice Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

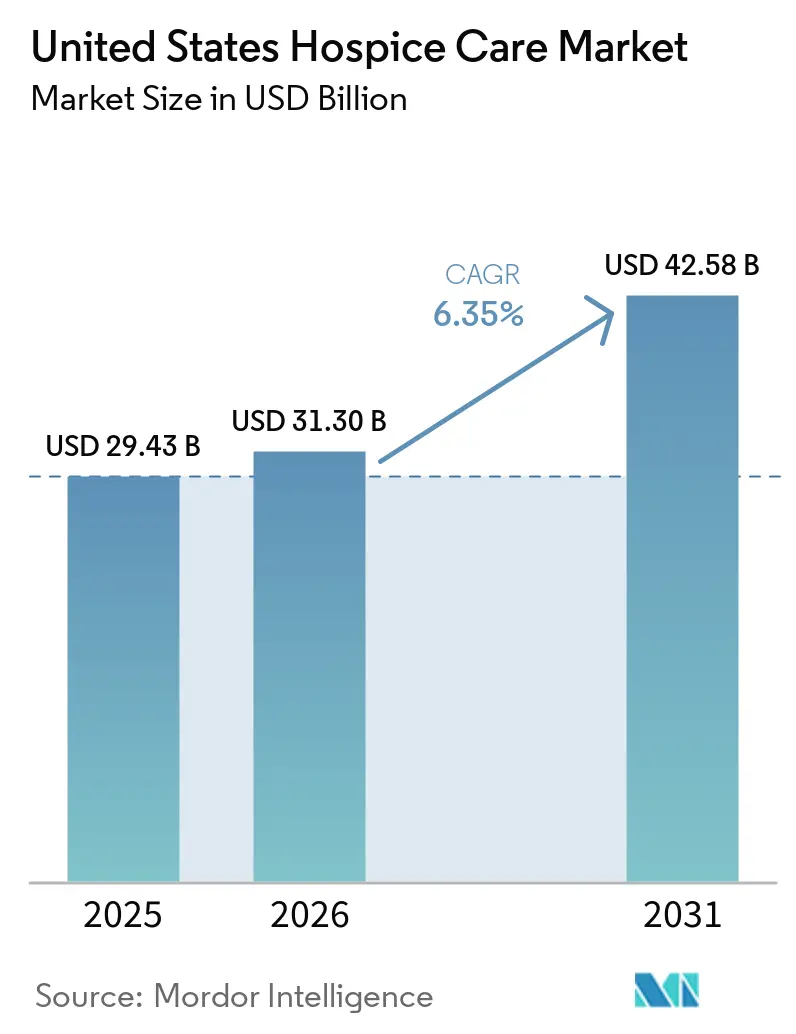

| Base Year Market Size (2025) | USD 29.43 Billion |

| Market Size (2026) | USD 31.30 Billion |

| Market Size (2031) | USD 42.58 Billion |

| Growth Rate (2026 - 2031) | 6.35% CAGR |

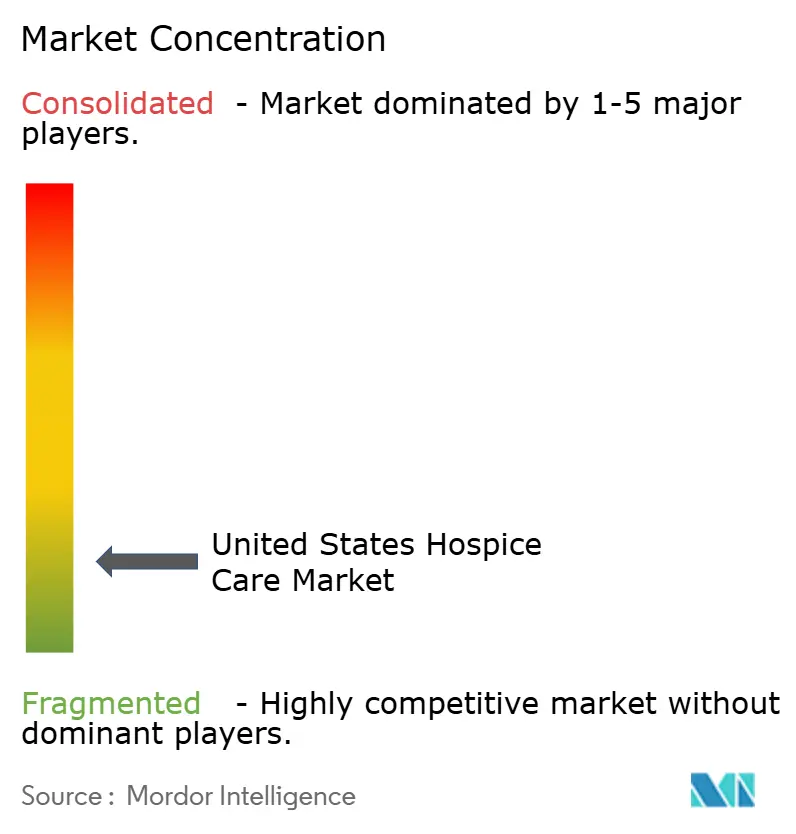

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Hospice Care Market Analysis by Mordor Intelligence

The United States Hospice Care Market size is projected to be USD 29.43 billion in 2025, USD 31.30 billion in 2026, and reach USD 42.58 billion by 2031, growing at a CAGR of 6.35% from 2026 to 2031.

Demand in the United States (US) hospice care market is being reinforced by the rise in older adults with multiple chronic conditions, the shift toward longer non-cancer stays, and the heavier revenue contribution from neurological and circulatory patients whose stays remain materially longer than those of cancer patients. Reimbursement conditions also remain supportive, with CMS finalizing a 2.6% hospice payment update for FY 2026 and MedPAC placing the projected 2026 fee-for-service Medicare margin at 9%, which continues to support operating expansion for scaled providers that can manage cap exposure and compliance requirements well. At the same time, the spread of home-based delivery, referral management technology, and AI-supported intake tools is helping providers convert a larger share of eligible patients without adding physical infrastructure at the same pace. Regulatory pressure is becoming more decisive in the US hospice care market, as OIG oversight, payment cap exposure, and tougher quality reporting requirements increasingly favor compliant and well-capitalized operators over smaller and more marginal providers.

Key Report Takeaways

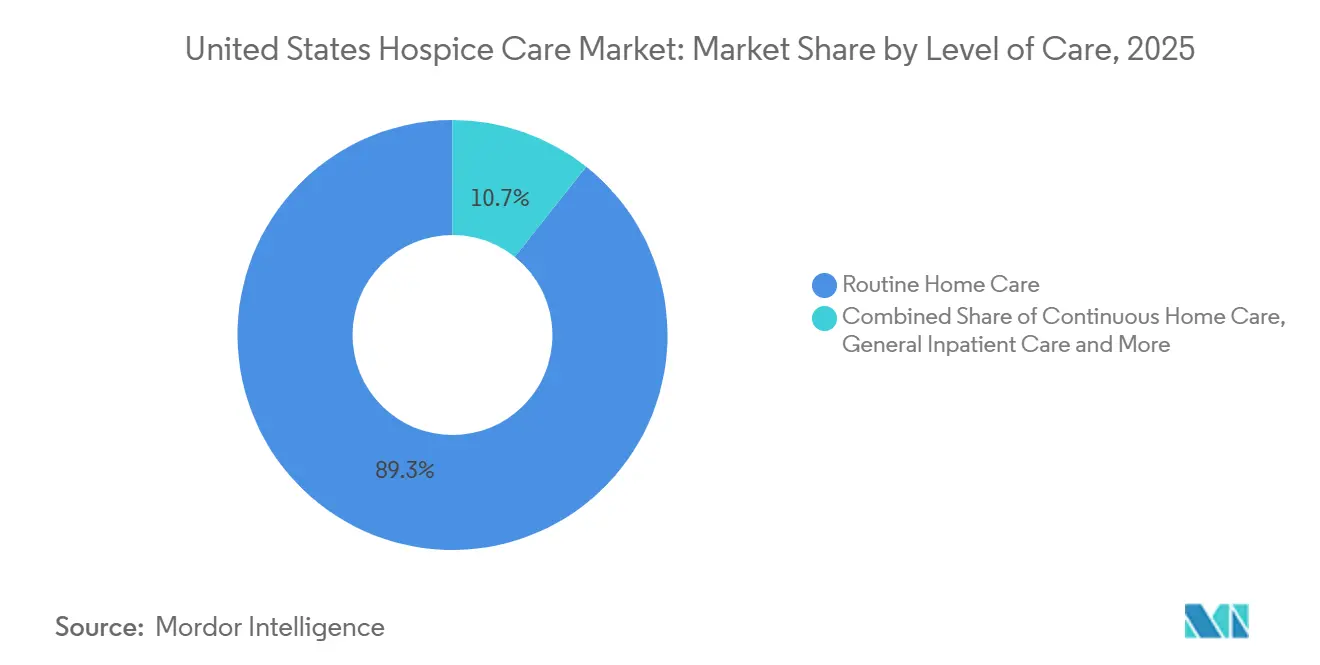

- By level of care, Routine Home Care held 89.31% of the US hospice care market share in 2025, while Continuous Home Care is projected to expand at a 9.38% CAGR through 2031.

- By care setting, Hospice Centers accounted for 61.24% share of the US hospice care market size in 2025, while Home Hospice Care is forecast to grow at a 9.52% CAGR through 2031.

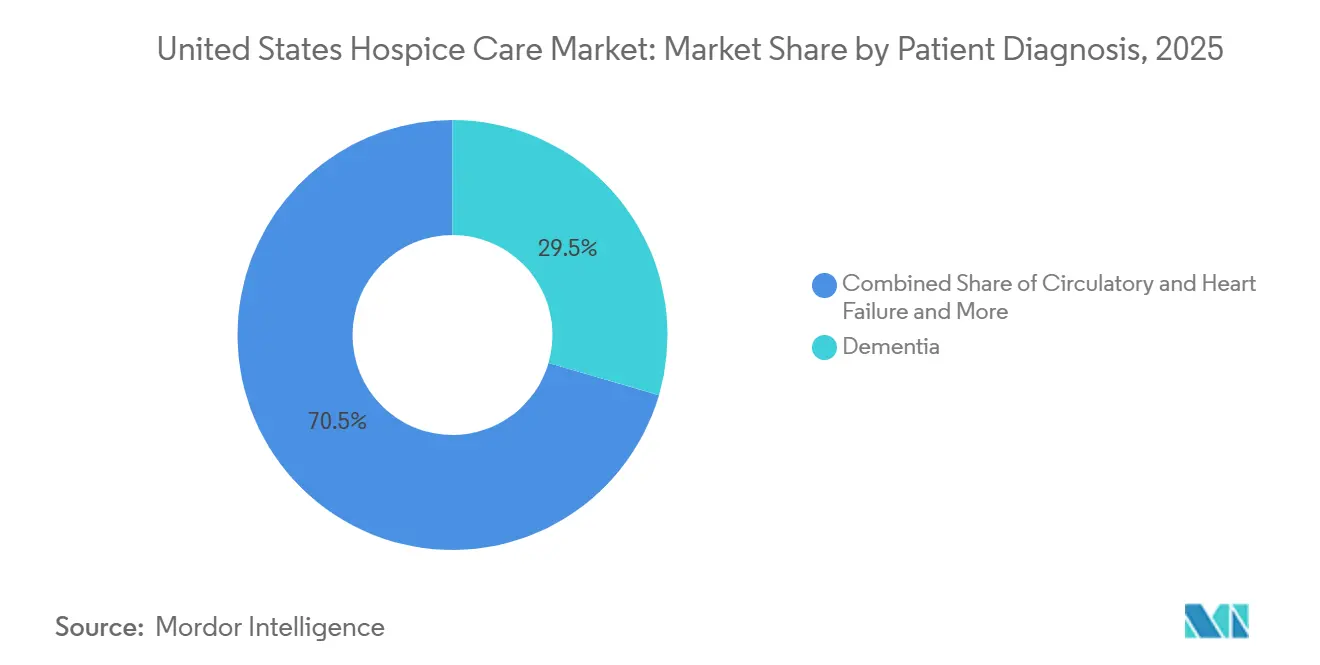

- By patient diagnosis, Dementia and Alzheimer's Disease represented 29.52% share of the US hospice care market size in 2025, while Circulatory and Heart Failure is expected to record the fastest growth at a 9.25% CAGR through 2031.

- By payer, Medicare commanded 88.52% of the US hospice care market share in 2025, while Private Insurance is projected to advance at an 8.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Hospice Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population and Multi-Morbidity | +1.8% | National, with concentrated effect in Florida, Arizona, California, and Texas | Long term (≥ 4 years) |

| Home-Based Hospice Preference | +1.3% | National, with spillover into rural and frontier markets gaining broadband-enabled telehealth access | Medium term (2-4 years) |

| Medicare and Payer Reimbursement Support | +1.1% | National, with margin uplift concentrated in high-wage index states such as California, New York, and New Jersey | Short term (≤ 2 years) |

| AI-Enabled Referral Analytics | +0.7% | National, with early adoption in large metropolitan markets in the South, West, and Mid-Atlantic | Medium term (2-4 years) |

| PE-Backed Micro-Market Roll-Ups | +0.6% | National, with near-term hotspots in Sun Belt and Midwest certificate-of-need states | Medium term (2-4 years) |

| Non-Cancer Disease-Specific Programs | +0.5% | National, with near-term traction in the South and West where cardiac and dementia burdens are highest | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Aging Population and Multi-Morbidity

The US hospice care market continues to draw long-range support from the expanding older population, with the number of Americans aged 65 and over projected to reach 65 million by 2026. Hospice use among Medicare decedents reached 52.9% in 2024, up by 1.2 percentage points from the prior year, which shows that penetration is still rising even after hospice became a mainstream care pathway. Multi-morbidity is also changing episode economics, because patients with neurological conditions averaged 169 hospice days in 2024, while cancer patients averaged 51 days, creating a materially different revenue profile for providers that can manage more complex symptom patterns. The gap remains meaningful in dementia, where 43% of Medicare beneficiaries diagnosed with dementia used hospice care, versus 45.4% for beneficiaries without dementia, leaving room for targeted outreach and earlier referral pathways[1]Alzheimer's Association, “2025 Alzheimer's Disease Facts and Figures,” Alzheimer's & Dementia, onlinelibrary.wiley.com. Hospice utilization among beneficiaries with end-stage renal disease reached 31.4% in 2024, and annual US deaths are projected to exceed 3.6 million by 2037, which keeps the demand base for the US hospice care market structurally durable over the forecast period.

Home-Based Hospice Preference

The US hospice care market is being pulled further toward home delivery, with 56% of all hospice claims provided at the patient's residence in 2024, while hospital-based hospice stays fell to 3% of all claims. This shift matters operationally because home hospice growth depends less on adding beds and more on improving admissions velocity, workforce coordination, and referral density around the patient's place of residence. Home Hospice Care is projected to expand at a 9.52% CAGR through 2031, which makes it the fastest-growing care setting in the US hospice care market. Providers that layer remote monitoring, telehealth triage, and stronger caregiver communication into the home model can absorb more admissions without a matching increase in fixed infrastructure or facility overhead. The result is a setting mix that increasingly favors platforms able to combine broad referral reach with flexible field operations, especially in suburban and rural territories where facility alternatives remain limited.

Medicare and Payer Reimbursement Support

The US hospice care market continues to benefit from a supportive reimbursement base, with CMS finalizing a USD 750 million increase in total Medicare hospice payments for FY 2026 through a 2.6% payment update. CMS set the FY 2026 hospice cap amount at USD 35,361.44 per patient, and MedPAC estimated the projected fee-for-service Medicare margin at 9% for 2026, which keeps hospice attractive relative to other post-acute service lines. Reimbursement support is not uniform across operators, because 28% of hospices exceeded the aggregate cap in FY 2023, with average repayments of USD 410,000 among above-cap providers. That pattern shows why large providers are becoming more selective in admission mix, length-of-stay management, and referral source development, especially in states with stronger growth but heavier cap exposure. Even with that discipline, Medicare remains the financial anchor of the US hospice care market, and its scale still gives compliant operators room to expand census, invest in documentation, and support more specialized programs.

AI-Enabled Referral Analytics

The US hospice care market is starting to see measurable gains from AI-supported referral workflows that reduce lag between referral, review, and admission. In January 2026, WellSky launched AI referral management capabilities, and one home health and hospice provider reported referral conversion improving from 20.7% to 44.8%, with referral throughput rising 38% using existing staff. Stanford Health Care also launched an LLM-based pilot in 2025 that reviewed clinical notes to identify inpatient hospice-eligible patients for daily team review, and the Phase 1 evaluation supported broader expansion. These tools matter because intake delays often translate directly into patient loss, lower conversion, and missed opportunities to admit patients before a hospital transfer or terminal deterioration changes the care path. With specialist supply still limited, AI-assisted intake is becoming a practical capacity substitute rather than a simple efficiency upgrade for the US hospice care market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Out-of-Pocket Burden and Payment Caps | -0.9% | National, with cap liability concentrated in Arizona, California, Nevada, and Texas | Short term (≤ 2 years) |

| Workforce Shortages and RN Turnover | -0.8% | National, with highest vacancy pressure in rural and frontier markets | Long term (≥ 4 years) |

| Heightened Compliance and Survey Scrutiny | -0.6% | National, with moratorium enforcement hotspots in Arizona, California, Georgia, Nevada, Ohio, and Texas | Short term (≤ 2 years) |

| Interoperability and Claims Friction | -0.4% | National, with higher friction in markets where MA plan penetration and post-acute technology adoption diverge | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Out-of-Pocket Burden and Payment Caps

The US hospice care market still faces friction from direct patient costs outside the standard Medicare hospice benefit, where uninsured or uncovered services can cost USD 150 to USD 500 per day depending on care intensity. The more persistent pressure point sits with the Medicare aggregate cap, because 28% of hospices exceeded the cap in FY 2023 and average excess payments among above-cap providers reached USD 410,000. Exposure is concentrated among freestanding and for-profit agencies, which represent 82% of all hospice providers but served 60% of Medicare hospice patients, showing a mismatch between provider composition and patient mix. This creates pressure for providers that depend heavily on long-stay and lower-acuity patients, because the same case mix that supports revenue growth can also trigger repayment risk and tighter audit attention. MedPAC's recommendation to eliminate the FY 2027 payment rate update adds another layer of uncertainty to forward planning in the US hospice care market, even though current margins still appear favorable on paper.

Workforce Shortages and RN Turnover

The US hospice care market is still constrained by staffing, even though some labor indicators improved in 2025. RN turnover measured 25.48% in 2025, down from 26.82% in 2024, while overall vacancy rates fell to 12.78% from 14.03%, but those gains remain modest against rising patient demand and expanding home-based workloads. Wage growth also slowed, with RN wage increases decelerating to 3.58% in 2025 from 3.97% in 2024, which weakens one of the few direct retention levers available to providers. Pressure is also building below the RN level, as CNA turnover rose to 29.02% in 2025 and undermined day-to-day care continuity for patients who depend on regular home visits and caregiver support[2]Hospital & Healthcare Compensation Service, “2025–2026 Hospice Salary & Benefits Report Summary,” LeadingAge, leadingage.org. The access impact is already visible, with 44.2% of Texas hospice agencies reporting in 2023 that they declined patients because of staffing constraints, which links workforce scarcity directly to lost admissions and unmet demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Level of Care: Continuous Home Care Redefines High-Acuity Home Delivery

Routine Home Care held 89.31% of the US hospice care market in 2025, which confirms that the benefit is still overwhelmingly built around a home-based daily service model rather than short institutional episodes. Its dominance is reinforced by Medicare design, because Routine Home Care accounted for 98.8% of all Medicare-covered hospice days, making it the financial and operational center of the US hospice care industry. CMS set the FY 2026 Routine Home Care rate at USD 230.83 per day for days 1 to 60 and USD 181.94 per day for day 61 onward, preserving the stepped payment structure that shapes provider behavior around longer stays. The scale of this level of care means even small shifts in diagnosis mix can reshape staffing burden, because circulatory, respiratory, and neurological patients often require more frequent symptom response than the historical cancer cohort. As a result, providers are being pushed to adjust care coordination, nurse scheduling, and aide coverage within the dominant service tier rather than relying on inpatient escalation as the default response.

Continuous Home Care is projected to grow at a 9.38% CAGR through 2031, making it the fastest-growing level of care in the US hospice care market as more patients remain at home during acute symptom crises. CMS set the FY 2026 Continuous Home Care rate at USD 1,674.29 for 24 hours of care, which reflects the premium intensity attached to this higher-acuity intervention. Growth in this level is tied closely to advanced heart failure, late-stage dementia, and other conditions where symptom spikes can be managed at home if skilled coverage is available quickly enough. General Inpatient Care and Inpatient Respite Care still remain necessary backstop services, especially when caregiver burden rises or home management fails, but they continue to represent a much smaller share of total days and revenue. The HOPE assessment tool, implemented in October 2025 under the Hospice Quality Reporting Program, adds another layer of operational discipline because missed requirements can trigger a 4% annual payment reduction, which weighs more heavily on smaller providers with thinner compliance capacity[3]Centers for Medicare & Medicaid Services, “2025 HQRP Information Gathering Report,” Centers for Medicare & Medicaid Services, cms.gov.

By Care Setting: Technology and Demographics Converge on Home Hospice

Hospice Centers held 61.24% of the US hospice care market in 2025, showing that freestanding and concentrated care settings still command the largest share of service delivery even as the home model expands. Facility concentration has historically offered stronger supervision, more predictable staffing, and easier scheduling control, which explains why dedicated centers retained the largest position in the setting mix. The RIHC Hospice Care Chartbook reported that inpatient hospice generated an average stay of 11 days and a median stay of 4 days in 2024, confirming that facility-based care remains concentrated in the final and more intensive phase of care. The provider base also supports this pattern, because for-profit freestanding hospices represented 82% of all providers in 2026 and continue to concentrate activity in settings where staffing, documentation, and margin management can be monitored more tightly. Even so, the setting mix is no longer static, because patient and family preferences are shifting faster than the installed base of dedicated hospice centers.

Home Hospice Care is forecast to grow at a 9.52% CAGR through 2031, making it the fastest-rising setting in the US hospice care market as care increasingly follows the patient rather than the facility. By 2024, 56% of all hospice claims were delivered at the patient's residence, and assisted living facilities accounted for another 21%, which shows that most hospice episodes are already anchored outside hospitals. Hospitals are steadily losing relevance in this setting mix, with hospital-based hospice stays accounting for only 3% of claims in 2024 and hospital-based provider count falling 4.1% between 2023 and 2024. This transition strengthens operators that can run distributed field teams, maintain reliable after-hours response, and use remote triage to support symptoms before they become inpatient events. Over time, that makes home capability less of an add-on service and more of a core competitive requirement inside the US hospice care market.

By Patient Diagnosis: Cardiac and Neurovascular Programs Unlock a New Revenue Layer

Dementia and Alzheimer's Disease held 29.52% of the US hospice care market by patient diagnosis in 2025, which makes neurocognitive illness the largest diagnosis-driven demand pool in current hospice utilization. CMS reported that 34% of hospice stays included a neurocognitive disorder diagnosis, which confirms how deeply dementia-related care now shapes staffing patterns, caregiver education needs, and stay duration across providers. The diagnosis mix also highlights an access problem, because hospital-based palliative consultation and earlier referral still remain inconsistent for dementia patients who would benefit from hospice before a late and crisis-driven transition. Federal attention to upstream dementia care is increasing, and that raises the likelihood that earlier identification and referral tools will become more common across the US hospice care market over time. Cancer now accounted for only 22% of hospice stays in 2024, which marks a clear break from the older cancer-centered hospice model that defined the program decades ago.

Circulatory and Heart Failure is projected to grow at a 9.25% CAGR through 2031, making it the fastest-growing diagnosis segment in the US hospice care market. Circulatory conditions represented 30% of hospice stays in 2024 and generated average per-stay Medicare spending of USD 15,867, which was 78% higher than the level recorded for cancer patients. The same group also averaged 104 days of stay, versus 47 days for cancer, which explains why cardiac and vascular programs are gaining commercial weight across the provider landscape. Respiratory disease, stroke and neurovascular disease, and chronic kidney disease add further room for growth because hospice penetration in these groups still trails terminal incidence, especially among non-White beneficiaries. The Alzheimer's Association reported that 47% of Hispanic Medicare decedents with dementia received hospice care, versus 68% among White patients, which points to a sizable access and outreach gap that can still expand utilization if referral barriers are addressed.

By Payer: Medicare Dominates, While Private Coverage Broadens the Revenue Base

Medicare held 88.52% of the US hospice care market in 2025, which keeps the payer structure heavily centered on the federal hospice benefit. Medicare spending on hospice services reached USD 28.2 billion in 2024, average payment stood at USD 191 per day of care, and total hospice days reached 148.2 million, up 7.7% year over year. That scale gives the payer segment its stability, but it also means revenue concentration remains closely tied to policy decisions on cap calculations, quality reporting, and annual payment updates. MedPAC's projected 2026 fee-for-service margin of 9% shows why hospice remains commercially viable under Medicare, even while compliance costs are rising across the US hospice care industry. Medicaid still plays a more limited role and remains more closely linked to dual-eligible populations in nursing facilities and other institutional settings.

Private Insurance is projected to grow at an 8.25% CAGR through 2031, making it the fastest-growing payer segment in the US hospice care market. Growth is being supported by stronger employer benefit integration, wider awareness among under-65 patients with terminal diagnoses, and the gradual broadening of palliative and hospice coverage outside traditional Medicare pathways. The path is not frictionless, because CMS ended the VBID Hospice Benefit Component in December 2024 after declining participation and implementation challenges, which limited the near-term pace of managed care integration. Industry associations also told CMS that hospice providers were left outside earlier interoperability funding efforts, which helps explain why claims exchange and plan coordination remain weaker than in other post-acute segments. Even so, private coverage is becoming a meaningful diversification layer for providers that want to reduce overdependence on one reimbursement channel within the US hospice care market.

Geography Analysis

Utah recorded a 68% hospice utilization rate among Medicare decedents in 2024, while New York stood at 29%, which shows how widely hospice adoption still varies across the country. Rhode Island followed at 63%, while Florida, Arizona, and Wisconsin each ranked among the higher-utilization states, confirming that the strongest adoption is not confined to one region alone. The South and West still carry the heaviest revenue intensity in the US hospice care market, with California's average Medicare spending per hospice stay at USD 19,500 in 2024 and Texas at USD 15,449, both above the USD 14,068 national average. Those spending patterns point to longer stays, greater case complexity, and broader penetration of diagnoses that remain enrolled for more days before death. At the same time, areas with rapid provider expansion and high cap exposure are seeing closer oversight, which raises the operating bar for providers that want to scale in already attractive Sun Belt geographies.

The Northeast presents a different pattern inside the US hospice care market, because dense hospital systems and late referral behavior continue to depress use despite older and well-insured populations. New York averaged 64 hospice days in 2024, versus 107 days in California, which shows that low-utilization states are also often late-entry states with shallower episode depth. The same pattern extends to DC at 32% and Alaska at 30%, where hospice use remained well below the national leaders in 2024. Research in the American Journal of Hospice & Palliative Medicine found that states with shorter hospice durations show a higher share of neoplastic disorders as primary diagnoses, which supports the view that cancer-centered referral habits still narrow utilization depth in certain regions. The Midwest shows a steadier profile, with Wisconsin and nearby states benefiting from more mature nonprofit infrastructure and quality performance that often tracks above national norms.

Frontier counties recorded a 38.8% hospice utilization rate in 2024, which left rural America well below the national average and exposed a clear service gap in the US hospice care market. Rural provider supply is also tightening, with rural hospices declining 0.5% in 2024 while urban providers grew 3.1%, which widens access differences over time. Spending data reflect the same disparity, with North Dakota at USD 13,648 per decedent and Wyoming at USD 13,935, compared with USD 38,205 per decedent in California. Telehealth-enabled coordination, AI-supported remote triage, and more portable clinical protocols offer one of the few realistic ways to close these geographic gaps without matching every underserved county with new fixed-site infrastructure.

Competitive Landscape

The US hospice care market remains highly fragmented, with the top 10 providers holding a significant share, which leaves the field open for regional consolidation and selective scale advantages. Fragmentation persists even as for-profit operator count continues to rise, because provider growth is spread across many local and regional agencies rather than a handful of nationally dominant platforms. In 2024, for-profit hospice provider count increased 4.8%, while nonprofit providers declined 7.4%, which shows that market expansion is being led by ownership groups with stronger appetite for growth and acquisition. This shift matters because ownership structure increasingly affects referral strategy, compliance investment, and the willingness to scale into denser metropolitan and Sun Belt territories. The competitive center of the US hospice care market is therefore moving toward operators that can balance growth discipline, documentation quality, and clinical specialization without becoming overly exposed to cap repayments or audit risk.

One important strategic move came in August 2025, when the Department of Justice required broad divestitures to resolve its challenge to UnitedHealth's acquisition of Amedisys, making scale possible only with clear structural remedies and tighter market scrutiny. That action shows that large combinations in the US hospice care market can still proceed, but they must now clear a higher threshold on competition and asset concentration. A second competitive move is taking place inside care delivery rather than ownership, where providers are building disease-focused pathways around dementia, cardiac decline, and complex chronic illness to secure referrals earlier in the terminal journey. A third move is operational, with providers adopting AI-supported referral screening and intake tools to improve conversion, shorten response times, and protect admissions volume during labor shortages. These strategies do not eliminate fragmentation, but they do widen the performance gap between organizations that can systematize referrals and those that still rely on slower and less data-driven intake processes.

Quality and compliance now shape competitive position almost as much as local referral reach in the US hospice care market. The HOPE tool raised reporting demands in late 2025, and payment penalties for noncompliance can reach 4%, which is a sizable financial burden for operators that lack formal documentation infrastructure. OIG's continuing focus on newly enrolled hospice providers adds further pressure, especially in markets where rapid entry already raised questions about billing patterns and program integrity. Taken together, these conditions favor established providers that can absorb compliance costs, standardize intake, and build specialized programs while still operating in a market where share remains widely dispersed.

United States Hospice Care Industry Leaders

Gentiva

VITAS Healthcare

Amedisys (UnitedHealth Group)

Compassus

AccentCare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: The Centers for Medicare & Medicaid Services (CMS) imposed a moratorium on new Medicare hospice agency enrollments to address integrity concerns. Six high-risk states, Arizona, California, Georgia, Nevada, Ohio, and Texas, face stricter oversight, including mandatory site visits and a public hospice scoring system. These measures disrupt new hospice launches, favoring established operators in certificate-of-need markets.

- May 2026: Private equity firm Kinderhook Industries acquired Enhabit, a home health and hospice provider, for USD 762 million, with a total deal value of USD 1.1 billion. Dallas-based Enhabit operates 251 home health and 117 hospice locations across 35 states. Kinderhook plans to invest in clinical quality and data analytics.

United States Hospice Care Market Report Scope

As per the scope of the report, hospice care is specialized medical care focused on providing comfort, support, and quality of life for individuals with serious, chronic, or terminal illnesses. It emphasizes symptom management, pain relief, emotional support, and spiritual care, typically when curative treatments are no longer effective.

The United States hospice care market is segmented by level of care into routine home care, continuous home care, general inpatient care, and inpatient respite care. By care setting, the market is categorized into hospice centers, home hospice care, hospitals, and skilled nursing facilities. By patient diagnosis, the segmentation includes dementia and Alzheimer's disease, circulatory and heart failure, cancer, respiratory disease, stroke and neurovascular disease, chronic kidney disease, and other terminal diagnoses. By payer, the market is divided into Medicare, Medicaid, private insurance, and out-of-pocket and other payers. For each segment, the market size and forecast are provided in terms of value (USD).

| Routine Home Care |

| Continuous Home Care |

| General Inpatient Care |

| Inpatient Respite Care |

| Hospice Centers |

| Home Hospice Care |

| Hospitals |

| Skilled Nursing Facilities |

| Dementia and Alzheimer's Disease |

| Circulatory and Heart Failure |

| Cancer |

| Respiratory Disease |

| Stroke and Neurovascular Disease |

| Chronic Kidney Disease |

| Other Terminal Diagnoses |

| Medicare |

| Medicaid |

| Private Insurance |

| Out-of-Pocket and Other Payers |

| By Level of Care | Routine Home Care |

| Continuous Home Care | |

| General Inpatient Care | |

| Inpatient Respite Care | |

| By Care Setting | Hospice Centers |

| Home Hospice Care | |

| Hospitals | |

| Skilled Nursing Facilities | |

| By Patient Diagnosis | Dementia and Alzheimer's Disease |

| Circulatory and Heart Failure | |

| Cancer | |

| Respiratory Disease | |

| Stroke and Neurovascular Disease | |

| Chronic Kidney Disease | |

| Other Terminal Diagnoses | |

| By Payer | Medicare |

| Medicaid | |

| Private Insurance | |

| Out-of-Pocket and Other Payers |

Key Questions Answered in the Report

What is the current and forecast value of US hospice care?

The US hospice care market stood at USD 29.43 billion in 2025, is estimated at USD 31.30 billion in 2026, and is projected to reach USD 42.58 billion by 2031 at a 6.35% CAGR.

What is driving growth in hospice care demand in the United States?

The main drivers are the aging population, rising multi-morbidity, longer stays for neurological and circulatory diagnoses, home-based care preference, and supportive Medicare reimbursement.

Which level of care leads hospice service delivery in the United States?

Routine Home Care led with an 89.31% share in 2025 and also represented 98.8% of Medicare-covered hospice days, which keeps it at the center of service delivery and reimbursement.

Which patient groups are expanding fastest in hospice use?

Dementia and Alzheimer's Disease remained the largest diagnosis segment at 29.52% in 2025, while Circulatory and Heart Failure is expanding fastest at a 9.25% CAGR through 2031.

Why is home hospice becoming more important?

Home Hospice Care is projected to grow at a 9.52% CAGR through 2031, supported by patient preference, the fact that 56% of 2024 claims were delivered at home, and better use of telehealth and remote triage.

Page last updated on: