Hospice Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

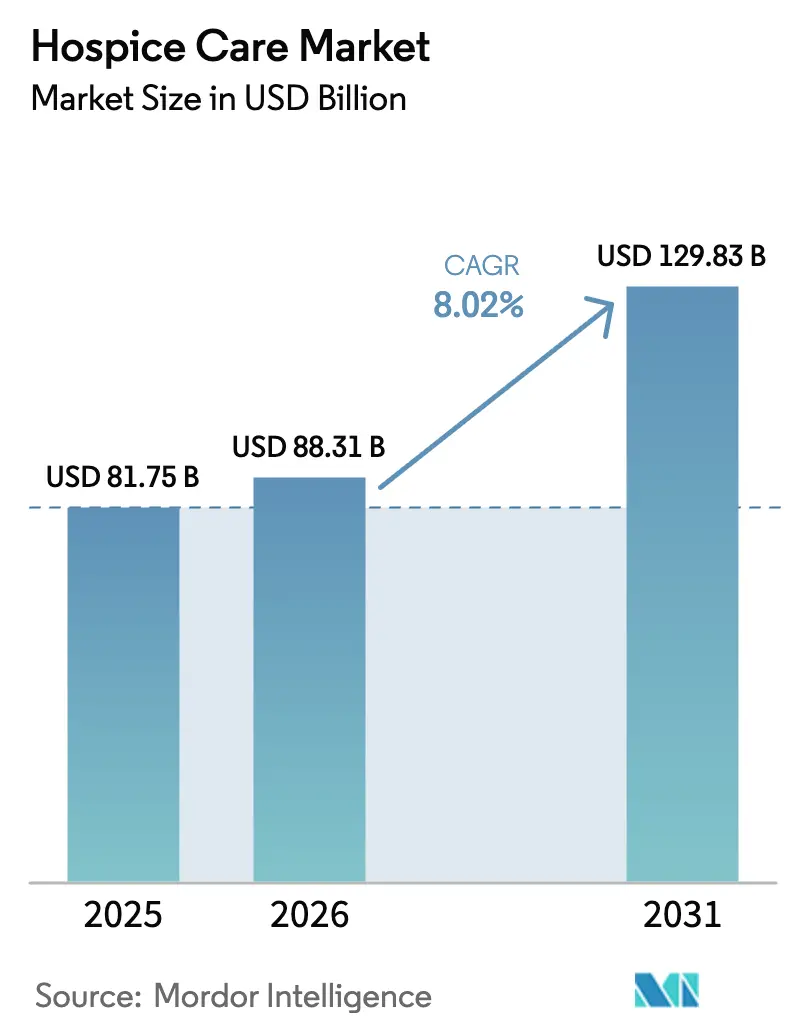

| Market Size (2026) | USD 88.31 Billion |

| Market Size (2031) | USD 129.83 Billion |

| Growth Rate (2026 - 2031) | 8.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Hospice Care Market Analysis by Mordor Intelligence

The global hospice care market size was valued at USD 81.75 billion in 2025 and estimated to grow from USD 88.31 billion in 2026 to reach USD 129.83 billion by 2031, at a CAGR of 8.02% during the forecast period (2026-2031). Robust expansion rests on an unprecedented rise in the older-than-65 population, widened reimbursement, and technology-enabled referral systems. Demographic pressure converges with strong patient preference for home-based services, while artificial-intelligence (AI) tools shorten the interval between terminal diagnosis and hospice enrollment. Medicare’s 2.9% payment increase for fiscal 2025, along with the upcoming Hospice Outcomes and Patient Evaluation (HOPE) tool, underpins revenue visibility for providers. Meanwhile, private insurers are broadening benefits to capture unmet demand, and private-equity ownership is accelerating consolidation, reshaping competitive dynamics.

Key Report Takeaways

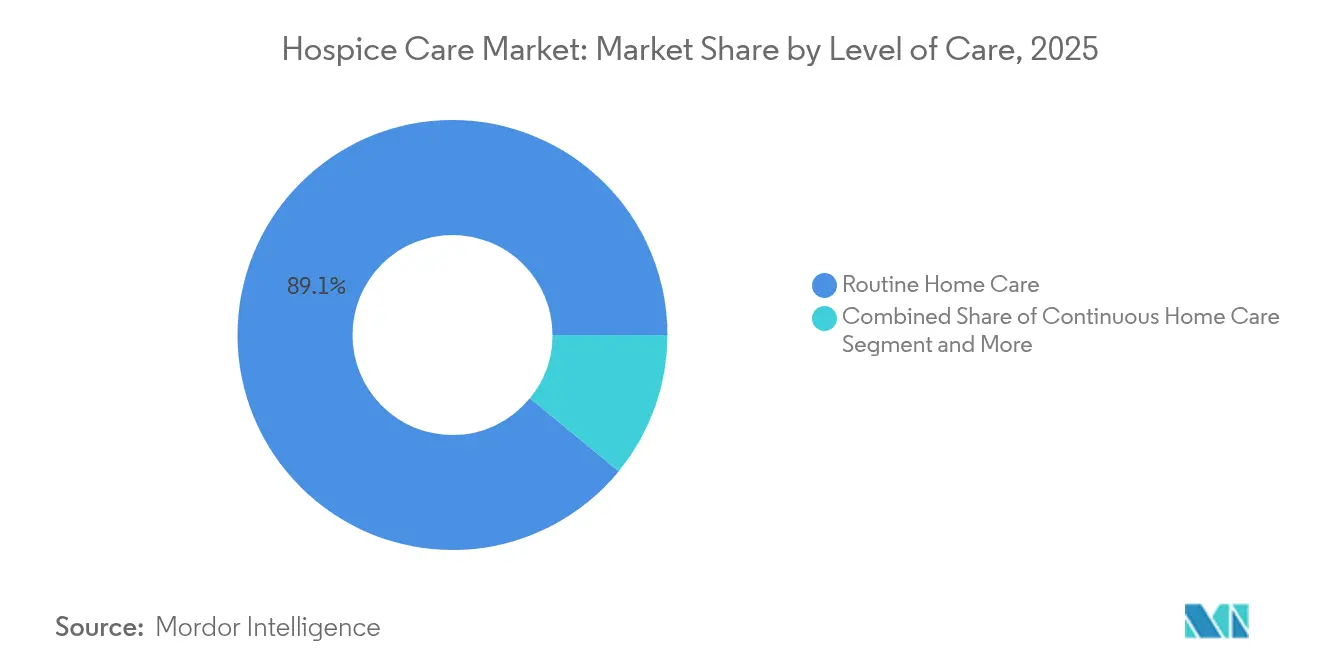

- By level of care, routine home care led with 89.08% hospice care market share in 2025; continuous home care is projected to expand at a 11.64% CAGR through 2031.

- By service provider, hospice care centers accounted for 60.98% of the hospice care market size in 2025, while home settings record the highest 10.32% CAGR to 2031.

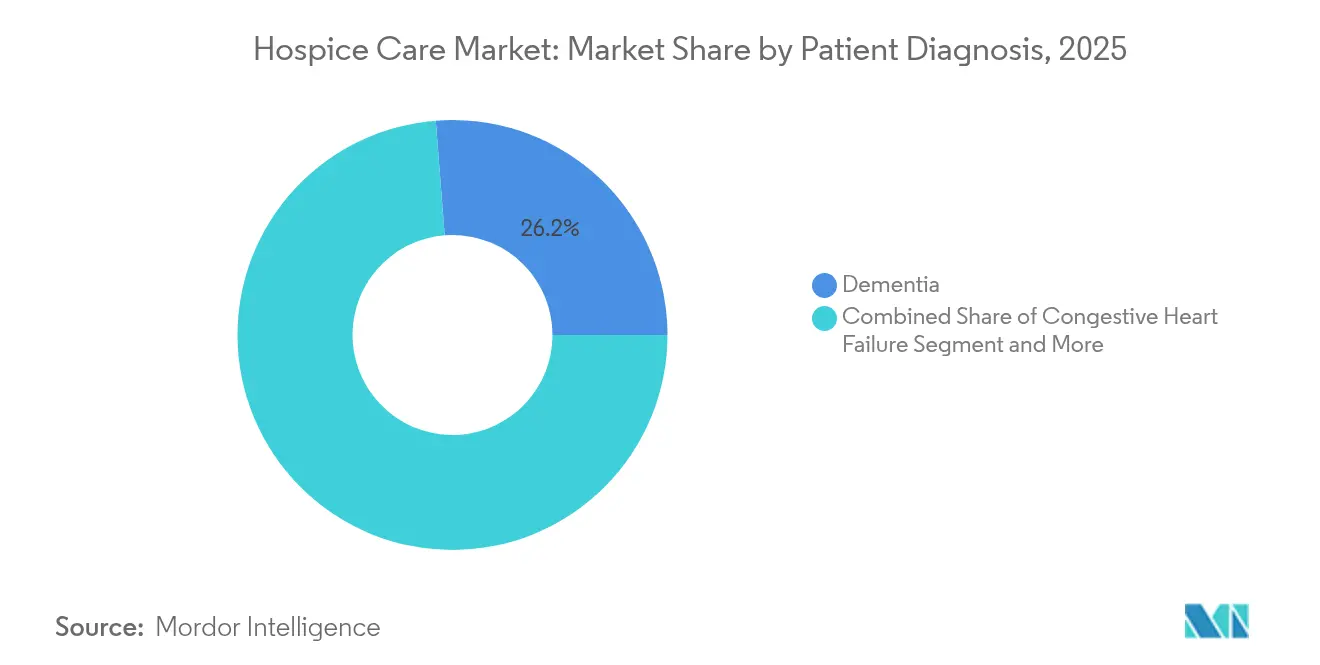

- By patient diagnosis, dementia commanded 26.24% of the hospice care market share in 2025; congestive heart failure is advancing at a 10.41% CAGR through 2031.

- By payer, Medicare financed 88.15% of the hospice care market size in 2025, yet private insurance exhibits the fastest 8.79% CAGR to 2031.

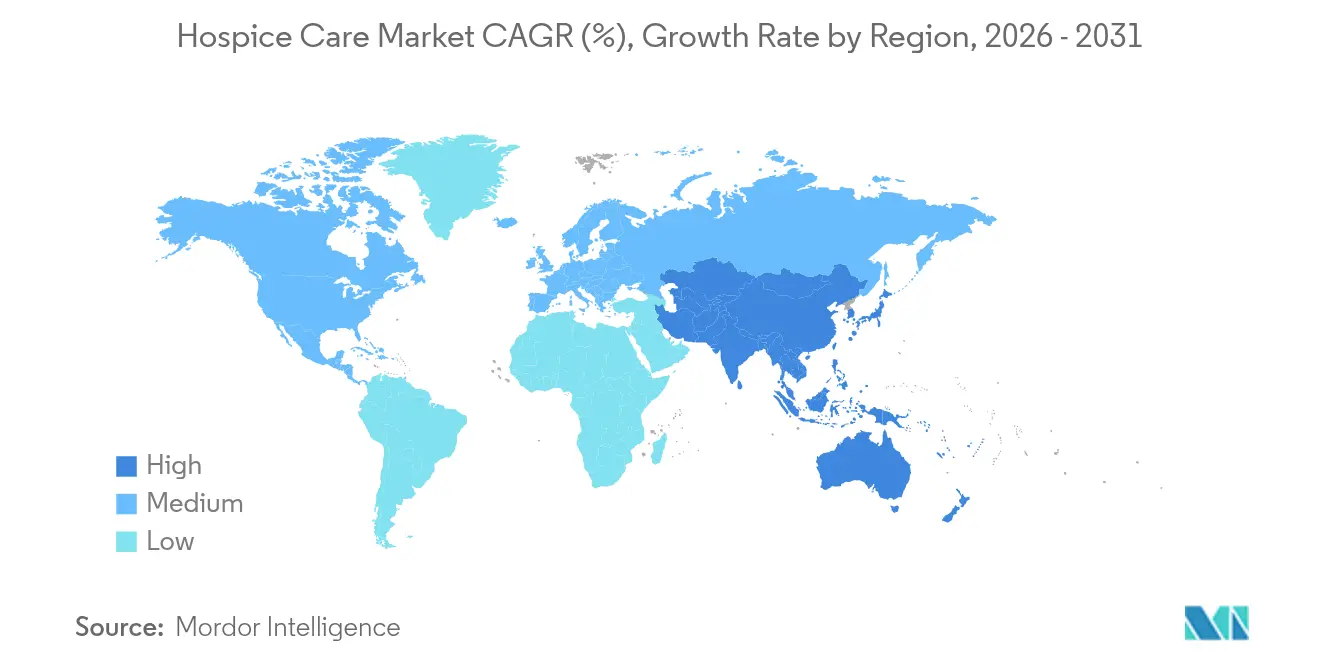

- By geography, North America retained the largest 40.95% share of the hospice care market in 2025, whereas Asia-Pacific registers the swiftest 10.74% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Hospice Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapidly Ageing Population & Rise In Multi-Morbidity | +1.3% | Global, with highest impact in North America, Europe, and Asia-Pacific | Long term (≥ 4 years) |

| Preference For Home-Based Routine Home Care (RHC) | +1.0% | Global, particularly strong in North America and Europe | Medium term (2-4 years) |

| Expanding Medicare/Medicaid & Private-Payer Reimbursement | +0.8% | North America primary, expanding to select Asia-Pacific markets | Medium term (2-4 years) |

| AI-Enabled Referral Analytics Shortening Diagnosis-To-Hospice Interval | +0.7% | North America and Europe early adoption, Asia-Pacific emerging | Short term (≤ 2 years) |

| Micro-Market Roll-Ups By PE-Backed For-Profit Chains | +0.6% | North America dominant, selective European markets | Medium term (2-4 years) |

| Culturally-Tailored, Non-Cancer Disease Programs | +0.5% | Asia-Pacific leading, North America and Europe following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapidly ageing population & rise in multi-morbidity

Global life expectancy gains translate into a doubling of the 65-plus cohort by 2050, sharply lifting the prevalence of multiple chronic diseases that require coordinated end-of-life support. Length of stay has lengthened for neurological conditions, reflecting evolving utilization patterns and reinforcing demand for longitudinal care. Advance-care planning multiplies the likelihood of hospice use more than fivefold, indicating the material influence of proactive discussions on service uptake. Collectively, these forces divert resources toward palliative pathways, reinforcing the economic case for home-based models that lower acute-care costs without compromising outcomes.

Preference for home-based routine home care (RHC)

Routine home care absorbs 89.51% of service days because patients value dignity and familiarity, and families associate home settings with emotional comfort. Medicare’s per-day payment of USD 218.33 for the first 60 days sustains provider economics while reinforcing the RHC tilt. Tele-monitoring and remote symptom assessment now enable clinicians to manage higher acuity from a distance, further emboldening the shift toward the home. As hospital-at-home programs mature, upstream acute episodes increasingly transition directly into hospice, accelerating RHC volumes.

Expanding Medicare/Medicaid & private-payer reimbursement

CMS raised aggregate hospice payments by 2.9% in fiscal 2025 and set the cap at USD 34,465.34, a decision that injects an estimated USD 790 million in additional revenue[1]Centers for Medicare & Medicaid Services, “FY 2026 Hospice Wage Index Proposed Rule Fact Sheet,” cms.gov. Proposed fiscal 2026 rules add another 2.4% uplift, sustaining predictable growth in the public-payer base. Private insurers respond by enhancing hospice benefits, propelling a forecast 9.14% CAGR in privately funded episodes. These combined moves reduce financial barriers, especially for middle-income families who fall outside Medicaid thresholds yet cannot sustain prolonged out-of-pocket spending.

AI-enabled referral analytics shortening diagnosis-to-hospice interval

Hospice providers deploying AI cut e-prescribing times from 20 seconds to 2-3 seconds while achieving 99% drug-codification accuracy, freeing clinical staff for direct care. Predictive models identify eligibility earlier, countering historical delays that eroded both patient quality of life and cost savings. Although ethical safeguards remain paramount, early evidence shows AI tools improve symptom management and streamline cross-continuum data exchange, positioning digital adoption as a strategic differentiator.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-Of-Pocket Costs & Annual Payment Caps | -0.7% | North America primary, emerging in private-pay markets globally | Medium term (2-4 years) |

| Hospice Workforce Shortages & >25% RN Turnover | -0.5% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| CMS Special Focus Program Heightening Compliance Burden | -0.3% | North America specific, regulatory spillover to other regions | Short term (≤ 2 years) |

| Data-Interoperability Gaps Delaying Claims | -0.3% | Global, particularly acute in markets with fragmented EHR systems | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High out-of-pocket costs & annual payment caps

Despite cap increases, 18.6% of U.S. hospices surpassed the fiscal-2020 limit, compressing margins and curtailing service expansion[2]Centers for Medicare & Medicaid Services, “Hospice Special Focus Program,” cms.gov. Families still face daily RHC bills of USD 172.35 after the first 60 days, while continuous home care commands USD 1,565.46 per day, discouraging extended utilization. Where private insurance is unavailable or benefits are exhausted, cost exposure deters timely enrollment, particularly for culturally diverse, lower-middle-income households.

Hospice workforce shortages & Greater Than 25% RN turnover

Registered nurse turnover above 25% drains institutional knowledge and inflates recruitment costs. Although the U.S. RN workforce is projected to reach 4.56 million by 2035, only a portion possess the pain-management and counseling skills integral to hospice practice. Competition from acute-care employers, emotional fatigue, and rural maldistribution constrain provider capacity, widening geographic inequities.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Level of Care: Routine home care dominance drives market foundation

Routine home care generated 89.08% of 2025 revenues, anchoring the hospice care market through services delivered in familiar surroundings under a per-day reimbursement model. Continuous home care, although small, is forecast to rise 11.64% annually as complex multimorbidity and caregiver stress stimulate demand for round-the-clock clinical oversight. General inpatient care remains a critical escalation pathway for uncontrolled symptoms, while inpatient respite eases caregiver burnout. The hospice care market size attributable to continuous home care is projected to expand fastest as technology and hospital-at-home models make high-acuity home treatment feasible.

Care-intensity shifts illustrate a broader evolution from episodic to longitudinal management. AI-driven triage flags symptom deterioration, triggering timely transitions from routine to continuous care. Hospital-at-home programs, now authorized for more than 320 U.S. hospitals, could migrate USD 265 billion of services into residences by 2025. This dynamic positions continuous home care as the next frontier for value-based contracting inside the hospice care market.

By Service Provider: Hospice care centers lead while home settings accelerate

Specialized hospice care centers captured 60.98% of 2025 revenue and underpin the hospice care market by offering multidisciplinary teams, on-site pharmacies, and bereavement services. Operating scale yields lower overhead per patient while maintaining robust quality metrics benchmarked through the new HOPE tool. Home settings, though smaller today, will outpace all others with a 10.32% CAGR through 2031 as virtual ward infrastructure spreads and families prioritize staying together.

Tele-triage, remote vitals, and AI-powered symptom scorers enable clinicians to deliver institution-level care in living rooms, driving payer enthusiasm for the lower-cost setting. Partnerships such as Providence Alaska Medical Center’s virtual hospice pilot underscore health-system appetite for integrated, tech-enabled models. Hospitals continue to feed referrals, and skilled nursing facilities fill gaps for patients whose functional limitations exceed routine home capabilities, balancing the provider mix within the hospice care market.

By Patient Diagnosis: Dementia leadership meets cardiac growth acceleration

Dementia accounted for 26.24% of revenue in 2025, reflecting growing recognition of advanced cognitive decline as a terminal path. Nonetheless, eligibility criteria often lag clinical reality, suppressing penetration. Congestive heart failure, while smaller, is projected to climb 10.41% annually as specialized protocols validate hospice’s role in symptom relief and family counseling. Cancer remains substantial owing to well-established pathways, yet non-cancer conditions collectively now constitute the majority of admissions, broadening the hospice care market.

Integrated home-health routes raise hospice conversion likelihood, especially for patients without dementia who start home services earlier in their disease trajectory. Prognostic tools such as cardiac risk indices and dementia staging scales boost physician confidence in timely referrals, aligning clinical need with benefit eligibility and sustaining segment diversification.

By Payer: Medicare dominance faces private-insurance growth challenge

Medicare financed 88.15% of hospice days in 2025, cementing its centrality to the hospice care market. The Hospice Benefit’s per-diem structure offers revenue predictability, although annual caps pressure providers exceeding expected lengths of stay. Private insurance, the fastest-growing 8.79% segment, increasingly mirrors public coverage while layering disease-management add-ons to differentiate products.

Regulatory shifts may alter payer mix. The Hospice Care Act 2024 imposed a five-year moratorium on new Medicare certifications, potentially nudging entrants toward commercial payers. Simultaneously, the Medicare Care Choices Model permits concurrent disease-directed therapy, testing blended reimbursement that may inspire broader value-based contracts. Medicaid continues to shield dual-eligible beneficiaries, but uneven state adoption complicates planning for national operators.

Geography Analysis

North America held 40.95% of 2025 revenue, anchored by the mature U.S. Medicare framework and Canada’s provincial palliative programs. Regional growth benefits from high technology penetration, advanced electronic health record infrastructure, and increasing private-equity roll-ups that improve operational scale. Workforce deficits and payment-cap pressures temper expansion, yet policy stability maintains investor confidence across the hospice care market.

Europe registers heterogeneous adoption, with only 13% of all deaths occurring under palliative care and stark divergence ranging from 0.3% in Slovenia to 30.4% in France. The United Kingdom’s charitable network cared for 310,000 people in 2023-24, supported by 95,000 volunteers, illustrating the power of civil-society engagement. Germany and Italy progressively integrate hospice into statutory insurance but still trail Western European leaders in bed capacity and home-care funding.

Asia-Pacific is the fastest-growing region at an 10.74% CAGR, propelled by rapid population ageing and evolving cultural attitudes. Japan’s home deaths correlate with higher reported quality scores versus hospital settings. South Korea’s hospice uptake among terminal cancer patients remains only 20.8%, pointing to ample runway. China advances community palliative pilots but must reconcile familial decision-making norms with patient autonomy initiatives. Government investment and mobile-health innovations position Asia-Pacific as a pivotal contributor to future hospice care market growth.

Competitive Landscape

The hospice care market is moderately consolidated. Chemed’s VITAS, Encompass-ENSG, and LHC/Pennant together account for roughly one-third of U.S. revenue, while dozens of midsized regionals round out share. Private-equity sponsors intensify roll-up activity, leveraging technology to compress back-office costs and negotiate favorable supplier contracts. UnitedHealth’s agreement to divest Amedisys sites to BrightSpring and Pennant, contingent on merger clearance, illustrates regulators’ antitrust vigilance.

Strategy increasingly revolves around integrated care ecosystems. Leading operators form joint ventures with acute-care hospitals, skilled-nursing chains, and home-health agencies to create seamless referral funnels. AI-enabled platforms that automate medication reconciliation and predict crisis episodes offer service differentiation and embed switching costs. However, CMS’s forthcoming Special Focus Program heightens compliance requirements, penalizing poor quality and creating headwinds for under-resourced independents.

Disruption risk emanates from virtual-first entrants combining tele-hospice, remote vitals, and gig-economy nurse staffing. While still niche, these models appeal to payers targeting rural beneficiaries where brick-and-mortar coverage is sparse. Incumbents respond by expanding mobile hospice teams and investing in speech-recognition documentation to free clinician time. Overall, success hinges on balancing scale efficiencies with the personalized ethos that underpins hospice care.

Hospice Care Industry Leaders

VITAS Healthcare Corporation

Amedisys Inc.

Gentiva Hospice (Kindred)

AccentCare Inc.

LHC Group (Optum)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: UnitedHealth and Amedisys agree to sell selected home-health and hospice branches to BrightSpring Health Services and The Pennant Group if their merger gains approval, reshaping ownership patterns in multiple states.

- March 2025: Wise Hospice Options deploys AI that trims e-prescribing from 20 seconds to 2-3 seconds and reaches 99% codification accuracy, demonstrating operational leverage from automation.

Global Hospice Care Market Report Scope

As per the scope of the report, hospice care focuses on the comfort, care, and quality of life of a person with a serious illness. Hospice care is designed for situations when it is impossible to cure a serious illness, or a patient may choose not to undergo certain treatments. The hospice care market is segmented by service, service provider, patient type, and geography. The services segment is further divided into general inpatient care, continuous care, routine home care, and respite. The service provider segment is further segmented into hospitals, home care settings, hospice care centers, and other service providers. The patient type segment is further divided into cancer, dementia, congestive heart failure, and other patient types. The geography segment is further divided into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (USD) for the above segments.

| Routine Home Care |

| Continuous Home Care |

| General In-patient Care |

| In-patient Respite Care |

| Hospice Care Centers |

| Home Care Settings |

| Hospitals |

| Skilled Nursing Facilities |

| Cancer |

| Dementia |

| Congestive Heart Failure |

| Chronic Obstructive Pulmonary Disease |

| Other Diagnoses |

| Medicare |

| Medicaid |

| Private Insurance |

| Out-of-Pocket & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Level of Care | Routine Home Care | |

| Continuous Home Care | ||

| General In-patient Care | ||

| In-patient Respite Care | ||

| By Service Provider | Hospice Care Centers | |

| Home Care Settings | ||

| Hospitals | ||

| Skilled Nursing Facilities | ||

| By Patient Diagnosis | Cancer | |

| Dementia | ||

| Congestive Heart Failure | ||

| Chronic Obstructive Pulmonary Disease | ||

| Other Diagnoses | ||

| By Payer | Medicare | |

| Medicaid | ||

| Private Insurance | ||

| Out-of-Pocket & Others | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the hospice care market?

The hospice care market size is USD 88.31 billion in 2026 and is expected to rise to USD 129.83 billion by 2031, reflecting an 8.02% CAGR.

Which level of care generates the most revenue?

Routine home care commands 89.08% of revenue in 2025, underscoring continued patient preference for familiar home settings.

Why is Asia-Pacific the fastest-growing region?

Rapid population ageing, policy support, and increasing adoption of home-based palliative models drive an 10.74% regional CAGR through 2031.

How is AI influencing hospice operations?

AI-enabled platforms cut administrative time, improve referral accuracy, and support earlier patient identification, boosting both quality and efficiency.

What challenges threaten future growth?

High out-of-pocket exposure, annual payment caps, and persistent workforce shortages could temper expansion unless policy and staffing solutions emerge.

Page last updated on: