U.S. Funeral Homes Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

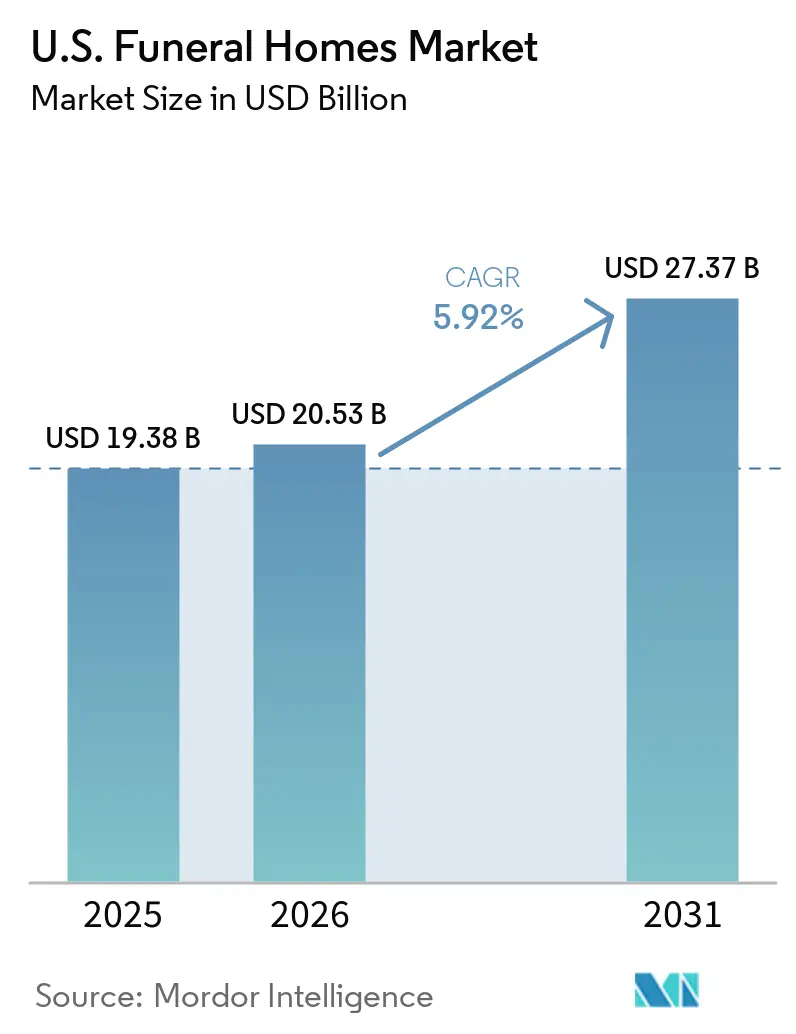

| Base Year Market Size (2025) | USD 19.38 Billion |

| Market Size (2026) | USD 20.53 Billion |

| Market Size (2031) | USD 27.37 Billion |

| Growth Rate (2026 - 2031) | 5.92% CAGR |

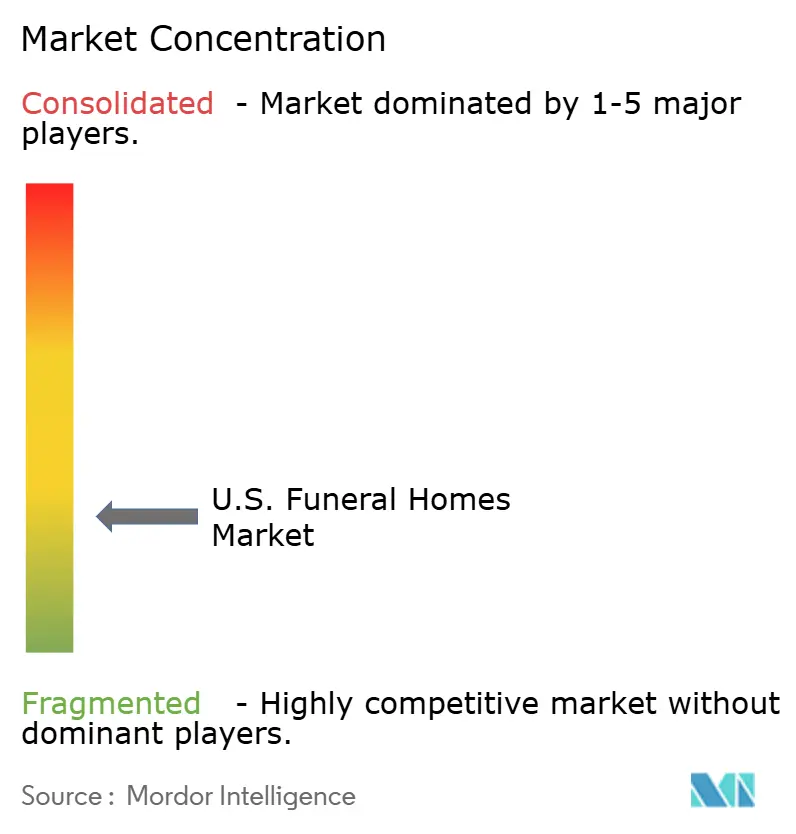

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

U.S. Funeral Homes Market Analysis by Mordor Intelligence

The U.S. Funeral Homes Market size was valued at USD 19.38 billion in 2025 and is estimated to grow from USD 20.53 billion in 2026 to reach USD 27.37 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

The demand base for United States funeral homes is entering a visible expansion phase as the first Baby Boomers turn 80 in 2026. This demographic shift moves a significant population segment into an age group with sharply rising mortality rates. Projections from the United States Census Bureau estimate annual deaths to reach 3.45 million by 2030 and 3.6 million by 2035, indicating sustained demand for the funeral homes market over the long term. However, revenue growth may not align directly with volume increases due to the growing preference for cremation over traditional burial. Cremation services typically generate lower revenue per case. Operators focusing on preneed contracts, celebration-of-life services, digital arrangement tools, and strategic acquisitions are better positioned to maintain revenue quality as consumer preferences evolve in the United States funeral homes market.

Key Report Takeaways

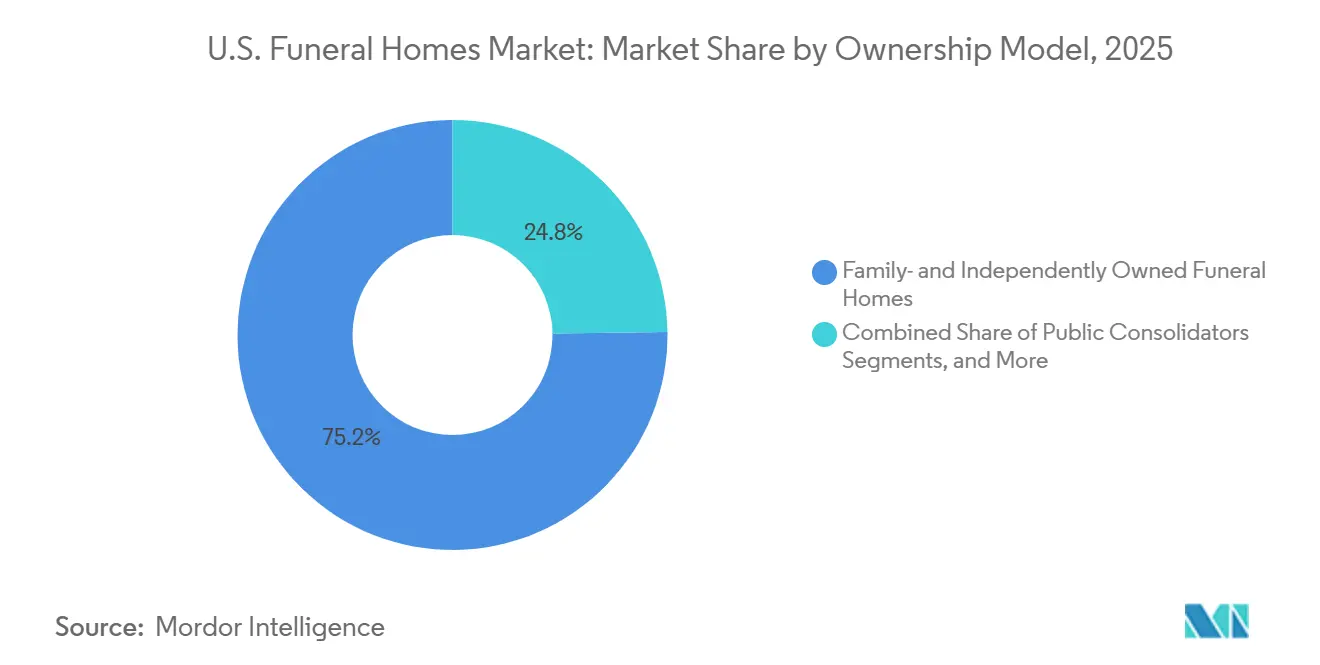

- By ownership model, family and independently owned operators held 75.25% of the US funeral homes market share in 2025, while public consolidators are projected to grow at a 7.28% CAGR through 2031.

- By arrangement timing, at-need services captured 79.56% share of the US funeral homes market size in 2025, while preneed services are expected to grow at a 7.96% CAGR through 2031.

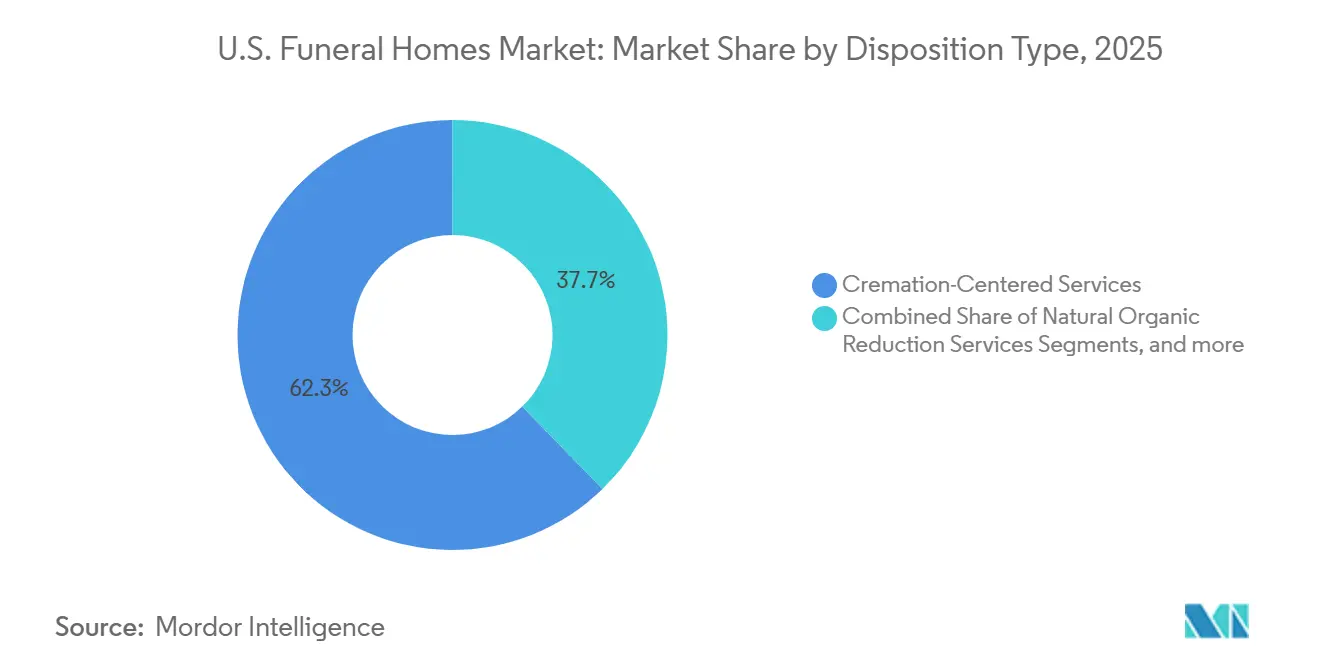

- By disposition type, cremation-centered services accounted for 62.34% share of the US funeral homes market size in 2025, while natural organic reduction is expected to expand at a 6.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

U.S. Funeral Homes Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Aging population and rising death volumes | +1.8% | National, with concentrated near-term impact in Sun Belt states including Florida, Arizona, Texas, and the Carolinas | Short term (≤ 2 years) |

| Preneed contract growth | +1.4% | National, with higher penetration in metropolitan markets with established preneed sales infrastructure | Medium term (2-4 years) |

| Personalization and celebration-of-life spending | +1.0% | National, with highest uptake in Pacific Coast, Northeast, and Sun Belt markets | Medium term (2-4 years) |

| Succession-driven consolidation | +0.8% | National, accelerating in rural and suburban Midwest, Southeast, and Mountain West | Long term (≥ 4 years) |

| Hybrid online-offline arrangement adoption | +0.6% | National, disproportionately advanced in urban and suburban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population and Rising Death Volumes Are Transitioning From Projection to Cash Flow

Demographic trends are now shaping the operational landscape of the United States funeral homes market. In 2024, 3,072,666 resident deaths were recorded, with a 3.8% decline in the age-adjusted death rate to 722.1 per 100,000. However, deaths among Americans aged 65 and older rose by 1.3%, highlighting the impact of an aging population.[1]National Center for Health Statistics, “Mortality Data Brief 2024,” Centers for Disease Control and Prevention, cdc.gov The first Baby Boomers will turn 80 in 2026, and the 75 to 90 age group will expand through the mid-2030s. Projections estimate annual deaths to reach 3.45 million by 2030 and 3.6 million by 2035, signaling sustained demand. Operators investing in staff, preneed sales, and family service systems are positioning for long-term growth.[2]Society of Actuaries, “Quarterly Mortality Monitoring Report Through December 2025,” Society of Actuaries, soa.org Mortality rates in the 60+ demographic remain consistent with aging trends, supporting a positive operational outlook.

Preneed Contract Growth Exposes a USD 3 Billion Addressable Gap

Preneed planning is driving revenue growth in the United States funeral homes market by improving demand timing and cash flow. In 2024, 535,503 preneed insurance policies were sold, with a gross face value of USD 3.04 billion, reflecting a 3.5% to 4% increase from 2023. Despite this, fewer than 22% of Americans over 55 who passed away had preneed arrangements, leaving over 78% of potential demand untapped.[3]Foundation Partners Group, “Company Press Release On Ownership And Strategy,” Foundation Partners Group, foundationpartners.com SCI's preneed backlog grew from USD 11.1 billion in 2019 to USD 17.0 billion by 2025, while Carriage Services reported a 27.4% rise in insurance-funded preneed contracts, showcasing the potential for structured sales growth.

Personalization and Celebration-of-Life Spending Are Redefining Per-Case Revenue

The United States funeral homes market is adapting to consumer demand for personalized and flexible services. In 2025, 61.4% of consumers expressed interest in eco-friendly funeral options, while 72% preferred personalized services. This shift enables operators to offset declining cremation revenue with offerings like event space rentals, catering, and customized memorial formats. SCI responded by converting casket selection rooms into event spaces and expanding celebration services. Independent operators leverage local relationships and community ties to deliver tailored services, making revenue increasingly dependent on personalized experiences.

Succession-Driven Consolidation Is Compressing the Independent Segment's Timeline

Succession challenges are driving consolidation in the United States funeral homes market, as many of the nearly 19,000 independent funeral homes are owned by operators aged 55 and older without family successors. In 2025, Foundation Partners Group reorganized operations across its 230+ locations, signaling a shift toward operational efficiency. Everstory Partners noted a significant portion of independent funeral homes is expected to change ownership, supporting acquisition pipelines for larger players. Private equity is raising acquisition valuations, particularly in growth regions like the Sun Belt, creating challenges for mid-sized private chains lacking the resources of national consolidators.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Cremation-led ticket compression | -1.5% | National, with strongest pressure in Pacific Coast and Mountain West states where cremation rates exceed 70% | Short term (≤ 2 years) |

| Licensed labor scarcity | -0.9% | National, with the sharpest impact in rural markets and high-cost-of-living metropolitan areas | Medium term (2-4 years) |

| FTC price transparency enforcement | -0.7% | National, with compliance burden concentrated among independent operators without dedicated legal and compliance support | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cremation-Led Ticket Compression Is the Primary Per-Case Revenue Headwind

The United States funeral homes market is experiencing revenue pressure due to the shift from traditional burials to cremations. The National Funeral Directors Association (NFDA) projects a cremation rate of 63.4% in 2025, while the Cremation Association of North America (CANA) reported a 2024 rate of 61.8%, with an expected increase to 67.9% by 2029. A median cremation service generates USD 6,280 compared to USD 7,848 for a burial, creating a USD 1,568 gap per case. This gap is challenging to offset as core costs like labor and facilities remain fixed. Operators not offering additional services, such as memorialization or premium options, may see volume growth without corresponding margin increases. The FTC Funeral Rule further limits pricing flexibility by requiring itemized disclosures and restricting bundling.

Licensed Labor Scarcity Creates a Structural Capacity Ceiling

Licensed labor shortages are a key growth constraint in the United States funeral homes market. The NFDA identifies this as a leading challenge for 2025, while the Bureau of Labor Statistics forecasts only 4% employment growth in the funeral sector from 2023 to 2033. This growth lags behind the rising service demand driven by an aging population. Licensing requirements, including 1 to 3 years of education and apprenticeships, result in a 2 to 4-year timeline to become a licensed professional. Rural operators face limited labor pools due to fewer training programs, while urban areas contend with rising wage expectations. Larger operators benefit from the ability to redeploy staff across locations, a flexibility smaller independents lack.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership Model: Consolidators Gain Ground as Succession Pressures Mount

In 2025, family- and independently owned operators accounted for 75.25% of revenue, maintaining their leadership in the United States funeral homes market despite ongoing consolidation. Their success stems from community trust, generational referrals, and familiarity during critical decisions.

Public consolidators are projected to grow at a 7.28% CAGR through 2031, driven by access to capital, centralized procurement, advanced technology budgets, and resource flexibility. SCI’s 2026 capital plan allocated USD 25 million for digital investments, a level unattainable for many independents. Many independents prioritized debt reduction over modernization in 2020-2021, widening the capability gap. This has created a divide between strong independents with local differentiation and weaker operators facing succession pressures, compliance costs, and acquisition offers.

By Arrangement Timing: Preneed's Growth Rate Signals the Market's Long-Term Revenue Architecture

In 2025, at-need services contributed 79.56% of revenue, reflecting families’ tendency to make funeral decisions only after a death. Emotional barriers and the absence of pre-arranged contracts keep at-need services as the primary revenue driver. However, increased price transparency and digital comparison tools are influencing family choices, with regulatory scrutiny further emphasizing compliance.

Preneed services are projected to grow at a 7.96% CAGR through 2031, the fastest among arrangement timing segments. In 2024, 535,503 preneed policies were sold, representing significant growth potential compared to 3.07 million annual deaths. The average preneed contract reached USD 5,398 in 2024, up 1% from the prior year. Carriage Services reported a 13.4% increase in preneed cemetery sales in 2025, with interment rights priced at USD 5,807, up 8.1%. Preneed services are reshaping the industry by advancing customer engagement and revenue visibility.

By Disposition Type: Cremation Consolidates Its Structural Lead While Alternative Methods Expand From a Small Base

In 2025, cremation services accounted for 62.34% of the disposition segment, aligning with the national cremation rate of 63.4%. Cremation has shifted the revenue mix, offering lower median values than burial. Funeral homes with in-house crematories benefit from improved control over timing, quality, and costs. Burial services remain significant in markets with strong religious or cultural preferences, preserving higher-value cases.

Natural Organic Reduction (NOR) is projected to grow at a 6.35% CAGR through 2031, with legalization in 14 states by 2026 and further expansion anticipated. Earth Funeral opened the largest NOR facility in Maryland in 2026, marking a milestone for the East Coast. Alternative disposition methods are gaining traction but remain influenced by regulatory and operational readiness. The projected increase in annual United States deaths from 3.1 million in 2023 to 3.91 million in 2045 expands the service base, with revenue outcomes depending on operators’ service mix.

Geography Analysis

In 2026, Sun Belt states are expected to lead growth in the United States funeral homes market due to their large retirement-age populations and continued migration of older adults from colder, high-cost states. Florida, Texas, Arizona, and the Carolinas stand out with favorable demographics, active preneed opportunities, and increased interest from consolidators. Florida’s age profile accounts for a significant share of annual United States deaths, making it attractive for larger buyers.

The Pacific Coast and Mountain West regions exhibit higher cremation rates than the national average, impacting service offerings and pricing strategies in the United States funeral homes market. Washington, Oregon, and Colorado, early adopters of NOR legalization, have developed a strong customer base for alternative dispositions. However, higher cremation rates can reduce revenue per case, prompting operators to enhance memorialization and celebration services.

The Northeast and Midwest bring unique dynamics to the United States funeral homes market. Northeastern states like New York, New Jersey, Massachusetts, and Connecticut benefit from population density and a willingness to spend on personalized memorial services, boosting optional spending. New Jersey’s September 2025 NOR legalization opened new opportunities for alternative disposition providers, with licensed services expected to begin by mid-2026.

Competitive Landscape

The United States funeral homes market remains fragmented at the local level, while consolidation progresses nationally. SCI and Carriage Services together accounted for nearly 23% of combined funeral and cemetery revenue, reflecting significant scale but not dominance in a market with numerous local providers. As of Q1 2026, SCI operated 1,487 funeral service locations and 503 cemeteries across 44 states. Its scale enables purchasing leverage, efficient resource allocation, and a preneed backlog of USD 17.0 billion by year-end 2025. This provides SCI with a competitive advantage in dense markets, though local competitors continue to thrive by leveraging community trust and service quality.

Other operators are driving competition through strategic initiatives rather than footprint expansion. Foundation Partners Group, with over 230 locations in 21 states, is strengthening its consumer acquisition strategy through Afterall and its Cake acquisition, targeting earlier stages of end-of-life planning. In 2025, Everstory implemented digitized contracts and aerial drone mapping across nearly 400 cemeteries and extended these innovations to around 100 funeral homes, modernizing operations at scale. Security National Financial is reinforcing its combined funeral-and-life-insurance model, aligning with the growth of preneed funding. Competition in the United States funeral homes market now hinges on early relationship-building, workflow digitization, and converting planning activities into funded contracts.

U.S. Funeral Homes Industry Leaders

Service Corporation International

Carriage Services, Inc.

Foundation Partners Group

Everstory Partners

Park Lawn Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Earth Funeral launched the world's largest human composting facility in Elkridge, Maryland, marking the East Coast's entry into the NOR market after Maryland legalized Natural Organic Reduction in October 2024.

- April 2026: Illinois' House of Representatives passed HB 5425, advancing the state toward becoming the 15th in the U.S. to legalize human composting, with significant market potential due to its large population.

- August 2025: Foundation Partners Group restructured under new ownership, shifting focus from acquisitions to operational efficiency and workforce investment, supported by key C-suite appointments.

- March 2025: Everstory Partners digitized operations across nearly 400 cemetery locations and began extending the initiative to approximately 100 funeral homes.

U.S. Funeral Homes Market Report Scope

As per the scope of the report, a funeral home (also known as a mortuary or funeral parlor) is an establishment licensed to prepare deceased individuals for burial or cremation. It serves as a central venue where bereaved families can view the body, hold memorial services, and receive professional grief support.

The U.S. Funeral Homes Market is segmented by ownership model, arrangement timing, and disposition type. By ownership model, the market includes family- and independently owned funeral homes, local and regional private chains, public consolidators, and nonprofit and community-owned operators. By arrangement timing, the market is segmented into at-need services and preneed services. By disposition type, the market is categorized into burial-centered services, cremation-centered services, alkaline hydrolysis services, and natural organic reduction services. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Family- and Independently Owned Funeral Homes |

| Local and Regional Private Chains |

| Public Consolidators |

| Nonprofit and Community-Owned Operators |

| At-Need Services |

| Preneed Services |

| Burial-Centered Services |

| Cremation-Centered Services |

| Alkaline Hydrolysis Services |

| Natural Organic Reduction Services |

| By Ownership Model | Family- and Independently Owned Funeral Homes |

| Local and Regional Private Chains | |

| Public Consolidators | |

| Nonprofit and Community-Owned Operators | |

| By Arrangement Timing | At-Need Services |

| Preneed Services | |

| By Disposition Type | Burial-Centered Services |

| Cremation-Centered Services | |

| Alkaline Hydrolysis Services | |

| Natural Organic Reduction Services |

Key Questions Answered in the Report

How large is the US funeral homes market in 2026?

The US funeral homes market stands at USD 20.53 billion in 2026 and is projected to reach USD 27.37 billion by 2031 at a 5.92% CAGR.

What is driving growth in funeral services across the United States?

The main driver is the aging population, especially the Baby Boomer cohort entering higher-mortality ages, alongside rising preneed adoption and spending on more personalized memorial services.

Why does cremation matter so much for funeral home revenue?

Cremation accounted for 63.4% of U.S. dispositions in 2025, and the median cremation service generated USD 6,280 compared with USD 7,848 for a traditional burial, which creates a clear revenue gap per case.

Which service type is growing fastest in funeral planning?

Preneed services are growing the fastest by arrangement timing, with a projected 7.96% CAGR through 2031, supported by low current penetration and a large uncontracted customer base.

Who currently leads the ownership structure in funeral services?

Family and independently owned operators still led with 75.25% of revenue in 2025, although public consolidators are expanding faster at a 7.28% CAGR through 2031.

What new funeral options are expanding in the United States?

Natural Organic Reduction is the fastest-growing disposition segment at a 6.35% CAGR through 2031, supported by legalization in 14 states by 2026 and new facility openings such as the Elkridge, Maryland site.

Page last updated on: