Long Term Care Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.34 Trillion |

| Market Size (2031) | USD 1.82 Trillion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

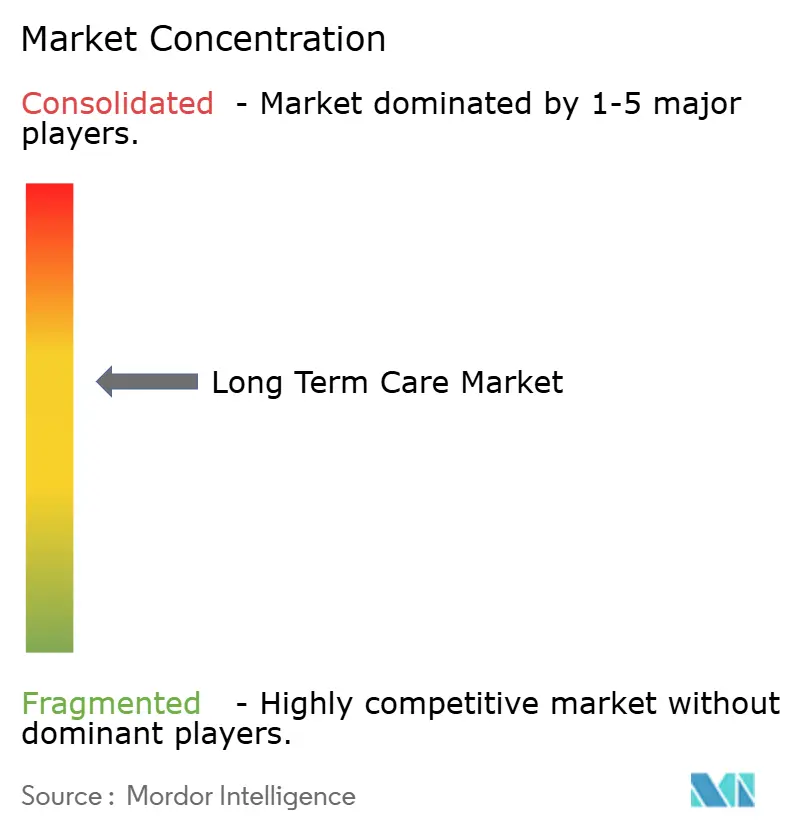

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Long Term Care Market Analysis by Mordor Intelligence

The Long Term Care Market size is expected to grow from USD 1.26 trillion in 2025 to USD 1.34 trillion in 2026 and is forecast to reach USD 1.82 trillion by 2031 at 6.31% CAGR over 2026-2031.

Growth reflects deliberate policy moves that redirect spending toward home- and community-based models, greater reliance on remote-monitoring technology, and payer migration to value-based contracts. Medicaid home- and community-based services (HCBS) outlays surpassed institutional care in fiscal 2024, freeing capacity in lower-cost settings and spurring demand for AI-enabled care coordination. Private insurers are embedding functional-outcome clauses into contracts, which compresses margins for operators lacking demonstrable quality metrics. Wage inflation, coupled with electronic health-record (EHR) mandates, adds cost pressure but also accelerates consolidation among providers that can leverage scale for technology procurement.

Key Report Takeaways

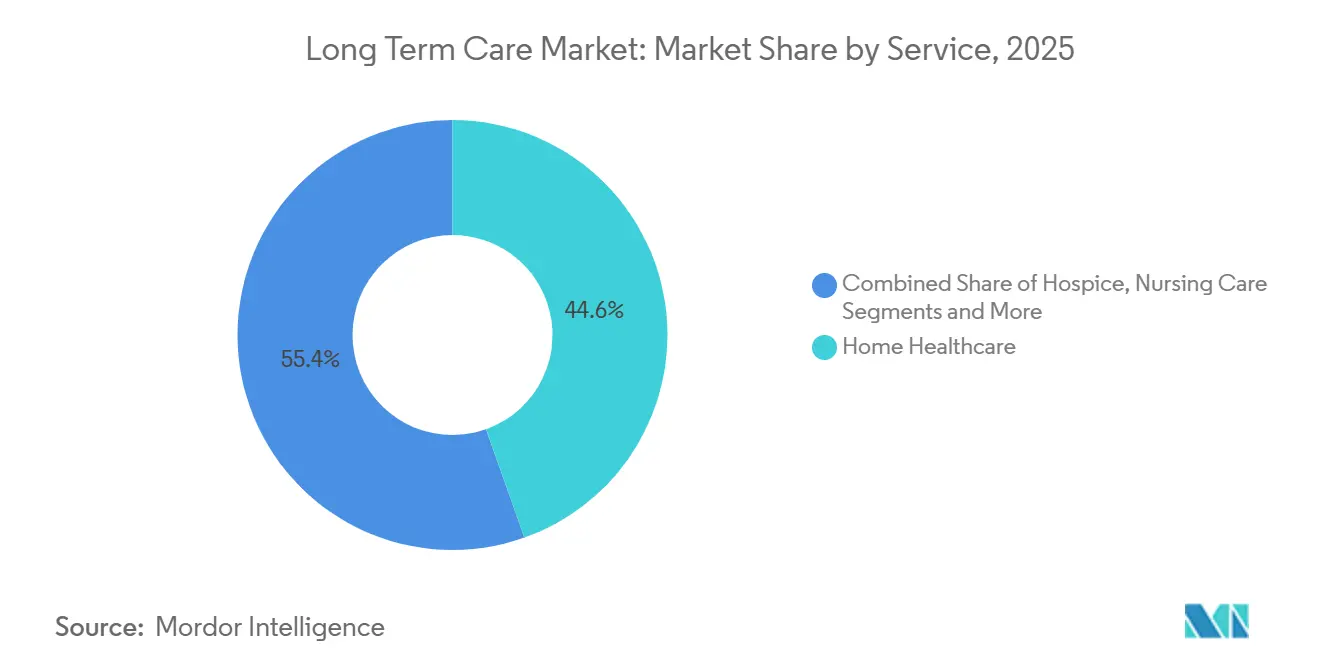

- By service line, Home Healthcare captured 44.56% of the long term care market share in 2025, while Adult Day-Care Centers posted the fastest CAGR at 9.25% through 2031.

- By payer, public programs held 57.53% of spending in 2025; Managed-Care and Value-Based Contracts are expanding at a 7.85% CAGR to 2031.

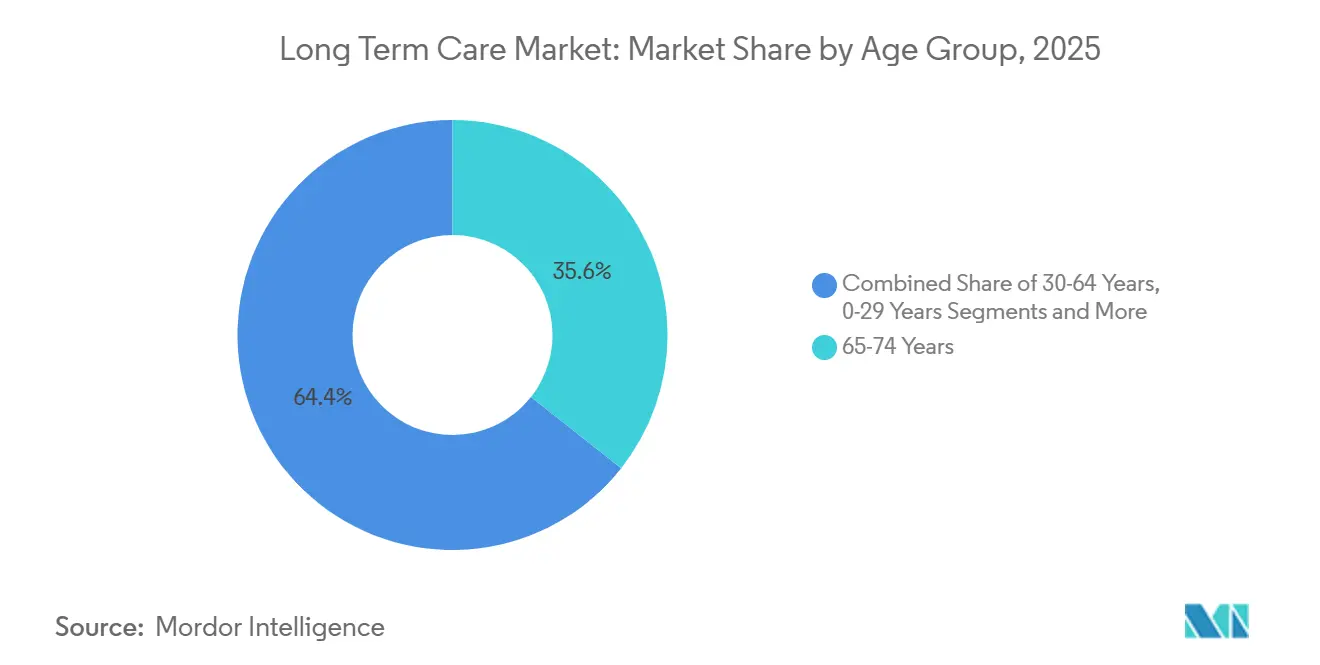

- By age group, adults aged 65-74 led revenue with 35.63% in 2025, but the 85 Years and Above bracket is advancing at a 6.87% CAGR.

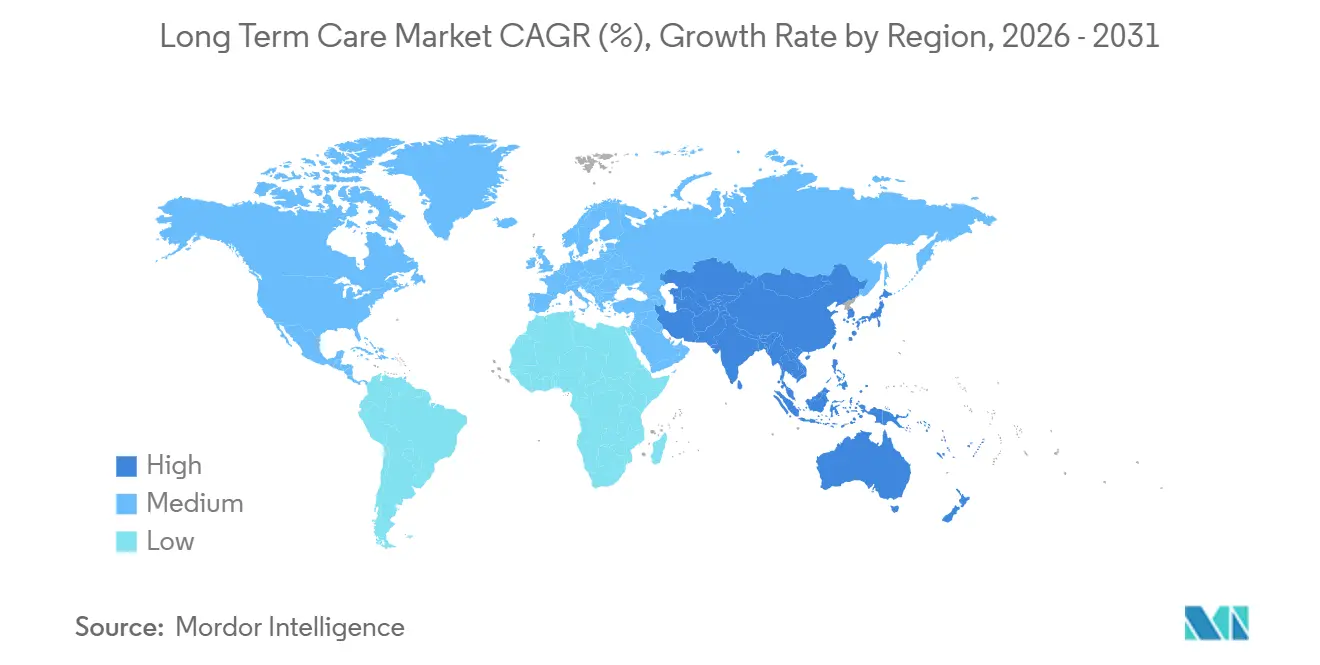

- By geography, North America generated 40.53% of 2025 spending, whereas Asia-Pacific is set to grow at an 8.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Long Term Care Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Favorable Long-Term Care Insurance Plans | +0.8% | North America, Western Europe, Japan | Medium term (2-4 years) |

| Growing Elderly Population Driving Service Uptake | +1.2% | Global, highest in APAC and Europe | Long term (≥ 4 years) |

| Government Incentives for Home & Community-Based Care | +0.9% | North America, EU | Short term (≤ 2 years) |

| AI-Enabled Remote Monitoring & Predictive Analytics | +0.7% | North America, urban APAC | Medium term (2-4 years) |

| Integration of Smart-Home Robotics for ADL Support | +0.6% | Japan, South Korea, China pilots | Medium term (2-4 years) |

| Venture-Capital Funding of Home-Based Platforms | +0.5% | North America, select EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Favorable Long-Term Care Insurance Plans

Hybrid life policies with chronic-illness riders registered a 19% sales jump in 2024 as U.S. tax incentives under Section 7702B allowed pre-tax premium payment[1]National Association of Insurance Commissioners, “Long-Term Care Insurance Experience Reports,” naic.org. Insurers now bundle nurse hotlines and caregiver training, lowering claim frequency by steering policyholders to home settings. Japan maintained a 10% beneficiary co-pay in its 2025 premium reset, protecting affordability and sustaining provider revenue. France raised monthly Allocation Personnalisée d'Autonomie allowances and pegged future increases to inflation, anchoring purchasing power for highly dependent seniors. Collectively, these measures enlarge the long term care market by broadening coverage and stabilizing demand.

Growing Elderly Population Driving Service Uptake

China’s cohort aged 60 plus reached 21.1% of population in 2024 and is growing 3.2% annually, outpacing institutional capacity[2]National Bureau of Statistics of China, “Population Statistics,” stats.gov.cn. South Korea’s 2025 “Silver Town” program subsidizes integrated senior-living complexes, channeling private capital into new supply. Italy, where 28.6% of residents were 65 plus in 2024, leans on migrant caregivers amid regional service gaps. These demographics intensify demand across the long term care market, particularly in community settings that delay or replace nursing-home stays. Operators able to scale home services stand to capture rising volumes.

Government Incentives for Home & Community-Based Care

Medicaid HCBS spending hit USD 125 billion in 2024 and overtook nursing-facility outlays, reflecting state rebalancing efforts. Twelve states received 1115 waivers in 2025 to fund non-medical supports such as meal delivery and home modifications, reducing institutional admissions. The Inflation Reduction Act temporarily boosted federal HCBS matching rates by 6 points, enabling wage hikes for direct-care workers and cementing higher baseline spend. The EU’s 2024 Long-Term Care Strategy earmarked EUR 2.3 billion for home-care digitalization. These policies accelerate the long term care market shift toward community-based models.

AI-Enabled Remote Monitoring & Predictive Analytics

FDA 510(k) submissions for elderly-focused remote-monitoring devices climbed 34% in 2024. A 2025 JAMDA study reported an 18% fall in nursing-home readmissions after AI analytics deployment, translating to USD 3,200 savings per resident annually. Medicare Advantage plans now waive premiums for beneficiaries consenting to continuous data sharing, stimulating device adoption. The Office for Civil Rights clarified HIPAA rules for wearables in March 2025, steering vendors toward edge-computing to limit cloud transmission. Resulting efficiencies and payer incentives enlarge the addressable base for the long term care market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low Consumer Awareness in Emerging Economies | -0.4% | South Asia, Sub-Saharan Africa, Latin America | Long term (≥ 4 years) |

| Skilled Nursing & Caregiver Workforce Shortages | -0.8% | Global, acute in North America & Europe | Short term (≤ 2 years) |

| Data-Privacy & Cyber-Risk Concerns | -0.3% | North America, EU (GDPR) | Medium term (2-4 years) |

| Rising Inflation-Driven Wage Pressures | -0.6% | North America, Western Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Skilled Nursing & Caregiver Workforce Shortages

Certified nursing assistant vacancies in U.S. skilled-nursing facilities hit 13% in 2025, forcing 40% cost premiums for contract labor and eroding margins[3]American Health Care Association, “Workforce Vacancy Report,” ahca.org. The Bureau of Labor Statistics forecasts 22% growth in demand for home-health aides from 2024-2034, dwarfing the 3% all-occupation average. Germany reported 47,000 open care positions in 2024 and is fast-tracking visas for Filipino and Vietnamese nurses. Japan projects a 690,000-worker deficit by 2040 and is investing in robotics to offset shortages. Persistent staffing gaps restrict capacity expansion across the long term care market.

Rising Inflation-Driven Wage Pressures on Facility Operators

Consumer price inflation cooled to 3.2% in the United States during 2025, yet wages in the healthcare and social assistance sector climbed 5.8%, reflecting tight labor supply and new union contracts with annual escalators. Labor accounts for 60%–70% of operating expenses at long-term care facilities, so elevated pay scales erode margins unless reimbursements rise in tandem. Medicaid payments, which generate more than half of nursing-home revenue, often lag inflation by up to two years because state legislatures reset rates on biennial cycles. Average skilled-nursing occupancy slipped to 78.4% in the fourth quarter of 2024, below the 85% breakeven threshold, and 92 facilities filed for bankruptcy in 2025. Assisted living operators possess greater pricing latitude, but families resist rate hikes once monthly charges exceed USD 6,000, capping pass-through in many markets. In response, some providers are rolling out tiered pricing that separates housekeeping, transportation, and social activities, enabling residents to tailor spending while operators capture incremental revenue from higher-acuity clients.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Home Healthcare Dominates, Day Care Surges

Home Healthcare generated the largest slice of the long term care market size, claiming 44.56% of 2025 revenue on the strength of Medicare’s home-health benefit that served 3.4 million enrollees in 2024. Average 60-day episode costs of USD 3,200 compare favorably to USD 15,000 hospital readmission expenses, aligning payer incentives with patient preferences. Agencies with robust EHRs illustrate lower readmission rates, positioning themselves for shared-savings bonuses under value-based contracts. Adult Day-Care Centers, though smaller, are forecast to expand at 9.25% annually to 2031, the fastest clip in the long term care market; 2024 attendance rose 11% as programs added memory-care tracks and door-to-door transport. Their hybrid structure permits caregivers to stay employed, delaying costly institutionalization.

Nursing Care facilities continue to struggle with sub-80% occupancy and Medicaid rate lag, yet specialized dementia units command premiums that partially offset labor inflation. Assisted Living appeals to private-pay households seeking autonomy, with tiered-service models unbundling amenities to capture revenue. Hospice, a smaller slice of the long term care market share, drew USD 22.4 billion in 2024 but faces stricter oversight on length of stay. CMS’s 2024 GUIDE dementia-care model pays a monthly care-management fee across service lines, rewarding operators that integrate home health, day care, and respite offerings and demonstrate quality improvements.

By Payer: Managed Care Gains, Fee-for-Service Recedes

Public programs accounted for 57.53% of 2025 spending, underscoring Medicaid’s central role in financing the long term care market. Yet capitated Managed-Care and Value-Based Contracts are increasing at a 7.85% CAGR as states transition risk to managed long-term services and supports plans. Providers must meet utilization-management and quality-reporting standards that vary across plans, adding administrative complexity. A 2025 survey found 63% of agencies flag documentation requirements as a top pain point. Nevertheless, providers that hit quality benchmarks can earn shared-savings supplements, lifting margins. Private Insurance—including hybrid policies—remains a modest share but is growing as underwriters refine actuarial models and bundle care-coordination services. Out-of-Pocket outlays stay material, especially for assisted living, where Medicaid coverage is limited and household assets bridge the gap; nearly half of Americans turning 65 in 2024 face lifetime long-term care costs above USD 100,000.

By Age Group: Oldest Cohort Expands Fastest

Adults aged 65-74 held 35.63% of 2025 revenue, reflecting large Baby-Boomer cohorts still in relatively good health who favor adult day care and low-acuity home services. The 85 Years and Above group, although smaller, is set to log a 6.87% CAGR to 2031, outpacing all other brackets and lifting the long term care market size for high-acuity offerings. One-third of this cohort has Alzheimer’s disease or related dementias, doubling per-capita care costs. Providers serve the middle-old (75-84 years) with preventive programs aimed at preserving function, such as the CAPABLE model that cut nursing-home admission by 30% over two years. Adults aged 30-64 with disabilities depend on Medicaid waivers for community support, while pediatric long-term care remains a niche within the broader long term care market.

Geography Analysis

North America led the long term care market with 40.53% of 2025 spending, driven by the United States’ USD 450 billion outlay in 2024. Federal payers dominate institutional nursing and home-health reimbursement, but private pay shoulders assisted living and continuing-care retirement community fees. Canada’s provincial home-care programs pursue integrated medical-social models, yet vast rural provinces contend with staffing shortages that inflate unit costs. Mexico logged fewer than 1,000 licensed nursing homes in 2025 and launched a pilot to train community health workers and pay stipends to family caregivers.

Asia-Pacific is the fastest-growing region at an 8.21% CAGR, propelled by Japan’s mature insurance system, China’s subsidy for in-home robotics, and South Korea’s Silver Town initiative. Japan spent JPY 11.2 trillion (USD 75 billion) on long-term care in fiscal 2024, 70% for in-home and day-care services. China selected 15 cities in 2025 for robot deployments that support rural elders where labor is scarce. India’s nascent long term care market attracted USD 180 million private equity in senior living during 2024 but remains fragmented.

Europe commands significant share through Germany, the United Kingdom, France, Italy, and Spain. Germany lifted Pflegeversicherung benefits by 5% in 2025 and added coverage for mild cognitive impairment, expanding eligibility to 180,000 people. The United Kingdom tightens means testing, pushing costs onto families and spurring private-pay home-care demand. France expanded its APA benefit in 2024, preserving household purchasing power. Italy’s southern provinces rely on migrant caregivers in the informal economy, reflecting regional disparities.

Elsewhere, the Gulf Cooperation Council invests in senior-living campuses for expatriate and national populations. Brazil’s 2024 national long-term care policy sets federal standards and co-finance for municipal home-care expansion. Australia introduced a star-rating system and stepped-up inspections in 2024, lifting compliance costs but improving transparency.

Competitive Landscape

The long term care market features moderate concentration. Large operators leverage scale for EHR procurement and labor sourcing, while regional chains and independents fill niche needs such as culturally tailored dementia programs. Wage inflation of 12% for certified nursing assistants in 2025 tightened operating margins. Brookdale Senior Living committed to ambient-sensing installations across 200 communities in 2025 to strengthen risk-based contract negotiation. The Ensign Group added 16 skilled-nursing facilities via acquisition to bulk referral networks, while Encompass Health formed joint ventures with acute-care hospitals to embed post-acute pathways that feed its home-health arm.

Venture-backed platforms that match independent caregivers with families raised sizeable funding and offer higher take-home pay, pressuring traditional agencies. Yet CMS’s Five-Star Quality Rating System and state licensing create regulatory hurdles that shield incumbents. Managed-care payers increasingly require real-time data exchange; operators without certified EHR modules risk exclusion from high-volume referral channels. Corporate strategies therefore center on technology adoption, workforce pipelines, and service line diversification to manage reimbursement risk.

Cyber-security has become a board-level priority. The Department of Health and Human Services logged 87 data breaches involving long-term care entities in 2024. Larger chains are investing in zero-trust architectures and staff training, whereas smaller providers frequently lack in-house expertise, creating acquisition targets for better-capitalized firms seeking to extend compliant networks. Overall, the long term care industry continues to consolidate around organizations capable of meeting payer data demands and absorbing wage escalation.

Long Term Care Industry Leaders

Brookdale Senior Living, Inc.

Extendicare, Inc.

Sunrise Senior Living

Atria Senior Living, Inc.

Sonida Senior Living

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Long-term care insurance covered nearly 7 million Americans, offering flexibility to receive services at home, in community settings, or facilities.

- October 2025: Provider Partners launched a value-based care program that embeds VBC services directly into nursing-home workflows, sharing savings tied to functional outcomes.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the long-term care market as the value generated by formal providers that deliver medical and non-medical support for individuals needing assistance with activities of daily living for 90 days or longer, across settings such as home healthcare, nursing homes, assisted-living residences, adult day-care centers, and hospice. We count only revenue earned from client fees or public reimbursements in 2025 values.

Scope Exclusions: informal family caregiving, standalone long-term care software, and transitional rehabilitation units inside acute hospitals are excluded to keep the focus tight.

Segmentation Overview

- By Service

- Home Healthcare

- Hospice

- Nursing Care

- Assisted Living Facilities

- Adult Day-Care Centers

- Other Services

- By Payer

- Public

- Private Insurance

- Out-of-Pocket / Self-Funded

- Managed-Care & Value-Based Contracts

- By Age Group

- 0-29 Years

- 30-64 Years

- 65-74 Years

- 75-84 Years

- 85 Years & Above

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor's team interviewed administrators of home-care networks, geriatricians, state-level Medicaid planners, and group purchasing managers across North America, Europe, and Asia-Pacific. Insights on wage pressure, average daily reimbursement, and occupancy thresholds allowed us to refine service-mix weights and stress-test preliminary desk estimates.

Desk Research

We relied on publicly available cornerstones, including the Centers for Medicare & Medicaid Services National Health Expenditure tables, Organisation for Economic Co-operation and Development health accounts, United Nations Ageing and Population dashboards, and industry statistics from bodies such as the American Health Care Association, Eurostat's Long-Term Care Indicators, and Japan's Ministry of Health, Labor and Welfare, to size resident pools, payment splits, and service capacity. Company 10-Ks, state Medicaid waiver databases, and respected journals like Health Affairs provided utilization rates, staffing ratios, and cost inflation trends. According to Mordor analysts, paid databases such as D&B Hoovers and Dow Jones Factiva supplied facility revenue snapshots and deal pipelines that sharpened growth assumptions. This list is illustrative, as many additional sources were consulted for cross-checks.

We also tapped Marklines for medical transport fleet counts and Questel for patent signals around smart-monitoring devices, which hint at upcoming shifts toward home-based models. These inputs anchor price and adoption curves before primary validation.

Market-Sizing & Forecasting

A top-down reconstruction begins with country health-expenditure outlays tagged as long-term care, which are then split by service line using utilization and payer shares. Results are corroborated with selective bottom-up roll-ups, sampled facility counts multiplied by average spend per bed or home-care visit, to catch anomalies. Key model drivers include: 65+ population growth, prevalence of dementia, median caregiver wages, Medicaid HCBS waiver penetration, facility occupancy, and average length of stay. Forecasts employ multivariate regression with scenario analysis; wage escalation and dependency-ratio trends act as lead variables, while expert consensus guides terminal growth moderation. Gaps in bottom-up data, such as missing private-facility fee schedules, are bridged with regional proxies vetted during interviews.

Data Validation & Update Cycle

We, the analysts, run three-step variance checks against historical spending, competitor filings, and sentinel indicators (staffing levels, insurer payouts). Senior reviewers sign off only after outliers are reconciled. Reports refresh each year, and interim updates trigger when policy or reimbursement shifts move the baseline materially.

Why Mordor's Long Term Care Baseline Proves Dependable

Stakeholders notice that published market figures rarely align because publishers diverge on service scope, inflation treatment, and refresh cadence.

We acknowledge these variations upfront and outline them below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.26 T (2025) | Mordor Intelligence | |

| USD 1.18 T (2024) | Global Consultancy A | Excludes adult day-care and applies uniform 3 % price uplift rather than wage-linked indexing |

| USD 1.16 T (2024) | Industry Research House B | Omits Medicaid HCBS spend and leaves home-health revenue to a separate study, narrowing scope |

Our comparison shows that once consistent scope and wage-driven pricing are applied, Mordor delivers a balanced, transparent baseline clients can trace to measurable variables and replicate with confidence.

Key Questions Answered in the Report

How large is the long term care market today?

The long term care market size reached USD 1.34 trillion in 2026 and is forecast to top USD 1.82 trillion by 2031.

Which service line leads spending?

Home Healthcare holds the largest 2025 share at 44.56%, driven by Medicare coverage and lower episode costs relative to hospital readmissions.

Which region is growing fastest?

Asia-Pacific is on an 8.21% CAGR trajectory through 2031, fueled by Japan's insurance reforms and China's robotics subsidies.

What is the biggest operational challenge for providers?

Workforce shortages remain acute, with a 13% vacancy rate for U.S. certified nursing assistants in 2025 and similar gaps in Europe and Japan.

How are payers influencing the market?

Medicaid and managed-care plans tie reimbursement to functional outcomes, pushing operators to adopt interoperable EHRs and remote-monitoring tools.

Are technology investments paying off?

Facilities deploying AI-powered analytics cut hospital readmissions by 18%, saving about USD 3,200 per resident per year and improving their position in risk-based contracts.

Page last updated on: